Market Overview

| Study Period | 2020 - 2031 |

|---|---|

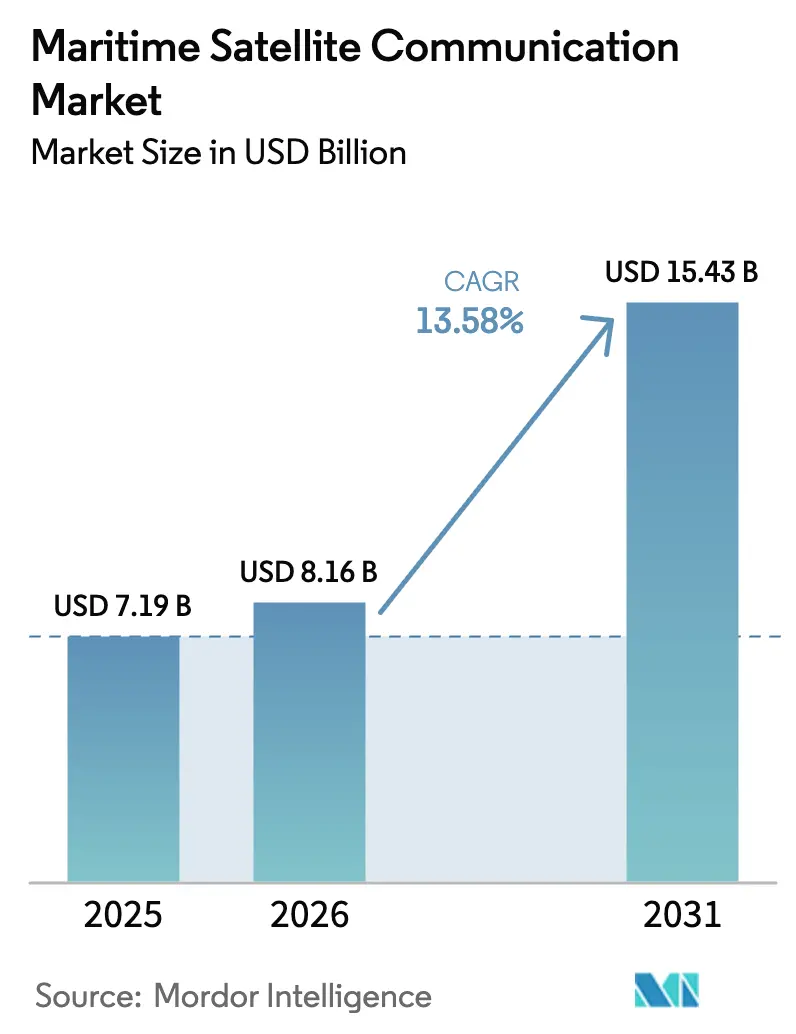

| Market Size (2026) | USD 8.16 Billion |

| Market Size (2031) | USD 15.43 Billion |

| Growth Rate (2026 - 2031) | 13.58% CAGR |

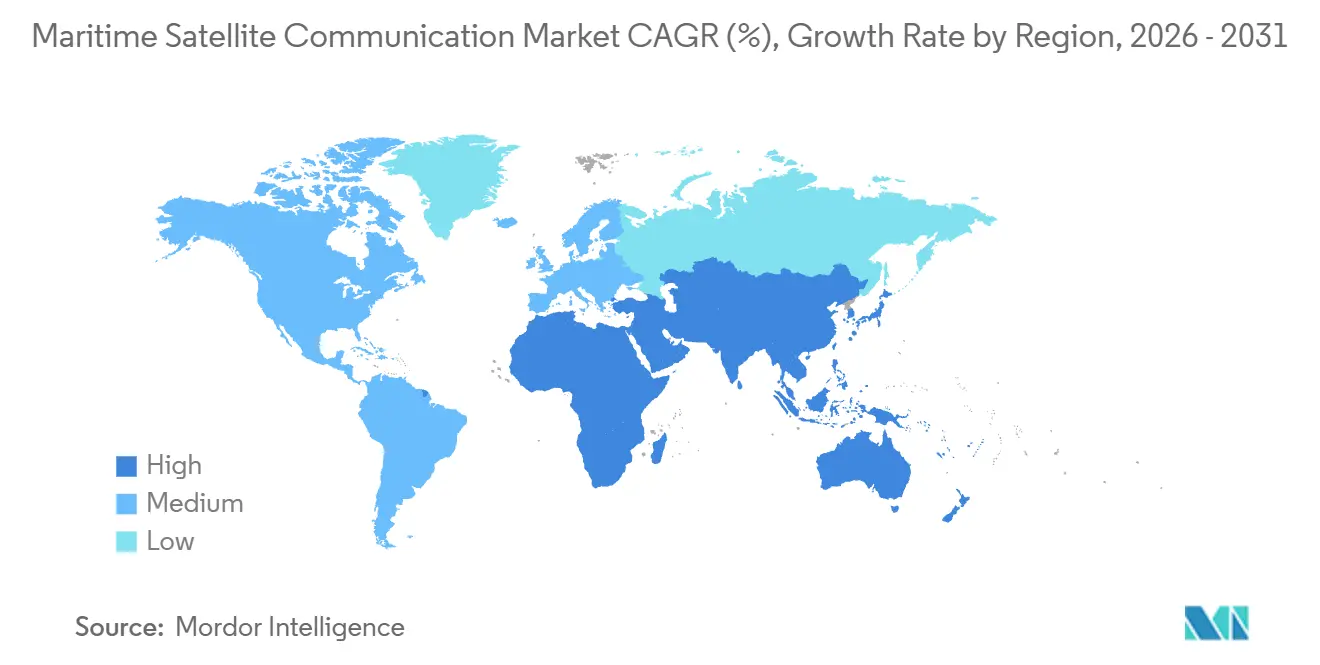

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

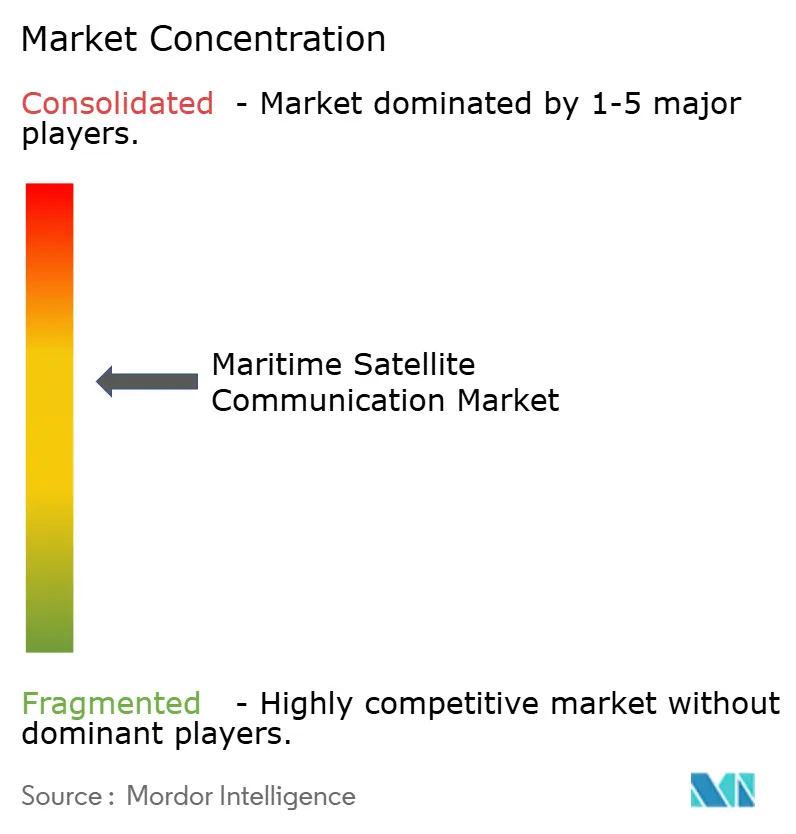

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Maritime Satellite Communication Market Analysis by Mordor Intelligence

The Maritime Satellite Communication Market size is projected to expand from USD 7.19 billion in 2025 and USD 8.16 billion in 2026 to USD 15.43 billion by 2031, registering a CAGR of 13.58% between 2026 to 2031. Rising regulatory reporting, low-latency LEO capacity, and crew-welfare mandates are moving connectivity from a cost center to an operational pillar of fleet efficiency. Vessel operators now bundle fuel-emissions telemetry, AI route optimization, and passenger internet on the same link, accelerating hardware refresh cycles and service-layer innovation. Price disruption from Starlink and OneWeb is forcing incumbents to defend share by offering turnkey cybersecurity and analytics, while flat-panel antennas are shrinking form-factor barriers for fishing, leisure, and coastal craft. At the same time, hybrid VSAT-5G hand-off solutions are lowering near-shore airtime expenses, and classification societies are certifying integrated SATCOM-plus-software suites that satisfy IMO carbon-intensity rules.

Key Report Takeaways

- By connectivity type, geostationary VSAT led with 49.32% revenue share in 2025; non-GEO broadband is advancing at a 14.12% CAGR to 2031.

- By frequency band, Ku-Band accounted for 38.63% of the maritime satellite communication market share in 2025, while Ka-Band is forecast to grow at a 14.23% CAGR through 2031.

- By offering, connectivity services held 46.28% of the maritime satellite communication market size in 2025, and managed services are expanding at a 15.32% CAGR to 2031.

- By end user, merchant cargo and tanker vessels commanded 29.47% revenue share in 2025; passenger vessels recorded the highest 16.72% CAGR through 2031.

- By geography, the Asia Pacific contributed 32.71% of the revenue in 2025, whereas Africa is poised for the fastest growth of 14.83% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Maritime Satellite Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Crew Welfare Mandates and Onboard Digitalization | +2.8% | Global, early adoption in Europe and North America | Medium term (2-4 years) |

| Emergence of LEO Constellations Disrupting Bandwidth Economics | +3.2% | Global, accelerated in Asia Pacific and North America | Short term (≤ 2 years) |

| IMO Decarbonization Data-Reporting Requirements | +2.1% | Global, driven by IMO MEPC resolutions | Long term (≥ 4 years) |

| Hybrid VSAT-5G Coastal Hand-Off Architectures | +1.4% | North America, Europe, coastal Asia Pacific | Medium term (2-4 years) |

| AI-Driven Route Optimization Platforms Embedding SATCOM | +1.9% | Global, concentrated in merchant cargo and tanker segments | Medium term (2-4 years) |

| Rising Defence Demand for Resilient Maritime SATCOM | +1.7% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Crew Welfare Mandates And Onboard Digitalization

Amendments to the Maritime Labour Convention, ratified in 2024, oblige shipowners to provide reasonable internet access, making broadband a compliance item rather than a perk.[1]International Labour Organization, “Maritime Labour Convention Amendments 2024,” ilo.org Seafarer surveys in 2025 ranked Wi-Fi among the top three retention factors, linking connectivity directly to crew turnover costs. Operators now merge welfare and operational data over a single high-capacity Ka-Band link, prompting shipyards to pre-install flat-panel antennas on newbuilds. The shift is most visible in long-haul container and tanker tonnage, where rotations last eight months, and mental-health benefits translate into safety gains. Overall, crew mandates underpin steady demand for bandwidth, insulating the maritime satellite communication market from price volatility.

Emergence Of LEO Constellations Disrupting Bandwidth Economics

Starlink Maritime delivers sub-40 ms latency and speeds up to 220 Mbps, commoditizing raw bandwidth and forcing GEO incumbents to pivot toward service layers. OneWeb’s global footprint and flat-rate packages remove per-megabyte overage fees, while Project Kuiper is slated to enter trials in 2026, intensifying price pressure. Vessel operators embrace LEO for real-time video, cloud dashboards, and remote piloting, yet phased-array antennas raise capital hurdles and create a niche for hybrid GEO-LEO terminals. As multi-orbit modems mature, the maritime satellite communication market is migrating to flexible architectures that select the optimal link per application. The immediate result is double-digit traffic growth, especially on cruise, offshore energy, and research vessels.

IMO Decarbonization Data-Reporting Requirements

The IMO Data Collection System and CII grading compel ships above 5,000 GT to transmit fuel consumption and voyage emissions daily.[2] International Maritime Organization, “IMO Data Collection System for Fuel Oil Consumption,” imo.org Continuous telemetry demands encrypted satellite links, turning connectivity into a prerequisite for port clearance and insurance underwriting. Shipowners integrate weather, sea-state, and fuel-flow data with AI route planners, cutting fuel 8%-12% and improving their CII grade. Classification societies now certify SATCOM-plus-analytics packages that consolidate compliance and efficiency. Consequently, decarbonization regulation provides a durable volume floor for the maritime satellite communication market.

Hybrid VSAT-5G Coastal Hand-Off Architectures

Dual-mode terminals switch to 5G within 12 nautical miles of shore, lowering airtime costs by up to 70% and freeing satellite capacity for blue-water legs. FCC spectrum allocations and European port 5G corridors hasten adoption, especially among ferries and offshore supply vessels. Integrated vendors bundle Ku-Band VSAT, 5G radios, and SD-WAN controllers, delivering a single invoice and seamless performance. Regional spectrum fragmentation, however, requires multi-band support and diverse authentication protocols. Overall, coastal hand-off expands addressable demand without eroding satellite revenue, reinforcing the maritime satellite communication market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Flat-Panel Antennas | −1.8% | Global, acute for small fleets in Africa and South America | Short term (≤ 2 years) |

| Cybersecurity Compliance Burden for Small Fleets | −1.2% | North America and Europe | Medium term (2-4 years) |

| Spectrum Coordination Congestion in Ku/Ka | −0.9% | Global, bottlenecks in Asia Pacific and Europe | Long term (≥ 4 years) |

| Export-Control Limits on Advanced Modems | −0.7% | Middle East, Africa, select Asia Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX For Flat-Panel Antennas

Electronically steered antennas cost USD 15,000-50,000 per unit, representing up to 25% of some small-vessel annual budgets. Early models also suffered performance degradation in rough seas, leading operators to defer purchases until second-generation units emerged. Leasing programs bundle hardware and airtime to soften upfront spending but lock customers into multi-year terms that lengthen payback periods. The gap creates a two-tier connectivity landscape, where large fleets enjoy multi-gigabit LEO links and small craft remain on narrowband L-Band. Unless hardware prices fall sharply, CAPEX friction will temper adoption velocity in the maritime satellite communication market.

Cybersecurity Compliance Burden For Small Fleets

USCG rules and IACS requirements mandate network segmentation, encryption, and continuous monitoring, adding USD 10,000-30,000 in hardware and audit costs per vessel. For operators on thin margins, these expenses can exceed annual connectivity fees, deterring them from upgrading. Managed-service providers offer turnkey compliance, but outsourcing concentrates risk and introduces vendor lock-in. Cyber rules nevertheless remain non-negotiable for port access, prompting some owners to delay nonessential digitalization until subsidized options become available. Over the medium term, compliance outlays may weigh on the maritime satellite communication market, especially in fragmented coastal trades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity Type: LEO Gains Share As GEO Defends Installed Base

Revenue from non-GEO broadband is expanding at 14.12% CAGR, underscoring the speed with which operators are migrating to low-latency solutions. The maritime satellite communication market size attached to geostationary VSAT remains sizable because 49.32% of 2025 connectivity revenue flowed through established GEO contracts. Yet LEO newcomers are eroding price points, prompting GEO providers to fold cybersecurity and analytics into long-term bundles. Hybrid modems that mesh LEO and GEO on a single enclosure blur segmentation boundaries and future-proof fleet investments. SpaceX’s direct-to-cell capability, entering trials in 2026, could siphon narrowband spending by allowing smartphones to connect to satellites without specialized terminals.

Continued MEO investment by SES offers mid-latency alternatives where polar coverage or guaranteed uptime is critical. ITU spectrum rulings have lessened interference worries and bolstered low-orbit deployment plans. Overall, the maritime satellite communication market sees connectivity choice shifting from orbit-centric to performance-centric procurement, with service quality, SLA uptime, and cybersecurity overtaking raw bandwidth in contract criteria.

By Frequency Band: Ka-Band Ascends As Flat Panels Proliferate

Ka-Band revenue is projected to grow 14.23% CAGR, the highest among bands, as lightweight flat-panel antennas dominate new installations. Ku-Band retains a 38.63% slice of maritime satellite communication market share due to a vast installed reflector base and plentiful GEO capacity. Yet Ku filings are waning while Ka and emerging Q/V bands attract fresh satellite investment. Renesas beamforming chips have cut Ka-terminal power use 40% and pushed unit pricing below USD 20,000, driving mid-size merchant adoption.

Flat-panel gain constraints favor higher frequencies, anchoring Ka-Band’s growth narrative. L-Band maintains a vital safety niche for GMDSS and IoT, but limited throughput caps its commercial upside. Regulatory moves to authorize maritime 5G-satellite hybrids in the 27.5-28.35 GHz slice further brighten Ka prospects.[3]Federal Communications Commission, “Maritime 5G Spectrum Allocation,” fcc.gov Consequently, frequency strategy now hinges on matching antenna economics with application bandwidth, locking Ka-Band into pole position within the maritime satellite communication market.

By Offering: Managed Services Outpace Airtime As Cyber And Analytics Add Value

Managed and value-added services are growing at a 15.32% CAGR, reflecting an industry shift from selling megabytes to selling outcomes. Although connectivity plans still accounted for 46.28% of 2025 revenue, commodity pricing prompted providers to incorporate cybersecurity, CII reporting, and AI routing into bundled contracts. KVH’s connectivity-as-a-service model waives terminal CAPEX in exchange for multi-year fees, inflating lifetime value while raising switching barriers. The maritime satellite communication market size tied to hardware alone is flattening as amortized subscription models reclassify capital outlays as operating costs.

Service portfolios now range from 24/7 SOC monitoring to telemedicine links. Certification by DNV and Lloyd’s Register lends credibility and eases compliance headaches for operators. However, deep integration can handcuff owners if performance disappoints, and termination penalties often exceed USD 50,000 per vessel. The commerce prize, therefore, belongs to vendors that pair open architectures with tangible ROI metrics.

By End-User Vertical: Cruise Connectivity Surges As Passengers Demand Gigabit Wi-Fi

Passenger vessels are forecast to post a 16.72% CAGR, the fastest within end users, as cruise lines monetize high-speed internet packages and leverage free Wi-Fi as a booking incentive. Merchant cargo and tanker ships still represent the largest slice of the maritime satellite communication market, contributing 29.47% of the revenue in 2025, as they dominate global tonnage and must meet IMO reporting rules. Offshore energy platforms integrate SATCOM with edge computing to predict equipment failures, resulting in tangible downtime savings. Fishing and aquaculture adopt low-bandwidth L-Band IoT to validate quota and deter illegal catch, while superyacht owners specify Ka-Band flat panels for entertainment and remote work.

Defence procurement remains robust as navies pursue anti-jamming resilience. Multi-orbit terminals ordered by the U.S. Navy and NATO allies are expected to trickle down to commercial production volumes, reducing per-unit costs and broadening uptake. Overall, usage diversity protects the maritime satellite communication market from cyclical shocks in any single shipping segment.

Geography Analysis

The Asia Pacific contributes 32.71% of the 2025 revenue, reflecting its concentration in shipbuilding, container traffic, and fishing operations. Chinese, Japanese, and South Korean yards pre-wire new hulls with Ka-Band flat panels to meet charterer connectivity clauses. Belt-and-Road port digitalization in Southeast Asia embeds satellite-based manifest and AIS requirements, expanding regional demand. Japan’s autonomous coastal corridor tests lean on low-orbit backhaul for HD video and LiDAR streams. India’s Sagarmala expansion is adding AIS and SATCOM mandates for coastal cargo vessels, reinforcing volume.

Africa is the fastest-growing region, with a 14.83% CAGR, as Nigeria, Kenya, and South Africa digitalize their ports with satellite container tracking, financed by multilateral lenders. South-Atlantic fisheries deploy L-Band IoT to enforce quotas, yet CAPEX hurdles constrain the adoption of flat-panel technology. North Africa’s offshore oil reactivation in Egypt and Libya injects high-throughput VSAT spending.

North America and Europe sustain steady growth on the back of stringent cyber mandates and early hybrid VSAT-5G rollouts. The U.S. Gulf of Mexico 5G trials and EU Connecting Europe Facility grants incentivize terminal upgrades. Middle-East energy majors equip tankers with multi-orbit links to oversee cargo integrity through chokepoints. South America’s deep-water oil in Brazil and Guyana deploys GEO-HTS, while Argentina’s fisheries migrate to Ku for electronic documentation. Together, these dynamics keep geographic demand broad and resilient for the maritime satellite communication market.

Competitive Landscape

The top five providers, Inmarsat, Viasat, Speedcast, Marlink, and KVH, held roughly 55-60% global revenue in 2025, signaling moderate concentration. Starlink Maritime’s flat-rate offer is fragmenting share, compelling incumbents to differentiate through managed services and uptime SLAs. Viasat’s acquisition of Inmarsat’s government unit and Eutelsat’s merger with OneWeb create vertically integrated giants controlling satellite capacity and service layers.

Technology is the weapon of choice. Intellian’s multi-band flat panel and Iridium’s compact Certus 9704 terminal target opposite ends of the vessel spectrum, from large cargo ships to small fishing boats. Hybrid GEO-LEO modems and 5G satellite edge devices are forming new competitive arenas, where smaller specialists, such as Tototheo Maritime, are carving out niches. Regulatory tightening around cybersecurity pushes providers to bundle SOC oversight, further blurring lines between connectivity and IT outsourcing.

Service lock-in, driven by subscription bundles and proprietary analytics, raises switching costs and extends the average customer life. Conversely, over-the-air firmware and open-API designs offer a countertrend toward interoperability, giving fleet managers leverage in negotiations. Against this backdrop, price competition in raw bandwidth coexists with premium pricing for integrated solutions, shaping profit pools across the maritime satellite communication market.

Maritime Satellite Communication Industry Leaders

Inmarsat Group Limited

Marlink SAS

KVH Industries Inc.

Speedcast International

NSSL Global Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Eutelsat OneWeb began live trials of 5G backhaul over its LEO network on feeder vessels serving North Sea offshore wind farms.

- October 2025: SpaceX deployed its 8,000th Starlink satellite, extending polar coverage and surpassing 15,000 maritime subscribers.

- September 2025: Viasat integrated Inmarsat Fleet Xpress into its Ka-Band network, creating a unified GEO-LEO platform for 12,000 maritime customers.

- August 2025: Carnival Corporation has signed a USD 250 million contract to retrofit 92 cruise ships with Starlink terminals, aiming for 40% growth in onboard connectivity revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the maritime satellite communication market as the total revenue generated worldwide from ship-borne hardware, airtime, and managed value-added services that rely on L-, C-, Ku-, and Ka-band links supplied through geostationary and non-geostationary satellites. According to Mordor Intelligence, the scope spans merchant cargo, passenger, offshore energy, fishing, leisure, and governmental vessels that require voice, data, or video connectivity while at sea.

(Exclusion) Military tactical satcom terminals that operate exclusively on classified networks are kept outside this assessment.

Segmentation Overview

- By Connectivity Type

- Mobile Satellite Services (MSS)

- Geostationary VSAT

- Non-GEO Broadband (LEO/MEO)

- By Frequency Band

- L-Band

- S-Band

- C-Band

- Ku-Band

- Ka-Band

- By Offering

- Hardware and Terminals

- Connectivity Services (Airtime)

- Managed and Value-Added Services

- By End-User Vertical

- Merchant Cargo and Tanker

- Offshore Energy and Support Vessels

- Passenger (Cruise and Ferry)

- Fishing and Aquaculture

- Leisure and Yachts

- Government and Defence

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed satellite network operators, maritime ICT integrators, ship managers, and classification-society experts across North America, Europe, and Asia Pacific. These conversations validated tariff trends, typical bandwidth per vessel class, and the pace at which low-earth-orbit constellations are substituting legacy links.

Desk Research

Our desk work begins with public datasets from the International Telecommunication Union, the UN Conference on Trade and Development, and regional port authorities, which reveal vessel counts, trade lanes, and bandwidth demand growth. Trade groups such as the Global VSAT Forum and the International Chamber of Shipping supply adoption benchmarks, while patent analytics through Questel highlight antenna and modem innovation cycles. Company 10-Ks, flag-state registries, and press releases are mined to size service revenues and terminal shipments. Select paid feeds, notably D&B Hoovers for financial splits and Dow Jones Factiva for deal flow, enrich the evidence base. This list is illustrative, not exhaustive; many additional sources inform data collection and cross-checks.

Market-Sizing & Forecasting

A top-down demand pool is built from active vessel counts, average in-service terminals per hull, and mean annual airtime spend, which are then reconciled with selective bottom-up checks such as sampled terminal shipments and reseller channel audits. Key variables modeled include new-build deliveries, satellite capacity launches, maritime IoT device penetration, service price erosion, and regulatory safety mandates. A multivariate regression, complemented by scenario analysis for NGSO uptake, produces the 2025-2030 outlook. Bottom-up gaps, for example in smaller fishing fleets, are bridged through region-specific adoption proxies drawn from port call statistics.

Data Validation & Update Cycle

Outputs face layered variance checks against alternate data signals, peer review by senior analysts, and recontact of respondents when anomalies arise. Reports refresh annually, and interim revisions are triggered by material events such as major constellation activations or spectrum rule changes.

Why Mordor's Maritime Satellite Communication Baseline Commands Credibility

Published estimates often diverge because firms vary in vessel coverage, exchange-rate treatment, and how they factor emerging NGSO bandwidth.

Key gap drivers here include rival scopes that omit leisure craft, assume static service tariffs, or ignore hardware-service bundling. Mordor's model reflects real-time tariff declines, dual-orbit adoption, and yearly currency re-settlement.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.18 B (2025) | Mordor Intelligence | - |

| USD 5.90 B (2023) | Regional Consultancy A | Excludes NGSO capacity and uses 2023 exchange rates |

| USD 6.63 B (2025) | Industry Intelligence B | Relies on supply-side roll-up and single-band ASP |

The comparison shows that, by selecting the right vessel universe, adjusting for multi-orbit price shifts, and refreshing data every year, Mordor delivers a balanced baseline that decision-makers can trace back to transparent variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the maritime satellite communication market?

The market stands at USD 8.16 billion in 2026 and is forecast to reach USD 15.43 billion by 2031.

How fast is the maritime satellite communication market expected to grow?

Aggregate revenue is projected to advance at a 13.58% CAGR from 2026 to 2031, with LEO and managed-service segments outpacing the mean.

Which segment is growing the quickest?

Passenger vessels, especially cruise lines, are expanding connectivity spend at a 16.72% CAGR as travelers demand high-speed Wi-Fi.

Why are flat-panel antennas important?

Electronically steered flat panels enable multi-orbit tracking, weigh less than gimbaled dishes, and unlock Ka-Band throughput suited to modern cloud applications.

What regulatory rules are pushing SATCOM adoption?

IMO carbon-intensity reporting, ILO crew-welfare mandates, and USCG cyber-risk management rules all require secure, high-availability satellite links.

Page last updated on: