Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

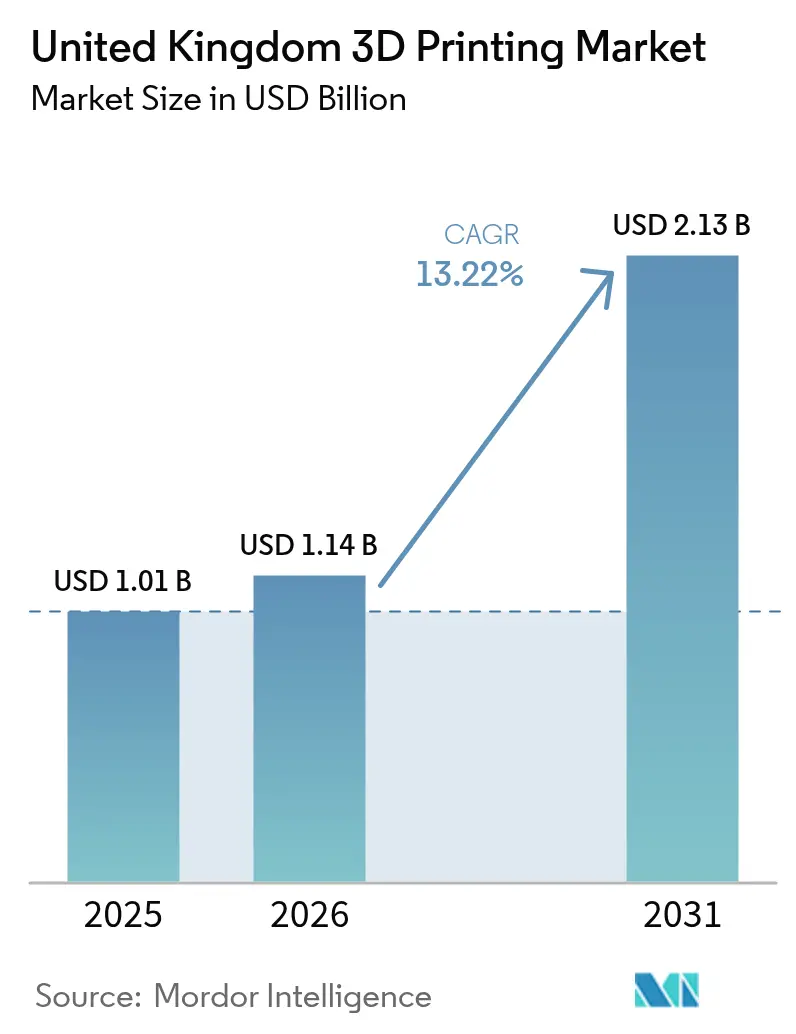

| Base Year Market Size (2025) | USD 1.01 Billion |

| Market Size (2026) | USD 1.14 Billion |

| Market Size (2031) | USD 2.13 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom 3D Printing Market Analysis by Mordor Intelligence

The United Kingdom 3D printing market size was valued at USD 1.01 billion in 2025 and estimated to grow from USD 1.14 billion in 2026 to reach USD 2.13 billion by 2031, at a CAGR of 13.22% during the forecast period (2026-2031). Strong government grants, defense‐linked on-site metal printing mandates, and an NHS pathway for hospital-based device fabrication form the core growth engine. Industrial customers continue to dominate purchases, but rapidly improving desktop hardware and additive-ready design software are widening the addressable user base. Certified titanium and aluminum powders keep aerospace demand high, while fast-moving ceramic applications are opening diversification opportunities. Parallel skills initiatives and Net-Zero regulations reinforce adoption momentum across automotive, rail, and renewable-energy supply chains.[1]UK Government, “Made Smarter Innovation: Digital Manufacturing,” GOV.UK

Key Report Takeaways

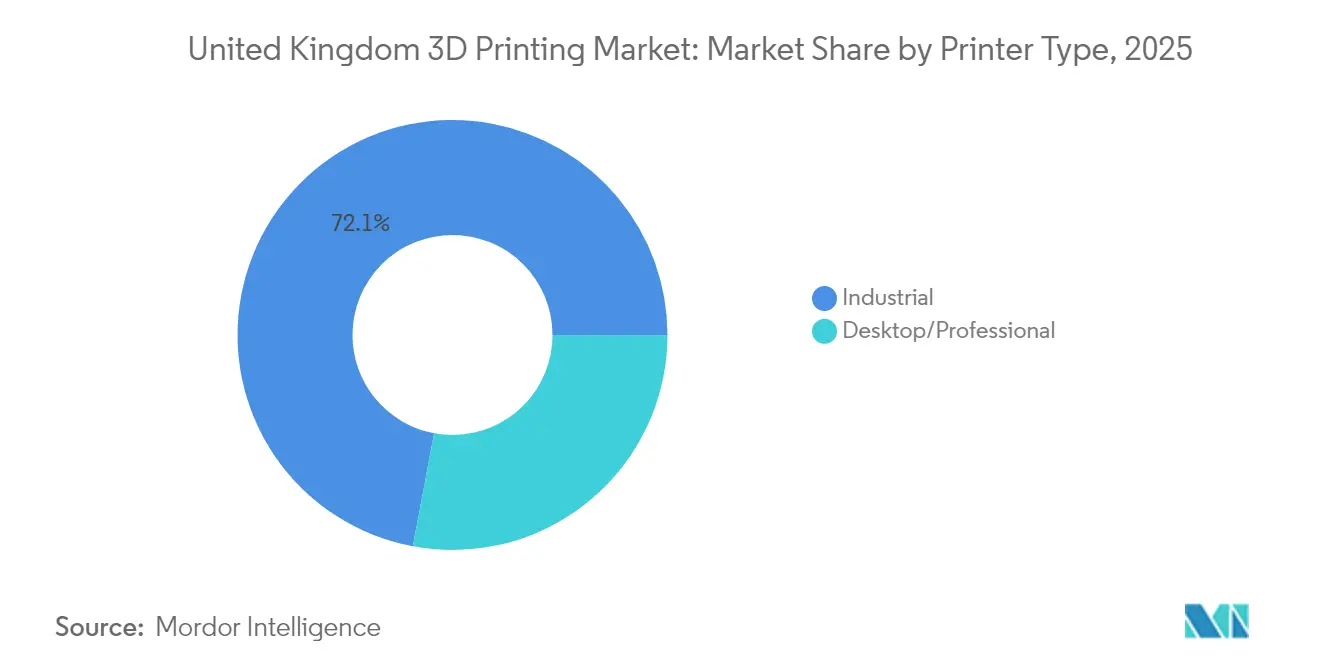

- By Printer Type, Industrial printer systems led with 72.05% of United Kingdom 3D printing market share in 2025, while desktop and professional systems are projected to clock the fastest 14.21% CAGR through 2031.

- By Material Type, Metal materials commanded 50.35% share of the United Kingdom 3D printing market size in 2025; ceramic materials are slated to rise at a 14.56% CAGR to 2031.

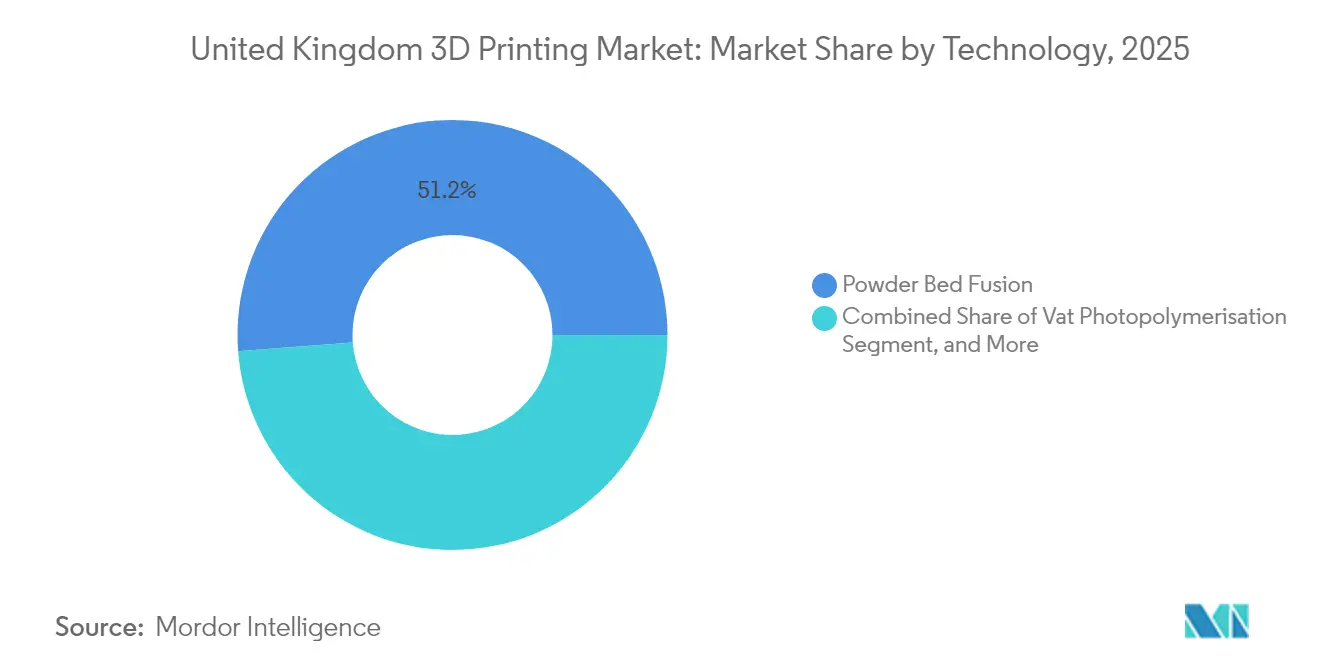

- By Technology, Powder bed fusion secured 51.20% share of the United Kingdom 3D printing market size in 2025, whereas vat photopolymerization shows the strongest 14.88% CAGR outlook.

- By Application, Aerospace and defense retained 32.68% United Kingdom 3D printing market share in 2025, yet healthcare and medical devices are expanding at a 15.05% CAGR.

- By Region, England accounted for 68.95% of the United Kingdom 3D printing market size in 2025; Northern Ireland is advancing at a 14.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom 3D Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government grants accelerate industrial adoption | +2.1% | National (England and Scotland hubs) | Medium term (2-4 years) |

| Surging demand for large-format industrial printers | +1.8% | England and Scottish manufacturing clusters | Short term (≤ 2 years) |

| NHS framework for hospital-based medical printing | +1.5% | National, early focus in England | Medium term (2-4 years) |

| Ministry of Defence offset clauses for on-site metal AM | +1.3% | National defense corridors | Long term (≥ 4 years) |

| Net-Zero regulations drive lightweight lattice parts | +1.1% | Nationwide automotive and aerospace hubs | Long term (≥ 4 years) |

| Rise of digital spares marketplaces in rail and defense | +0.9% | National networks and depots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government grants accelerate industrial adoption

Made Smarter Innovation and Innovate UK programs make capital equipment grants contingent on commercial deployment within 18 months, compressing payback horizons and de-risking first-time purchases. By 2024, Innovate UK committed GBP 78 million (USD 98.5 million) to additive manufacturing projects that span automotive tooling, certified flight parts, and hospital devices. The Aerospace Technology Institute’s matching funds reduce certification costs for powder bed fusion components, encouraging prime contractors to qualify full assemblies rather than single parts. Grant conditions also require detailed skills transfer plans, pushing equipment vendors to bundle training with every sale. As a result, small and medium enterprises secure industrial-grade printers that were previously out of reach, widening the supplier base for Tier-1 manufacturers.[2]UK Government, “Innovate UK: Advanced Manufacturing Supply Chain Initiative,” GOV.UK

Surging demand for large-format industrial printers

Automotive toolmakers and architecture studios increasingly request cubic-meter build volumes to consolidate multicomponent jigs into single prints. Large-format systems such as the BigRep ONE enable production of bumper molds, HVAC ducts, and casting patterns in a single overnight run, reducing fixture lead time by up to 70% and slashing transport-related emissions. English and Scottish clusters are adopting these platforms first because of co-located composite shops and foundries that can immediately consume the printed tooling. Equipment leasing models, aided by accelerated tax allowances, support rapid fleet expansion for service bureaus.

NHS framework for hospital-based medical printing

The MHRA-endorsed pathway allows ISO 13485-accredited hospital labs to print surgical guides, maxillofacial implants, and prosthetics without per-device regulatory submissions. Early pilots at major English trusts trimmed device turnaround from four weeks to less than twenty-four hours and lowered unit costs by 60-80%. Resulting clinical success stories drive copycat adoption in Scotland and Wales. Materials suppliers benefit from steady volumes of photopolymers and PEEK filament certified for in-situ sterilization, while software vendors capture revenue from patient-specific modeling modules.

Ministry of Defence offset clauses for on-site metal AM

Defense contracts now oblige primes to integrate live metal powder bed fusion cells within production lines, ensuring secure, on-demand spares. The LAMDA project injected GBP 15 million (USD 18.9 million) into certifying titanium and aluminum alloys for flight-critical parts, accelerating qualification by harmonizing test protocols across air, land, and sea systems. Tier-1 suppliers like BAE Systems run 24-hour AM bays that also serve civil customers, unlocking economies of scale. Powder producers secure long-term volume contracts, stabilizing local supply and reducing import dependency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex and OPEX of metal systems | -1.9% | Nationwide industrial regions | Short term (≤ 2 years) |

| Skills shortage in design-for-additive and QC | -1.6% | Scotland and Northern England | Medium term (2-4 years) |

| Metal-powder price volatility post-Ukraine conflict | -1.2% | National titanium and alloy markets | Short term (≤ 2 years) |

| IP liability uncertainty for on-demand parts | -0.8% | Service providers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High cap-ex and OPEX of metal systems

Production-class metal printers cost GBP 500,000–2 million (USD 631,000–2.5 million) and demand parallel investment in heat treatment, machining, and non-destructive testing. Metal powder, often 30–40% of total part cost, escalated 25–30% in 2024 amid supply shocks. SMEs struggle to pencil profitability without batch volumes that aerospace programs rarely offer. Leasing pools and shared hubs ease entry but introduce scheduling friction and IP leakage fears. Equipment makers now bundle closed-loop powder handling and in-chamber monitoring to shrink operating expense, yet breakeven horizons remain two to four years for most adopters.[3]Renishaw plc, “Financial Reports: Additive Manufacturing Division,” RENISHAW.COM

Skills shortage in design-for-additive and QC

Topology optimization, support design, and in-process inspection remain scarce competencies. The High Value Manufacturing Catapult highlights a two- to three-year lag before new graduates attain production-level proficiency. Industry responds with joint curricula: Renishaw funds additive modules at UK universities, while Skills England underwrites fast-track certifications for displaced machinists. Nevertheless, limited instructor capacity slows cohort throughput, capping short-term scaling potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Industrial systems hold the lead yet accessible desktops narrow the gap

Industrial machines captured 72.05% United Kingdom 3D printing market share in 2025 as government subsidies favor production-grade hardware and as Tier-1 aerospace OEMs expanded certified lines. Desktop and professional platforms, though smaller, are climbing at a 14.21% CAGR because colleges and micro-businesses now justify in-house validation prints that compress design cycles. The United Kingdom 3D printing market size for desktop systems is projected to almost double by 2031, helped by sub-USD 10,000 resin machines that approach medical-grade accuracy.

Hybrid offerings blur categories: mid-sized gantry printers bundle industrial motion control with desktop-style UI, offering line changeover in minutes rather than hours. Vendors court education customers with subscription models that combine hardware, slicer updates, and curriculum content, ensuring sticky annual revenue. In parallel, industrial fleet operators add robot-assisted depowdering to scale throughput, minimizing labor dependencies that previously capped utilization.

By Material Type: Metals dominate but ceramic momentum rises

Metal powders delivered 50.35% of 2025 revenue, anchored in titanium and aluminum alloys for defense airframes and civil engine components. The United Kingdom 3D printing market size for metals benefits from multi-year framework agreements that shelter end users from spot price spikes. Ceramics, however, post the fastest 14.56% CAGR as dental crowns, semiconductor packages, and thermal-shock-resistant tooling shift from subtractive routes to binder-jet and stereolithography options.

Polymer filaments and resins sustain prototyping demand and enter functional roles through carbon-fiber-filled grades that replace machined aluminum fixtures. Composite pellets for large-format printers gain share in automotive jigs as OEMs target five-day concept-to-fit timelines. Powder suppliers invest in local atomization lines to derisk import reliance, while ceramic feedstock players exploit readily available raw minerals, smoothing price curves relative to metals.

By Technology: Powder bed fusion retains authority amid photopolymer surge

Powder bed fusion held 51.20% of the 2025 value, reflecting widespread qualification across Rolls-Royce engines and NHS cranial implants. Tight layer control and 30 µm laser spot sizes secure the dimensional stability required for safety-critical geometries. Vat photopolymerization, racing ahead at a 14.88% CAGR, dominates dental aligners and jewelry masters where surface finish trumps tensile strength.

Material extrusion remains the entry point for vocational schools testing design iteration, while binder jetting gains traction for stainless steel pumps that favor speed over ultimate tensile. Directed energy deposition, though niche, underpins in-situ repair of turbine blades at RAF bases, cutting aircraft downtime. Equipment roadmaps converge toward multi-process workcells that seamlessly alternate deposition and five-axis milling, promising single-setup part realisation.

By Application: Healthcare growth nibbles at aerospace lead

Aerospace and defense still account for 32.68% revenue, due to backlog conversions and export engine programs. Yet the United Kingdom 3D printing market size in healthcare is accelerating at 15.05% CAGR as MHRA guidance legitimizes point-of-care manufacturing. Patient-specific cranial plates, scoliosis braces, and surgical drill guides illustrate the breadth of medical uptake.

Motorsport outfits leverage AM for race-weekend iterations, validating wind-tunnel tweaks overnight. Rail operators print cab components for legacy fleets, avoiding twelve-month tooling waits. Construction pilots explore concrete printing for complex staircases, although regulatory codes slow broad adoption. Consumer electronics brands toy with conductive polymer traces for integrated antenna housings, indicating future diversification.

Geography Analysis

England contributed 68.95% of the 2025 spend due to Midlands aerospace clusters, West Midlands automotive plants, and London’s access to venture finance. England remains the nucleus of additive activity, hosting Jaguar Land Rover’s tooling centers, Rolls-Royce’s lattice flight-part line, and Renishaw’s headquarters. Regional Made Smarter offices shepherd more than 60% of funded projects inside England, especially across the Midlands, where apprenticeship pipelines are deepest. Financial institutions in London structure equipment leases at competitive rates, boosting adoption among supply-chain SMEs.

Scotland combines offshore energy heritage with aerospace R&D to build a balanced AM portfolio. Aberdeen yards print corrosion-resistant valve components for subsea kits, mitigating extended North Sea downtime. Glasgow’s innovation district attracts photopolymer startups that cater to the city’s dental labs. Government support arrives via zero-interest loans pegged to job-creation targets, accelerating machine installs at SMEs.

Wales exploits its automotive lineage, where composite-laden FDM jigs cut Aston Martin fixture costs by 30%. Cardiff University’s research hub feeds graduates to local contract printers. Northern Ireland’s 14.72% CAGR is fueled by Bombardier using on-site additive to shrink nacelle spare part lead times, while Belfast software startups supply build monitoring solutions bundled with machine sales incentives.

Competitive Landscape

The supplier base is moderately fragmented; the five largest vendors account for roughly 55% of installed revenue, leaving white space for consolidation. Renishaw blends metrology with dual-laser powder bed fusion, differentiating with closed-loop control that slashes scrap rates. Photocentric champions photopolymer LCD economies, selling resin formulations with 25% margin uplift over hardware. Wayland Additive deploys neutral-atom e-beam technology aimed at high-density tungsten parts for defense optics.

Service bureaus pursue vertical integration. 3DPRINTUK broadened its HP MJF fleet and insourced maintenance crews, raising uptime to 95% and capturing larger aerospace blanket orders. Rapid Fusion demonstrated a robot-tended cell that runs 24 hours with one supervisor, easing the labor bottleneck. Hybrid machine builders partner with CAM software firms to embed AI-driven parameter search, shortening job-qualification cycles and lowering the skills threshold for first-time adopters.

M&A interest rises as desktop vendors eye industrial markets. Polymer specialist RYSE 3D, fresh from a 58% sales surge and a King’s Award, is rumored to scout strategic investors. Materials providers lock in long-term powder contracts to hedge volatility and secure ISO compliance for end-use parts. Certification remains a moat: ISO 9001 and ISO 13485 accreditations unlock regulated sectors, prompting smaller players to pool resources for shared audit expenses.

United Kingdom 3D Printing Industry Leaders

Renishaw plc

Stratasys Ltd.

EOS GmbH

Materialise NV

Nikon SLM Solutions AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Solid Print3D showcased large-format AM for luxury furniture, illustrating diversification into high-value consumer goods.

- February 2025: UK rocket launch consortium secured GBP 20 million to embed additive manufacturing for propulsion and avionics components.

- January 2025: Rapid Fusion opened a robot-integrated demonstration center after recording a sales boom in automated metal AM cells.

- December 2024: RYSE 3D posted a 58% hike in annual printer sales and received the King’s Award for Innovation.

United Kingdom 3D Printing Market Report Scope

3D printing is a range of digital manufacturing technologies that produce component parts layer-by-layer through the additional use of materials. There are many different types of 3D printing processes, which are all controlled using three-dimensional digital data.

The 3D Printing Market in the United Kingdom is classified as follows: Printer (Industrial and Desktop), Material (Metal, Plastic, Ceramics, Others), and Application (Automotive, Aerospace and Defense, Healthcare, Construction and Architecture, and Other Applications).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Printer Type

| Industrial |

| Desktop/Professional |

By Material Type

| Metal |

| Polymer |

| Ceramic |

| Composite/Other |

By Technology

| Powder Bed Fusion |

| Material Extrusion (FDM / FFF) |

| Vat Photopolymerisation |

| Binder Jetting |

| Directed Energy Deposition |

By Application

| Aerospace and Defence |

| Automotive and Motorsport |

| Healthcare and Medical Devices |

| Construction and Architecture |

| Consumer Products and Electronics |

| Other Industrial Applications |

By Region

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Printer Type | Industrial |

| Desktop/Professional | |

| By Material Type | Metal |

| Polymer | |

| Ceramic | |

| Composite/Other | |

| By Technology | Powder Bed Fusion |

| Material Extrusion (FDM / FFF) | |

| Vat Photopolymerisation | |

| Binder Jetting | |

| Directed Energy Deposition | |

| By Application | Aerospace and Defence |

| Automotive and Motorsport | |

| Healthcare and Medical Devices | |

| Construction and Architecture | |

| Consumer Products and Electronics | |

| Other Industrial Applications | |

| By Region | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

How big is the United Kingdom 3D printing market in 2026?

The market stands at USD 1.14 billion in 2026 and is on track for a 13.22% CAGR to 2031.

Which segment grows fastest through 2031?

Healthcare and medical devices expand at a 15.05% CAGR, outpacing all other application areas.

What printer category leads spending today?

Industrial systems hold 72.05% share, reflecting strong aerospace and automotive demand.

Which material type is gaining momentum beyond metals?

Ceramic feedstocks post a 14.56% CAGR due to uptake in dental, electronics, and high-temperature components.

Why is Northern Ireland significant for future growth?

Targeted incentives and aerospace cluster investment lift Northern Ireland’s CAGR to 14.72%, the highest across UK regions.

Page last updated on: