Oil And Gas NDT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.22 Billion |

| Market Size (2031) | USD 8.27 Billion |

| Growth Rate (2026 - 2031) | 5.88% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas NDT Market Analysis by Mordor Intelligence

The Oil and Gas NDT market size is expected to grow from USD 5.87 billion in 2025 to USD 6.22 billion in 2026 and is forecast to reach USD 8.27 billion by 2031 at 5.88% CAGR over 2026-2031. This expansion mirrors the sector’s role in safeguarding upstream, midstream, and downstream assets while regulators tighten integrity rules and operators modernize aging pipelines. Digital inspection platforms, increased subsea activity, and stricter environmental mandates are driving capital toward advanced ultrasonic, radiographic, and computed tomography systems. Consolidation among major service providers is reshaping competitive boundaries, and data-centric value propositions now decide contract awards. In parallel, predictive maintenance programs built on AI analytics are unlocking new recurring revenue opportunities, particularly in cases where inspection intervals are shortened.

Key Report Takeaways

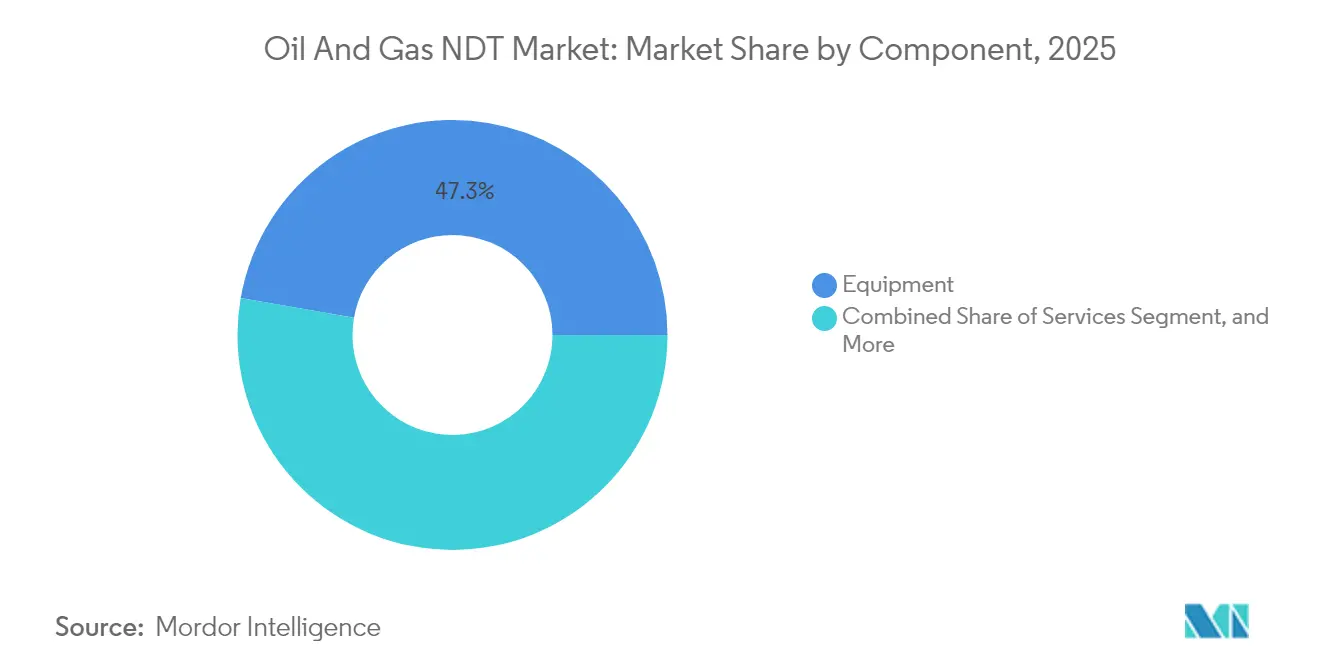

- By component, equipment held 47.25% of the Oil and Gas NDT market share in 2025, whereas services are projected to register a 6.62% CAGR through 2031.

- By testing method, ultrasonic testing is expected to lead the Oil and Gas NDT market with a 33.20% revenue share in 2025, while computed tomography is forecasted to advance at a 7.52% CAGR through 2031.

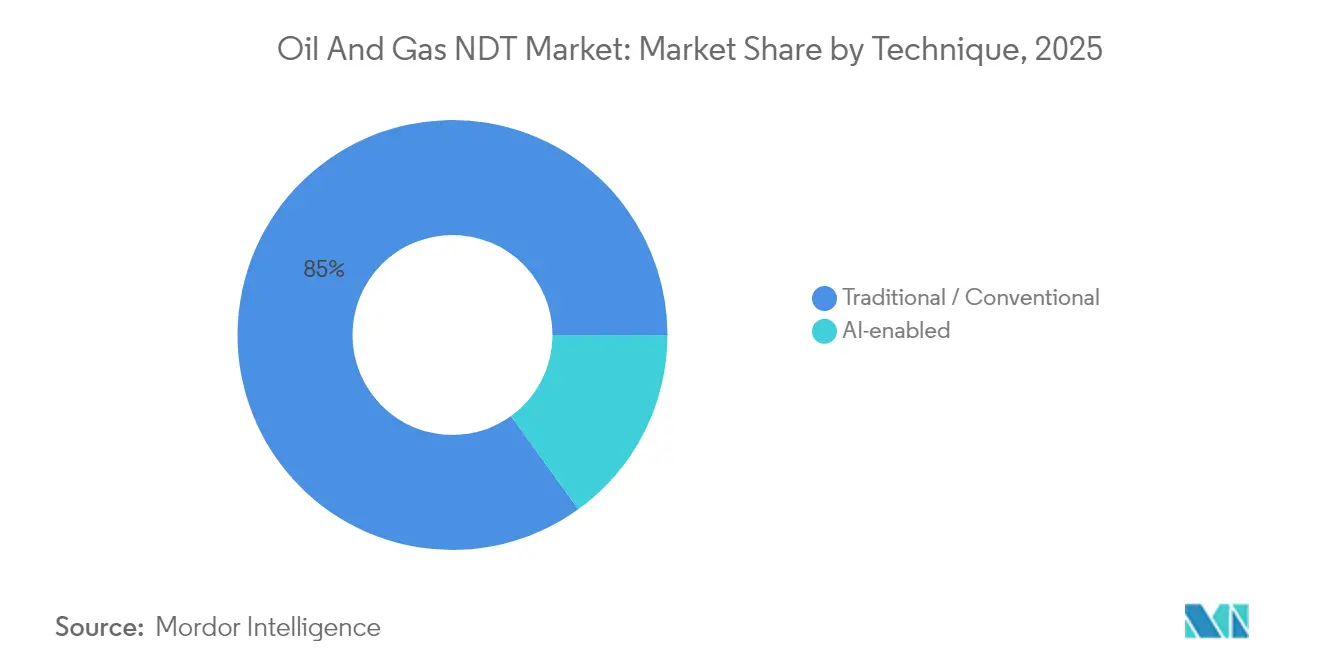

- By technique, traditional modalities accounted for an 84.95% share of the Oil and Gas NDT market size in 2025; AI-enabled approaches are expected to expand at a 6.32% CAGR to 2031.

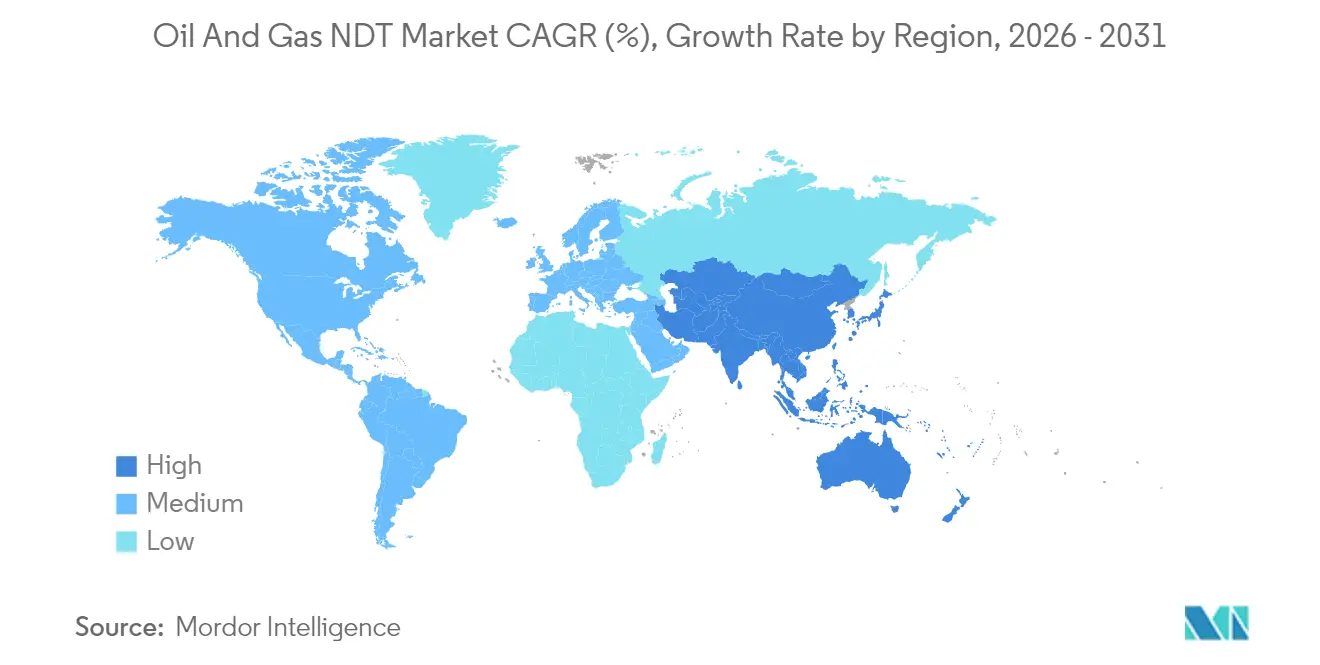

- By geography, North America commanded 38.35% of the Oil and Gas NDT market size in 2025, while the Middle East is set to post the quickest regional CAGR at 6.78% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oil And Gas NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of upstream asset integrity management | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Increasing deepwater and ultra-deepwater exploration projects | +0.8% | Global offshore regions, particularly Gulf of Mexico, North Sea, Brazil | Long term (≥ 4 years) |

| Aging pipeline infrastructure in mature fields | +1.5% | North America core, spill-over to Europe and mature Asia-Pacific fields | Short term (≤ 2 years) |

| Mandated periodic inspection intervals tightened by regulators | +1.1% | North America and EU, expanding to Middle East and Asia-Pacific | Medium term (2-4 years) |

| Adoption of phased array ultrasonic and advanced computed tomography | +0.9% | Global, with higher penetration in North America and Europe | Medium term (2-4 years) |

| Integration of drones and robotics for hazardous area inspection | +0.7% | Global, with early adoption in Middle East, North America offshore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digitization of Upstream Asset Integrity Management Accelerates NDT Transformation

Artificial-intelligence engines embedded in ultrasonic and visual inspection workflows now cut interpretation cycle times by as much as 90%.[1]Baker Hughes, “How to Use AI for Assisted Defect Recognition in Visual Testing,” bakerhughes.com Operators adopting cloud-connected analytics gain real-time defect classification and automated report generation that eases regulatory compliance. Early deployments, including AI-driven weld classification achieving 94% accuracy, demonstrate consistent outcomes that tackle skilled-labor shortages. The same algorithms underpin predictive maintenance routines that shift inspections from calendar-based schedules to risk-based triggers, elevating asset uptime and reducing total inspection spend. Equipment vendors are increasingly bundling edge computing modules with phased-array probes, transforming hardware into data nodes that feed digital twins. As data lakes grow, service contracts increasingly specify performance-based fees rather than hourly rates, rewarding vendors that deliver measurable reliability improvements.

Deepwater Exploration Projects Drive Advanced NDT Requirements

The installation of floating production systems at depths exceeding 3,000 m stimulates demand for subsea-rated phased-array scanners capable of detecting ±0.5 mm wall loss. ROV-deployed instruments eliminate diver exposure while trimming vessel time by up to 70%.[2]Deep Trekker, “Discover How ROVs Can Help with Offshore Energy Inspections,” deeptrekker.com New sensor packages combine eddy-current arrays with acoustic emission modules to survey fatigue hotspots in catenary risers that are subjected to extreme dynamic loads. Novel magnetic-memory diagnostics, paired with deep-learning models, have achieved 95.4% validation accuracy in classifying pitting, groove loss, and wear on riser interiors.[3]Xiangyuan Liu and Jianchun Fan, “Research on Nondestructive Testing Technology for Drilling Risers Based on Magnetic Memory and Deep Learning,” Sustainability, doi.org Given higher barrel costs, operators accept premium day rates for inspection vessels that deliver full digital data sets during a single mobilization. These high-value projects secure multi-year service agreements, ensuring predictable cash flows for suppliers of deepwater NDT solutions.

Aging Pipeline Infrastructure Creates Sustained Inspection Demand

Pipelines laid before 1970 account for 67% of U.S. natural-gas transmission mileage, underscoring the need for regular integrity assessments. PHMSA issued USD 196 million in modernization grants that finance replacements of high-risk cast-iron networks. Advisory bulletins now compel operators to locate “hard spots” in vintage steel, driving demand for high-resolution ultrasonic crawlers and metallurgical verification testing. Service providers that fuse historical data with modern imaging re-rating programs secure recurring engagements as clients revisit older assessments in light of newer models that account for flaw growth.

Regulatory Compliance Tightens Inspection Requirements

PHMSA’s 2025 leak-detection rule requires a 90% probability of detection for 10 kg/h methane leaks on transmission lines, effectively mandating more frequent surveys and stricter repair windows. Pipeline Safety Management Systems, covering nearly 85% of U.S. mileage, embed continuous-improvement loops that institutionalize NDT data analytics. In 2025, the agency formally accepted unmanned aerial systems and satellite lidar for right-of-way patrols, broadening the solution set for integrity managers. This evolving rulebook favors vendors certified under the latest consensus standards and able to provide audit-ready digital records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude oil prices curbing CAPEX cycles | -0.9% | Global, with higher sensitivity in North America shale regions | Short term (≤ 2 years) |

| Limited skilled workforce for advanced NDT methods | -0.7% | Global, particularly acute in emerging markets and specialized techniques | Medium term (2-4 years) |

| Data security concerns with cloud-based NDT analytics | -0.4% | Global, with heightened sensitivity in regulated industries and government contracts | Medium term (2-4 years) |

| High initial cost of advanced equipment | -0.6% | Global, with higher impact on smaller operators and emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil Price Volatility Constrains Service Demand

A double-digit slide in Brent prices to USD 66.65/bbl early 2025 prompted forecasts of a 20% dip in U.S. onshore activity if crude falls below USD 60. A decline of USD 5 historically reduces shale spending by about 5%, resulting in fewer welds, risers, and flowlines that require inspection. Although international work shows lower sensitivity, domestic service companies face rig-count retrenchments that compress utilization and squeeze day rates. Simultaneously, an M&A wave valued at USD 200 billion has concentrated purchasing power among fewer super-majors, enabling them to negotiate sharper pricing and longer payment terms. While high-spec deepwater projects remain insulated, short-cycle land activity displays amplified elasticity to price swings.

Workforce Limitations Challenge Technology Adoption

Advanced modalities such as phased-array ultrasonics and computed tomography require inspectors who hold multi-level ASNT certifications and possess data analytics fluency. An aging workforce and limited training pipelines keep vacancy rates elevated, prompting equipment makers to embed AI engines that automate image interpretation and documentation.[4]Baker Hughes, “Leading the Shift: Q&A on the Future of Imaging,” bakerhughes.com Certification bodies have expanded hybrid courses, yet offshore roles still demand extra survival and rope-access credentials, lengthening onboarding cycles. Higher wage premiums can inflate project budgets, while staffing shortages in emerging markets can delay the adoption of cutting-edge systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Propel Outsourcing Momentum

Services captured growing budget allocations as operators pivoted from owning equipment to procuring turnkey inspection outcomes. The Oil and Gas NDT market size tied to services is on track for a 6.62% CAGR, driven by the adoption of AI analytics, robotics, and integrity data hosting, which favors specialized vendors over in-house crews. Global service chains bundle multidisciplinary teams with cloud dashboards that reduce internal administrative costs and provide instant regulatory reports.

Equipment retains a substantial 47.25% revenue share, underpinned by capital spending on phased-array arrays, high-speed radiography, and compact CT scanners. Vendors differentiate hardware through open APIs that stream inspection data directly into enterprise asset-management platforms, extending lifecycle revenues via predictive-maintenance software and calibration contracts.

By Testing Method: Computed Tomography Advances High-Resolution Imaging

Ultrasonic testing remains the workhorse, holding 33.20% of the Oil and Gas NDT market share in 2025, thanks to its single-side access and deep penetration capabilities. Time-of-flight diffraction and phased-array configurations now mount on drones for elevated pipe racks and ROVs for subsea spools. Computed tomography, although nascent, is the fastest-growing method, with a projected 7.52% CAGR.

Recent studies confirmed CT’s ability to pinpoint delamination and fiber breakage in 1,500 psi fiberglass lines that conventional ultrasound can miss. Portable CT scanners, paired with fast-scan modes, shorten acquisition times, thereby improving field practicality. Radiography continues to serve heavy-wall welds, while magnetic-particle and dye-penetrant techniques tackle ferromagnetic forgings and surface-breaking flaws, respectively.

By Technique: AI-Enabled Workflows Gain Traction

Traditional techniques still account for 84.95% of 2025 revenues, reflecting a decades-long acceptance by regulators and asset owners. However, AI-enabled inspection pipelines are forecasted to have a 6.32% CAGR as machine-learning algorithms automate weld classifications, corrosion mapping, and anomaly clustering.

Early deployments show end-to-end reporting cycle trims of 50-90%, freeing inspectors to focus on verification rather than slogging through raw data. Cloud architectures enable large-scale model training on diverse defect libraries, continually improving detection fidelity without requiring hardware swaps. Consequently, vendors position AI modules as subscription add-ons, reshaping revenue mixes toward higher-margin software streams.

Geography Analysis

North America accounted for 38.35% of global 2025 spending, driven by a 2.6-million-mile pipeline grid and stringent PHMSA mandates that mandate tighter inspection frequencies. Recent rules on leak detection and hard-spot evaluation are expected to guarantee rising bid volumes, while public-funded replacement projects are expected to enlarge the addressable footage. Major service providers deepen scale through acquisitions that integrate labs, field crews, and digital platforms, enabling one-stop solutions across shale basins and Gulf of Mexico deepwater fields.

The Middle East is recording the fastest trajectory, with a 6.78% CAGR, as national oil companies upgrade their integrity programs in alignment with Vision 2030 diversification targets. Extended partnerships with Aramco and ADNOC prioritize the use of robotic crawlers and inline-inspection tools for previously unpiggable lines, while local content policies drive the establishment of new training centers to certify indigenous technicians. High-temperature desert settings encourage remote and autonomous inspections, accelerating the adoption of drones and crawler robots equipped with panoramic cameras and phased-array probes.

Europe posts steady gains tied to the rejuvenation of mature assets and stringent environmental objectives. Operators refurbish North Sea infrastructure with advanced corrosion-mapping and weld-overlay technologies. Simultaneously, EU methane regulations drive demand for high-sensitivity leak detection, blending conventional ultrasound with satellite data feeds. In the Asia-Pacific region, Australia and Japan focus on extending the life of end-of-life gas assets, whereas India and Southeast Asia build new midstream capacity, opening up dual opportunities for construction-phase radiography and operations-phase ultrasonic mapping. Across Latin America and Africa, demand for inspections tracks offshore campaigns in Brazil and Mozambique, although funding cycles remain more sensitive to price volatility and political shifts.

Competitive Landscape

The Oil and Gas NDT market exhibits moderate concentration, with the top five groups capturing roughly 50-60% of global revenues. SGS’s USD 1.325 billion purchase of Applied Technical Services expanded its North American footprint and integrated metallurgy labs with field inspection teams. Baker Hughes’ planned USD 13.6 billion acquisition of Chart Industries strengthens its equipment breadth, from cryogenic tanks to rotary compressors, and integrates proprietary InspectionWorks software into a larger installed base. These moves illustrate a race to bundle hardware, services, and analytics inside single contracts.

Technology remains the key differentiator. Waygate Technologies embeds AI in visual testing, enabling automated crack detection and report generation within minutes on handheld devices. NDT Global utilizes ultrasonic constellations to capture high-resolution corrosion metrics in pipelines up to 56 inches in diameter, while innovators such as INGU supply palm-sized smart balls for low-pressure distribution networks. Vendors capable of integrating inspection data into enterprise resource planning stacks gain stickiness and unlock upsell paths in data analytics and compliance dashboards.

Regional challengers employ localization strategies. Middle-East service firms co-invest with OEMs to establish repair hubs and training academies, thereby ensuring asset owner confidence and shortening turnaround times. Similar localization mandates in Brazil and India stimulate joint ventures that transfer phased-array fabrication know-how. As consolidation proceeds, smaller specialists position themselves as niche experts for high-temperature reactors or subsea flexible risers, banking on deep domain knowledge that larger conglomerates may overlook.

Oil And Gas NDT Industry Leaders

Baker Hughes Company

Mistras Group Inc.

SGS SA

Intertek Group plc

Applus Services SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: PHMSA published a direct final rule permitting the use of drones and satellites for right-of-way patrols, validating remote sensing as a compliance option.

- July 2025: SGS finalized the USD 1.325 billion acquisition of Applied Technical Services, creating North America’s largest integrated inspection network.

- July 2025: Baker Hughes agreed to acquire Chart Industries for USD 13.6 billion, targeting USD 325 million in annual cost synergies.

- June 2025: Metalogic bought Houston-based NDT-PRO Services, extending Gulf Coast coverage for high-compliance energy clients.

- January 2025: PHMSA issued its Gas Pipeline Leak Detection and Repair final rule, introducing strict performance criteria and higher survey frequencies.

Global Oil And Gas NDT Market Report Scope

Non-Destructive Testing (NDT) is the process of inspecting, testing, or evaluating materials, components, or assemblies for discontinuities or differences in characteristics without destroying the serviceability of the part or system. Aerospace, defense, oil and gas, power generation, and automotive are leading sectors that use NDT techniques to ensure the quality of products. These sectors use the NDT test to determine the physical properties of materials such as impact resistance, ductility, yield, ultimate tensile strength, fracture toughness, and fatigue strength. Visual testing is the most widely used nondestructive testing (NDT) method. The market is segmented by Type (Equipment, Services), Type (Upstream, Midstream, Downstream), Technique (Ultrasonic, Radiography, Visual Inspection, Liquid Penetrant), and Geography (North America, Europe, Asia-Pacific, and Rest of the World).

The market sizes and forecasts are provided in terms of value (in USD million) for all the above segments.

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Equipment | |

| Software | ||

| Services | ||

| Consumables | ||

| By Testing Method | Ultrasonic Testing | |

| Radiographic Testing | ||

| Magnetic Particle Testing | ||

| Liquid Penetrant Testing | ||

| Visual Inspection Testing | ||

| Eddy-Current Testing | ||

| Acoustic Emission Testing | ||

| Thermography / Infrared Testing | ||

| Computed Tomography Testing | ||

| By Technique | Traditional / Conventional | |

| AI-enabled | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the oil and gas NDT market in 2026?

Global spending reaches USD 6.22 billion in 2026 and is forecast to rise to USD 8.27 billion by 2031.

Which testing method currently leads spend in oil and gas inspections?

Ultrasonic testing holds the top position with 33.20% of 2025 revenue.

Why are AI-enabled inspection techniques gaining traction?

They automate defect classification, cut interpretation cycle times by up to 90%, and support predictive maintenance, easing skilled-labor shortages.

What region is projected to grow fastest for oil and gas NDT through 2031?

The Middle East is expected to post the quickest expansion at a 6.78% CAGR during 2026-2031.

How do new PHMSA rules influence inspection demand?

The 2025 leak-detection rule mandates a 90% probability of detecting 10 kg/h methane leaks and tighter repair windows, driving more frequent and sophisticated surveys.

What is the main benefit of ROV-deployed phased-array systems for deepwater assets?

They deliver ±0.5 mm wall-loss detection accuracy, eliminate diver exposure, and reduce vessel costs by as much as 70%.

Page last updated on: