Smart Gas Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.78 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Gas Meter Market Analysis by Mordor Intelligence

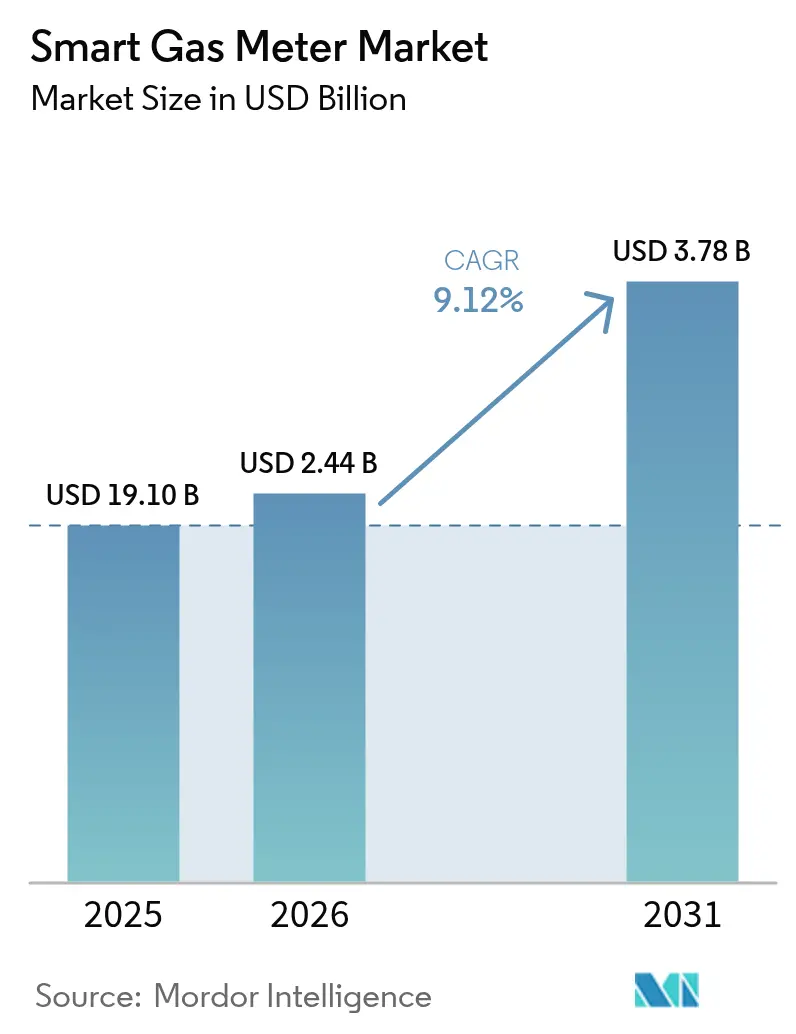

The Smart Gas Meter Market size was valued at USD 2.24 billion in 2025 and estimated to grow from USD 2.44 billion in 2026 to reach USD 3.78 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031). In terms of shipment volume, the market is expected to grow from 19.10 million units in 2025 to 27.70 million units by 2030, at a CAGR of 7.72% during the forecast period (2025-2030). This growth is propelled by mandatory meter-replacement programs, utilities’ cost-reduction targets, and safety regulations that mechanical meters cannot satisfy. The convergence of NB-IoT connectivity, hydrogen-ready measurement standards, and multi-fuel grid modernization has positioned the smart gas meters market as a critical infrastructure investment. Utilities are accelerating procurement despite semiconductor shortages, driven by firm compliance deadlines in Australia, Germany, and several US states. Suppliers capable of delivering hydrogen-ready ultrasonic meters and long-life batteries stand to benefit most as procurement cycles favor future-proof assets over the lowest upfront cost.

Key Report Takeaways

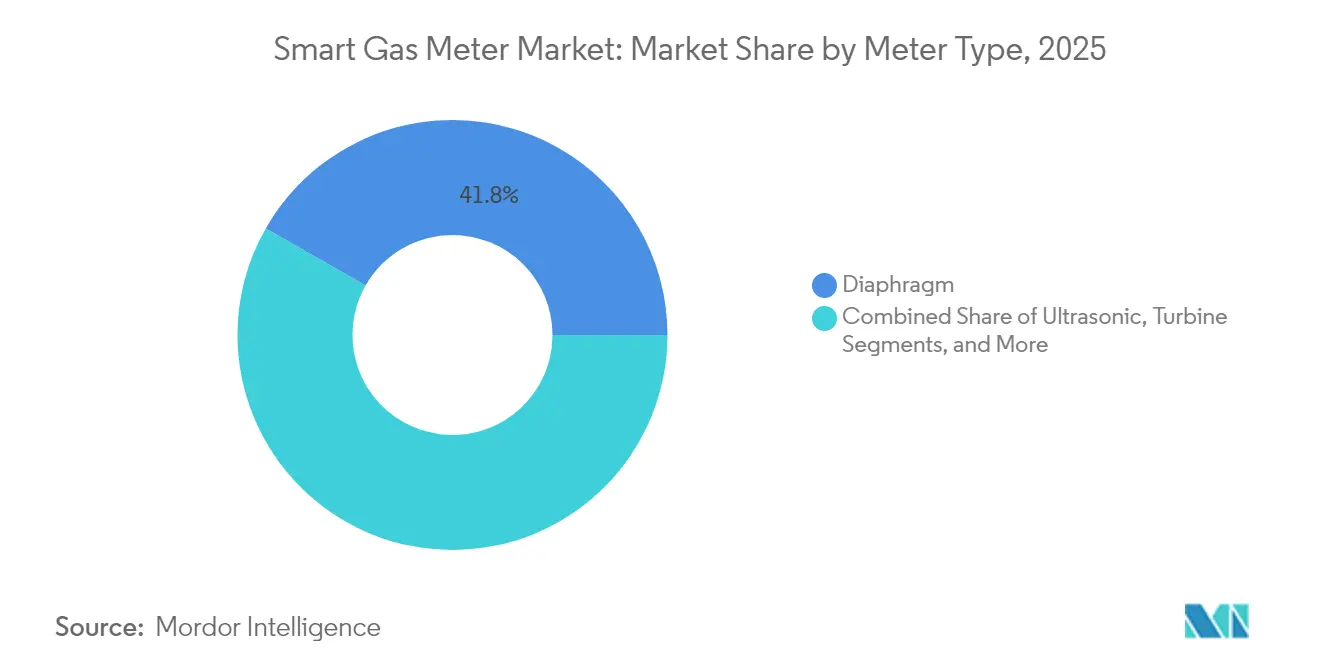

- By meter type, diaphragm meters led with 41.75% revenue share in 2025, while ultrasonic meters posted the highest projected CAGR at 12.1% through 2031.

- By communication technology, RF systems commanded 38.10% of the smart gas meters market share in 2025, whereas NB-IoT/LTE-M is forecast to expand at a 10.72% CAGR to 2031.

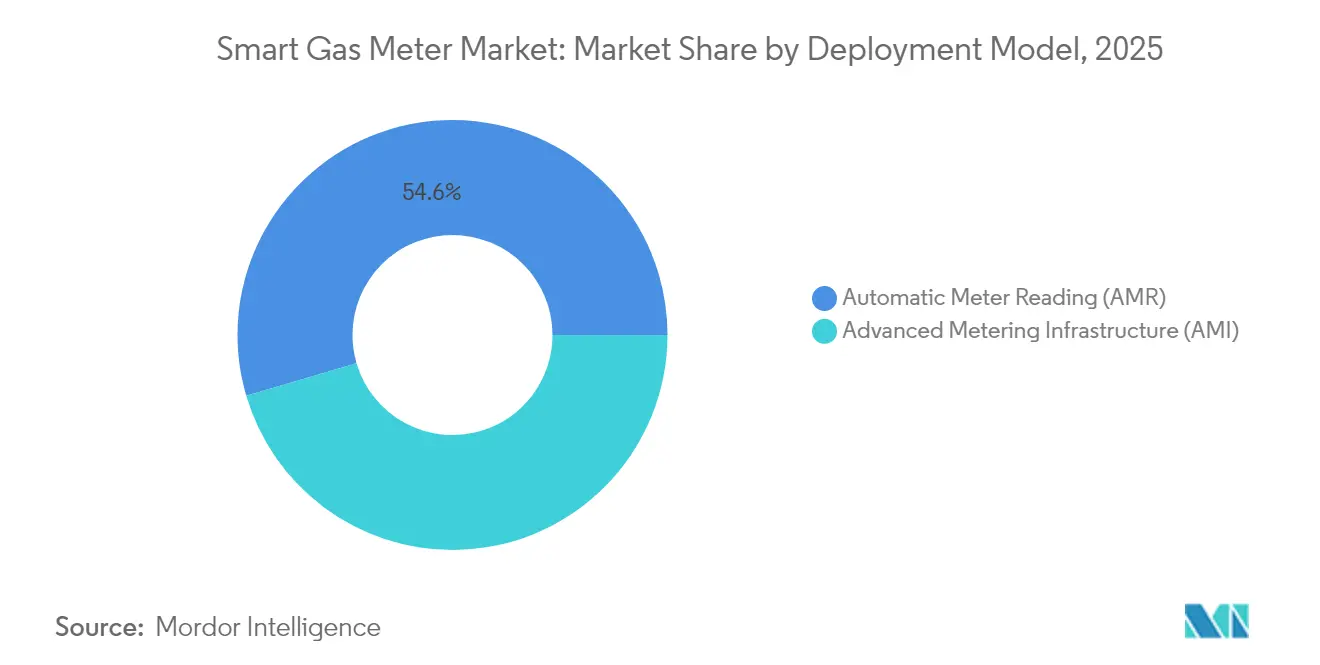

- By deployment model, Automatic Meter Reading held 54.55% of the smart gas meters market size in 2025, but Advanced Metering Infrastructure is projected to grow at a 13.1% CAGR to 2031.

- By end-user, residential applications accounted for a 38.45% share of the smart gas meters market size in 2025, whereas industrial installations advance at a 14.8% CAGR through 2031.

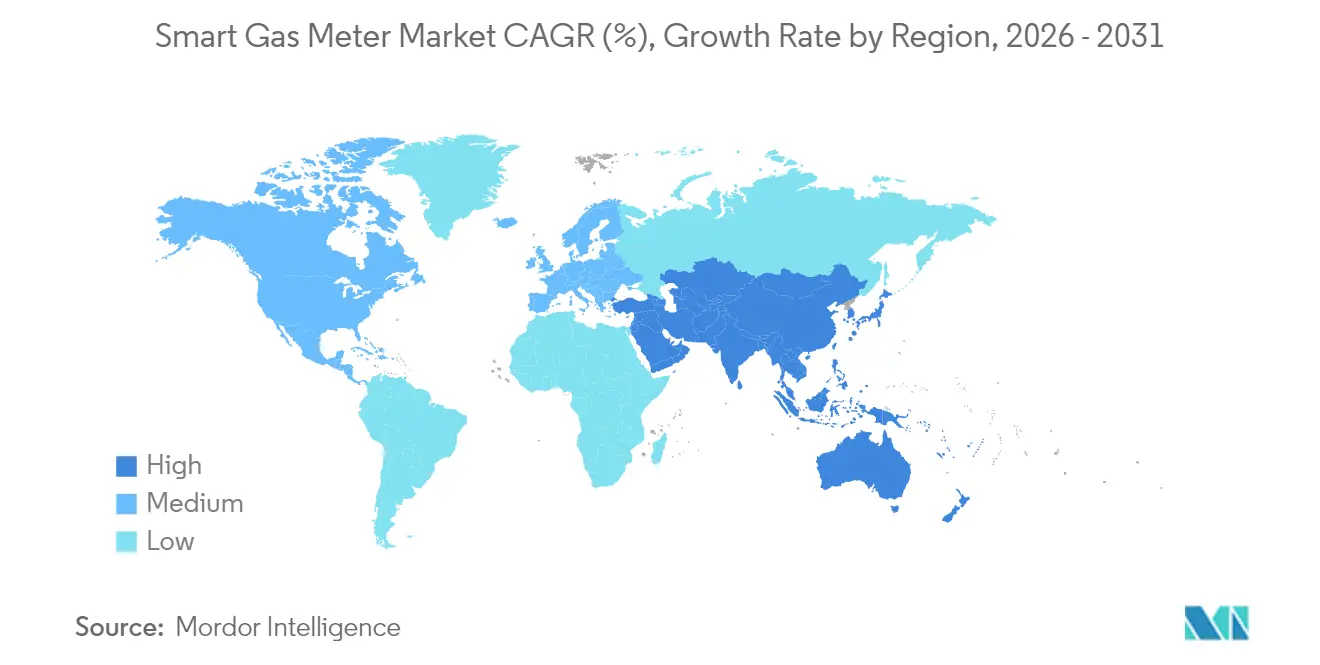

- By geography, Asia Pacific captured a 41.65% share in 2025 and leads growth at a 15.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Gas Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates and mass roll-outs | +2.8% | Global - early in EU, Australia, North America | Medium term (2-4 years) |

| Utility OPEX reduction and billing accuracy | +2.1% | Global | Short term (≤ 2 years) |

| Rising downstream natural-gas demand | +1.7% | Asia Pacific core; spill-over to Middle East and Africa | Long term (≥ 4 years) |

| NB-IoT and LPWAN boosting battery life and coverage | +1.5% | Global; advanced in Europe and Asia Pacific | Medium term (2-4 years) |

| Mandatory replacement of ageing diaphragm meters | +1.2% | North America and EU | Short term (≤ 2 years) |

| Safety-centric shift to ultrasonic meters w/ shut-off | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates and Mass Roll-outs

Governments have moved beyond voluntary adoption by setting hard deadlines that force utilities to act regardless of internal ROI hurdles. Australia’s Energy Market Commission requires full residential smart gas coverage by 2030, while Germany mandates meters on all new heat-pump installations from 2025. The European Union’s allowance of up to 2% hydrogen in distribution networks adds a compliance layer because legacy diaphragm devices cannot meet accuracy thresholds. FortisBC’s 1.1 million-unit exchange running 2025-2028 illustrates how regulations convert discretionary investment into obligatory procurement. Vendors with certified cybersecurity and interoperability credentials are preferred as policymakers tie rollout approvals to data-protection standards.

Utility OPEX Reduction and Billing Accuracy

Utilities battling labor inflation and manual-reading delays can cut 80-90% of truck rolls while bumping billing accuracy from 95% to 99.5% [1]National Grid, “Advanced Metering Infrastructure Puts Customers in Control of Their Energy Use,” nationalgrid.com. National Grid’s combined electric-gas deployment shows that continuous data streams unlock time-of-use tariffs that shift demand and defer expensive peak-capacity upgrades. Leak-detection analytics reduce unaccounted-for gas losses and mitigate safety incidents, magnifying lifetime OPEX savings over 15-year meter lifecycles. These economic paybacks justify accelerated rollouts even in jurisdictions lacking direct mandates.

Rising Downstream Natural-Gas Demand

Industrial gas use in petrochemicals, hydrogen production, and LNG-fueled power plants is climbing 1.0-2.4% yearly across the Asia Pacific. Large sites need real-time flow data for carbon accounting and process optimization, tasks that mechanical meters cannot meet. Blending biomethane and synthetic methane introduces composition variability, elevating demand for composition-aware ultrasonic devices. Middle Eastern utilities confronting supply tightness are turning to smart metering at gate stations and large industrial hubs to optimize allocation between domestic, industrial, and export streams.

NB-IoT and LPWAN Boosting Battery Life and Coverage

NB-IoT extends battery life from seven to nearly twenty years and penetrates basements where proprietary RF struggles. Itron’s solar battery access point, released in 2025, eliminates the need for power drops, cutting network expansion costs by up to 30% [2]Itron Inc., “Itron Introduces Solar-Powered Access Point to Expand Intelligent Connectivity,” itron.com . Cellular standardization under 3GPP offers long-term vendor support, enabling over-the-air firmware updates critical for cybersecurity compliance. Utilities in rural Canada, coastal Australia, and mountainous Japan cite connectivity as the chief hurdle, making LPWAN a decisive adoption driver.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and slow ROI | -1.8% | Global, acute in developing economies | Short term (≤ 2 years) |

| Cybersecurity and data privacy risks | -1.2% | Global; heightened in North America and EU | Medium term (2-4 years) |

| Semiconductor and battery supply constraints | -0.9% | Global | Short term (≤ 2 years) |

| Interoperability gaps in mixed-fleet retrofits | -0.7% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Slow ROI

Smart meters cost USD 150-300 each versus USD 30-50 for mechanical units. When communications backhaul, head-end software, and cybersecurity upgrades are included, full-deployment costs can double. Payback periods stretch to 7-12 years, clashing with utilities’ preference for quicker investment cycles. In emerging markets, foreign-exchange volatility and limited concessional funding widen the affordability gap, especially for small municipal utilities with sub-100,000 customer bases.

Cybersecurity and Data Privacy Risks

Advanced meters introduce new attack vectors across firmware, communications, and backend systems. The US Cybersecurity and Infrastructure Security Agency warns that compromised endpoints can propagate across the meter mesh, threatening system-wide outages [3]CISA, “Mitigating Cyber Threats with Limited Resources,” cisa.gov . FERC’s 2025 ruling obliges gas network operators to meet strict encryption and patch-management protocols. Granular consumption data can reveal household occupancy patterns, triggering GDPR enforcement exposure in Europe. Utilities must therefore spend on continuous monitoring, PKI management, and third-party audits, expenses that dilute ROI projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meter Type: Ultrasonic Technology Drives Premium Transition

Diaphragm devices accounted for 41.75% of the smart gas meters market size in 2025, a legacy advantage built on cost and incumbent installed base. Ultrasonic meters, though pricier, are projected to grow at a 12.1% CAGR as hydrogen blending and multi-gas scenarios demand higher accuracy bands.

The migration is most visible in Europe and Japan, where regulators reference ultrasonic performance in hydrogen-ready standards. Utilities prefer future-proof assets to avoid stranded costs should hydrogen ratios rise. Itron has shipped more than 1 million ultrasonic units, confirming scale economics and reliability gains. Turbine and rotary piston meters stay relevant in high-flow industrial niches, while MEMS-based solid-state sensors remain early-stage, constrained by temperature-drift concerns. With expanded production, ultrasonic list prices have fallen 18% since 2023, narrowing the gap and accelerating replacement cycles within the smart gas meters market.

By Communication Technology: NB-IoT Challenges RF Dominance

RF solutions operating at 169 MHz in Europe and 902-928 MHz held 38.10% of the smart gas meters market share in 2025. However, NB-IoT/LTE-M is advancing at a 10.72% CAGR, taking share as utilities piggyback on nationwide cellular rollouts.

Cellular modules provide firmware-over-the-air, carrier-grade security, and deep indoor penetration. In China and Italy, national operators offer discounted NB-IoT tariffs to utilities, slashing connectivity OPEX. RF remains competitive in territories where utilities desire network ownership or cellular coverage is patchy, such as Alberta oil fields or rural Indonesia. PLC retains a niche where power-line infrastructure already exists, chiefly in European apartment blocks. LoRaWAN serves sparsely populated districts needing long-range, low-bit-rate connectivity. Over the forecast period, hybrid architectures combining RF mesh backhaul with NB-IoT edge redundancy are emerging to maximize reliability within the smart gas meters market.

By Deployment Model: AMI Gains Despite AMR’s Current Lead

Automatic Meter Reading still represents 54.55% of the global smart gas meters market size in 2025 because it fulfills billing automation at a lower capital cost. Yet Advanced Metering Infrastructure is rising at 13.1% CAGR as utilities value two-way command, remote shutoff, and demand-response integration.

AMI momentum is reinforced by carbon-reporting obligations that require interval data granularity. European DSOs integrating gas with electric and water metering platforms gain analytics synergies that justify incremental AMI expense. North American utilities highlight outage management and emergency disconnect features as critical safety upgrades. While some cash-constrained utilities opt for AMR today, most new tenders stipulate AMI readiness clauses to future-proof procurements within the smart gas meters market.

By End-user: Industrial Segment Outpaces Residential Growth

Residential service retains a 38.45% stake in the smart gas meters market share owing to regulatory mandates and sheer customer volume. Industrial sites, however, are forecast to grow at a 14.8% CAGR until 2031.

Large industrial consumers see real-time telemetry as indispensable for ISO 14001 certification and carbon trading compliance. Petrochemical complexes in South Korea, steel mills in India, and LNG terminals in Qatar are pilot-testing ultrasonic meters with SCADA hooks for instantaneous flow, temperature, and pressure data. Commercial buildings, including hotels and shopping malls, record stable uptake shaped by building-automation retrofits. As ESG reporting grows stringent, industrial demand may escalate further, reinforcing the diversification of revenue streams within the smart gas meters market.

Geography Analysis

Asia Pacific dominated the smart gas meters market with a 41.65% share in 2025 and is advancing at a 15.2% CAGR through 2031. China’s province-level smart-city budgets earmark gas metering as a priority, while Japan’s net-zero roadmap forces utilities to upgrade to hydrogen-compatible devices. Local manufacturing ecosystems lower hardware costs by 12-18% versus imports, improving project IRR calculations. Osaka Gas Network’s adoption of MEEQ SIM for mobile IoT management exemplifies the region’s leadership in network innovation.

North America remains the second-largest smart gas meters market, shaped by structured replacement programs and cybersecurity regulation. FortisBC’s 1.1 million-meter rollout running 2025-2028 illustrates the region’s steady conversion pace. FERC cybersecurity standards, effective in 2025, elevate certification barriers, favoring established vendors with validated encryption stacks. The US Inflation Reduction Act’s incentives for methane-leak reduction also sharpen the economic case for AMI adoption.

Europe shows robust growth driven by hydrogen blending and energy-security imperatives following geopolitical disruptions. Germany’s 2025 heat-pump rule and the UK’s push for 100% hydrogen-ready networks sustain procurement volume. Subsidy schemes under the EU Resilience and Recovery Facility help smaller DSOs finance AMI upgrades, while privacy and interoperability standards maintain vendor accountability.

The Middle East and Africa, though smaller, post above-average growth as governments deploy smart-city projects tied to 5.5G connectivity. Saudi Arabia’s NEOM and the United Arab Emirates’ Masdar City specify NB-IoT smart metering within master plans. Currency volatility and technical-skill shortages present challenges; however, multilaterals such as the World Bank’s EDGE initiative are stepping in with concessional loans, smoothing adoption curves.

Regulatory Landscape

Regulation is tightening around smart metering as a compliance tool for safety, accuracy, and multi-gas readiness. In the European Union, Directive (EU) 2026/706 (signed 11 March 2026, effective 9 April 2026) amends the Measuring Instruments Directive (2014/32/EU) to address smart gas metering and the integration of hydrogen and other non-conventional fuel gases. This raises the bar for conformity assessment and hydrogen-compatible measurement performance.

In Asia, the Energy Market Authority of Singapore published the Gas Metering Code 2026, anchoring installation and testing expectations to defined standards (SS 608 and test procedures referencing BS EN 1359, BS EN 12480, and BS EN 12261). In North America, approval pathways are becoming more explicit at the state level, exemplified by the New York State Public Service Commission order (May 2026) approving an ultrasonic smart gas meter for use by Niagara Mohawk Power Corporation (National Grid) under 16 NYCRR Part 227. This reinforces the role of regulator-approved equipment lists in procurement and deployment sequencing.

Value Chain Analysis

The smart gas meter value chain covers metrology and materials inputs (sensing elements, enclosure polymers, batteries), electronics and connectivity modules (MCUs, RF/NB-IoT chipsets, secure elements), and meter assembly and calibration. It also includes utility-facing software (head-end/MDMS/analytics) and field services such as installation, commissioning, and maintenance.

On the demand side, utilities and gas distribution operators typically procure through multi-year tenders that bundle meters with communications infrastructure and software integration. Telecom operators and LPWAN network providers support NB-IoT/LTE-M and LoRaWAN connectivity as part of the deployment stack. Two structural shifts stand out in recent activity. First, more programs combine meter hardware with communications retrofits to accelerate digitization of installed fleets, illustrated by Landis+Gyr partnering with Origin Energy in June 2026 to deploy intelligent IoT modules onto existing infrastructure over an 18-month program window. Second, solution ecosystems are widening beyond meter OEMs into network operators and financiers, as shown by Netmore Group collaborating with Green Frog Asset Management and Sensational Systems (May 2026) to deliver an end-to-end LoRaWAN-based smart gas metering solution in the United Kingdom. Execution remains sensitive to electronics lead times and installer availability, so certified field partners and dual-sourcing for critical electronics are differentiators for on-time rollout delivery.

Competitive Landscape

The smart gas meters market is moderate in concentration. Landis+Gyr, Itron, and Honeywell hold notable shares through deep product portfolios, strong after-sales service, and cybersecurity certifications. Utilities deliberately split tenders to hedge supply-chain risk and prevent lock-in.

Technology differentiation now centers on hydrogen measurement accuracy, low-power connectivity, and embedded security modules. Honeywell reported 8% organic growth in Building Automation during Q1 2025 as smart metering offset softness in legacy controls. Itron’s solar access point broadens AMI reach in off-grid areas, positioning the firm as a connectivity innovator.

Partnerships between meter vendors and telecom operators are accelerating. Verizon’s January 2025 alliance with Honeywell seeks to combine 5G private networks with edge analytics, hinting at convergence between OT and IT stacks. Mergers and acquisitions speculation is rising after Honeywell’s plan to spin off its Automation division by H2 2026, potentially triggering consolidation as pure-play firms pursue scale. Regional entrants like Kamstrup in Scandinavia and Goldcard in China are leveraging local support and price competitiveness to erode incumbent share, underscoring the dynamic nature of competition within the smart gas meters market.

Smart Gas Meter Industry Leaders

Landis+Gyr Group AG

Itron Inc.

Honeywell International Inc.

Sensus (Xylem Inc.)

Diehl Stiftung and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A core opportunity is hydrogen-ready and multi-gas compliant metering, supported by updated standards and directives that drive upgrades beyond basic AMR functionality. The EU effort to amend the Measuring Instruments Directive via Directive (EU) 2026/706 (effective 9 April 2026), alongside associated standard updates (for example, Commission Implementing Decision (EU) 2025/375 updating harmonized standards with effect tied to August 27, 2026), creates whitespace for ultrasonic and advanced metrology designs that can document performance under changing gas compositions. This direction also aligns with cybersecurity and remote-management requirements.

Utility programs and product approvals are creating nearer-term procurement lanes that favor vendors able to supply certified devices, connectivity, and software integration as a package. Examples include the New York Public Service Commission approval (May 2026) for the Landis+Gyr G480 ultrasonic smart gas meter for use by Niagara Mohawk Power Corporation (National Grid), and Polska Spolka Gazownictwa initiating the E-Gas Meter project (August 2025) to replace 1.38 million meters with smart devices targeted for completion by December 2026. In addition, large, multi-year supply awards such as MeteRSit (SIT Group) securing a 100 million euro contract for the Netherlands with deliveries starting in 2027 show how long-dated framework contracts reward suppliers that can lock component availability, field-service capacity, and interoperability with mixed communication architectures (RF plus NB-IoT/LTE-M) over extended rollout timelines.

Recent Industry Developments

- June 2026: The New York State Public Service Commission approved Landis+Gyr's Surent G480 ultrasonic gas meter for use in New York State, marking a milestone for ultrasonic smart gas metering adoption under state utility equipment approval processes. With an integrated shut-off valve designed to meet gas tightness expectations, the approval supports utility procurement pathways that prioritize safety features alongside measurement accuracy.

- June 2025: Itron introduced the Solar Battery Access Point for North American gas and water utilities to extend AMI coverage where grid power is unavailable. The product positions network expansion as a hardware plus connectivity problem, reducing the need for new power drops and supporting broader rollouts in difficult-to-serve locations.

- February 2024: The US Department of Energy issued updated federal metering guidance for facility energy and water metering, reinforcing standardized approaches to data collection and system management across federal sites. While not gas-specific, the guidance supports a broader shift toward digital metering practices that can influence vendor requirements for interoperability, cybersecurity, and long-life remote communications in public-sector deployments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the smart gas meter market covers digital gas metering devices installed at customer sites that measure gas consumption and securely transmit readings to utilities using wired or wireless communication.

Scope exclusions: Standalone mechanical gas meters without remote communication, plus pure services that are not bundled with meter shipments, are not counted.

Segmentation Overview

- By Meter Type

- Diaphragm

- Ultrasonic

- Turbine

- Rotary Piston

- MEMS/Solid-state

- By Communication Technology

- RF (169/868 MHz)

- PLC

- GSM/GPRS

- NB-IoT/LTE-M

- LoRaWAN

- By Deployment Model

- Automatic Meter Reading (AMR)

- Advanced Metering Infrastructure (AMI)

- By End-user

- Residential

- Commercial

- Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia and New Zealand

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of the Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting structure for the model and keep the assumptions realistic across regions. We reviewed public statistics and standards references such as energy regulator publications, national energy ministries, and smart metering rollout documents that outline timelines and compliance requirements. Utility annual reports, investor presentations, and procurement notices were also reviewed to understand replacement cycles, tender sizes, and installation pace.

On the data side, we used sources such as customs and trade statistics, smart grid and metering association releases, peer reviewed journal articles on metering technology shifts (including ultrasonic and communications), and patent databases to track where innovation and cost curves are heading. Where public disclosures were thin, we used a paid subscription for company financials and news to validate revenue exposure, and we selectively checked shipment level import and export data for directional reasonableness. These examples are not exhaustive, and we relied on additional public references for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on utility metering teams, distribution network stakeholders, system integrators, and component and meter suppliers who see order flow and deployment constraints firsthand. We used these conversations to pressure test rollout timing, typical unit pricing bands, the AMI versus AMR mix, and how communication choices such as NB-IoT affect the total system cost across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 32% | EMEA: 37% |

| Smaller Players: 19% | Managers: 52% | Americas: 23% |

Market-Sizing & Forecasting

Sizing started with a top-down build where country level smart metering programs, utility replacement schedules, and installed gas customer bases were used to reconstruct annual shipment demand. From there, value was derived using typical average selling price ranges by meter type and deployment model, then adjusted for regional communication and certification differences.

To keep the totals grounded, we corroborated the outputs using selective bottom-up approximations such as supplier revenue exposure checks, sampled price quotes from tenders, and discussions with channel contacts on annual volumes. When gaps existed, for example where program timing was not clearly published, we used neighboring market analogs and then corrected them through primary feedback.

Key inputs that shaped the model included mandated rollout timelines, meter replacement cycles, AMI versus AMR adoption share, communication technology mix (including cellular options like NB-IoT), and shipment volumes implied by utility procurement activity. Forecasting relied on scenario analysis supported by expert views, where base, faster, and slower rollout cases were tied back to regulation timing, funding availability, and supply lead times.

Data Validation & Update Cycle

Outputs were checked through multiple steps so the final numbers stay consistent with real market signals. We compared the modeled shipment and value trends against independent indicators such as published rollout targets, tender cadence, and reported utility capital spend patterns, and then we reviewed outliers before sign-off.

If a major variance showed up, we revisited assumptions and re-contacted respondents to confirm what changed and why. The report is refreshed annually, and interim updates are made when material events occur, including policy changes, large procurement announcements, or sudden pricing shifts. Before delivery, we rechecked the latest public releases so clients receive an updated view that matches the current market context.

Mordor Intelligence's Smart Gas Meter Market Sizing Compared With Other Published Estimates

Published market sizes for smart gas meters can vary even when the topic sounds identical, mainly because studies draw different lines around what is included and how the yearly demand pool is constructed. Differences in whether AMI and AMR are both counted, how replacement cycles are timed, and what is assumed for price erosion are usually the biggest drivers.

By tracking program based shipment timing and refreshing communication driven ASP assumptions, Mordor Intelligence keeps the total tied to utility rollout realities instead of mixing in broader smart grid spending or software heavy bundles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.44 B (2026) | |

| Global Consultancy A | USD 2.49 B (2024) | Uses an earlier base year and a slightly different study window, and the component framing can pull software and broader system elements into the value, which lifts the total when compared year to year. |

| Industry Publisher B | USD 6.60 B (2024) | The scope appears wider and can overcount by combining adjacent smart metering system spend with device revenue, and it can also assume faster rollout and higher blended prices across applications. |

The spread across sources is mostly explained by scope boundaries and the way annual deployments and pricing are translated into dollars. When the model sticks to shipment based demand, clear AMI versus AMR treatment, and repeatable pricing logic, the resulting number is easier to reconcile with utility procurement and rollout schedules.

Key Questions Answered in the Report

What is the forecast value of the smart gas meters market by 2031?

The market is projected to reach USD 3.78 billion by 2031, reflecting a 9.12% CAGR.

Which meter type is growing fastest within smart gas metering?

Ultrasonic meters are forecast to expand at 12.1% CAGR due to hydrogen-ready performance and higher accuracy.

Why are utilities shifting from RF to NB-IoT connectivity?

NB-IoT offers deeper indoor coverage and boosts battery life to nearly 20 years, reducing maintenance costs and improving data reliability.

Which region leads both in size and growth rate?

Asia Pacific holds the largest share at 41.65% in 2025 and advances at 15.2% CAGR through 2031.

How do regulatory mandates influence deployment?

Mandates set hard deadlines that override ROI hurdles, exemplified by Australia’s 2030 target and Germany’s 2025 requirements, forcing accelerated procurement.

What are the key cybersecurity concerns with smart gas meters?

Vulnerabilities in firmware and communication protocols can enable unauthorized access or remote shutoff, prompting strict encryption and patch-management standards.

Page last updated on: