United Kingdom Hedge Funds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

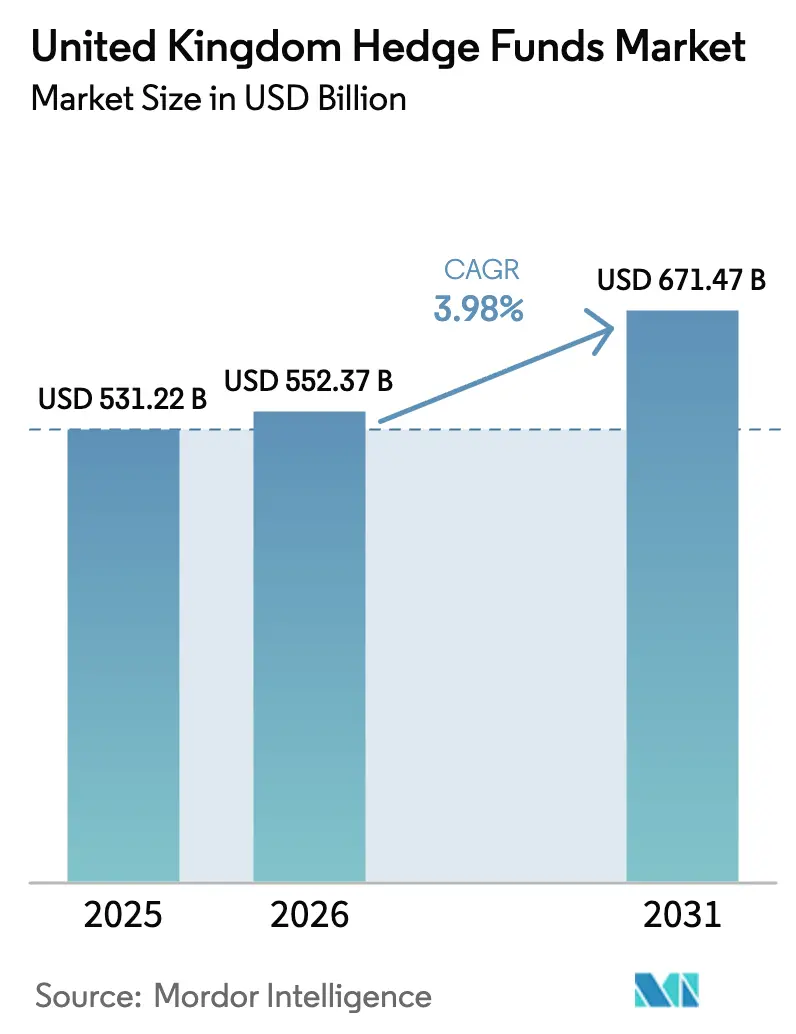

| Base Year Market Size (2025) | USD 531.22 Billion |

| Market Size (2026) | USD 552.37 Billion |

| Market Size (2031) | USD 671.47 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

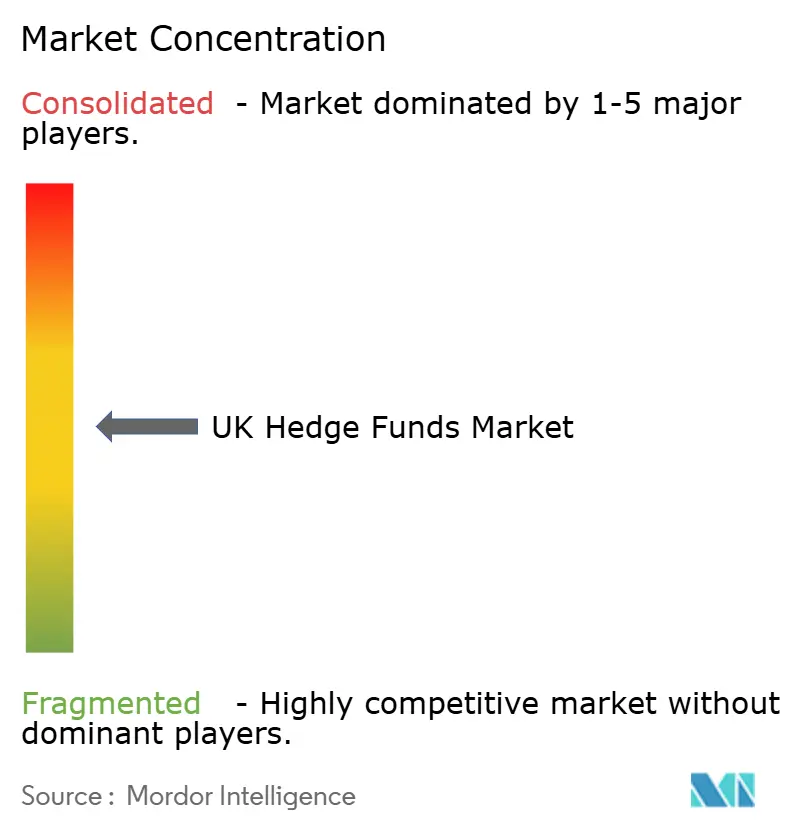

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Hedge Funds Market Analysis by Mordor Intelligence

The United Kingdom hedge fund market size was valued at USD 531.22 billion in 2025 and estimated to grow from USD 552.37 billion in 2026 to reach USD 671.47 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). London’s post-Brexit resilience, a decisive regulatory push toward cross-border harmonization, and the continued reallocation of pension assets away from leveraged LDI mandates are the prime engines of this expansion. Institutions are directing fresh capital toward systematic and ESG-labelled strategies while daily-dealing UCITS vehicles broaden the regional investor base and lower perceived liquidity risk. Technology spending on alternative data, cloud-native execution, and low-latency connectivity is redefining competitive advantage, allowing managers to harvest alpha from volatile macro conditions. However, higher compliance costs, talent drift to US funds, and lingering uncertainty over EU passporting remain headwinds; a pro-growth stance from HM Treasury and the FCA keeps the United Kingdom hedge fund market on a firm upward trajectory.

Key Report Takeaways

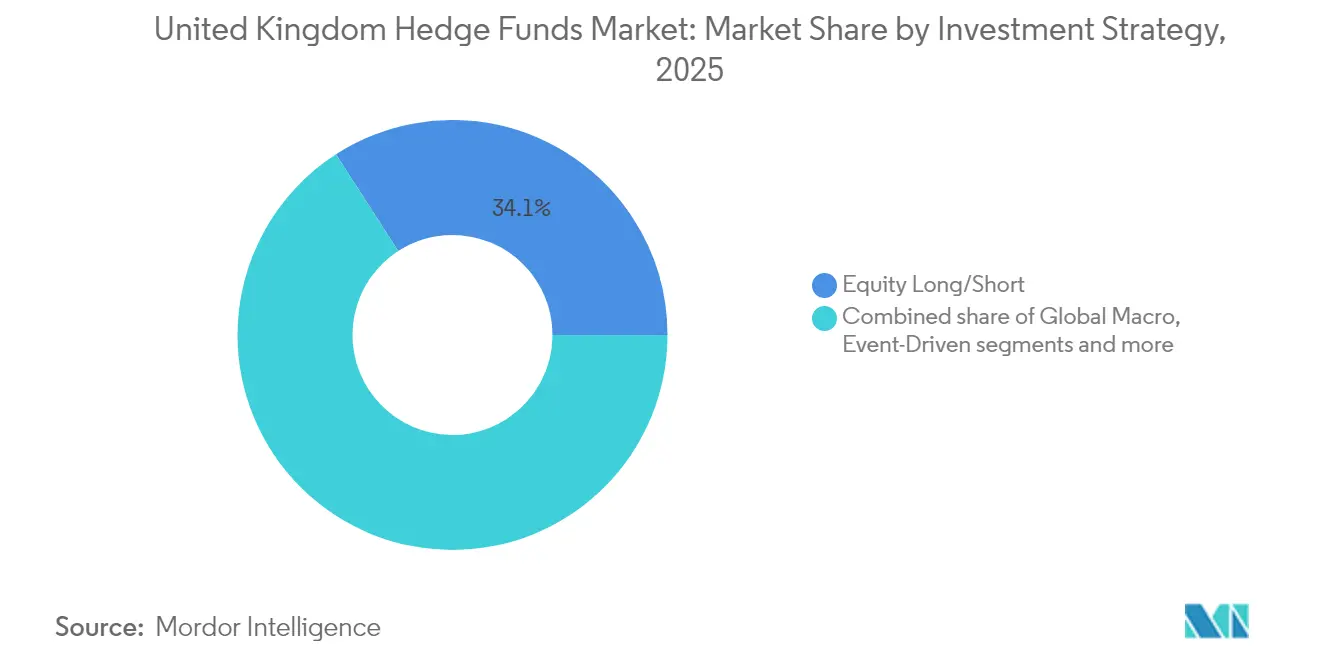

- By investment strategy, equity long/short led with 34.12% of the United Kingdom hedge fund market share in 2025, while the global macro is projected to post the fastest 6.22% CAGR through 2031.

- By investor type, pension funds held 56.25% of the United Kingdom hedge fund market share in 2025; family offices are expected to advance at a 6.78% CAGR to 2031.

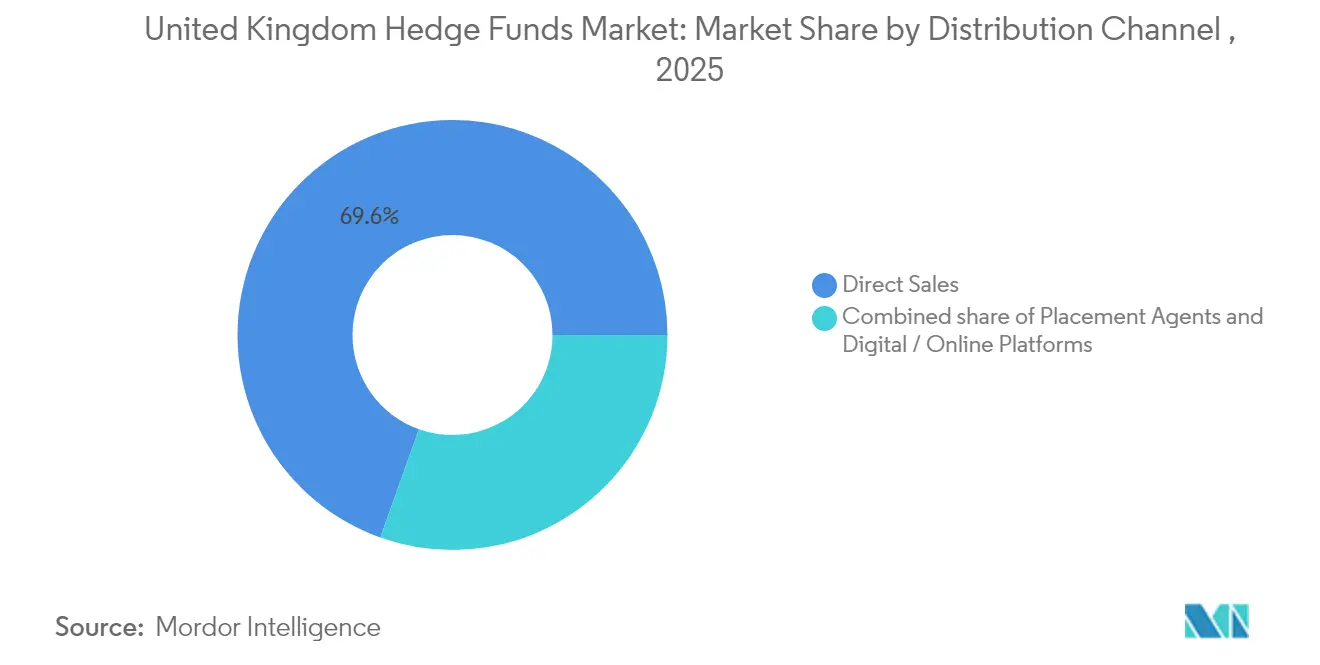

- By distribution channel, direct sales commanded 69.55% of the United Kingdom hedge fund market size in 2025, whereas digital/online platforms are set to grow at a 5.15% CAGR.

- By fund domicile & structure, UK-onshore funds accounted for a 45.32% share of the United Kingdom hedge fund market size in 2025, and UCITS-compliant hedge funds are forecast to expand at a 4.55% CAGR.

- By investment location, London captured a 37.15% share of the United Kingdom hedge fund market in 2025 and is also the fastest-growing center at 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Hedge Funds Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UK pension schemes’ post-LDI shift to alternatives | +1.2% | UK, Channel Islands | Medium term (2-4 years) |

| Rise of UCITS/AIFMD-compliant hedge-fund structures | +0.8% | UK and EU | Long term (≥ 4 years) |

| ESG-driven capital inflows into sustainable strategies | +0.6% | Global, London-centric | Medium term (2-4 years) |

| Volatility-rich macro environment unlocking alpha | +0.7% | Global | Short term (≤ 2 years) |

| London’s quant-talent magnetism | +0.4% | London | Long term (≥ 4 years) |

| Adoption of alternative-data & cloud-native execution tech | +0.5% | UK-wide, London-focused | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

UK Pension Schemes’ post-LDI Shift to Alternatives

The gilt-market shock of 2022 exposed leverage vulnerabilities in LDI portfolios, triggering a structural rethink among trustees. Defined-benefit schemes have raised alternative allocations from 14% to 39% of risky assets, and hedge-fund exposure now stands near 6% of total scheme assets, up from zero at the start of the millennium[1]William Schomberg, “UK pension schemes boost hedge-fund exposure after LDI crisis,” Reuters, reuters.com. An estimated USD 254 billion in redeployed assets is expected to filter into hedge funds before 2030. Added oversight from the pensions regulator and stricter leverage caps on LDI mandates create durable tailwinds for uncorrelated strategies. Managers able to package downside-risk mitigation and liquidity management are best placed to win these mandates.

Rise of UCITS/AIFMD-compliant hedge-fund structures

Since the Overseas Funds Regime launched in September 2024, 47 new UCITS hedge funds have debuted, marking a 34% increase from 2023, and have drawn in USD 19.05 billion from European investors[2]KPMG, “Overseas Funds Regime opens door for EEA UCITS in the UK,” kpmg.com. This growth highlights the increasing appeal of UCITS wrappers as the primary passport for European distribution. Insurers and wealth managers eager for hedge-fund-style returns within a retail framework are drawn to UCITS wrappers. These wrappers provide liquidity and daily NAV reporting and enforce strict risk-diversification rules, making them a preferred choice for institutional and retail investors alike. While the AIFMD delegation rules pose challenges, UCITS vehicles present a scalable solution, allowing London-based portfolio management to align with EU marketing regulations. This adaptability ensures that UCITS funds remain a competitive and compliant option for cross-border distribution in Europe.

ESG-driven capital inflows into sustainable strategies

Starting in July 2024, the FCA's Sustainability Disclosure Requirements rolled out four distinct labels alongside a stringent anti-greenwashing clause. These measures aim to enhance transparency and accountability in sustainable investments. With clearer compliance guidelines, sustainable hedge-fund assets surged 23% year-over-year, reaching USD 113.03 billion[3]ICAEW, “FCA Sustainability Disclosure Requirements: what asset managers need to know,” icaew.com. This growth reflects increased investor confidence and reduced hesitation in adopting sustainable strategies. Family offices led the charge, with 43% increasing their allocations in 2024, showcasing their proactive approach to sustainability. Managers funneled USD 2.92 billion into climate-data feeds, transition-risk models, and stewardship resources, significantly raising the stakes for new entrants by creating higher entry barriers. Systematic platforms that can adeptly harness detailed ESG datasets are reaping the benefits of their early-mover status, positioning themselves as leaders in the evolving sustainable investment landscape.

Volatility-rich macro environment unlocking alpha.

Cross-asset volatility hit post-2008 highs in 2024, fuelled by rate-path bifurcation, commodity supply shocks, and geopolitical cross-currents. UK-based macro funds returned 18.7% on average, outpacing the broader hedge-fund composite by nearly 1,000 basis points. Discretionary specialists exploited interest-rate convexity in Gilts and short-duration EU sovereigns, while systematic trend followers captured extended currency and commodity moves. London’s time zone straddles between US and Asian sessions, combined with dense liquidity and multi-dealer connectivity, enables rapid risk deployment.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory uncertainty on EU passporting post-Brexit | −0.9% | UK-EU | Long term (≥ 4 years) |

| HMRC tightening on performance-fee & carried-interest tax | −0.6% | UK | Medium term (2-4 years) |

| Compensation-led talent migration to US funds | −0.4% | London-centric | Short term (≤ 2 years) |

| Rising ODD & cyber-security compliance costs | −0.3% | UK-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory uncertainty on EU passporting post-Brexit

Due to the lack of comprehensive equivalence, the EU investor base has contracted by roughly 35%. It has compelled managers to navigate private placement filings across all 27 member states, significantly increasing the complexity of compliance processes. Stricter reporting and delegation clauses under AIFMD II, set to take effect in April 2024, have led to a surge in legal fees and operational costs, rising by as much as 60%. These changes have placed additional pressure on mid-tier firms, many of which lack the scale to absorb such costs. As a result, several firms have shifted their trading and compliance functions to Dublin or Luxembourg, undermining London’s traditional clustering advantage and reducing its role as a central hub. Furthermore, as clarity on these regulations remains elusive, the incentive for new fund launches to establish themselves within the EU bloc continues to grow, driven by the need to ensure smoother access to the European investor market.

HMRC tightening on performance fee and carried-interest tax

In 2024, close to 10,000 high-net-worth individuals exited the United Kingdom, driven by retrospective investigations into disguised remuneration schemes and the Labour Party's indications of tightening non-dom exemptions. These measures have created significant uncertainty for wealthy individuals and professionals in the financial sector. The HMRC has issued retrospective tax bills to over 200 hedge-fund professionals, depleting partnership capital through substantial back payments and penalties. Additionally, proposals to treat carried interest as ordinary income could raise the effective tax rate to 45%, prompting some portfolio managers to explore relocation options in Switzerland and Singapore, which offer more favorable tax regimes. The rising costs of advisory services, particularly for compliance and tax planning, are placing a disproportionate burden on emerging managers. This financial strain is accelerating consolidation within the industry as smaller players struggle to compete with larger, more established firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Investment Strategy: Systematic approaches drive the alpha generation

Equity long-short strategies captured 34.12% of the United Kingdom hedge fund market in 2025, driven by improved factor-decomposition tools and real-time risk dashboards that refine gross and net exposure limits. Managers exploit single-stock dispersion, which widened as retail flows and thematic rotations heightened idiosyncratic volatility. Global Macro, though smaller today, is projected to expand at a 6.22% CAGR, buoyed by central-bank divergence that creates persistent currency and rates trades. Event-driven books revived alongside a 38% pick-up in United Kingdom-listed M&A announcements, while Relative-Value desks profit from widening credit-curve kinks as quantitative tightening drains primary-dealer balance sheets.

Multi-strategy giants such as Citadel and Millennium allocate incremental capital dynamically across these sleeves, using risk-budgeting engines that optimize marginal Sharpe contribution. The United Kingdom hedge fund market size tied to quantitative signals keeps rising as systematic funds represent 60% of recent launches, integrating alternative datasets on supply chains, satellite imagery, and consumer web traffic. Managers spent USD 1.50 billion in 2024 on data curation, feature engineering, and GPU clusters. London’s deep pool of PhDs fuels machine-learning adoption, and Man Group’s rebuilt Condor platform showcases the direction of travel with real-time data ingestion and reinforced model governance.

By Investor Type: Family offices accelerate alternative allocations

Pension funds controlled 56.25% of the United Kingdom hedge fund market in 2025 as stricter funding ratio targets compelled trustees to diversify beyond traditional 60/40 mixes. The shift away from leveraged LDI structures following gilt turmoil anchors stable long-term capital for hedge-fund managers. Family offices, though smaller in absolute terms, are growing at 6.78% CAGR as multi-generational wealth transfer aligns with direct relationships and bespoke mandates. Insurers remain steady allocators, targeting capital-efficient strategies compatible with Solvency II.

Sovereign wealth funds have opened London offices to secure deal flow and co-investment rights, enhancing the prestige of the United Kingdom hedge fund market. Digital onboarding portals reduce operational friction, letting smaller institutions and charities allocate with lower minimums. Funds-of-funds face fee compression as allocators opt for direct exposure and co-investment, forcing them to pivot toward operational due diligence services. Family offices’ appetite for ESG-aligned systematic products boosts seeding opportunities for niche managers, fostering a vibrant start-up pipeline.

By Distribution Channel: Digital transformation reshapes access

In 2025, direct sales commanded a dominant 69.55% share of the United Kingdom's hedge fund market, highlighting the deep-rooted ties in institutional capital-raising. Chief Investment Officers (CIOs) and trustees continue to value in-person meetings and tailored reporting when bestowing multi-million-pound mandates. These face-to-face interactions and customized solutions remain critical in building trust and ensuring alignment with institutional objectives. However, digital platforms are on the rise, boasting a 5.15% CAGR due to streamlined KYC modules that have slashed onboarding durations from weeks to mere days. This shift reflects the growing demand for efficiency and technological integration in the capital-raising process.

Placement agents are evolving, focusing on ESG verification, cybersecurity diligence, and navigating regulatory nuances for cross-border marketing. These agents are increasingly seen as vital intermediaries, helping funds meet stringent compliance requirements while addressing investor concerns about sustainability and security. Leveraging AI, matching engines analyze style-factor exposures and volatility profiles, ensuring investor preferences align seamlessly with fund offerings, thus enhancing visibility for smaller managers. This technology-driven approach improves fund discovery and levels the playing field for emerging managers seeking to attract institutional capital. The shift to virtual operational due diligence, a trend solidified by the pandemic, has diminished geographic barriers. This normalization of virtual processes has enabled allocators to evaluate funds more efficiently, regardless of location. As a result, the United Kingdom hedge fund market is reaping the benefits of a wider allocator base, all while keeping travel expenses in check and fostering a more inclusive investment landscape.

By Fund Domicile & Structure: Regulatory arbitrage drives optimization

In 2025, UK-onshore funds secured a 45.32% market share, as domestic pension trustees leaned towards familiar oversight and sterling share classes. This preference stems from the perceived stability and regulatory familiarity offered by onshore funds, which align with the operational and compliance needs of pension trustees. The FCA, with its tailored AIFMD adjustments, lightened Annex IV reporting and introduced risk-based supervisory tiers. These moves aim to reduce cost burdens, making onshore options more appealing compared to their offshore counterparts. Offshore vehicles, such as those in the Channel Islands and Cayman Islands, continue to cater to end investors seeking tax neutrality. However, these vehicles face challenges from increased operational overheads driven by heightened transparency mandates, which add complexity to their management.

Since Brexit, assets totaling USD 56.54 billion have shifted to Ireland and Luxembourg, ensuring continued EU marketing flexibility. UCITS-compliant funds, growing at a brisk 4.55% CAGR, provide daily liquidity within a risk-diversified framework, making them a favorite for wealth-management platforms. 2024 saw the introduction of Long-Term Asset Funds (LTAFs), designed for illiquid strategies like private credit, tapping into new inflows from defined-contribution pensions. This structural diversity empowers the United Kingdom hedge fund market to navigate varied liquidity horizons and regulatory landscapes, all while retaining portfolio management in London.

Geography Analysis

London remains the undisputed nucleus of the United Kingdom hedge fund market, boasting a 37.15% share in 2025 and a projected 5.12% CAGR. The abolition of bonus caps in 2024, paired with a spike in foreign direct investment, solidified its edge over New York and Hong Kong for cross-asset liquidity and human capital. Large banks escalated compensation bands for quants and execution traders, reinforcing the city’s talent gravity. Cloud-native execution, co-located data centers, and low-latency fiber routes to US and EU markets keep trading costs competitive. The FCA’s early adoption of sustainability disclosure rules further differentiates London from ESG-committed allocators.

South-East England operates as a strategic extension, absorbing cost-sensitive functions while maintaining proximity to counterparties. The corridor from Reading to Brighton hosts cybersecurity operations, fund-administration hubs, and data-archiving centers. Improved rail and fiber connectivity means portfolio managers can run real-time risk oversight from satellite offices without compromising execution quality. The region’s business-park ecosystems also appeal to start-ups rolling out AI-driven analytics and liquidity-sourcing tools for the broader United Kingdom hedge fund market.

Scotland and North-West England contribute niche specializations that diversify the geographic footprint. Edinburgh’s fintech sandbox accelerates regulatory-technology pilots, while Glasgow’s university partnerships funnel data science graduates into systematic trading teams. Manchester focuses on trade reconciliation and compliance analytics, leveraging lower operating costs and solid STEM talent. Although investment decision-making gravitates to London, regional hubs mitigate operational risk concentration and cultivate local expertise, reinforcing the resilience of the United Kingdom hedge fund industry.

Competitive Landscape

In the United Kingdom hedge fund market, the top 20 managers control nearly half of the assets under management (AUM), indicating moderate market concentration. These multi-strategy behemoths leverage platform economics, centralized risk management, a shared research infrastructure, and scale-driven fee reductions to draw in trading pods. Their ability to operate at scale allows them to negotiate favorable terms and maintain a competitive edge. With their substantial financial resources, they gain priority access to premium data feeds and cutting-edge execution venues, which are critical for maintaining operational efficiency. This competitive advantage forces mid-sized peers to focus on high-conviction, specialized niches to differentiate themselves in the market.

Technology defines the competitive frontier. Man Group invested USD 125.6 million in upgrading its Condor platform to integrate machine-learning libraries, real-time order-book analytics, and automated model-governance checks. US titans Citadel, Millennium, and Point72 ramped London headcount, inflating pay packets to record levels and triggering a compensation spiral that squeezes smaller boutiques. ESG-compliant systematic strategies represent lucrative white space, but the data and governance spend required to win the FCA’s sustainability label limits entrant numbers.

Distribution is also in flux. Fintech marketplaces match allocators to managers by factor footprint and liquidity tolerance, shaving intermediary fees. Placement agents shift toward advisory on cyber-resilience and operational due diligence to sustain relevance. Heightened FCA oversight on valuation, conflicts of interest, and side-pocket governance adds compliance layers that favor well-capitalized houses. Consequently, emerging managers pursue seeding deals with family offices to attain critical mass, ensuring the United Kingdom hedge fund market sustains entrepreneurial churn despite scale pressures.

United Kingdom Hedge Funds Industry Leaders

Man Group plc

Marshall Wace LLP

Citadel Europe LLP

Millennium Capital Partners LLP

Brevan Howard Asset Management LLP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Jane Street reported a record USD 20.5 billion trading revenue for 2024, eclipsing several investment-bank FICC desks and underscoring the profitability of ETF market-making and systematic arbitrage.

- April 2025: HM Treasury opened a consultation on a tiered AIFMD framework linked to net asset value, pledging lighter reporting for sub-USD 1.25 billion funds.

- March 2025: Lumyna Partners teamed with Marshall Wace to launch a global equity long/short UCITS fund, expanding Marshall Wace’s retail footprint.

- February 2025: Man Group posted USD 1.3 billion Q4 2024 net inflows, driven by demand for long-only systematic mandates.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom hedge fund market as all assets under management (AUM) held in UK-domiciled or UK-managed hedge fund vehicles that pursue absolute-return strategies across equities, fixed income, currencies, and multi-asset mandates.

Scope exclusion note: Performance fees, management company revenues, and offshore pools with no UK portfolio management presence are not counted.

Segmentation Overview

- By Investment Strategy

- Equity Long/Short

- Global Macro

- Event-Driven

- Relative Value / Arbitrage

- Quantitative / Systematic

- Multi-Strategy

- Credit / Fixed-Income

- By Investor Type

- Pension Funds

- Insurance Companies

- Sovereign Wealth Funds

- Family Offices

- High-Net-Worth Individuals

- Funds of Funds

- By Distribution Channel

- Direct Sales

- Placement Agents / Intermediaries

- Digital / Online Platforms

- By Fund Domicile & Structure

- UK-Onshore (Ltd / LLP / AIF)

- Offshore (Channel Islands, Cayman)

- EU Onshore (Ireland, Luxembourg)

- UCITS-Compliant Hedge Funds

- By Region

- London

- South East England

- Scotland

- North West England

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed portfolio managers, prime broker personnel, and pension trustees across London, Edinburgh, and Jersey. Conversations tested preliminary growth drivers (post-LDI reallocations, UCITS launches) and supplied strategy-level asset splits that public data lack, which we then reconciled with the secondary findings.

Desk Research

We began by mapping the investable universe through public filings at the Financial Conduct Authority, quarterly Bank of England fund statistics, and HMRC Stamp Duty data. Additional color came from trade bodies such as the Alternative Investment Management Association, academic journals in the SSRN Hedge Fund series, and open datasets from the Bank for International Settlements. To profile capital flows, we tapped paid resources, D&B Hoovers for manager financials and Dow Jones Factiva for deal news. These sources establish baseline AUM and strategy distribution, yet the list is illustrative rather than exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction of industry AUM starts with FCA-reported fund assets, which are then adjusted for double counting of umbrella structures and reconciled with custodian asset aggregates. Select bottom-up checkpoints, sampled manager AUM roll-ups and average ticket size × fund count, guard against overstatement. Key variables include gilts-to-alternatives allocation ratios, new UCITS launches, average prime broker leverage, regulatory capital shifts, and ESG label inflows. Forecasts to 2030 rest on a multivariate regression that links these drivers to historical AUM growth, with scenario analysis layering macro volatility ranges discussed with interviewees. Gaps in underlying data (for example, undisclosed managed account assets) are bridged by applying transparency discounts derived from our primary interviews.

Data Validation & Update Cycle

Outputs pass variance checks against Bank of England flow-of-funds tables and HFR strategy indices. Senior reviewers sign off after anomaly resolution. We refresh models each year and trigger interim updates when material events, rule changes or market dislocations, arise, ensuring clients always receive our latest view.

Why Mordor's UK Hedge Funds Baseline Commands Reliability

Published estimates often diverge because firms mix revenue measures, offshore pools, or unverified leverage assumptions.

Key gap drivers include some studies that track fee income rather than AUM, others that fold in non-UK master funds, and a few that extrapolate growth from global trends without cleansing double-counted sub-funds. Mordor's disciplined scope, annual refresh, and dual-track validation minimize these distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 531.22 B (2025) | Mordor Intelligence | - |

| USD 1.21 T (2024) | Global Consultancy A | Includes offshore vehicles lacking UK management; no double-count adjustment |

| GBP 250 B (2025) | Industry Association B | Converts reported AUM to sterling but omits leverage offsets |

| USD 10.29 B (2024) | Trade Journal C | Tracks management company fee revenue, not client assets |

These comparisons show that when variables and scope shift, totals swing widely. Our approach grounds every figure in transparent FCA filings, corroborated interviews, and repeatable adjustments, giving decision-makers a balanced, dependable baseline.

Key Questions Answered in the Report

What CAGR is the United Kingdom hedge fund market expected to post through 2031?

The market is projected to register a 3.98% CAGR, rising from USD 531.22 billion in 2025 to USD 671.47 billion by 2031.

Which investor group currently allocates the largest share to hedge funds in the United Kingdom?

Pension funds hold 56.25% of assets, reflecting post-LDI diversification toward alternatives.

Why are UCITS structures important for United Kingdom hedge-fund managers after Brexit?

UCITS wrappers provide a recognized EU passport, enabling United Kingdom managers to distribute daily liquidity hedge-fund strategies across Europe despite the loss of full passporting rights.

How is ESG regulation shaping product development?

The FCA’s Sustainability Disclosure Requirements prompted a 23% jump in sustainable hedge-fund assets and forced managers to invest heavily in ESG data and verification frameworks.

What technological investments differentiate leading United Kingdom hedge-fund firms?

Spending on alternative data, GPU-accelerated machine-learning platforms, and cloud-native execution systems underpin alpha generation and operational scalability for top managers.

Has Brexit led to a mass relocation of hedge-fund activity out of London?

While some mid-tier firms opened EU subsidiaries, London still commands 37.15% domestic share and continues to attract foreign direct investment, anchored by talent depth and market access.

Page last updated on: