Middle East Hyperscale Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

| Historical Data Period | 2019 - 2023 |

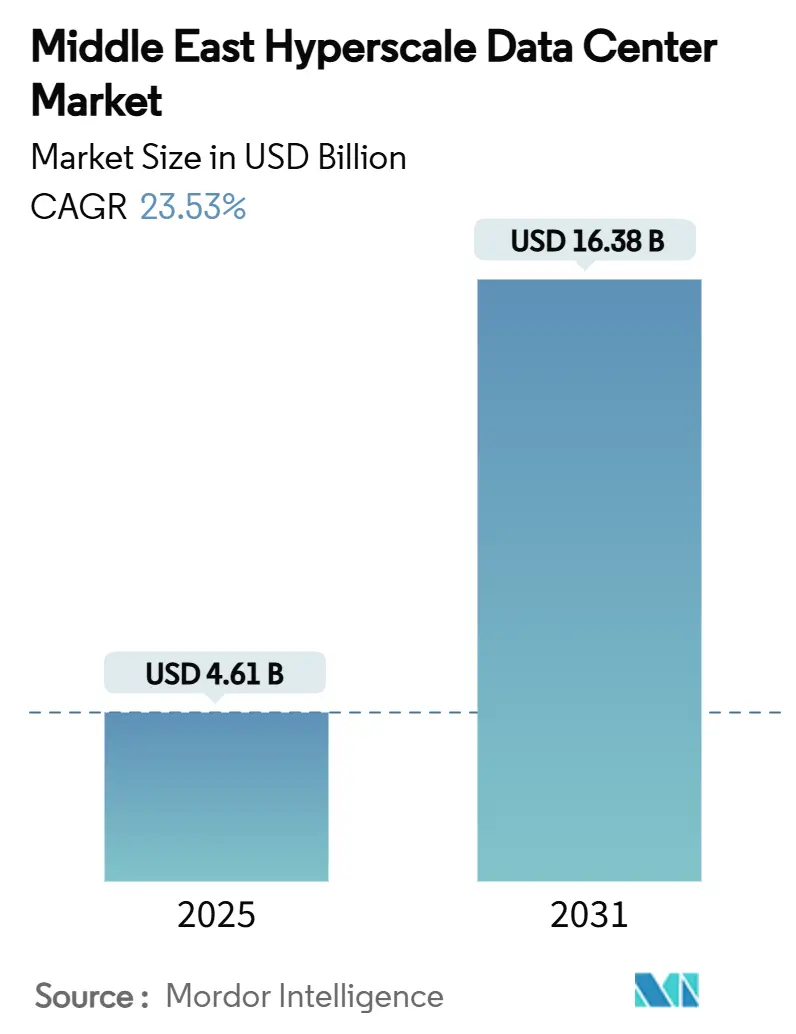

| Market Size (2025) | USD 4.61 Billion |

| Market Size (2031) | USD 16.38 Billion |

| Growth Rate (2025 - 2031) | 23.53% CAGR |

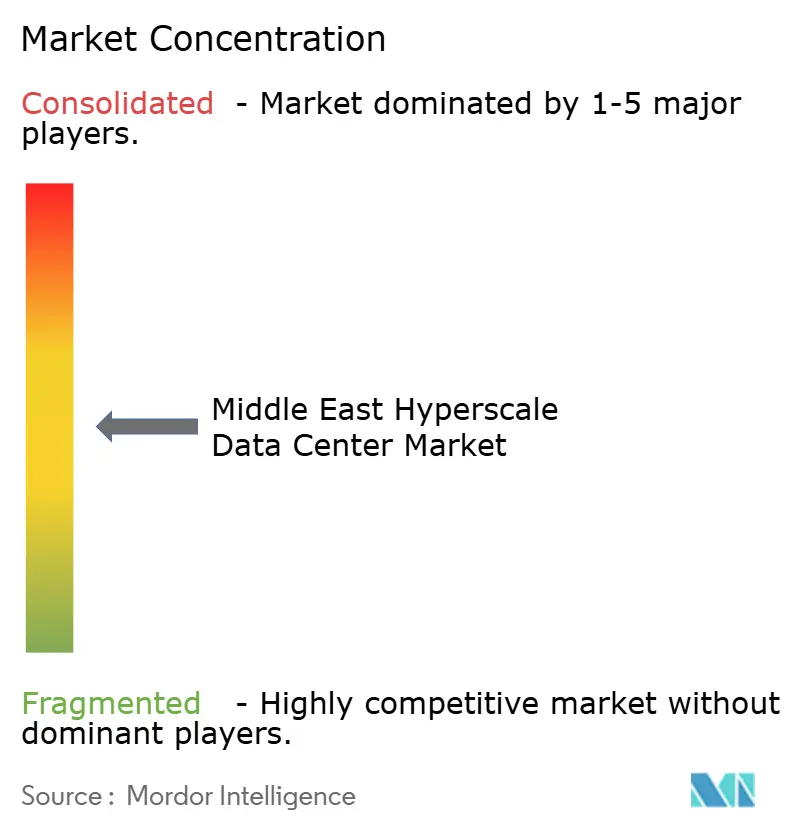

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Hyperscale Data Center Market Analysis by Mordor Intelligence

The Middle East hyperscale data center market size is valued at USD 4.61 Billion in 2025 and is forecast to reach USD 16.38 Billion by 2031, advancing at a 23.53% CAGR through the period. Rapid sovereign digital-economy agendas, the arrival of several cloud regions, and abundant renewable-energy resources position the market for sustained expansion. The shift toward artificial-intelligence workloads is inflating rack densities above 30 kW, accelerating the adoption of liquid-cooling systems and driving the volume of installed IT load from 1,850.4 MW in 2025 to 5,955.15 MW in 2031. The regional policy environment—especially Vision 2030 in Saudi Arabia and the UAE—reduces entry barriers for global operators, while submarine-cable landings transform Red Sea routes into latency-optimized corridors. Together, these factors underpin one of the fastest growth trajectories among global data-center regions.

Key Report Takeaways

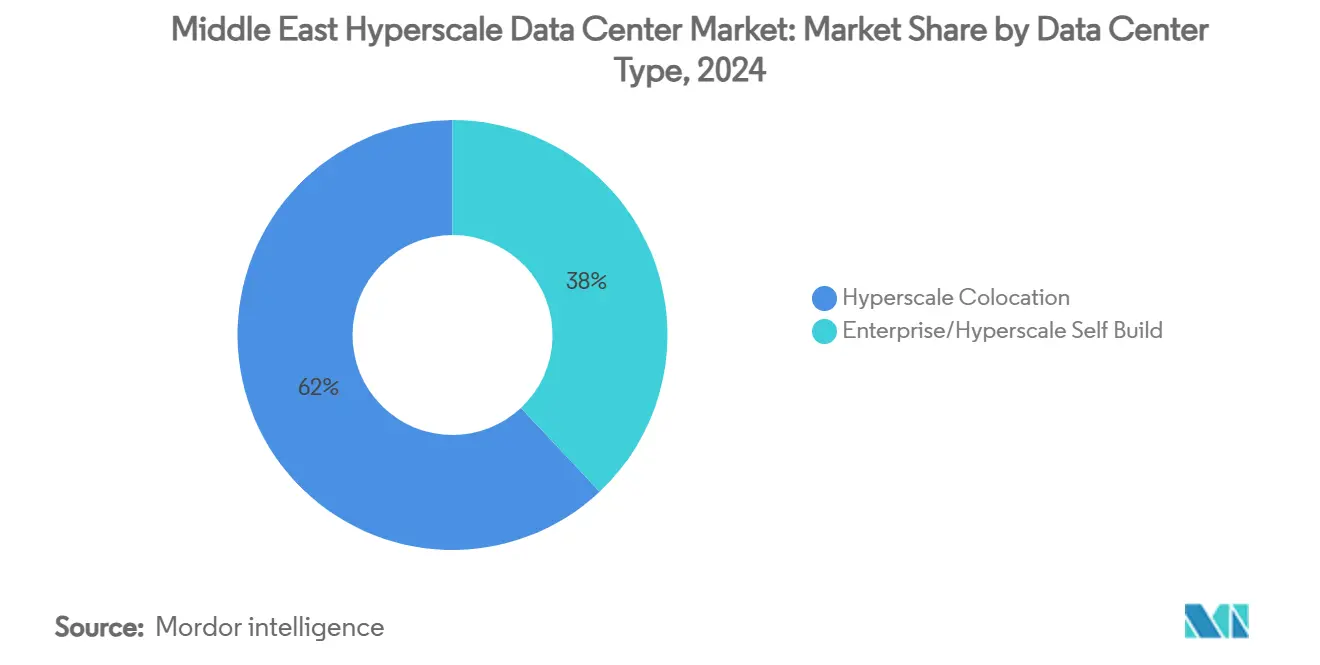

- By data center type, hyperscale colocation led with 62% revenue share in 2024, whereas hyperscaler self-build projects are projected to expand at a 23.60% CAGR through 2030.

- By component, IT infrastructure accounted for 43% of the Middle East hyperscale data center market share in 2024, while DCIM/BMS solutions are forecast to rise at a 24.60% CAGR to 2030.

- By tier standard, Tier III facilities captured 75% of the Middle East hyperscale data center market size in 2024; Tier IV deployments are advancing at a 23.80% CAGR through 2030.

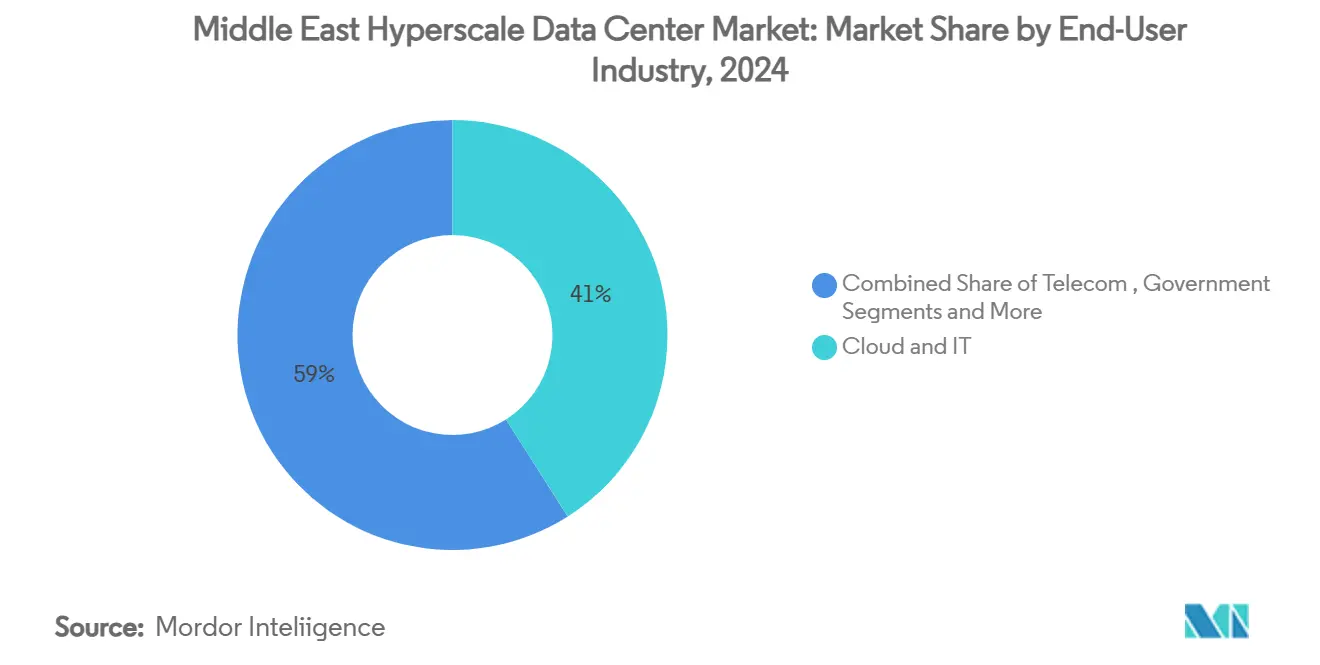

- By end-user industry, the cloud and IT segment held 41% of the Middle East hyperscale data center market size in 2024, while the government sector registers the highest CAGR at 25.50% through 2030.

- By data center size, massive facilities (25-60 MW) comprised 57% of total deployments in 2024, whereas mega campuses are growing at a 23.10% CAGR over the forecast horizon.

Dynamics observed within Middle east present a holistic view when set against the broader international context. The hyperscale data center market analysis by Mordor Intelligence provides that expanded global perspective.

Middle East Hyperscale Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 digital-economy programs accelerating hyperscale builds (KSA, UAE) | 6.2% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Cloud-region launches by AWS, Microsoft and Google in GCC | 5.8% | GCC countries | Short term (≤ 2 years) |

| Utility-scale solar and green-hydrogen PPAs unlocking greater than70% renewable power | 4.1% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Sovereign digital-twin and LLM projects driving greater than 30 kW liquid-cooled racks | 3.9% | UAE, Saudi Arabia | Medium term (2-4 years) |

| 2Africa and BlueRaman cable landings turning Red Sea corridor into latency hub | 2.7% | Regional connectivity | Long term (≥ 4 years) |

| Zero-tax free-zone financing lowering capex hurdle for colocation builds | 2.1% | UAE (ADGM, DIFC) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 digital-economy programs accelerating hyperscale builds

Government roadmaps in Saudi Arabia and the UAE treat digital infrastructure as a national-diversification pillar, unlocking USD 21 billion of confirmed investments and underwriting joint ventures such as Equinix’s 100 MW Riyadh project and DataVolt’s 1.5 GW campus in NEOM. Fast-tracked permitting, tax holidays, and sovereign-wealth-fund capital reduce execution risk for international operators, stimulating additional private finance inflows. The coordinated approach aligns urban-development timelines with power-transmission upgrades, ensuring that large-scale sites come online as domestic demand for cloud and AI services peaks. The Middle East hyperscale data center market therefore benefits from synchronized policy frameworks that are rarely observed elsewhere.

Cloud-region launches by AWS, Microsoft and Google in GCC

The announcement of three hyperscale cloud regions in Saudi Arabia, the UAE, and Qatar elevates local latency performance to parity with mature European nodes. Anchor-tenant commitments—USD 5.3 billion from AWS in Saudi Arabia and USD 544 million via Microsoft-du in the UAE—drive wholesale colocation pre-leasing and compel regional incumbents to enhance specifications.[1]Reuters, “Amazon's AWS to launch Saudi Arabia data centers,” reuters.comCompetitive coexistence among the hyperscalers spawns multicloud demand from enterprises and accelerates employer-led digital-skills development programs, thus deepening a talent pool essential for ongoing expansion of the Middle East hyperscale data center market.

Utility-scale solar and green-hydrogen PPAs unlocking greater than70% renewable power

The Gulf’s solar levelized cost of electricity has fallen below USD 0.02/kWh, enabling data-center operators to obtain 15- to 25-year renewable power purchase agreements without green premiums.[2]Bloomberg, “Race for AI supremacy in Middle East is measured in data centers,” bloomberg.comProjects such as Moro Hub’s solar-powered facility in Dubai and Masdar’s green-hydrogen pilot in Abu Dhabi furnish operators with credible pathways to net-zero operations. High irradiation levels and available land grant the region a unique energy-cost advantage over many European and Asian peers, improving the total cost of ownership prospects for future entrants into the Middle East hyperscale data center market.

Sovereign digital-twin and LLM projects driving greater than30 kW liquid-cooled racks

G42’s Jais 70B and its nine-system Cerebras AI supercomputer roadmap require rack power densities that cannot be met with air-cooling alone. In response, vendors such as Supermicro have shipped more than 2,000 liquid-cooled racks to GCC customers since mid-2024. Local engineering firms are building capabilities around immersion and direct-to-chip technologies, opening service revenue avenues for mechanical-infrastructure specialists. The densification trend elevates demand for sophisticated DCIM solutions able to orchestrate cooling, power, and workload placement in real time.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-capacity bottlenecks and multi-year permitting outside the Gulf | -3.4% | Levant, North Africa | Medium term (2-4 years) |

| Water-stress regulations curbing evaporative cooling in Riyadh and Doha | -2.8% | Saudi Arabia, Qatar | Short term (≤ 2 years) |

| Sparse Tier-1 fiber routes across Levant causing latency-risk | -2.1% | Levant, Jordan, Lebanon | Long term (≥ 4 years) |

| In-country data-sovereignty mirroring inflating TCO in smaller markets | -1.9% | Jordan, Qatar, Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-capacity bottlenecks and multi-year permitting outside the Gulf

Energy-transmission shortfalls elevate connection-queue lead times beyond 36 months in Jordan and Egypt, undermining build-commitment schedules for global colocation firms.[3]Uptime Institute, “News & Media,” uptimeinstitute.com Financing costs escalate when connection certainty diminishes, pushing non-GCC markets down the priority list for hyperscale investors. Governments are allocating stimulus packages for grid reinforcement, yet labor-supply constraints threaten execution speed and may cap short-term contributions from these geographies to the Middle East hyperscale data center market.

Water-stress regulations curbing evaporative cooling in Riyadh and Doha

Revisions to the Saudi Building Code and Qatar’s water-conservation mandates restrict the use of high-water-consumption cooling towers in arid urban areas. Operators must shift to closed-loop or liquid-immersion systems, increasing per-MW capex by up to 15%. Although sustainability outcomes improve, the financial burden could deter smaller entrants without access to scale economics, marginally tempering growth in the Middle East hyperscale data center market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Colocation Dominance Amid Self-Build Acceleration

Colocation held a 62% slice of 2024 revenue, underscoring regional reliance on service providers capable of navigating land-acquisition complexities and municipal approvals. Hyperscale tenants enjoy rapid market access and the risk-sharing benefits inherent in the colocation model. Yet the self-build path shows a 23.60% CAGR through 2030. Microsoft’s dedicated Abu Dhabi campus and AWS’s proprietary Riyadh region exemplify the pivot toward owner-operated infrastructure that offers deeper optimization for AI workloads. The Middle East hyperscale data center market therefore witnesses a dual-track maturation in which both models coexist: colocation capturing new entrants and self-build serving operators at scale.

Infrastructure specialists finance hybrid build-operate-transfer structures, enabling tenants to shift from multi-tenant suites into custom shells without relocating workloads. The arrangement preserves colocation cash flow while satisfying hyperscaler demands for unique power-density envelopes, particularly for liquid-cooled GPU clusters. Consequently, the colocation value proposition evolves toward shell-and-core readiness alongside modular expansion rights that meet the unpredictable scaling curves of sovereign AI projects.

By Component: IT Infrastructure Leadership with DCIM Acceleration

Servers, storage, and networking contributed 43% of 2024 expenditure, driven by continuous refresh cycles necessary to feed AI training clusters and maintain compliance with data-sovereignty mandates. Emirates NBD’s recent deployment of AMD-powered servers illustrates the enterprise embrace of high-core-count platforms. Mechanical-infrastructure budgets swell as operators implement rear-door heat exchangers and direct-to-chip cold plates to sustain >30 kW racks. Electrical systems likewise advance, with solid-state switchgear and static-transfer modules designed for ultra-short switchover times that Tier IV facilities demand.

DCIM and building-management solutions grow the fastest at a 24.60% CAGR. G42’s Core42 Compass 2.0 integrates telemetry from liquid-cooling loops, uninterruptible power supplies, and workload schedulers, presenting operators a single observability plane. AI-infused analytics predict failure signatures hours in advance, reducing unplanned downtime in the Middle East hyperscale data center market.

By Tier Standard: Tier III Prevalence with Tier IV Momentum

Tier III captured 75% of 2024 capacity, aligning with industries that mandate concurrent maintainability rather than full fault tolerance. Local providers have amassed expertise in meeting Uptime-Institute audit criteria, as demonstrated by Najm for Insurance Services’ facility certification. Several banking regulators still stipulate Tier III as the minimum requirement for domestic transaction processing, locking in baseline demand.

Still, Tier IV is advancing 23.80% annually, catalyzed by AI research and defense workloads intolerant of interruption. Projects like Stargate UAE rely on 2(N+1) electrical architecture and geographically separated dual-utility feeds to guarantee zero downtime. Long-term, national digital-twin platforms and autonomous-vehicle simulators are expected to anchor Tier IV expansion, bridging service-level obligations with next-generation workload sensitivity.

By End-User Industry: Cloud Dominance with Government Acceleration

Cloud and IT accounted for 41% of consumption in 2024, spearheaded by hyperscalers and SaaS providers that exploit regional footholds for multicloud redundancy. Enterprise migration pipelines from oil-and-gas majors and retail conglomerates fill compute pipelines, sustaining healthy take-up rates across service classes. However, government agencies register a 25.50% CAGR—the highest of all verticals—as ministries digitalize citizen-services portals and national health records. The Ministry of Health and Prevention’s deployment of Fortinet security fabric across 160 sites underscores new cybersecurity compliance drivers.

Telecom carriers leverage tower footprints for edge nodes, while media-streaming platforms localize transcoding clusters to minimize latency during live events. Manufacturing and e-commerce tenants adopt IIoT and omni-channel analytics, respectively, both contributing incremental megawatts to the Middle East hyperscale data center market.

By Data Center Size: Massive Scale Preference with Mega Growth

Facilities rated 25-60 MW constitute 57% of 2024 deployments, balancing capex efficiency and grid-connection pragmatics. Gulf Data Hub’s 16 MW Dubai site exemplifies the model: scalable pods connected to an on-site 132 kV substation mitigate expansion disruptions. The category supports multitenant leasing strategies, dividing halls among cloud, CDN, and enterprise users.

Mega campuses beyond 60 MW are growing at 23.10% CAGR, driven by AI-factory blueprints such as Stargate UAE’s 5 GW roadmap and DataVolt’s 1.5 GW NEOM agreement. These sites integrate utility-scale solar arrays and hydrogen backup, deploying medium-voltage liquid-cooled busways to maintain efficiency under extreme densities. The trend signals a paradigm shift in the Middle East hyperscale data center market, pivoting from city-edge campuses toward multi-gigawatt industrial clusters anchored by on-site renewables.

Geography Analysis

The UAE and Saudi Arabia collectively command the lion’s share of installed IT load and new-build pipelines, courtesy of accommodative regulations and subsidized renewable-energy tariffs. Dubai hosts 28 active colocation sites and functions as an intercontinental gateway, leveraging a 100-plus-Tbps subsea bandwidth pool that assures low-latency routes to Europe and Asia. Abu Dhabi’s strategy, underpinned by the ADQ-ECP USD 25 billion energy alliance, underwrites grid upgrades essential for multi-gigawatt data-center estates.

Saudi Arabia’s Vision 2030 policy funnels USD 21 billion toward data-center builds across Riyadh, Jeddah, and Dammam, chasing a 525 MW IT-load target by 2030. Blue-Raman landing points augment Jeddah’s stature as a latency hub, catalyzing enterprise demand for in-county cloud zones. The government’s zero-tax-holiday incentives further tilt investment toward the kingdom and reinforce the Middle East hyperscale data center market trajectory.

Turkey’s Eurasian bridge status draws AI-workload spillover; Khazna’s planned Ankara footprint aims at dual-market service aggregation. Qatar strengthens its position through sovereign-fund-backed smart-city deployments post-FIFA 2022. While Levant and North African states trail because of grid constraints, pockets of edge deployments emerge around submarine-cable landing sites, ensuring a region-wide distribution of the Middle East hyperscale data center market opportunity.

Coverage of the hyperscale data center market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for South America, Asia, and Europe, alongside detailed country-level intelligence for Saudi Arabia, Israel, United Kingdom, Brazil, Argentina, and Chile, each shaped by local operating conditions.

Competitive Landscape

Market concentration is moderate. Global hyperscalers—AWS, Microsoft, and Google—anchor demand through multi-billion-dollar region launches, guaranteeing long-term capacity offtake. Regional specialists such as G42’s Khazna and Gulf Data Hub exploit deep government relationships and cultural fluency to secure prime land parcels quickly. International colocation groups form joint ventures—KKR’s USD 5 billion stake in Gulf Data Hub typifies this pattern—to marry global design standards with local execution.

Technology differentiation is now central. Supermicro, Vertiv, and Iceotope chase liquid-cooling dominance, supplying custom manifolds and chassis-level immersion solutions to hyperscale campuses in Abu Dhabi and Riyadh. Sustainability credentials are becoming a bidding prerequisite; Khazna pledges diesel-free backup, while DataVolt’s NEOM site targets net-zero operations from day one. In parallel, telecom incumbents such as du and STC leverage dark-fiber assets to craft competitive colocation propositions. These dynamics create an ecosystem where alliances and technological agility dictate share capture within the Middle East hyperscale data center market.

Middle East Hyperscale Data Center Industry Leaders

Amazon Web Services (AWS)

Microsoft Corporation

Khazna Data Centers

Google LLC

Equinix Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: G42 launched Stargate UAE, a 5 GW AI cluster in Abu Dhabi.

- April 2025: Microsoft and du agreed on a USD 544 million UAE hyperscale facility.

- March 2025: ADQ joined Energy Capital Partners for USD 25 billion in power projects.

- March 2025: Alfanar announced USD 1.4 billion for Saudi data centers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Middle East hyperscale data center market as revenue generated from new facilities that supply more than 25 MW of installed IT load and are owned or leased by cloud, AI, social-media, and SaaS providers; capacity additions are valued alongside associated managed-service fees.

Scope Exclusions: Enterprise server rooms, telecom edge nodes below 1 MW, and refurbished shell conversions are not counted.

Segmentation Overview

- By Data Center Type

- Hyperscale Self-build

- Hyperscale Colocation

- By Component

- IT Infrastructure

- Server Infrastructure

- Storage Infrastructure

- Network Infrastructure

- Electrical Infrastructure

- Power Distribution Units

- Transfer Switches and Switchgears

- UPS Systems

- Generators

- Other Electrical Infrastructure

- Mechanical Infrastructure

- Cooling Systems

- Racks

- Other Mechanical Infrastructure

- General Construction

- Core and Shell Development

- Installation and Commisioning Services

- Design Engineering

- Fire Detection, Suppression and Physical Security

- DCIM/BMS Solutions

- IT Infrastructure

- By Tier Standard

- Tier III

- Tier IV

- By End-User Industry

- Cloud and IT

- Telecom

- Media and Entertainment

- Government

- BFSI

- Manufacturing

- E-Commerce

- Other End Users

- By Data Center Size

- Large (Less than equal to 25 MW)

- Massive (Greater than 25 MW and less than equal to 60 MW)

- Mega (Greater than 60 MW)

- By Geography

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Rest of Middle East

- Middle East

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed facility operators, EPC contractors, and hyperscale procurement leads across the UAE, Saudi Arabia, and Israel to validate utilization ramps, liquid-cooling timelines, and achievable PUE targets; insights refined assumptions we drew from desk work.

Desk Research

We gathered foundational data from telecom regulator ICT statistics, Gulf Energy grid bulletins, Uptime Institute tier certificates, customs records detailing server imports, and construction filings captured in D&B Hoovers, while news flows were screened through Dow Jones Factiva. These references exposed hyperscale construction pipelines, prevailing rack densities, and regional power tariffs that anchor our baseline. Additional context stemmed from GCC smart-city master plans, subsea-cable landing schedules, and AI policy white papers. The sources listed are illustrative; numerous further references informed verification.

Market-Sizing & Forecasting

A top-down build starts with country power-capacity inventories and announced megawatt additions, which are then priced using sampled $/kW rates and service uplifts. Supplier roll-ups of switchgear, generator, and prefabricated-module shipments offer bottom-up checks before totals are finalized. Key variables like 400 G port shipments, GPU rack densities, sovereign-cloud deadlines, hyperscaler capex disclosures, regional power prices, and new cable landings feed a multivariate regression that projects revenue to 2031. Scenario bands cover energy-cost or policy shifts, and data gaps in supplier roll-ups are bridged by moderated averages from interviewed peers.

Data Validation & Update Cycle

Model outputs undergo dual analyst reviews, variance screens against independent capacity trackers, and a re-check with prior interviewees. Reports refresh yearly, with interim revisions when a single event moves regional capacity by five percent or more.

Why Mordor's Middle East Hyperscale Data Center Baseline Commands Reliability

Published estimates often diverge because firms slice geography differently, rely on dated construction pipelines, or apply flat price escalators.

Key gap drivers include combining Africa with the Middle East, omitting self-build revenue, or freezing rack pricing even as density rises.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.61 B (2025) | Mordor Intelligence | |

| USD 1.51 B (2024) | Regional Consultancy A | Combines MEA, revenue only, limited capacity audit |

| USD 1.74 B (2023) | Trade Journal B | Folds Tier II-III colocation into scope, older baseline, no price-density adjustment |

These comparisons illustrate that Mordor Intelligence's step-wise variable selection, yearly refresh cadence, and dual-track validation deliver a balanced, transparent baseline that decision-makers can retrace with publicly verifiable inputs.

Key Questions Answered in the Report

What is the current value of the Middle East hyperscale data center market?

The market is valued at USD 4.61 billion in 2025 and is projected to reach USD 16.39 billion by 2031.

Which segment holds the largest share of the market?

Hyperscale colocation accounts for 62% of 2024 revenue.

How fast are Tier IV facilities growing?

Tier IV deployments are expanding at a 23.80% CAGR through 2030.

Why are liquid-cooled racks gaining popularity?

AI training clusters demand power densities above 30 kW per rack, which liquid-cooling systems can support more efficiently than traditional air cooling.

Which countries dominate regional capacity?

The United Arab Emirates and Saudi Arabia together hold the majority of installed IT load, thanks to supportive policies and renewable-energy access.

What sustainability measures are operators adopting?

Many campuses procure solar power via long-term PPAs and explore green-hydrogen backup, aiming for renewable-energy mixes exceeding 70%.

Page last updated on: