Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

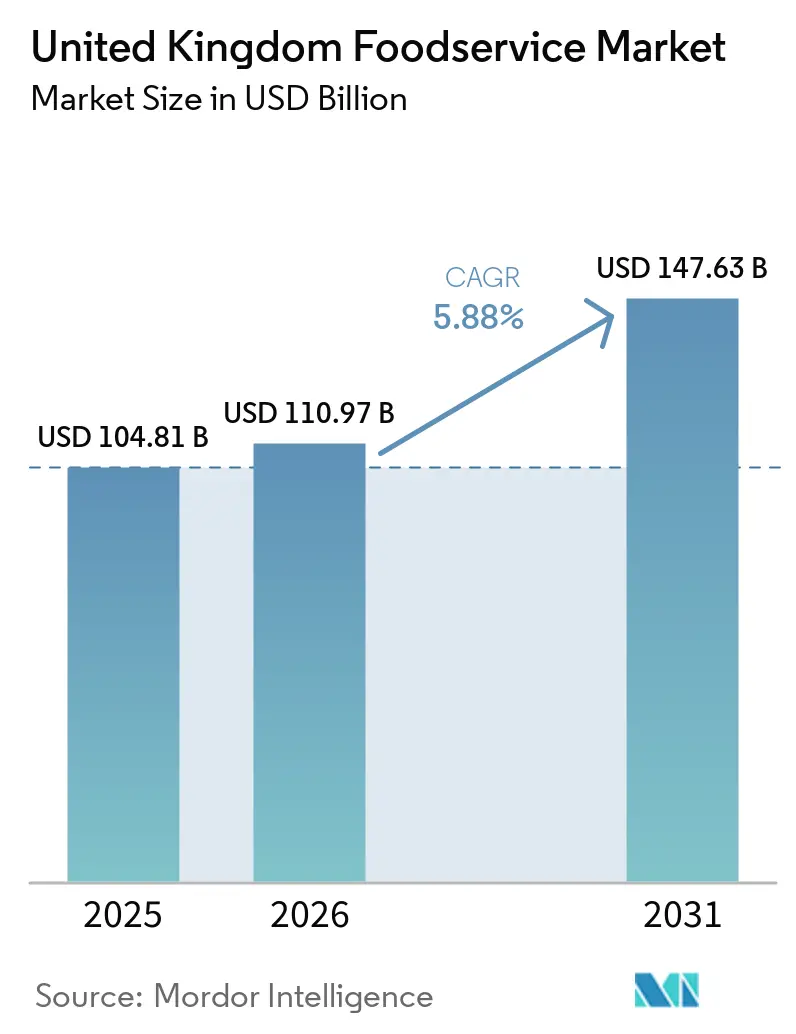

| Base Year Market Size (2025) | USD 104.81 Billion |

| Market Size (2026) | USD 110.97 Billion |

| Market Size (2031) | USD 147.63 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Foodservice Market Analysis by Mordor Intelligence

The United Kingdom foodservice market size is expected to grow from USD 104.81 billion in 2025 to USD 110.97 billion in 2026 and is forecast to reach USD 147.63 billion by 2031 at 5.88% CAGR over 2026-2031. Persistent consumer demand for convenience, technology-enabled ordering, and experiential dining is steering capital toward delivery infrastructure, menu innovation, and omnichannel engagement. Operators that embed artificial-intelligence insights into inventory planning, labor scheduling, and targeted promotions are widening margin buffers even as labor inflation and energy costs tighten unit economics. Rapid uptake of hybrid models, blending dine-in ambiance with robust off-premise fulfillment, has rewritten location economics by pairing high-street visibility with distributed “dark” production facilities. Sustainability compliance is becoming an equally strong growth catalyst: chains that invest early in carbon-neutral kitchens and transparent ingredient sourcing are capturing the expanding pool of values-driven diners.

Key Report Takeaways

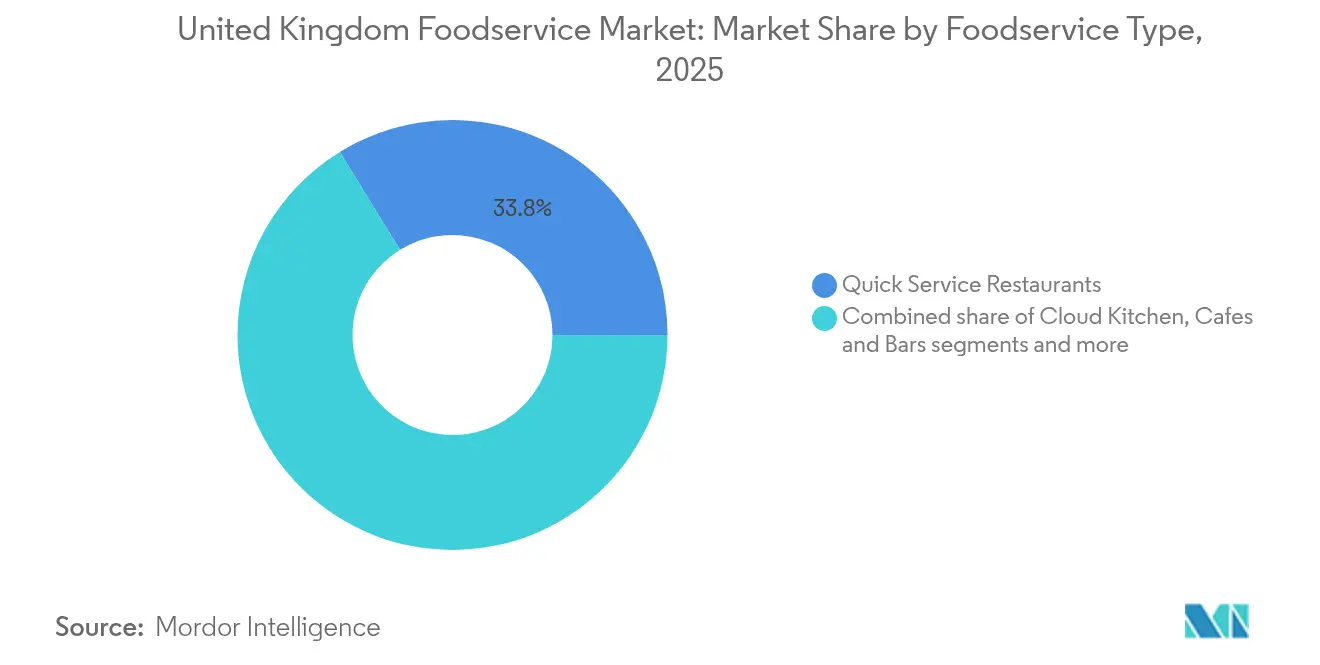

- By foodservice type, quick service restaurants led with 33.78% of the United Kingdom foodservice market share in 2025, while cloud kitchens posted the fastest expansion, registering a 12.10% CAGR through 2031.

- By outlet type, independents retained 56.72% of the United Kingdom foodservice market in 2025 as chains accelerated digital investment; however, it is also projected to capture the highest incremental value, rising 6.35% annually through 2031.

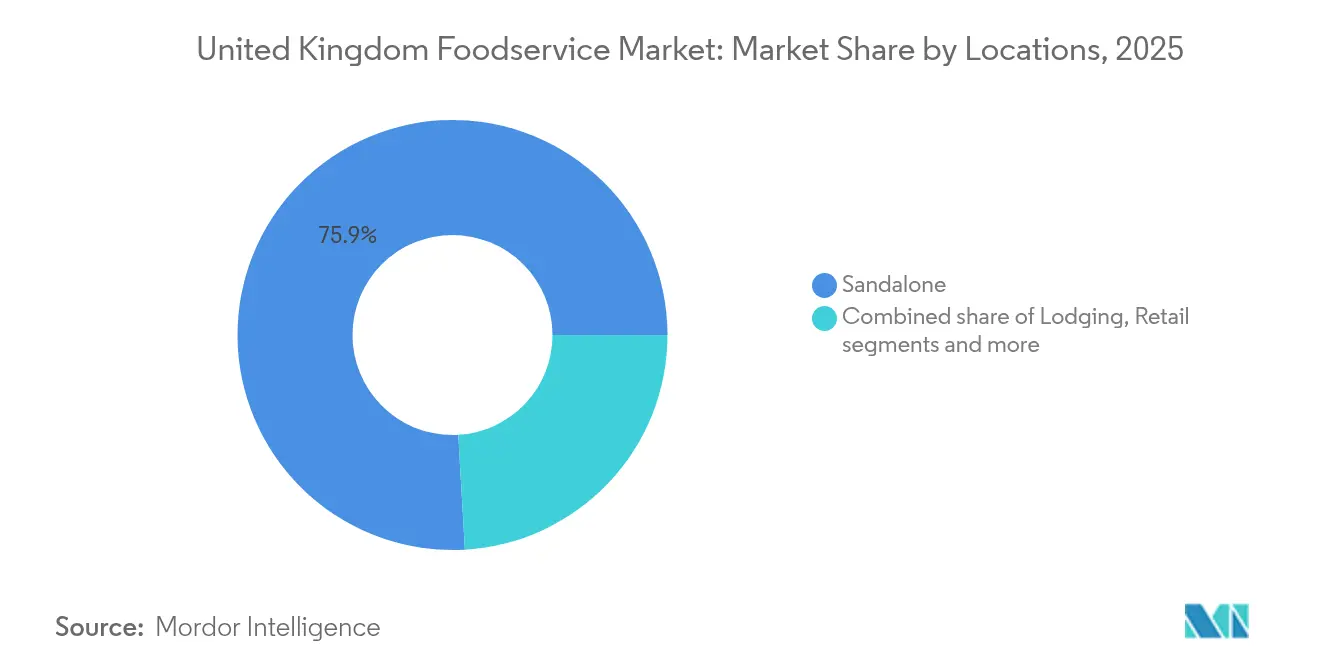

- By location, standalone venues accounted for 75.92% of the United Kingdom foodservice market activity in 2025, whereas lodging-based venues are forecast to grow at a 9.78% CAGR on the back of hospitality rebound and bundled guest-experience programs.

- By service type, dine-in remained dominant with 54.62% the United Kingdom foodservice market size in 2025, yet delivery services are advancing at a 7.11% CAGR to 2031 as consumers retain pandemic-era order habits even after the return of in-person dining.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of food delivery apps | +1.8% | National, with concentration in urban centers | Medium term (2-4 years) |

| Increased demand for healthier, vegan, low-calorie, and allergen-free menu options | +1.2% | National, with premium segments in London and Southeast | Long term (≥ 4 years) |

| Emergence and rapid growth of cloud/ghost kitchens | +0.9% | Urban centers, expanding to suburban markets | Short term (≤ 2 years) |

| Growing consumer interest in authentic global cuisines and fusion menus | +0.7% | Metropolitan areas with diverse populations | Medium term (2-4 years) |

| Social media trends and “Instagrammable” dining shape consumer choices | +0.6% | National, with younger demographics driving adoption | Short term (≤ 2 years) |

| Menu simplification and value offers | +0.4% | National, with emphasis on cost-conscious segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of food delivery apps

Food delivery apps have significantly transformed revenue streams and consumer access for foodservice operators, enabling them to overcome traditional dine-in limitations through expanded geographic reach. Partnerships such as Uber Eats with Pret A Manger demonstrate how third-party aggregators enhance customer acquisition and brand visibility. However, they introduce challenges like commission fees ranging from 15% to 30% per order. This financial pressure has driven restaurants to redesign physical spaces with dedicated delivery preparation zones, ensuring efficient order fulfillment while maintaining dine-in standards. Operators are increasingly integrating real-time technology to balance relationships with aggregator platforms and their own direct-to-consumer tools, aiming to retain margins and build customer loyalty. High-street chains like Greggs leverage proprietary apps for personalized offers and efficient order batching while maintaining a presence on third-party platforms to maximize exposure. To support omnichannel growth, workflows, kitchen operations, and shift patterns are restructured, with investments in automation or specialized delivery teams enhancing efficiency. As delivery becomes a core revenue driver, strict controls over order tracking, packaging, and time management are essential to uphold service quality. However, reliance on delivery apps raises concerns about fluctuating commission rates and disintermediation risks, prompting a focus on data ownership and customer engagement through proprietary channels. The integration of digital ordering, aggregator partnerships, and in-house platforms requires operators to adapt continuously, balancing new revenue opportunities with cost management and brand control.

Increased demand for healthier, vegan, low-calorie, and allergen-free menu options

Health-conscious consumption patterns are reshaping the foodservice industry, driving both major chains and independent operators to innovate and expand their offerings beyond traditional dietary restrictions and allergen avoidance. For instance, Pizza Hut has introduced plant-based pizzas and sides to cater to the vegan demographic, which, according to The Vegan Society in 2024, has grown to approximately 2 million people (3% of Great Britain) [1]Source: The Vegan Society, "Nationwide Trends Highlight Growing Shift Toward Plant-Based Diets", vegansociety.com. McDonald’s has also developed a vegan menu, including the McPlant burger, Vegetable Deluxe, Spicy Veggie One wrap, Veggie Dippers, and select breakfast items, balancing indulgent classics with health-focused alternatives to meet the diverse demands of its consumers. Menu development is increasingly incorporating trends such as lower-calorie options, allergen-free items, and functional foods, aligning with the World Health Organization’s updated dietary guidance that emphasizes reduced consumption of processed foods. Regulatory requirements for transparent nutritional labeling and ingredient sourcing, driven by the Food Standards Agency (FSA) allergen management rules, necessitate comprehensive staff training and supply chain visibility. While these regulations pose challenges, they also create opportunities for premiumization through clean-label positioning. As clean-label and sustainability considerations gain prominence, ingredient sourcing practices and eco-friendly packaging are becoming critical marketing tools. The evolving regulatory landscape and shifting consumer preferences are accelerating innovation and operational changes, making health-conscious and transparent menus essential for growth and customer loyalty.

Emergence and rapid growth of cloud/ghost kitchens

Cloud and ghost kitchens are transforming the foodservice industry by leveraging lower real estate costs and delivery-optimized layouts to achieve superior unit economics compared to traditional restaurants in high-rent urban areas. Karma Kitchen’s expansion across London demonstrates the efficiency of purpose-built delivery hubs, where multiple virtual brands operate from a single location, optimizing kitchen utilization and reducing expenditures on customer-facing infrastructure. London’s dominance in this space is evident from The Autonomy Institute’s 2024 data, which reports 32 Editions (shared kitchen) sites in the city, far surpassing the combined total of 21 sites across other United Kingdom regions and solidifying London as Deliveroo’s strategic hub [2]Source: The Autonomy Institute, "The Future of Cloud Kitchens: A Municipal Approach", autonomy.work. This model lowers market entry barriers and shifts competition to virtual delivery zones, where data-driven heatmaps replace traditional footfall metrics. Technology is integral, with cloud kitchens relying on advanced digital platforms, analytics, and demand-forecasting tools to adapt operations in real time. The scalability and asset-light nature of this model continue to attract significant venture capital investment, as seen in recent funding rounds for operators like Foodstars, reflecting confidence in its long-term commercial potential.

Growing consumer interest in authentic global cuisines and fusion menus

Consumer demand for authentic global cuisines and fusion menus is evolving, driven by demographic diversification and increased exposure to international flavors through travel. In 2023, the OECD reported that 15.2% of the United Kingdom population, approximately 10.3 million people, were foreign-born, with significant contributions from communities such as India (9%), Poland (7%), and Pakistan (5%) [3]Source: Organisation for Economic Co‑operation and Development (OECD), "International Migration Outlook 2025", oecd.org . This demographic shift has fueled demand for culturally distinct food offerings, with independent operators like Dishoom leveraging ethnicity-driven menus to compete with major chains through differentiated products and authentic storytelling. Social media platforms, particularly Instagram, amplify the appeal of visually distinctive and culturally unique dishes, driving customer engagement. Larger chains face challenges in scaling authentic preparation methods, often requiring specialized training and supply chain adaptations to ensure consistency. Fusion concepts, blending familiar and international techniques, broaden consumer appeal while maintaining cultural authenticity. Ingredient traceability and regional sourcing are increasingly emphasized to enhance transparency and build trust with informed consumers. Operators also invest in chef exchanges, themed pop-ups, and menu collaborations to sustain authenticity and innovation. The interplay of demographic changes, travel-inspired tastes, social media influence, and operational strategies has created a competitive landscape where businesses must balance authenticity and accessibility to meet evolving consumer preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food and labour cost inflation | -0.8% | National, with acute pressure in London and Southeast | Short term (≤ 2 years) |

| Rising competition drives need for differentiation | -0.6% | National, with intensification in saturated urban markets | Medium term (2-4 years) |

| Brand loyalty erosion | -0.5% | National, affecting established chains disproportionately | Long term (≥ 4 years) |

| Sustainability-reporting compliance costs | -0.4% | National, with stricter enforcement in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food and labour cost inflation

Food and labor cost inflation is exerting significant pressure on the United Kingdom foodservice market, compelling operators to adjust menu pricing, sourcing strategies, and operational protocols to remain viable amidst shrinking profit margins. Rising labor costs, driven by substantial minimum wage increases and higher employer contributions in 2025, are particularly challenging for brands like Wetherspoons, which face the dual burden of escalating wage bills and increasing costs for key ingredients and energy. This combination of inflationary pressures has led to frequent menu price adjustments, with quick-service chicken and burger outlets often implementing the largest price increases, while casual dining chains focus on operational efficiencies and moderate price hikes to manage higher staff costs. To maintain perceived value and address input cost inflation, many businesses are adopting data-driven pricing strategies, optimizing menu offerings, and reallocating staff resources to protect profitability without alienating cost-sensitive customers. Additionally, operators are engaging in more intense supplier negotiations, pursuing strategic sourcing initiatives, and facing heightened vulnerability to supply chain disruptions, particularly in volatile food categories such as oils, dairy, and proteins. As inflation continues to impact both food and labor costs, the need for efficiency has become critical. Organizations are increasingly automating processes, investing in multisite analytics, and revisiting loyalty programs or promotional strategies to sustain customer traffic while preserving margins. The cumulative effect is an industry-wide challenge, where inflation amplifies operational complexities, requiring businesses to adapt quickly and demonstrate resilience in the face of evolving consumer expectations and persistent cost pressures.

Rising competition drives need for differentiation

Intensifying competition in saturated prime locations has driven foodservice operators in the United Kingdom to focus on differentiation through unique menus, innovative services, and experiential offerings that support premium positioning. The rise of delivery options has reduced traditional location-based advantages, pushing brands to prioritize food quality, speed, and value across broader geographies. Investments in advanced technologies, such as integrated POS systems, customer relationship management platforms, and operational analytics, are becoming essential for optimizing performance and enhancing consumer experiences. Smaller operators face challenges in funding these technologies and maintaining competitive pricing, leading to consolidation pressures favoring larger chains like Greggs and Leon, which utilize scale to implement advanced digital strategies. Differentiation increasingly hinges on local authenticity, personalization, and strategic collaborations, with thematic events and community-focused experiences aligning with evolving consumer preferences. Data-driven pricing and menu simplification improve operational flexibility while loyalty apps and targeted promotions help retain customer engagement. While technology enhances efficiency and insights, personal service remains critical for fostering brand loyalty and improving dining experiences. Investments in online visibility, social media engagement, and influencer partnerships further strengthen brand awareness, enabling operators to establish distinct market identities in a competitive environment. The interplay of market saturation, technological adoption, and innovation underscores the need for agility, authenticity, and customer-centric strategies to achieve sustainable competitive advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: QSR Dominance Faces Cloud Kitchen Disruption

Quick service restaurants (QSRs) are projected to maintain market leadership with a 33.78% share in 2025. This reflects consumer preferences for speed, convenience, and value, which align with economic uncertainty and time-constrained lifestyles. Meanwhile, cloud kitchens are expected to achieve an impressive 12.10% compound annual growth rate (CAGR) through 2031, indicating a significant shift toward delivery-optimized formats. These formats reduce customer-facing real estate costs while maximizing kitchen efficiency. Full-service restaurants face challenges due to their traditional dine-in model, which involves higher labor costs and premium locations. However, their diverse cuisine offerings, ranging from Asian to European concepts, provide differentiation opportunities that QSR formats cannot easily replicate. Cafes and bars benefit from trends in social gatherings and remote work, which drive daytime traffic. Specialist coffee shops, in particular, capitalize on premium pricing through artisanal positioning and experiential elements.

The evolution of the foodservice segment highlights the role of technology in reshaping operational models. Cloud kitchens leverage data analytics to optimize menu offerings and delivery routes, providing efficiencies that traditional restaurants cannot match. For example, McDonald's digital transformation initiatives, such as AI-powered drive-through ordering and mobile app integration, illustrate how established QSR operators invest in technology to maintain competitive advantages against delivery-native competitors. Additionally, regulatory compliance is becoming increasingly complex, as different foodservice types face varying health and safety requirements. Full-service establishments, in particular, require more comprehensive staff training and customer interaction protocols compared to delivery-focused formats.

By Outlet: Independent Resilience Amid Chain Consolidation

Independent outlets are projected to hold a 56.72% market share in 2025, with a compound annual growth rate (CAGR) of 6.35% through 2031. This growth underscores their resilience despite challenges such as technology adoption costs and supply chain complexities. The performance of independent outlets reflects consumer preferences for authentic, locally-sourced dining experiences, which these operators deliver more effectively compared to standardized chain formats. In contrast, chained outlets benefit from economies of scale in purchasing, marketing, and technology deployment. However, their growth rates remain lower than those of independents, indicating that operational efficiency alone cannot fully address consumer demand for unique dining experiences and stronger community connections.

The competitive landscape between independent and chained outlets is evolving as independent operators increasingly adopt chain-like practices. These include franchise-style partnerships and shared service platforms that enhance technology and purchasing capabilities while preserving local identity. For example, McDonald's expansion strategy, which combines company-owned locations with franchise partnerships, demonstrates how chains can balance standardization with local market adaptation. Independent operators, on the other hand, leverage their flexibility in menu innovation and customer relationship management. However, they face growing pressure to invest in digital ordering systems and delivery partnerships, which require significant capital investments typically associated with larger operators. Additionally, compliance with Food Standards Agency (FSA) regulations adds operational complexity for independents, particularly those without dedicated compliance staff. While this creates challenges, it also establishes barriers to entry that protect established operators from new competition.

By Locations: Standalone Strength with Lodging Surge

Standalone locations are projected to account for 75.92% of the market share in 2025, underscoring the continued significance of dedicated restaurant spaces that allow for complete control over customer experience and operational efficiency. In contrast, lodging-based foodservice is expected to exhibit the highest growth potential, with a CAGR of 9.78%. This growth is driven by the recovery of the hospitality sector and integrated guest experience strategies, which foster captive customer bases and higher average spending per visit. Retail locations benefit from synergies with foot traffic and extended operating hours, while travel locations face challenges due to transportation pattern fluctuations and regulatory restrictions, leading to operational uncertainties.

The strong growth in the lodging segment highlights the impact of strategic partnerships between hotel operators and restaurant brands, which create mutual value through shared customer acquisition and operational efficiencies. For instance, Whitbread's Premier Inn has integrated restaurant concepts to enhance guest satisfaction while generating additional revenue streams from both hotel guests and local customers. Leisure locations, on the other hand, experience seasonal demand fluctuations, necessitating flexible staffing models and menu adjustments. This operational complexity benefits operators with expertise in managing variable capacity utilization. Standalone operators retain advantages in location selection and lease negotiation flexibility but face increasing competition from multi-location concepts, which can secure premium real estate by leveraging diversified revenue streams across multiple sites.

By Service Type: Dine-in Recovery Meets Delivery Innovation

Dine-in services are projected to maintain a 54.62% market share in 2025, reflecting consumer preferences for social dining experiences and full-service hospitality that delivery formats cannot replicate. Meanwhile, the delivery service segment is expected to grow at a compound annual growth rate (CAGR) of 7.11% through 2031, driven by lasting behavioral shifts toward convenience-focused consumption. These changes, initially accelerated by pandemic restrictions, continue to expand due to advancements in technology platforms and logistics networks. Takeaway services occupy an intermediate position, offering speed and convenience while preserving direct customer relationships, which can be disrupted by third-party delivery platforms.

The evolution of service types necessitates that operators optimize operations across multiple channels simultaneously. Successful concepts are investing in kitchen layouts designed to efficiently handle dine-in, takeaway, and delivery orders without compromising quality or speed for any channel. For example, Domino's has invested in delivery optimization technologies, such as GPS tracking and predictive analytics for route planning, to enhance service quality while reducing operational costs. Moreover, dine-in services benefit from higher average order values and opportunities for upselling through personal service interactions. However, these advantages come with higher labor costs and significant real estate investments, which delivery-focused competitors can often avoid. On the other hand, the integration of digital ordering systems across all service types has become essential. These systems not only meet customer expectations for convenience but also provide valuable data for operational optimization and customer relationship management.

Geography Analysis

Regional differences in the foodservice market are shaped by economic conditions, demographic trends, and regulatory frameworks across England, Scotland, Wales, and Northern Ireland. London and the Southeast exhibit the highest market concentration due to factors such as population density, higher disposable income levels, and significant tourism activity. However, these regions also face intense competition and elevated operational costs. Scotland benefits from robust tourism demand and a distinctive culinary identity, while Wales and Northern Ireland offer growth potential through lower competition levels and government support programs aimed at developing the hospitality sector. Regional consumer preferences further create opportunities for locally tailored menu concepts and service formats that align with cultural tastes and spending behaviors.

Brexit has introduced regional variations in supply chains, with Northern Ireland's unique regulatory position influencing ingredient sourcing and compliance requirements differently compared to other United Kingdom regions. Additionally, the government's leveling-up initiatives provide targeted support for hospitality sector development in economically disadvantaged areas. These initiatives create opportunities for expansion-oriented operators to benefit from favorable financing options and regulatory assistance.

Regional employment patterns significantly impact labor availability and wage levels. For instance, London's tight labor market drives higher compensation costs, presenting challenges for operators. However, this also creates opportunities to attract talent by offering superior working conditions and career development programs. Also, urban and rural markets present distinct operational requirements. Urban locations benefit from delivery density and access to public transportation, while rural areas offer advantages such as lower real estate costs and reduced competition. These differences necessitate tailored operational strategies to address the unique characteristics of each market type.

Competitive Landscape

The foodservice market in the United Kingdom exhibits moderate fragmentation, with established chains like McDonald's, Starbucks, and Domino's operating alongside independent businesses and innovative digital-native brands. Leading players benefit from scale advantages in areas such as purchasing, marketing, and technology adoption. However, they face ongoing competition from smaller operators who quickly adapt to local preferences and emerging consumer trends. This competitive environment drives continuous innovation in menu offerings, service delivery, and customer engagement. Operators must balance the efficiencies of standardization with the need for localization to effectively appeal to diverse market segments.

Technology adoption has become increasingly important, serving as a critical factor in improving operational efficiency and enhancing customer experiences. Investments in AI-driven inventory management, predictive demand analytics, and integrated digital ordering platforms enable operators to optimize performance and remain competitive. For example, Starbucks’ mobile ordering system demonstrates how established brands utilize technology to maintain market share amidst competition from traditional rivals and delivery-focused disruptors. These technological advancements also provide deeper customer insights and enable personalized engagement, allowing brands to refine their service models in real time.

While competition is intense in mature urban markets, significant opportunities exist in underserved regions, emerging cuisine categories, and hybrid service formats that combine traditional dining with delivery optimization. These areas present growth potential for both established operators and new entrants, offering avenues to innovate and capture market share through strategic positioning and operational excellence. The interplay of market fragmentation, technological advancements, and untapped niches creates a dynamic and evolving competitive landscape in the United Kingdom foodservice market. Adaptability and differentiation remain essential for achieving growth and sustaining long-term success.

United Kingdom Foodservice Industry Leaders

-

McDonald's Corporation

-

Whitbread PLC

-

The Coca-Cola Company

-

Greggs plc

-

Starbucks Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Subway rolled out its 'Spudway' jacket potato range across the United Kingdom following a successful trial earlier this year. Jacket potatoes became a permanent menu item in all Subway restaurants in the United Kingdom. Available toppings included Cheese and Beans, Tuna Mayo, Meatball Marinara, and Chicken Tikka. Customers were also able to customize their jacket potatoes with any toppings from Subway's signature sandwich ingredients, such as proteins, salads, and sauces.

- September 2025: Domino’s launched a chicken-focused sub-brand, Chick ’N’ Dip. The sub-brand was trialed at 187 Domino’s locations in the northwest of England and Northern Ireland, with plans for nationwide expansion. The menu included a variety of chicken tenders, wings, and boneless bites, accompanied by a selection of nine dips inspired by global flavors: Garlic Aioli, BBQ, Hot Honey, Ghost Chilli Glaze, Katsu Curry, Mexican Mayo, Teriyaki, Garlic and Herb, and Buffalo Hot.

- August 2025: Costa Coffee announced the launch of a takeaway-only store at London Stansted Airport in the United Kingdom. Located airside, the store offered a selection of breakfast items, lunch options, and desserts, all designed for takeaway. The store's design emphasized quick and convenient service, with customers able to use the Click and Collect feature through the Costa Coffee app to place orders and minimize wait times.

United Kingdom Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

By Foodservice Type

| Cafes and Bars | Bars and Pubs |

| Café | |

| Juice/Smoothie/Desserts Bars | |

| Specialist Coffee and Tea Shops | |

| Cloud Kitchen | |

| Full Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| Quick Service Restaurants | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-based Cuisines | |

| Pizza | |

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafes and Bars | Bars and Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | Asian | |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | Bakeries | |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines | ||

| By Outlet | Chained Outlets | |

| Independent Outlets | ||

| By Locations | Leisure | |

| Lodging | ||

| Retail | ||

| Sandalone | ||

| Travel | ||

| By Service Type | Dine-in | |

| Takeaway | ||

| Delivery | ||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms