Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Ireland Data Center Power Market is Segmented by Component (Electrical Solutions and Services), Data Center Type (Hyperscaler/Cloud Service Providers, Colocation Providers, and More), Data Center Size (Small Size Data Centers, Medium Size Data Centers, Large Size Data Centers and More), Tier Type (Tier I and II, Tier III, Tier IV). The Market Forecasts are Provided in Terms of Value (USD)

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

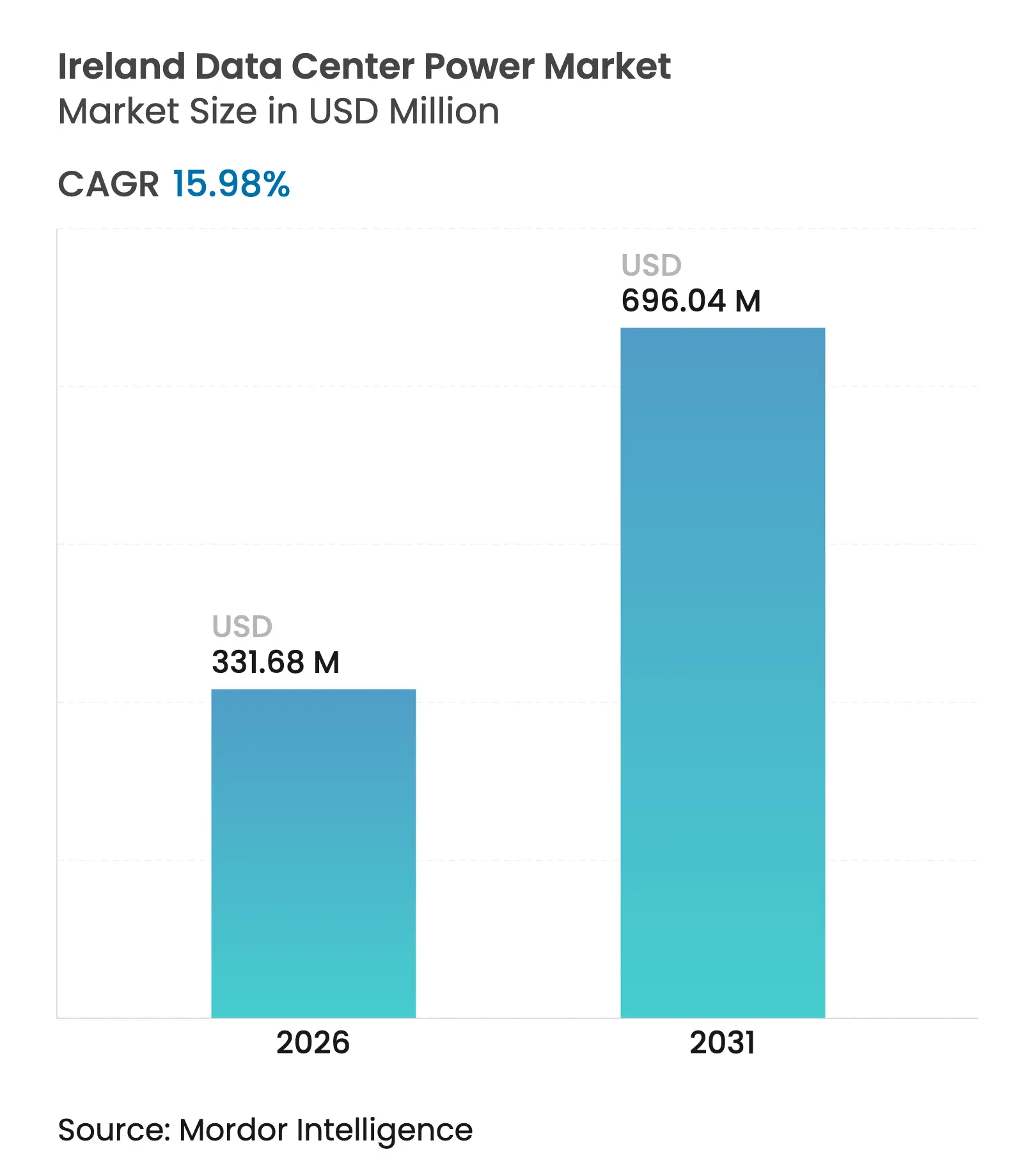

| Market Size (2026) | USD 331.68 Million |

| Market Size (2031) | USD 696.04 Million |

| Growth Rate (2026 - 2031) | 15.98 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Ireland data center power market size was valued at USD 285.98 million in 2025 and estimated to grow from USD 331.68 million in 2026 to reach USD 696.04 million by 2031, at a CAGR of 15.98% during the forecast period (2026-2031). Rapid cloud adoption, AI-driven workloads, and new on-site generation mandates are stretching existing infrastructure even as operators chase growth. Demand is shifting toward grid-interactive uninterruptible power supplies (UPS) and high-density power distribution units (PDUs) that can manage power peaks linked to generative AI servers. At the same time, the moratorium on new grid connections in Dublin is steering investment toward locations with headroom for renewable generation. Competitive dynamics now hinge on who can deploy modular power blocks fastest, monetize waste heat, and align with stricter sustainability rules.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Hyperscale

and Cloud Expansion

Hyperscale

and Cloud Expansion

| +5.2% | National, with concentration in Dublin | Medium term (2-4 years) |

(~)%

Impact on CAGR Forecast

:

+5.2%

|

Geographic Relevance

:

National,

with concentration in Dublin

|

Impact Timeline

:

Medium

term (2-4 years)

|

Opex-reduction

Demand (High-Efficiency UPS, PDUs)

Opex-reduction

Demand (High-Efficiency UPS, PDUs)

| +2.8% | National | Short term (≤ 2 years) | |||

AI/ML

Workloads Driving High-Density Power

AI/ML

Workloads Driving High-Density Power

| +4.5% | National, with concentration in Dublin | Medium term (2-4 years) | |||

Grid-Interactive

UPS and PPA Adoption

Grid-Interactive

UPS and PPA Adoption

| +1.9% | National | Medium term (2-4 years) | |||

CRU

On-Site Generation Mandate Fuelling Micro-Grids

CRU

On-Site Generation Mandate Fuelling Micro-Grids

| +3.1% | National | Short term (≤ 2 years) | |||

Monetisation

of Waste-Heat for District Heating

Monetisation

of Waste-Heat for District Heating

| +1.4% | National, with early gains in Dublin | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Hyperscale and Cloud Expansion: Reshaping Ireland’s Digital Infrastructure

Dublin now hosts 5% of global hyperscale capacity, making it the third-largest hyperscale hub worldwide. Power densities in these campuses exceed those of enterprise sites, compelling operators to standardize modular 100 MW building blocks that can be energized quickly. Microsoft’s newest Dublin build is tailored to European AI demand and incorporates pre-fabricated power rooms that shave two years off construction schedules. Financing models increasingly bundle long-term renewable power purchase agreements (PPAs) to hedge rising electricity costs. Colocation players are upgrading older halls to compete on efficiency, often layering grid-support capabilities into UPS fleets to create fresh revenue streams. As hyperscalers scale outward, secondary cities now court projects by guaranteeing land, natural-gas access, and fast-track permits.

AI/ML Workloads: Redefining Power Density Requirements

Generative AI servers in Ireland draw three to four times the power of legacy CPU racks, accelerating a shift to liquid cooling and busbar-based distribution. The International Energy Agency warns that global data center demand could touch 945 TWh by 2030, with AI workloads representing one-fifth of that total.[1]International Energy Agency / Ifri, “AI, Data Centers and Energy Demand,” ifri.org Irish operators now specify rack densities above 70 kW, driving adoption of smart PDUs that report circuit-level draw in real time. Liquid-to-chip cooling loops are being paired with heat-recovery skids that supply district networks, exemplified by the Tallaght scheme that taps AWS waste heat to warm municipal buildings.

CRU On-Site Generation Mandate: Catalyzing Microgrid Development

Since 2025, new Irish data centers must match imported power with on-site generation or storage, effectively turning each campus into a micro-utility. Developers now integrate gas turbines, solar arrays, and battery energy storage systems (BESS) into the base design to satisfy the rule. Eaton and Siemens Energy’s modular 500 MW plant concept illustrates how packaged gas-plus-hydrogen solutions can be dropped into constrained grids and later converted to zero-carbon fuels.[2]Eaton Corporation, “Eaton, Siemens Energy Join Forces to Provide Power and Technology,” stocktitan.net Financing structures reward plants that trade surplus generation into the wholesale market, giving operators a hedge against volatile tariffs. The mandate also spurs collaboration with utilities to align dispatch schedules with national renewable peaks, minimizing curtailment.

Grid-Interactive UPS: Turning Loads into Grid Assets

Microsoft proved that a modern UPS fleet can deliver frequency-response capacity without jeopardizing uptime, unlocking new income via the DS3 ancillary-services program. A single 50 MW campus can dedicate up to 20% of its power budget to system-stabilization calls, a critical lever as data centers now represent 21% of Ireland’s electricity load and could hit 30% by 2030.[3]Commission for Regulation of Utilities, “Large Energy Users Connection Policy Proposed Decision Paper,” cru.ie Vendors such as ABB and Vertiv embed grid-support logic into new UPS frames, synchronizing discharge windows with EirGrid’s dispatch signals. Participation allows operators to offset higher energy costs tied to AI racks while bolstering national grid resilience.

Restraint Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

Installation and Maintenance Costs

High

Installation and Maintenance Costs

| -2.1% | National | Medium term (2-4 years) |

(~)%

Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

National

|

Impact Timeline

:

Medium

term (2-4 years)

|

Dublin

Grid Moratorium and Capacity Constraints

Dublin

Grid Moratorium and Capacity Constraints

| -4.3% | Dublin region | Short term (≤ 2 years) | |||

Pending

Diesel-Genset Phase-Out Regulation

Pending

Diesel-Genset Phase-Out Regulation

| -1.8% | National | Medium term (2-4 years) | |||

Li-ion

UPS Battery Supply-Chain Bottlenecks

Li-ion

UPS Battery Supply-Chain Bottlenecks

| -1.5% | National | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Dublin Grid Moratorium: Reshaping Development Patterns

EirGrid’s freeze on new megawatt-scale connections in Dublin through 2028 affects the 82 facilities that already dominate national capacity. Operators lacking signed agreements are diverting budgets to counties Wicklow and Westmeath, where land banks can be coupled with private gas feeds. Echelon’s EUR 3.5 billion Wicklow campus showcases this pivot, combining wind PPAs and embedded generation to bypass urban bottlenecks. The moratorium also accelerates interest in subsea connectivity projects that anchor outside the capital, such as Amazon’s Cork landing station linking Ireland to the US.

Pending Diesel-Genset Phase-Out: Accelerating Backup Innovation

Ireland’s forthcoming rules that curb diesel standby units are pushing operators toward gas-fired sets, hydrogen-ready turbines, and battery energy storage. Lithium-ion prices now justify installing BESS blocks sized to ride through typical outage windows, complemented by renewable firming during off-peak hours. Some operators trial hydrotreated vegetable oil (HVO) in existing diesel fleets to cut emissions ahead of formal deadlines. Schneider Electric’s microgrid controller orchestrates these hybrids, ensuring seamless failover while reporting real-time emissions to meet compulsory annual disclosures.

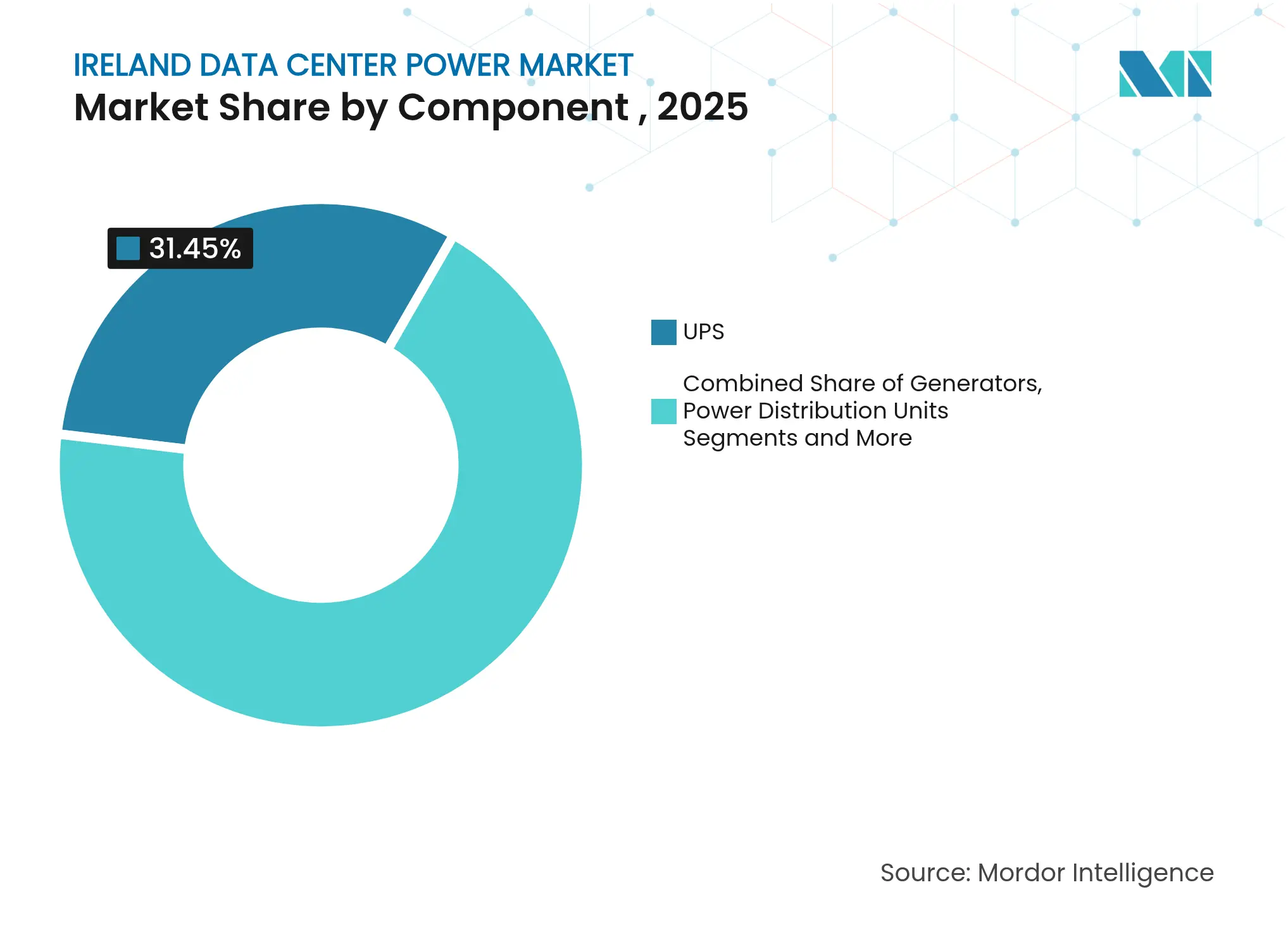

By Component: Shift Toward Intelligent Power Platforms

UPS systems generated 31.45% of 2025 revenue, anchoring the Ireland data center power market as operators prize proven ride-through capability. The newest frames add lithium-ion batteries and grid-interactive controls, turning traditional backup into dispatchable capacity that earns ancillary-service fees. Vendors such as Eaton bundle predictive analytics that flag battery degradation early, cutting maintenance spend and averting unplanned outages. Intelligent bypass features also let technicians isolate modules without dropping load, a key factor for Tier IV contracts driving zero-downtime service-level agreements.

PDUs represent the fastest-growing slice, expanding at 16.92% CAGR as sensors and branch-circuit monitoring become compulsory in AI halls. Granular insight into sub-rack consumption supports dynamic load placement, helping to shave peaks that would otherwise trigger expensive grid-capacity charges.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Colocation Dominance Meets Hyperscale Momentum

Colocation vendors held 34.62% of 2025 revenue, capturing enterprises that prefer opex-friendly footprints over greenfield builds. Established grid contracts give these incumbents bargaining power in a constrained market, allowing them to resell capacity to newer entrants that lack permits in Dublin. Inter-connection density within carrier-neutral halls also attracts content providers that need low-latency hand-offs, making colocation a durable pillar of the Ireland data center power market.

Hyperscale operators, however, post the steepest growth at 19.74% CAGR to 2031 as generative AI drives server refresh cycles. Cloud giants increasingly co-locate dedicated power substations on campus to meet CRU’s one-to-one import rules, effectively securing control over their energy destiny. Many pairs of on-site turbines with wind PPAs to meet corporate carbon targets while navigating curtailment risks. This self-sufficiency model is reshaping supplier negotiations, with hyperscalers insisting on modular power skids that arrive pre-wired to compress deployment timelines.

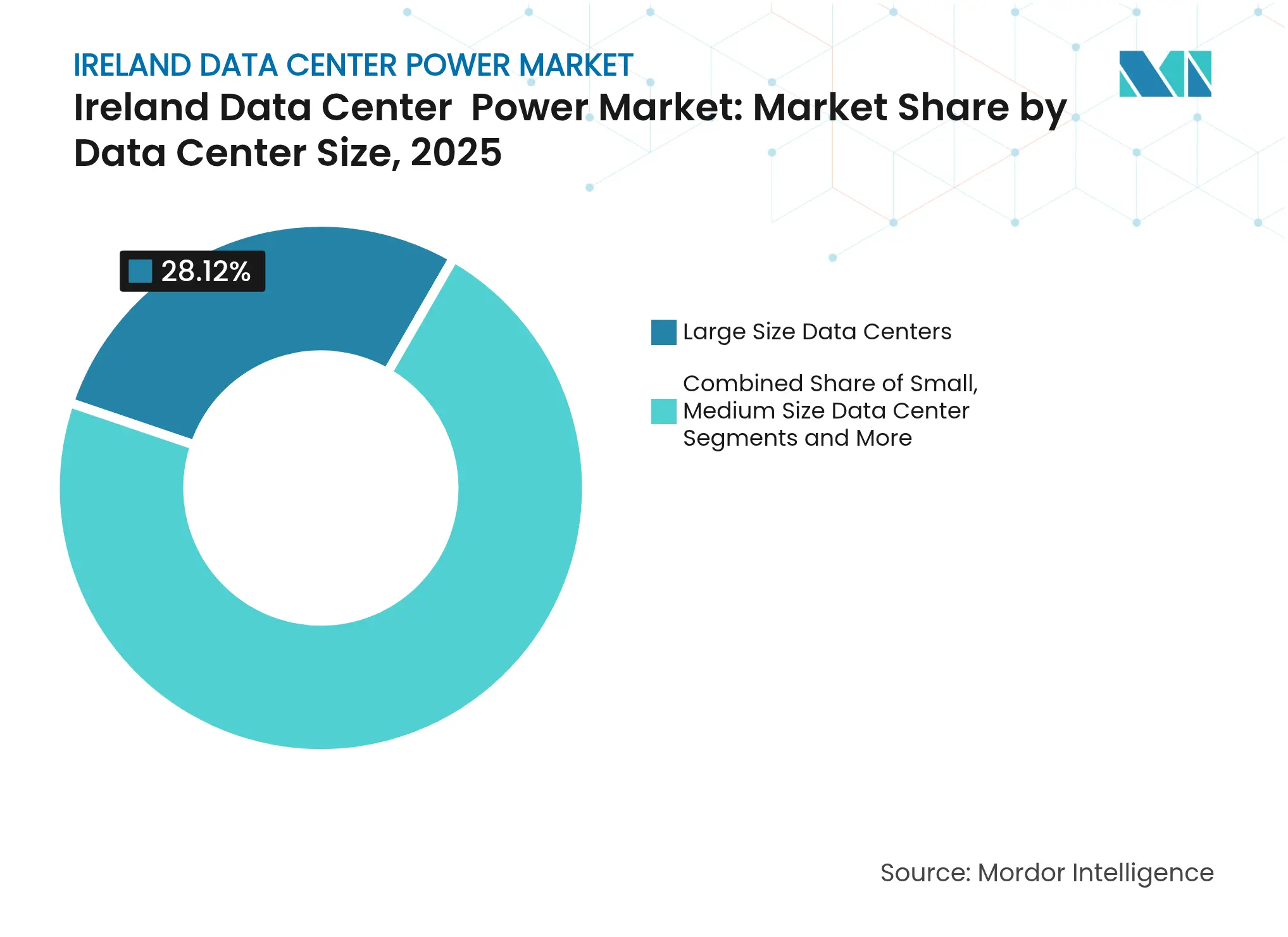

By Data Center Size: Scaling Up for AI Era

Large sites accounted for 28.12% of the Ireland data center power market size in 2025, offering a practical bridge between legacy enterprise footprints and hyperscale campuses. These facilities often tap existing industrial feeders, avoiding lengthy transmission upgrades in Dublin’s urban core. Operators invest in AI-driven predictive maintenance that parses vibration and thermal signatures, extending asset life without sacrificing uptime.

Mega centers will log a 21.06% CAGR through 2031, propelled by multinationals consolidating European workloads. A single mega campus can require 100 MW of power, prompting developers to site projects near gas pipelines and wind corridors outside Dublin. The Ireland data center power market size for mega builds is set to climb sharply once Wicklow and Westmeath campuses reach full energisation, underlining the migration of capacity toward regions with grid headroom.

Note: Segment shares of all individual segments available upon report purchase

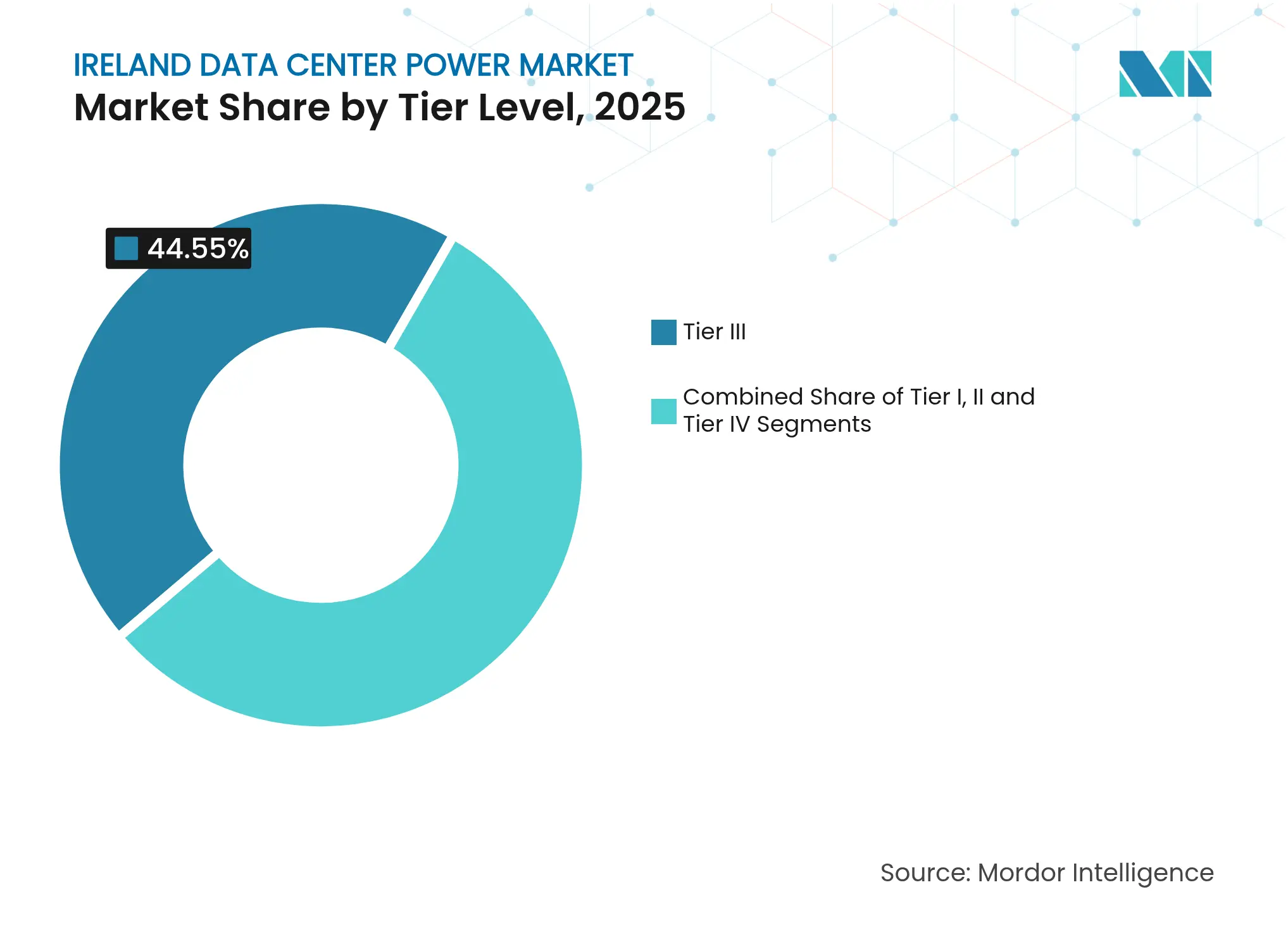

By Tier Level: Reliability Premium Intensifies

Tier III facilities captured 44.55% of the Ireland data center power market size in 2025, balancing cost with the N+1 redundancy most enterprises deem sufficient. Concurrent maintainability lets operators swap components without downtime, aligning with service-credit clauses in colocation contracts. Financing partners favor the proven Tier III template because design risk is lower and payback periods are clearer.

Tier IV footprints will expand at 20.58% CAGR as AI inference clusters, fintech trading engines, and sovereign-cloud mandates demand fault-tolerant environments. Double-bus UPS topologies, dual utility feeds, and mirrored switchgear grids drive capex but unlock premium pricing among latency-sensitive clients. The CRU’s generation rule accelerates Tier IV adoption of micro-grids that couple gas turbines, BESS, and potentially green hydrogen to guarantee uptime while staying within carbon budgets.

Note: Segment shares of all individual segments available upon report purchase

County Wicklow demonstrates the new playbook. Echelon’s EUR 3.5 billion campus will run hybrid gas-plus-wind micro-grids that export surplus energy, satisfying CRU’s import-matching requirement and monetizing excess through wholesale markets. Wicklow also benefits from planned subsea cables that will land outside Dublin, lowering latency to North America and the UK, a draw for hyperscalers seeking resilient routes.

Attention is shifting westward where robust wind resources and cool Atlantic air enable free cooling for much of the year. Counties Clare and Galway market available land close to high-voltage lines carrying renewable flows from offshore arrays, positioning themselves as future growth corridors. The government’s Climate Action Plan, targeting 80% renewable electricity by 2030, bolsters this pitch by prioritizing transmission upgrades that deliver clean energy to industrial clusters Over the next five years, the Ireland data center power market is likely to mature into a multi-node ecosystem that spreads load, supports higher renewable penetration, and reduces the capital’s grid strain.

Market Concentration

Global power-infrastructure majors ABB, Eaton, Schneider Electric, and Vertiv anchor the supply side of the Ireland data center power market. Their portfolios span UPS, switchgear, DCIM, and micro-grid controls, allowing one-stop procurement for hyperscale clients. Recent strategy centers on embedding data-enabled services; Vertiv’s AI-ready UPS line launched in April 2025 adds neural-network algorithms that learn load patterns and optimize inverter performance. In niche segments, startups provide edge-scale power skids that can be delivered in containerized modules within 12 weeks, a value proposition for telecoms deploying distributed AI inference nodes.

Partnerships are multiplying as hardware and generation worlds converge. Eaton’s tie-up with Siemens Energy on a 500 MW modular plant targets developers who must meet on-site generation quotas fast, promising two-year schedule savings compared with bespoke builds. ABB teams with gas-turbine specialists to market hydrogen-ready backup blocks, aligning with anticipated diesel exit requirements.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Ireland Data Center Power Baseline Earns Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 285.98 mn (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 245.90 mn (2025) | Regional Consultancy A | narrower scope (UPS and gensets only) and biennial updates | ||

EUR 400 mn (2024) | Trade Journal B | counts capex outlays and uses fixed 2022 exchange rate |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.