Aspherical Lens Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

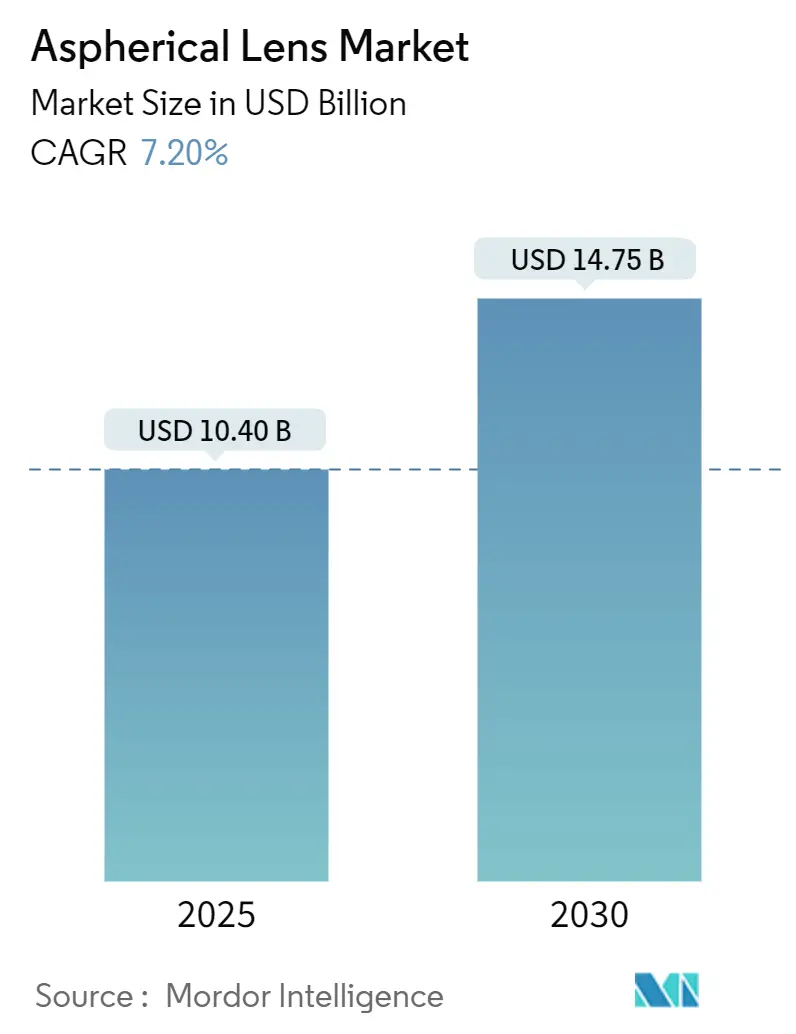

| Market Size (2025) | USD 10.40 Billion |

| Market Size (2030) | USD 14.75 Billion |

| Growth Rate (2025 - 2030) | 7.20% CAGR |

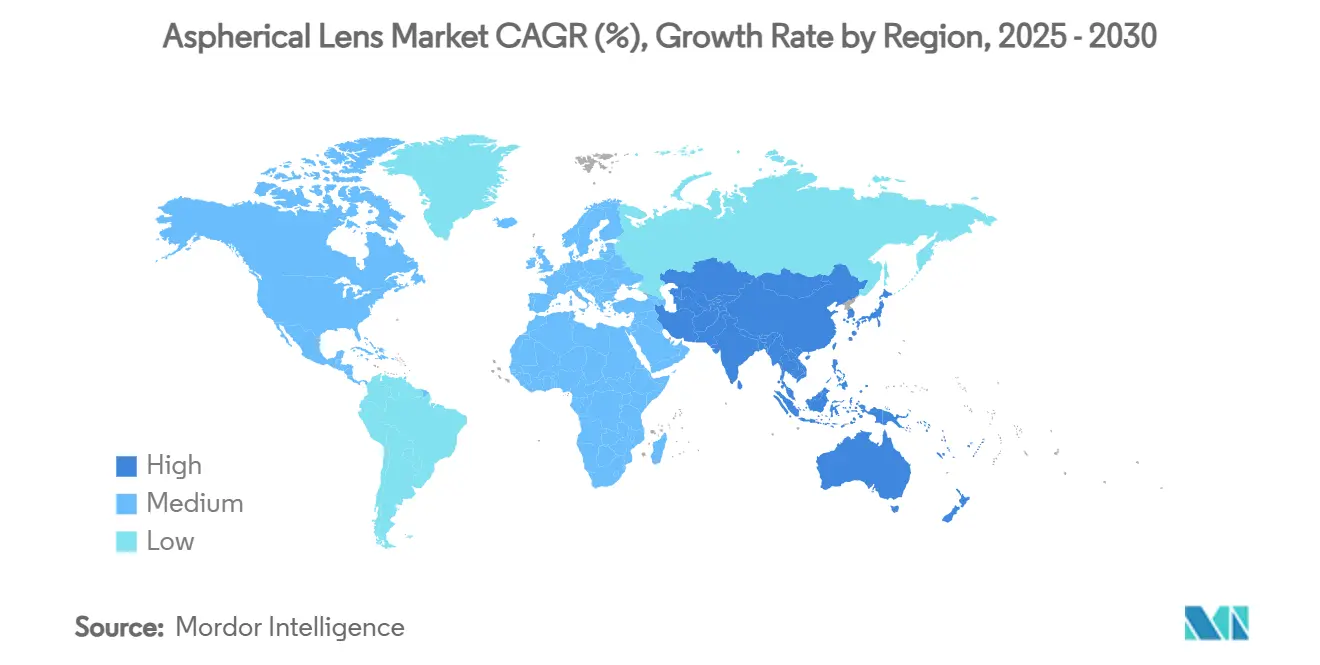

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Aspherical Lens Market Analysis by Mordor Intelligence

The aspherical lens market size reached USD 10.40 billion in 2025 and is forecast to rise to USD 14.75 billion by 2030, delivering a 7.20% CAGR. This expansion reflects the growing need to correct spherical aberration while designing thinner optical modules across smartphones, automotive LiDAR, medical imaging, and AR/VR hardware. Demand concentrates in Asia-Pacific, where vertically-integrated supply chains shorten product cycles, while North America and Europe accelerate adoption in autonomous driving and healthcare. Competitive intensity rises as legacy optical majors defend premium niches and specialized Asian vendors scale high-volume production. Cost-down pressures continue in consumer devices, yet advances in precision glass molding, wafer-level fabrication, and hybrid materials sustain pricing power for complex, high-value elements.

Key Report Takeaways

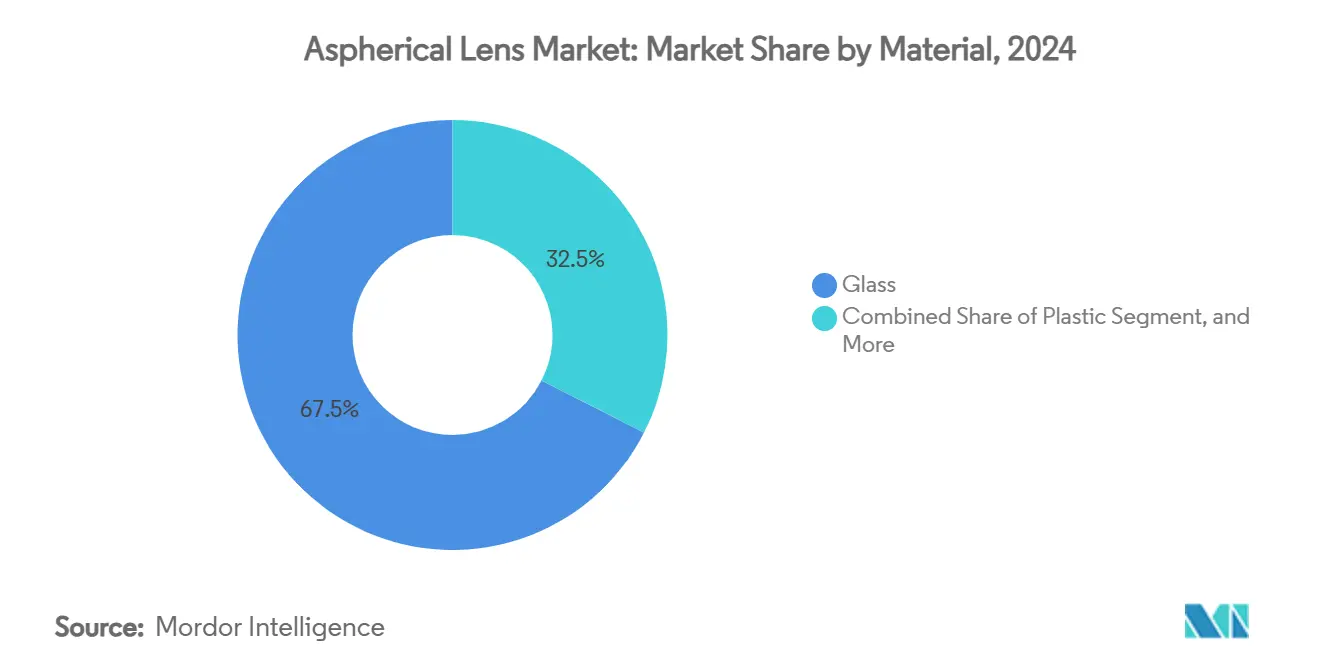

- By material, glass lenses held 67.50% of the aspherical lens market share in 2024. By material, plastic lenses are expanding at a 7.90% CAGR through 2030.

- By manufacturing technology, precision glass molding led with 44.50% of the aspherical lens market size in 2024. By manufacturing technology, wafer-level glass molding is projected to post an 8.05% CAGR to 2030.

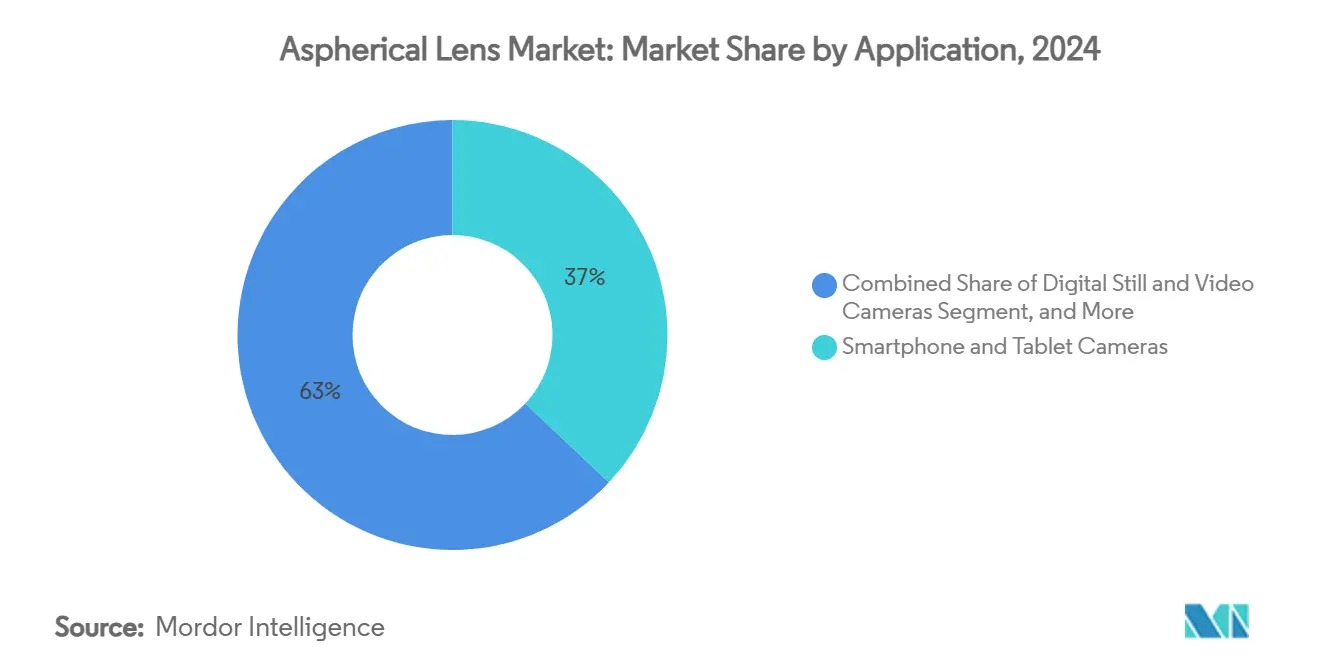

- By application, smartphone and tablet cameras dominated with 37.02% revenue share in 2024. By application, AR/VR displays are forecast to achieve a 7.76% CAGR over 2025-2030.

- By end-user industry, consumer electronics commanded 43.63% share of the aspherical lens market size in 2024. By end-user industry, healthcare is set to expand at 8.30% CAGR between 2025-2030.

- Asia Pacific accounted for 56.34% of 2024 revenue and is advancing at an 8.60% CAGR.

Market Trends and Insights

Drivers Impact Analysis of Aspherical Lens Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of multi-camera smartphones | +1.8% | Global, with APAC manufacturing concentration | Medium term (2–4 years) |

| Rising demand for ADAS automotive cameras | +1.2% | North America and EU regulations, APAC production | Long term (≥ 4 years) |

| Growing adoption in AR/VR head-mounted displays | +0.9% | Global; early uptake in North America and APAC | Medium term (2–4 years) |

| Shift toward minimally-invasive medical imaging devices | +0.7% | Global, led by developed markets | Long term (≥ 4 years) |

| Wafer-level aspheres in silicon-photonics packaging surge | +0.6% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Non-aqueous electrowetting liquid lenses | +0.5% | Global; advanced optics applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of multi-camera smartphones

Year-round flagship launches continue to raise optical complexity. Periscope telephoto stacks now integrate up to eight aspherical elements, doubling content per device. Largan Precision recorded 28.87% year-over-year Q1 2025 revenue growth as Apple and Samsung scaled advanced modules. Larger image sensors increase aberration, yet handset thickness must stay below 8 mm, so only aspheres satisfy both constraints. Volume growth funnels through APAC capacity where wafer-level glass molding reaches sub-5 µm alignment tolerances, sustaining the aspherical lens market despite falling average selling prices.

Rising demand for ADAS automotive cameras

Level-2+ autonomy requires surround-view cameras, driver monitoring, and LiDAR. Each subsystem needs thermally stable optics operating from -40 °C to +85 °C. LiDAR optics alone could exceed USD 3.6 billion by 2029.[1]SPIE Europe Ltd., “Yole trims automotive lidar expectations as prices drop,” optics.org ZEISS and Hyundai Mobis co-develop windshield projection units that depend on holographic aspherical lenses. Solid-state FMCW LiDAR moves toward packaged lens arrays, boosting unit counts per vehicle and lifting the aspherical lens market.

Growing adoption in AR/VR head-mounted displays

Metaverse hardware pivots to pancake folding optics built around cemented aspherical doublets. Liquid crystal polarization holograms shrink form factors while preserving 100° fields of view. Next-gen headsets integrate varifocal liquid-crystal lenses to solve vergence-accommodation conflict, each requiring dynamically tunable aspherical surfaces. As device weight targets 200 g, glass-polymer hybrid aspheres replace bulky Fresnel plates, catalyzing 7.76% CAGR in this sub-segment.

Shift toward minimally-invasive medical imaging devices

Olympus EVIS X1 endoscopes embed sub-millimeter glass aspherics delivering 4K output.[2]Olympus Corporation, “Olympus Medical Business Overview,” olympus-global.com Carl Zeiss Meditec posted EUR 1,050.5 million H1 2024/25 revenue on strong ophthalmic optics demand. Spiral diopter freeform lenses enable simultaneous multifocal imaging, reducing probe diameter for robotic surgery. Healthcare purchasing favors premium optics, insulating margins even as consumer pricing erodes elsewhere in the aspherical lens market.

Restraints Impact Analysis of Aspherical Lens Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-precision manufacturing cost and yield challenges | –1.1% | Global; heavier burden on small manufacturers | Short term (≤ 2 years) |

| Pricing pressure from plastic lens substitution | –0.8% | Global in consumer electronics | Medium term (2–4 years) |

| Sensitivity of aspherical IOLs to tilt and decentration | –0.6% | Global medical sector | Long term (≥ 4 years) |

| Patent thickets around precision glass molding | –0.4% | Global entry barrier | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-precision manufacturing cost and yield challenges

Surface accuracy must hold within single-digit nanometers. Yield dips below 70% for extreme profiles, raising cost 300-500% above spherical optics. Tool wear and ±0.1 °C mold control restrict fast capacity scaling. The aspherical lens market therefore faces near-term supply tightness, especially for automotive-grade parts.

Pricing pressure from plastic lens substitution

Injection-molded polycarbonates clock sub-30 s cycle times. High-index polymers now meet many mid-tier smartphone requirements. Cost gaps push OEMs to blended glass-plastic stacks, trimming bill-of-materials and eroding some glass volumes. Yet durability limits curb penetration into LiDAR and medical devices, moderating long-run impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aspherical Lens Market Segment Analysis

By Material:

Glass advantage persists under cost pressureGlass lenses controlled 67.50% of 2024 revenue and anchored performance-critical systems such as LiDAR and surgical imaging. Superior thermal stability keeps focus shift below 0.5 µm across -40 °C to +85 °C. Plastic, however, charts the fastest 7.90% CAGR as smartphone OEMs chase thinner stacks. High-index polymers close performance gaps, but scratch resistance and moisture uptake remain limiting factors. Polymer composites containing glass fillers now enter premium handsets, blending refractive power with moldability.

Plastic’s growth also benefits low-cost security cameras and entry-level wearables where lifetime is shorter. Even so, the aspherical lens market size attributed to glass is projected to exceed USD 9 billion in 2030, reflecting sustained demand from automotive, medical and industrial sectors.

By Manufacturing Technology:

Wafer-level molding acceleratesPrecision glass molding retained 44.50% share, with cycle-to-cycle form repeatability under 20 nm. Tool amortization favors volumes above one million units, matching smartphone demand patterns. Wafer-level glass molding grows 8.05% CAGR as silicon photonics needs hundreds of identical microlenses per die. Coherent’s 6-inch InP process quadruples throughput, slashing per-die lens cost and elevating the aspherical lens market.

CNC polishing and single-point diamond turning remain for prototypes and defense programs where volume is low but surface quality extreme. Hybrid molding, injecting plastic over pre-formed glass cores, promises cost savings yet retains glass at critical surfaces. Such innovations broaden supplier base but reinforce IP-driven barriers.

By Application:

Consumer imaging still leads, XR surgesSmartphone and tablet cameras captured 37.02% revenue in 2024 on shipments exceeding 1.3 billion units. Multi-module arrays lift lens counts from 6 to 10 per handset, sustaining volume. Meanwhile, AR/VR devices forecast a 7.76% CAGR, with pancake optics and varifocal engines multiplying asphere demand per headset. Automotive cameras and LiDAR expand rapidly with regulatory mandates for crash-avoidance, adding as many as 30 lenses to each Level-3 vehicle.

Medical imaging holds smaller volumes but delivers a margin. Endoscopes, ophthalmic scanners, and robotic surgery viewports pay premium pricing for ultra-low scatter glass. Industrial laser processing relies on beam-shaping aspheres in F-theta configurations, evidenced by Coherent’s multi-wavelength lens launch in January 2025.

By End-User Industry:

Electronics dominates, healthcare fastestConsumer electronics represented 43.63% of 2024 revenue. Continuous camera upgrades and wearables adoption anchor demand. Automotive follows with escalating ADAS fitment, while healthcare posts the highest 8.30% CAGR as minimally invasive surgery spreads. Industrial manufacturing maintains steady uptake in machine vision and laser micro-machining. Defense and aerospace remain small yet technology-rich, pushing diffraction-limited performance in harsh environments.

Cross-industry learning accelerates progress. Smartphone volume enables cost reduction that later benefits medical probes. Conversely, aerospace freeform design tools trickle into VR headset engineering, reinforcing synergies within the aspherical lens market.

Geography Analysis

APAC Aspherical Lens Market

Asia Pacific accounted for 56.34% of 2024 revenue and is forecast to grow 8.60% CAGR. Taiwan leads premium camera modules, with Largan posting NT$14.58 billion Q1 2025 sales, up 28.87%. China drives scale for mid-tier handsets and emerging electric vehicles. South Korea pioneers OLED-centric XR optics, while Japan’s legacy giants hone metrology and semiconductor tools. Regional governments support optical clusters through tax incentives and workforce training, cementing APAC dominance in the aspherical lens market.

North America Aspherical Lens Market

North America captures high-value niches in autonomous driving, advanced medical devices and datacenter photonics. Applied Optoelectronics more than doubled Q1 2025 revenue to USD 99.9 million as AI workloads spiked. Integration skills allow suppliers to bundle lenses with sensors and algorithms, capturing system margins. Venture funding sustains startups targeting LiDAR and XR, reinforcing a virtuous innovation cycle.

Europe Aspherical Lens Market

Europe focuses on precision and regulation-driven markets. ZEISS invests 14% of its EUR 11 billion revenue in R&D, maintaining lead in lithography and medical optics.[3]ZEISS, “Half-year figures 2024/25,” zeiss.com Germany’s automotive sector mandates high-grade imaging, while EU medical directives favor premium IOLs. Sustainability goals encourage lightweight optics, aligning with thinner aspherical designs. Collaborative projects such as ZEISS–Hyundai Mobis windshield displays illustrate Europe’s role as technology integrator within the global aspherical lens market.

Competitive Landscape

Regulatory Tightening on EMC Compliance

The competitive field is moderately concentrated. ZEISS, Canon, and Nikon defend high-end positions through deep IP and metrology control, while Largan, Sunny Optical, and AAC Technologies leverage volume leadership in smartphones. Largan's Q1 2025 revenue jump underscores scale advantages in 1-µm alignment manufacturing. Sunny Optical grew optics sales 24.9% year-over-year in H1 2024.

Coherent Corp bridges semiconductors and optics, posting USD 1.43 billion Q2 FY25 revenue on AI component demand.[4]Coherent, "Investor Presentation," coherent.com Patent moats around glass molding and electrowetting deter new entrants, steering M&A activity: Alcon's USD 356 million purchase of LENSAR targets integrated cataract solutions. Gooch & Housego's Phoenix Optical buy-out secures single-point diamond turning expertise OPTICS.ORG.

Strategic moves focus on vertical integration and diversification. Canon scales wafer-level optics for next-gen imaging, ZEISS partners with automotive suppliers, and semiconductor fabs explore 3D-printed freeforms. Market participants who combine lens fabrication with sensor co-design and software correction capture higher value, shaping the future structure of the aspherical lens market.

Aspherical Lens Industry Leaders

-

Largan Precision Co., Ltd.

-

Sunny Optical Technology Company Limited

-

Canon Inc.

-

Nikon Corporation

-

Carl Zeiss AG

- *Disclaimer: Major Players sorted in no particular order

Aspherical Lens Market Companies Covered in this Report

- Largan Precision Co., Ltd.

- Sunny Optical Technology Company Limited

- Canon Inc.

- Nikon Corporation

- Carl Zeiss AG

- HOYA Corporation

- Panasonic Holdings Corporation

- Coherent Corp.

- EssilorLuxottica S.A.

- AAC Technologies Holdings Inc.

- Kinko Optical Co., Ltd.

- AGC Inc.

- Genius Electronic Optical Co., Ltd.

- Tamron Co., Ltd.

- Sekonix Co., Ltd.

- Calin Technology Co., Ltd.

- Kantatsu Co., Ltd.

- JENOPTIK AG

- Edmund Optics Inc.

- Jos. Schneider Optische Werke GmbH

Recent Industry Developments in Aspherical Lens Market

- March 2025: Alcon agreed to acquire LENSAR Inc. for USD 356 million to strengthen robotic cataract platforms.

- March 2025: Coherent Corp unveiled 6-inch InP wafer fabrication cutting die cost 60%.

- February 2025: Coherent Corp reported USD 1.43 billion Q2 FY25 revenue, up 27% year-over-year.

- January 2025: Coherent Corp launched a multi-wavelength F-theta aspherical lens for EV battery welding.

Global Aspherical Lens Market Report Scope

Segmentation Overview

| Glass |

| Plastic |

| Other Materials (Polymer Composites, etc.) |

| Precision Glass Molding (PGM) |

| Hybrid / Injection Molding |

| CNC Polishing and Grinding |

| Single-Point Diamond Turning |

| Other Manufacturing Technologies |

| Smartphone and Tablet Cameras |

| Digital Still and Video Cameras |

| AR/VR and Wearable Displays |

| Automotive Cameras and LiDAR |

| Medical and Life-Science Imaging |

| Industrial Laser and Machine Vision |

| Defense and Aerospace Optics |

| Other Applications |

| Consumer Electronics |

| Automotive |

| Healthcare |

| Industrial Manufacturing |

| Defense and Aerospace |

| Other End-user Industries |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Material | Glass |

| Plastic | |

| Other Materials (Polymer Composites, etc.) | |

| By Manufacturing Technology | Precision Glass Molding (PGM) |

| Hybrid / Injection Molding | |

| CNC Polishing and Grinding | |

| Single-Point Diamond Turning | |

| Other Manufacturing Technologies | |

| By Application | Smartphone and Tablet Cameras |

| Digital Still and Video Cameras | |

| AR/VR and Wearable Displays | |

| Automotive Cameras and LiDAR | |

| Medical and Life-Science Imaging | |

| Industrial Laser and Machine Vision | |

| Defense and Aerospace Optics | |

| Other Applications | |

| By End-User Industry | Consumer Electronics |

| Automotive | |

| Healthcare | |

| Industrial Manufacturing | |

| Defense and Aerospace | |

| Other End-user Industries | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What drives current growth in the aspherical lens market?

Smartphone multi-camera adoption, ADAS automotive cameras, AR/VR headsets and minimally-invasive medical imaging drive most incremental demand.

Which region contributes the highest revenue to the aspherical lens market?

Asia Pacific supplies 56.34% of global revenue and is expanding the fastest at 8.60% CAGR through 2030.

Why are glass aspherical lenses still dominant despite plastic cost advantages?

Glass provides superior thermal stability and optical precision essential for LiDAR, medical and industrial uses where performance cannot be compromised.

What manufacturing technology is gaining momentum beyond precision glass molding?

Wafer-level glass molding is growing at 8.05% CAGR as silicon-photonics packaging requires batch fabrication of microlens arrays.

How will healthcare influence the aspherical lens market by 2030?

Healthcare applications are projected to expand at 8.30% CAGR as endoscopy, ophthalmic surgery and robotic systems rely on high-quality aspherical optics.

Which companies are strengthening positions through recent acquisitions?

Alcon, Gooch & Housego, ZEISS and Teledyne have all completed deals aimed at enhancing precision optics capabilities across medical and defense segments.

Page last updated on: