United Kingdom Prepaid Card Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

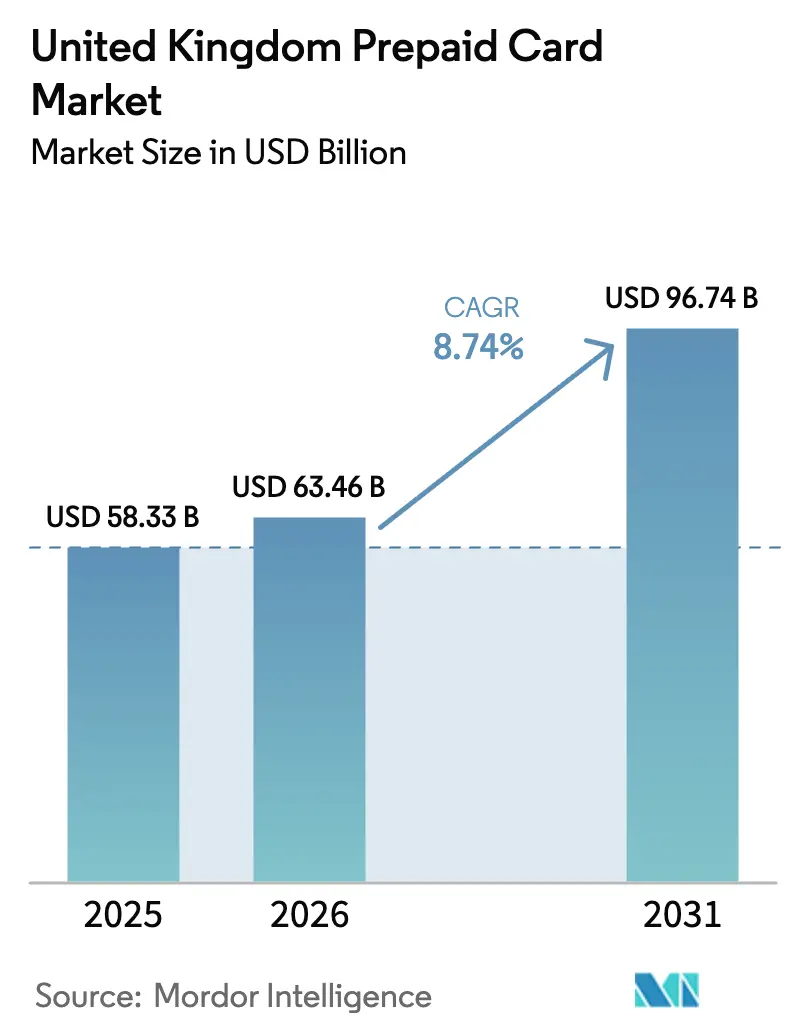

| Base Year Market Size (2025) | USD 58.33 Billion |

| Market Size (2026) | USD 63.46 Billion |

| Market Size (2031) | USD 96.74 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Prepaid Card Market Analysis by Mordor Intelligence

The United Kingdom Prepaid Card Market size is expected to increase from USD 58.33 billion in 2025 to USD 63.46 billion in 2026 and reach USD 96.74 billion by 2031, growing at a CAGR of 8.74% over 2026-2031.

Momentum reflects continued migration away from cash and toward digital payments, supported by strong contactless and mobile wallet usage in daily commerce. Issuer disclosures point to rising card monetization at scale, as leading players report growth in card fee income and volumes in 2025 and 2026. Regulatory changes around authorised push payment reimbursement sharpen issuer incentives to harden fraud defences and to reconfigure disbursement flows for vulnerable users. Open-loop configurations gain traction on acceptance strength and wallet integration, while government benefit programs strengthen the demand case for controlled prepaid rails. Revolut reported that its systems prevented over USD 809.47 million (GBP 600 million) of attempted fraud during 2024, underscoring a widening security investment cycle as adoption scales.[1]Revolut Group Holdings Ltd., “2024 Annual Report,” Revolut Group Holdings Ltd., assets.revolut.com

Key Report Takeaways

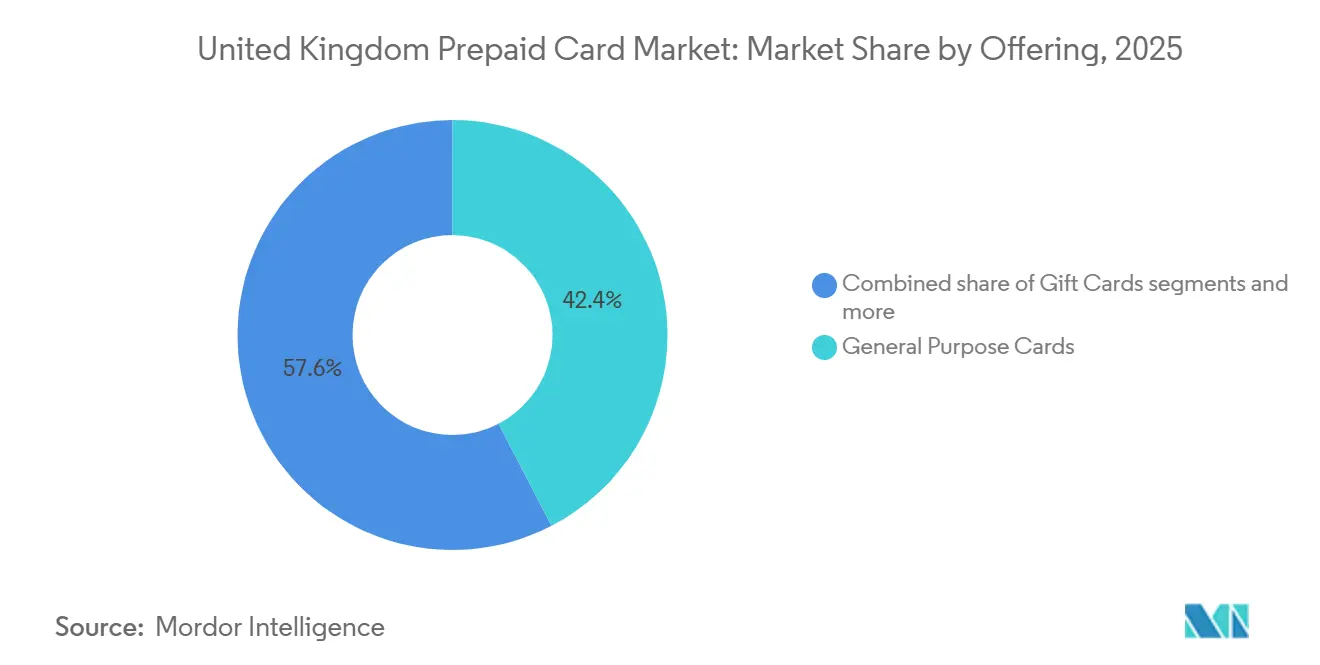

- By offering, general-purpose cards led the United Kingdom prepaid card market with 42.38% market share in 2025, while government benefit cards are projected to expand at a 12.73% CAGR through 2031.

- By card type, open-loop cards held 59.85% of the United Kingdom prepaid card market share in 2025 and are expected to advance at a 10.74% CAGR through 2031.

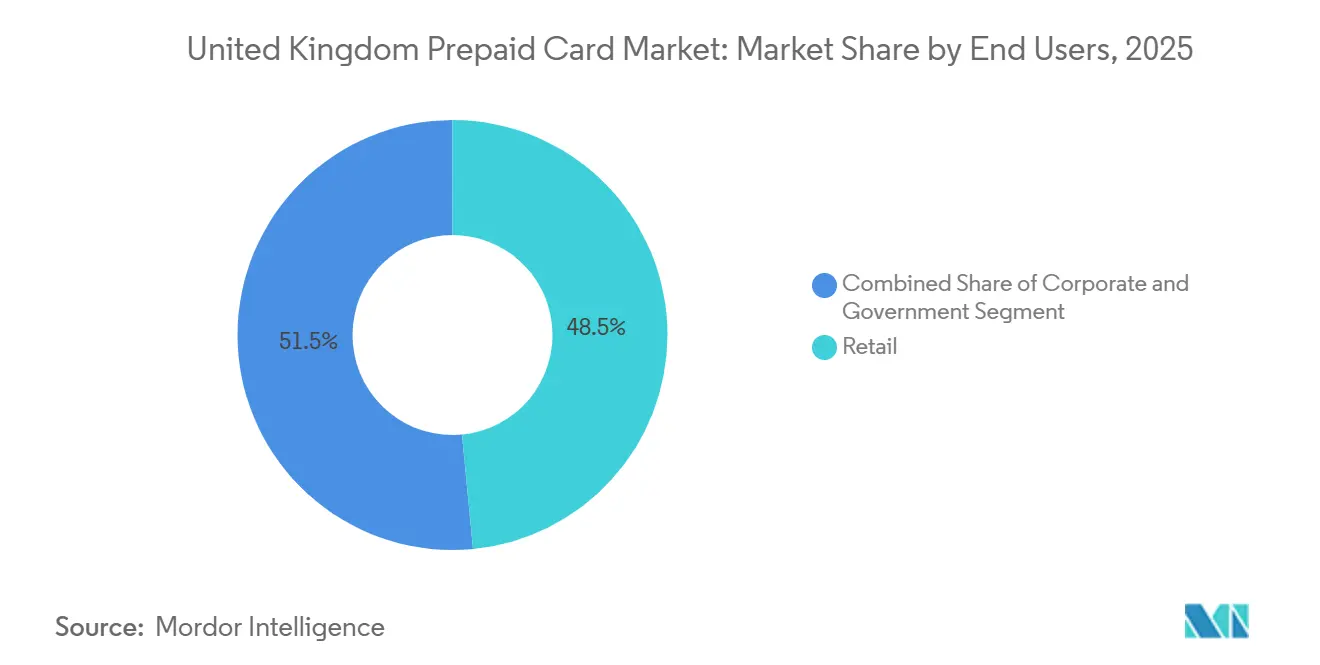

- By end user, retail accounted for 48.48% of the United Kingdom prepaid card market share in 2025, while government channels are projected to grow at an 11.44% CAGR through 2031.

- By geography, England held 82.74% of the United Kingdom prepaid card market share in 2025, and Northern Ireland recorded the highest projected CAGR at 8.84% to 2031.

- Market structure remains moderately fragmented in 2026, with no single issuer group holding a dominant share across consumer, corporate, and public-sector programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Prepaid Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ubiquity of contact-free payments post-COVID-19 | +1.8% | Global | Medium term (2-4 years) |

| Shift of benefits disbursement to prepaid rails | +1.5% | England, Scotland, Wales, with Northern Ireland leading adoption | Long term (≥ 4 years) |

| Open-banking integrations boosting card utility | +1.3% | England, Scotland, and Northern Ireland, Wales | Medium term (2-4 years) |

| E-commerce marketplaces are adopting embedded prepaid wallets | +1.1% | England, Scotland, and early urban Wales | Short term (≤ 2 years) |

| Embedded finance for gig-economy worker payouts | +0.9% | England core, spill-over to Scotland, Wales | Short term (≤ 2 years) |

| ESG-linked prepaid programmes for the under-banked | +0.7% | National, with early gains in England, Wales | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift of Benefits Disbursement to Prepaid Rails

Central and local authorities are expanding prepaid use in disbursing social support and emergency entitlements to improve control and visibility while reducing administrative overhead. England accounts for the majority of program volumes, and councils increasingly rely on e-money issuers that can segment permitted merchant categories and provide near real-time reporting. The Payment Systems Regulator’s authorised push payment reimbursement model, which took effect in October 2024, is shifting liability across sending and receiving institutions and has increased funding flows to victims, which also nudges public bodies to limit exposure through more controlled disbursement instruments. PrePay Technologies, trading as Edenred Payment Solutions, is an FCA-authorized (Financial Conduct Authority authorized) e-money issuer and partners with local authorities and enterprise platforms, which positions it to support high-volume benefit programs that require strong controls.[2]The Payments Association, “Edenred Payment Solutions | Directory,” The Payments Association, thepaymentsassociation.orgAs policy teams prioritize transparency and fraud resilience, the United Kingdom prepaid card market gains from the shift of welfare and emergency support disbursements onto cards that constrain cash withdrawal and restrict merchant categories. The liability split for Authorized Push Payment (APP) fraud and the operational need for programmable rails combine to strengthen the case for prepaid in government workflows over the forecast period. This structural move supports faster growth in the government segment relative to the overall United Kingdom prepaid card market through 2031.

Open-Banking Integrations Boosting Card Utility

Open banking infrastructure is now a core feature of the United Kingdom’s retail payments ecosystem, and widespread deployment of Confirmation of Payee and robust API standards enable faster, safer top-ups into prepaid accounts. Pay.UK reports that Confirmation of Payee is embedded across a broad set of Faster Payments participants, and this has reduced misdirected transfers and supported consumer trust in account-to-account flows that link to prepaid cards.[3]Barclaycard, “Business Essentials Spring 2024,” Barclaycard, barclaycard.co.uk Issuers integrate account information services to give customers a single view of funds and spending, and this improves the utility of prepaid accounts in budgeting and subscription management. Wise highlights multi-currency card usage and continued growth in card revenue, signalling that the interplay of card rails and open banking is deepening engagement. The regulatory framework under PSD2 (Payment Services Directive 2) and FCA oversight ensures third-party providers receive consistent access, which prevents incumbents from limiting integrations that prepaid programs need. As open banking volumes expand and API performance improves, prepaid issuers can orchestrate better onboarding, instant top-ups, and tailored spend controls that raise retention in the United Kingdom prepaid card market.

E-commerce Marketplaces Adopting Embedded Prepaid Wallets

Marketplaces are adopting embedded finance to issue virtual cards that fund seller payouts, buyer refunds, and escrow balances with real-time control and automated reconciliation. Modulr disclosed the acquisition of accounts payable platform Nook in November 2024 to integrate invoice automation with embedded virtual card issuance for B2B clients, and this stack is now available for the United Kingdom businesses that need faster settlement and audit-ready records.[4]Modulr Finance, “Modulr Acquires Accounts Payable Automation Disruptor Nook,” Modulr Finance, modulrfinance.com Edenred Payment Solutions serves program managers who distribute virtual and physical cards for corporate travel, incentives, and expense management, and its United Kingdom team continues to expand product capability for enterprise clients. Partnerships with sector specialists enable single-use virtual cards that reduce fraud risk and speed refund cycles, which can lower support costs for high-velocity merchant platforms. As embedded workflows gain traction among mid-market and enterprise merchants, the United Kingdom prepaid card market captures additional transaction flows that previously sat in bank transfer queues. Program managers capitalize on interchange, FX spreads, and premium service tiers to diversify revenue in the face of capped consumer interchange.

Embedded Finance for Gig-Economy Worker Payouts

Gig platforms and sole traders value instant access to earnings, and prepaid expense cards with automated bookkeeping are filling that need. Tide serves nearly 800,000 members in the United Kingdom and reports strong penetration among small businesses that want real-time expense controls and automated recordkeeping, which supports consistent card usage for operational spend. The Home Office extended Right to Work checks to more working arrangements, including platform-based roles, which increases onboarding costs that prepaid providers embed into their digital KYC flows to streamline activation for workers. Wage growth in accommodation, food service, and caring occupations through 2024 increased payroll complexity for employers, and prepaid payroll cards offer a way to manage cyclical staffing while avoiding some of the fixed costs of legacy payroll infrastructure. Program managers partner with FCA-authorized issuers that can support both e-money accounts and card issuance at scale, which ensures compliance in a fast-changing regulatory environment. As platform work stabilizes at a meaningful share of the workforce, the United Kingdom prepaid card market expands its role as a primary payout mechanism and daily spend tool for these users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening FCA e-money safeguarding rules | -1.2% | National | Short term (≤ 2 years) |

| Growing interchange-fee compression | -0.9% | National | Medium term (2-4 years) |

| Fraud rings exploiting BIN sponsorship gaps | -0.7% | England, Scotland metropolitan | Short term (≤ 2 years) |

| Consumer data privacy backlash on neo-banks | -0.5% | England, Scotland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening FCA E-Money Safeguarding Rules

The FCA intensified scrutiny of e-money safeguarding during 2024 and 2025 and required higher assurance on how customer funds are protected. The United Kingdom e-money firms must hold safeguarded funds in segregated accounts at authorized credit institutions or obtain comparable guarantees from investment-grade sureties, which raises operational complexity and capital costs for smaller providers. Wise reports that it has secured significant safeguarding guarantees, and it notes that prevailing United Kingdom rules restrict the ability to pay interest on e-money balances, which affects competitiveness versus interest-bearing bank accounts. Industry participants have also increased investment in machine learning risk models after enforcement actions underscored AML and sanctions-screening gaps at some institutions. The near-term effect is a shift of capital toward compliance, audits, and legal reserves, which can slow product rollouts and marketing spend in the United Kingdom prepaid card market. Over time, tighter safeguards help stabilize trust, but the transition introduces a drag on growth as firms adapt systems and controls.

Growing Interchange-Fee Compression

Consumer prepaid interchange remains capped at 0.2% for domestic transactions, and scheme programs for government and personal payments reinforce the ceiling across most merchant categories. Barclaycard materials confirm the persistently low consumer prepaid interchange economics, while corporate prepaid maintains different pricing that provides relatively better margins for B2B programs. Issuers are therefore diversifying revenue toward subscription tiers, FX spreads, and interest income where permissible, as disclosed in recent company results. The European Payments Council’s threat report notes the extent of regulatory pressure on card economics in the region, which encourages a focus on volume over value and can discourage investment in advanced fraud defences for low-margin products. This pricing environment weighs on consumer-facing prepaid propositions while strengthening the case for embedded corporate solutions. The overall effect is a medium-term restraint on the United Kingdom prepaid card market while issuers shift their monetization mix.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Institutional Demand Outpaces Consumer Segments

General purpose cards held a 42.38% share by offering in 2025, and government benefit cards are positioned for the fastest growth through 2031 as disbursement programs expand. The shift of public-sector payments toward controlled prepaid rails reflects a desire for transparency and restricted spending categories that help safeguard vulnerable users. Local authorities and program managers partner with FCA-authorized issuers to deliver cards with near real-time reporting, which strengthens case management and compliance. The Payment Systems Regulator’s reimbursement model reinforces the need to manage exposure in direct deposit channels, which indirectly supports program adoption of prepaid instruments for social support. As councils use cards that restrict cash withdrawal and enable monitoring, the United Kingdom prepaid card market gains a steady stream of recurring transactions. PrePay Technologies, which is issued under United Kingdom e-money permissions, supports multiple benefits programs and provides merchant category restrictions that match local authority safeguards.

Gift cards and incentive or payroll cards show steady use in corporate recognition and workforce payouts, where prepaid systems provide better control than traditional wage deposits. Employer programs that limit spend to defined categories and that integrate with HR systems are driving gradual uptake in expense and incentive subsegments. Edenred’s United Kingdom materials show scale across employee benefits, with reward systems that embed cards and vouchers into a unified experience, which keeps spend inside curated merchant networks. Employers and gig platforms favour prepaid when they need near real-time payouts, controls, and simple onboarding for workers who may not qualify for overdrafts. These patterns reinforce the growth of targeted offerings in the United Kingdom prepaid card market as welfare programs and corporate incentives move to programmable rails.

By Card Type: Open-Loop Dominance Fueled by Network Acceptance Yet Closed-Loop Retains Niche Appeal

Open-loop prepaid cards accounted for 59.85% of market share by card type and are set to grow faster than closed-loop alternatives through 2031. Broad merchant acceptance and integration into mobile wallets prop up everyday usage in transit, retail, and travel. Issuer reports point to strong growth in card volumes and revenue, supported by recurring spend at merchants across categories, which is reinforced by robust network tokenization in digital wallets. Pay.UK confirms that Confirmation of Payee has been widely implemented in Faster Payments, which helps secure account-to-account top-ups that feed card balances and daily usage. These conditions underpin a sustained advantage for open-loop programs in the United Kingdom prepaid card market and help drive the open-loop share of the United Kingdom prepaid card market size alongside healthy growth rates into 2031.

Closed-loop and semi-closed systems remain relevant when employers or sponsors need granular control over merchant acceptance or when loyalty economics require spend within a defined network. Program managers use single-use virtual cards to control vendor payments and manage refunds with reduced fraud exposure. Embedded platforms that serve travel, gig economy, and B2B procurement use constrained merchant networks to address security and reconciliation objectives at scale. Corporate programs benefit from different interchange economics than consumer products and can maintain better unit margins in expense or procurement use cases. Open-loop remains the anchor for broad consumer and travel spend, while closed-loop solutions persist where controls and loyalty justify acceptance scope in the United Kingdom prepaid card market.

By End User: Retail Leads on Ubiquity, Government Accelerates on Welfare Modernization

Retail users constitute the largest base of 48.48% of market share, and adoption is tied to contactless ubiquity and mobile wallet usage that put prepaid at the centre of everyday spend. Large issuers report rising card spend across groceries, dining, and e-commerce, which suggests prepaid cards have moved into mainstream checkout choices. Consumer survey data confirms broad wallet use and growing adoption of loadable prepaid cards among adults, including higher use by self-employed people who value expense segregation and better control. As more merchants accept tokenized payments and as wallets integrate budgeting tools, retail spend supports sustained growth in the United Kingdom prepaid card market. The combination of wallet adoption and stronger issuer controls is key to maintaining growth while keeping fraud manageable.

Government use is increasing faster than retail, with a CAGR of 11.44% for the forecast period, driven by the modernization of disbursement models and the need for auditable rails with built-in restrictions. Local authorities are partnering with e-money issuers for benefits programs with near real-time data feeds to safeguarding teams, which shortens reconciliation cycles and strengthens oversight. The PSR’s reimbursement rules raise the cost of misdirected or fraudulent transfers, and this underpins the case for cards that constrain cash-out and merchant types. Corporate adoption is steady in segments where platforms integrate card issuance with accounts payable, expense management, and automated bookkeeping for small businesses. These patterns together keep retail in the lead on absolute share, while government programs outpace aggregate growth in the United Kingdom prepaid card market.

Geography Analysis

England held the largest proportion of activity in 2025, and its dominance reflects population density, fintech clustering, and retail penetration in urban centres. Northern Ireland shows the fastest trajectory on a projected basis due to cross-border payment needs and welfare digitization pilots. Significant adoption of mobile wallets across the country supports prepaid usage in transit and retail, and that extends to England, Scotland, Wales, and Northern Ireland. Issuer disclosures show strong United Kingdom fee income growth during 2024 and 2025, which aligns with high transaction activity in England, while Northern Ireland posts a higher expansion rate into 2031. Security improvements in account-to-account rails through Confirmation of Payee also support the flow of top-ups into prepaid accounts across all four nations.

Scotland and Wales contribute a smaller share but show steady adoption supported by devolved inclusion initiatives and council-led programs. Program managers working with FCA-authorized issuers deploy benefit cards with category controls, which support auditors and safeguarding teams at the local level. Rural connectivity challenges in parts of Scotland can temper the pace of contactless use, but wallet adoption and merchant acceptance broaden each year in metro areas. The PSR’s reimbursement dashboards show material reimbursements for APP scams, which underscores a nationwide need for control enhancements across both sending and receiving institutions. These dynamics point to continued engagement with prepaid as councils and issuers refine models that balance access, protection, and ease of use.

Northern Ireland benefits from proximity to the Republic of Ireland and relies on dual-currency capabilities and strong cross-border acceptance. Multi-currency cards and seamless wallet tokenization provide value to consumers and SMEs that operate on both sides of the border, and issuer disclosures indicate rising card engagement among users with frequent cross-border needs. The technical backbone supports this growth, as Pay.UK and Faster Payments integration with Confirmation of Payee reduces misdirection risk and supports instant funding of prepaid balances. With councils testing benefit card programs and embedded finance gaining traction among marketplaces, the United Kingdom prepaid card market maintains broad geographic relevance. England’s concentration reflects scale, while Northern Ireland’s higher growth reflects policy pilots and cross-border flows that suit prepaid rails.

Competitive Landscape

The competitive field in the United Kingdom prepaid cards market is moderately fragmented, with neo-banks, e-money issuers, embedded-finance platforms, and hybrid providers competing across overlapping customer needs. Revolut’s annual filings show strong growth in UK fee income and total card spend, which demonstrates the leverage of scale across cards, FX, and subscriptions. Wise discloses continued growth in card volumes and revenue, reflecting engagement with multi-currency accounts and the role of cards as a daily spend tool. Starling combines deposit-funded banking with card issuance and its Engine-by-Starling platform, which extends core-banking capabilities to third-party institutions and creates a diversified revenue base. Tide focuses on small business members and supports expense management with prepaid cards, which has resonated among sole traders and small companies that want integrated bookkeeping. These models together define a market where no single issuer captures a majority share of spend across consumer, corporate, and public-sector programs.

Strategic moves in 2025 strengthened positioning across the value chain. Equals Group completed a take-private transaction with a consortium that includes Railsr investors, aligning cross-border capabilities with embedded card issuance to accelerate B2B growth. Paysafe advanced its portfolio optimization by divesting a non-strategic processing unit, which allows resource reallocation to digital wallets and embedded use cases. Modulr acquired Nook to integrate accounts payable automation with embedded payment issuance, and the combined offer supports instant settlement and automated reconciliation for the United Kingdom businesses. Edenred Payment Solutions continued to expand product capability and partnerships in the United Kingdom and Europe, with materials that highlight scale in employer-sponsored benefits and card-based solutions. These moves point to deeper integration of cards into enterprise software and workflow automation.

Risk and compliance investments remained central to strategy. Starling’s disclosure of an FCA penalty for historical AML and sanctions-screening issues was accompanied by expanded investment in risk controls and system upgrades across onboarding and transaction monitoring. Wise described remediation following a United States multi-state examination of its money services subsidiary and affirmed that it is on track with the program, which underscores how cross-border models face multi-jurisdiction oversight. Revolut’s disclosures on fraud prevention emphasize defence-in-depth, and its banking license in mobilization signals a strategy to broaden product scope in the United Kingdom as operations mature. Program managers and issuers are deploying Confirmation of Payee and strong authentication methods in top-up flows, which should reduce errors and accelerate funding. The net result is a market characterized by rapid product innovation tempered by rigorous compliance, which supports the resilience of the United Kingdom prepaid card market.

United Kingdom Prepaid Card Industry Leaders

Revolut Ltd

PrePay Technologies (PPS)

Barclaycard

Edenred UK

Wise Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Tide Platform Ltd secured a strategic investment exceeding USD 120 million led by TPG’s The Rise Funds, with support from existing investor Apax Digital Funds, achieving a USD 1.5 billion valuation, to accelerate expansion and product development for small businesses in the United Kingdom and Europe.

- November 2025: Wise plc agreed to pay a USD 4.2 million penalty as part of a consent order following a routine examination conducted between July 2022 and September 2023 by the Multi-State MSB Examination Taskforce of Wise US, Inc., and confirmed it is on track with remediation.

- April 2025: Equals Group Plc was acquired in a USD 381.80 million (GBP 283 million) all-cash deal by a consortium backed by TowerBrook Capital Partners, J.C. Flowers & Co., and Railsr shareholders. Effective April 2025, the merger integrates Equals' cross-border payments and card issuing with Railsr's embedded finance platform.

- March 2025: Edenred Payment Solutions launched a new product utilizing virtual cards to transform insurance payouts by enabling instant digital disbursements and enhancing security for policyholders across the United Kingdom and Europe.

United Kingdom Prepaid Card Market Report Scope

A prepaid card can be used to make purchases across a physical or online store. A prepaid card is purchased as a card with funds pre-loaded on it. The card can then be used to make purchases up to that amount. A prepaid card is sometimes known as a stored-value card or a prepaid debit card. This report aims to provide a detailed analysis of the UK Prepaid Cards Market. It focuses on the market dynamics, emerging trends in the segments, the future of markets, and insights into various drivers and restraints. Also, it analyzes the key players and the competitive landscape in the market.

The United Kingdom Prepaid Card Market Report is Segmented by Offering (General Purpose Cards, Gift Cards, Government Benefit Cards, Incentive/Payroll Cards, Other Offerings), Card Type (Closed-Loop Cards, Open-Loop Cards), End User (Retail, Corporate, Government), and Geography (England, Scotland, Wales, Northern Ireland). The Market Forecasts are Provided in Terms of Value (USD).

| General Purpose Cards |

| Gift Cards |

| Government Benefit Cards |

| Incentive/Payroll Cards |

| Other Offerings |

| Closed-Loop Cards |

| Open-Loop Cards |

| Retail |

| Corporate |

| Government |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Offering | General Purpose Cards |

| Gift Cards | |

| Government Benefit Cards | |

| Incentive/Payroll Cards | |

| Other Offerings | |

| By Card Type | Closed-Loop Cards |

| Open-Loop Cards | |

| By End User | Retail |

| Corporate | |

| Government | |

| By Geography | England |

| Scotland | |

| Wales | |

| Northern Ireland |

Key Questions Answered in the Report

What is the current size and growth outlook of the United Kingdom prepaid card market?

The United Kingdom prepaid card market size is USD 63.46 billion in 2026 and is projected to reach USD 96.74 billion by 2031 at an 8.74% CAGR, supported by strong wallet adoption and issuer investments in fraud controls.

Which segments are leading and growing fastest within the United Kingdom prepaid card market?

General-purpose cards lead by offering and government benefit cards grow fastest, open-loop dominates by card type with higher growth than closed-loop, retail leads by end user, while government grows fastest, and England leads by geography, while Northern Ireland posts the highest projected CAGR.

How are regulations shaping the United Kingdom prepaid card market in 2026?

The PSR’s APP reimbursement model and tighter FCA safeguarding rules increase compliance and liability requirements, prompting issuers to invest in controls and program design that favour structured disbursement and secure top-up flows.

Why are open-loop prepaid cards gaining share in the United Kingdom prepaid card market?

Open-loop cards benefit from network acceptance, mobile wallet tokenization, and secure account-to-account top-ups enabled by Confirmation of Payee, which together expand everyday use in retail and travel.

What is driving government adoption of prepaid solutions in the United Kingdom prepaid card market?

Government bodies favour programmable controls, faster reconciliation, and better fraud mitigation for welfare support and emergency disbursements, which improves oversight and claimant experience compared with direct deposits.

How are fraud and safeguarding trends influencing the United Kingdom prepaid card market?

Rising misuse-of-facility cases and APP scam risks push issuers to enhance monitoring and authentication, while FCA safeguarding requirements raise operational standards industry-wide.

Page last updated on: