Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

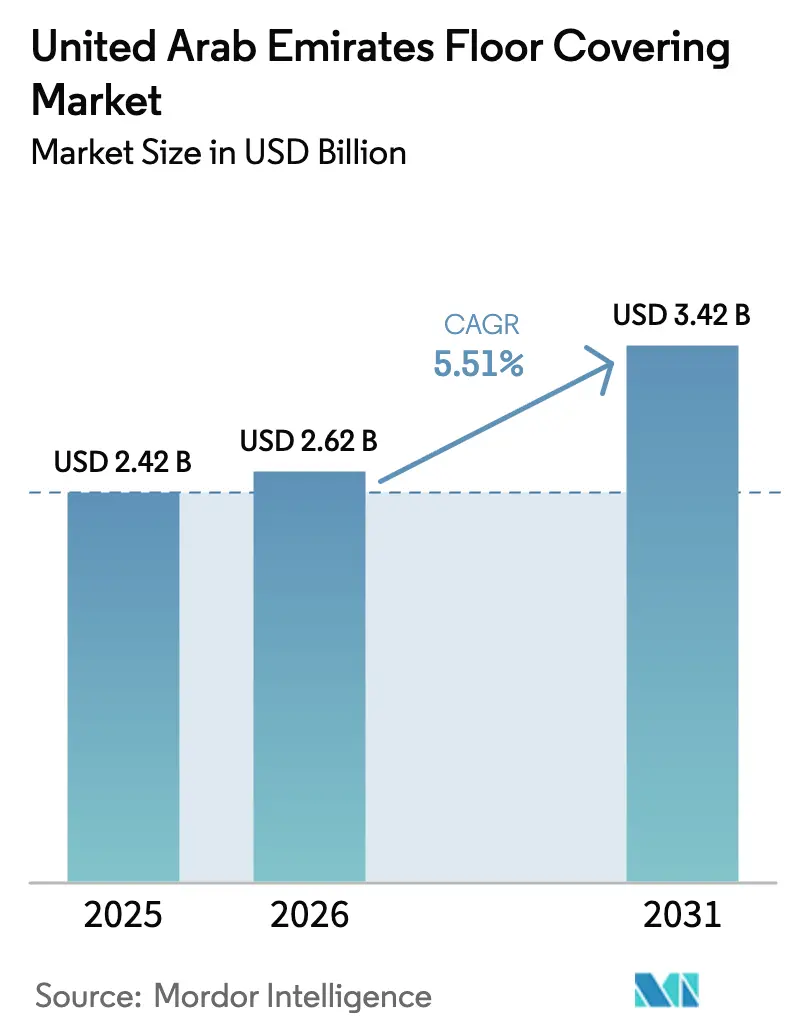

| Base Year Market Size (2025) | USD 2.42 Billion |

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.42 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

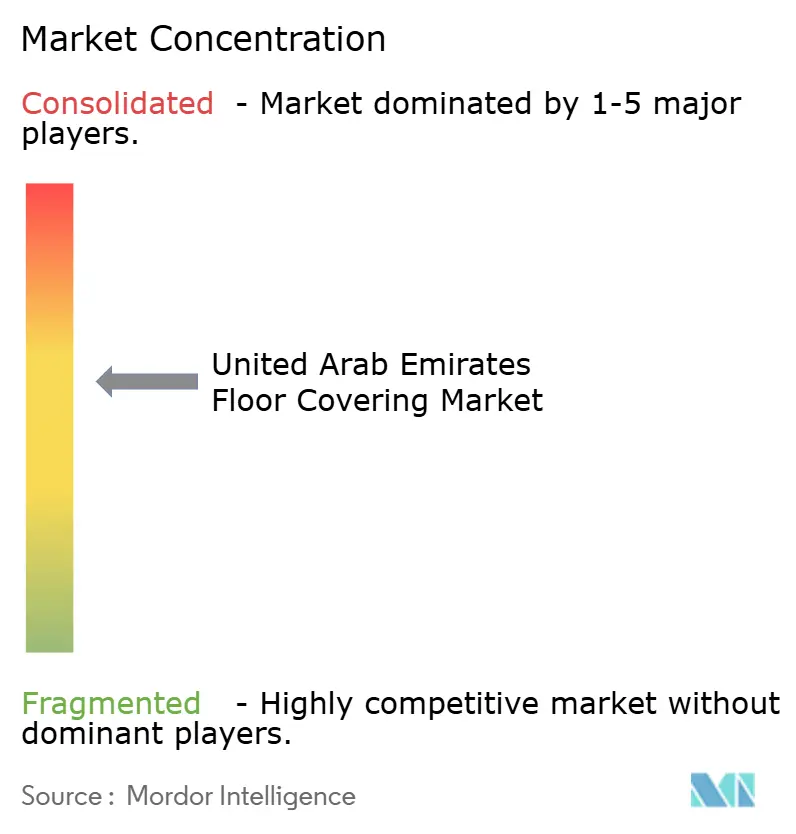

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Floor Covering Market Analysis by Mordor Intelligence

The United Arab Emirates Floor Covering Market size is expected to grow from USD 2.42 billion in 2025 to USD 2.62 billion in 2026 and is forecast to reach USD 3.42 billion by 2031 at a 5.51% CAGR over 2026–2031. This expansion aligns with a shift from discretionary residential upgrades toward public infrastructure, hospitality-led construction, and compute-heavy facilities that sustain multi-year flooring demand in the United Arab Emirates floor covering market. Federal capital expenditure in 2025 totals USD 1,378 million (AED 5,065 million), with the report highlighting federal roads construction and maintenance projects of USD 206.8 million (AED 760 million) for 2024–2025, alongside multiple distinct federal building projects and USD 0.15 billion (AED 0.58 billion) in maintenance expenditures for buildings and roads[1]Source: Ministry of Finance, “Federal General Budget Annual Report 2025,” Ministry of Finance, mof.gov.ae. Visitor volumes also sustain contract activity, with Dubai recording 9.88 million overnight visitors in H1 2025 and maintaining occupancy above 79%, which tightens project timelines and drives the selection of durable, low-maintenance surfaces across the United Arab Emirates floor covering market[2]Source: Dubai Department of Economy and Tourism, “Tourism Performance Report January to June 2025,” Dubai Department of Economy and Tourism, dubaidet.gov.ae. Indoor air quality rules add a second layer of specification discipline that guides material selection for large buildings in both Dubai and Abu Dhabi, which raises the threshold for product compliance and favors proven brands and tested formulations. Data infrastructure plans also create a specialized demand pool for modular raised flooring systems that are engineered for dense electrical and cooling loads, expanding the application mix addressed by the United Arab Emirates floor covering market.

Key Report Takeaways

- By product type, ceramic and porcelain tiles led with 37.32% revenue share in the United Arab Emirates floor covering market in 2025, while vinyl flooring is projected to expand at a 9.76% CAGR through 2031.

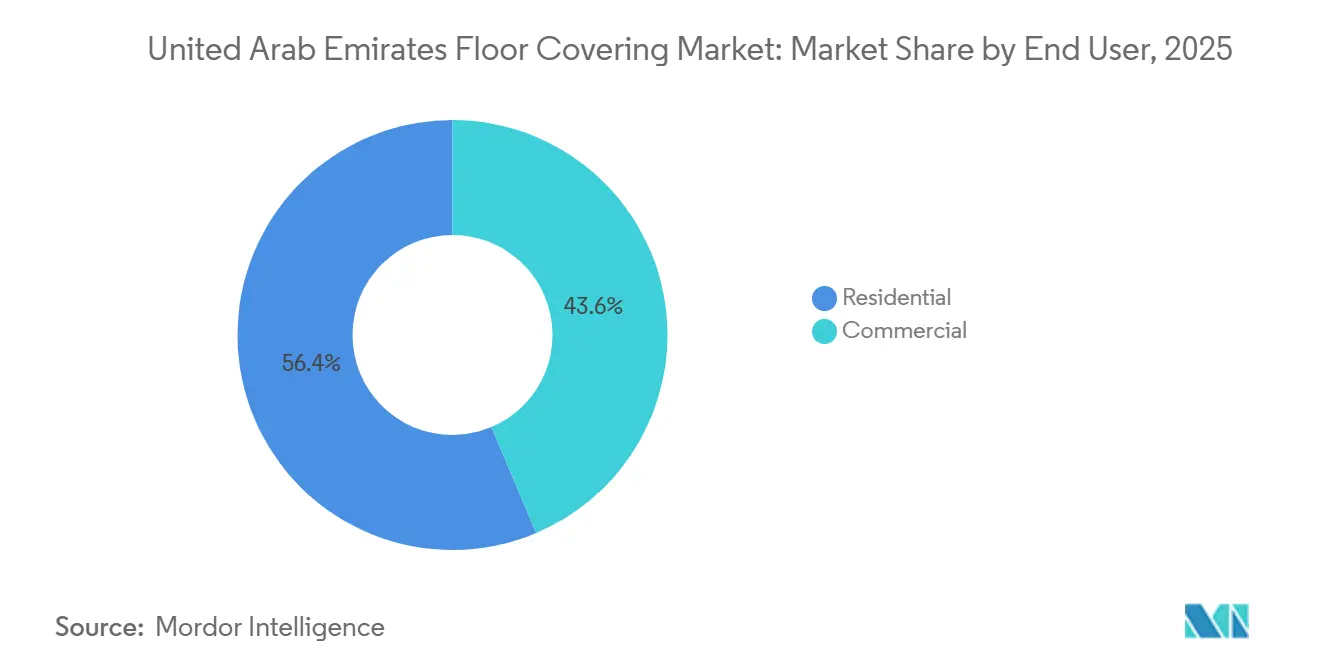

- By end user, residential accounted for a 56.37% share in the United Arab Emirates floor covering market in 2025, and the commercial segment recorded the highest projected growth with a 9.26% CAGR through 2031.

- By distribution channel, B2C retail represented 63.67% of transactions in the United Arab Emirates floor covering market in 2025, while B2B contractors are projected to grow at a 9.87% CAGR during 2026 to 2031.

- By geography, Dubai held 36.37% of market revenue in the United Arab Emirates floor covering market in 2025, and Abu Dhabi is projected to grow at a 10.38% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance-driven public housing programmes | +0.7% | National, concentrated in Abu Dhabi, Sharjah, and the Northern Emirates | Medium term (2-4 years) |

| Tourism-led hospitality expansion | +1.2% | Dubai core, Abu Dhabi growth node, Ras Al Khaimah emerging | Long term (≥ 4 years) |

| Shift toward premium LVT & SPC flooring | +1.4% | Global, with early gains in the Dubai and Abu Dhabi luxury segments | Long term (≥ 4 years) |

| Demand surge from mega mixed-use projects | +0.9% | Dubai (Palm Jebel Ali, Dubai Islands), Abu Dhabi (Saadiyat), Sharjah | Medium term (2-4 years) |

| Mandatory Estidama low-VOC specifications | +0.6% | Abu Dhabi mandatory, Dubai voluntary adoption | Long term (≥ 4 years) |

| Data-centre modular raised-floor boom | +0.8% | Spill-over to Dubai, Abu Dhabi free zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Compliance-Driven Public Housing Programmes Anchor Baseline Demand and Compress Upgrade Cycles

Public housing programs maintain steady unit delivery and increase predictability for flooring volumes, although they can limit room for product premiumization at the point of specification. The Sheikh Zayed Housing Programme disbursed USD 523.22 million (AED 1,922.5 million) across 2,442 beneficiaries in 2024 for new residences and modifications, which channelled demand toward compliant, value-priced materials suitable for baseline codes and rapid handover timelines. Process efficiency improved through VAT refunds for new-build residences, where the Federal Tax Authority processed 6,971 applications in 2024 via the Maskan smart application, which helped accelerate completion milestones and cash-flow clarity for homeowners[3]Source: Federal Tax Authority, “Annual Report 2024,” Federal Tax Authority, tax.gov.ae. The UAE’s specification environment complements these financial measures, since minimum indoor air quality criteria in new buildings steer product selection toward tested formulations that carry recognized certifications. This integrated policy and regulatory framework supports predictable demand patterns in the United Arab Emirates floor covering market through a combination of steady public-housing throughput and compliance-led specifications. These dynamics sustain a consistent baseline for residential installations while enabling scale efficiencies for suppliers that maintain compliant inventories across multiple emirates in the United Arab Emirates floor covering market.

Tourism-Led Hospitality Expansion Elevates Foot-Traffic Resilience and Aesthetic Benchmarks

Demand from hospitality remains an important growth node for the United Arab Emirates floor covering market, with Dubai recording 9.88 million overnight visitors in H1 2025 and maintaining occupancy above 79%, which drives robust refurbishment cycles and steady new-build fit-out activity. Property operators continue to emphasize low-VOC specifications and surfaces that balance durability with guest experience, which pushes the adoption of certified resilient flooring in high-traffic areas and suites where noise attenuation and ease of maintenance matter. This preference aligns with global wellness positioning in upper-tier hospitality, making third-party certification and verifiable product documentation common preconditions in design submittals for the market. The cumulative effect is visible in project tendering that prioritizes reliable lead times and compliant materials, especially for corridors, lobbies, and amenity zones that experience constant footfall. This environment reinforces a long-term volume base for resilient and hard-surface categories within the market, as destination branding and steady visitor flows sustain continuous investment in accommodation assets.

Shift Toward Premium LVT & SPC Flooring Redefines Material Hierarchy and Margin Distribution

Premium LVT and SPC formats continue to gain share due to fast-installation systems, moisture impermeability, and realistic textures that meet aesthetic briefs without structural load penalties common to heavier materials. On the specification side, opacity around subfloor conditions is reduced by rigid cores that maintain dimensional stability across temperature swings, which improves performance in air-conditioned interiors exposed to sand ingress and humidity variations. Pricing ladders show a clear premium tier for commercial-grade SPC offerings that include thicker wear layers and integrated acoustic underlay, reinforcing the value proposition when downtime costs are factored into the total installed price. Resilient flooring growth across the region also creates a favourable backdrop for LVT and SPC adoption in healthcare and education assets, where ease of sanitation and certification trails are critical. These attributes collectively lift the share of resilient formats within project specifications across the market as owners and contractors standardize on quick-turn, compliant solutions.

Data-Center Modular Raised-Floor Boom Multiplies High-Density Infrastructure Demand

Growth in AI-ready and sovereign cloud capacity underpins a specialized demand pool for modular raised floors designed for heavy loads and advanced cable access. The Stargate United Arab Emirates initiative announced by G42 and partners adds a major supercomputing footprint with phased capacity, which accelerates procurement of steel-panel systems with integrated grounding and load-bearing specifications for dense racks. A separate expansion announcement by Microsoft and G42 in November 2025 introduced an additional 200 MW of data center capacity to meet AI and cloud workloads, which reinforces the volume outlook for raised-flooring packages in the United Arab Emirates floor covering market[4]Source: G42, “Microsoft and G42 Accelerate UAE’s Digital Future with Major Data Centre Expansion,” G42, g42.ai. Project schedules emphasize fast delivery for compute workloads, making factory-ready modular systems attractive to EPC contractors and operators. This build-out influences supplier strategies around local inventory, installation training, and quality assurance to meet commissioning windows in 2026 and beyond. The long-tailed nature of digital infrastructure in free zones and industrial districts broadens the addressable mix for the United Arab Emirates floor covering market into technical flooring solutions that differ from standard commercial applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PVC & timber price volatility | -0.9% | Global supply chain, direct impact on UAE imports | Short term (≤ 2 years) |

| Influx of low-cost Asian tile imports | -0.6% | National, competitive pressure on RAK Ceramics, Emirates Ceramics | Medium term (2-4 years) |

| Tight indoor-air-quality emission caps | -0.4% | Abu Dhabi Estidama, Dubai Municipality IAQ guidelines | Long term (≥ 4 years) |

| Shortage of certified master installers | -0.7% | National, acute in specialized segments (SPC, raised floor) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight Indoor-Air-Quality Emission Caps Exclude Non-Certified Products and Elevate Testing Overhead

Dubai Municipality’s IAQ guidelines set clear limits on formaldehyde and total VOC concentrations for new buildings, which compels the use of flooring products and adhesives that comply with independent testing protocols. Field studies in Dubai have highlighted the role of interior materials in cumulative indoor emissions profiles and reinforced the need for certified components across floors, finishes, and furnishings in residential and mixed-use assets. Abu Dhabi planning and sustainability programs further codify expectations for high-performance buildings, as evidenced by Masdar City’s project delivery model that targets Estidama and LEED certifications, which increases documentation and product-selection rigor for the United Arab Emirates floor covering market. Suppliers that can provide consistent testing documentation and environmental product declarations gain an advantage under these rules, particularly for government-linked developments. The net effect narrows supplier pools to firms with robust compliance track records and increases the emphasis on transparent certification in the market.

Shortage of Certified Master Installers Delays Premium Projects and Inflates Labor Budgets

Skill gaps in construction logistics and specialized installation work have measurable impacts on project timelines across the region. A 2025 scholarly assessment of Middle East construction logistics ranked sudden labour shortages and limited expertise among the more influential challenges, underscoring the need for targeted training and skill development in construction processes used by flooring contractors. UAE labour market structure adds complexity since the workforce is predominantly expatriate, which requires ongoing credentialing programs to maintain a pipeline of qualified craft workers for specialized flooring systems. The federal priority on workforce development includes accreditation frameworks for professional skills, which aim to alleviate bottlenecks in certified trades that are relevant to complex installations in the United Arab Emirates floor covering market. Technical flooring categories like click-lock SPC or modular raised floors require trained crews with precise tolerances, which shape contractor selection and on-site supervision practices. These labour dynamics influence procurement and scheduling strategies along the supply chain for the United Arab Emirates floor covering market, where project delivery depends on proven installer credentials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vinyl Surges as Ceramics Hold but Shift to Slabs

Ceramic and porcelain tiles led the category mix with a 37.32% share in 2025, which reflects specification compatibility with strict indoor air quality and durability criteria in public and hospitality assets in the United Arab Emirates floor covering market. RAK Ceramics’ domestic capacity and active project channel participation underpin this position, supported by ongoing upgrades and capital investments disclosed in the 2025 releases. The company also scaled slab formats for large areas and premium settings, which enables designers to minimize joints and reduce grout maintenance in high-visibility zones. In parallel, the regulatory environment in Dubai and Abu Dhabi keeps a premium on tested and certifiable surfaces, which helps ceramic and porcelain retain a core role in institutional and hospitality specifications. This mix positions porcelain slabs and high-performance gres variants as complementary to resilient formats in the United Arab Emirates floor covering market.

Vinyl flooring, which includes LVT and SPC, is projected to grow the fastest at a 9.76% CAGR from 2026 to 2031, as click systems and waterproof cores shorten renovation cycles and simplify installation planning in the United Arab Emirates floor covering market. Regional production investments by global brands improved availability and lead times for rigid LVT, supporting adoption across commercial and residential renovations. The performance of rigid-core planks in climate-controlled interiors and sandy conditions is a practical driver for facility managers to commit to resilient surfaces in high-traffic corridors. Premium SPC products position above mid-range alternatives on wear-layer thickness and integrated acoustics, which fit hotel and healthcare needs for quiet and durable surfaces with lower disruption risk during turnaround windows. The resulting convergence between performance, compliance, and lifecycle cost reinforces the format’s multi-year growth profile within the United Arab Emirates floor covering market.

By End User: Residential Absorbs Subsidies, while Commercial Rides Hospitality Momentum

Residential accounted for 56.37% of installations in 2025, consistent with state-backed housing programs, VAT refunds for new homes, and consumer preferences for value-aligned products that meet code and IAQ requirements in the United Arab Emirates floor covering market. Funding flows under the Sheikh Zayed Housing Programme totalled USD 523.22 million (AED 1,922.5 million) in 2024, which kept volume steady and sustained procurement predictability for compliant flooring selections in new units and modifications. Administrative support accelerated handover cycles as 6,971 VAT refund applications were processed by the Federal Tax Authority, which helped to de-bottleneck delivery and installation scheduling in residential projects. This baseline supports consistent throughput in the United Arab Emirates floor covering market across villas and multi-family units when coupled with showroom-driven product selection for finishes. The distribution of spend favors ceramic and resilient alternatives that provide predictable performance under code and warranty conditions for occupied homes.

Commercial is projected to grow at a 9.26% CAGR through 2031, driven by hospitality fit-outs and refurbishments, as well as compute-related facilities that require technical flooring systems in the United Arab Emirates floor covering market. Hotel occupancy and visitor growth in Dubai through H1 2025 support frequent refresh cycles for lobbies and corridors, where resilient surfaces with low VOC profiles and realistic textures meet brand standards for guest experience. In data infrastructure, multi-hundred-megawatt capacity additions announced by Microsoft and G42 for the United Arab Emirates, signalling 2026 readiness, create a distinct demand for modular raised floors designed for high-density cooling and power. This subsegment resides alongside retail and office fit-outs, which prize reconfigurable surfaces that support tenant changes with limited disruption. Together, these drivers diversify commercial flooring demand beyond hospitality and increase the share of specialized systems within the United Arab Emirates floor covering market.

By Distribution Channel: Retail Showrooms Dominate Yet Contractor Direct Gains on Mega-Project Velocity

Retail showrooms handled 63.67% of transactions in 2025, reflecting the role of in-store selection for texture, finish, and acoustic performance in large residential purchases within the United Arab Emirates floor covering market. Domestic brands also integrate retail presence with project channels, leveraging capacity, compliance, and design curation to influence both trade and end-consumer decisions in the United Arab Emirates floor covering market. This model encourages larger ticket sizes that combine floor coverings with adjacent categories, particularly in new-home packages. The result maintains high showroom relevance even as commercial demand accelerates.

Contractors are projected to grow at a 9.87% CAGR as public tenders and hospitality fit-outs compress lead times and tighten specification control in the United Arab Emirates floor covering market. Procurement teams value just-in-time deliveries, certified documentation, and consistent lot quality as they stage materials for multi-building master plans and large hospitality assets. Suppliers with regional inventory and robust certification stacks gain an advantage in contractor-direct frameworks that lock in technical details during design development. Framework agreements and staged delivery arrangements support price certainty and coordination across phases, which strengthens contractor-direct purchasing. This supports a gradual channel shift toward wholesale project execution in the United Arab Emirates floor covering market.

Geography Analysis

Dubai held 36.37% of market revenue in 2025, supported by large hospitality capacity and steady visitor throughput that together sustain frequent refurbishment and expansion cycles in the United Arab Emirates floor covering market. Dubai welcomed 9.88 million overnight visitors in H1 2025 and maintained occupancy above 79%, which kept hotel operators on a consistent upgrade cadence across public areas and guestrooms. The city’s compliance environment complements these cycles, since indoor air quality rules steer product choices toward low-emission solutions that support guest comfort and operational standards. Developers and operators coordinate specifications to balance aesthetic outcomes with durability under high footfall and environmental factors. These conditions set stable foundations for project volume within the UAE floor covering market in Dubai.

Abu Dhabi is projected to post the highest growth at a 10.38% CAGR from 2026 to 2031 as public-sector commitments and sustainability mandates shape a defined pipeline for compliant flooring solutions in the United Arab Emirates floor covering market. The combination of citizen housing support and VAT refund processing for new residences accelerates build-and-handover cycles, which supports consistent demand for compliant surfaces in new communities. Masdar City’s emphasis on Estidama and LEED delivery sets a template for city-scale sustainability requirements that cascade to flooring product specifications. Large cultural and innovation districts replicate these documentation standards for quality and emissions, tightening supplier pools to firms with comprehensive test records. These elements work together to support a durable growth profile for the United Arab Emirates floor covering market in Abu Dhabi.

The rest of the United Arab Emirates includes emirates with targeted tourism and industrial initiatives that broaden the demand profile for floor coverings beyond the two largest markets. Data infrastructure and sovereign cloud capacity expansions announced by G42 and partners strengthen the case for technical flooring systems in free zones and industrial campuses, which adds a specialized component to regional demand. This growth layer complements residential and retail projects that follow local development strategies. Suppliers that maintain compliant inventories and installation readiness across multiple emirates capture these multi-track opportunities in the United Arab Emirates floor covering market. The resulting mosaic makes the regional demand base more resilient than single-sector models. It also supports a distribution footprint aligned with public-sector timelines and regulatory expectations.

Competitive Landscape

The United Arab Emirates floor covering market features moderate concentration with meaningful roles for domestic manufacturers and international brands that localize supply and compliance. RAK Ceramics anchors local tile supply with extensive installed capacity and disclosed capital programs that include slab production capabilities to serve premium and large-area projects. The company’s project and retail exposure across the United Arab Emirates enables coordinated fulfillment and increases responsiveness to developer schedules in the United Arab Emirates floor covering market. International manufacturers are also bolstering regional access, as evidenced by Tarkett’s JV setup to manufacture rigid LVT in the Gulf, which supports quick-turn resilient offerings and improves control over certification and documentation. Compliance leadership factors into competitive advantage, particularly on large public or hospitality projects that operate under strict IAQ rules. These dynamics maintain room for multiple players across categories in the United Arab Emirates floor covering market.

Strategic moves in 2025 illustrate expansion, integration, and product capability upgrades that align with priority segments. RAK Ceramics increased its capital expenditure and reported steady project and retail momentum while commissioning slab production to serve high-end applications and reduce installation joints. The company’s portfolio breadth supports combined bathroom and flooring packages for project owners, which can simplify procurement in the United Arab Emirates floor covering market. Tarkett’s regional manufacturing plan for rigid LVT synchronizes with the rising adoption of premium resilient formats in hospitality and healthcare across the Gulf. Sustainability-focused building environments in Abu Dhabi and Dubai reward surfacing solutions with validated emissions profiles, which narrows approval lists and favours brands with extensive test libraries. These steps underpin a competitive field that balances scale production, design, and compliance within the United Arab Emirates floor covering market.

Category adjacency and innovation are also visible. RAK Porcelain Group broadened its European presence with a 2025 brand acquisition that leverages related distribution and design ecosystems relevant to premium interior specifications. Local innovators are moving to meet emissions constraints in wood-based subfloors and parquet components, as seen in DesertBoard’s formaldehyde-free certification milestone in 2025. This progress complements the market’s emphasis on compliance for interior surfaces and supports a broader supply base that can answer diverse project needs in the United Arab Emirates floor covering market. Microsoft and G42’s data centre expansion announcement adds a technology-led demand pathway for modular raised-floor systems that rely on specialized suppliers, which further diversifies the competitive canvas. The combined set of moves points to a market in which scale, compliance, and application specialization shape competitive outcomes.

United Arab Emirates Floor Covering Industry Leaders

RAK Ceramics

Carpet Land

AB Gustaf Kahr

Emirates Ceramic

Terrazzo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Microsoft and G42 announced a 200 MW datacenter capacity expansion in the UAE to serve AI and cloud workloads with commissioning before end-2026.

- November 2025: Flooring House introduced the Richmond Chevron SPC Elite collection to the UAE market with commercial-grade wear layers and integrated acoustic underlay.

- October 2025: RAK Porcelain Group completed the acquisition of Bankook Design Chambre S.L., owner of Cookplay, deepening its premium tableware portfolio and European exposure.

- September 2025: DesertBoard received Abu Dhabi Quality and Conformity Council certification for formaldehyde-free palm-strand boards used in subflooring and parquet components.

United Arab Emirates Floor Covering Market Report Scope

Flooring and carpets are essential in households and have various applications in different settings. These materials are crafted from wood, polymer staple fibers, vinyl sheets, ceramic tiles, carpets, and rugs. The United Arab Emirates floor covering market is segmented by product type, end user, distribution channels, and region. By product type, the market is segmented into carpet & area rugs, wood flooring, ceramic tile, laminate flooring, vinyl flooring [LVT, Sheet, VCT], stone flooring, and other products. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/retail, B2B/contractors. By geography, the market is segmented into Dubai, Abu Dhabi, and the Rest of the UAE. The report offers market size and forecasts for the United Arab Emirates floor covering market in value (USD) for all the above segments.

By Product Type

| Carpet & Area Rugs |

| Wood Flooring |

| Ceramic & Porcelain Tiles |

| Laminate Flooring |

| Vinyl Flooring (LVT, Sheet, VCT) |

| Stone Flooring |

| Other Products |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors |

By Region

| Dubai |

| Abu Dhabi |

| Rest of UAE |

| By Product Type | Carpet & Area Rugs | |

| Wood Flooring | ||

| Ceramic & Porcelain Tiles | ||

| Laminate Flooring | ||

| Vinyl Flooring (LVT, Sheet, VCT) | ||

| Stone Flooring | ||

| Other Products | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors | ||

| By Region | Dubai | |

| Abu Dhabi | ||

| Rest of UAE | ||

Key Questions Answered in the Report

What is the size and growth outlook for the United Arab Emirates floor covering market through 2031?

The United Arab Emirates floor covering market size is USD 2.62 billion in 2026 and is projected to reach USD 3.42 billion by 2031 at a 5.51% CAGR, reflecting steady public, hospitality, and data-infrastructure demand.

Which product categories are leading, and which are growing fastest in the United Arab Emirates floor covering market?

Ceramic and porcelain tiles lead with a 37.32% share in 2025, while vinyl formats, including LVT and SPC, are projected to expand at a 9.76% CAGR through 2031.

How is end-user demand split in the United Arab Emirates floor covering market, and where is growth strongest?

Residential accounts for 56.37% of installations in 2025, supported by housing programs and VAT refunds, while commercial is projected to grow fastest at a 9.26% CAGR due to hospitality and data-centre fit-outs.

Which distribution channels are most relevant in the United Arab Emirates floor covering market?

B2C retail showrooms handle 63.67% of transactions for in-person selection, while B2B contractor-direct is projected to grow at a 9.87% CAGR on public and hospitality tenders with tight specification control.

What geographic patterns define demand in the United Arab Emirates floor covering market?

Dubai holds 36.37% of 2025 revenue on the back of tourism throughput and steady refurbishment cycles, while Abu Dhabi is projected to lead growth at a 10.38% CAGR with sustainability-led development.

Which regulations matter most for product selection in the United Arab Emirates floor covering market?

Dubai IAQ guidelines and Abu Dhabi sustainability mandates drive low-emission material selection, favouring flooring with robust certification and documentation across major public and hospitality projects.

Page last updated on: