Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

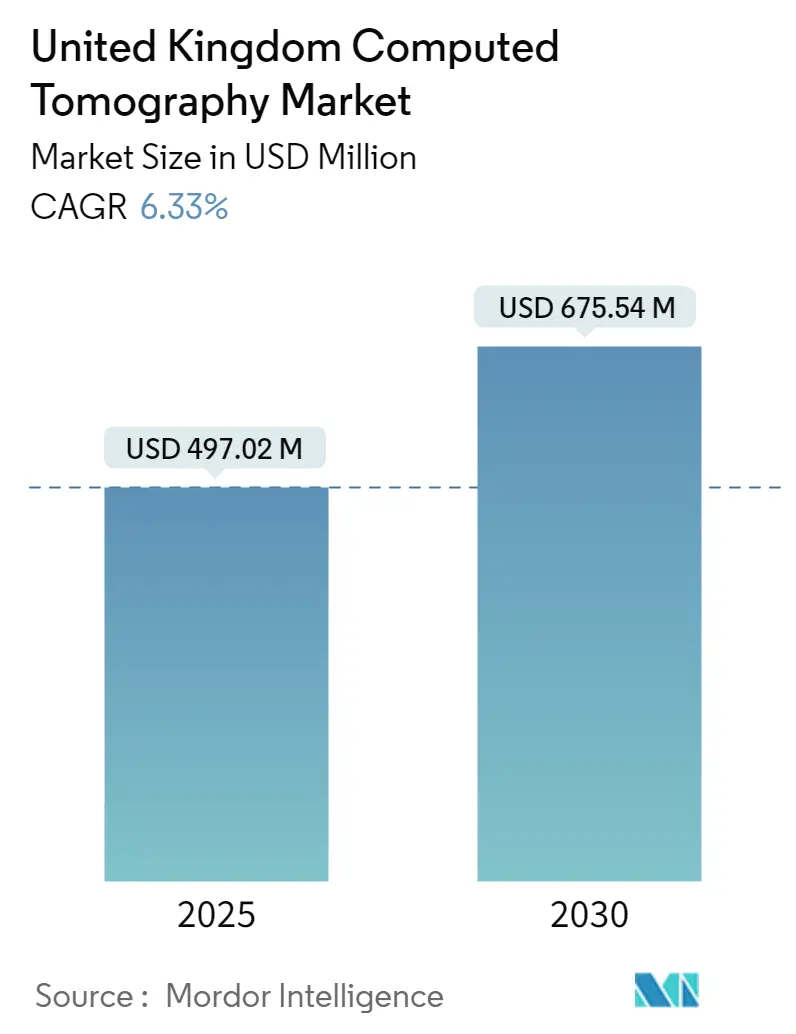

| Market Size (2025) | USD 497.02 Million |

| Market Size (2030) | USD 675.54 Million |

| Growth Rate (2025 - 2030) | 6.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Computed Tomography Market Analysis by Mordor Intelligence

The United Kingdom Computed Tomography Market size is estimated at USD 497.02 million in 2025, and is expected to reach USD 675.54 million by 2030, at a CAGR of 6.33% during the forecast period (2025-2030).

The United Kingdom's computed tomography landscape is undergoing significant transformation driven by substantial healthcare infrastructure investments and technological advancement. The UK government has demonstrated a strong commitment to expanding diagnostic imaging capabilities through major funding initiatives, including a landmark EUR 350 million pledge in October 2021 to establish 40 new "one-stop-shops" for checks, scans, and tests. This investment strategy aims to address NHS care backlogs and enhance accessibility to advanced imaging services. The infrastructure expansion continued with an additional EUR 250 million allocation to NHS trusts in November 2021, earmarked for establishing over 100 diagnostic centers across England over three years, representing a substantial boost to the country's medical imaging capabilities.

Technological innovation is reshaping the computed tomography landscape, with manufacturers introducing increasingly sophisticated systems. Recent developments include the launch of Siemens Healthineers' Somatom X.ceed, featuring advanced imaging capabilities and automated user guidance through myExam Companion. Canon Medical's introduction of CT-in-a-box represents another significant innovation, offering mobile and ready-to-use CT solutions that enhance flexibility in healthcare delivery. These technological advancements are particularly crucial given that the United Kingdom currently maintains approximately 9 CT scanners per 1,000,000 inhabitants, according to OECD data.

The market is experiencing a shift toward more integrated and efficient medical diagnostic imaging solutions, with a growing emphasis on artificial intelligence and automation. Healthcare providers are increasingly adopting systems that offer enhanced image quality while reducing radiation exposure and scan times. This evolution is particularly significant in addressing the rising demand for cancer diagnostics, with projections indicating cancer cases in the UK will reach 595,909 by 2040, necessitating more efficient and accurate diagnostic capabilities.

The industry is witnessing a trend toward more specialized and application-specific computed tomography solutions, particularly in cardiac imaging and emergency care settings. Healthcare facilities are increasingly investing in systems that offer versatility across different clinical applications while maintaining high image quality and patient safety standards. This trend is supported by the growing adoption of spectral CT technology and photon-counting detectors, which enable more detailed tissue characterization and reduced radiation doses, marking a significant advancement in healthcare imaging capabilities.

United Kingdom Computed Tomography Market Trends and Insights

Rising Prevalence of Cancer and Enhanced Healthcare Infrastructure

The increasing burden of cancer cases in the United Kingdom has become a significant driver for the computed tomography market, supported by substantial government initiatives to enhance diagnostic capabilities. According to GLOBOCAN 2020 data, the country recorded 56,780 cases of prostate cancer and 53,889 cases of breast cancer, highlighting the critical need for advanced medical imaging solutions. The government's commitment to improving cancer diagnosis is evident through its October 2021 initiative of investing EUR 350 million to establish 40 new diagnostic centers, designed as "one-stop-shops for checks, scans, and tests" across England.

The expansion of healthcare infrastructure through strategic partnerships and equipment deployment has further strengthened the market's growth trajectory. This is exemplified by Canon Medical System UK's deployment of 15 relocatable CT scanners to NHS trusts nationwide, significantly improving accessibility to advanced diagnostic services. Additionally, the establishment of new CT facilities, such as the installation of cutting-edge scanners at Surrey and Sussex Healthcare NHS Trust, which performs approximately 1,000 CT scans monthly, demonstrates the growing infrastructure support for diagnostic imaging services.

Understand The Key Trends Shaping This Market

Download PDF

Technological Advancements and Research Investment

The United Kingdom's computed tomography market is experiencing significant momentum driven by continuous technological innovations and substantial research investments. The launch of advanced imaging solutions, such as HeartFlow technology as part of the NHS England initiative, has revolutionized diagnostic capabilities by enabling the conversion of CT scans into detailed 3D images, allowing for faster and more accurate diagnosis within 20 minutes. This technological progression is further supported by the establishment of Digital Pathology and Imaging Artificial Intelligence Centres of Excellence, which received a USD 50 million funding boost to develop cutting-edge digital diagnostic tools.

The commitment to research and development is evident through various collaborative initiatives and partnerships. For instance, the British Institute of Radiology, in partnership with Siemens Healthineers, introduced the BIR/Siemens Healthineers Research Award, providing GBP 1,000 for initial research support in fields including nuclear medicine, radiology, and medical physics. Furthermore, the National Research Facility's investment in lab-based X-ray Computed Tomography, involving collaborations between multiple universities including Manchester, Southampton, and University College London, demonstrates the strong focus on advancing CT technology through research excellence.

Growing Burden of Chronic Diseases and Aging Population

The increasing prevalence of chronic diseases, particularly cardiovascular conditions and musculoskeletal disorders, has emerged as a crucial driver for the medical imaging market. According to the British Heart Foundation, approximately 7.4 million people were living with heart and circulatory diseases in the United Kingdom, with hospital admissions reaching 1,170,206 cases in recent years. This significant patient population requires regular diagnostic imaging, creating sustained demand for CT scanning services across healthcare facilities.

The aging demographic profile of the United Kingdom further amplifies the market growth potential. Population projections indicate that the number of individuals aged 65 years and older is expected to increase from 12.49 million to 15.16 million by 2030. This demographic shift is particularly significant as the elderly population is more susceptible to various chronic conditions, including orthopedic disorders. For instance, research from Arthritis Research UK reveals that approximately one in five adults over 45 years in England experiences knee osteoarthritis, while one in nine adults suffers from hip osteoarthritis, necessitating regular diagnostic imaging for monitoring and treatment planning. The demand for medical diagnostic equipment, including cardiac CT, is expected to rise as a result.

Segment Analysis: By Type

Medium Slice Segment in UK Computed Tomography Market

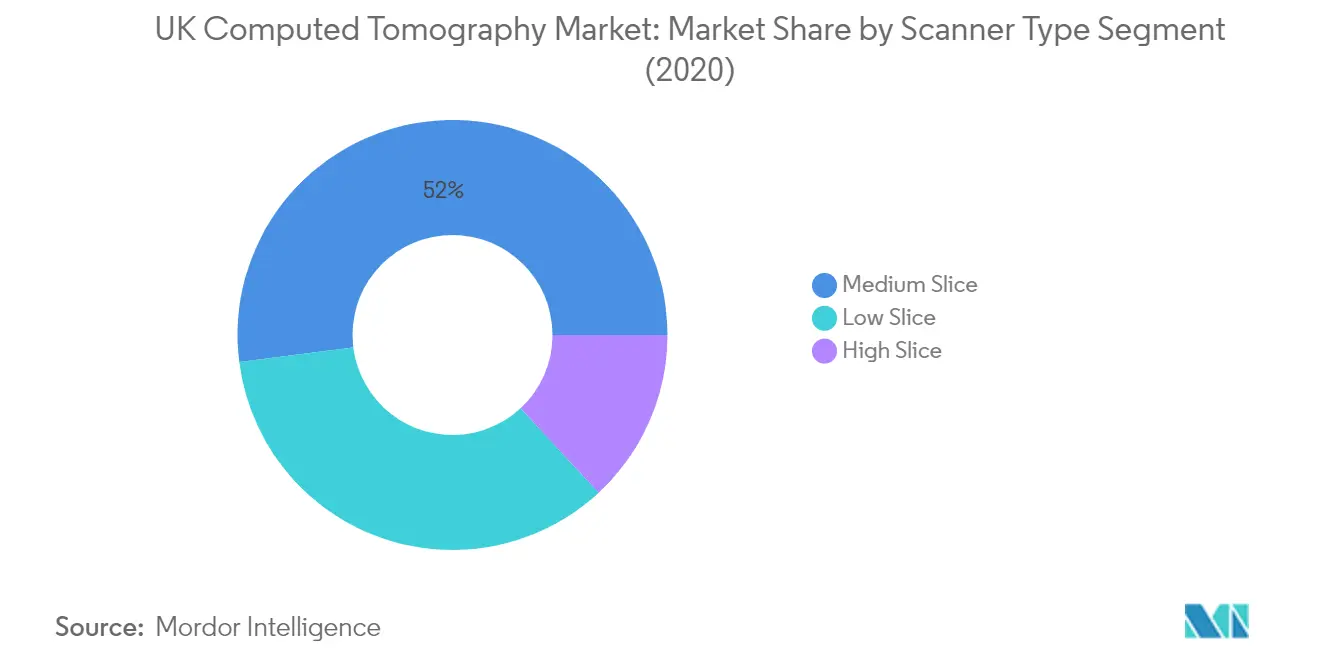

The medium slice segment, which includes 32-slice and 64-slice CT scanners, dominates the United Kingdom computed tomography market with approximately 52% market share. These systems are particularly valued for their superior imaging capabilities in visualizing soft tissue structures, tumors, cysts, and diseases across various organs, including the liver, lungs, and coronary arteries. The 64-slice CT scanners are especially notable for their ability to produce detailed cross-sectional images as thin as half a millimeter, providing physicians with highly accurate diagnostic information. The segment's leadership position is reinforced by continuous technological advancements, such as Siemens Healthineers' introduction of Somatom X.ceed, which features automated user guidance through diagnostic procedures. Additionally, the increasing installation of these systems in major healthcare facilities across the UK, coupled with their optimal balance of speed, precision, and cost-effectiveness, continues to drive their widespread adoption in both routine diagnostics and specialized medical procedures.

High Slice Segment in UK Computed Tomography Market

The high slice segment, encompassing CT scanners with more than 128 slices, including 256, 320, and 640 slice variants, demonstrates significant growth potential in the UK market. These advanced systems offer notable advantages, including reduced scan time, increased patient throughput, and lower radiation doses, while providing more detailed images with fewer artifacts. The segment's growth is particularly driven by its effectiveness in specialized applications such as cardiovascular examinations, where the faster scanning speed and larger imaging area prove beneficial for patients with arrhythmias, rapid heart rates, and obesity. The increasing demand for these high-end systems is further supported by their superior capabilities in handling pediatric patients and complex diagnostic procedures, making them essential for advanced healthcare facilities aiming to provide cutting-edge diagnostic imaging services.

Remaining Segments in CT Scanner Types

The low slice segment, comprising 4 and 16 slice CT scanners, continues to maintain its presence in the UK computed tomography market, particularly in facilities where basic diagnostic capabilities are sufficient. While 4 to 8 slice scanners are gradually being phased out, 16-slice CT scanners remain relevant, especially in urgent care centers and smaller hospitals where they effectively meet routine imaging needs. These systems offer a practical solution for healthcare facilities with moderate patient volumes and standard diagnostic requirements, providing reliable performance for everyday scanning procedures while being more cost-effective compared to their higher-slice counterparts.

Segment Analysis: By Application

Oncology Segment in UK Computed Tomography Market

The oncology segment dominates the UK computed tomography market, holding approximately 30% of the total market share in 2024. This significant market position is driven by the increasing prevalence of various types of cancer in the United Kingdom and the critical role of CT imaging in cancer diagnosis, treatment planning, and monitoring. The segment's leadership is further strengthened by continuous technological advancements in CT imaging capabilities that enable more precise tumor detection and characterization. The rising adoption of advanced CT scanning protocols for cancer screening programs, particularly in breast, lung, and colorectal cancers, has also contributed to the segment's dominant position. Additionally, the integration of artificial intelligence and machine learning algorithms in oncological CT imaging has enhanced diagnostic accuracy and improved workflow efficiency, making it an indispensable tool in cancer care pathways across the UK healthcare system.

Cardiovascular Segment in UK Computed Tomography Market

The cardiovascular segment is projected to experience the fastest growth in the UK computed tomography market during 2024-2029, with an expected growth rate of approximately 7%. This accelerated growth is primarily attributed to the increasing adoption of cardiac CT for non-invasive coronary artery disease assessment and the rising prevalence of cardiovascular conditions in the UK population. The segment's growth is further fueled by technological innovations in cardiac CT imaging, including improved temporal resolution and reduced radiation exposure. The integration of advanced visualization tools and AI-powered analysis software has enhanced the diagnostic capabilities of cardiovascular CT, making it an increasingly preferred choice for cardiac imaging. Moreover, the expansion of cardiac CT services across NHS trusts and private healthcare facilities, coupled with growing awareness about early cardiovascular disease detection, continues to drive the segment's rapid growth in the UK market.

Remaining Segments in UK CT Market by Application

The other significant segments in the UK computed tomography market include neurology, musculoskeletal, and other applications. The neurology segment plays a crucial role in diagnosing various neurological conditions, brain injuries, and stroke cases, benefiting from advanced CT perfusion imaging techniques. The musculoskeletal segment continues to be essential in orthopedic imaging, trauma cases, and surgical planning, particularly with the growing elderly population requiring orthopedic care. The other applications segment encompasses various clinical applications, including dental CT, pulmonary, and emergency medicine, contributing to the overall market growth through diverse use cases and expanding applications of CT technology in different medical specialties.

Segment Analysis: By End User

Hospitals Segment in UK Computed Tomography Market

The hospitals segment continues to dominate the United Kingdom computed tomography market, accounting for approximately 54% of the total market share in 2024. This significant market share is attributed to the increasing installation of CT scanners in hospitals across the UK, driven by the growing burden of chronic diseases and an aging population. The segment's dominance is further strengthened by technological advances in CT systems that have enhanced workflow efficiency in hospitals, along with the implementation of mobile and ready-to-use CT solutions that provide flexibility in patient care. Additionally, the increasing number of hospitals in the United Kingdom, coupled with substantial investments in healthcare infrastructure and the rising adoption of advanced medical imaging technologies, has contributed to the segment's leading position. The presence of well-established healthcare systems and favorable reimbursement policies has also played a crucial role in maintaining hospitals as the primary end-users of CT systems.

Diagnostic Centers Segment in UK Computed Tomography Market

The diagnostic centers segment is experiencing robust growth in the UK computed tomography market, with an expected growth rate of approximately 6% during 2024-2029. This growth is primarily driven by the increasing establishment of specialized diagnostic facilities and imaging centers across the country. The segment's expansion is supported by government initiatives to reduce waiting times for diagnostic imaging procedures and improve accessibility to advanced imaging services. The trend towards standalone diagnostic centers offering specialized imaging services, coupled with strategic partnerships between diagnostic center operators and medical imaging equipment manufacturers, is further accelerating segment growth. Additionally, the focus on providing cost-effective diagnostic solutions and the increasing preference for outpatient imaging services has positioned diagnostic centers as an attractive alternative to hospital-based imaging services.

Remaining Segments in End User Market

The other end users segment, which includes ambulatory surgery centers, research institutes, nursing homes, and specialty clinics, plays a vital role in the UK computed tomography market. These facilities are increasingly adopting CT imaging technologies to provide specialized care and support research activities. Ambulatory surgery centers are particularly notable for their growing adoption of CT systems to support minimally invasive procedures, while research institutes contribute significantly to advancing CT imaging technologies through clinical studies and validation of new applications. Nursing homes and specialty clinics are also incorporating CT imaging capabilities to provide comprehensive diagnostic services to their specific patient populations, thereby enhancing the overall accessibility of CT imaging services across different healthcare settings.

Competitive Landscape

Top Companies in United Kingdom Computed Tomography Market

The United Kingdom computed tomography market features prominent players like GE Healthcare, Siemens Healthineers, Philips Healthcare, Canon Medical Systems, and Fujifilm Holdings Corporation leading the competitive landscape. These companies are heavily investing in research and development to advance their CT imaging technologies, particularly focusing on artificial intelligence integration and deep learning reconstruction capabilities. Strategic partnerships with healthcare providers and research institutions have become increasingly common to enhance product development and market penetration. Companies are also emphasizing operational efficiency through digital solutions and improved workflow management systems. The market has witnessed significant product launches featuring advanced technologies like spectral imaging and reduced radiation exposure, while companies are expanding their service networks through both direct presence and distributor partnerships across the United Kingdom.

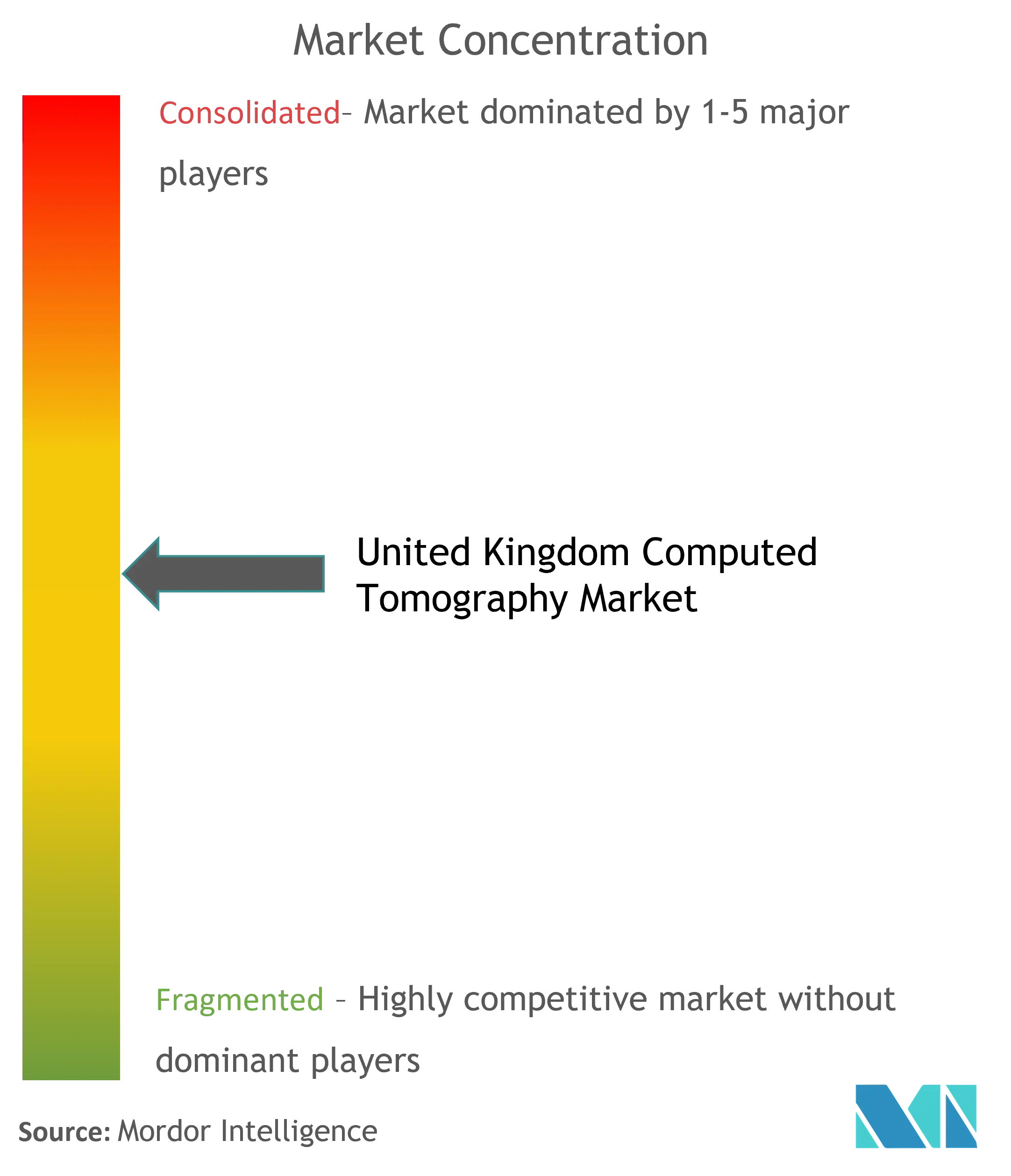

Consolidated Market with Strong Global Players

The United Kingdom medical imaging market is characterized by the strong presence of large multinational medical technology conglomerates that leverage their extensive research capabilities and established healthcare relationships. These global players have built comprehensive portfolios through decades of technological innovation and strategic acquisitions, making it challenging for new entrants to gain significant market share. The market structure shows high consolidation, with the top players controlling a substantial portion of the market through their established distribution networks and long-term partnerships with major healthcare institutions.

The market has witnessed several strategic mergers and acquisitions aimed at expanding technological capabilities and strengthening market position. Companies are increasingly focusing on acquiring specialized imaging technology firms to enhance their artificial intelligence and advanced visualization capabilities. Local distribution partnerships play a crucial role in market penetration strategies, with global players establishing strong relationships with regional healthcare providers and imaging centers. The competitive dynamics are further shaped by the National Health Service's procurement policies and requirements, influencing companies' market approach and product development strategies.

Innovation and Service Excellence Drive Success

For established players to maintain and expand their market share, a focus on technological innovation and comprehensive service offerings has become crucial. Companies are investing in developing integrated solutions that combine advanced medical imaging equipment capabilities with data analytics and artificial intelligence. The ability to provide end-to-end solutions, including equipment maintenance, staff training, and workflow optimization, has become a key differentiator. Market leaders are also emphasizing the development of specialized applications for different medical specialties and creating value through improved clinical outcomes and operational efficiency.

New entrants and challenger brands need to focus on identifying specific market niches and developing innovative solutions that address unmet needs in the computed tomography space. Success factors include building strong relationships with healthcare providers, offering competitive pricing models, and providing excellent after-sales support. The regulatory environment, particularly regarding radiation safety and image quality standards, continues to influence product development and market entry strategies. Companies must also consider the increasing emphasis on value-based healthcare and the growing importance of integrated diagnostic imaging solutions in their strategic planning.

United Kingdom Computed Tomography Industry Leaders

Canon Medical Systems Corporation (Toshiba Corporation)

Koning corporation

GE Healthcare

Planmeca Group (Planmed OY)

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- In April 2022, a new EUR 1.3m CT scanner was installed at North Tyneside Hospital with the funding of EUR 350 million from the Department of Health and Social Care (DHSC).

- In October 2021, at Surrey and Sussex Healthcare NHS Trust, two new CT scanners were installed by Canon Medical Systems UK. They will increase the capability for outpatient imaging by completing 1000 CT scans each month.

United Kingdom Computed Tomography Market Report Scope

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images or scans of areas inside the body. It is also called computerized axial tomography (CAT) scanning, primarily used in cancer diagnosis. The United Kingdom Computed Tomography Market is segmented by Type (Low Slice, Medium Slice, and High Slice), Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), and End User (Hospitals, Diagnostic Centers, and Other End Users). The report offers the value (in USD million) for the above segments.

By Type

| Low Slice |

| Medium Slice |

| High Slice |

By Application

| Oncology |

| Neurology |

| Cardiovascular |

| Musculoskeletal |

| Other Applications |

By End User

| Hospitals |

| Diagnostic Centers |

| Other End Users |

| By Type | Low Slice |

| Medium Slice | |

| High Slice | |

| By Application | Oncology |

| Neurology | |

| Cardiovascular | |

| Musculoskeletal | |

| Other Applications | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Other End Users |

Key Questions Answered in the Report

How big is the United Kingdom Computed Tomography Market?

The United Kingdom Computed Tomography Market size is expected to reach USD 497.02 million in 2025 and grow at a CAGR of 6.33% to reach USD 675.54 million by 2030.

What is the current United Kingdom Computed Tomography Market size?

In 2025, the United Kingdom Computed Tomography Market size is expected to reach USD 497.02 million.

Who are the key players in United Kingdom Computed Tomography Market?

Canon Medical Systems Corporation (Toshiba Corporation), Koning corporation, GE Healthcare, Planmeca Group (Planmed OY) and Koninklijke Philips NV are the major companies operating in the United Kingdom Computed Tomography Market.

What years does this United Kingdom Computed Tomography Market cover, and what was the market size in 2024?

In 2024, the United Kingdom Computed Tomography Market size was estimated at USD 465.56 million. The report covers the United Kingdom Computed Tomography Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United Kingdom Computed Tomography Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: