Ultrafast Lasers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

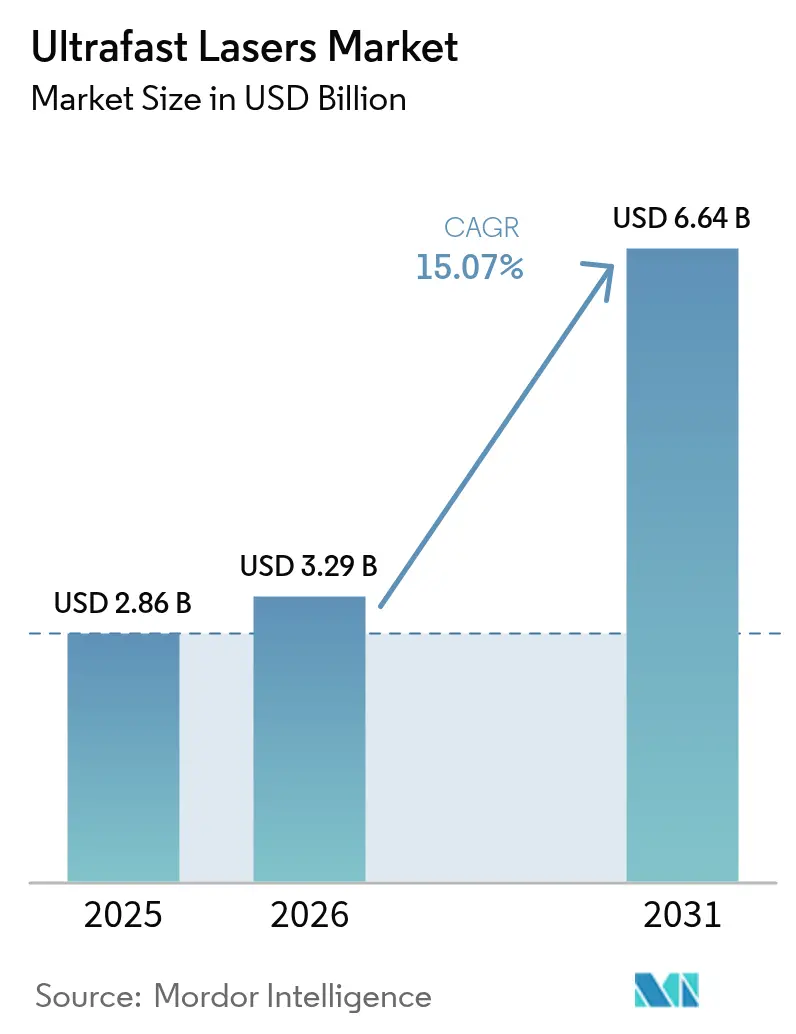

| Market Size (2026) | USD 3.29 Billion |

| Market Size (2031) | USD 6.64 Billion |

| Growth Rate (2026 - 2031) | 15.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultrafast Lasers Market Analysis by Mordor Intelligence

Ultrafast lasers market size in 2026 is estimated at USD 3.29 billion, growing from 2025 value of USD 2.86 billion with 2031 projections showing USD 6.64 billion, growing at 15.07% CAGR over 2026-2031. Growth accelerates because femtosecond-level pulse control delivers sub-20 µm features that conventional continuous-wave lasers cannot achieve. Semiconductor miniaturization, foldable display adoption, and electric-vehicle battery innovation collectively reinforce demand as manufacturers migrate toward precision, heat-free machining methods. Fiber architectures dominate deployments owing to superior beam quality and thermal management, while all-fiber femtosecond systems gain traction by removing alignment-sensitive free-space optics. Asia-Pacific leads installations because wafer fabs, battery plants, and display lines cluster across China, Japan, and South Korea. Strategic mergers-such as Hamamatsu’s USD 800 million purchase of NKT Photonics-signal vertical-integration moves that help suppliers combine sources, optics, and software into turnkey production tools.

Key Report Takeaways

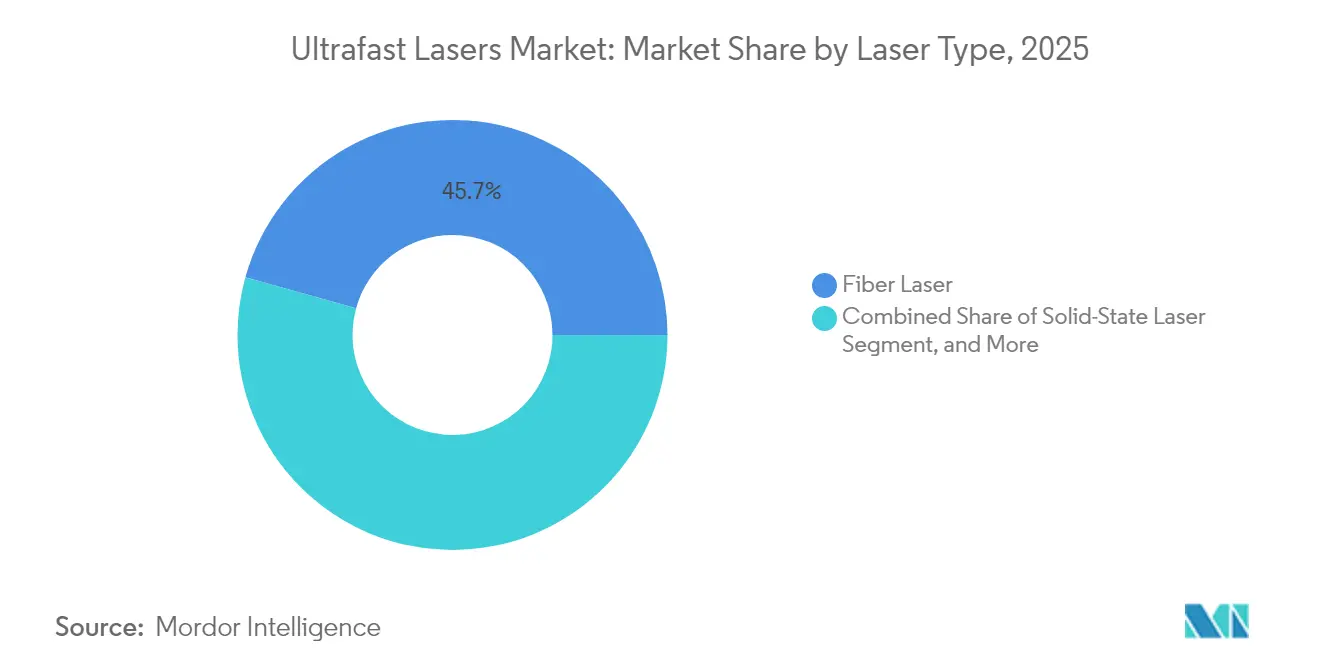

- By laser type, fiber lasers led with 45.68% ultrafast lasers market share in 2025; all-fiber femtosecond lasers are projected to advance at a 16.28% CAGR through 2031.

- By pulse duration, femtosecond systems accounted for 62.35% share of the ultrafast lasers market size in 2025 and are growing at 16.42% CAGR to 2031.

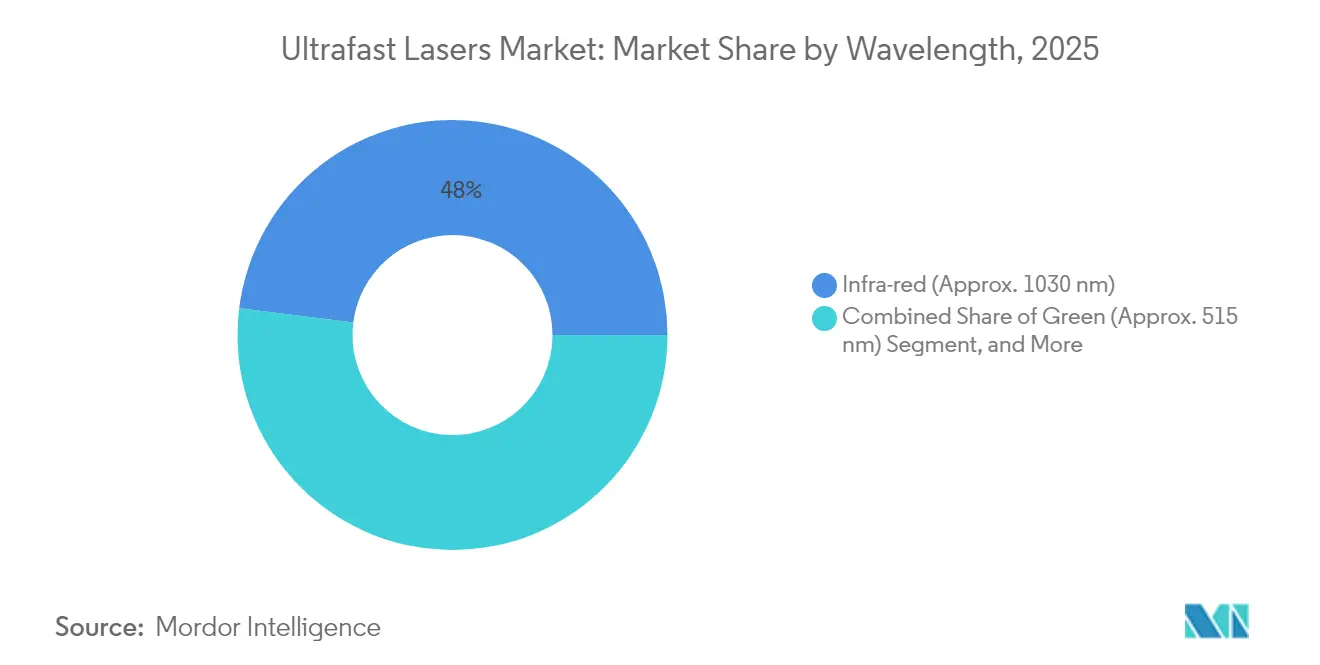

- By wavelength, UV platforms represented the fastest segment with an 17.83% CAGR, while infrared maintained 48.02% of 2025 revenue.

- By application, material processing and micromachining commanded a 53.62% share of the ultrafast lasers market size in 2025; biomedical imaging is climbing at a 17.39% CAGR through 2031.

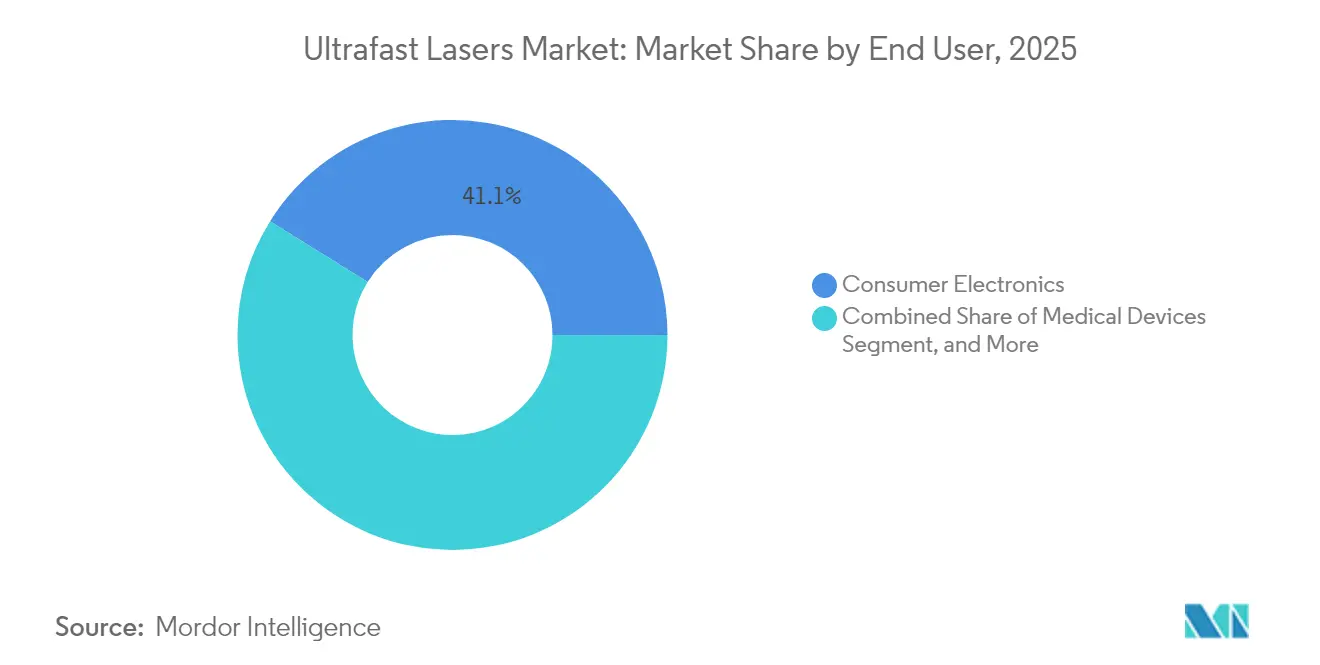

- By end user, Consumer Electronics led the market with a market share of 41.12% while Automotive is expected to expand at a 17.02% CAGR through 2031.

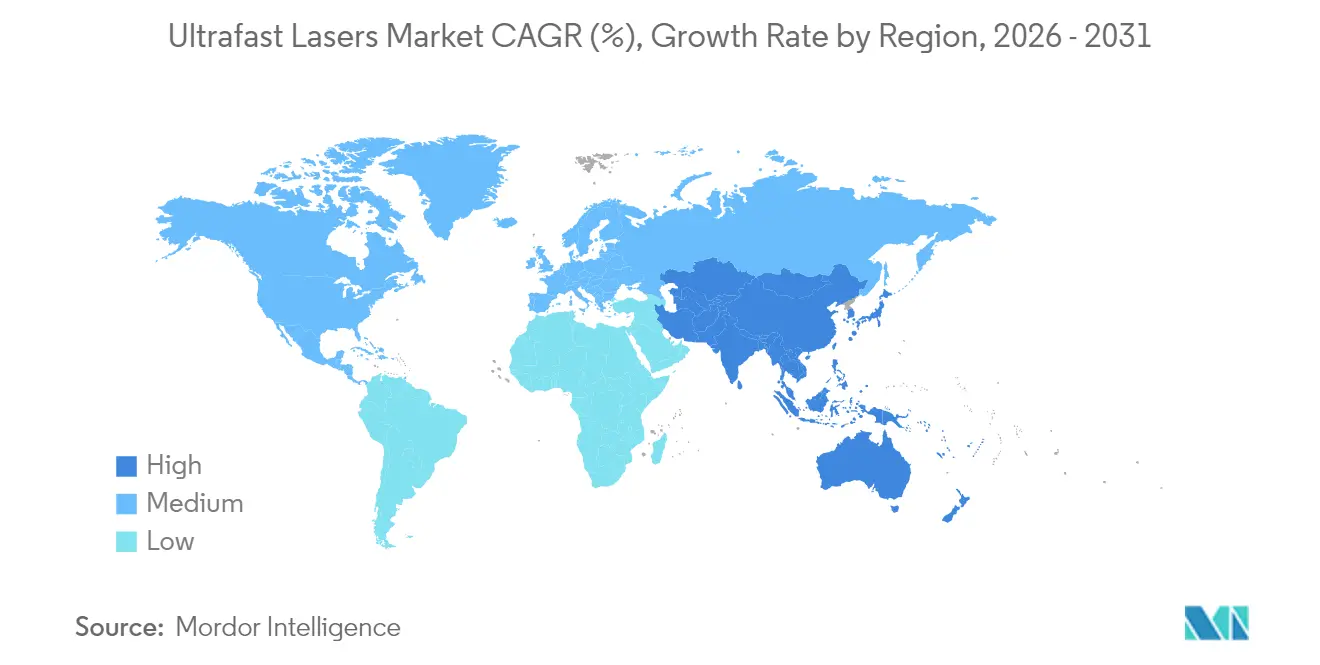

- By geography, Asia-Pacific held 38.14% share in 2025 and is expected to expand at 18.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultrafast Lasers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor mini-maturization wave fuels Less than 20 µm feature machining demand | +2.50% | APAC core, spill-over to North America | Medium term (2-4 years) |

| EV battery foil cutting shift to ultrafast "burst-mode" lasers | +2.80% | Global, with early gains in China, Germany, United States | Short term (≤ 2 years) |

| High-aspect-ratio glass drilling for foldable displays | +3.10% | APAC core, spill-over to North America | Medium term (2-4 years) |

| On-wafer quantum photonics prototyping needs sub-200 fs pulses | +2.40% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Government incentives for reshoring advanced manufacturing | +1.90% | North America & EU | Medium term (2-4 years) |

| AI-assisted adaptive optics boosting multi-beam throughput | +2.10% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Mini-Miniaturization Wave Fuels < 20 µm Feature Machining Demand

Chipmakers migrating to 3D packaging architectures depend on femtosecond pulses that drill through-silicon vias with aspect ratios beyond 10:1 while eliminating heat-affected zones. Samsung and SK Hynix already deploy such systems for high-bandwidth memory stacking. Tool vendors report that ultrafast platforms represented 35% of new wafer-processing orders in 2024, up from 18% in 2022. Continuous node shrinkage below 20 nm widens the addressable ultrafast lasers market by forcing abandonment of mechanical or CW-laser options. Volume ramps in Asia-Pacific amplify equipment demand across allied photomask and substrate houses.

EV Battery Foil Cutting Shift to Ultrafast “Burst-Mode” Lasers

Gigafactory data show femtosecond burst-mode cutting improves 6 µm foil throughput by 40% while eliminating edge burrs that trigger short circuits.[1]Tesla Inc., “Tesla 2024 Impact Report,” Tesla.com CATL and BYD invested USD 150 million in laser cutting lines during 2024, illustrating commercialization momentum. Precision demand rises as battery energy density climbs, pushing manufacturers to thinner foils that favor ablation over mechanical shearing. Multiplexed beam splitting allows simultaneous processing of stacked sheets, lifting utilization, and justifying higher capital expenditure. These factors enlarge the ultrafast lasers market share devoted to automotive manufacturing lines.

High-Aspect-Ratio Glass Drilling for Foldable Displays

Femtosecond drilling delivers 10 µm holes through 100 µm glass without micro-cracks, satisfying foldable OLED production tolerances.[2]Samsung Display, “Foldable OLED production lines adopt femtosecond drilling,” Samsungdisplay.com Corning invested USD 200 million in ultrafast capacity during 2024 to supply glass for under-display cameras. Display resolution upgrades to 8K, narrow placement tolerances to 2 µm, which only sub-300 fs pulses achieve. Asia-Pacific panel makers accelerate orders, propelling the regional ultrafast lasers market growth. Suppliers integrating laser, scanner, and software subsystems secure design-in wins that lock them into multiyear capex cycles.

On-Wafer Quantum Photonics Prototyping Needs Sub-200 fs Pulses

IBM achieved 99.5% single-photon source fidelity using ultrafast waveguide writing, surpassing 87% produced with longer pulses.[3]IBM Corporation, “Quantum photonics breakthrough 2024,” Ibm.com IonQ’s partnership with NKT Photonics targets femtosecond sources for trapped-ion devices. University labs such as Dayton’s USD 2.5 million RAAM facility further expand research demand. As quantum computing roadmaps call for integrated photonic circuits, industrial-quality ultrafast tools become indispensable. Long-term growth in the ultrafast lasers market, therefore, hinges on pulse stability below 200 fs with industrial uptime metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain choke points in ytterbium-doped fiber | -1.80% | Global | Short term (≤ 2 years) |

| Productivity gap vs. CW fiber lasers in thick-metal cutting | -1.20% | Global, particularly in heavy manufacturing regions | Medium term (2-4 years) |

| IEC 60825 laser-safety compliance costs for SMEs | -0.90% | Global | Short term (≤ 2 years) |

| Thermal-lens instability above 500 W average power | -1.10% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Choke Points in Ytterbium-Doped Fiber

Lead times for high-power ytterbium fibers lengthened to six months in 2024 as only a handful of firms master the rare-earth uniformity needed for femtosecond stability.[4]Nufern, “Specialty optical fibers supply-chain update,” Nufern.com Chinese newcomers struggle with impurities that trigger mode instabilities, limiting penetration to sub-100 W systems. Restricted supply threatens production ramps for all-fiber femtosecond lasers, the fastest expanding slice of the ultrafast lasers market. Vendors respond by qualifying dual sources, yet process complexity slows capacity additions until at least 2026. Any prolonged shortage risks capping revenue even as downstream demand spikes.

Productivity Gap vs. CW Fiber Lasers in Thick-Metal Cutting

TRUMPF measured 3-5× faster speeds and 40% lower power draw when CW lasers cut 10 mm steel compared with ultrafast units.[5]TRUMPF SE + Co. KG, “Advances in laser cutting productivity,” Trumpf.com Automotive body panels and ship hull sections thus continue to favor melt-based approaches. Operational costs remain 60% higher per kilogram processed on ultrafast platforms, limiting addressable volume in heavy fabrication. Burst-mode gains shrink but do not erase the gap, maintaining a ceiling on ultrafast lasers market uptake for thick-section machining. Suppliers concentrate instead on thin metals, brittle substrates, or micro-patterning niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Laser Type: Fiber Dominance Drives Integration

Fiber architectures captured 45.68% of the ultrafast lasers market in 2025, underpinned by a mean time between failures above 50,000 hours that satisfy factory uptime targets. Solid-state and diode-pumped bulk platforms retain utility for peak energies above 1 mJ, yet they see slower sales into production lines. The ultrafast lasers market size for all-fiber femtosecond units is projected to climb at a 16.28% CAGR as alignment-free layouts cut maintenance visits. Vendors like Coherent compress sources, power supplies, and chiller units into footprint-saving racks, allowing direct integration inside wafer or battery tools.

System simplification lets OEMs embed lasers within motion stages, removing external beam paths that previously invited contamination. Integration also strengthens service stickiness, because swapping brands would mean requalifying the entire machine. Fiber leaders thus extend firmware, scanner, and AI optics suites that raise switching costs, deepening control of the ultrafast lasers market. Bulk-laser specialists pivot toward research or exotic-wavelength niches where fibers lag in pulse energy or tunability.

By Pulse Duration: Femtosecond Applications Expand

Femtosecond devices owned 62.35% revenue in 2025 because non-thermal ablation prevents substrate damage in silicon, glass, and polymer films. Advancing burst-mode architectures now achieve fivefold material-removal rate jumps while restraining heat below 100 nm penetration. The ultrafast lasers market segment is forecast at 16.42% CAGR to 2031 as tooling costs converge with picosecond options. Picosecond sources persist where slight heat zones are acceptable, and higher average power is required for large-area texturing.

Convergence blurs the boundary as femtosecond prices fall and speed rises. Equipment buyers increasingly specify pulse duration by application physics rather than budget constraints, tightening competition. Suppliers augment controllers that switch between single-pulse and burst sequences, enabling one head to serve dicing, marking, and trimming within the same line, broadening the ultrafast lasers market addressable reach.

By Wavelength: UV Growth Accelerates Medical Applications

Infrared around 1030 nm preserved 48.02% share in 2025 on the back of mature ytterbium-fiber gain media. Yet UV 355 nm units grow at 17.83% CAGR as medical-device and advanced-packaging firms seek sub-micron kerfs with negligible thermal load. Frequency-converted femtosecond sources unlock transparent-material processing that IR beams cannot tackle, swelling the ultrafast lasers market pipeline among catheter, stent, and polymer-lens makers.

Amplitude Laser’s Fastlite purchase brings internal harmonic modules that shoot deep-UV lines under 266 nm, letting a single IR source service multi-wavelength tasks. This modularity trims spares inventory for contract manufacturers juggling diversified jobs. Green 515 nm platforms keep share in copper foil and display pixel repair, but UV leads momentum thanks to regulatory familiarity within FDA device filings, reinforcing its pull on total ultrafast lasers market revenues.

By Application: Biomedical Imaging Drives Innovation

Material processing and micromachining remained the backbone at 53.62% share in 2025, spanning wafer dicing, via drilling, and foil cutting lines that crave micrometer fidelity. Yet biomedical imaging logs the highest 17.39% CAGR because ultrafast pulses enable multiphoton microscopy and femtosecond laser surgery with minimal collateral tissue effects. Hospitals eye precise corneal reshaping and neural mapping, while instrument OEMs embed compact lasers for operating-room settings, expanding the ultrafast lasers market in healthcare.

Spectroscopy and metrology add incremental demand through improved signal-to-noise ratios in pump-probe setups. Scientific institutions act as incubators, proving new beam-shaping and wavelength-mixing approaches before transfer to industry. Cross-fertilization shortens commercialization cycles, keeping the ultrafast lasers market pipeline vibrant across disciplines.

By End User: Automotive Transformation Accelerates

Consumer electronics held 41.12% of 2025 revenue as smartphone brands laser-cut ultra-thin glass and flexible PCBs. Automotive plants, however, post 17.02% CAGR because EV batteries and lightweight aluminum chassis need burr-free, low-heat machining. Tesla uses automated femtosecond clusters to process millions of battery foils each year, validating industrial scalability.

Medical-device fabricators grow steadily by adopting femtosecond texturing for implant osseointegration. Aerospace and defense shops integrate high-power sources for composite drilling and titanium trimming. This end-user diversification insulates suppliers from cyclic swings and lifts resilience within the overall ultrafast lasers market.

Geography Analysis

Asia-Pacific commanded 38.14% of the ultrafast lasers market in 2025 and is forecast at 18.21% CAGR to 2031 because wafer fabs, battery gigafactories, and display lines cluster across China, Japan, and South Korea. China’s policy incentives nurture domestic laser suppliers, but Western brands still dominate high-precision tiers that demand sub-300 fs stability. Japan retains innovation leadership; Hamamatsu’s USD 800 million NKT Photonics buy enlarges its quantum and biomedical portfolio, increasing local system integration density. South Korean chip and display leaders anchor steady tool demand, ensuring the region remains the primary engine for ultrafast lasers market revenue.

North America benefits from research funding and reshoring grants. Programs like Massachusetts’ Manufacturing Accelerate deliver USD 200,000 subsidies that offset IEC 60825 certification costs, prompting SMEs to adopt femtosecond tools. U.S. labs pilot quantum-photonics prototypes, while automotive suppliers in Michigan and Texas turn to burst-mode lasers for EV modules. Canadian universities bolster fiber-laser research, providing a pipeline of photonics graduates who sustain regional service ecosystems.

Europe maintains strongholds in automotive and medical devices. German tier-ones specify ultrafast systems for battery enclosure welding and stent machining, preserving premium margins. French and Lithuanian vendors contribute specialty wavelength modules, enhancing intra-EU supply security. Meanwhile, Middle East and Africa emerge slowly as governments fund research hubs in the United Arab Emirates. Though volume remains small, pilot lines in aerospace composites and photonic sensors foreshadow future contributions to the ultrafast lasers market once technical workforces mature.

Competitive Landscape

The ultrafast lasers industry shows moderate concentration; the top five vendors capture a major revenue market, leaving room for niche specialists to flourish. TRUMPF’s serial acquisitions, including Amphos, Access Laser, and Philips Photonics, stack source, optics, and automation know-how into end-to-end solutions that cut buyer integration risk. Coherent exploits AI-assisted adaptive optics that auto-correct beam distortions, locking customers into proprietary control software. Hamamatsu leverages NKT Photonics’ hollow-core fiber and supercontinuum sources to differentiate quantum-ready toolkits, sharpening competitive edges within Europe and North America.

MKS Instruments focuses on burst-mode femtosecond platforms that raise throughput in battery foil and glass drilling lines, winning deals where productivity parity with CW lasers is critical. IPG Photonics capitalizes on vertically integrated fiber manufacturing, safeguarding supply in an era of ytterbium shortages. Asian challengers like Raycus and Wuhan Huaray gain share in low-to-mid-power segments, pressure Western pricing, yet still trail in consistency at sub-500 fs durations. Overall, solution completeness, service reach, and component self-reliance shape differentiation across the ultrafast lasers market.

Consolidation is set to continue. Vendors seek pulse-shaping, harmonic-generation, and software analytics assets that shorten time-to-solution for OEMs deploying next-node fabs or foldable display lines. Specialized outfits excelling in niche wavelengths or quantum photonics remain attractive takeover targets because large suppliers want turnkey portfolios. Nonetheless, open-architecture advocates could carve positions by championing interoperable controls that lower switching barriers, sustaining healthy competition in the ultrafast lasers market.

Ultrafast Lasers Industry Leaders

TRUMPF SE + Co. KG

Coherent Corp.

IPG Photonics Corporation

MKS Instruments Inc. (Spectra-Physics and Newport)

Lumentum Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amplitude Laser Group completed the acquisition of Fastlite, enhancing femtosecond pulse-shaping capabilities for biomedical imaging and quantum photonics applications.

- April 2025: MKS Instruments unveiled the Spectra-Physics Element 2 family and Spirit-NOPA-VISIR system, targeting bio-imaging and medical-device manufacturing.

- March 2025: University of Dayton Research Institute opened the USD 2.5 million RAAM Laboratory featuring a RoboCLASP femtosecond system to support quantum photonics research.

- March 2025: Fluence inaugurated an Ultrafast Laser Application Laboratory in Poland to accelerate automotive and medical-device process development.

Global Ultrafast Lasers Market Report Scope

An Ultrafast Laser is a short light pulse with an electromagnetic pulse whose time duration is almost a picosecond or less. Ultrafast lasers come with a broadband optical range and can be produced by mode-locked oscillators.

The ultrafast lasers market is segmented by laser type (solid-state laser, fiber laser), pulse duration (picosecond, femtosecond), application (material processing and micromachining, medical and bioimaging, research), end user (consumer electronics, medical, automotive, aerospace and defense, research) and geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Fiber Laser |

| Solid-State Laser |

| Diode-Pumped Bulk Laser |

| All-Fiber Femtosecond Laser |

| Femtosecond |

| Picosecond |

| Infra-red (Approx. 1030 nm) |

| Green (Approx. 515 nm) |

| UV (Approx. 355 nm) |

| Deep-UV (Less than or Equal to 266 nm) |

| Material Processing and Micromachining |

| Biomedical and Bio-imaging |

| Spectroscopy and Metrology |

| Scientific Research |

| Consumer Electronics |

| Medical Devices |

| Automotive |

| Aerospace and Defense |

| Research Institutes |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Laser Type | Fiber Laser | ||

| Solid-State Laser | |||

| Diode-Pumped Bulk Laser | |||

| All-Fiber Femtosecond Laser | |||

| By Pulse Duration | Femtosecond | ||

| Picosecond | |||

| By Wavelength | Infra-red (Approx. 1030 nm) | ||

| Green (Approx. 515 nm) | |||

| UV (Approx. 355 nm) | |||

| Deep-UV (Less than or Equal to 266 nm) | |||

| By Application | Material Processing and Micromachining | ||

| Biomedical and Bio-imaging | |||

| Spectroscopy and Metrology | |||

| Scientific Research | |||

| By End User | Consumer Electronics | ||

| Medical Devices | |||

| Automotive | |||

| Aerospace and Defense | |||

| Research Institutes | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the ultrafast lasers market in 2026?

The market stands at USD 3.29 billion in 2026 and is set to double by 2031 on a 15.07% CAGR trajectory.

Which region grows fastest for ultrafast lasers?

Asia-Pacific leads with an 18.21% CAGR thanks to dense semiconductor, battery, and display manufacturing clusters.

What segment is gaining most share by pulse duration?

Femtosecond systems dominate with 62.35% share in 2025 and grow quickest at 16.42% CAGR.

Why are ultrafast lasers attractive for EV batteries?

Burst-mode femtosecond cutting delivers 40% higher throughput and zero-burr edges on 6 µm foils, preventing internal shorts.

What limits ultrafast laser adoption in heavy metal cutting?

Continuous-wave fiber lasers still cut 10 mm steel 3-5× faster and at 40% lower power, making ultrafast options costlier for thick sections.

Which wavelength segment is expanding fastest?

UV 355 nm platforms, propelled by medical-device and advanced-packaging demand, are advancing at an 17.83% CAGR.

Page last updated on: