United Arab Emirates Full Service Restaurants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

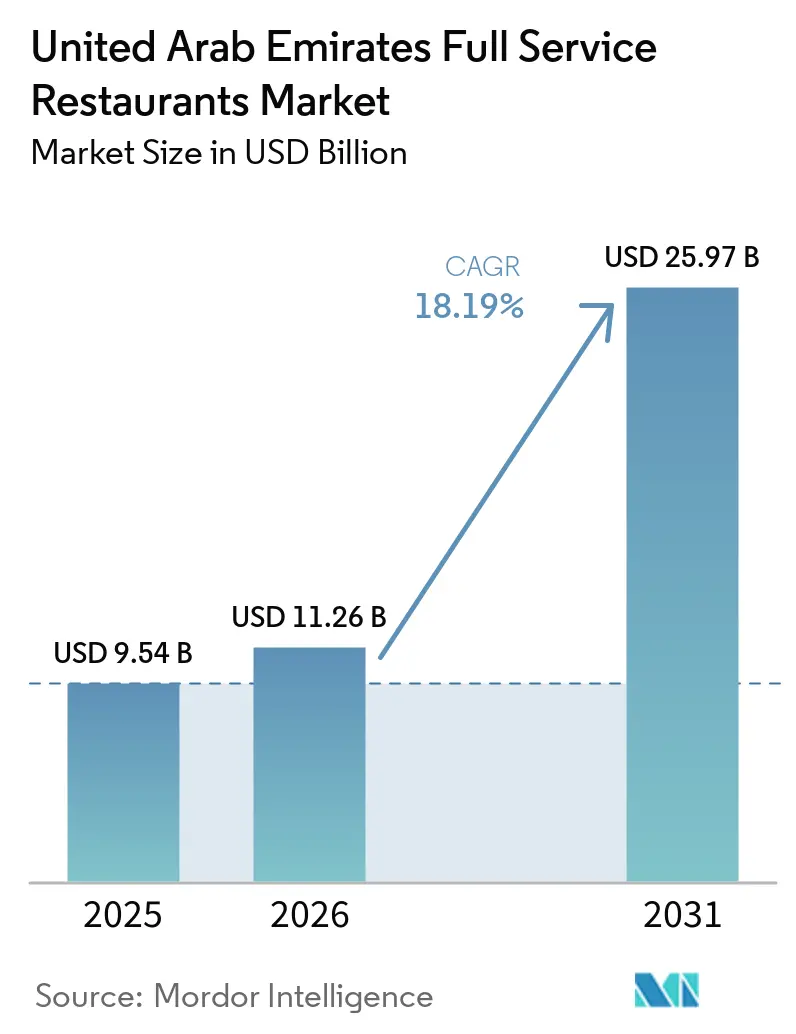

| Base Year Market Size (2025) | USD 9.54 Billion |

| Market Size (2026) | USD 11.26 Billion |

| Market Size (2031) | USD 25.97 Billion |

| Growth Rate (2026 - 2031) | 18.19% CAGR |

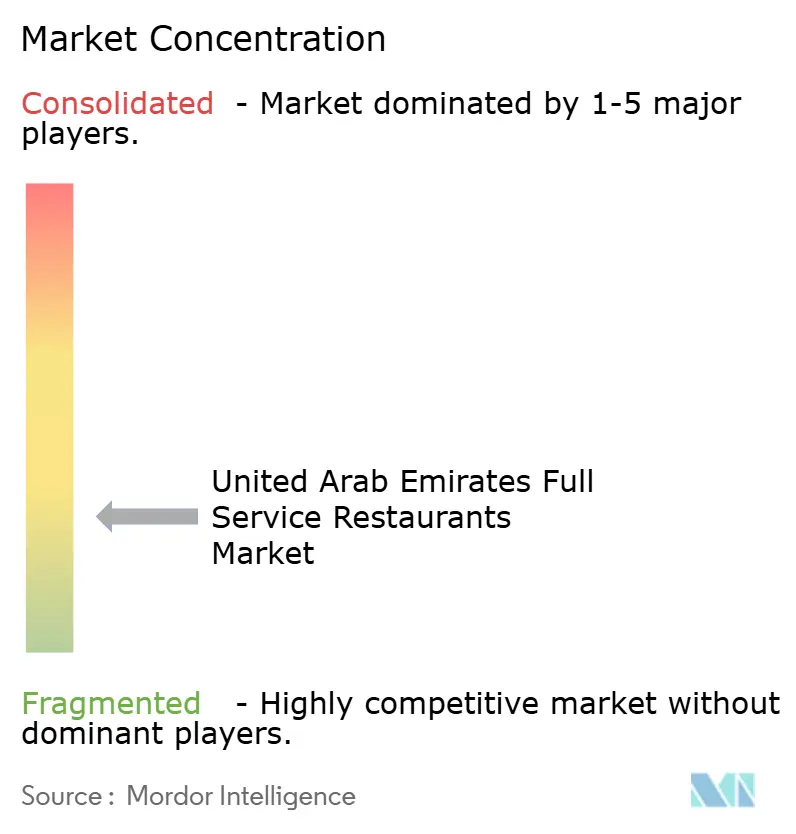

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Full Service Restaurants Market Analysis by Mordor Intelligence

The United Arab Emirates' full service restaurants market size is projected to be USD 9.54 billion in 2025, USD 11.26 billion in 2026, and reach USD 25.97 billion by 2031, growing at a CAGR of 18.19% from 2026 to 2031. The driving force behind this growth is the momentum in tourism, all of which channels affluent travelers into upscale dining establishments. This trend is further bolstered by rapid brand expansion; in 2024 alone, Dubai issued over 1,200 new restaurant licenses. Moreover, the MICHELIN Guide Dubai 2025 awarded the region's inaugural two three-star ratings, underscoring the emirate's stature in fine dining and boosting culinary tourism, which, as per the Dubai government, spends 30–40% more per visit than leisure tourists. Latin American culinary concepts are making waves, buoyed by Chipotle's franchise debut and Fogo de Chão's launch in DIFC, both strategically appealing to a demographic that prioritizes authentic and experiential dining over standard international options. However, rising operational costs pose challenges: rents for prime-zone restaurants surged by 15-20% in 2024, and payrolls for skilled labor saw an 8-12% increase. In response, independent restaurants are turning to cloud-kitchen extensions, dynamic pricing, and stringent supply-chain controls to safeguard their profit margins, as highlighted by the United Arab Emirates government.

Key Report Takeaways

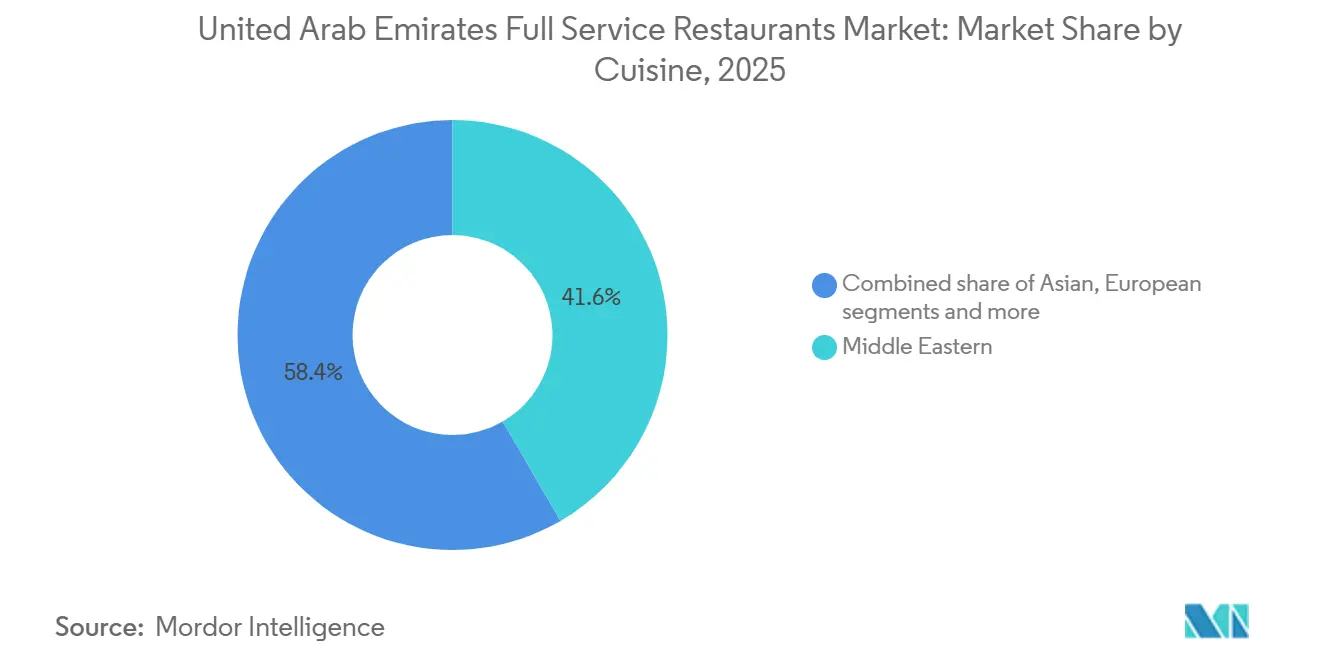

- By cuisine, Middle Eastern concepts led with 41.62% revenue share in 2025, while Latin American menus are forecast to advance at a 19.80% CAGR to 2031.

- By outlet type, independents held 62.74% of the United Arab Emirates full service restaurants market share in 2025; chained formats register the highest projected growth at 18.72% CAGR through 2031.

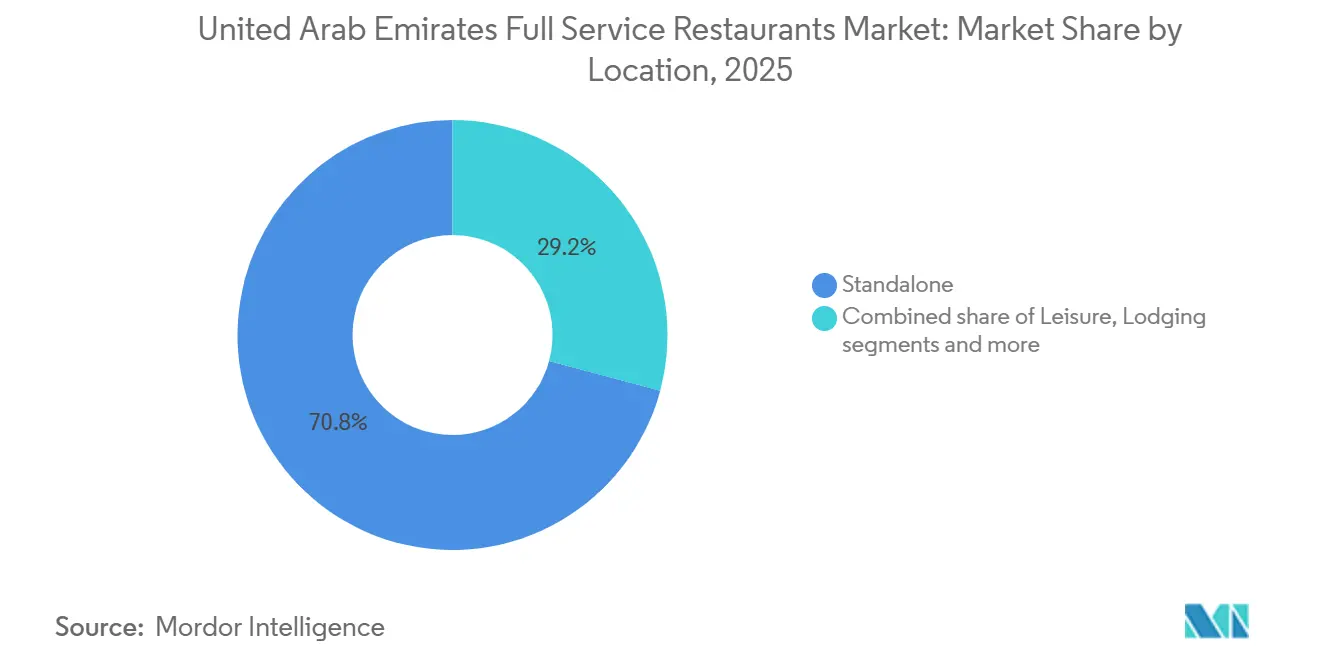

- By location, standalone venues delivered 70.82% of 2025 revenue, yet lodging-based outlets are projected to expand at an 18.38% CAGR over 2026-2031.

- By service, dine-in transactions represented 66.12% of 2025 activity; takeaway occasions exhibit an 18.12% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Full Service Restaurants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism and hospitality expansion | +3.5% | Dubai core, Abu Dhabi secondary, spillover to Sharjah and Ras Al Khaimah | Medium term (2-4 years) |

| Entry and expansion of international brands | +3.2% | Dubai, Abu Dhabi, with an emerging presence in the Northern Emirates | Short term (≤ 2 years) |

| Influencer and social media discovery | +2.8% | United Arab Emirates-wide, concentrated in Dubai and Abu Dhabi lifestyle districts | Short term (≤ 2 years) |

| Menu innovation and localization | +2.3% | Dubai, Abu Dhabi, with gradual adoption in secondary cities | Medium term (2-4 years) |

| Deeply embedded dining out culture | +2.5% | United Arab Emirates-wide, strongest in expatriate-dense urban centers | Long term (≥ 4 years) |

| Focus on sustainability and environmental responsibility | +1.5% | Dubai, Abu Dhabi fine dining clusters, expanding to mid-tier concepts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tourism and hospitality expansion

Dubai's visitor arrivals reached 19.59 million in 2025, a 5% increase over 2024, with Western European tourists accounting for 21% of the total and GCC nationals contributing 15%, both cohorts demonstrating higher per-capita restaurant spending than the average, according to the Dubai Department of Economy and Tourism[1]Source: Dubai Department of Economy & Tourism, “Dubai Tourism Performance 2025,” det.gov.ae. Hotel occupancy remained at 80.7% with an average daily rate of AED 579 (USD 158) and revenue per available room of AED 467 (USD 127), indicating robust demand for ancillary services, including in-house and nearby dining. The emirate's positioning as a stopover hub for long-haul routes amplifies short-stay dining occasions; transit passengers with layovers exceeding six hours increasingly book restaurant reservations in advance, a behavior tracked by concierge platforms. Abu Dhabi's integrated resort projects, such as the Ritz-Carlton Reserve slated for 2029, will add high-end culinary venues that cater to ultra-high-net-worth individuals seeking exclusive experiences. This tourism-driven demand underpins the lodging segment's 18.38% CAGR and reinforces the United Arab Emirates's role as a regional gastronomy gateway.

Entry and expansion of international brands

International restaurant chains are increasingly partnering with established United Arab Emirates conglomerates to navigate regulatory complexities and tap into local real estate networks. In December 2024, Chipotle Mexican Grill inked its inaugural franchise deal with M.H. Alshaya Co., setting up shop in Dubai and Kuwait. This move not only marks Chipotle's Middle Eastern debut but also underscores the rising popularity of Latin American cuisine. Steak 'n Shake, in collaboration with Saleh Bin Lahej Group, is rolling out 40 units, eyeing both mall food courts and standalone venues. Meanwhile, Brazilian steakhouse Fogo de Chão opened its doors in Dubai International Financial Centre in 2024, strategically targeting the area's corporate clientele. While these new entrants challenge the market share of established players, they also uplift industry standards. These chains bring in centralized procurement, digital ordering, and rigorous staff training, setting a benchmark that independent operators must meet to keep their clientele.

Influencer and social media discovery

According to a 2025 consumer survey by the Dubai Statistics Center, 70-82% of diners in the United Arab Emirates turn to social media platforms, mainly Instagram, TikTok, and Snapchat, to find restaurants, compare menus, and confirm their choices before making a reservation[2]Source: Dubai Statistics Center, “UAE Dining Frequency Survey 2025,” dsc.gov.ae . Restaurants are increasingly relying on influencer partnerships, dedicating 15-25% of their marketing budgets to both micro and macro influencers. These influencers play a pivotal role, creating user-generated content during exclusive tasting events. The announcement of the MICHELIN Guide Dubai 2025, which recognized 119 restaurants, including four with two stars and 14 with one star, generated a significant buzz on social media. This buzz translated into a 30% spike in online reservations just 48 hours post-announcement. Data from 2024, sourced from Google Trends United Arab Emirates, highlighted the United Arab Emirates's diverse culinary interests: "Indian restaurants" accounted for 34% of all cuisine-related searches, while "Chinese cuisine" saw a 79% year-on-year increase, and "Lebanese cuisine" rose by 32%. This trend underscores the United Arab Emirates's multicultural demographic and its diverse culinary palate. The shift towards a digital-first discovery approach favors visually appealing concepts, while those with a lackluster online presence find themselves at a disadvantage, altering the competitive landscape.

Deeply embedded dining out culture in the country's social life

In 2024, United Arab Emirates residents and expatriates dined out an average of 2.5 times a week, highlighting the significance of dining occasions, as reported by the Dubai Statistics Center. With expatriates making up over 85% of the emirate's population and often lacking extended family networks, restaurants have become the go-to venues for celebrations, business meetings, and weekend gatherings. A 2025 study on consumer priorities revealed that hygiene topped the list of concerns for 50% of diners, followed closely by cuisine type at 49%, ambiance at 43%, service quality at 42%, and value at 38%. This indicates that restaurant operators need to excel in multiple areas to ensure repeat visits. The rise of dual-income households and demanding work hours has intensified the demand for convenient, high-quality dining. This consistent demand bolstered the dine-in segment's 66.12% market share in 2025 and provided a buffer against cyclical downturns, but it also heightened the importance of consistent service and unique menu offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food safety and labelling requirements | -1.2% | United Arab Emirates-wide, with stricter enforcement in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Intensifying competition from QSR/fast-casual formats | -2.5% | Dubai, Abu Dhabi, and Sharjah urban centers | Short term (≤ 2 years) |

| Supply chain vulnerabilities | -1.8% | United Arab Emirates-wide, acute in specialty ingredient categories | Medium term (2-4 years) |

| High rental and operating expenses | -2.3% | Dubai prime districts (DIFC, Jumeirah, Downtown), Abu Dhabi Corniche | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from QSR/fast-casual formats

In 2025, quick-service and fast-casual concepts, many operating from cloud kitchens with minimal front-of-house overhead, captured incremental share from traditional full-service restaurants, particularly among younger consumers prioritizing speed and value. Delivery-first brands, like Kitopi-backed virtual restaurants, harness data analytics to optimize menus and pricing in real time. This agility poses a challenge for full-service operators, who find it hard to replicate without hefty tech investments. In Dubai, the average ticket price for a QSR meal in 2025 undercut that of a full-service dinner, highlighting a price-sensitivity threshold that splits the market. In response, full-service players rolled out takeaway-optimized menus and forged partnerships with aggregators like Deliveroo and Talabat. However, these partnerships come with 20-30% commission fees, further squeezing already-tight margins. The competitive pressure peaks during weekday lunches, as office workers increasingly opt for grab-and-go over sit-down service.

High rental and operating expenses

In 2024, rental prices surged by 15-20% in Dubai's prime dining districts, including the Dubai International Financial Centre, Jumeirah, and Downtown. Notably, certain high-traffic locales witnessed a 25% spike, as reported by CBRE Middle East. These rental hikes, spurred by a limited supply and strong demand from international brands, compelled many independent operators to either shift to secondary areas or exit the market altogether. Concurrently, labor costs surged. This was largely due to the United Arab Emirates government's decision to elevate minimum wage thresholds and enforce stricter visa regulations. As a result, full-service restaurants, which heavily depend on skilled chefs and front-of-house personnel, saw their annual payroll expenses swell by 8-12%. In a region where outdoor dining is only feasible for four months annually, utility expenses, especially for air conditioning, account for 6-8% of a typical operator's revenue. When considering these rising costs, net margins for well-managed establishments dwindle to 8-12%. Meanwhile, less efficient players find themselves operating at a loss. This financial strain has hastened consolidation in the market, with larger chains, benefiting from centralized procurement and economies of scale, emerging as the primary beneficiaries.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: Latin American Surge Challenges Middle Eastern Dominance

In 2025, Middle Eastern cuisine held a 41.62% share, reflecting the United Arab Emirates's ties to the Levant and Gulf. The culinary scene ranges from traditional mezze houses to modern fine dining, like Orfali Bros, which earned a MICHELIN Green Star for its zero-waste approach. Latin American cuisine is projected to grow at a 19.80% CAGR through 2031, driven by openings like Fogo de Chão in Dubai and ALMA Mexican at Emirates Palace. Chipotle's 2024 franchise deal with M.H. Alshaya Co. highlights the United Arab Emirates's role as a launchpad for U.S.-based Latin brands. European cuisine, led by French and Italian fine dining, remains a staple, while Asian offerings thrive due to the United Arab Emirates's large South and East Asian expatriate communities. North American concepts, such as steakhouses and casual dining chains, cater to Western expatriates and tourists. The United Arab Emirates's diverse cuisine mix underscores its global crossroads status, with operators gaining an edge by localizing offerings like date-based desserts or halal-certified proteins.

All cuisines must comply with Dubai Municipality's Food Code and ESMA standards, requiring Certificates of Conformity for imports and regular health inspections[3]Source: Dubai Municipality, “Food Code (Latest Edition),” dm.gov.ae . Latin American growth is boosted by social media, with visually striking dishes like churrasco and ceviche driving discovery among the 70-82% of United Arab Emirates diners who use digital platforms, per Dubai Statistics Center. Middle Eastern operators are modernizing presentations and investing in chef-driven concepts blending heritage and innovation, as seen with Trèsind Studio's three-MICHELIN-star recognition in 2025.

By Outlet Type: Franchise Models Accelerate Despite Independent Majority

In 2025, independent outlets captured a dominant 62.74% share, underscoring the United Arab Emirates's vibrant entrepreneurial dining scene and the allure of chef-owned establishments that promise unique experiences. Meanwhile, chained outlets are on an impressive trajectory, expanding at an 18.72% CAGR through 2031. This growth is largely fueled by international franchisors, who are teaming up with local giants like M.H. Alshaya Co., Apparel Group, and Cravia Inc. These partnerships not only help navigate the intricate regulatory landscape but also secure coveted real estate. Illustrating the franchise model's scalability and shared risk are Steak 'n Shake's 40-unit pact with Saleh Bin Lahej Group and Five Guys' ongoing expansion. While chains enjoy advantages like centralized procurement, uniform training, and robust marketing budgets, luxuries often out of reach for independents, they grapple with tailoring menus to local palates and countering the authenticity narrative that independents champion. In 2024, the United Arab Emirates issued 1,200 new restaurant licenses, split almost evenly between chains and independents, hinting at parallel growth paths, as reported by Dubai Economy.

Technology adoption stands out as a pivotal differentiator; chains harness AI-driven ordering systems, kitchen automation, and CRM platforms to enhance table turnover and tailor promotions. In a bid to bridge this technological divide, independent operators are increasingly collaborating with third-party tech providers. However, they grapple with challenges like implementation costs and the need for staff training. The competitive dynamics are further influenced by the MICHELIN Guide Dubai 2025, which predominantly honored independent, chef-led establishments, bolstering their upscale image. As 2024 saw rental prices in prime areas surge by 15-20%, chains with multiple outlets leveraged their scale to negotiate discounts. In contrast, independents either felt the pinch on their margins or had to consider relocating, as highlighted by CBRE Middle East.

By Location: Standalone Prevalence Meets Lodging Acceleration

In 2025, standalone locations dominated revenue, accounting for 70.82%. This trend reflects the United Arab Emirates's car-centric urban design and the popularity of dining clusters in areas like Jumeirah, Al Barsha, and Abu Dhabi's Corniche. Lodging-based restaurants are projected to grow at a CAGR of 18.38% through 2031, driven by integrated resorts and luxury hotels expanding culinary offerings to boost guest spending and attract external diners. For example, Emirates Palace Mandarin Oriental features 12 diverse dining outlets, while Rosewood Abu Dhabi's 9 restaurants contribute an estimated 30-40% of the property's revenue. The Ritz-Carlton Reserve Abu Dhabi, opening in 2029 with 50 luxury villas, plans to offer exclusive, reservation-only dining experiences at premium prices.

Restaurants in retail spaces, especially in malls like The Dubai Mall and Mall of the Emirates, benefit from high foot traffic but face steep rental costs and short lease terms, limiting capital investments. Airport and transit hub outlets cater to time-sensitive passengers, generating high revenue per square meter but dealing with restrictive concession agreements. Leisure dining spots, such as those on beaches or in entertainment districts, experience seasonal demand influenced by weather and tourism. To address this, standalone operators are investing in outdoor seating and climate-control systems to extend the dining season beyond the November-to-March peak. The lodging segment's growth is supported by the United Arab Emirates's expanding hotel pipeline. Dubai had 150,000 hotel rooms in 2025, with 30,000 more in development, and each new hotel typically adds 3-5 food-and-beverage outlets.

By Service Type: Dine-In Core Coexists with Takeaway Expansion

In 2025, dine-in services accounted for 66.12% of transactions, reflecting the United Arab Emirates's vibrant social dining culture, where ambiance, service, and unique experiences dominate. Takeaway services are growing at an 18.12% CAGR through 2031, driven by platforms like Deliveroo and Talabat strengthening restaurant partnerships and consumers favoring off-premise dining during weekday lunches and late-night meals. According to the Dubai Statistics Center, in 2024, the average United Arab Emirates resident dined out 2.5 times weekly and ordered takeaway 1.2 times, showing that off-premise channels complement dine-in revenues. Full-service operators have introduced takeaway-focused menus with streamlined dishes, tamper-evident packaging, and reheating instructions. However, aggregator commission fees of 20-30% compress margins, forcing operators to raise prices or absorb costs.

Technology is reshaping the landscape; restaurants integrating point-of-sale systems with delivery platforms reduce order errors and improve fulfillment speed, boosting customer satisfaction and loyalty. The MICHELIN Guide Dubai 2025 highlighted restaurants excelling in both dine-in and takeaway, proving off-premise offerings can match on-premise quality when executed well. The United Arab Emirates's focus on experiential dining supports dine-in growth, with concepts like live cooking stations and chef's tables commanding premium checks and generating social media buzz. Takeaway growth is fueled by the United Arab Emirates's 95% smartphone penetration in 2025 and the convenience of cashless payments via Apple Pay and local digital wallets. Rising rental costs in prime areas in 2024 prompted some operators to shift space from dining areas to kitchens, reflecting evolving consumer preferences.

Geography Analysis

The United Arab Emirates restaurant market concentrates primarily in Dubai and Abu Dhabi, which capture most tourism spending and expatriate dining demand. Dubai's position as a business hub and tourist destination ensures consistent demand, enabling premium pricing and diverse cuisine offerings. The city's hospitality infrastructure and continuous development attract international food brands and new dining concepts, positioning it as the core of the United Arab Emirates's foodservice market. Dubai Municipality data shows the Emirate housed 25,000 food establishments in the first half of 2024, indicating its market scale .

Abu Dhabi, as the United Arab Emirates' capital and cultural center, maintains a steady demand for upscale and diverse dining options. The city's government sector presence and cultural institutions support premium full-service restaurants. International events, hospitality developments, and urban expansion increase demand for high-quality dining experiences. Abu Dhabi's steady growth complements Dubai's expansion, establishing these emirates as the primary drivers of the United Arab Emirates restaurant market's volume, revenue, and innovation.

The Northern Emirates, such as Sharjah, Ajman, and Fujairah, offer emerging opportunities through residential development and local economic growth. These regions show increasing consumer spending on foodservice as populations grow and lifestyle preferences change. New retail centers, leisure developments, and infrastructure improvements expand dining demand. This geographic expansion presents growth potential for full-service restaurants in less saturated markets, supplementing the established markets of Dubai and Abu Dhabi.

Competitive Landscape

The United Arab Emirates' Full-service restaurant Market is fragmented, with competition among international chains, regional players, and local independent operators. Companies like Americana Restaurants International and M.H. Alshaya Co. maintain a significant presence through their extensive brand portfolios, while the market structure continues to support innovation and broad participation.

International chains leverage standardized operations and global supply chains to achieve operational efficiency and consistent quality. Local operators focus on cultural authenticity and customized menus that appeal to specific demographic preferences, building customer loyalty in targeted segments. This balance between global reach and local expertise creates a dynamic market environment across all segments.

Technology adoption has emerged as a key differentiator in the market. Operators implement artificial intelligence for personalization, integrated delivery platforms, and digital ordering systems to enhance customer experience and operational efficiency. Growth opportunities exist in underserved cuisine categories, suburban locations, and health-focused dining concepts, reflecting increasing consumer interest in wellness. Market expansion depends on experience enhancement, digital integration, and strategic location selection.

United Arab Emirates Full Service Restaurants Industry Leaders

Americana Restaurants International PLC

M.H. Alshaya Co. WLL

Brinker International Inc.

Al Khaja Group of Companies

Apparel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Atlantis Dubai introduced summer menus at its restaurants. The main course offerings include spicy prawns, roasted truffle duck, stir-fried lotus root, asparagus, black pepper, and edamame egg fried rice.

- July 2025: 3 Fils has opened its second location at The Abu Dhabi Edition hotel. The menu features signature dishes such as Spicy Tuna on Crispy Rice and Uni Scallop Nigiri. The dessert selection includes Coconut Raspberry, Vanilla Flan, and Take Me To The Moon.

- March 2025: Vietnamese Foodies has opened their largest restaurant in Dubai. The menu features signature dishes, such as the 14-hour bone broth and Vit Nuong Hoisin grilled duck breast. The restaurant offers a variety of house-made drinks, including authentic Vietnamese coffees and teas.

- May 2024: Fifth Flavor opened a restaurant in Al Wasl Square, Dubai, offering a contemporary dining environment with a focus on innovative cuisine and desserts.

United Arab Emirates Full Service Restaurants Market Report Scope

Full-service restaurants (FSRs) are dining establishments where customers are seated at a table, their orders are taken by a server, and food is delivered directly to them. The UAE full service restaurants market is segmented by Cuisine, outlet, location, and service type. By cuisine, the market is segmented into Asian, European, Latin American, Middle Eastern, North American, and More. By outlet, the market is segmented into chained outlets and independent outlets. By location, the market is segmented into leisure, lodging, retail, standalone, and travel. By service, the market is segmented into dine-in, takeaway, and delivery. The Market forecasts are provided in terms of value (USD).

| Asian |

| European |

| Latin American |

| Middle Eastern |

| North American |

| Other FSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Cuisine | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| Outlet | Chained Outlets |

| Independent Outlets | |

| Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| Service Type | Dine-in |

| Takeaway |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms