Ultra-pure Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.36 Billion |

| Market Size (2031) | USD 14.73 Billion |

| Growth Rate (2026 - 2031) | 9.50% CAGR |

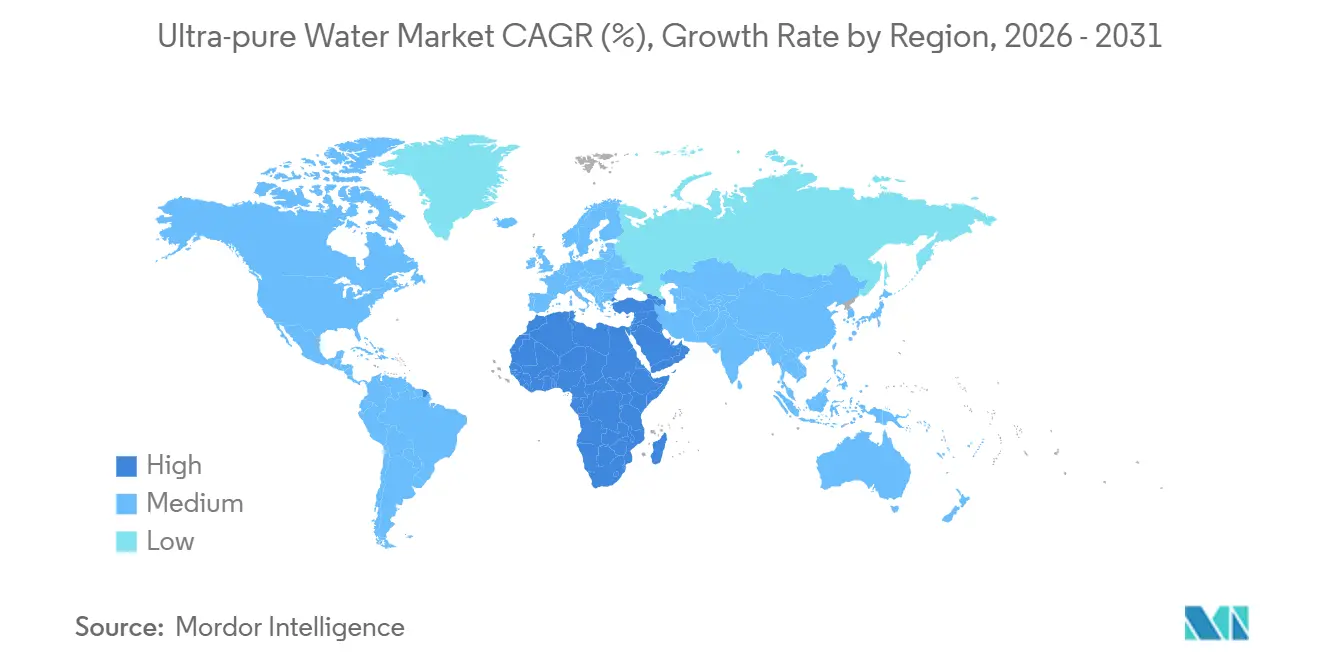

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra-pure Water Market Analysis by Mordor Intelligence

The Ultra-pure Water Market size is expected to increase from USD 8.55 billion in 2025 to USD 9.36 billion in 2026 and reach USD 14.73 billion by 2031, growing at a CAGR of 9.50% over 2026-2031. Three structural growth forces underpin this trajectory. First, semiconductor fabs migrating to sub-3 nm nodes demand water with total organic carbon (TOC) below 0.1 ppb, pushing plants to install multi-stage polishing loops and real-time analyzers. Second, continuous-bioprocessing lines in pharmaceuticals require water-for-injection systems that run 24/7 with inline conductivity and TOC monitoring, creating new installations in North America and Europe. Third, developers of gigawatt-scale green-hydrogen projects specify feed-water resistivity above 18 MΩ-cm and conductivity under 0.1 µS/cm, opening a multiregional pipeline of reverse-osmosis (RO) and electrodeionization (EDI) skids. Supplementary demand stems from the rapid scale-up of 300 mm silicon-carbide lines, the rise of ultrahigh-pressure liquid-chromatography labs, and stricter Scope 3 carbon-disclosure rules that spotlight energy intensity across RO and EDI stages.

Key Report Takeaways

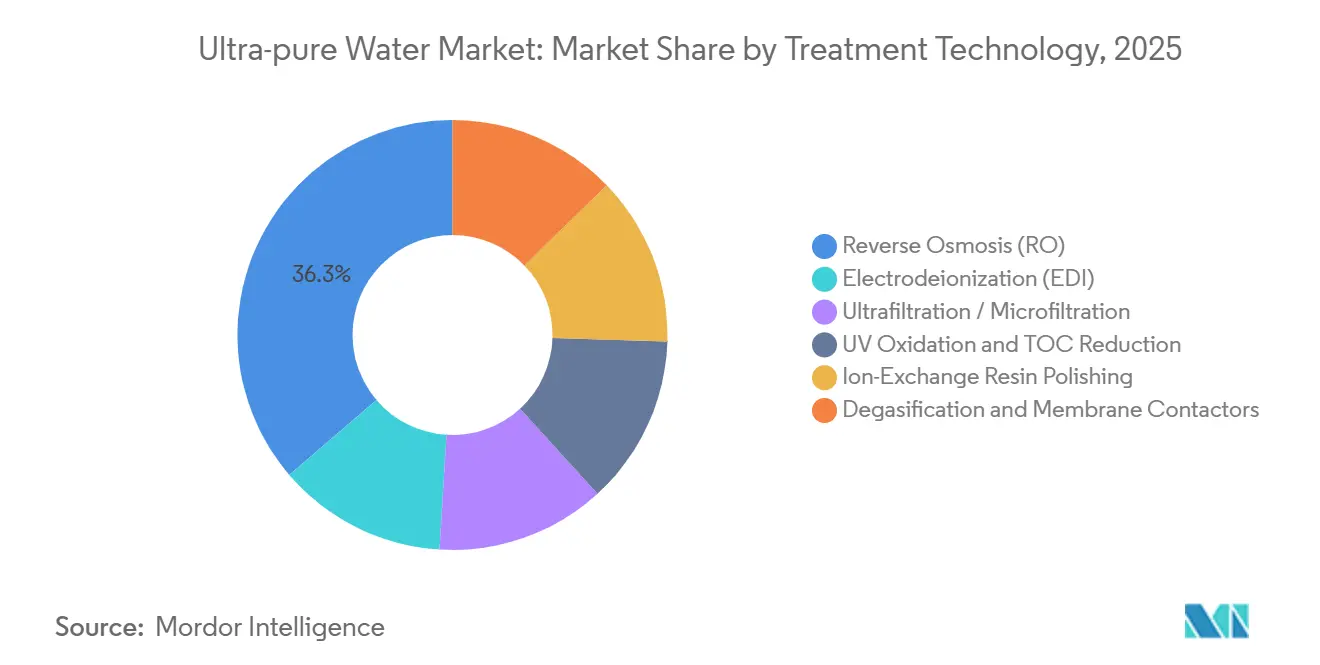

- By treatment technology, reverse osmosis (RO) led with 36.28% of the ultra-pure water market share in 2025; electrodeionization (EDI) is advancing at a 9.92% CAGR through 2031.

- By application, cleaning held 38.12% of the ultra-pure water market size in 2025 while high-performance liquid chromatography (HPLC) is forecast to expand at a 9.89% CAGR to 2031.

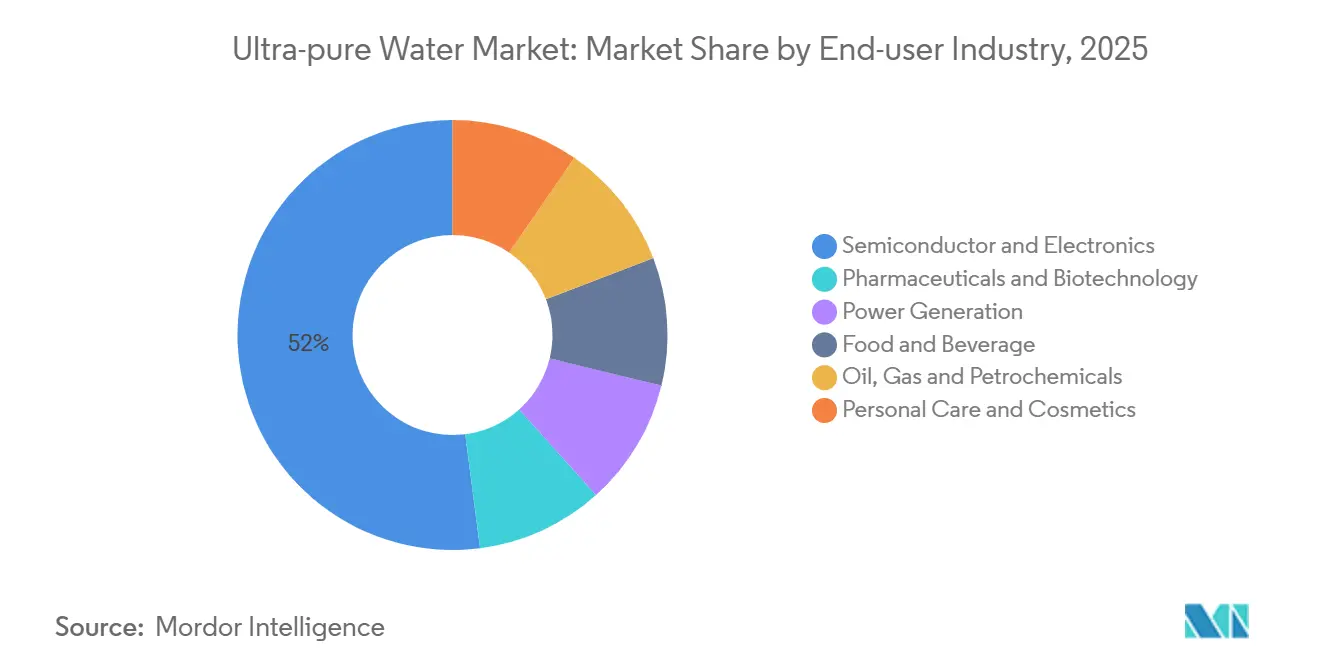

- By end-user industry, semiconductor and electronics accounted for 52.05% share of the ultra-pure water market size in 2025, whereas pharmaceuticals and biotechnology is growing at a 9.83% CAGR through 2031.

- By geography, Asia-Pacific captured 47.35% revenue share in 2025 and the Middle-East and Africa region is advancing at a 9.73% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultra-pure Water Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying wafer-cleaning volumes in advanced-node semiconductor fabs | +2.8% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Rapid expansion of 300mm and 12-inch SiC device lines | +1.9% | Asia-Pacific, North America | Medium term (2-4 years) |

| Pharmaceutical shift toward continuous bioprocessing | +1.6% | North America, Europe | Short term (≤ 2 years) |

| Booming green-hydrogen electrolyzer build-out (Giga-scale) | +2.1% | Global, with concentration in Europe, Middle-East | Long term (≥ 4 years) |

| Decentralised micro-LED display fabs adopting on-site mini-UPW skids | +1.0% | Asia-Pacific, selective North America sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Wafer-Cleaning Volumes in Advanced-Node Semiconductor Fabs

Gate-all-around transistors at the 2 nm node require rinse cycles that cut metal ions to below 0.01 ppb, forcing fabs to add ultraviolet oxidation and mixed-bed polishing beyond conventional RO. Taiwan Semiconductor Manufacturing Company’s Arizona campus, online since 2024, uses EDI to remove the need for caustic regeneration and lowers hazardous waste by 40%. Japan’s National Institute of Advanced Industrial Science and Technology showed in 2025 that extreme-ultraviolet lithography demands PFAS-free rinse chemistry, quickening uptake of ozone-based oxidation. Each 300 mm wafer now passes through 12 rinse steps, translating to 2.5 million gpd for a fab at 40,000 wafer starts per month[1]National Institute of Standards and Technology, “CHIPS Program Environmental Assessment,” nist.gov .

Rapid Expansion of 300 mm and 12-Inch SiC Device Lines

Silicon-carbide power devices need pre-clean water with resistivity above 18 MΩ-cm and dissolved oxygen below 5 ppb to avert micro-roughness. SK Siltron’s Gumi plant switched to an on-site UPW system in Dec 2024, cutting logistics cost by 25%. Infineon’s Villach fab consumes 1.8 million gpd today and plans to recycle 60% of rinse water by 2027. Degasification membrane contactors that strip CO₂ without particles are fast becoming standard to protect EPI reactors.

Pharmaceutical Shift Toward Continuous Bioprocessing

ICH Q13, finalized in Mar 2023, mandates real-time quality verification of water-for-injection, guiding firms to membrane-based systems sanitized by hot water rather than distillation. The International Society for Pharmaceutical Engineering endorsed 0.2 µm filtration at ≥ 70 °C in May 2022, widening acceptance of skid-mounted UPW generators. Eli Lilly’s Lebanon facility uses inline TOC sensors that trip diversion valves on any quality drift, reinforcing demand for advanced control loops.

Booming Green-Hydrogen Electrolyzer Build-Out (Giga-Scale)

The International Energy Agency logs 1,100 announced projects totaling 570 GW electrolyzer capacity by 2030, equivalent to more than 2 billion gpd of UPW demand if built. Saudi Arabia’s NEOM complex integrates three-pass RO, EDI, and ultraviolet oxidation to hit TOC below 10 ppb on a 2.2 GW array scheduled for 2026. The U.S. Hydrogen Shot targets cost parity at USD 1/kg by 2031, compelling operators to slash downtime through tighter pretreatment specs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of multi-stage polishing systems (less than 0.1 ppb TOC) | -1.4% | Global, acute in emerging semiconductor markets | Short term (≤ 2 years) |

| Supply–demand imbalance of semiconductor-grade ion-exchange resins | -1.1% | Asia-Pacific, North America | Medium term (2-4 years) |

| Rising energy-intensity scrutiny under net-zero disclosure mandates | -0.8% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Multi-Stage Polishing Systems (Less Than 0.1 ppb TOC)

Meeting sub-0.1 ppb TOC dictates dual-wavelength UV, mixed-bed resin, and 0.05 µm filtration, costing up to USD 50 million for a single 300 mm fab line and raising payback periods beyond five years for smaller players[2]United States Environmental Protection Agency, “RCRA Hazardous Waste Regulations,” epa.gov. UV lamps need replacement every 8,000 – 12,000 h while resin regeneration consumes acids and caustics that trigger hazardous-waste permits, adding operational drag.

Supply–Demand Imbalance of Semiconductor-Grade Ion-Exchange Resins

Nuclear-grade resins with leachables under 0.01 ppb come from fewer than ten sites worldwide. Lead times hit 18 months in 2024. Mitsubishi Chemical’s 30% Mizushima expansion announced Apr 2026 (5,000 t/y) will ease pressure only after late 2027. DuPont cited 14-month order backlogs in 2025 even after 12% YoY output growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Technology: Electrodeionization Gains on Regeneration-Free Operation

Reverse osmosis captured 36.28% of the ultra-pure water market share in 2025, while electrodeionization is forecast at a 9.92% CAGR through 2031, reflecting end-user moves to avoid chemical regeneration downtime. RO membranes now reject more than 99.5% dissolved salts at 15-25 bar, cutting single-pass salinity to sub-10 ppm and setting the stage for downstream polishing. EDI uses ion-exchange membranes plus direct current to continuously strip ions, delivering resistivity above 17 MΩ-cm without acids or caustics, trimming hazardous waste by up to 6 m³ per m³ of resin and reducing energy bills by 30% in continuous lines.

Ultraviolet oxidation at 185 nm photolyzes organics down to 1 ppb TOC for semiconductor rinse water. Ion-exchange resin beds still dominate the final pass for sub-0.1 ppb TOC, despite resin scarcity. Degasification membrane contactors remove dissolved O₂ and CO₂, protecting SiC epi reactors that crack above 1,100 °C and require silica under 0.02 ppm. Inline analyzers mandated by SEMI F63 now track resistivity, TOC, particles, and metals in real time, integrating with fab SCADA loops.

By Application: High-Performance Liquid Chromatography Rides Biopharmaceutical Expansion

Cleaning held 38.12% of the ultra-pure water market size in 2025 as each 300 mm wafer uses about 15 L per etch rinse and fabs averaged 4.25 billion gal annual UPW draw in the United States. SEMI F63 drives TOC below 1 ppb and particles under 0.05 mL⁻¹, sustaining demand for multi-loop polish and redundant filtration in wafer cleans.

High-performance liquid chromatography is rising at a 9.89% CAGR because UHPLC systems need Type 1 water at 18.2 MΩ-cm and TOC less than 5 ppb to prevent ghost peaks. Continuous-manufacturing adoption after ICH Q13 pushes labs to replace aging deionizers with EDI skids that hold water quality steady without regeneration spikes. Ingredient-grade water for injectables and beverages follows the U.S. Pharmacopeia TOC less than 500 ppb and endotoxin less than 0.25 EU/mL, widening point-of-use polish cartridge purchases.

By End-user Industry: Pharmaceuticals Accelerate on Continuous Bioprocessing

Semiconductor and electronics retained 52.05% of revenue in 2025 as 300 mm fabs draw 2-3 million gpd and refresh loops to satisfy sub-32 nm particle limits EPA.GOV. TSMC’s Kumamoto and Samsung’s Pyeongtaek expansions both installed dual-pass RO plus EDI trains that achieved less than 1 ppb TOC for 12 nm and 3 nm flows TSMC.COM.

Pharmaceuticals and biotechnology are growing at 9.83% CAGR to 2031, fueled by skid-mounted WFI systems that deliver endotoxin below 0.25 EU/mL and operate continuously under ICH Q13 guidance. CSL, Pfizer, and Eli Lilly now specify inline TOC analyzers across both upstream and downstream suites, driving demand for modular UPW rooms with 24/7 data logging.

Power generation, food and beverage, and petrochemicals round out end-user demand. ASME boiler codes limit silica to less than 0.02 ppm, steering conventional plants toward condensate polishing. Saudi Aramco’s Jazan refinery integrates RO and ion-exchange polish to feed hydrogen reformers at 15 million gpd.

Geography Analysis

Asia-Pacific contributed 47.35% of 2025 revenue, energized by TSMC’s Kumamoto fab online in Feb 2024, Samsung’s Pyeongtaek 3 nm ramp, and SMIC’s self-reliance drive that collectively consume more than 1.2 billion gpd of UPW. Japan’s METI pledged JPY 476 billion (USD 3.2 billion) to back TSMC-2, adding 1.5 million gpd UPW by 2028. Regionalization is spreading as SK Siltron localizes resin and UPW logistics in South Korea.

In North America, Arizona’s groundwater caps compelled TSMC and Intel to invest in closed-loop reclaim plants that recover more than 75% rinse water. The Hydrogen Shot has seeded electrolyzer hubs in Texas and California that will need 150 million gpd UPW by 2030.

Europe is led by Infineon’s Villach SiC line (1.8 million gpd) and EU Hydrogen Bank subsidies that pair RO-EDI trains with Spanish coastal electrolyzers. GlaxoSmithKline and AstraZeneca are retrofitting continuous-bioprocess WFI systems under MHRA’s 2024 ICH Q13 adoption.

South America, plus Middle-East and Africa supplied the lower share. The NEOM hydrogen complex will anchor 2.2 GW PEM electrolyzers and lift regional growth through 2031. UAE petrochemical corridors co-locate desalination brine polishers to satisfy catalyst‐grade purity.

Competitive Landscape

The ultra-pure water market shows moderate concentration. Kurita Water Industries, Veolia, and Organo control most turnkey engineering, while DuPont, Pall, and Asahi Kasei dominate membranes and resins. Kurita posted 14% YoY electronics growth in fiscal 2025 and is co-developing pre-fabricated skids with Samsung Engineering to cut install time by 20%. Veolia signed a 15-year O&M deal for a New Jersey WFI plant using membrane-based generation compliant with ICH Q13.

Technology edge now lies in sub-0.1 ppb TOC at lower energy. DuPont’s FilmTec Fortilife XC RO membrane series operates 15% lower feed pressure, saving 0.2 kWh/m³ and paring Scope 2 CO₂ under ISSB rules. SnowPure and Rodi Systems chase decentralized micro-LED fabs with containerized UPW skids sized at 10,000-50,000 gpd and 12-week lead times. Patent activity in 2024-25 on graphene-oxide RO and plasma-enhanced UV foretell margin resets by 2028.

Ultra-pure Water Industry Leaders

Veolia

Kurita Water Industries Ltd.

Xylem

Organo Corporation

Ovivo Water Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ion Exchange (India) Limited secured contracts valued at approximately INR 205 crore for ultra-pure water and wastewater treatment systems from Rayzon Energy and INOX Solar. These included an INR 95 crore contract for a 5.1 GW solar project in Gujarat and an INR 110 crore contract for a solar cell facility in Odisha.

- March 2025: Gradiant secured a contract to design and construct a significant ultrapure water (UPW) facility for a prominent semiconductor manufacturer in Dresden, Germany. The project, managed by Gradiant's Germany-based team, supported the region's chip supply chain and marked their second major specialized water treatment project in the city.

Global Ultra-pure Water Market Report Scope

Ultra-pure water (UPW) has been purified to high standards and is used to ensure contaminants don't impact various processes. Semiconductor, pharmaceutical, and power generation are major industries that utilize ultrapure water for cleaning, etching, and other applications.

The ultra-pure water market is segmented by treatment technology, application, end-user industry, and geography. By treatment technology, the market is segmented into reverse osmosis (RO), electrodeionization (EDI), ultrafiltration/microfiltration, UV oxidation and TOC reduction, ion-exchange resin polishing, and degasification and membrane contactors. By application, the market is segmented into cleaning, etching, ingredient, high-performance liquid chromatography (HPLC), and immune chemistry. By end-user industry, the market is segmented into semiconductor and electronics, pharmaceuticals and biotechnology, power generation, food and beverage, oil, gas and petrochemicals, and personal care and cosmetics. The report also covers the market size and forecasts for ultra-pure water in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Reverse Osmosis (RO) |

| Electrodeionization (EDI) |

| Ultrafiltration/Microfiltration |

| UV Oxidation and TOC Reduction |

| Ion-Exchange Resin Polishing |

| Degasification and Membrane Contactors |

| Cleaning |

| Etching |

| Ingredient |

| High-performance Liquid Chromatography (HPLC) |

| Immune Chemistry |

| Semiconductor and Electronics |

| Pharmaceuticals and Biotechnology |

| Power Generation |

| Food and Beverage |

| Oil, Gas and Petrochemicals |

| Personal Care and Cosmetics |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Treatment Technology | Reverse Osmosis (RO) | |

| Electrodeionization (EDI) | ||

| Ultrafiltration/Microfiltration | ||

| UV Oxidation and TOC Reduction | ||

| Ion-Exchange Resin Polishing | ||

| Degasification and Membrane Contactors | ||

| By Application | Cleaning | |

| Etching | ||

| Ingredient | ||

| High-performance Liquid Chromatography (HPLC) | ||

| Immune Chemistry | ||

| By End-user Industry | Semiconductor and Electronics | |

| Pharmaceuticals and Biotechnology | ||

| Power Generation | ||

| Food and Beverage | ||

| Oil, Gas and Petrochemicals | ||

| Personal Care and Cosmetics | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast is the ultra-pure water market expected to grow between 2026 and 2031?

The Ultra-pure Water Market size is expected to increase from USD 8.55 billion in 2025 to USD 9.36 billion in 2026 and reach USD 14.73 billion by 2031, growing at a CAGR of 9.50% over 2026-2031.

Which end-use sector dominates demand today?

Semiconductor and electronics facilities held 52.05% revenue share in 2025, owing to the massive rinse-water needs of sub-32 nm fabs.

What segment is expanding the quickest?

Electrodeionization technology is advancing at a 9.92% CAGR through 2031 as operators shift away from mixed-bed resin regeneration cycles.

Which region leads the ultra-pure water market?

Asia-Pacific generated 47.35% of global revenue in 2025, anchored by new fab capacity in Japan, South Korea, and China.

Page last updated on: