Adaptive Optics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

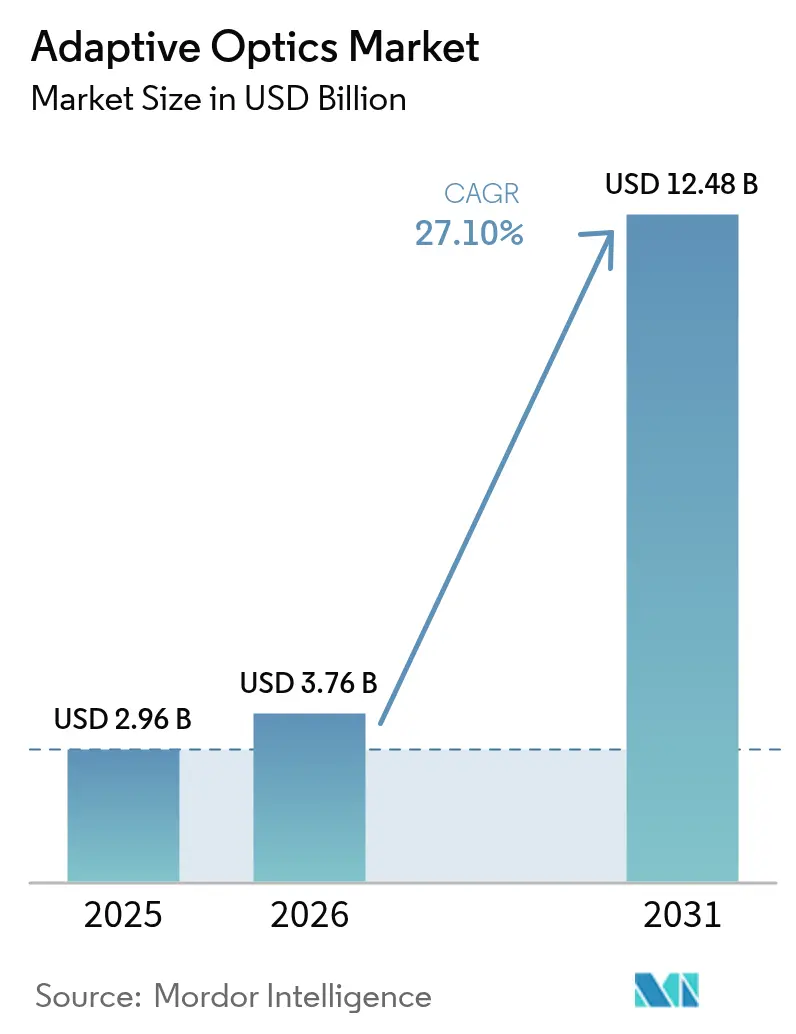

| Market Size (2026) | USD 3.76 Billion |

| Market Size (2031) | USD 12.48 Billion |

| Growth Rate (2026 - 2031) | 27.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Adaptive Optics Market Analysis by Mordor Intelligence

Adaptive optics market size in 2026 is estimated at USD 3.76 billion, growing from 2025 value of USD 2.96 billion with 2031 projections showing USD 12.48 billion, growing at 27.10% CAGR over 2026-2031. Demand is powered by government spending on directed-energy programs, semiconductor inspection needs at sub-nanometer precision, and rising consumer electronics applications such as AR/VR waveguide displays. Large-aperture telescope upgrades in Europe and Asia’s expanding space-situational-awareness programs reinforce the technology’s relevance. Machine-learning-based wavefront reconstruction, pivotal in next-generation control systems, is reducing calibration latency and broadening commercial appeal. The adaptive optics market is also benefitting from rapid adoption in retinal imaging devices as FDA classification changes shorten approval timelines for advanced ophthalmic platforms.

Key Report Takeaways

- By end-user industry, Defense & Security led with a 31.05% share of the adaptive optics market in 2025, while Consumer Electronics is forecast to expand at 31.30% CAGR to 2031.

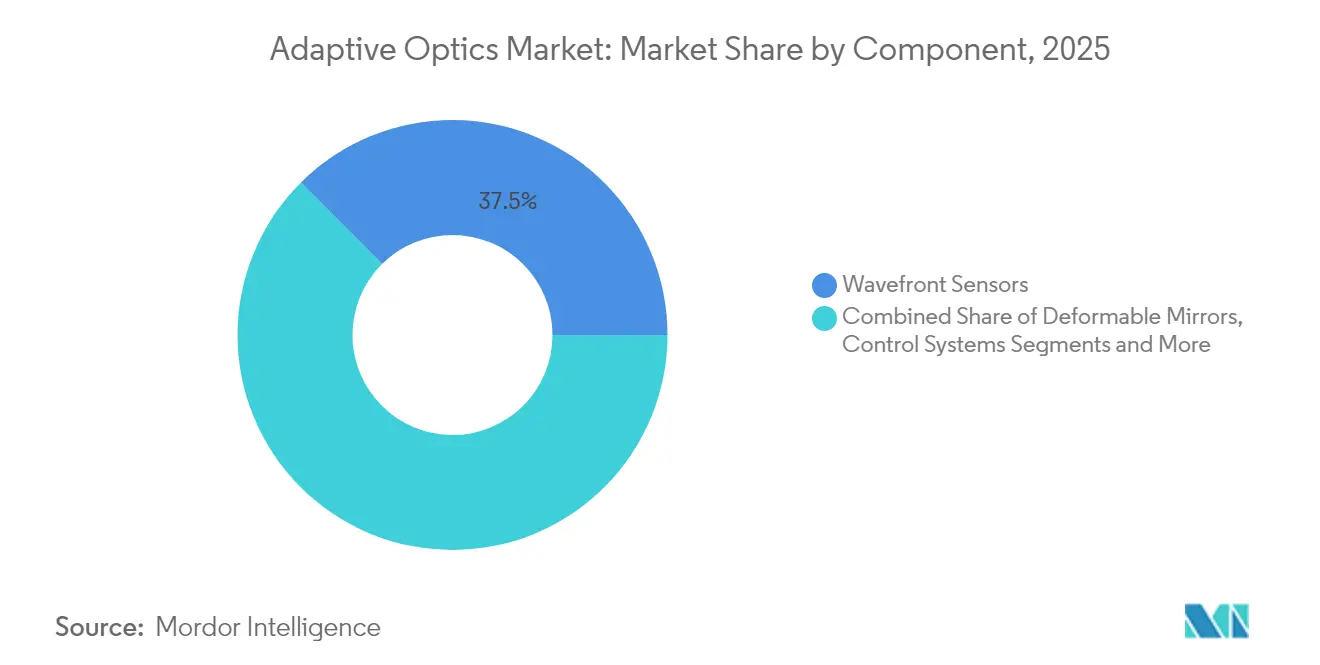

- By component, Wavefront Sensors held 37.45% of the adaptive optics market share in 2025; Control Systems & Software are projected to grow the fastest at 30.20% CAGR through 2031.

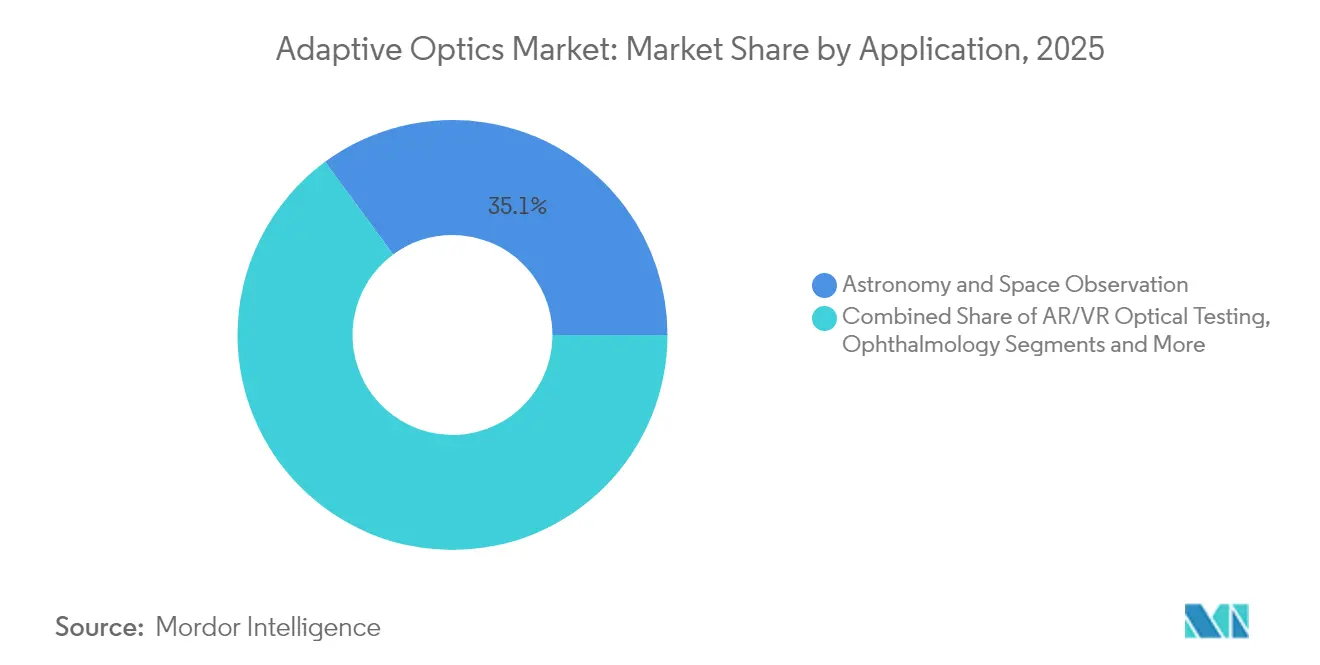

- By application, Astronomy & Space Observation commanded 35.10% share of the adaptive optics market size in 2025; AR/VR Optical Testing is set to advance at 32.10% CAGR between 2026-2031.

- By technology, MEMS-Based Deformable Mirrors accounted for 41.52% share of the adaptive optics market size in 2025; Liquid-Crystal Spatial Light Modulators will register the highest 33.00% CAGR.

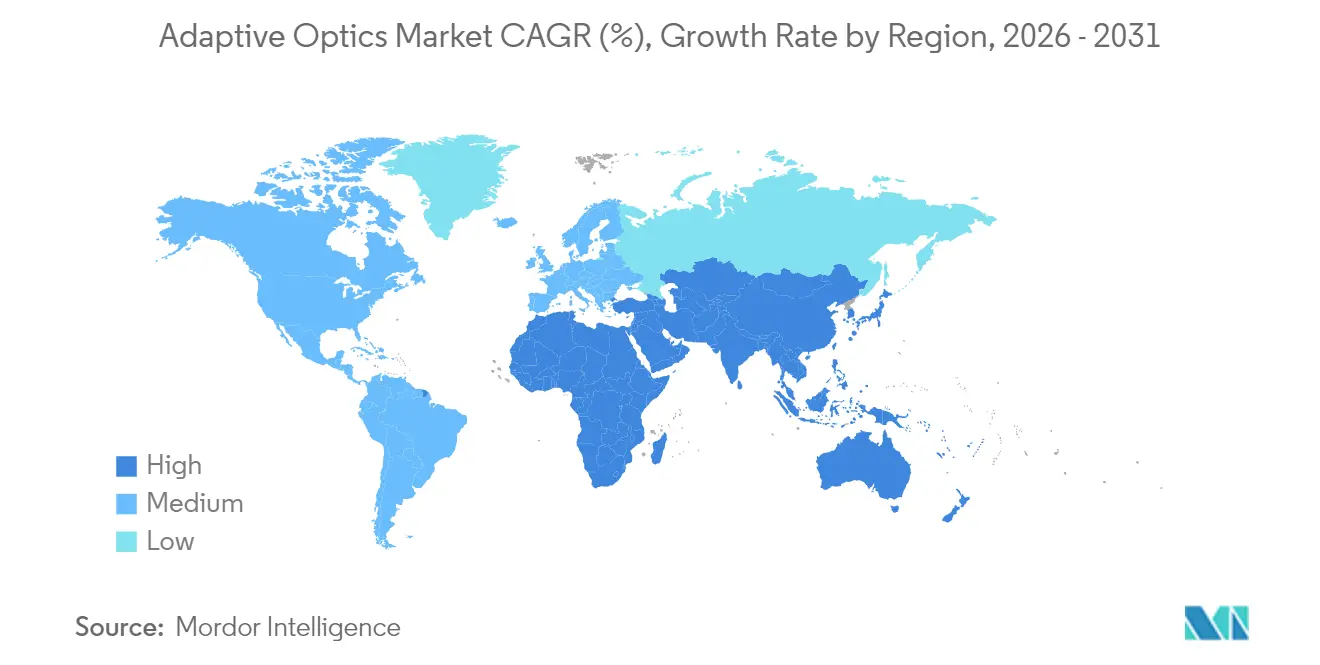

- By geography, North America held 37.45% revenue share in 2025, while Asia-Pacific is the fastest-growing region at 29.60% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adaptive Optics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging in North America | +4.2% | North America, with spillover to Europe | Medium term (2-4 years) |

| Deployment in Directed-Energy & Free-Space Laser Communication Programs by U.S. DoD | +5.8% | North America, extending to allied nations | Short term (≤ 2 years) |

| Large-Aperture Telescope Upgrades (ELT, TMT) Accelerating Demand in Europe | +3.7% | Europe, with global scientific collaboration | Long term (≥ 4 years) |

| Commercial Semiconductor Wafer & EUV Mask Inspection Requiring Sub-Nanometer Precision | +6.1% | Global, concentrated in Taiwan, South Korea, Netherlands | Medium term (2-4 years) |

| Emergence of AR/VR Waveguide Display Manufacturing Using AO-Enhanced Metrology | +4.9% | Global, led by North America and APAC | Medium term (2-4 years) |

| National Space Agencies' Funding for Space Debris Tracking (Asia & Middle East) | +3.8% | APAC core, with spillover to Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Adaptive Optics for High-Resolution Retinal Imaging

Ophthalmic device makers now integrate multi-conjugate adaptive optics to capture cellular-level retinal images, enabling earlier disease detection. FDA reclassification of ultrasound cyclodestructive devices from Class III to Class II in 2024 signals a more predictable pathway for advanced imaging platforms. Alcon’s Unity VCS and Unity CS clearances illustrate growing commercial readiness, while AI-powered wavefront algorithms reduce chair-time calibration. Start-ups such as Profundus Imaging are developing prototypes that widen corrected fields of view through multiple deformable mirrors. These advances lower ownership hurdles for clinics beyond major academic centers and accelerate the adaptive optics market’s healthcare reach.[1] Government Federal Register, “Ophthalmic Devices; Reclassification of Ultrasound Cyclodestructive Device,” federalregister.gov

Deployment in Directed-Energy & Free-Space Laser Communication Programs

The U.S. Department of Defense channels more than USD 1 billion annually into high-energy laser systems, with Lockheed Martin scaling to 300 kW devices that rely on adaptive optics for beam quality over long distances. The Space Development Agency’s Proliferated Warfighter Space Architecture budgets USD 35 billion through 2029, embedding laser cross-links that need precise wavefront control. AI-enabled turbulence-forecasting tools such as TAROQQO from the University of Ottawa now refine free-space quantum channels in real time. Together these programs shorten development cycles, reinforce supply chains, and enlarge the adaptive optics market for military and secure-communication uses.[2]SPIE, “Zapping enemy targets: Viable laser weapons remain critical to military strategy,” spie.org

Large-Aperture Telescope Upgrades (ELT, TMT)

Europe’s Extremely Large Telescope integrates the ANDES instrument with high-density deformable mirrors that feature 120 × 120 actuators, elevating image contrast for exo-planet searches. The Cassiopée project targets 10^9 contrast ratios, exploiting e-APD infrared detectors optimized for extreme adaptive optics. Procurement notices for wavefront-sensing cameras confirm multi-million-dollar orders that stimulate regional suppliers. U.S. roadmaps also advocate visible-band AO investments to maximize Astro2020 priorities. Hybrid variable-reluctance actuators, pioneered by TNO, improve efficiency over voice-coil models, enabling thicker mirror facesheets and more robust adaptive secondary mirrors.

Commercial Semiconductor Wafer & EUV Mask Inspection

Advances in extreme-ultraviolet interference lithography have reached 5 nm pattern fidelity, a milestone that hinges on adaptive optics to mitigate diffraction losses. Phase-shift masks for EUV deploy absorbent sidewalls requiring nanometer-level wavefront tuning. Equipment vendors such as MKS Instruments posted Q1 2025 revenue of USD 936 million on strong demand for high-precision optics. Their World Class Optics program underscores how predictive control algorithms now govern inspection stations that push the adaptive optics market deeper into semiconductor fabs.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High CapEx of High-Actuator Deformable Mirrors Limiting Wider Industrial Adoption | -3.4% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Complex Closed-Loop Design & Calibration Skills Gap in Emerging Markets | -2.8% | APAC emerging economies, Latin America, MEA | Long term (≥ 4 years) |

| Long Qualification Cycles for AO-Enabled Optical Payloads in Defense Sector | -2.1% | North America & Europe, extending to allied nations | Long term (≥ 4 years) |

| Miniaturization Challenges for Consumer-Grade Modules (< 5 mm Aperture) | -1.9% | Global, concentrated in consumer electronics hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CapEx of High-Actuator Deformable Mirrors

Deformable mirrors with 120 × 120 actuators raise unit costs that small manufacturers struggle to justify. Supply chain pressures, including export restrictions on germanium and gallium, inflate raw-material pricing for optical substrates. Alternative chalcogenide materials, such as BDNL4, lower dependence on restricted metals but require re-tooling that adds near-term expenses. The flat photonics-laser market, valued at USD 23 billion in 2024, narrows suppliers’ ability to absorb capital outlays. These factors trim growth in price-sensitive verticals and impose caution on prospective entrants to the adaptive optics market.

Complex Closed-Loop Design & Calibration Skills Gap

Closed-loop adaptive optics systems call for specialist expertise in wavefront sensing, real-time control, and optical alignment. Emerging economies lack sufficient training pipelines, delaying project execution even when hardware budgets exist. Machine-learning-driven reconstruction tools ease some burdens yet introduce data-science skill requirements. Sensorless intensity-adaptive optics aims to simplify configurations but still needs meticulous validation. Until broader workforce upskilling occurs, installation timelines in developing regions will remain longer, constraining the adaptive optics market adoption curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Control Systems Drive Innovation

Wavefront Sensors dominated 37.45% of the adaptive optics market share in 2025, anchored by Shack-Hartmann arrays that feed real-time aberration data to downstream controls. Shack-Hartmann’s simplicity keeps cost low, while pyramid sensors gain traction for extreme adaptive optics astronomy. Control Systems & Software are projected to grow at 30.20% CAGR; spatiotemporal Gaussian process models cut wavefront phase variance by up to 3.5× versus non-predictive loops. Deformable Mirrors, the mechanical workhorses, are shifting toward MEMS architectures with 41.52% technology share that supports consumer price points. Other components, including tip-tilt mirrors, address specialized fine-pointing tasks in laser communications.

Control software now embeds reinforcement-learning agents that optimize gain schedules under turbulent conditions, reducing overshoot while preserving bandwidth. Frequency-based data-driven controllers, tested on SPHERE’s SAXO+ upgrade, safeguard system stability through convex optimization. Suppliers bundle AI-ready firmware within modular hardware, shortening development cycles for integrators. As predictive control proliferates, the adaptive optics market size for control platforms is forecast to capture a larger revenue slice through 2031.

By End-User Industry: Consumer Electronics Accelerate Growth

Defense & Security held 31.05% revenue share in 2025, underpinned by DoD programs that depend on adaptive optics to maintain laser-beam coherence. Government purchases remain sizable, but the fastest growth comes from Consumer Electronics, which will advance at 31.30% CAGR as AR/VR headsets and smartphone cameras require compact wavefront modulators. Apple’s head-mounted displays have popularized high-pixel-density micro-OLED panels that rely on adaptive optics testing during fabrication.

Industrial Manufacturing leverages MEMS mirrors in semiconductor metrology lines, with inspection stations measuring sub-nanometer deviations. Medical & Life Sciences gain momentum from cellular-level retinal diagnosis platforms, further diversifying the adaptive optics market. Research & Academia continue to pioneer innovations such as metasurface-based wavefront sensors, ensuring a steady pipeline of intellectual property.

By Application: AR/VR Testing Leads Innovation

Astronomy & Space Observation captured 35.10% of the adaptive optics market in 2025, upheld by telescope consortia and space-agency missions. Laser Communication & Directed Energy rank high due to atmospheric-compensation needs in defense projects. Yet AR/VR Optical Testing, advancing at 32.10% CAGR, shows the steepest trajectory as consumer OEMs bring millions of units to market.

Semiconductor Inspection & Metrology maintain double-digit growth because EUV mask fabrication demands error budgets below one nanometer. Ophthalmology/Retinal Imaging benefits from FDA’s smoother regulatory pathways, allowing advanced systems into community clinics. Additional niches such as widefield microscopy and environmental remote sensing cluster within the Others category, supplying steady though smaller revenue streams across the adaptive optics market.

By Technology: Liquid-Crystal Systems Gain Momentum

MEMS-Based Deformable Mirrors retained 41.52% share of the adaptive optics market size in 2025 owing to batch-fabrication economies and scalability. Piezoelectric mirrors address high-speed correction in astronomy and directed-energy systems, while magnetic voice-coil mirrors serve rugged environments. Liquid-Crystal Spatial Light Modulators, projected to grow 33.00% CAGR, meet slim-profile requirements in AR smart glasses.

Emerging hybrid actuators combine variable reluctance and piezoelectric stacks, boosting efficiency over traditional voice coils. MEMS varifocal optical elements classified into reflective, microlens, and phased designs enable focus control without bulky mechanics. Femtosecond-laser-processed confocal microlens arrays now achieve multi-depth imaging without repeated axial scanning. These innovations ensure that the adaptive optics market continues to broaden its technology palette.

Geography Analysis

North America contributed 37.45% of 2025 revenue, anchored by the DoD’s billion-dollar directed-energy budget and NASA laser-communications initiatives. Suppliers such as Northrop Grumman’s Xinetics deliver lead-magnesium-niobate deformable mirrors for multiple military branches. The Space Development Agency integrates adaptive mirrors into satellite cross-links within its USD 35 billion architecture program. Canadian research on atmospheric distortion complements United States programs, jointly reinforcing the North American adaptive optics market.

Asia-Pacific is the fastest-growing region at 29.60% CAGR as Japan’s Space Strategy Fund stimulates launch-vehicle and constellation programs, and China expands optical payloads for space-situational-awareness satellites. China’s remote-sensing sector is projected to escalate toward USD 55-68 billion by 2033, magnifying demand for precision optics. JAXA’s XRISM mission validates soft-X-ray sensors that depend on adaptive mirrors, illustrating regional competence in space-borne instrumentation.

Europe’s large-aperture telescopes and defense research consortia drive sustained orders. ESO’s procurements for the ELT secure long-term contracts for continental suppliers. South America and the Middle East & Africa are nascent but promising as local space programs mature, yet limited technical talent and capital budgets slow adoption relative to leading regions. Collectively, these dynamics keep the adaptive optics market on a multi-regional growth path without over-reliance on a single geography.

Regulatory Landscape

Adaptive optics hardware and related know-how fall under dual-use controls because they support directed-energy platforms, free-space laser communications, and high-resolution sensing. Export licensing and end-use compliance are shaped by frameworks such as the Wassenaar Arrangement dual-use lists and the EU dual-use regime (Commission Delegated Regulation (EU) 2020/1749), which can affect cross-border shipments of deformable mirrors, wavefront sensors, and related control electronics and software when performance thresholds and military end uses apply.

Laser-link deployments also face a tightening safety and operational standards environment as optical ground stations and open-air links scale. EN IEC 60825-12:2026 sets safety requirements for free-space optical communication systems, and defense procurement rules can influence supplier qualification and traceability for optical materials and subsystems, adding compliance overhead for vendors selling into U.S. defense programs.

Value Chain Analysis

The adaptive optics value chain starts with precision materials and microfabrication inputs (optical substrates, coatings, MEMS wafers, and actuators), then moves into core component manufacturing. Key outputs include wavefront sensors (commonly Shack-Hartmann and pyramid designs), deformable mirrors (MEMS, piezoelectric, and voice-coil), and real-time control electronics. Control software and firmware operate in parallel, increasingly leveraging GPU-accelerated processing and machine-learning-based wavefront reconstruction to reduce calibration latency in closed-loop operation.

System integrators then combine these components into application-specific platforms for defense and laser communications, semiconductor inspection and metrology, astronomy and space observation, and ophthalmic imaging. Distribution typically follows direct, program-led selling for defense and space and module or component supply into industrial and consumer-electronics test ecosystems, with examples across the chain including Northrop Grumman (AOA Xinetics) and Bertin Alpao, as well as specialist manufacturers such as Flexible Optical B.V. (OKO Tech), Dynamic Optics, and Arizona Optical Systems.

Competitive Landscape

The adaptive optics market remains moderately fragmented. Top aerospace contractors anchor high-capex projects, while smaller firms address niche applications. Northrop Grumman’s Xinetics leverages three decades of R&D to supply deformable mirrors, wavefront sensors, and turnkey systems to NASA and defense agencies, preserving a technological edge. Teledyne’s acquisition of Qioptiq and other optical assets for USD 710 million broadens its vertical integration into heads-up displays and night-vision optics.

Consolidation continues as Thorlabs acquired Praevium Research in January 2025 to secure VCSEL technology critical for optical-coherence tomography. Semiconductor-focused vendors such as MKS Instruments enhance predictive-control algorithms to stake claims in wafer-inspection opportunities. AI-centric start-ups collaborate with academia to shorten feedback loops, an approach that larger incumbents are beginning to adopt through partnerships and internal incubators.

Price competition remains muted at the high-end because performance specifications outweigh unit cost. However, in consumer electronics, cost-down pressures intensify; MEMS suppliers scale production to millions of units, prompting process innovation. The steady pipeline of patents on metasurface sensors, varifocal MEMS, and learning-based controllers points to an adaptive optics market environment where intellectual capital and supply-chain agility define long-term winners.

Adaptive Optics Industry Leaders

-

Northrop Grumman Corp.

-

Thorlabs Inc.

-

Boston Micromachines Corp.

-

ALPAO SAS

-

Imagine Optics SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is the move from bespoke, rack-driven adaptive optics assemblies to compact, industrialized modules that reduce integration time for OEMs in semiconductor metrology, laser communications terminals, and advanced imaging instruments. This direction shows up in product architecture updates such as Bertin Alpao's launch of its eDM (Embedded Deformable Mirror) with integrated electronics (June 2026), which is designed for smaller housings and simpler electrical integration versus external driver boxes.

In large-aperture telescopes and space observation, programs continue to translate into procurement and engineering demand for high-order correction and stability, with spillover into autonomous alignment and tuning workflows in precision optical systems. Subaru Telescope and Tohoku University initiated test observations for the ULTIMATE-START adaptive optics system (March 2026), and RTX (Raytheon) confirmed development of a 3.1-meter aperture telescope for the Lazuli Space Observatory (June 2026), reinforcing supplier opportunities around high-actuator-count mirrors, low-latency control, and integration toolchains.

Recent Industry Developments

- June 2026: Bertin Alpao announced the launch of its eDM (Embedded Deformable Mirror) with integrated electronics to reduce housing size and simplify system integration for industrial users. The integrated approach shifts adaptive optics from lab-style setups with external drivers toward deployable modules, supporting faster adoption in metrology and optical communications terminals.

- January 2026: Thorlabs announced a strategic partnership with Xanadu Quantum Technologies to develop and manufacture customized optical fiber components for scaling photonic quantum computing. The collaboration increases demand for high-stability photonic subsystems and expands adjacent opportunities for precision wavefront control and test and measurement toolchains used to qualify advanced optical networks.

- June 2024: Boston Micromachines Corporation received a definitive contract (N6426724C0022) from Naval Surface Warfare Centers for a High Energy Laser Adaptive Optics System. The award points to ongoing defense investment in atmospheric compensation and beam-control architectures, supporting demand for high-speed deformable mirrors and real-time control hardware.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers adaptive optics systems that sense and correct wavefront distortions in real time to improve image or beam quality, across major end-use settings like astronomy, medical imaging, and defense.

Scope exclusions: Standalone hardware components such as sensors and drivers are not counted when they are sold as discrete parts rather than as part of an adaptive optics system.

Segmentation Overview

-

By Component

- Wavefront Sensors

- Deformable Mirrors

- Control Systems and Software

- Others (Beam Expanders, Tip-Tilt Mirrors)

-

By End-User Industry

- Defense and Security

- Medical and Life Sciences

- Industrial Manufacturing

- Consumer Electronics Brands and OEMs

- Research and Academia

- Other End-Users

-

By Application

- Astronomy and Space Observation

- Ophthalmology / Retinal Imaging

- Laser Communication and Directed Energy

- Semiconductor Inspection and Metrology

- AR/VR Optical Testing

- Others (Microscopy, Free-Space Optics RandD)

-

By Technology

- MEMS-Based Deformable Mirrors

- Piezoelectric (PZT) Deformable Mirrors

- Liquid-Crystal Spatial Light Modulators

- Magnetic / Voice-Coil Mirrors

- Others (Hybrid and Novel Actuation)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- Gulf Co-operation Council (GCC) Countries

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the first structure of the market and to set realistic guardrails around demand signals and supply readiness. We relied on public sources such as U.S. FDA databases for ophthalmic device clearances, USPTO and other patent publications to track innovation intensity, and NASA or major observatory program pages that outline telescope upgrade roadmaps.

To ground the model in measurable activity, trade data and macro series were also reviewed from sources such as UN Comtrade, the U.S. Census Bureau trade statistics, and OECD indicators for high tech manufacturing. Company filings, investor presentations, and reputable press were used to understand product positioning and typical shipment patterns, and a paid database subscription for company financials and patent analytics was used to standardize cross-company comparisons. This list is illustrative only, and many other public sources were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually sold as a system versus what is sold as a component, and on checking average selling price logic across end uses. We spoke with a mix of system suppliers, integrators, lab and hospital buyers, and domain experts across APAC, EMEA, and the Americas, and then used follow-up outreach when assumptions moved outside expected ranges.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 41% |

| Mid tier: 58% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 14% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Market sizing was built using top-down and bottom-up logic, where the top-down approach reconstructs the addressable demand pool by linking end-use activity to adoption of adaptive optics systems. In practice, we mapped indicators such as large-aperture telescope upgrade cycles, uptake of high resolution retinal imaging workflows, directed-energy and space tracking program momentum, and semiconductor inspection requirements that push for finer wavefront correction.

Those demand signals were converted into value using system-level volumes and typical ASP bands by use case, and then the totals were cross-checked with selective bottom-up approximations from supplier and channel conversations. Where publicly visible volumes were thin (for example, specialized defense or custom research builds), gaps were handled through constrained ranges that were tightened using expert feedback and consistency checks against adjacent capital equipment spending.

For forecasting, scenario analysis was used so that adoption timing, procurement cycles, and ASP progression could be tested separately. The outlook was then aligned to what interviewees expect for key variables like funding continuity, installation lead times, and the pace at which software-driven wavefront reconstruction improves system performance.

Data Validation & Update Cycle

Outputs were validated by triangulating the model against independent signals, including program announcements, regulatory milestones, and observable ordering patterns in core end uses. When a region or application showed a sharp jump, we reviewed the underlying drivers, checked currency conversions and year labeling, and then re-contacted sources if the variance could not be explained by a real market event.

A multi-step analyst review is applied before sign-off so that assumptions, units, and math consistency are checked in a repeatable way. The report is refreshed annually, and interim updates are triggered when material events occur, after which a final pre-delivery pass is completed to reflect the latest available data.

Mordor Intelligence's Adaptive Optics Market Size Compared With Other Published Estimates

Published market sizes for adaptive optics can look far apart, even when they are talking about similar end uses, because the counting rules and timing choices are not the same. Differences usually come from whether the estimate is system-only or includes components, how ASP changes are treated, and which year and currency conversion window is used.

In this study, the refresh cadence and the way prices are normalized to a consistent currency year are treated as first-order controls, which helps prevent one-off defense awards or large telescope projects from distorting the run rate, a modeling choice applied by Mordor Intelligence. Another common gap driver is scope overlap, since some estimates fold in wavefront sensors, drivers, or related optics hardware sold separately, which can lift the number quickly without a clear system boundary.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.76 B (2026) | |

| Global Research Publisher A | USD 0.78 B (2024) | Uses an earlier base year and a broader component view in its structure, so the number reads lower in-year but can scale faster as component demand is counted alongside systems. |

| Industry Research Publisher B | USD 0.61 B (2023) | Centers the sizing on a narrower set of end uses and a different base-year currency timing, which can suppress the starting value when large-capex cycles are between procurement peaks. |

The spread across sources mainly reflects timing and boundary choices, not just growth expectations. By keeping the counted unit as a system, stress-testing ASP bands, and re-checking anomalies against real program and adoption signals, our estimate stays traceable to clear inputs that can be revisited during updates.

Key Questions Answered in the Report

What is the current value of the adaptive optics market?

The adaptive optics market stands at USD 3.76 billion in 2026 and is forecast to reach USD 12.48 billion by 2031.

Which component segment is growing the fastest?

Control Systems & Software are expected to grow at 30.20% CAGR as predictive algorithms and AI tools improve wavefront reconstruction efficiency.

Why is Asia-Pacific the fastest-growing region?

Strategic government programs, such as Japan’s Space Strategy Fund and China’s expanding satellite-debris tracking missions, drive a 29.60% regional CAGR by funding large-scale optical projects.

How are consumer electronics influencing adaptive optics demand?

AR/VR headsets and smartphone camera modules require miniaturized wavefront modulators, pushing the Consumer Electronics segment to a 31.30% CAGR through 2031.

What factors limit wider industrial adoption?

High capital expenditure for high-actuator deformable mirrors and a shortage of closed-loop calibration expertise in emerging markets temper near-term growth.

Which technology type will see the highest growth?

Liquid-Crystal Spatial Light Modulators are projected to expand at 33.00% CAGR due to their slim form factor and electrical tunability suited for AR smart glasses.

Page last updated on: