Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

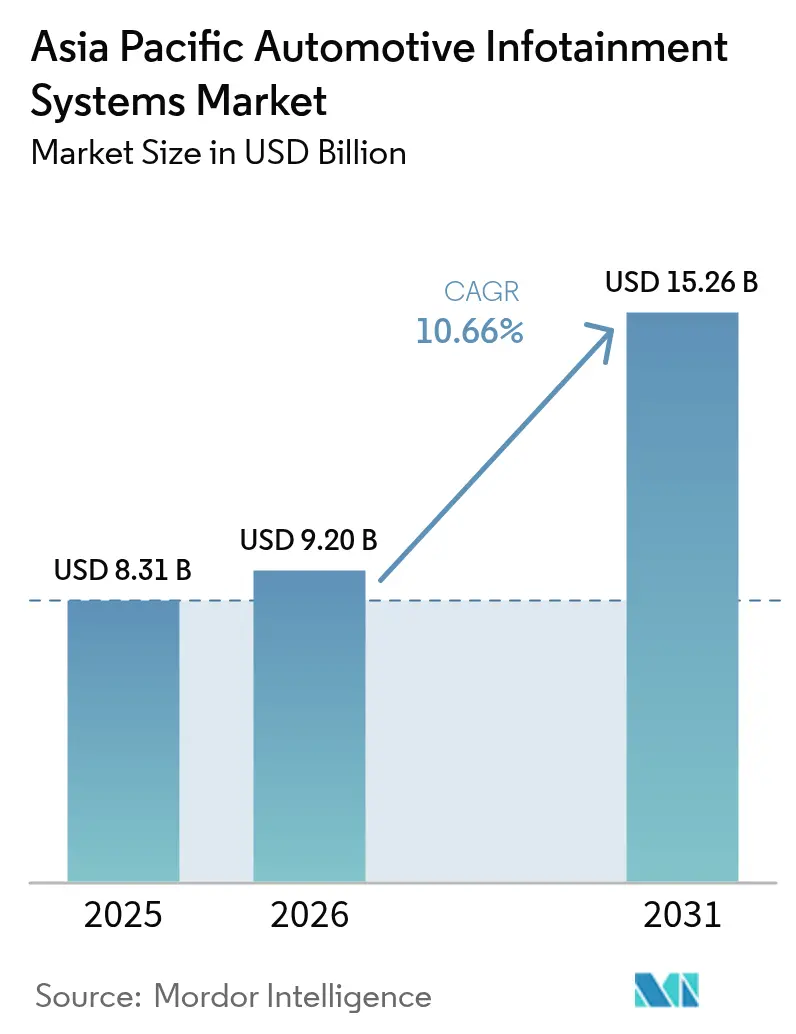

| Base Year Market Size (2025) | USD 8.31 Billion |

| Market Size (2026) | USD 9.2 Billion |

| Market Size (2031) | USD 15.26 Billion |

| Growth Rate (2026 - 2031) | 10.66% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia Pacific Automotive Infotainment Systems Market Analysis by Mordor Intelligence

The Asia-Pacific Automotive Infotainment System market size was valued at USD 8.31 billion in 2025 and estimated to grow from USD 9.2 billion in 2026 to reach USD 15.26 billion by 2031, at a CAGR of 10.66% during the forecast period (2026-2031). Growth stems from rising connected-car penetration, fast 4G-to-5G migration, and the pivot toward software-defined cockpits that monetize over-the-air upgrades. Hardware is commoditizing, so recurring revenue from app stores, navigation subscriptions, and feature unlocks is now central to OEM strategy. China anchors demand yet faces share dilution as India and ASEAN scale entry-level electrification, while regulatory mandates for eCall and telematics compress life cycles for non-connected head units. Competitive dynamics are shifting as tech platforms extend Android Automotive OS, Automotive Grade Linux, and bespoke cloud services directly into vehicle programs, eroding the historical moat of tier-one suppliers.

Key Report Takeaways

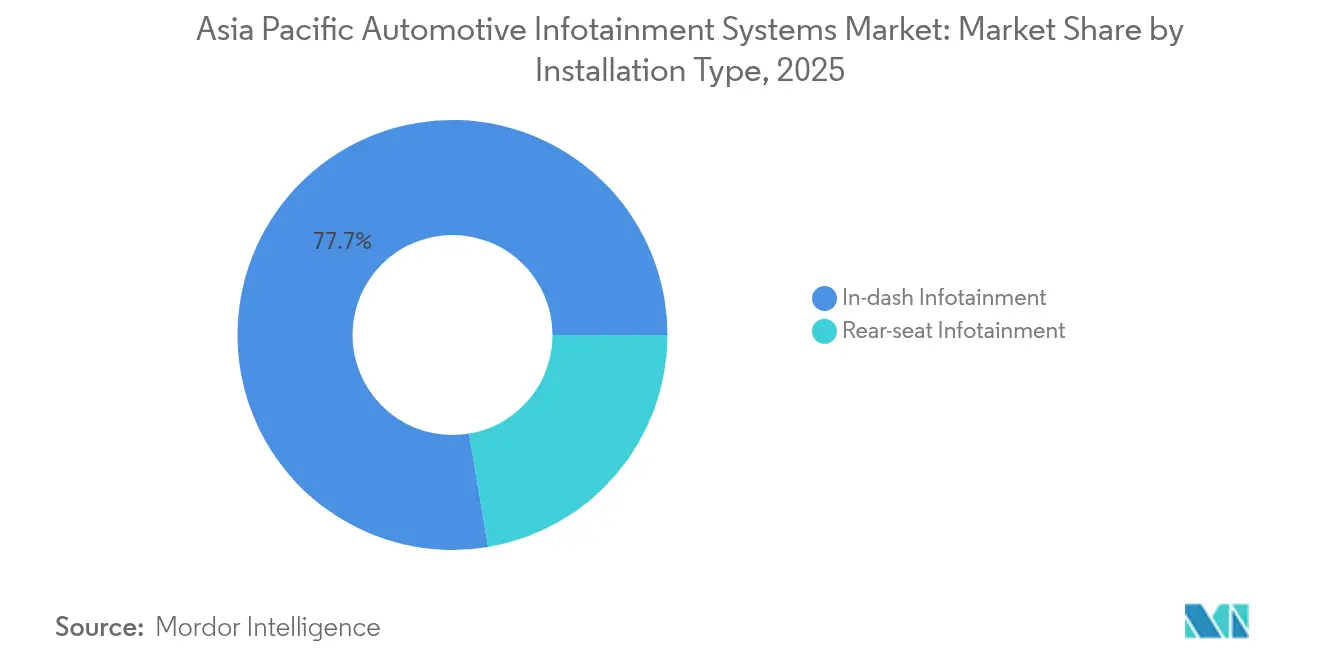

- By installation type, in-dash infotainment led with 77.65% revenue share in 2025, while rear-seat systems are projected to expand at a 12.04% CAGR through 2031.

- By vehicle type, passenger cars accounted for 71.78% of the Asia-Pacific Automotive Infotainment System market share in 2025, whereas light commercial vehicles are forecasted to grow at a 11.55% CAGR through 2031.

- By component, displays and touchscreens captured a 43.28% share of the Asia-Pacific Automotive Infotainment System market size in 2025, and operating-system software, along with apps, is advancing at a 13.18% CAGR during the outlook period.

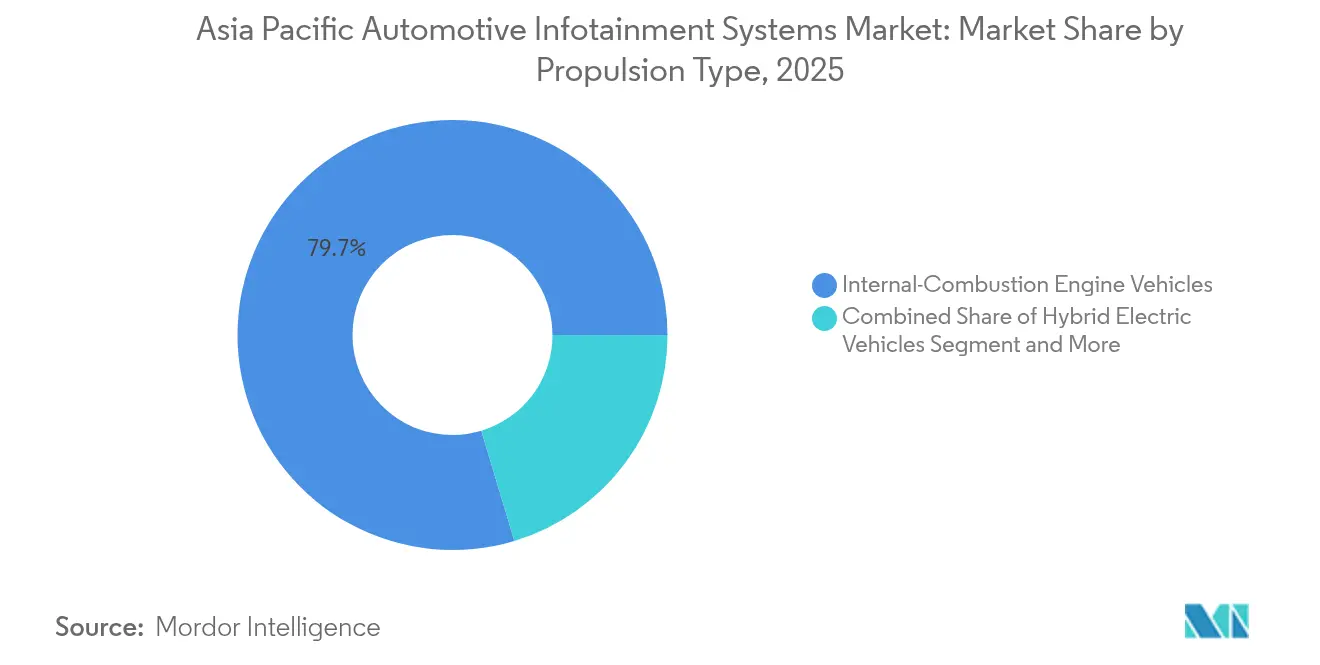

- By propulsion type, internal-combustion engine vehicles accounted for 79.65% of installations in 2025, while battery electric vehicles are set to increase at a 13.62% CAGR through 2031.

- By connectivity generation, 4G LTE commanded 60.62% share in 2025, whereas 5G connectivity is rising at a 13.05% CAGR toward 2031.

- By operating system, Linux-based platforms secured a 46.85% share in 2025, while Android Automotive OS is expected to expand at a 12.01% CAGR to 2031.

- By sales channel, OEM-installed systems dominated with an 82.85% revenue share in 2025; however, aftermarket solutions are projected to post a 11.91% CAGR during the same period.

- By country, China captured 48.35% of the Asia-Pacific Automotive Infotainment System market share in 2025, while India is forecast to expand at a 12.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Automotive Infotainment Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Connected-Car Services | +2.3% | China, India, South Korea | Medium term (2-4 years) |

| Shift to OTA-Upgradeable Software-Defined Vehicles | +2.1% | China, Japan, South Korea, Australia | Medium term (2-4 years) |

| OEM–Tech Giant Platform Partnerships | +1.9% | China, Japan, South Korea | Short term (≤2 years) |

| Regulatory Mandates for eCall and Telematics | +1.6% | Japan, South Korea, China, India | Long term (≥4 years) |

| Low-Cost SoC Penetration in Entry-Level Cars | +1.4% | India, China | Short term (≤2 years) |

| Localized OTT and Navigation Ecosystems | +1.1% | India, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Connected-Car Services

Fleet operators and ride-hailing aggregators now view infotainment as a critical tool for enhancing operational efficiency rather than a mere cabin luxury. The integration of telematics enables more efficient routing, provides insights into driver behavior, and supports predictive maintenance, all of which contribute to noticeable reductions in fuel consumption. In markets such as India and South Korea, usage-based insurance pilots are encouraging the adoption of connectivity-enabled head units by offering tailored incentives. Furthermore, the use of cloud-based traffic prediction has streamlined operations by eliminating the need for embedded maps, thereby reducing the overall Bill of Materials (BOM) and improving cost efficiency.

Shift to OTA-Upgradeable, Software-Defined Vehicles

In 2024, Volkswagen Group China introduced over-the-air (OTA) updates for a significant number of vehicles [1]"Intelligent and Fully Connected Vehicles", Volkswagen Group China, volkswagengroupchina.com.cn. At the same time, Hyundai and Kia plan to extend OTA updates to the majority of their upcoming models for the following year. Furthermore, BMW's iDrive 9.0 incorporates hypervisors to enable independent updates for cockpit systems. These advancements in faster iteration cycles are driving growth in subscription-based revenue streams while simultaneously reducing costs associated with vehicle recalls.

OEM–Tech Giant Platform Partnerships

Toyota has integrated Tencent's WeChat voice messaging into its models manufactured in China. Nissan is utilizing Baidu's Apollo APIs to effectively merge advanced driver-assistance systems (ADAS) and entertainment features through unified domain controllers. At the same time, LG Electronics and MediaTek are focusing on expanding their presence in the automotive market by offering a comprehensive webOS-Dimensity stack designed specifically for tier-two original equipment manufacturers (OEMs), aiming to achieve significant adoption in the years to come [2]“webOS Automotive partnership announcement,”, LG Electronics, lg.com.

Low-Cost SoC Penetration in Entry-Level Cars

Qualcomm's Snapdragon Auto 4100 and MediaTek's MT8676 have significantly reduced infotainment BOM costs, making it more affordable for entry-level cars in India to include touchscreen features. This advancement has enabled Tata Motors to integrate the platform into its Tiago and Punch models during the current year. At the same time, NXP's i.MX 8 has become a preferred choice in China's automotive market, particularly for budget-friendly vehicles within the lower price range.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM Cost in Price-Sensitive Markets | -1.7% | India, China tier-3 | Short term (≤2 years) |

| Software Fragmentation and Cybersecurity Risks | -1.3% | Global, esp. China, India | Medium term (2-4 years) |

| Patchy 5G Coverage Outside Metro Areas | -1.0% | India, rural China | Long term (≥4 years) |

| Head-Unit Shortages from Chip Supply Shocks | -0.9% | Japan, South Korea, Australia, China | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High BOM Cost in Price-Sensitive Markets

Display modules, connectivity ICs, and SoCs account for a major portion of the infotainment bill of materials. Due to cost constraints in India's mass-market cars, original equipment manufacturers are compelled to ship head units with simplified features to maintain affordability. Furthermore, import tariffs imposed by ASEAN countries significantly increase the overall cost of semiconductors. Meanwhile, local manufacturing capabilities in India remain limited, focusing primarily on the production of wiring harnesses and performing basic assembly tasks.

Patchy 5G Coverage Outside Metro Areas

5G services in India expanded significantly, covering numerous cities; however, rural areas saw minimal progress, with coverage remaining limited [3]"5G BTS Deployed", Department of Telecommunications, dot.gov.in. Similar challenges persist in Indonesia and Vietnam, where gaps in network expansion restrict the monetization of advanced services such as cloud navigation and HD streaming. These limitations reduce consumer interest in subscribing to premium plans, thereby impacting revenue potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Rear-Seat Systems Gain Traction

Rear-seat entertainment revenue is climbing at 12.04% CAGR, even as in-dash units dominated 77.65% of 2025 sales. Curved multi-zone displays from Continental reduce wiring weight and enable independent streaming for passengers. Chauffeur-driven cultures in China and South Korea accelerate demand, whereas cost-sensitive India and ASEAN remain in-dash centric. Premium EV brands, such as NIO, now bundle rear-seat screens as a baseline, moving a former luxury feature into mid-segment expectations.

Greater cabin screen real estate supports targeted advertising, unlocking fresh revenue for OEM app stores. The Asia-Pacific Automotive Infotainment System market, therefore, sees rear-seat uptake influencing supplier roadmaps toward modular domain controllers that independently power multiple displays—a critical differentiation frontier heading to 2031.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars account for 71.78% of revenue, yet they are pivoting to subscription models for navigation and ADAS upgrades. Light commercial vehicles deliver 11.55% CAGR, leveraging telematics-enabled infotainment for route optimization and driver analytics. Mahindra’s Treo Zor embeds fleet APIs accessible via cabin touchscreens, illustrating how logistics operators convert infotainment into a mission-critical dashboard.

Fleet buyers prioritize uptime and TCO, so ruggedized screens, remote diagnostics, and FOTA are vital. OEMs offer tiered SaaS plans that are packaged at the time of purchase, locking in multi-year data contracts. The Asia-Pacific Automotive Infotainment System market accrues incremental recurring revenue beyond the showroom, underpinning strategic focus on LCVs for suppliers.

By Component: Software Margins Eclipse Hardware

Displays secured a 43.28% value share in 2025, as OLEDs replace LCDs in premium tiers. Samsung Display’s 100,000:1-contrast automotive OLED enables augmented-reality overlays and microsecond response times. Yet, operating-system software and apps lead growth at a 13.18% CAGR, signaling a margin migration.

Domain controllers now integrate cockpit, cluster, and rear-seat logic into a single SoC, significantly reducing the bill of materials. With the shift to subscription-based economics, original equipment manufacturers retain a larger share of app-store revenues compared to traditional phone platforms. Consequently, the Asia-Pacific Automotive Infotainment System market increasingly benefits suppliers that adapt from focusing solely on hardware delivery to offering end-to-end software lifecycle services.

By Propulsion Type: BEVs Demand Integrated Ecosystems

Battery electric vehicles will expand at a 13.62% CAGR. BYD’s DiLink embeds charging-network APIs and range-optimized routing, improving efficiency. BEV infotainment doubles as a vehicle-control panel, replacing physical buttons with haptic-feedback screens.

ICE models focus on cost-efficient navigation and media. Hybrid cars sit between, displaying power-flow diagrams that educate drivers. The Asia-Pacific Automotive Infotainment System market supports unique UI-UX paths per propulsion archetype, challenging suppliers to design adaptable software layers.

By Connectivity Generation: 5G Rollout Accelerates

4G LTE still leads with 60.62% share in 2025, yet 5G connectivity climbs 13.05% CAGR on HD maps and V2X demand. RedCap 5G modules trim cost and power, making next-gen modems viable for mid-tier segments.

Premium marques leverage 5G low-latency streaming and cloud gaming in China, Japan, and South Korea. India follows swiftly as telecoms subsidize in-vehicle data to stimulate network usage. The Asia-Pacific Automotive Infotainment System market thus expects 5G share to overtake 4G near 2028, subject to rural coverage build-out.

By Operating System: Android Automotive OS Gains Momentum

Linux stacks account for 46.85% share, with Android Automotive OS tracking 12.01% CAGR. Hyundai and Google plan to deploy 20 million vehicles by 2030, mainstreaming native Google Maps, Assistant, and Play Store features. QNX remains indispensable for safety-critical clusters, leading to hybrid architectures where QNX governs real-time tasks and Android handles infotainment.

Chinese OEMs advance domestic platforms like Banma AliOS, reflecting their sovereignty goals, yet the app ecosystem depth lags behind Android. The Asia-Pacific Automotive Infotainment System market, therefore, exhibits a dual-track between open global ecosystems and protected regional stacks.

By Sales Channel: Aftermarket Retrofits Aging Fleets

OEM factory fitment accounts for 82.85% of sales, but aftermarket demand grows at a 11.91% CAGR as Japan and Australia retrofit vehicles built before 2018 with wireless CarPlay and Android Auto. Pioneer and Alpine expand 7-9 inch screen product lines to serve older fleets.

Complex wiring and warranty concerns restrict do-it-yourself installs, so professional channels flourish. OEM systems retain seamless integration with steering-wheel buttons and ADAS data buses. The Asia-Pacific Automotive Infotainment System market supports coexistence, as factory systems cater to new-car buyers, while aftermarket solutions extend the digital life of legacy vehicles.

Geography Analysis

China supplied 48.35% of 2025 regional revenue on the back of the world’s largest auto market and rapid electrification. Proprietary smart-cockpit platforms from BYD, NIO, and Xpeng integrate voice assistants, over-the-air updates, and payment apps, cementing software-defined differentiation. Mandatory GB standards, practical in 2026, further accelerate connected upgrades.

India is the fastest-growing geography at 12.49% CAGR through 2031, fueled by localization mandates and low-cost SoCs from Qualcomm and MediaTek. Tata Motors offers sub-$200 touchscreens in entry-level cars, expanding the addressable volume. Draft telematics legislation poised for 2025 will mandate emergency-call functions, driving another retrofit wave.

Japan and South Korea exhibit slower overall growth, but a high density of innovation. Sony Honda Mobility’s Afeela EV centers offer more than horsepower, signaling a future of infotainment-driven value propositions. Hyundai Mobis invests in holographic HUDs and AR navigation for luxury lines. Australia, with an aging fleet, stimulates aftermarket installations.

Competitive Landscape

Traditional tier-one players, such as Panasonic, Harman, Denso, Bosch, and Continental, collectively dominate a significant portion of the market revenue. However, their stronghold on hardware is increasingly under threat as OEMs shift toward ecosystems developed by technology leaders such as Google, Alibaba, and Tencent. For instance, Hyundai is advancing its plans with Android Automotive OS, while LG-MediaTek's webOS platform is also gaining traction; each aims to integrate its systems into millions of vehicles, effectively bypassing conventional supply chains.

Smaller engineering firms, including ThunderSoft and Tata Elxsi, are gaining momentum by offering customized open-source solutions tailored to the needs of budget-conscious OEMs. In this evolving landscape, cybersecurity has emerged as a critical differentiator. Companies like BlackBerry QNX and Aptiv are incorporating advanced features, such as secure boot and intrusion detection, into their architectures to comply with ISO/SAE 21434 standards. Additionally, segments like commercial-vehicle telematics and aftermarket retrofits present significant growth opportunities, as established players often lack the specialized focus required to address these areas effectively.

In the current market, factors such as cost efficiency, software flexibility, and the ability to offer a comprehensive ecosystem have become more critical than traditional considerations, including display resolution and CPU performance. Consequently, the Asia-Pacific Automotive Infotainment System market is increasingly favoring suppliers who evolve from being mere hardware providers to becoming integrators of robust and versatile platforms.

Asia Pacific Automotive Infotainment Systems Industry Leaders

-

Panasonic Corporation

-

Harman International Inc.

-

Robert Bosch GmbH

-

Visteon Corporation

-

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Harman, a subsidiary of Samsung Electronics, is investing INR 3.45 billion (USD 42 million) to bolster its automotive electronics manufacturing facility in Chakan, Pune, India. By 2027, this expansion will enable the plant to produce annually four million car audio components, 1.4 million infotainment units, and 0.8 million telematics control units.

- October 2025: Maruti Suzuki India has integrated Bosch Mobility's locally developed Smartplay Pro X Touchscreen Infotainment System into its new Victoris SUV model. This 10.1-inch Android-based system, proudly built in India, boasts features like Dolby Atmos 5.1 surround sound, the Alexa Auto voice assistant, an integrated surround view camera, wireless CarPlay and Android Auto, over-the-air software updates, an app store with over 35 applications, and various vehicle control and connectivity functions.

Asia Pacific Automotive Infotainment Systems Market Report Scope

The Asia Pacific Automotive Infotainment System covers all the latest trends and technological developments in the Automotive Infotainment System, demand of the installation type, products type, vehicle type, countries and market share of major automotive infotainment system manufacturers across the Asia Pacific region.

By Installation Type

| In-dash Infotainment |

| Rear-seat Infotainment |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Component

| Display / Touch-screen Module |

| Head Unit / Domain Controller |

| Operating-System Software and Apps |

| Connectivity ICs and Antenna Modules |

By Propulsion Type

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

By Connectivity Generation

| 4G LTE |

| 5G |

| Legacy 2G/3G |

By Operating System

| Linux-Based (AAOS, AGL, etc.) |

| QNX |

| Android Automotive OS |

| Others (Proprietary, RTOS) |

By Sales Channel

| OEM-Installed |

| Aftermarket |

By Country

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Installation Type | In-dash Infotainment |

| Rear-seat Infotainment | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| By Component | Display / Touch-screen Module |

| Head Unit / Domain Controller | |

| Operating-System Software and Apps | |

| Connectivity ICs and Antenna Modules | |

| By Propulsion Type | Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| By Connectivity Generation | 4G LTE |

| 5G | |

| Legacy 2G/3G | |

| By Operating System | Linux-Based (AAOS, AGL, etc.) |

| QNX | |

| Android Automotive OS | |

| Others (Proprietary, RTOS) | |

| By Sales Channel | OEM-Installed |

| Aftermarket | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and forecast for the Asia-Pacific Automotive Infotainment System market?

The Asia-Pacific Automotive Infotainment System market size is USD 9.2 billion in 2026 and is projected to reach USD 15.26 billion by 2031, growing at a 10.66% CAGR.

How are OEMs partnering with tech giants?

Automakers such as Hyundai and Toyota integrate Android Automotive OS, Google Maps, and Tencent WeChat to shorten development cycles and access mature app ecosystems.

Which vehicle segment is driving commercial-fleet growth?

Light commercial vehicles are growing at 11.55% CAGR, as last-mile delivery operators adopt telematics-enabled infotainment for route optimization and driver monitoring.

Why is software revenue outpacing hardware?

Operating-system software and apps expand at 13.18% CAGR, as OEMs monetize subscriptions, over-the-air updates, and app-store revenue that hardware alone cannot deliver.

Page last updated on: