Residential Air Purifiers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

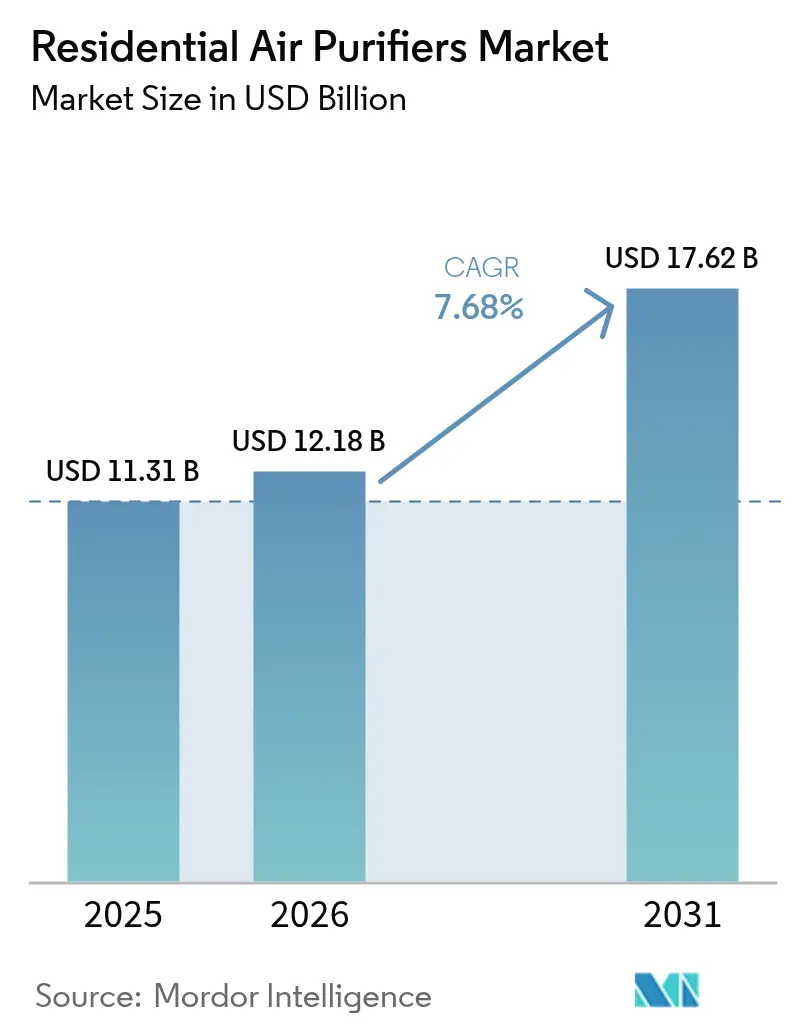

| Market Size (2026) | USD 12.18 Billion |

| Market Size (2031) | USD 17.62 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

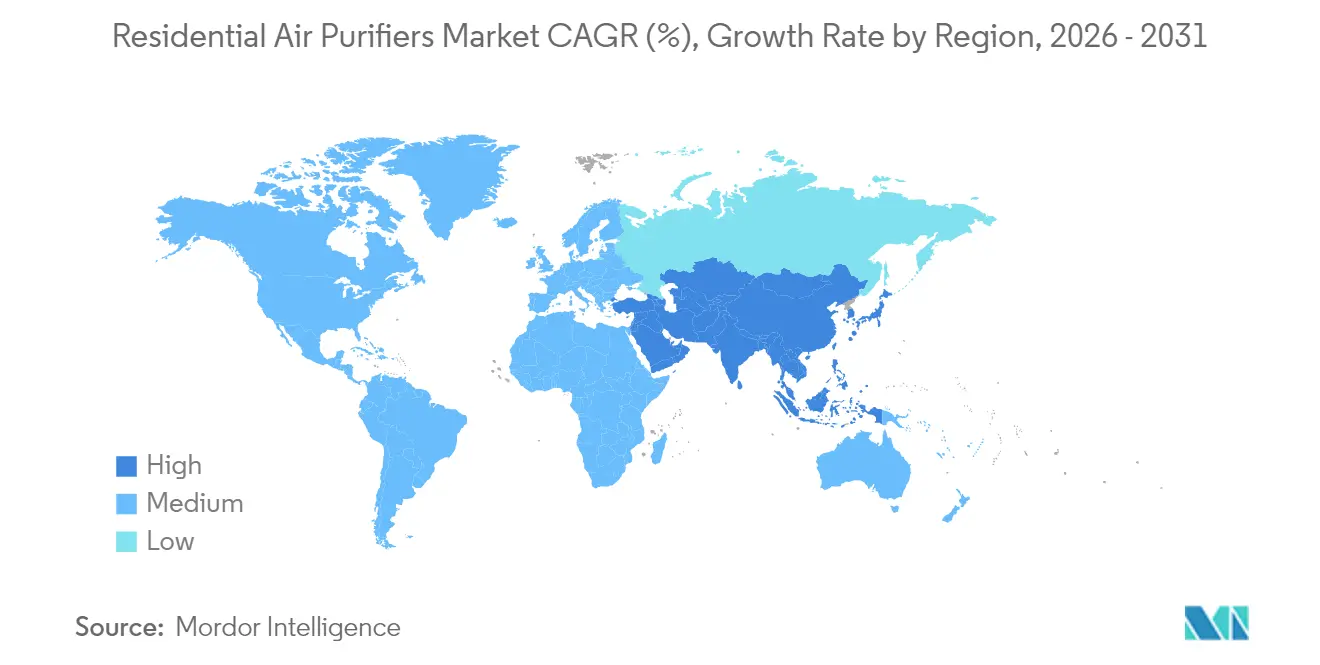

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Residential Air Purifiers Market Analysis by Mordor Intelligence

The Residential Air Purifiers Market size is expected to grow from USD 11.31 billion in 2025 to USD 12.18 billion in 2026 and is forecast to reach USD 17.62 billion by 2031 at 7.68% CAGR over 2026-2031.

Consumer concern about indoor pollutants increased significantly after the COVID-19 pandemic, and 53% of homeowners now rank indoor air quality among their top health priorities. Government efficiency rules, such as the U.S. Department of Energy standard that took effect in December 2023, are encouraging manufacturers to adopt lower-power designs. Asia-Pacific drives both volume and growth as chronic urban smog turns air purifiers into everyday appliances. Technology competition is heating up: HEPA remains the benchmark, yet hybrid systems that layer UV-C or carbon filters are gaining favor. Consolidation is underway as appliance giants acquire niche filtration brands to expand their portfolios and generate subscription revenue.

Key Report Takeaways

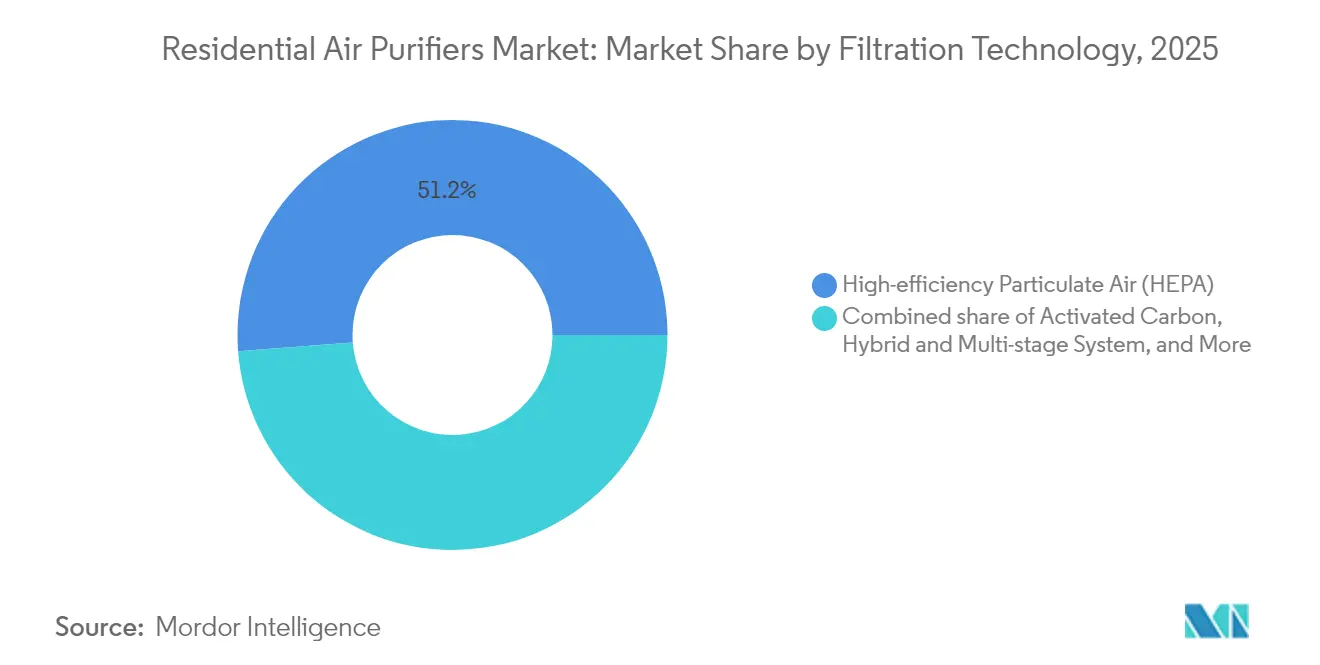

- By filtration Technology, HEPA filtration led with a 51.20% residential air purifiers market share in 2025, while hybrid systems are expected to deliver a 9.05% CAGR through 2031.

- By type, Portable units commanded 86.70% of the residential air purifiers market size in 2025; in-duct solutions are projected to expand at a 10.35% CAGR between 2026-2031.

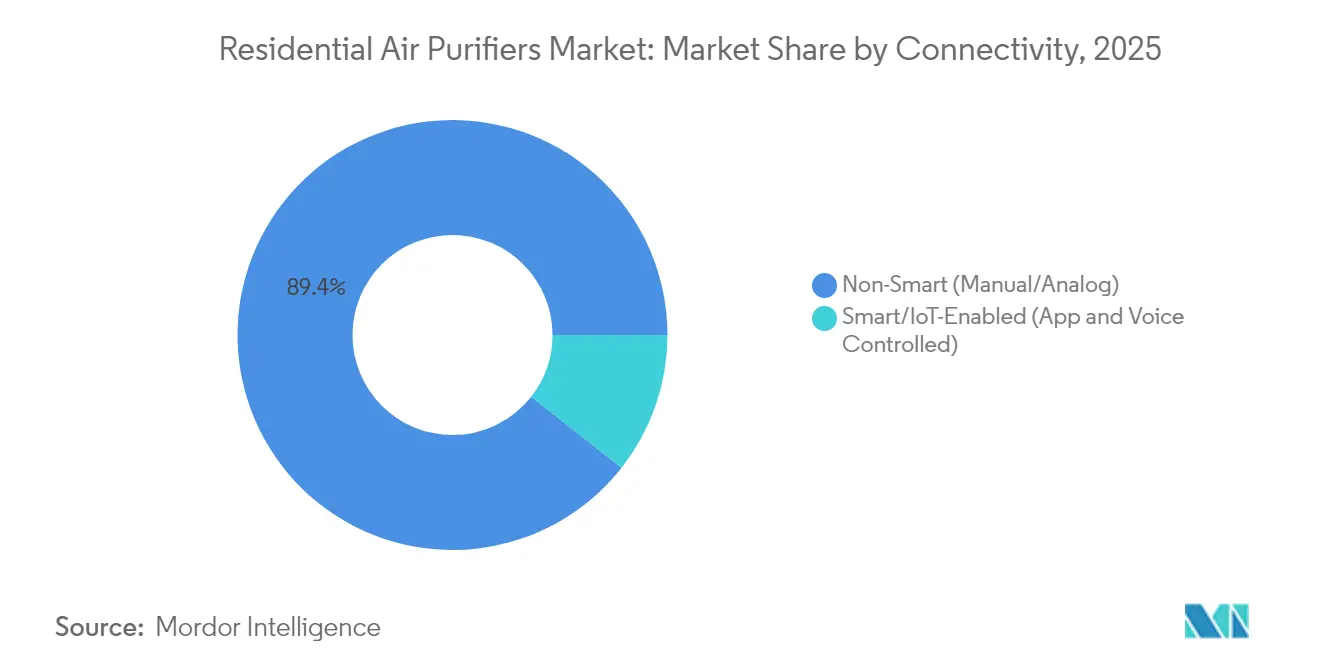

- By connectivity, Traditional non-smart devices held 89.40% of the residential air purifiers market in 2025, but smart models are poised for an 10.95% CAGR to 2031.

- By geography, Asia-Pacific captured 45.15% of the residential air purifiers market in 2025 and is forecast to post a 9.20% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Residential Air Purifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising ambient PM2.5 levels in urban centers | +2.1% | Asia-Pacific core, spill-over to global urban areas | Long term (≥ 4 years) |

| Post-COVID focus on indoor air quality (IAQ) | +1.8% | Global, with highest impact in North America & EU | Medium term (2-4 years) |

| Government incentives for energy-efficient IAQ devices | +1.2% | North America & EU, emerging in Asia-Pacific | Medium term (2-4 years) |

| Smart-home and IoT ecosystem pull-through | +0.9% | Global, led by North America and developed APAC | Long term (≥ 4 years) |

| Subscription-based filter-replacement models | +0.7% | North America & EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growth of remote work increasing indoor time | +0.5% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Ambient PM2.5 Levels in Urban Centers

Escalating fine-particle pollution across Asian megacities is driving the residential air purifiers market into a long-term uptrend. PM2.5 readings in Beijing and Delhi often exceed WHO guidelines by 300% to 400%. Health studies link these spikes to respiratory disease, and South Korea attributes 40,000 yearly deaths to pollution. Governments respond with multi-billion-dollar clean-air plans, yet indoor protection remains the consumer’s immediate defense. Manufacturers highlight particulate metrics; Panasonic’s nanoe X platform reports a 99% reduction in PM2.5 efficiency. Persistent smog, therefore, sustains demand for devices, positioning air purifiers alongside water filters as household essentials.

Post-COVID Focus on Indoor Air Quality

The pandemic repositioned clean air from optional comfort to a core health need, triggering new adoption in the residential air purifiers market. U.S. sales are projected to climb from USD 2.8 billion in 2022 to USD 4.78 billion by 2030. Public-health agencies endorse portable HEPA or UV-C units for pathogen control, bolstering trust. Research has shown that photocatalytic filters can deactivate SARS-CoV-2 effectively.[1]International Journal of Environmental Research and Public Health, “PM2.5 and Mortality in South Korea,” mdpi.com Start-ups such as Molekule gained FDA clearance for virus-targeting products, proving commercial traction. Continued expert messaging that better ventilation curbs future outbreaks keeps the momentum alive.

Government Incentives for Energy-Efficient IAQ Devices

Rebates and standards lower ownership costs and spur technology upgrades across the residential air purifiers industry. Oregon’s USD 75 rebate on ENERGY STAR units and California’s USD 2.8 million AB 617 grant in disadvantaged homes trim payback periods.[2]Energy Trust of Oregon, “Residential Air Cleaner Rebate,” energytrust.org Federal minimum efficiency levels, effective 2023, could yield USD 5.8-13.7 billion in lifetime consumer savings. These policies encourage the development of high-CADR, low-wattage models and create a transparent performance yardstick that lifts premium adoption.

Smart-Home and IoT Ecosystem Pull-Through

Connectivity converts standalone purifiers into data-rich nodes that appeal to tech-savvy buyers. The smart sub-segment is forecast to reach USD 17.7 billion by 2032 at a 10.1% CAGR. Products such as Winix’s C610 integrate WiFi control and sensor-driven automation. Vendors bundle predictive filter replacement and subscription financing, smoothing maintenance hurdles. Voice-assistant compatibility pushes penetration among busy households and elderly users, reinforcing premium positioning in the residential air purifiers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front and maintenance costs | -1.4% | Global, most pronounced in price-sensitive emerging markets | Medium term (2-4 years) |

| Ozone & by-product safety concerns | -0.8% | North America & EU, spreading to Asia-Pacific | Long term (≥ 4 years) |

| HVAC integrated filters reducing incremental demand | -0.6% | North America & EU, limited impact in Asia-Pacific | Long term (≥ 4 years) |

| Consumer "filter-replacement fatigue" | -0.4% | Global, particularly in markets without subscription models | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front and Maintenance Costs

Effective HEPA units range from USD 150 to USD 1,500, while replacement filters, costing USD 50 to USD 200 twice a year, inflate lifetime outlays. Total cost can match the purchase price within five years, discouraging lower-income families in the regions that need them most. DIY options such as the Corsi-Rosenthal box highlight price sensitivity. Although subscription plans and financing ease the burden, high ownership costs remain the strongest constraint on the residential air purifiers market.

Ozone & By-Product Safety Concerns

Ionic and electrostatic devices face regulatory pushback because they release ozone and secondary pollutants. California mandates that indoor cleaners emit less than 0.05 ppm of ozone, and the FDA labels ozone a toxic gas at any therapeutic level.[3]California Air Resources Board, “Indoor Air Cleaner Regulation,” carb.ca.gov Studies from the Lawrence Berkeley National Laboratory find that some generators are ineffective at removing VOCs while forming formaldehyde. Brands now pursue UL 2998 validation (<0.005 ppm ozone) or pivot to filter-based designs, but lingering safety doubts temper demand in sensitive consumer segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filtration Technology: HEPA Dominance Faces Hybrid Innovation

HEPA retained a 51.20% residential air purifier market share in 2025 thanks to its 99.97% capture rate for 0.3-micron particles. Hybrid systems that combine HEPA, activated carbon, and UV-C achieve the fastest 9.05% CAGR, as buyers seek comprehensive pollutant coverage. Ionic solutions decline under ozone rules, while emerging photocatalytic media attract pathogen-focused shoppers.

Manufacturers innovate around multi-stage stacks: Coway’s HyperVortex filter claims 99.999% efficiency down to 0.01 microns. Research into nanofiber HEPA and metal-organic frameworks promises lower pressure drop and longer life. This shift underpins the potential for premium pricing across the residential air purifiers market.

By Type: Portable Leadership Challenged by Integrated Solutions

Portable units captured 86.70% of the residential air purifiers market size in 2025 because they are easy to install, renter-friendly, and priced entry-level. In-duct systems, however, are growing at a rate of 10.35% annually, as homeowners favor whole-house coverage that leverages existing HVAC ducts.

Remote-work trends increase daily indoor hours and drive demand for broader protection. Filter-free electrostatic plates, now being piloted in Korea with over 90% ultrafine removal efficiency, could significantly reduce maintenance costs. Financing and subscription models are gradually narrowing the cost gap that once limited the use of central solutions.

By Connectivity: Smart Features Drive Premium Adoption

Non-smart models still dominate, with a 89.40% share in 2025, due to their budget appeal and perceived comfort in terms of privacy. Yet smart devices post an 10.95% CAGR, redefining the residential air purifiers market as part of the connected-home bundle.

Real-time AQI displays, cloud analytics, and voice-activated commands add functional value. Samsung and LG now pitch purifier subscriptions that pair AI diagnostics with automatic filter shipments. Data-rich services lock in customer loyalty and open pathways for energy-management tie-ins.

Geography Analysis

The Asia-Pacific region posted a 45.15% residential air purifiers market share in 2025 and is expected to lead future growth with a 9.20% CAGR. Chronic urban smog, combined with rising incomes, prompts Chinese and Indian households to view indoor air as a health utility. Xiaomi leverages an IoT ecosystem to scale mid-price purifiers, while Korean firms such as Coway excel with rental models that eliminate upfront cost. Government clean-air budgets accelerate replacement cycles.

North America follows a regulatory-driven path. U.S. incentive programs and wildfire smoke increase purchase urgency, driving the residential air purifiers market size in the region to an expected USD 5.14 billion by 2031. California’s strict ozone cap influences national product standards, and the adoption of smart homes yields a premium skew.

Europe values energy efficiency and low noise. Stringent eco-design directives favor low-wattage units, and consumers are willing to accept premium price tags for durable builds. South America and the Middle East & Africa remain nascent but are logging double-digit shipment growth as urbanization spreads and middle-class incomes rise, suggesting a long runway for the global residential air purifiers market.

Competitive Landscape

The residential air purifier market is fragmented, with no single player controlling a double-digit global share. Appliance majors such as Samsung, LG, and Dyson compete for volume with specialist brands like Coway and IQAir. Post-pandemic demand triggered M&A: iRobot acquired Aeris Cleantec to diversify beyond floor care, while Blade Air acquired InnerEco for its filtration expertise.

Technology differentiation centers on virus inactivation and energy savings. Sharp’s Plasmacluster ions cut SARS-CoV-2 titers by 99.4% in lab tests. Start-ups are harnessing nanomaterials for VOC capture, while incumbents are refining low-wattage fans to comply with forthcoming EU eco-design rules.

Business-model innovation is equally fierce. Samsung’s AI subscription club undercuts upfront pricing, and Coway’s rental accounts reach 10 million worldwide, with 34% outside of Korea. Vendors rely on recurring filter sales to stabilize revenue and finance research and development for the next leap in the residential air purifiers market.

Residential Air Purifiers Industry Leaders

Daikin Industries Ltd

Koninklijke Philips NV

Coway Co. Ltd

Xiaomi Corp.

Dyson Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Coway introduced the Airmega 350 and 450 in Canada, featuring HyperVortex filters that remove 99.999% of 0.01-micron particles.

- March 2025: Korea’s National Research Council deployed filter-free electrostatic purifiers, achieving 90% ultrafine particle removal, which signals a residential rollout.

- January 2025: LG Electronics (LG) has launched the LG PuriCare AeroBooster, an air care solution designed to enhance indoor comfort and improve overall health. This product features advanced air purification technology and a sleek design that combines style with convenience.

- December 2024: Samsung unveiled an AI subscription club that covers air purifiers and other appliances to minimize upfront costs.

Global Residential Air Purifiers Market Report Scope

The residential air purifier market report includes:

| High-efficiency Particulate Air (HEPA) |

| Activated Carbon |

| Ionic/Electrostatic Precipitators |

| UV-C and Photocatalytic Oxidation |

| Hybrid and Multi-stage Systems |

| Stand-alone/Portable |

| In-duct/Central HVAC |

| Non-Smart (Manual/Analog) |

| Smart/IoT-Enabled (App and Voice Controlled) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| Filtration Technology | High-efficiency Particulate Air (HEPA) | |

| Activated Carbon | ||

| Ionic/Electrostatic Precipitators | ||

| UV-C and Photocatalytic Oxidation | ||

| Hybrid and Multi-stage Systems | ||

| Type | Stand-alone/Portable | |

| In-duct/Central HVAC | ||

| By Connectivity | Non-Smart (Manual/Analog) | |

| Smart/IoT-Enabled (App and Voice Controlled) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current residential air purifiers market size and growth outlook?

The residential air purifiers market size reached USD 12.18 billion in 2026 and is projected to hit USD 17.62 billion by 2031, reflecting an 7.68% CAGR.

Which region leads the residential air purifiers market?

Asia-Pacific leads with a 45.15% share in 2025 and is forecast to grow at a 9.20% CAGR through 2031.

What technology dominates the residential air purifiers market?

HEPA filtration holds a 51.20% share, while hybrid multi-stage systems are the fastest-growing at a 9.05% CAGR.

How fast is the smart segment of the residential air purifiers market growing?

Smart/IoT-enabled purifiers are expanding at an 10.95% CAGR from 2026-2031 as connectivity features gain traction.

What is the biggest restraint on residential air purifier adoption?

High initial purchase and ongoing filter replacement costs are the main barriers, especially in price-sensitive regions.

Which companies are pursuing subscription models in the residential air purifiers market?

Samsung, LG, and Coway all offer subscription or rental programs that trade upfront hardware costs for recurring service fees.

Page last updated on: