Biological Seed Treatment Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

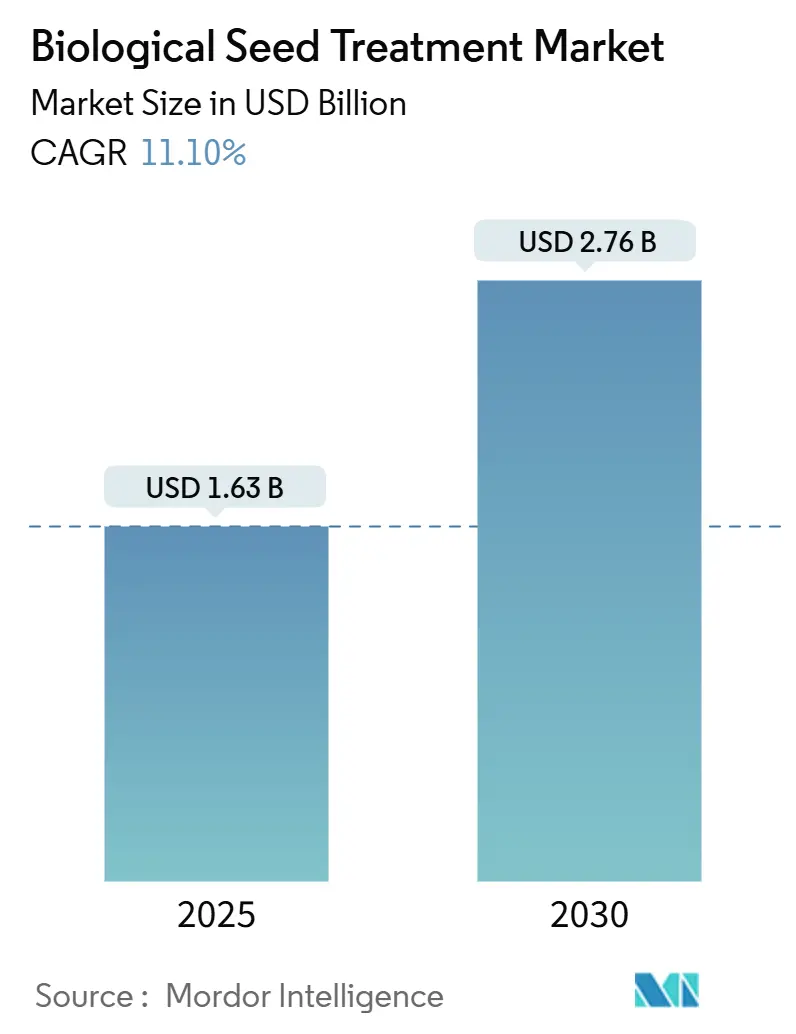

| Market Size (2025) | USD 1.63 Billion |

| Market Size (2030) | USD 2.76 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

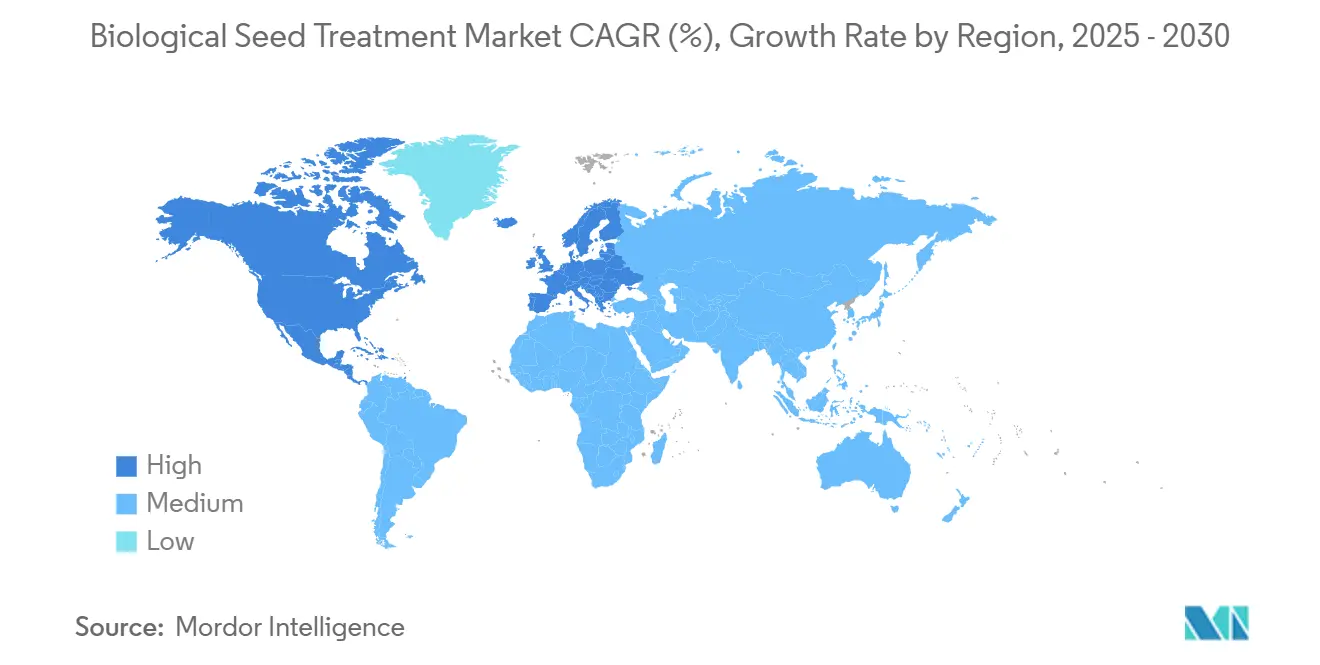

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

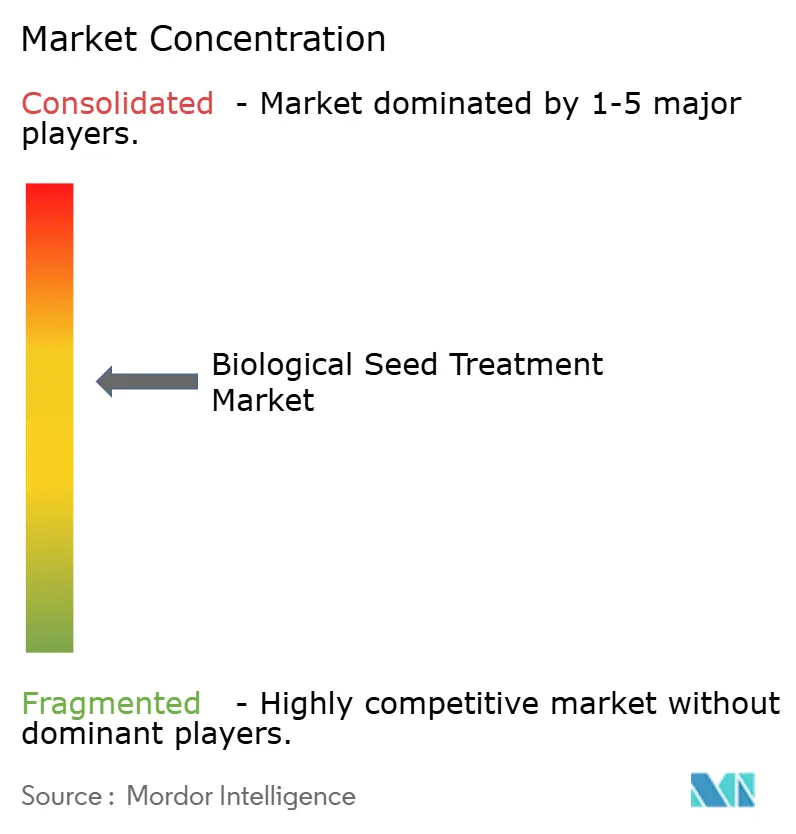

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biological Seed Treatment Market Analysis by Mordor Intelligence

The biological seed treatment market size stands at USD 1.63 billion in 2025 and is forecast to reach USD 2.76 billion by 2030, translating into an 11.1% CAGR for the period. This momentum is anchored in regulatory shifts that favor biological inputs, proven yield gains of up to 21%, and disease-control efficacy reaching 55% in controlled trials. In 2024, mandatory residue limits in controlled-environment agriculture, a EUR 1.6 billion (USD 1.7 billion) European biocontrol push, and rising investments in agricultural biotechnology in China and India further elevate demand [1]Source: European Commission Directorate-General for Health and Food Safety, “Sustainable Use of Pesticides Directive,” ec.europa.eu . . Competitive intensity is moderate; the top five companies hold a significant share, enabling innovators to capture emerging niches through nano-encapsulation and precision application technologies. The market is experiencing significant structural changes in its supply chain and distribution networks. Major agricultural input companies are establishing dedicated biological product divisions and investing in specialized production facilities. For instance, in May 2022, Corteva Agriscience opened a new Center for Seed Applied Technologies (CSAT) laboratory in South Africa, demonstrating the industry's commitment to regional expansion and technological advancement.

Key Report Takeaways

- By type, Microbial held 70.4% of the Biological seed treatment market share in 2024, while botanicals are predicted to grow at a 14.2% CAGR through 2030.

- By function, seed protection held 43.0% of the biological seed treatment market size in 2024, while Seed enhancement emerges as the fastest-growing segment at a 12.8% CAGR to 2030.

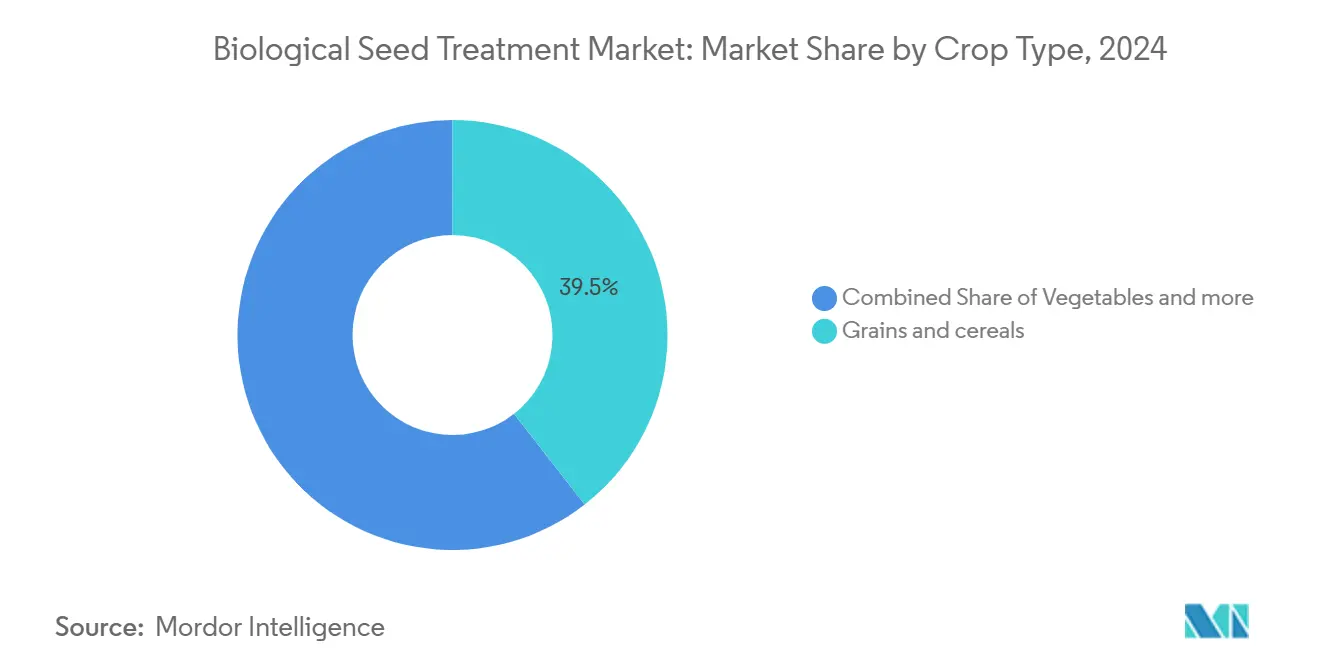

- By crop type, grains and cereals accounted for a 39.5% share of the biological seed treatment market size in 2024, and vegetables recorded the highest projected CAGR at 11.4% through 2030.

- By geography, North America led with 33.2% revenue share in 2024, whereas Asia-Pacific is forecast to post the fastest regional CAGR at 13.7% to 2030.

Global Biological Seed Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of organic and sustainable agriculture | +2.8% | North America and Europe lead, global relevance | Medium term (2-4 years) |

| Regulatory support and subsidies for bio-based inputs | +2.1% | North America, Europe, Brazil, India | Short term (≤ 2 years) |

| Higher yields and stress tolerance delivered by bio-priming | +1.9% | Asia-Pacific, South America, and global | Medium term (2-4 years) |

| Growing R& D investment from agro-biotech firms | +1.7% | North America, Europe, and China | Long term (≥ 4 years) |

| Expansion of controlled-environment agriculture requiring residue-free seeds | +1.4% | North America, Europe, Japan, and Singapore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Organic and Sustainable Agriculture

Consumer demand for residue-free produce is compelling growers to integrate biological seed treatments into their production systems, particularly as organic farmland reached 98.9 million hectares globally in 2024 [2]Food and Agriculture Organization Statistics Division, “Organic Agriculture Statistics 2024,” fao.org. . The European Union's Farm to Fork strategy mandates 25% organic farming by 2030, creating regulatory pressure that extends beyond certified organic operations to conventional growers seeking reduced chemical residue profiles. Controlled environment agriculture operations, valued at USD 5.6 billion in 2023 and projected to reach USD 24 billion by 2030, specifically require pathogen-free seed inputs that biological treatments uniquely provide. The trend accelerates as major food retailers implement zero-residue procurement standards, forcing supply chain compliance upstream to seed treatment selection.

Regulatory Support and Subsidies for Bio-Based Inputs

Government frameworks increasingly favor biological inputs through fast-track approval pathways and financial incentives that reduce market entry barriers for innovative formulations. Brazil's biopesticide registration program achieved 67 new biological product approvals in 2024, compared to 23 synthetic approvals, reflecting policy priorities that biological companies can leverage for rapid market penetration. India's new biopesticide policy reduces registration timelines from 36 months to 18 months while providing 50% fee reductions for biological products, creating competitive advantages for companies with robust regulatory capabilities. These policy shifts create first-mover advantages for companies that can navigate accelerated approval processes while building market presence ahead of synthetic competitors.

Higher Yields and Stress Tolerance Delivered by Bio-Priming

Scientific validation of biological seed treatment efficacy is converting skeptical growers, as peer-reviewed research demonstrates consistent yield improvements under abiotic stress conditions that are becoming more frequent due to climate variability. In 2022, a meta-analysis of 127 field trials published in Nature Plants showed that biological seed treatments increased crop yields by an average of 21% under drought stress and 18% under salinity stress, with effects most pronounced in vegetables and legumes. The mechanism involves defense priming, where beneficial microorganisms enhance plant immune responses and nutrient uptake efficiency, creating a measurable return on investment that justifies premium pricing. This performance data is particularly compelling in Asia-Pacific markets where smallholder farmers operate on thin margins and require demonstrable economic benefits to justify input cost increases.

Growing R&D Investment from Agro-Biotech Firms

Major agricultural companies are channeling unprecedented resources into biological innovation as they recognize the technology platform's potential to capture higher-margin market segments while addressing regulatory constraints on synthetic chemistry. BASF committed EUR 900 million (USD 970 million) to agricultural solutions R&D in 2023, with 40% allocated to biological product development, including fermentation capacity expansion and microbial strain optimization. Corteva increased biological R&D spending by 35% year-over-year in 2024, focusing on seed-applied biologicals that integrate with their germplasm portfolio to create differentiated value propositions. The R&D intensity reflects industry recognition that biological platforms offer sustainable competitive advantages through proprietary strain libraries and application technologies that are difficult to replicate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs versus synthetic treatments | -1.8% | Emerging markets most affected | Short term (≤ 2 years) |

| Stringent and slow regulatory approval timelines | -1.4% | Europe, North America | Medium term (2-4 years) |

| Cold-chain gaps in emerging markets are limiting microbial viability | -1.1% | Africa, rural Asia-Pacific, South America | Medium term (2-4 years) |

| Farmer skepticism due to inconsistent field performance under abiotic stress | -0.9% | Global smallholder regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production Costs Versus Synthetic Treatments

Manufacturing complexity and specialized infrastructure requirements create cost structures that price biological seed treatments 20-30% above synthetic alternatives, limiting adoption among price-sensitive grower segments that represent the majority of global agricultural production. Fermentation-based production requires sterile facilities, quality control systems, and cold-chain logistics that synthetic chemistry manufacturers avoid, creating inherent cost disadvantages that biological companies struggle to overcome through scale economies. Smallholder farmers in developing markets, who cultivate 80% of global farmland, often cannot justify the premium pricing despite demonstrated yield benefits, particularly when synthetic alternatives provide adequate pest control at lower input costs. The cost differential is most pronounced in commodity crops like grains and oilseeds, where thin profit margins make input cost optimization critical for farm profitability.

Stringent and Slow Regulatory Approval Timelines

Regulatory frameworks designed for chemical pesticides create approval bottlenecks that delay biological product launches by 7-10 years in Europe compared to 2-3 years in Brazil, giving synthetic competitors time advantages that biological companies cannot easily overcome. The European Food Safety Authority requires extensive toxicology studies for biological products despite their inherently lower risk profiles, creating regulatory costs that can exceed USD 10 million per active ingredient. This regulatory burden disproportionately affects smaller biological companies that lack the resources to navigate complex approval processes, consolidating market opportunities among large agricultural corporations with established regulatory capabilities. The approval timeline disparity between regions creates strategic challenges for global product launches, as companies must sequence market entry based on regulatory efficiency rather than commercial opportunity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Microbials Lead While Botanicals Accelerate

Microbial held 70.4% of the Biologicals seed treatment market share in 2024, driven by accelerated regulatory approvals and consumer preference for plant-based inputs. The microbial segment's dominance stems from decades of research validating beneficial bacteria and fungi for crop protection and enhancement, with companies like Novozymes and BASF leveraging proprietary strain libraries that create sustainable competitive advantages. Regulatory agencies exhibit greater comfort with microbial registrations due to extensive safety databases and established risk assessment protocols, enabling faster market entry compared to novel botanical extracts that require more comprehensive toxicology studies.

Botanicals are predicted to grow at a 14.2% CAGR through 2030, through regulatory frameworks that favor plant-derived active ingredients over synthetic chemistry, particularly in organic agriculture, where botanical seed treatments meet certification requirements without compromising efficacy. The segment benefits from consumer perception advantages and simplified regulatory pathways in key markets like the European Union, where botanical pesticides receive expedited review under the low-risk active substance category.

By Function: Protection Dominance Drives Enhancement Innovation

Seed protection commands the largest 43.0% market share in 2024, reflecting grower prioritization of disease and pest control over enhancement benefits. The protection segment's dominance stems from regulatory frameworks that favor biological fungicides and insecticides over synthetic alternatives, particularly in European markets where chemical restrictions create market opportunities for biological solutions. Companies like BASF leverage this regulatory tailwind through products like Poncho/VOTiVO, which combine biological and synthetic active ingredients to deliver comprehensive protection while meeting residue requirements.

Seed enhancement emerges as the fastest-growing segment at 12.8% CAGR through 2030 as multi-functional formulations gain traction. Seed enhancement represents the innovation frontier where companies integrate plant growth promotion, stress tolerance, and nutrient efficiency into single formulations that command premium pricing. The functional segmentation reflects evolving grower preferences toward integrated solutions that address multiple production challenges simultaneously, driving convergence between protection and enhancement technologies. Nano-encapsulation advances enable combination products that release different active ingredients at optimal timing during crop development, creating differentiated value propositions that justify premium pricing.

By Crop Type: Grains Anchor Growth While Vegetables Drive Innovation

Grains and cereals dominate with a 39.5% market size in 2024, leveraging large cultivation areas and established seed treatment adoption patterns. The grains segment benefits from mechanized application systems and bulk purchasing power that reduce per-unit costs, making biological treatments economically viable despite premium pricing over synthetic alternatives. Major grain producers like Cargill and ADM increasingly specify biological seed treatments in their supply chain requirements to meet zero-residue procurement standards from food manufacturers and retailers[3]Source: Cargill Incorporated, “Sustainability Report 2024,” cargill.com ..

Vegetables emerge as the fastest-growing segment at 11.4% CAGR through 2030, driven by premium pricing tolerance and controlled environment agriculture requirements. Vegetables command premium pricing that offsets biological treatment costs while requiring pathogen-free inputs for greenhouse and hydroponic production systems that cannot tolerate chemical residues. The segment's growth acceleration reflects expansion in controlled environment agriculture, where biological seed treatments are mandatory rather than optional inputs due to system contamination risks.

Geography Analysis

North America holds the largest 33.2% market share in 2024 through advanced seed treatment infrastructure and regulatory frameworks that favor biological inputs. The North American market benefits from established distribution networks, technical support systems, and grower familiarity with biological products that reduce adoption barriers compared to emerging markets. Major seed companies like Corteva and Bayer leverage their North American presence to launch biological innovations before expanding globally, creating first-mover advantages in key crop segments.

Asia-Pacific emerges as the fastest-growing region at 13.7% CAGR through 2030, driven by policy liberalization in China and India that reduces regulatory barriers while expanding market access for biological companies. The Asia-Pacific region represents a dynamic market for biological seed treatments, characterized by diverse agricultural systems and varying levels of technology adoption. The region encompasses major agricultural economies, including China, Japan, India, Thailand, Vietnam, and Australia. Each country presents unique opportunities and challenges for biological seed treatment adoption, influenced by factors such as farming practices, regulatory frameworks, and environmental conditions. The region's increasing focus on sustainable agriculture and growing awareness about environmental protection has created favorable conditions for market expansion.

Europe stands as a crucial market for biological seed treatments, driven by stringent regulations on chemical pesticides and a strong emphasis on sustainable agriculture. The region encompasses diverse markets, including Spain, the United Kingdom, France, Germany, Russia, and Italy, each with unique agricultural needs and adoption patterns. The European Union's policies promoting organic farming and sustainable agriculture have created a favorable environment for biological seed treatment solutions. The region's strong focus on research and development, coupled with increasing consumer demand for organic products, has fostered innovation in biological seed treatment technologies.

Competitive Landscape

The biological seed treatment market exhibits moderate concentration, with the top players including BASF SE, Bayer AG, Syngenta AG, Corteva Agriscience, and Novozymes. These players are creating opportunities for specialized biological companies to capture white-space segments through innovative formulations and targeted crop applications. The competitive landscape favors companies with proprietary microbial strain libraries, regulatory expertise, and global distribution networks that can navigate complex approval processes while scaling production efficiently. Emerging disruptors like Indigo Ag deploy digital-biological platforms that integrate seed treatment with precision agriculture systems, creating differentiated value propositions that established players struggle to replicate quickly.

Technology convergence around nano-encapsulation, precision application systems, and multi-functional formulations is reshaping competitive dynamics as companies invest in R&D capabilities that enable sustainable differentiation. Patent analysis reveals increasing focus on controlled-release mechanisms and microbial strain optimization, with companies filing 340% more biological seed treatment patents in 2024 compared to 2020, indicating intensifying innovation competition.

Opportunities exist in specialized crop segments, emerging markets with inadequate cold-chain infrastructure, and controlled environment agriculture applications where biological treatments command premium pricing without direct synthetic competition. The competitive intensity reflects industry recognition that biological platforms offer sustainable advantages through proprietary technologies and regulatory positioning that create barriers to entry for new competitors while enabling market share capture from synthetic alternatives.

Biological Seed Treatment Industry Leaders

BASF SE

Bayer AG

Syngenta AG

Corteva Agriscience

Novozymes A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Locus Agriculture expanded its Rhizolizer Duo product line with the introduction of six new biological treatments. The latest additions encompass three in-furrow biologicals tailored for corn, cotton, and legumes, alongside three seed treatments designed for wheat and cereals, soybeans, and corn. These innovations cater to the dynamic requirements of row crop farmers, seed treatment firms, and agricultural retailers and distributors.

- December 2023: Syngenta Seedcare has enhanced its focus on biologicals and expanded its leadership in seed treatment by opening its first biologicals service center at The Seedcare Institute in Maintal, Germany. This center, equipped with state-of-the-art technologies, meets the increasing demand from farmers across the European Union for biological seed treatment solutions, providing exceptional service and application support for its customers.

- December 2023: DPH Biologicals has unveiled BellaTrove Companion Maxx ST, a multi-action fungicide seed treatment designed to bolster seedlings against pathogens and promote robust root systems. BellaTrove Companion Maxx ST is crafted from DPH Biologicals' exclusive strain of a plant-stimulating rhizobacterium. This EPA-registered and OMRI-certified biofungicide and bactericide not only enhances a plant's innate defenses against pathogens but also boosts nutrient absorption and root vitality.

Global Biological Seed Treatment Market Report Scope

Biological seed treatments include active ingredients such as microbes (fungi and bacteria), plant extracts, and algae extracts. These treatments are applied to seeds in either powder or liquid form before planting. The Biological Seed Treatment Market is segmented by Function (Seed Protection, Seed Enhancement, and Other Functions), Crop Type (Grains and Cereal, Oil Seeds, Vegetables, and Other Crop Types), Geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers market size and forecasts in terms of value (USD) for all the above segments.

| Microbial |

| Botanicals |

| Others (biofermentation products and natural polymers & derivatives) |

| Seed Protection |

| Seed Enhancement |

| Other Functions |

| Grains and Cereal |

| Oil Seeds |

| Vegetables |

| Other Crop Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Spain |

| United Kingdom | |

| France | |

| Germany | |

| Russia | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa |

| Type | Microbial | |

| Botanicals | ||

| Others (biofermentation products and natural polymers & derivatives) | ||

| Function | Seed Protection | |

| Seed Enhancement | ||

| Other Functions | ||

| Crop Type | Grains and Cereal | |

| Oil Seeds | ||

| Vegetables | ||

| Other Crop Types | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Spain | |

| United Kingdom | ||

| France | ||

| Germany | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the biological seed treatment market expected to grow to 2030?

It is projected to post an 11.1% CAGR, rising from USD 1.63 billion in 2025 to USD 2.76 billion in 2030.

Which region leads the current demand for biological seed treatments?

North America holds the largest share at 33.2% owing to advanced infrastructure and favorable EPA(Environmental Protection Agency) approvals.

Which segment is expanding the quickest within the market?

Seed enhancement functions are forecast to grow at a 12.8% CAGR as growers adopt multi-benefit formulations.

Why are vegetables a high-growth crop category for biological treatments?

Greenhouse and hydroponic systems demand residue-free seeds, and premium pricing offsets higher input costs, driving an 11.4% CAGR.

What technological trend is helping biological products reach new markets?

Nano-encapsulation extends shelf life to 18-24 months under ambient temperatures, reducing cold-chain dependence and logistics costs.

Page last updated on: