Ultra Wideband Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

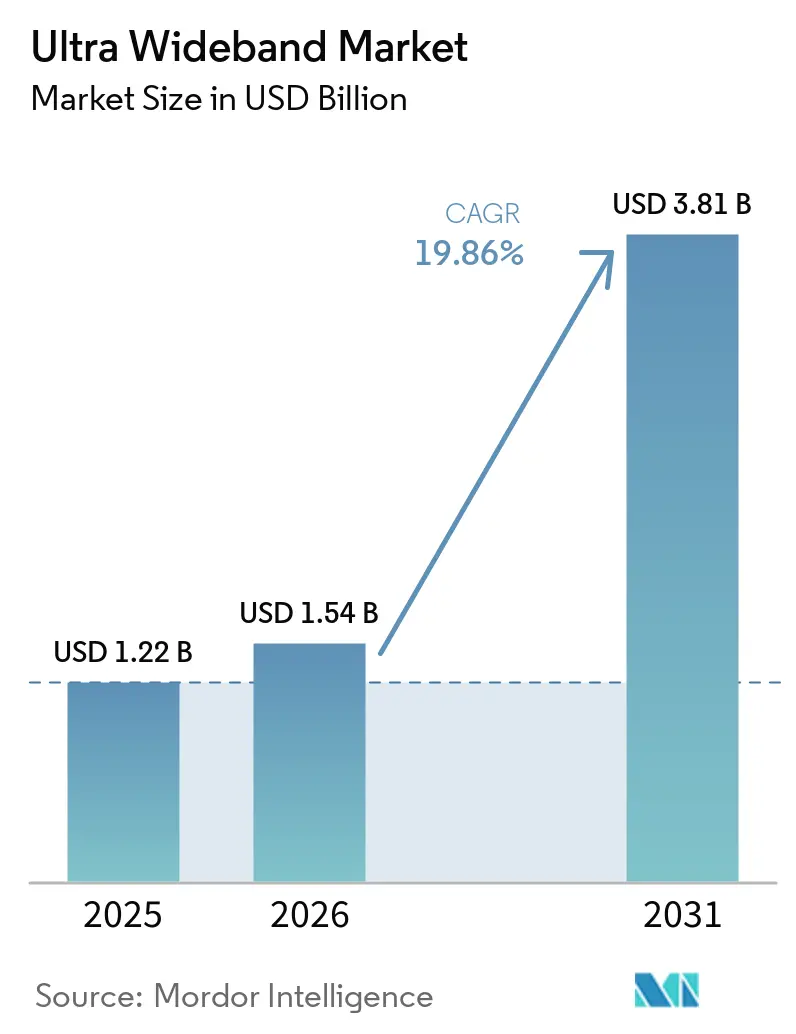

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 19.86% CAGR |

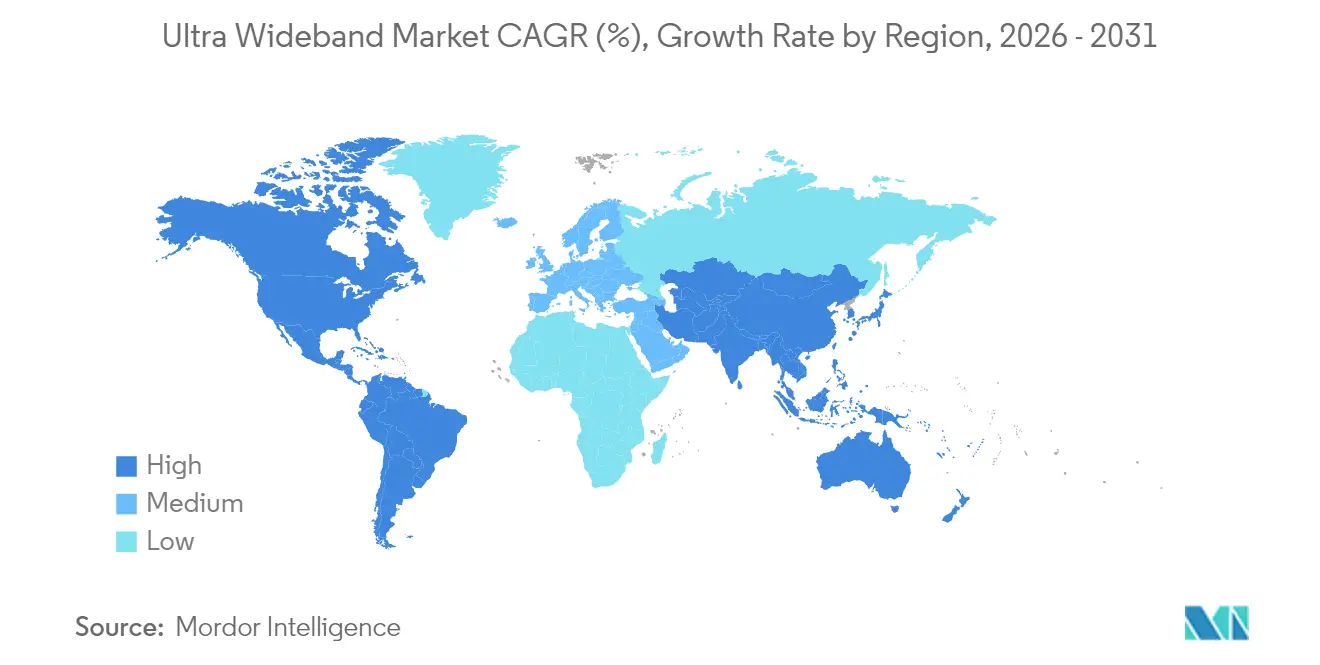

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

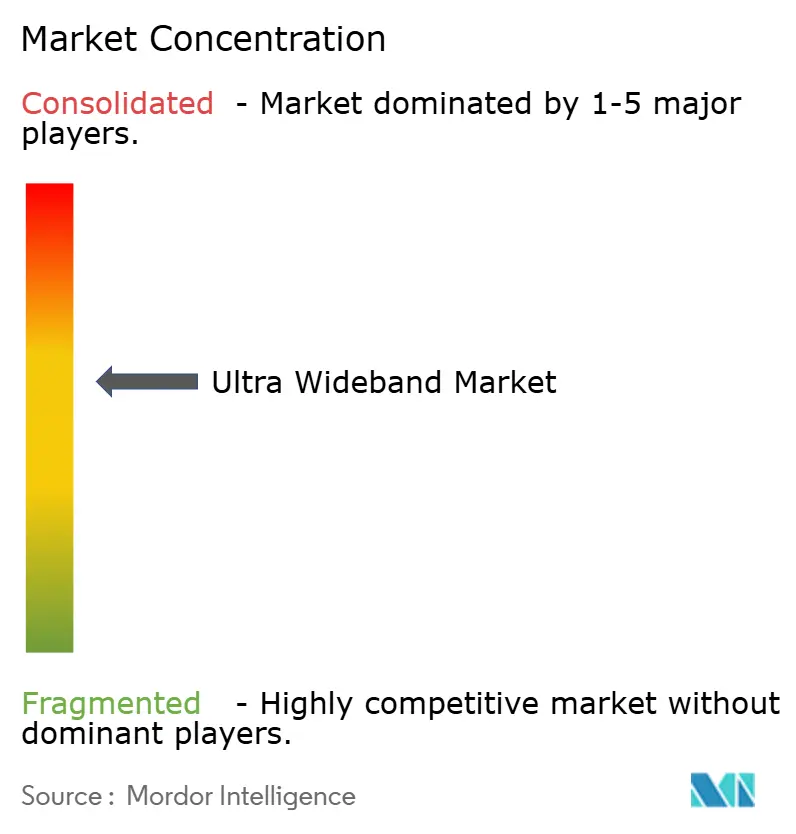

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra Wideband Market Analysis by Mordor Intelligence

The Ultra-Wideband market size was valued at USD 1.23 billion in 2025 and estimated to grow from USD 1.54 billion in 2026 to reach USD 3.81 billion by 2031, at a CAGR of 19.86% during the forecast period (2026-2031). Centimeter-level positioning accuracy is shifting the technology from smartphone novelty to an indispensable layer in Industry 4.0 automation, port logistics, and relay-attack-resistant digital keys. Manufacturers observed a 30%-40% drop in forklift-collision insurance claims after adopting sub-10-centimeter asset tracking, while fleet-leasing insurers cut premiums by up to 12% for vehicles fitted with UWB-based passive-entry systems. Regulatory momentum, notably European Union Decision 2024/1467 and China MIIT rules, doubled permissible outdoor range and removed provincial certification delays, creating an incentive for large-scale infrastructure rollouts. Meanwhile, BLE angle-of-arrival systems now reach 50-centimeter precision at one-third of UWB silicon cost, positioning cost as the main competitive battleground rather than raw accuracy. Chip supply below 28 nanometers remains tight because foundries prioritize higher-margin smartphone processors, extending module lead times to 18 weeks and forcing chipmakers to secure alternative capacity or migrate to finer geometries.

Key Report Takeaways

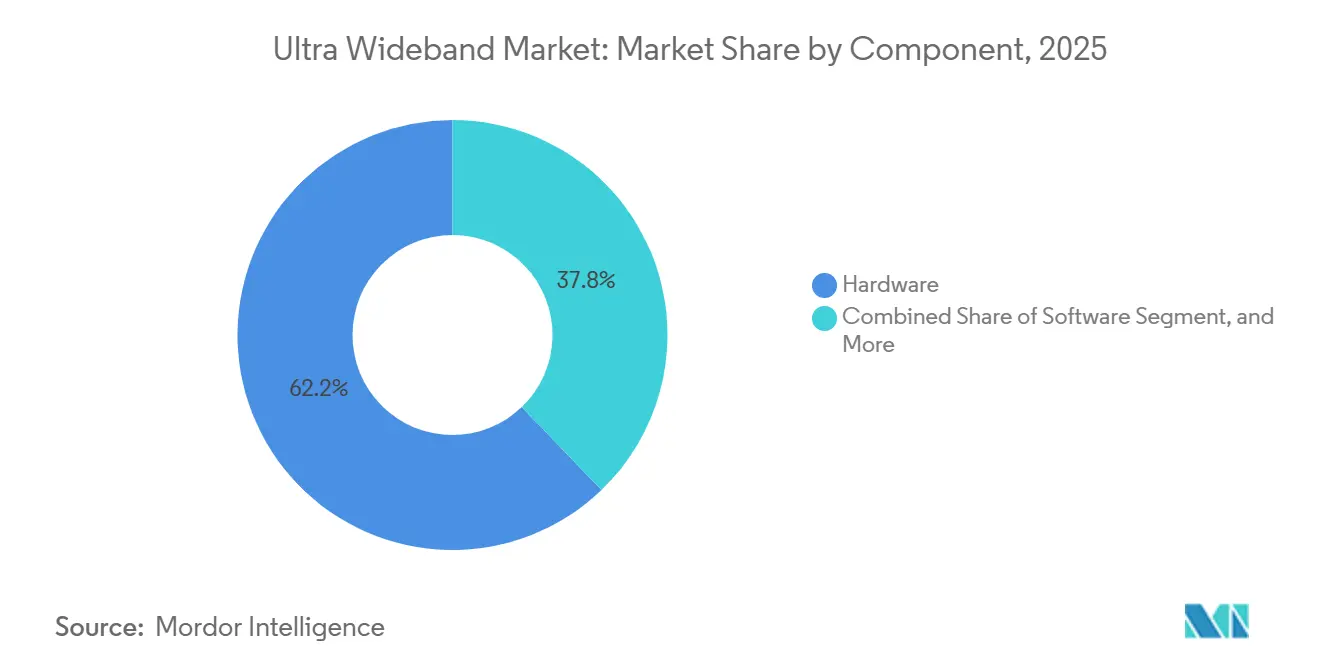

- By component, hardware led with 62.19% of 2025 revenue, while services is projected to advance at a 20.22% CAGR through 2031.

- By end-user vertical, consumer electronics held 27.42% revenue share in 2025, whereas smart buildings is forecast to expand at a 20.96% CAGR to 2031.

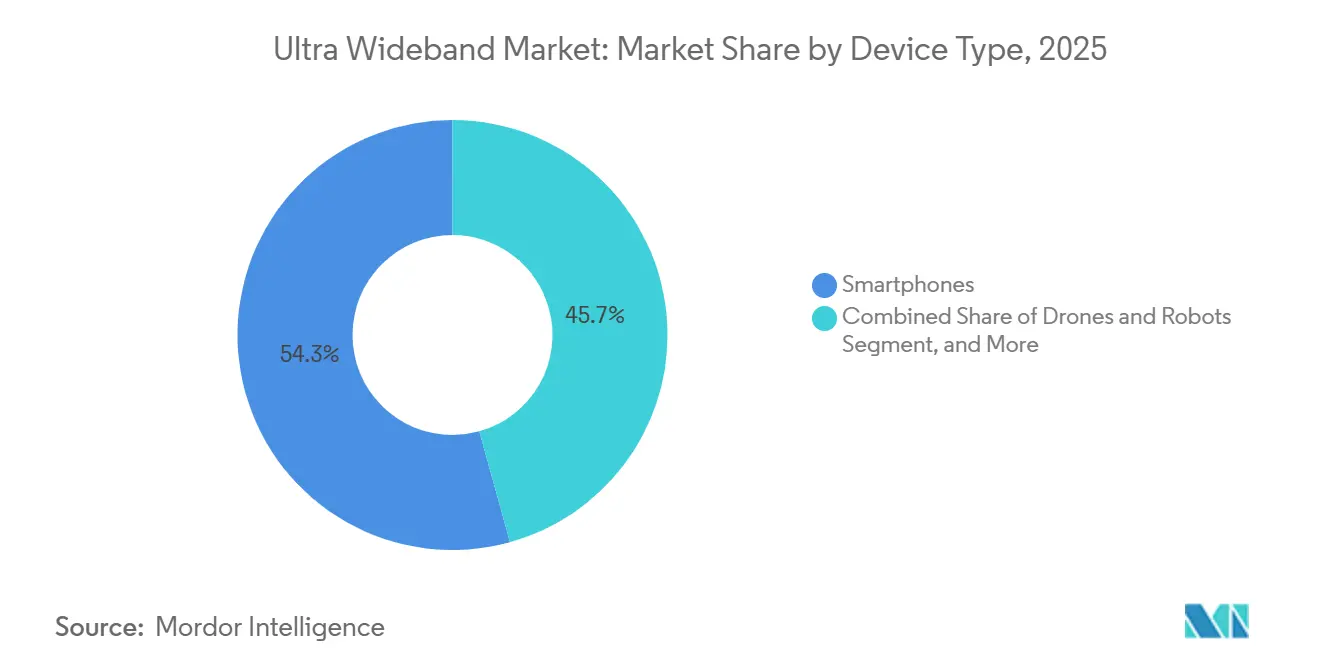

- By device type, smartphones captured 54.31% revenue share in 2025, and drones and robots are expected to grow at a 20.53% CAGR through 2031.

- By frequency band, the 6-10.6 GHz segment commanded 71.29% of 2025 deployments, whereas the 3.1-4.8 GHz band is set to progress at a 20.31% CAGR through 2031.

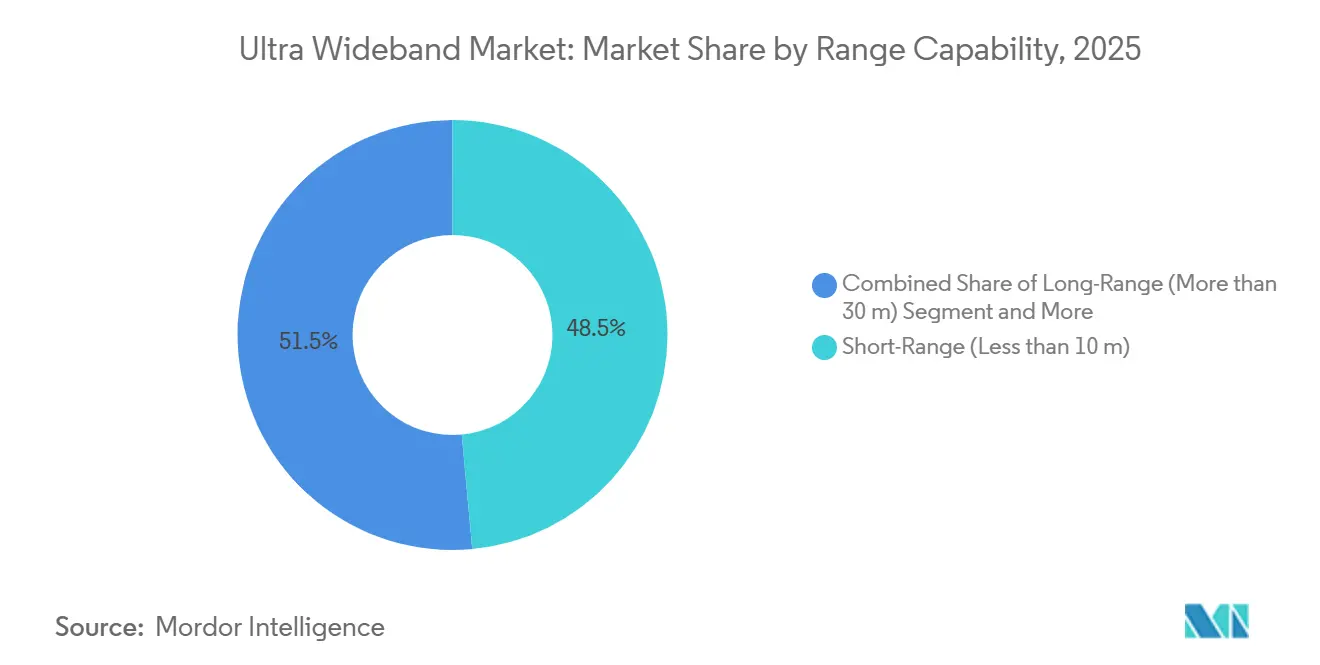

- By range capability, short-range systems accounted for 48.53% share in 2025, while long-range platforms are on track for a 20.78% CAGR toward 2031.

- By application, real-time location systems led with 41.82% revenue share in 2025, and AR and VR mapping is poised to rise at a 20.84% CAGR through 2031.

- By geography, North America maintained 36.93% share in 2025, whereas Asia-Pacific is anticipated to record a 21.01% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultra Wideband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive RTLS Demand Across Industry 4.0 Plants | +4.20% | Global, with concentration in Germany, United States, Japan, and South Korea manufacturing corridors | Medium term (2-4 years) |

| Smartphone OEM Mandate for Spatial-Awareness Features | +3.80% | Global, led by North America and Asia-Pacific premium-tier devices | Short term (≤ 2 years) |

| Regulatory Green-Lights for Sub-GHz UWB in Europe and Asia-Pacific | +3.10% | Europe (EU Decision 2024/1467), China (MIIT 7163-8812 MHz), Japan (ARIB STD-T91), South Korea | Medium term (2-4 years) |

| Automotive Shift to Digital Keys and In-Cabin Radar | +2.90% | North America, Europe, China (Tier-1 supplier ecosystems) | Long term (≥ 4 years) |

| Open-Source UWB Firmware Lowering Entry Barriers | +1.70% | Global, with early adoption in Southeast Asia and Eastern Europe developer communities | Long term (≥ 4 years) |

| National Infrastructure Funding for Smart Ports and Airports | +1.50% | Europe (TEN-T corridors), Middle East (GCC logistics hubs), Asia-Pacific (China Belt and Road terminals) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive RTLS Demand Across Industry 4.0 Plants

Automotive and discrete-parts manufacturers documented 18%-25% cuts in work-in-progress inventory after replacing barcode scans with UWB anchors that integrate directly into SAP manufacturing execution systems, triggering pallet delivery within 90 seconds.[1]Fraunhofer IML, “Industry 4.0 RTLS Deployment Guide,” Fraunhofer IML, iml.fraunhofer.de German suppliers alone deployed anchors across 1.2 million m² of floor space in 2025. Japanese electronics assemblers extended UWB to collaborative-robot safety zones where IEEE 802.15.4z secure ranging prevents spoofed emergency-stop overrides.[2]IEEE Standards Association, “IEEE 802.15.4z Technical Report,” IEEE, ieeexplore.ieee.org Module price erosion to below USD 3.50 at 10,000-unit volumes removed a key cost barrier, and South Korean semiconductor fabs are piloting cleanroom tool tracking to avert process-bay misrouting. The result is a structural transition from proof-of-concept to enterprise-wide adoption across global factory networks.

Smartphone OEM Mandate for Spatial-Awareness Features

Apple shipped iPhones with UWB across its entire 2025 lineup, enabling precise AirTag finding, spatial audio head-tracking, and relay-attack-resistant payments.[3]Apple Newsroom Staff, “Vision Pro 2 Announcement,” Apple, apple.com Samsung followed with Galaxy S25 Ultra and Z Fold 6, and Xiaomi’s 15S Pro paired UWB with digital keys for BYD and NIO vehicles. Insurers responded by offering 5%-8% discounts on devices carrying UWB secure-ranging chips, catalysing demand in premium-tier smartphones. Google added UWB commissioning to Android 15’s Matter-compliant smart-home setup, shortening onboarding time by 40% in beta trials. Interoperability pressure from FiRa Consortium profiles made cross-brand compatibility table stakes for any flagship handset.

Regulatory Green-Lights for Sub-GHz UWB in Europe and Asia-Pacific

European Union Decision 2024/1467 raised indoor transmit power by 10 decibels and opened outdoor operation in the 6-8.5 GHz band, doubling effective line-of-sight range to 30 meters. Pilot smart-city deployments in Bremen and Rotterdam now manage pedestrian flows and grant emergency-vehicle priority through UWB beacons. China MIIT harmonized the 7163-8812 MHz band on 1 August 2025, cutting smartphone certification from six months to eight weeks. Japan and South Korea aligned national rules with IEEE 802.15.4z, enabling rapid commercialization of dual-band devices. Collectively, these moves clear the regulatory fog that once slowed large-scale deployments.

Automotive Shift to Digital Keys and In-Cabin Radar

Car Connectivity Consortium Digital Key 3.0 mandates UWB secure ranging within a 2-meter perimeter, pushing BMW, Mercedes-Benz, and Hyundai to embed NXP Trimension chips in 2026 model-year vehicles. Fleet-leasing insurers responded with premium reductions of up to 12%, and relay-attack thefts fell in pilot regions. Tier-1 suppliers are also adding in-cabin radar functions for child-presence detection to satisfy Euro NCAP 5-star safety ratings. Chinese EV makers use UWB to align cars within battery-swap stations, cutting swap time from five minutes to 90 seconds. These operational benefits reinforce UWB’s value proposition beyond door unlocking.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BLE AoA/AoD Cost Advantage Under 50 cm Accuracy | -2.80% | Global, particularly in price-sensitive retail, healthcare, and hospitality segments | Short term (≤ 2 years) |

| Chip Supply Bottlenecks Below 28 nm | -2.10% | Global, with acute pressure in North America and Europe automotive supply chains | Medium term (2-4 years) |

| Fragmented Regional Spectrum Rules Slowing Certification | -1.40% | Middle East, Africa, South America (excluding Brazil), Southeast Asia (excluding Singapore) | Long term (≥ 4 years) |

| Sophisticated Micro-Location Spoofing and Side-Channel Attacks | -0.90% | Global, with heightened concern in defense, financial services, and critical infrastructure verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BLE AoA/AoD Cost Advantage Under 50 cm Accuracy

Bluetooth direction-finding modules priced near USD 1.20 achieved sub-50-centimeter precision inside retail stores, giving budget-conscious operators a viable alternative to UWB. Hospitals tracking tens of thousands of assets save USD 2 per tag, translating into six-figure capital savings. Retail pilots in 2025 confirmed BLE sufficiency for aisle-level inventory searches, with UWB justified only for theft prevention. Bluetooth SIG’s 6.0 roadmap narrows the accuracy gap to 20 centimeters, intensifying price pressure. UWB suppliers now emphasize secure ranging and relay-attack resistance, benefits that resonate in automotive and finance but less so in horizontal markets.

Chip Supply Bottlenecks Below 28 nm

Foundries prioritize higher-margin AI accelerators over mixed-signal UWB dies, stretching module lead times to 18 weeks. Automotive demand surged when digital-key designs locked for 2026 vehicles, outstripping wafer allocations by 30% in early 2026. NXP locked a long-term deal with GlobalFoundries on 22-nanometer FD-SOI to guarantee 12-week delivery, while Qorvo invested USD 150 million to migrate its DW3000 to 16-nanometer FinFET. Until these moves reach volume output in late 2027, supply tightness will moderate shipment growth and slow price declines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Monetize Post-Deployment Complexity

Ultra-wideband market size momentum rests on hardware dominance, yet enterprises increasingly outsource network calibration and firmware updates, driving services toward a 20.22% CAGR through 2031. Facilities installing 200-500 anchors across multiple buildings learned that predictive propagation models fail to capture metal racks and conveyor belts, requiring on-site tuning that often costs USD 50,000-USD 150,000 per plant. Hardware price erosion is rapid; DW3000 module costs fell 40% between 2023 and 2025, putting pressure on margins.

Software’s mid-teens slice translates raw coordinates into business triggers such as AGV dispatch, while antenna innovation from fractal and ceramic designs trims footprint 50%, enabling smartwatch and earbud use cases. Modules that bundle chips, antennas, and power management now cut certification time in half. Recurring maintenance contracts, typically 12%-18% of deployment cost, secure predictable cash flows for integrators.

By End-User Vertical: Smart Buildings Unlock Occupancy and Access Control

Smart-building deployments propel the ultra-wideband market as LEED Platinum retrofits demand occupancy sensing to optimize HVAC loads. Commercial landlords reported 20%-30% space-utilization gains, postponing costly expansions. Consumer electronics led 2025 revenue at 27.42%, yet its growth is plateauing as UWB becomes a standard flagship feature.

Secure ranging prevents badge cloning, making UWB access control the default choice in high-security facilities. Automotive and logistics maintain double-digit share via digital keys and vehicle-to-infrastructure positioning, while healthcare tracks infusion pumps and wheelchairs to reduce loss write-offs. Recurring analytics fees bolster smart-building margins, supporting continued investment even as hardware commoditizes.

By Device Type: Drones and Robots Demand Centimeter Precision

Smartphones dominated the ultra-wideband market share in 2025 at 54.31%, but drones and robots will post a 20.53% CAGR to 2031 as warehouses automate beyond pilot scale. Amazon’s 2025 rollout cut mis-sort errors by 35% versus QR-code navigation.

Outdoor drone delivery couples GPS with ground UWB to land within 10 centimeters, ideal for precision agriculture, yet constrained to 200 meters by anchor line-of-sight. Wearables and hearables add spatial audio and find-my-device utility, increasing attach rates in premium earbuds. Vehicle integration follows multi-year design cycles, signalling volume uplift only from 2027. Chinese anchor suppliers undercut incumbents by up to 60%, moving differentiation to software network effects.

By Frequency Band: Sub-6 GHz Gains Regulatory Momentum

The 6-10.6 GHz band retains 71.29% of 2025 deployments, but sub-6 GHz frequencies are on a 20.31% CAGR trajectory as regulation favours better wall penetration. Dual-band chipsets that switch between 3.1-4.8 GHz and 7.25-10.25 GHz entered 2026 roadmaps at Qorvo and NXP.

The ultra-wideband market size for industrial verticals leans toward lower frequencies to overcome metal clutter, even though dual-band antennas increase module footprint 20%. Outside the core regions, fragmented rules complicate certification, keeping single-band phones on the legacy spectrum. Over time, industrial preference for range and consumer demand for compactness will coexist, encouraging flexible radios that reconfigure in software.

By Range Capability: Long-Range Unlocks Port and Airport Use Cases

Short-range platforms held 48.53% of 2025 revenue, yet long-range systems above 30 meters are projected to grow 20.78% through 2031 on the back of port and airport automation. Rotterdam’s 12 km² deployment cut truck dwell time by 18% with 20-centimeter accuracy.

Range expansion is physics-limited because signal power decays with distance, so providers either push transmit power where regulations allow or add low-noise amplifiers that lift silicon cost USD 1-USD 2. Baggage mishandling costs airlines USD 2.5 billion annually, and UWB tracking reduces errors up to 50%. Ultimately, the right-sized network balances anchor density against accuracy and battery life.

By Application: AR and VR Mapping Emerges as Growth Leader

Real-time location systems produced 41.82% of 2025 revenue, but AR and VR mapping will accelerate at a 20.84% CAGR, powered by Apple Vision Pro 2 headsets that anchor virtual objects with 2-centimeter fidelity.

Industrial training apps from Siemens and Rockwell Automation cut technician onboarding time 30%-40% by overlaying step-by-step guides. Secure digital keys stay resilient thanks to CCC mandates, whereas asset tracking now competes head-to-head with lower-cost BLE in price-sensitive sectors. Smart-home automation leaps forward under Matter 1.3, which uses UWB commissioning to eliminate QR scans, delivering a smoother consumer experience.

Geography Analysis

North America accounted for 36.93% of 2025 revenue, with United States insurers granting 8%-12% fleet-premium cuts for UWB digital-key vehicles and factories covering 15 million ft² with anchors. Canada lagged due to delayed spectrum allocation, corrected only in January 2026, while Mexico’s nearshoring boom deployed RTLS from day one. Cost-sensitive verticals lean toward BLE, and semiconductor shortages exacerbate automotive wait times.

Asia-Pacific is forecast to register a 21.01% CAGR, the fastest globally. China’s unified 7163-8812 MHz rules shortened smartphone approval cycles to eight weeks, and flagship phones paired UWB with EV digital keys. Japan’s 2024 ARIB update enabled 50,000 daily UWB payments at Tokyo metro stations starting March 2026. South Korea’s rule harmonization let Samsung launch UWB-enabled Galaxy S25 Ultra without extra certification. India and most of Southeast Asia remain early-stage due to price sensitivity, though Singapore and Kuala Lumpur pilots improved pedestrian flow 30%-40%. Australia and New Zealand mirrored EU standards, easing mining-sector adoption.

Europe captured a mid-twenties share in 2025 thanks to Decision 2024/1467 that opened outdoor use and raised power limits. Germany leads with automotive mandates and 8 million ft² of RTLS-equipped plants. France and United Kingdom face dual certification, slowing market entry by up to 12 weeks. Spain and Italy focus on temperature-controlled pharma logistics, while Russia’s access to advanced chipsets is limited by trade restrictions. GCC ports in Dubai and Abu Dhabi piloted 20-centimeter container tracking, whereas African adoption is nascent, with South Africa trailing mining safety programs.

Competitive Landscape

The ultra-wideband market is highly concentrated at the silicon level yet fragmented in software. Apple, Qorvo, and NXP jointly owned 70% of chipset shipments in 2025, leveraging strong patent portfolios and FiRa Consortium leadership. Apple’s closed U2-chip ecosystem connects 200 million devices, although it limits cross-platform interoperability.

Qorvo dominates industrial RTLS through its DW3000 line, while NXP’s Trimension chip secured most automotive digital-key wins. Open-source firmware in Zephyr RTOS and low-cost Chinese modules priced between USD 30-USD 50 are eroding entry barriers, creating a white-space opportunity for integrators that bundle Omlox-compliant software with consumer-grade Matter flows.

Strategies diverge: Qualcomm and Broadcom embed UWB in combo connectivity SoCs to gain ecosystem scale, whereas niche players like Humatics and Sewio monetize vertical expertise via SaaS models. Patent concentration is 65% among the top five firms, attracting antitrust interest in Europe and China. Differentiation now hinges on power draw, security layers, and multi-band agility rather than sub-10-centimeter accuracy, which is already table stakes across leading chipsets.

Ultra Wideband Industry Leaders

Qorvo Inc.

NXP Semiconductors NV

Zebra Technologies Corp.

Texas Instruments Inc.

Samsung Electronics Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Qorvo launched the QM35825 fully integrated low-power UWB System-on-Chip targeting automotive and industrial designs.

- December 2024: Syntiant completed the USD 150 million acquisition of Knowles Consumer MEMS Microphones, enhancing edge-AI audio for UWB-enabled gadgets.

- November 2024: NXP Semiconductors unveiled the first UWB wireless battery-management system for electric-vehicle packs.

- October 2024: Qualcomm and STMicroelectronics formed a strategic collaboration to merge Qualcomm connectivity platforms with ST’s MEMS sensors for IoT devices.

- February 2024: Qualcomm introduced the FastConnect 7900 single-chip solution, integrating Wi-Fi 7, Bluetooth, and UWB for premium smartphones and connected cars.

Global Ultra Wideband Market Report Scope

The Ultra Wideband Market Report is Segmented by Component (Hardware, Software, Services), End-User Vertical (Consumer Electronics, Automotive and Transportation, Healthcare, Manufacturing and Industrial, Retail and Warehousing, Defense and Public Safety, Smart Buildings), Device Type (Smartphones, Wearables and Hearables, Vehicles, Drones and Robots, Fixed Infrastructure), Frequency Band (3.1-4.8 GHz, 6-10.6 GHz), Range Capability (Short-Range, Mid-Range, Long-Range), Application (RTLS, Secure Digital Keys, AR/VR Mapping, Asset Tracking, Smart Home Automation), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Hardware | ICs/Chipsets |

| Antennas | |

| Modules | |

| Software | |

| Services |

| Consumer Electronics |

| Automotive and Transportation |

| Healthcare |

| Manufacturing and Industrial |

| Retail and Warehousing |

| Defense and Public Safety |

| Smart Buildings |

| Smartphones |

| Wearables and Hearables |

| Vehicles |

| Drones and Robots |

| Fixed Infrastructure (Gateways, Beacons) |

| 3.1-4.8 GHz |

| 6-10.6 GHz |

| Short-Range (Less than 10 m) |

| Mid-Range (10-30 m) |

| Long-Range (More than 30 m) |

| Real-Time Location Systems (RTLS) |

| Secure Digital Keys |

| Augmented and Virtual Reality (AR/VR) Mapping |

| Asset Tracking and Inventory Management |

| Smart Home and Building Automation |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Component | Hardware | ICs/Chipsets |

| Antennas | ||

| Modules | ||

| Software | ||

| Services | ||

| By End-User Vertical | Consumer Electronics | |

| Automotive and Transportation | ||

| Healthcare | ||

| Manufacturing and Industrial | ||

| Retail and Warehousing | ||

| Defense and Public Safety | ||

| Smart Buildings | ||

| By Device Type | Smartphones | |

| Wearables and Hearables | ||

| Vehicles | ||

| Drones and Robots | ||

| Fixed Infrastructure (Gateways, Beacons) | ||

| By Frequency Band | 3.1-4.8 GHz | |

| 6-10.6 GHz | ||

| By Range Capability | Short-Range (Less than 10 m) | |

| Mid-Range (10-30 m) | ||

| Long-Range (More than 30 m) | ||

| By Application | Real-Time Location Systems (RTLS) | |

| Secure Digital Keys | ||

| Augmented and Virtual Reality (AR/VR) Mapping | ||

| Asset Tracking and Inventory Management | ||

| Smart Home and Building Automation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the ultra wideband market in 2026?

The ultra wideband market size is estimated at USD 1.54 billion in 2026 based on the latest forecast.

What is the expected growth rate for ultra wideband through 2031?

The market is projected to grow at a 19.86% CAGR from 2026 to 2031, reaching USD 3.81 billion.

Which segment will expand fastest within ultra wideband deployments?

Smart-building solutions are forecast to post the highest 20.96% CAGR as occupancy sensing and secure access control gain regulatory traction.

Why are drones and robots adopting ultra wideband?

Warehouse and delivery robots need centimeter-level navigation that GPS and visual markers cannot provide reliably indoors, and UWB meets that accuracy requirement while resisting lighting changes.

How are regulations influencing ultra wideband uptake?

European Union and China spectrum reforms raised power limits and standardized bands, effectively doubling outdoor range and eliminating multi-province certifications, which accelerates device launches.

What threat does Bluetooth direction finding pose to ultra wideband?

BLE angle-of-arrival systems now reach 50-centimeter accuracy at one-third the silicon cost, which can satisfy many retail and healthcare use cases and slow UWB adoption where centimeter precision is not essential.

Page last updated on: