Erectile Dysfunction Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

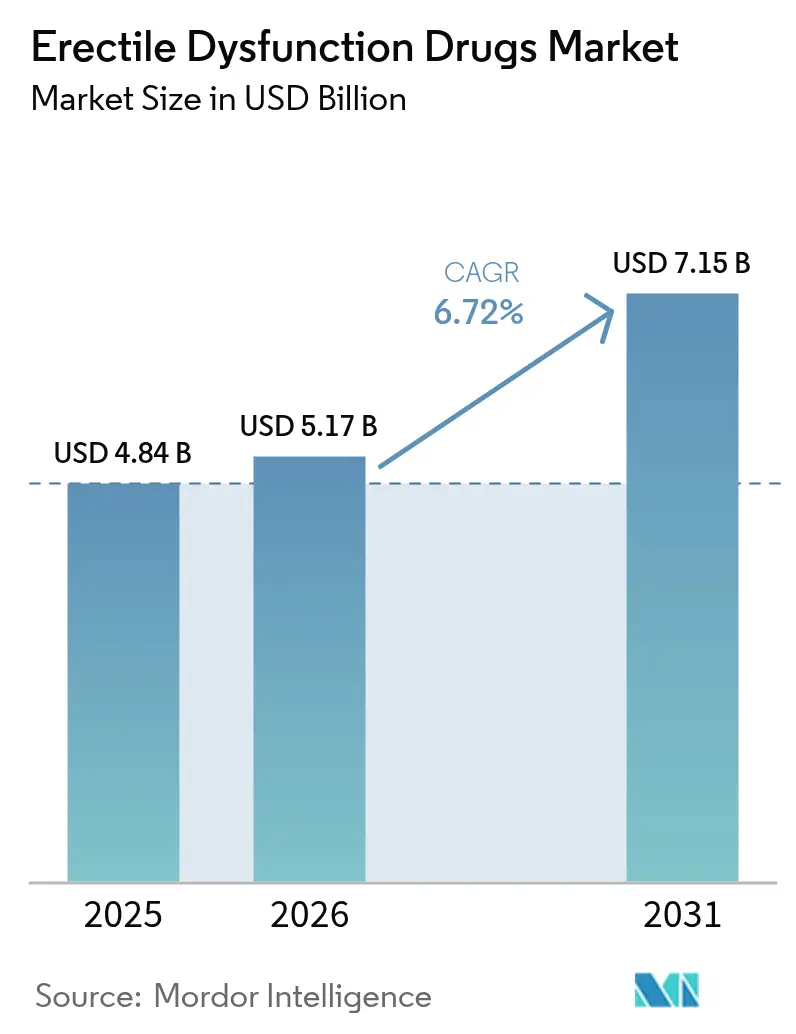

| Market Size (2026) | USD 5.17 Billion |

| Market Size (2031) | USD 7.15 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Erectile Dysfunction Drugs Market Analysis by Mordor Intelligence

The erectile dysfunction drugs market size was valued at USD 4.84 billion in 2025 and estimated to grow from USD 5.17 billion in 2026 to reach USD 7.15 billion by 2031, at a CAGR of 6.72% during the forecast period (2026-2031). Growth reflects an accelerating migration from traditional retail dispensing toward integrated telemedicine ecosystems that combine virtual consultation, electronic prescribing, and home delivery. Over-the-counter (OTC) regulatory pathways, especially in the United States and parts of Europe, are broadening patient access while lowering entry barriers for consumer-health companies. Aging populations, rising obesity and diabetes prevalence, and wider recognition of erectile dysfunction as an early cardiometabolic warning sign reinforce steady baseline demand. Competitive dynamics intensify as branded patents expire and generic competition compresses prices, prompting originators to develop alternative formulations, pursue combination products, and deepen partnerships with digital health platforms.

Key Report Takeaways

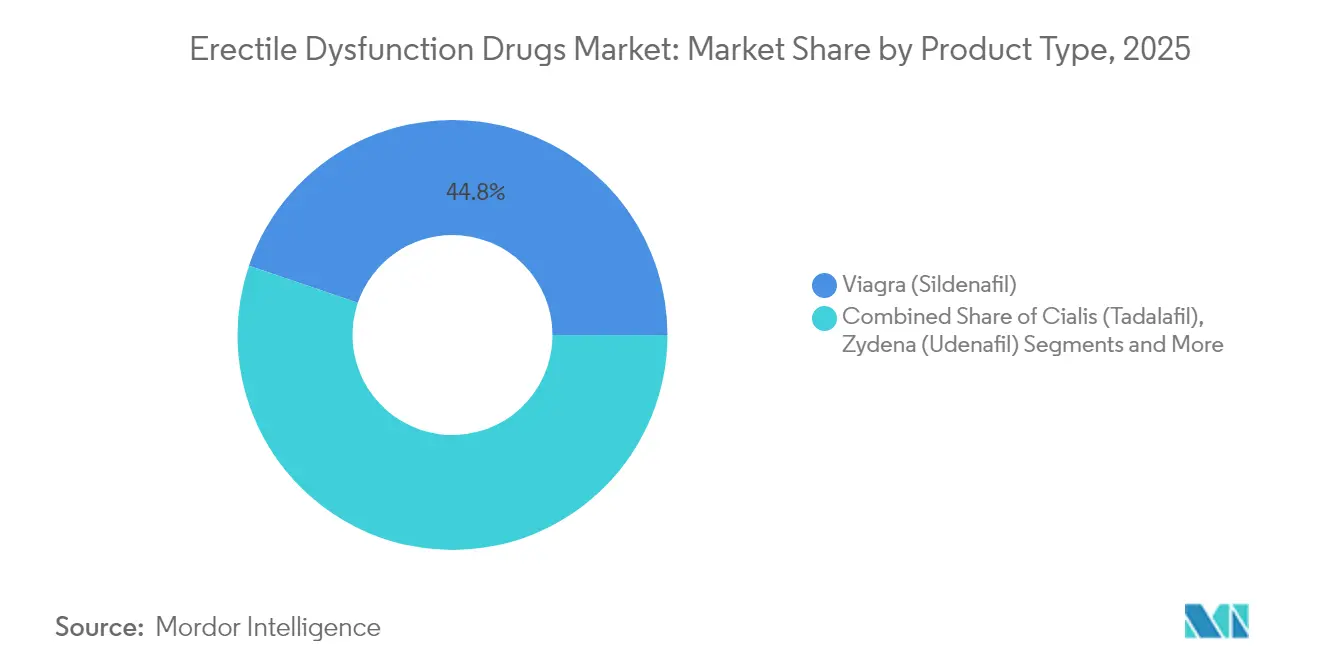

- By product type, Viagra retained 44.78% revenue share in 2025, while Stendra is set to grow at a 9.72% CAGR to 2031.

- By drug class, phosphodiesterase-5 (PDE5) inhibitors commanded 85.12% of the erectile dysfunction drugs market share in 2025; novel mechanisms are forecast to expand at an 11.1% CAGR through 2031.

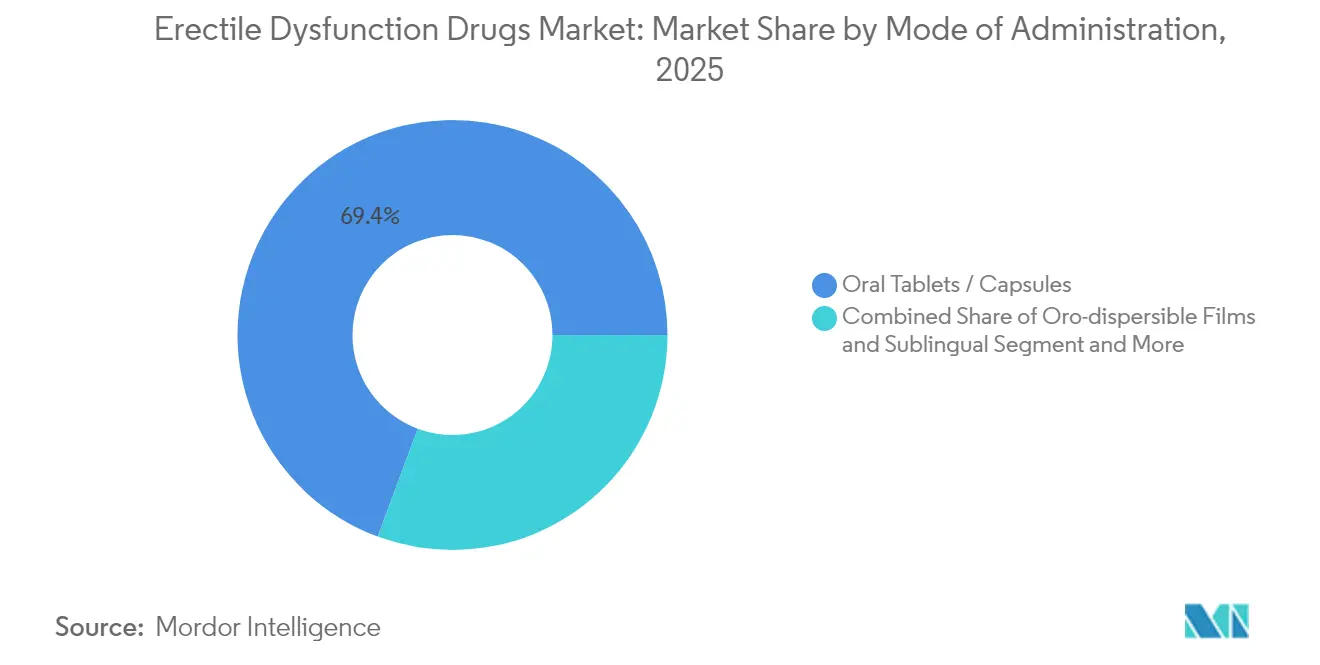

- By mode of administration, oral tablets accounted for 69.35% of the erectile dysfunction drugs market size in 2025, whereas oro-dispersible films and sublingual formats will rise at a 12.05% CAGR to 2031.

- By distribution channel, retail pharmacies held 47.20% of the erectile dysfunction drugs market size in 2025, yet online pharmacies and direct-to-consumer platforms are advancing at a 11.7% CAGR.

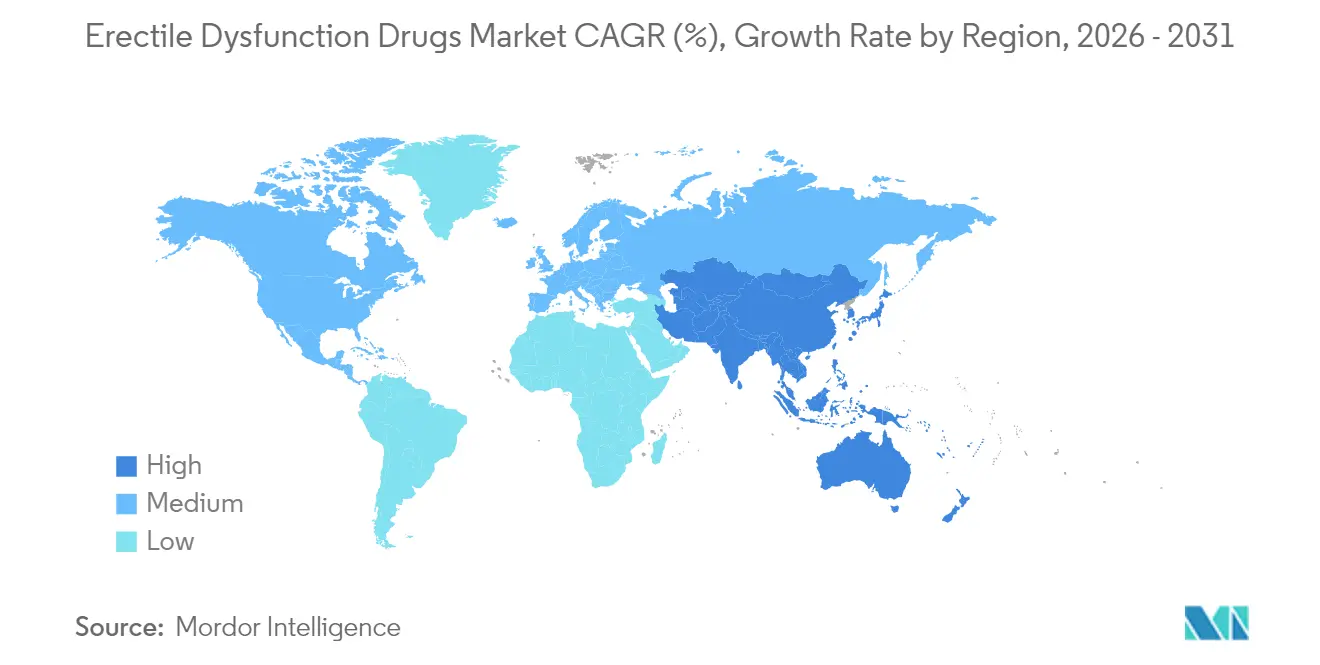

- By geography, Asia-Pacific is projected to grow at a 10.04% CAGR and thereby represents the fastest-expanding regional pocket within the erectile dysfunction drugs market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Erectile Dysfunction Drugs Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Related Comorbidities Boost PDE5 Demand | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Increasing Lifestyle-Induced Stress & Obesity Prevalence | +1.2% | Global, particularly urban centers in APAC & North America | Medium term (2-4 years) |

| Growing Tele-Medicine & E-Pharmacy Penetration | +2.1% | Global, led by North America with rapid APAC adoption | Short term (≤ 2 years) |

| Wider Off-Label Use In BPH & LUTS Management | +0.9% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Nasal & Topical Fast-Onset Formulations Nearing Approval | +1.4% | Global, initial launch in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Telemedicine & E-Pharmacy Penetration

Digital platforms remove geographic and psychological barriers, allowing discreet consultations and mail-order fulfillment in a single workflow. Hims & Hers expanded to 2.4 million subscribers and more than doubled revenue in Q1 2025 by integrating asynchronous medical evaluations with low-cost generic sildenafil hims.com. Similar models from Lemonaid Health price sildenafil at USD 2 per pill, undercutting brick-and-mortar pharmacies and encouraging price-sensitive users to enter the erectile dysfunction drugs market. GoodRx launched a subscription service for erectile dysfunction therapies in June 2025, reinforcing consumer appetite for predictable monthly costs. Platform data analytics guide personalized adherence nudges that improve refill persistence, lifting lifetime value per patient. As governments relax telehealth reimbursement restrictions, particularly in Asia-Pacific, digital incumbents enjoy a first-mover trust advantage that is hard for late-stage entrants to replicate.

Nasal & Topical Fast-Onset Formulations Nearing Approval

Formulations that shorten onset time from nearly an hour to under 15 minutes solve a key dissatisfaction point cited in follow-up surveys of oral PDE5 non-responders. LTR Pharma’s SPONTAN nasal spray peaks plasma levels in 12 minutes with half the oral dosage, positioning the drug for premium pricing when approved. The FDA’s 2024 De Novo clearance for Eroxon gel created the first OTC topical category, with 60% of users reporting erection within 10 minutes[1]United States Food and Drug Administration, “DENOVO CLASSIFICATION REQUEST FOR EROXON,” fda.gov. Futura Medical is pursuing enhanced versions that target both male and female sexual dysfunction, broadening addressable revenue pools. Topical agents also serve patients contraindicated for systemic therapy, extending market reach without cannibalizing established oral brands. Manufacturers expect accelerated global rollouts once real-world safety data accumulate.

Aging-Related Comorbidities Boost PDE5 Demand

Beyond sexual function restoration, longitudinal research links long-term tadalafil use to reduced cardiovascular mortality and slower cognitive decline[2]PubMed, “Benefits of Tadalafil and Sildenafil on Mortality, Cardiovascular Disease, and Dementia,” pubmed.ncbi.nlm.nih.gov. Among diabetics, erectile dysfunction prevalence stands at 65.8%, with peripheral vascular disease as a key exacerbating factor. Clinicians increasingly prescribe tadalafil daily dosing to treat both erectile dysfunction and benign prostatic hyperplasia, simplifying polypharmacy for older men. ENTADFI’s fixed-dose combination of finasteride and tadalafil exemplifies how converging disease burdens stimulate innovation in the erectile dysfunction drugs industry. Health-system protocols that screen for erectile dysfunction during routine cardiology visits drive earlier diagnosis, ultimately feeding a virtuous prescription cycle.

Increasing Lifestyle-Induced Stress & Obesity Prevalence

Younger men once viewed as a marginal customer segment now represent a sizable source of incremental prescriptions. A 2024 Nature study found 57.1% erectile dysfunction prevalence in men aged 18-40, with 39.0% reporting prior therapy use. Urban lifestyles marked by poor sleep hygiene, high-glycemic diets, and chronic stress disrupt endothelial health, accelerating vasculogenic dysfunction. Telemedicine portals bundle mindfulness coaching, dietary advice, and prescription refills, integrating pharmacologic and behavioral interventions under one subscription. This holistic approach widens appeal beyond acute symptom relief, cultivating sticky engagement inside the erectile dysfunction drugs market.

Restraints Impact Analysis of Erectile Dysfunction Drugs Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting Social Stigma & Under-Diagnosis | -1.5% | Global, particularly pronounced in conservative societies | Long term (≥ 4 years) |

| High Out-Of-Pocket Cost For Branded Therapies | -1.1% | Global, most significant in markets with limited insurance coverage | Medium term (2-4 years) |

| Online Counterfeit Supply Hurting Safety & Trust | -0.8% | Global, concentrated in regions with weak regulatory oversight | Short term (≤ 2 years) |

| Sub-Optimal Long-Term Adherence In Cardio-Metabolic Patients | -0.7% | Global, particularly affecting diabetic and cardiovascular patient populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persisting Social Stigma & Under-Diagnosis

Cultural taboos limit physician-patient dialogue, especially in rural regions where urologist density tracks well below search-term interest levels. Anonymous telehealth chats mitigate embarrassment yet cannot fully replace in-person screening where psychological or relational factors complicate assessment. Younger men often self-diagnose via online forums, delaying professional evaluation until comorbidities surface. Education campaigns timed around OTC launches aim to reframe erectile dysfunction as an early cardiometabolic signal rather than a purely sexual issue. Nevertheless, stigma is expected to weigh on adoption rates for at least the next decade.

High Out-of-Pocket Cost for Branded Therapies

Private insurers continue to classify many erectile dysfunction products as lifestyle agents, limiting reimbursement. Cigna’s 2025 policy caps tadalafil quantities and mandates prior authorization, adding friction that drives cash-pay behaviors[3]Cigna, “Tadalafil (Cialis) Coverage Position Criteria,” cigna.com. Medicare’s exclusion of oral PDE5s steers seniors toward higher-cost surgical solutions that paradoxically receive coverage. Generic entries from Teva and Camber have narrowed price spreads, yet branded makers still command premiums through patient-support programs and perceived quality assurance. While digital pharmacies advertise USD 2 sildenafil, absence of insurance reimbursement keeps many middle-income patients under-treated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Erectile Dysfunction Drugs Market Segment Analysis

By Product Type:

Generics Challenge Brand DominanceThe Viagra franchise maintained a leading 44.78% slice of the erectile dysfunction drugs market in 2025, reflecting decades-long brand equity and prescriber familiarity. However, Teva’s AB-rated sildenafil tablets priced at a deep discount eroded trademark loyalty throughout 2025. Stendra’s rapid onset profile and limited food interaction helped the brand register a 9.72% CAGR, the highest among on-patent agents. Cialis benefited from its dual-indication label covering benign prostatic hyperplasia, sustaining cash flows despite generic tadalafil entries in several markets. Levitra lost shelf space as payers prioritized lower-cost therapeutic equivalents. Topical Eroxon created a non-pill alternative that appeals to patients wary of systemic side effects, marking a structural inflection in the erectile dysfunction drugs market. Regional brands such as Zydena remained confined to South Korea and select Asian countries, limiting global influence. Overall, generics are projected to capture incremental volume, but innovative delivery formats will protect premium niches. Branded incumbents respond with life-cycle extensions like oro-dispersible films to defend share.

Second-generation brands also exploit pharmacokinetic tweaks to differentiate, offering ultra-rapid uptake or longer half-lives. Fixed-dose combination products such as ENTADFI illustrate how shared pathophysiology between prostate enlargement and erectile dysfunction supports multi-symptom positioning. These dynamics align with broader OTC liberalization efforts, pointing to a fragmented yet opportunity-rich competitive canvas for the erectile dysfunction drugs market.

By Drug Class:

Novel Mechanisms EmergePDE5 inhibitors generated 85.12% of 2025 revenue, cementing their status as first-line pharmacotherapy. Nevertheless, a pipeline of nitric-oxide donors, Rho-kinase inhibitors, and centrally acting agents is moving through Phase II and III trials. Novel mechanisms collectively post an 11.1% CAGR, suggesting room for differentiated efficacy and tolerability profiles. Prostaglandin analogues preserved a niche role for patients with nitrate contraindications but face compliance challenges due to local administration discomfort. Clinical interest in protein kinase C inhibition rose after MDPI-published data showed restored nitric-oxide signaling in diabetic cavernosal tissue. Combination regimens mixing low-dose PDE5 with peripheral vasodilators seek to reduce systemic exposure while maintaining potency, a strategy expected to entice risk-averse prescribers.

Patents surrounding pyrazolopyrimidinone derivatives exemplify the ongoing innovation race as originators attempt to lock in next-generation exclusivity drugpatentwatch.com. Should centrally acting molecules overcome safety hurdles, they could redefine therapeutic sequencing in the erectile dysfunction drugs industry by addressing psychogenic etiology more directly. For now, PDE5s dominate treatment algorithms, but pharmacologic diversification is gathering momentum.

By Mode of Administration:

Convenience Drives InnovationOral tablets retained 69.35% of volume in 2025 thanks to established physician comfort and wide retail distribution. Yet oro-dispersible films, sublingual wafers, and nasal sprays are expanding the erectile dysfunction drugs market by solving pain points around timing and discretion. Sublingual avanafil delivers higher bioavailability while avoiding first-pass metabolism, translating to lower required dosages. Viatris introduced a discreet melting wafer formulation of sildenafil, leveraging patient feedback that blue tablets invite embarrassment. Nasal sprays promise near-immediate responsiveness, particularly attractive to younger men who value spontaneity. OTC topical gels like Eroxon circumvent systemic exposure, making them suitable for users with polypharmacy concerns. Physicians also favor topical and nasal routes for patients on antihypertensive regimens, where systemic vasodilation could be problematic. The administration landscape is therefore bifurcating: convenience-oriented devices court new adopters while tablets maintain baseline adherence among long-time users. Manufacturers that master multi-format portfolios can hedge against shifting preferences in the erectile dysfunction drugs market.

Across formats, packaging innovations emphasize user confidentiality, with single-dose sachets and unbranded shipping boxes. These enhancements align with digital subscription services that replenish inventory automatically, ensuring on-hand supply and reducing non-adherence related to pharmacy visits or stigma.

By Distribution Channel:

Digital Disruption AcceleratesRetail pharmacies captured 47.20% of 2025 sales but now face margin compression from vertically integrated telehealth players. Online channels are posting a 11.7% CAGR, propelled by rapid e-script processing and same-day shipping promises. Hims & Hers’ acquisition of Europe-based ZAVA delivered instant licensing coverage across four major EU markets, demonstrating roll-up economics that favor capital-rich incumbents hims.com. Hospital pharmacies remain critical for post-prostatectomy care, where injectable agents or vacuum devices supplement oral therapy. Direct-to-consumer portals differentiate via transparent pricing and ancillary lab testing bundles, locking customers into multi-product ecosystems that extend beyond erectile dysfunction. OTC approvals will likely redistribute volume back to mass-market chains, yet subscription discounts and auto-refill convenience may keep digital penetration high. Regulators are also weighing mandates for verified internet pharmacy seals to combat counterfeit risk, potentially raising entry barriers for small online retailers. Overall, channel diversification intensifies competition while widening patient choice inside the erectile dysfunction drugs market.

Drug manufacturers increasingly strike exclusive supply agreements with telehealth networks, exchanging volume commitments for preferred-brand positioning. Such deals mirror historical managed-care formularies, except that the purchasing decision now sits directly with the consumer, making user experience and digital marketing pivotal success factors.

Geography Analysis

North America and Europe Erectile Dysfunction Drugs Market

North America generated 38.44% of global revenue in 2025, sustained by high discretionary income, advanced telehealth coverage, and early OTC regulatory pilots. The FDA’s landmark green light for Eroxon established a template other regulators now study, reinforcing the region’s leadership in self-care models. Still, generic saturation and payer cost controls temper absolute growth, bending the North American CAGR closer to the 6.72% global mean. Europe shares similar maturity, yet remains a focal point for digital health expansion; the Hims & Hers-ZAVA deal instantly unlocked multi-country reach without protracted license registrations.

APAC, South America and MEA Erectile Dysfunction Drugs Market

Asia-Pacific posted the highest CAGR at 10.04%, driven by demographic aging in China, Japan, and South Korea, coupled with regulatory modernization. China’s 2025 guideline overhaul accelerates new-drug reviews, slashing approval timelines to under 200 days and attracting cross-border license applications. Japan’s pharmaceutical revitalization initiatives include fee waivers for digital trial submissions, encouraging global sponsors to site late-phase studies locally. Regional distributors such as Zuellig Pharma bought Cialis rights in ASEAN markets to consolidate supply chains and localize marketing. South America and the Middle East & Africa trail in absolute size but show accelerating online-pharmacy adoption as smartphone penetration climbs. Payment-gateway innovation in Brazil and Saudi Arabia lowers cross-border import frictions, allowing global brands to seed awareness ahead of formal regulatory approvals. However, fragmented reimbursement frameworks and lingering cultural stigma remain structural hurdles. Long-term prospects hinge on public-health recognition that sexual health intersects broader non-communicable disease management, a narrative gaining traction among regional policymakers.

Competitive Landscape

The erectile dysfunction drugs market features a moderately concentrated structure where the top five brands control significant global revenue. Viatris’ stewardship of Viagra faces erosion from low-cost generics, prompting the firm to prioritize life-cycle extensions such as oro-dispersible films that target discretion-oriented consumers. Mixed Q2 2024 revenue underscored vulnerability to patent cliffs, yet Viatris’ global manufacturing footprint remains a formidable moat. Teva leverages scale and early ANDA filings to flood markets with price-competitive sildenafil, tadalafil, and vardenafil, siphoning share from incumbents while still profiting from volume efficiencies.

Digital-native challengers compete on convenience, service bundling, and brand community rather than molecule ownership. Hims & Hers doubled revenue year on year by curating subscription bundles that combine teleconsultations, generic medication, and at-home diagnostics, thereby extending wallet share beyond a single therapeutic class. GoodRx and Amazon Clinic are fast followers, exploiting data-rich ecosystems to personalize offers and optimize inventory.

White-space innovators explore under-served niches such as rapid-onset nasal sprays and gender-inclusive topicals. LTR Pharma’s SPONTAN positions itself for cardiology co-management protocols, given its low systemic exposure profile. Futura Medical aims to penetrate female arousal disorder markets with an enhanced Eroxon variant, multiplying addressable sales without diluting male-focused branding. Patent filings for combination therapies indicate that future rivalry will extend into fixed-dose hybrids addressing comorbid urinary symptoms.

Regulatory acumen becomes a competitive weapon as firms jockey to secure OTC status. Sanofi’s Opella division is running the first real-world self-selection study for OTC Cialis, a move that could grant multi-year head-start advantages in pharmacy aisles. Manufacturers unable to demonstrate consumer comprehension of labeling may find themselves locked out of the fastest-growing channel. Overall, competition is shifting from chemistry to channel and consumer experience, altering the traditional pharmaceutical playbook inside the erectile dysfunction drugs market.

Erectile Dysfunction Drugs Industry Leaders

Pfizer Inc.

Bayer AG

Eli Lilly and Company

GSK plc

Lupin Limited

- *Disclaimer: Major Players sorted in no particular order

Erectile Dysfunction Drugs Market Companies Covered in this Report

- Pfizer

- Eli Lilly and Company

- Bayer

- Teva Pharmaceutical Industries

- Viatris

- Cipla

- Lupin

- Aurobindo Pharma

- Dr. Reddy’s Laboratories

- Sun Pharmaceuticals Industries

- Futura Medical plc

- Petros Pharmaceuticals

- Apricus Biosciences

- Vivus

- S.K. Chemicals

- LTR Pharma Pty Ltd

- Endo International

- Sanofi

- Glenmark Pharmaceuticals

Recent Industry Developments in Erectile Dysfunction Drugs Market

- January 2025: Sanofi’s Opella division received FDA clearance to initiate an actual-use study for OTC Cialis, the first PDE5 inhibitor to reach this stage.

- October 2024: Camber Pharmaceuticals introduced generic Stendra tablets in 50 mg, 100 mg, and 200 mg strengths following patent expiry.

- June 2024: Teva launched generic Viagra tablets across the United States, accelerating price erosion in sildenafil.

Erectile Dysfunction Drugs Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global erectile dysfunction drugs market as prescription and over-the-counter pharmacological agents, principally PDE-5 inhibitors, prostaglandin analogues, centrally acting agents, nitric-oxide donors, and pipeline novel mechanisms, sold through hospital, retail, and online channels to treat male erectile dysfunction. Value estimates cover 17 major countries and reflect branded and generic sales in U.S. dollars at ex-manufacturer prices, converted quarterly.

Scope exclusion: mechanical devices, implants, shock-wave therapy, and vacuum pumps are not counted.

Segments Covered in This Report

- By Product Type

- Viagra (Sildenafil)

- Cialis (Tadalafil)

- Levitra / Staxyn (Vardenafil)

- Stendra / Spedra (Avanafil)

- Zydena (Udenafil)

- Vitaros / Alprostadil

- Others

- By Drug Class

- PDE5 Inhibitors

- Prostaglandin Analogues

- Centrally-acting Agents

- NO Donors / Novel MOA

- By Mode of Administration

- Oral Tablets / Capsules

- Oro-dispersible Films & Sublingual

- Topical & Transdermal

- Nasal Sprays

- Injectable / Intra-urethral

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies & DTC Platforms

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed practicing urologists, telehealth executives, bulk API suppliers, and pharmacy buying groups across North America, Europe, Asia, and Latin America. These discussions verified diagnosis trends, cash-pay shares, e-pharmacy mark-ups, and emerging nasal/topical adoption, letting us adjust secondary findings and reconcile regional anomalies.

Desk Research

We began by mapping supply and demand indicators from open sources such as the U.S. CDC's National Health Interview Survey, Eurostat aging statistics, WHO diabetes prevalence dashboards, and trade data from UN Comtrade that capture bulk tadalafil and sildenafil movements. Regulatory updates from the FDA Orange Book, EMA public assessment reports, and patent filings (Questel) helped us time generic waves and price resets. Company 10-Ks, investor decks, and leading urology journals supplied typical dosing patterns and average selling prices. The sources named above illustrate, not exhaust, the wider pool consulted.

Market-Sizing & Forecasting

A top-down epidemiology build, prevailing adult-male population × ED prevalence × treatment-seeking rate, yields the treated patient pool, which is then multiplied by weighted annual doses and ASPs. Select bottom-up checks, such as sample wholesaler sell-out and online prescription volumes, temper the totals. Key model variables include geriatric male population growth, diabetes incidence, generic penetration levels, telemedicine visit rates, and post-patent ASP erosion curves. We project 2025-2030 values through multivariate regression, anchoring on those drivers plus per-capita GDP. Scenario analysis captures regulatory or pipeline shocks. Data gaps in distributor splits are bridged using regional channel mixes drawn from primary interviews.

Data Validation & Update Cycle

Outputs pass variance checks against independent sales trackers and customs data before a senior analyst review. Models refresh every twelve months, with mid-cycle revisions triggered by major approvals, OTC switches, or price caps, ensuring clients receive the latest view.

How Mordor Intelligence's Erectile Dysfunction Drugs Market Size Compares to Other Published Estimates

Published estimates often vary; definitions, base years, and channel visibility rarely align.

We openly spell out inclusions, refresh annually, and convert currencies using the same IMF average, giving decision-makers a stable anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.84 B (2025) | Mordor Intelligence | - |

| USD 2.92 B (2024) | Global Consultancy A | excludes generics and Asia's telehealth sales |

| USD 3.88 B (2024) | Industry Association B | limited to oral PDE-5 tablets; uses list prices |

| USD 2.90 B (2024) | Regional Consultancy C | counts only seven core countries; biennial updates |

In sum, our disciplined scope choices, simultaneous top-down epidemiology and bottom-up validation, and continuous update cadence make Mordor Intelligence's baseline the dependable reference for strategic planning.

Key Questions Answered in the Report

What is the current size of the erectile dysfunction drugs market?

The market stood at USD 5.17 billion in 2026 and is forecast to reach USD 7.15 billion by 2031.

Which product holds the largest erectile dysfunction drugs market share?

Viagra retained 44.78% of revenue in 2025, maintaining its lead despite generic competition.

Why are digital pharmacies gaining traction in the erectile dysfunction drugs industry?

They combine teleconsultation, e-prescribing, and home delivery, offering discretion and lower pricing than many retail outlets.

Which region is growing fastest for erectile dysfunction medications?

Asia-Pacific is expanding at a 10.04% CAGR thanks to regulatory reform and rising healthcare access.

What new formulations are on the horizon?

Nasal sprays like SPONTAN and OTC topical gels such as Eroxon promise faster onset and fewer systemic effects.

Page last updated on: