Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.12 Billion |

| Market Size (2031) | USD 28.60 Billion |

| Growth Rate (2026 - 2031) | 28.64% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Robotic Process Automation Market Analysis by Mordor Intelligence

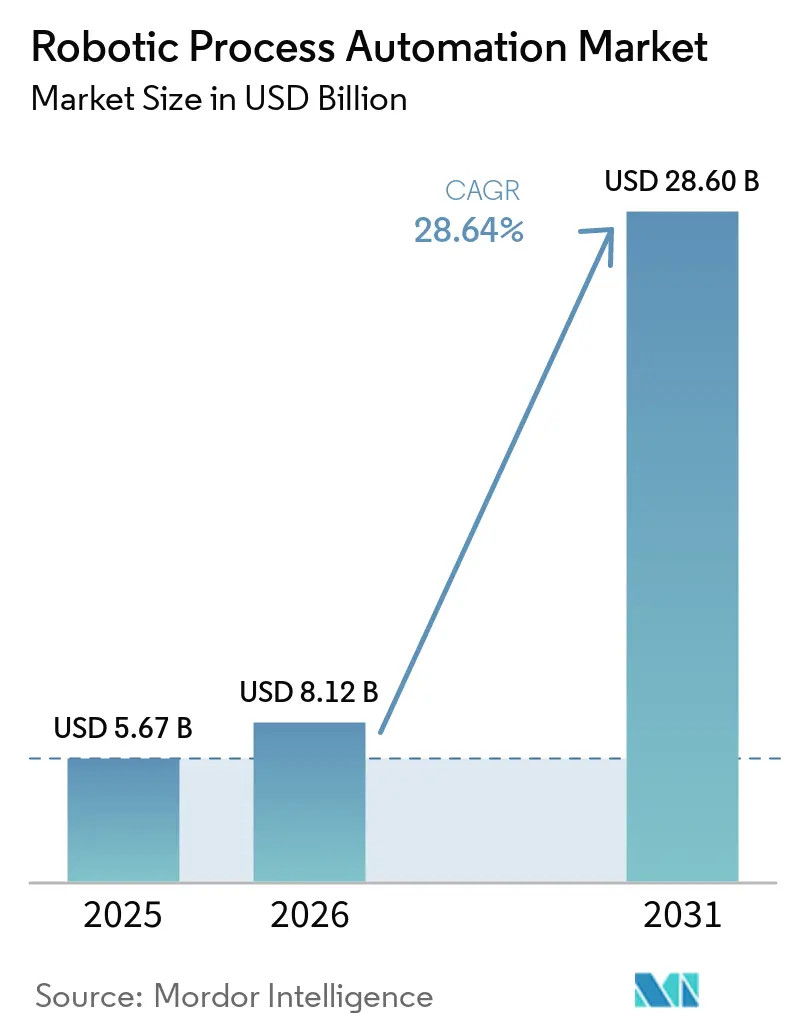

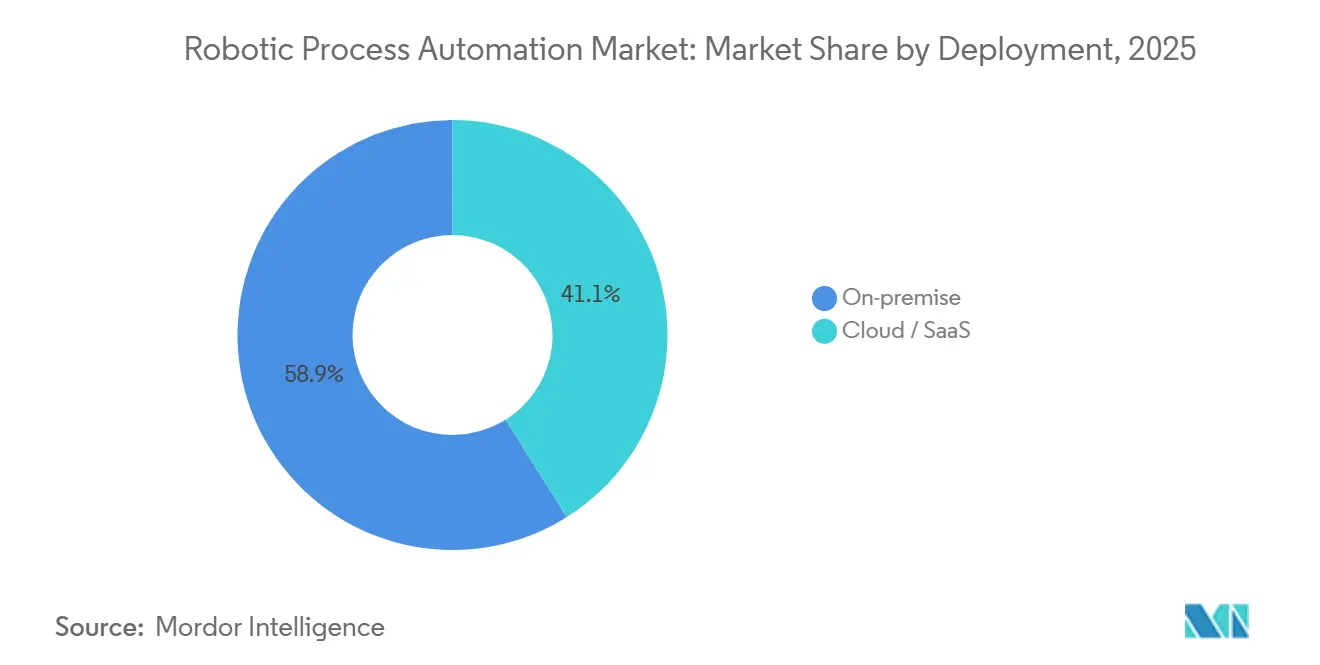

The Robotic Process Automation market size is projected to expand from USD 5.67 billion in 2025 and USD 8.12 billion in 2026 to USD 28.60 billion by 2031, registering a CAGR of 28.64% between 2026 to 2031. Rising generative-AI functions compress bot-design cycles from weeks to hours, making automation economically attractive even for short-lived processes. Pay-as-you-go licensing available on hyperscaler marketplaces lets mid-market buyers validate return on investment without committing to perpetual licenses. Compliance mandates such as the European Union’s Digital Operational Resilience Act (DORA) and heightened HIPAA enforcement in the United States obligate financial institutions and healthcare providers to maintain immutable audit trails, accelerating demand for rule-based and cognitive bots. Although on-premise deployments preserved 58.92% of 2025 revenue, cloud and SaaS models are scaling at close to the overall growth rate as vendors embed large language models directly into orchestration consoles.

Key Report Takeaways

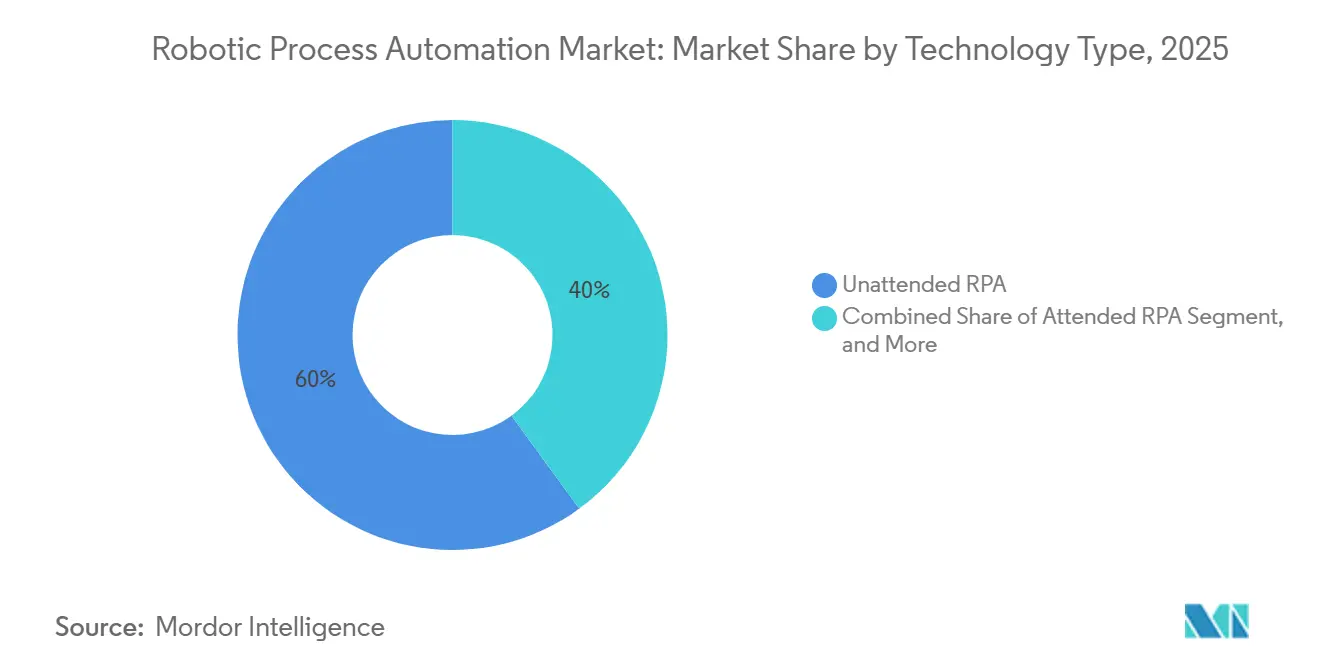

- By deployment, on-premise installations led with 58.92% of 2025 revenue, while cloud/SaaS is forecast to expand at a 29.03% CAGR through 2031.

- By solution component, software platforms captured 65.43% of 2025 spending; services are projected to grow at a 28.71% CAGR to 2031.

- By enterprise size, large enterprises accounted for 70.12% of 2025 adoption, whereas small and medium enterprises are advancing at a 28.72% CAGR.

- By technology type, unattended bots held 60.04% of 2025 revenue and intelligent RPA is set to rise at a 29.12% CAGR through 2031.

- By end-user industry, BFSI commanded 27.89% of 2025 demand; healthcare is the fastest-growing segment at a 30.89% CAGR.

- By geography, North America held 39.62% of 2025 revenue, and Asia-Pacific is positioned for a 30.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotic Process Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Retail Omni-Channel Order-Fulfillment Automation | +4.8% | Global (North America, Europe lead) | Medium term (2-4 years) |

| SME Adoption of Cloud-Native RPA Platforms | +5.2% | Global (Asia-Pacific, South America accelerate) | Short term (≤2 years) |

| Gen-AI Powered Bot-Design Assistants | +6.1% | North America, Europe lead; Asia-Pacific follows | Short term (≤2 years) |

| Pay-As-You-Go Bots on Hyperscale Marketplaces | +3.9% | Global | Medium term (2-4 years) |

| Compliance-Driven Automation Post-DORA and HIPAA | +5.4% | Europe, North America, spillover Asia-Pacific | Long term (≥4 years) |

| Global Talent Shortages in Shared-Service Centers | +4.3% | North America, Europe, India BPO hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Retail Omni-Channel Order-Fulfillment Automation

Retail margins remain under pressure as buyers expect same-day delivery, curbside pickup, and friction-free returns, driving demand in the Robotic Process Automation market. Bots bridge disparate order-management, warehouse-management, and transportation systems without forcing costly ERP re-platforming. Generative AI now summarizes unstructured customer inquiries into structured fields and predicts stock-out risks from historical sales patterns. Pre-built connectors for Shopify and leading last-mile carriers cut integration time, which favors cloud-native vendors offering subscription pricing aligned with seasonal volume spikes. The resulting faster cycle times drive measurable working-capital improvements for omnichannel retailers.

SME Adoption of Cloud-Native RPA Platforms

Historically, server procurement and specialist talent needs deterred smaller firms from adopting Robotic Process Automation solutions. Browser-based designers and subscription tiers under USD 10,000 per year now allow finance and HR managers without coding expertise to launch production bots in days. Integration of Microsoft Power Automate with Microsoft 365 brings basic attended and unattended functionality to more than 400 million commercial Office 365 users.[1]Microsoft, “Power Automate Pricing,” microsoft.com Churn risk remains higher in the SME cohort because process volatility disrupts bot scripts, yet vendors mitigate that risk with self-healing logic and template libraries.

Gen-AI Powered Bot-Design Assistants

Large language models convert natural-language prompts into workflow steps, cutting proof-of-concept time from more than eight weeks to under three. For example, UiPath Autopilot converts a plain-English request “extract invoice data and post to ERP” into an executable process in minutes.[2]UiPath, “Autopilot Product Page,” uipath.com Enterprises benefit from lower dependence on scarce RPA developers and from expanded automation backlogs supplied by business users. Sandboxing, testing, and explainability layers are gaining focus so that probabilistic AI-driven steps do not violate compliance policies.

Pay-As-You-Go Bots on Hyperscale Marketplaces

Listing bots on AWS Marketplace and similar storefronts lets buyers meter usage in the same billing cycle as their broader cloud workloads, supporting growth in the Robotic Process Automation (RPA) market. Enterprises scale capacity upward for quarter-end closes or holiday order surges, then scale down to cap cost of ownership. Transparent per-hour pricing and star ratings intensify competition among vendors, while tight integration with AWS Lambda or Azure Functions increases switching costs and fosters hyperscaler loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Bot Breakage from UI Changes | -3.2% | Global | Short term (≤2 years) |

| Governance and Ethical Scrutiny of Unattended Bots | -2.1% | Europe, North America | Medium term (2-4 years) |

| High Switching Cost from Legacy RPA Suites | -1.8% | Global | Long term (≥4 years) |

| Low Process Standardization in Emerging Markets | -2.4% | Asia-Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Bot Breakage from UI Changes

Frequent updates in ERP, CRM, and web portals alter element identifiers that bots rely on, forcing script rewrites. Surveys indicate 40% of bots need monthly maintenance, consuming up to one-fifth of automation-team capacity. Computer-vision selectors and self-healing logic reduce but do not eliminate the breakage, especially in single-page applications built on React or Angular. Downtime during repairs erodes the realized savings that justified automation budgets in the first place.

Governance and Ethical Scrutiny of Unattended Bots

Unattended bots perform high-value transactions without human supervision, raising questions about accountability when errors occur. Regulators and internal auditors require clear responsibility matrices and detailed activity logs. As cognitive components introduce probabilistic reasoning, explainability expectations rise, and high-risk tasks remain reserved for attended or human-in-the-loop models. Added governance layers slow deployment velocity and inflate compliance overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Gains as Enterprises Replatform

In 2025, on-premise deployments retained 58.92% of Robotic Process Automation market revenue because highly regulated enterprises valued data-residency control and tight integration with legacy ERP systems. North American banks and European healthcare providers frequently cite sovereign-data considerations as continuing hurdles to cloud migration. Even so, the Robotic Process Automation market size attributable to cloud subscriptions is forecast to grow at a 29.03% CAGR, helped by regional hyperscaler data centers and customer-managed encryption keys. Firms shifting workloads to AWS, Azure, or Google Cloud now favor elastically scaling automation so that bot capacity matches transaction peaks, which trims idle license costs.

Hybrid strategies dominate the medium term in the Robotic Process Automation market. Logistics firms keep bots that touch customs documents on local servers while moving invoice-processing bots into SaaS environments for global access. Vendors respond with unified consoles that orchestrate on-premise and cloud bots from a single pane of glass, making the deployment choice largely invisible to process owners. Cloud vendors, for their part, bundle pre-trained language models to read invoices or classify emails, creating incremental upsell opportunities while deepening platform stickiness. These moves steadily erode on-premise share even in conservative industries, positioning cloud as the default architecture by the end of the forecast window.

By Solution Component: Services Surge as Complexity Rises

Software licenses represented 65.43% of the Robotic Process Automation market share in 2025 because buyers initially prioritized tool acquisition to launch pilot bots quickly. As automation estates scale from a few dozen to several hundred bots, however, enterprises need governance playbooks, performance analytics, and continuous improvement roadmaps. Consequently, the services segment is projected to deliver a 28.71% CAGR to 2031, outpacing the platform segment and shifting vendor revenue mixes toward annuity consulting income.

System integrators increasingly offer outcome-based contracts that tie fees to cycle-time reductions or cost savings, aligning incentives with client value. Platform vendors are responding by acquiring boutique consultancies to bring implementation skills in-house alongside product engineering. Automation programs now span finance, HR, supply chain, and customer experience, each with distinct compliance and change-management needs. Services partners who package accelerators, pre-built bots, testing scripts, and governance templates reduce total deployment time, making them vital to realizing large-scale benefits in the Robotic Process Automation market.

By Enterprise Size: SMEs Accelerate Adoption

Large organizations consumed 70.12% of the Robotic Process Automation market in 2025, as global service-center mandates and sizable IT budgets enabled the deployment of 500–2,000 bots across multiple regions. Efforts focus on replacing repetitive finance and procurement tasks to offset talent gaps and rising wages. SMEs, however, are expected to post a 28.72% CAGR through 2031, signaling a democratization trend within the Robotic Process Automation industry.

Cloud-based subscription tiers under USD 500 per month, bundled with intuitive drag-and-drop designers, place automation within reach of finance controllers and HR managers lacking coding expertise. Early successes such as cutting invoice-matching cycles from two days to two hours generate executive sponsorship for phased expansions. Vendors capture this long-tail growth by offering free community editions, academy-style training, and marketplace-ready templates that minimize ramp-up times.

By Technology Type: Intelligent RPA Gains Share

Unattended bots dominated 60.04% of 2025 revenue because lights-out processing of reconciliations and data migrations delivers the most direct labor-elimination savings. Simultaneously, intelligent and cognitive bots are forecast to log a 29.12% CAGR, enlarging their proportion of Robotic Process Automation market size as enterprises ingest unstructured medical charts, supply-chain documents, and legal contracts.

Natural-language processing and computer-vision components route customer emails, extract bill-of-lading data, and validate shipping labels, all without human keystrokes. Convergence between attended and unattended architectures is rising: a contact-center agent might hand off a completed case to an unattended workflow that closes back-office records overnight. Unified orchestration ensures error tracking and audit trails remain centralized, strengthening the platform play for vendors that can harmonize all bot types.

By End-User Industry: Healthcare Leads Growth

BFSI entities commanded 27.89% of 2025 spending because anti-money-laundering checks, loan-origination workflows, and regulatory reporting maps well to rule-based automation. Yet healthcare is projected to post the fastest 30.89% CAGR, reflecting interoperability mandates that force payers and providers to extract and normalize electronic health record data. The Robotic Process Automation market share associated with healthcare claims processing is therefore expected to widen throughout the forecast.

Hospitals deploy bots that gather prior-authorization details, schedule patient appointments, and reconcile revenue-cycle data. Payers automate enrollment updates and claims adjudication, aided by bots that ingest 837-format data and apply policy rules. Retailers, manufacturers, telecom operators, and governments also continue to launch bots focused on inventory allocation, quality-control forms, network provisioning, and citizen-service queues, broadening the vertical reach and making cross-industry best practices more transferable.

Geography Analysis

North America generated 39.62% of 2025 Robotic Process Automation market revenue. U.S. banks use bots to streamline anti-money-laundering investigations, while healthcare payers compensate for staff shortages by automating claims adjudication and eligibility checks. Canadian financial institutions embrace bots to meet operational-resilience guidelines similar to Europe’s DORA, and Mexico’s BPO providers leverage automation to preserve competitiveness against near-shoring rivals. Although enterprise penetration exceeds 60% among Fortune 500 companies, mid-market and public-sector organizations remain under-served, sustaining double-digit regional growth potential.

Asia-Pacific is projected for a 30.72% CAGR through 2031 as India’s BPO giants bundle outcome-based automation into managed services, Japan counters demographic labor gaps with attended bots for public services, and China’s exporters automate customs and quality-control reporting for compliance with Western import regulations. Australia, South Korea, and Southeast Asian economies adopt cloud-delivered platforms as hyperscalers add regional availability zones, lowering latency and easing data-sovereignty concerns. Local-language interfaces and partnerships with regional system integrators expedite uptake among mid-sized enterprises.

Europe maintains a sizable installed base, driven by DORA-motivated investments across Germany, the United Kingdom, and France. On-premise preferences persist due to GDPR and national privacy statutes, yet sovereign cloud initiatives accelerate the shift toward SaaS. Eastern European shared-service hubs in Poland and Romania deploy bots to offset rising labor costs, mirroring earlier North American patterns. Emerging regions South America, the Middle East, and Africa account for a smaller slice of Robotic Process Automation market size but show accelerating uptake in banking, oil and gas, and public-sector digitization, often through local integrator alliances that package bots with process-standardization consulting.

Competitive Landscape

The five largest vendors UiPath Inc., Automation Anywhere Inc., SS&C Blue Prism Ltd., Microsoft Corp., and Pegasystems Inc. held major share of 2025 revenue, indicating a moderately concentrated field. Hyperscalers blur boundaries by embedding bot runtimes into broader infrastructure services, while open-source frameworks such as Robocorp introduce cost-efficient alternatives for developer-led teams. Incumbents differentiate by integrating process mining, document understanding modules, and AI co-pilots that translate plain-language requests into executable workflows, thereby reducing the total cost of ownership for clients seeking end-to-end intelligent automation.

Technology roadmaps now emphasize self-healing bots and explainable AI. UiPath patents cover computer-vision selectors that recognize visual context rather than brittle HTML tags, while Automation Anywhere invests in reinforcement-learning algorithms that optimize exception-handling pathways.[3]United States Patent and Trademark Office, "Patent Database," uspto.gov Markets are also segmenting vertically; vendors release pre-configured bots for insurance claims, pharmaceutical submissions, or telco order management, shortening deployment cycles and commanding premium pricing. Regional specialists such as EdgeVerve in India, Laiye in China, and Rocketbot in Latin America win deals where local regulatory knowledge and language support weigh heavily.

Price models shift toward consumption-based billing. Blue Prism Cloud on AWS Marketplace bills per bot-execution hour, aligning costs with transaction peaks and expanding addressable demand among risk-averse buyers. Microsoft bundles advanced RPA with Microsoft 365 E5, pressuring standalone vendors on total-suite economics. Strategic investments, like Salesforce Ventures’ USD 200 million in Automation Anywhere, underscore ecosystem integration as a competitive lever. The field therefore balances platform breadth, vertical depth, and commercial flexibility as primary vectors of differentiation.

Robotic Process Automation Industry Leaders

-

UiPath Inc.

-

Automation Anywhere Inc.

-

SS&C Blue Prism Ltd.

-

NICE Ltd. (Robotic Automation)

-

Pegasystems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: UiPath launched Autopilot for Everyone, embedding generative-AI bot design in its platform to let non-coders build automations via natural-language prompts.

- January 2026: Microsoft added Power Automate Premium features to Microsoft 365 E5 subscriptions at no extra cost, integrating attended and unattended RPA directly into Office workflows.

- December 2025: Automation Anywhere secured a USD 200 million investment from Salesforce Ventures to co-develop lead-to-cash automation connectors for Salesforce CRM instances.

- November 2025: SS&C Blue Prism unveiled consumption-based pricing on AWS Marketplace, letting users pay per bot-execution hour.

Global Robotic Process Automation Market Report Scope

The Robotic Process Automation (RPA) market is witnessing significant growth due to increasing demand for automation across various industries. Organizations are adopting RPA solutions to enhance operational efficiency, reduce costs, and improve accuracy in repetitive tasks. The integration of advanced technologies, such as artificial intelligence and machine learning, is further driving the adoption of RPA globally.

The Robotic Process Automation Report is Segmented by Deployment (On-premise, Cloud/SaaS), Solution Component (Software, Services), Enterprise Size (SMEs, Large Enterprises), Technology Type (Attended RPA, Unattended RPA, Intelligent/Cognitive RPA), End-user Industry (BFSI, IT and Telecom, Healthcare, Retail and CPG, Manufacturing, Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment

| On-premise |

| Cloud / SaaS |

By Solution Component

| Software (Platforms and Licences) |

| Services (Implementation, CoE, Support) |

By Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Technology Type

| Attended RPA |

| Unattended RPA |

| Intelligent / Cognitive RPA |

By End-user Industry

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and CPG |

| Manufacturing |

| Other End-user Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment | On-premise | |

| Cloud / SaaS | ||

| By Solution Component | Software (Platforms and Licences) | |

| Services (Implementation, CoE, Support) | ||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

| By Technology Type | Attended RPA | |

| Unattended RPA | ||

| Intelligent / Cognitive RPA | ||

| By End-user Industry | BFSI | |

| IT and Telecom | ||

| Healthcare | ||

| Retail and CPG | ||

| Manufacturing | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Robotic Process Automation market by 2031?

Forecasts indicate the market will reach USD 28.60 billion by 2031, rising from USD 8.12 billion in 2026.

Which deployment model is growing fastest within Robotic Process Automation?

Cloud and SaaS subscriptions are projected to grow at a 29.03% CAGR between 2026 and 2031 as enterprises replatform to hyperscaler clouds.

Why is healthcare the fastest-growing vertical for RPA?

Interoperability mandates and administrative backlogs push payers and providers to automate claims, prior-authorizations, and EHR data extraction, driving a 30.89% CAGR.

How do generative-AI copilots impact automation economics?

Language models now translate plain-English prompts into executable workflows, cutting proof-of-concept cycles from several weeks to a few days and lowering development costs.

What regions offer the highest growth potential outside North America?

Asia-Pacific leads with a forecast 30.72% CAGR, fueled by India’s BPO sector and China’s export-oriented manufacturers automating compliance and documentation tasks.

Page last updated on: