Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

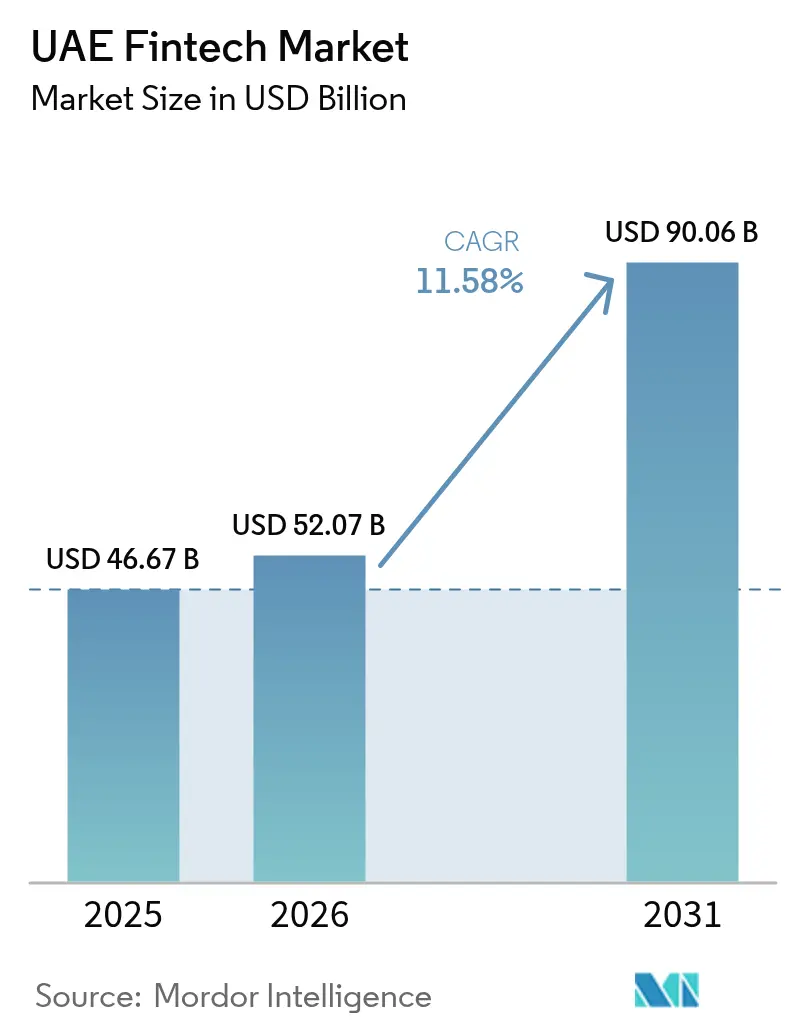

| Base Year Market Size (2025) | USD 46.67 Billion |

| Market Size (2026) | USD 52.07 Billion |

| Market Size (2031) | USD 90.06 Billion |

| Growth Rate (2026 - 2031) | 11.58% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Fintech Market Analysis by Mordor Intelligence

UAE fintech market size in 2026 is estimated at USD 52.07 billion, growing from 2025 value of USD 46.67 billion with 2031 projections showing USD 90.06 billion, growing at 11.58% CAGR over 2026-2031. This growth reflects sustained public-private investment, rising digital wallet use, and progressive open-finance regulations that reinforce the UAE’s position as the dominant fintech hub in the Middle East. Smartphone penetration above 96% has accelerated mobile-first payment adoption, while the Central Bank’s Financial Infrastructure Transformation (FIT) program and the Digital Dirham project are reshaping wholesale and retail settlement rails. Strategic capital from sovereign wealth funds is deepening the venture pipeline, and the multiplicity of common-law financial free zones enables firms to choose optimal regulatory pathways. Competitive intensity is also rising as incumbent banks form technology partnerships to safeguard deposits and fee income against agile newcomers.

Key Report Takeaways

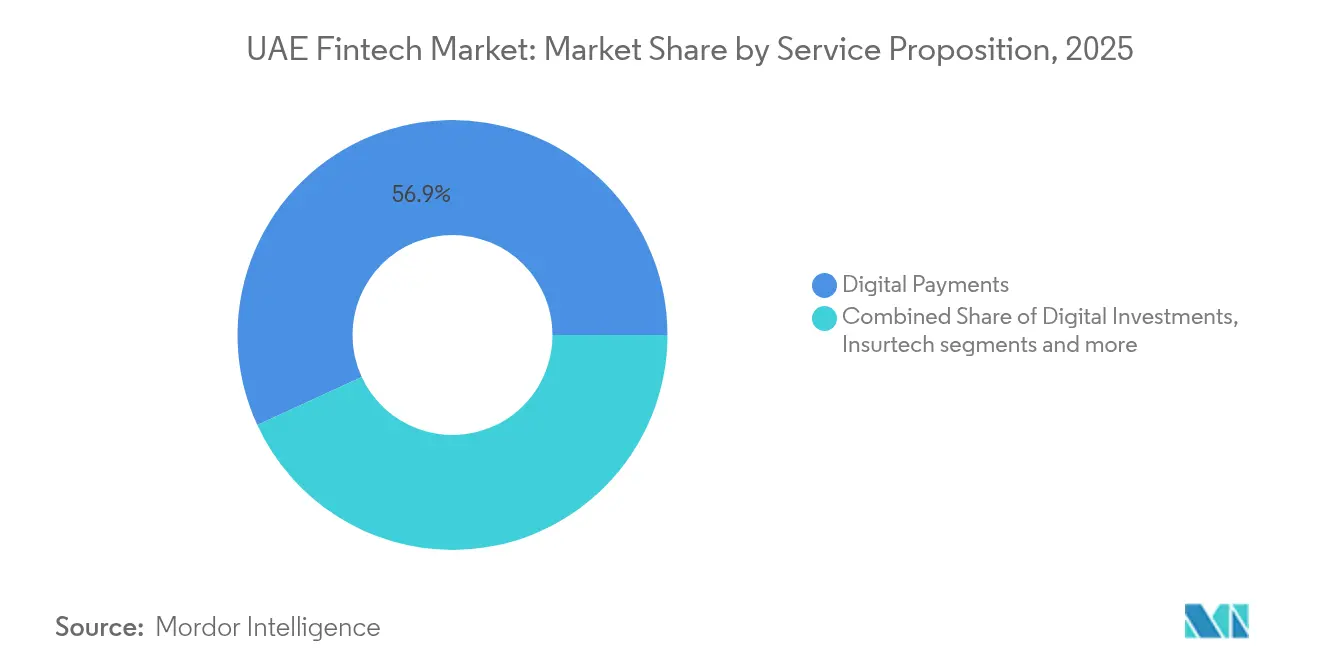

- By service proposition, digital payments commanded 56.88% of UAE fintech market share in 2025, while insurtech is advancing at a 13.91% CAGR to 2031.

- By end-user, retail consumers represented 60.02% of UAE fintech market size in 2025; the business segment is expanding at a 12.85% CAGR through 2031.

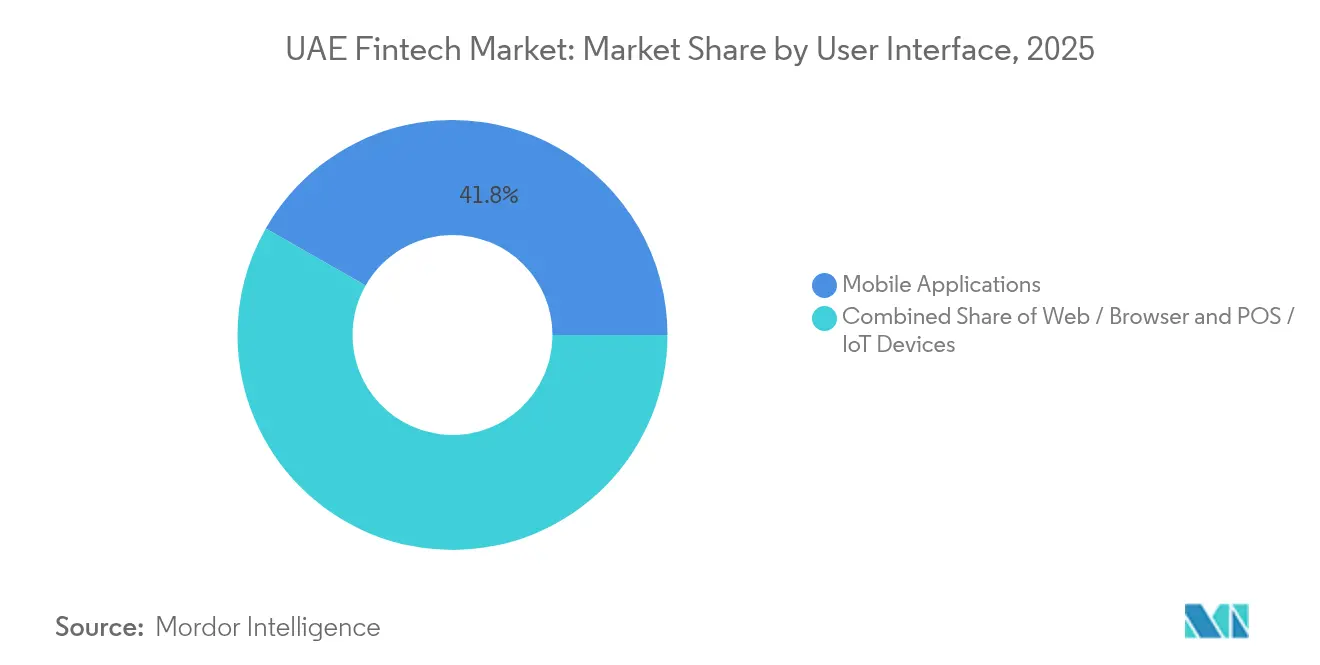

- By user interface, mobile applications held 41.75% share of UAE fintech market size in 2025, whereas web browsers are projected to grow at 14.2% CAGR to 2031.

- By Emirate, Dubai led with 59.68% UAE fintech market share in 2025; Abu Dhabi shows the highest CAGR at 13.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Fintech Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Venture-capital inflows | +2.8% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| 96% smartphone penetration | +2.1% | National | Short term (≤ 2 years) |

| ESG-linked Islamic fintech | +1.4% | National & GCC | Long term (≥ 4 years) |

| AI & blockchain adoption | +1.9% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Regulatory sandboxes | +1.6% | DIFC, ADGM | Long term (≥ 4 years) |

| Bank-fintech collaboration | +1.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Venture-Capital Inflows Accelerate Ecosystem Expansion

Record 2024 funding rounds such as Qashio’s USD 19.8 million Series A and Fortis’s USD 20 million raise underscore growing institutional confidence in the UAE fintech market[1]Central Bank of the UAE, “Open Finance Regulation,” rulebook.centralbank.ae. Sovereign wealth funds, including Mubadala and ADQ, have begun supporting early-stage deals to reinforce local intellectual property creation. Access to patient capital shortens go-to-market cycles and enables rapid regional rollout of payment corridors linking Asia, Africa, and Europe. Deeper pools of growth equity are also allowing scale-ups to pursue strategic buy-and-build plays that widen product portfolios and lift switching costs for corporate clients. The resulting flywheel is expected to sustain double-digit expansion even as global venture activity moderates.

Smartphone Penetration Drives Mobile-First Finance

With 96% of residents owning smart devices, mobile banking adoption surpassed 83% in 2025, and 69% of users favor digital wallets over cards[2]Central Bank of the UAE, “Open Finance Regulation,” rulebook.centralbank.ae. Frictionless onboarding, biometric log-ins, and QR payments have become baseline expectations, compelling providers to continuously iterate user-experience design. Riding on this established infrastructure, the upcoming Digital Dirham retail wallet will facilitate programmable payroll, remittances, and government disbursements. This initiative is expected to streamline financial transactions, enhance accessibility for users, and support the broader adoption of digital payment systems. Moreover, heightened mobile engagement contributes to data lakes, bolstering credit scoring for under-banked microbusinesses and promoting inclusive finance throughout the northern emirates.

ESG-Linked Islamic Fintech Bolsters Sustainable Finance

With the UAE's Net Zero 2050 agenda, green sukuk issuances and Shariah-compliant robo-advisory platforms are positioning the nation as a pivotal hub for ethical capital flows, extending their reach into broader MENA projects. These initiatives not only support sustainable development but also attract global investors seeking Shariah-compliant and environmentally responsible financial instruments. Banks, including Abu Dhabi Islamic Bank, are catering to the values-driven investment preferences of younger demographics by embedding carbon-footprint dashboards into their personal finance apps. Such tools empower users to make informed financial decisions aligned with their ethical and environmental priorities. Furthermore, fintech orchestration layers are streamlining intricate profit-and-loss sharing calculations, thereby reducing structuring costs and broadening retail access to sustainable Islamic products.

AI and Blockchain Enable Next-Generation Solutions

Government targets to migrate 50% of federal transactions onto blockchains by 2030 are catalyzing enterprise demand for distributed-ledger compliance, identity, and payments modules[3]UAE Government, “Blockchain in the UAE Government,” u.ae. Emirates NBD has teamed up with Microsoft, showcasing how traditional banks are integrating generative AI into their customer service and risk management processes. This partnership highlights the growing adoption of advanced technologies by financial institutions to enhance operational efficiency, improve customer experiences, and strengthen decision-making frameworks. Concurrently, in early 2024, the Central Bank's mBridge pilot successfully executed a real-value AED 50 million cross-border CBDC transfer to China. The achievement underscores the effectiveness of wholesale settlement systems that sidestep the delays of correspondent banking, paving the way for faster, more secure, and cost-efficient international transactions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity & data privacy risks | -1.8% | National | Short term (≤ 2 years) |

| Senior tech-talent shortage | -1.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Fragmented API standards limiting interoperability | -0.9% | National, with impact on cross-border operations | Medium term (2-4 years) |

| Valuation bubble risk amid late-stage funding squeeze | -1.1% | Dubai and Abu Dhabi venture capital ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cybersecurity and Data-Privacy Risks Moderate Adoption

The Central Bank’s Open Finance Regulation embeds mandatory on-shore data-residency rules, compelling providers to maintain costly local hosting infrastructure while also adhering to strict encryption thresholds. Rising consumer anxiety due to repeated high-profile breaches continues to undermine trust, slowing wallet adoption unless firms proactively invest in zero-trust architectures and obtain ISO 27001 certification. The rapid expansion into virtual-asset services further increases attack surfaces, making coordinated threat-intelligence sharing between DIFC and VARA licensees a critical requirement. These challenges highlight the importance of building strong regulatory-technology partnerships to ensure resilience. At the same time, providers must prioritize customer education to reduce misinformation and strengthen confidence in digital financial ecosystems.

Senior Tech-Talent Shortage Constrains Product Velocity

Even with incentives such as Golden Visas and salary premiums, the pool of senior AI, ML, and blockchain engineers remains shallow compared to market demand, extending time-to-market for specialized products. Smaller fintech firms face difficulty in competing with the compensation packages offered by global technology multinationals, creating capability gaps in critical areas like privacy-preserving analytics and decentralized-finance tooling. Academic initiatives, including the Mohamed bin Zayed University of Artificial Intelligence, are helping to increase local talent supply, though meaningful relief is projected only in the medium term. This persistent shortage places additional pressure on firms to rely on offshore expertise and cross-border collaborations. Furthermore, it underlines the urgent need for stronger industry-academia partnerships to accelerate skills transfer and innovation capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Digital Payments Sustain Leadership

Digital payments held 56.88% of UAE fintech market size in 2025 on the back of instant mobile transfers and a thriving remittance corridor. Insurtech, although smaller, is projected to log a 13.91% CAGR to 2031, underpinned by API-driven micro-policy issuance at e-commerce checkout points. Wio Bank’s embedded-insurance partnership with Shory exemplifies cross-selling synergies that lift average revenue per user. Meanwhile, regulatory clarity around AED-backed stablecoins is catalyzing B2B invoice settlement solutions, providing corporates with near-real-time liquidity management.

Asset-light neobanks continue to grow their share by routing salary accounts to digital wallets, capturing transaction data that feeds lending algorithms. Point-of-sale financing tools now convert retail purchases into installments within seconds, reducing cart abandonment for electronics and travel merchants. In parallel, ADGM’s tokenization sandbox is enabling fractional real-estate investments, generating new fee lines for platform operators. These intertwined developments ensure the UAE fintech market remains the nexus for end-to-end embedded finance across the Gulf.

By End-User: Business Uptake Outpaces Retail Growth

Retail users accounted for 60.02% of the UAE fintech market share in 2025 as super-apps bundled payments, ride-hailing, and grocery delivery into unified interfaces. However, the business segment is forecast to grow at 12.85% CAGR through 2031 as SMEs digitalize trade flows. Hubpay’s multicurrency virtual IBAN, for instance, enables exporters to receive GCC proceeds in hours rather than days. The Central Bank’s API mandates further ease reconciliation by standardizing transaction meta-data. As digital adoption accelerates, more SMEs are expected to integrate fintech solutions directly into their ERP systems. This shift is likely to generate new demand for cross-border compliance tools and automated trade-finance platforms.

Large corporates are pivoting to pay-by-link and request-to-pay models that lower card interchange costs. Treasury heads also value programmable settlement logic embedded in the Digital Dirham pilot, which can automate withholding tax or customs levies at source. Collectively, these enterprise-grade innovations will gradually rebalance the UAE fintech market toward a 55-45 retail-business split by decade end. The evolution of these payment models also supports greater cash-flow visibility and working-capital efficiency for large firms. At the same time, regulatory sandboxes will play a key role in scaling pilot programs into mainstream adoption.

By User Interface: Mobile Dominates While Browser Tools Scale

Mobile apps retained 41.75% of UAE fintech market size in 2025 due to single-tap authentication and push-notification bill alerts. The surge in progressive web applications is now fueling a 14.2% CAGR for browser interfaces, especially among CFOs who prefer larger displays for cash-flow dashboards. Cloud-native banking cores seamlessly synchronize session data, letting users toggle between devices without friction. This flexibility encourages higher daily engagement across both retail and corporate user bases. In parallel, cybersecurity investments are being stepped up to safeguard multi-device access against session hijacking and phishing attempts.

Contactless POS and IoT endpoints—such as connected vending machines at Expo City—extend acceptance networks into high-footfall public venues. Biometric-enabled wearables are also entering payroll and transport niches, reinforcing the UAE’s smart-city ambitions. The Digital Dirham wallet will support these heterogeneous endpoints through open SDKs, ensuring vendor-agnostic adoption across retail and enterprise ecosystems. These innovations illustrate how fintech is becoming embedded into everyday environments rather than remaining app centric. Over time, such pervasive integration is expected to reduce reliance on traditional payment rails while expanding real-time settlement options.

By Emirate: Dual-Hub Model Enhances National Reach

Dubai contributed 59.68% of the UAE fintech market share in 2025, anchored by DIFC’s 5-day licensing track and VARA’s crypto framework that attracted exchanges like Binance. Abu Dhabi’s 13.74% CAGR outlook is propelled by ADGM’s institutional DLT foundation law, which gives regulatory certainty to token-asset infrastructure providers. Combined, the twin hubs balance retail and wholesale specializations, offering startups optionality that few rival markets can match.

Digital channels are reducing the reliance on dense branch networks, benefiting the northern emirates by enabling greater accessibility to financial services. This shift is particularly advantageous for regions with limited physical banking infrastructure, as it bridges the gap between urban and rural areas. Thanks to federal FIT initiatives, KYC utilities are now standardized across all seven emirates. This advancement enables customers to remotely onboard using their Emirates ID biometrics, streamlining the process and enhancing customer convenience. By adopting this distributed model, the UAE fintech market not only mitigates geographic concentration risks but also guarantees inclusive services across the nation, fostering financial inclusion and supporting the growth of the fintech ecosystem.

Geography Analysis

Dubai, capitalizing on its mature payments culture and robust venture capital scene, is set to welcome over 18 million tourists in 2025. Retail-centric fintechs in the city are adeptly navigating VARA’s crypto-marketing guidelines, rolling out compliant reward tokens. These initiatives not only enhance customer engagement but also foster innovation in the retail payments ecosystem. Meanwhile, as DIFC-licensed banks connect with the mBridge CBDC network, volumes for cross-border settlements surge, aligning Dubai with China and Hong Kong. This integration strengthens Dubai's position as a global financial hub, attracting further investments and partnerships in the fintech space.

Abu Dhabi, harnessing its sovereign capital, is nurturing infrastructure fintechs to bridge gaps in B2B trade finance. The emirate's strategic focus on long-term investments ensures the development of sustainable fintech solutions. Thanks to ADGM’s pacts with the Monetary Authority of Singapore and the U.K. FCA, export-focused platforms enjoy expedited market entry through reciprocal sandbox access. These agreements not only reduce time-to-market but also encourage knowledge sharing and collaboration across borders. AI-driven anti-money-laundering analytics, powered by high-performance computing clusters in Khalifa Economic Zones, bolster the emirate's reputation as a hub for institutional innovation. This technological advancement positions Abu Dhabi as a leader in regulatory technology and compliance solutions.

While Dubai and Abu Dhabi lead, Sharjah and Ras Al Khaimah are establishing fintech-friendly industrial free zones, exempting import tariffs on payment hardware. These zones aim to attract global fintech players by reducing operational costs and providing a supportive business environment. With nationwide 5G coverage enhancing user experience and the Central Bank's unified QR code standard streamlining merchant acceptance in stores and taxis, the UAE solidifies its fintech unity amidst rising regional competition. This cohesive approach not only strengthens the national fintech market but also ensures that smaller emirates contribute to the country's overall progress in financial technology.

Competitive Landscape

In the UAE fintech landscape, around 329 firms operate, yet the top five command a mere 28% of the transaction value, highlighting a moderate level of fragmentation. Instead of outright disruptions, the competitive scene is largely influenced by strategic alliances. For instance, Emirates NBD has bolstered its credit underwriting through a partnership with Microsoft Azure OpenAI services, while FAB's investment in Wio Bank paves the way for embedded banking solutions tailored for corporate clients. These partnerships underline the growing trend of leveraging technology and collaboration to enhance operational efficiency and customer offerings.

Payment experts like Tap and Mamo are expanding their reach by offering white-labeled cross-border services to regional banks that lack advanced APIs. This approach allows these banks to modernize their payment infrastructure without significant in-house development. In the crypto realm, providers are transitioning to fiat services as a regulatory safeguard. A case in point is OKX, which secured a retail derivatives license from VARA, emphasizing the need for onshore fiat settlements. This shift reflects the increasing regulatory scrutiny in the region, pushing crypto-native firms to adapt their business models. On another front, insurtechs like Yallacompare are diversifying their revenue streams by embedding micro-policies within travel portals. This strategy not only drives fee diversification but also addresses the challenges posed by the current low-interest-rate environment, ensuring sustained growth.

Sovereign wealth backing provides select portfolio companies with the resilience to navigate market challenges, offering them a competitive edge. However, rising compliance costs are expected to drive consolidation, particularly in over-served niches such as buy-now-pay-later (BNPL) services. Firms equipped with modular, cloud-agnostic cores are better positioned to integrate with government super-apps, which are becoming essential for achieving long-term distribution reach in the UAE fintech market. This adaptability will likely determine the success of firms in maintaining relevance and scaling operations in an increasingly competitive environment.

UAE Fintech Industry Leaders

Tabby

Careem Pay

Liv Digital Bank

Mamo Pay

Beehive FinTech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Central Bank confirmed the Digital Dirham will support instant seven-second transfers following successful cross-border pilots with China and India.

- July 2025: OKX rolled out the UAE’s first regulated retail crypto derivatives under VARA’s pilot framework, offering futures and options with up to 5x leverage.

- May 2025: Ripple announced Zand Bank and Mamo as its first UAE blockchain-enabled payment partners after securing a Dubai license.

- February 2025: Hubpay and Aquanow launched the country’s first fully regulated crypto-payment gateway for merchants, integrating fiat and digital-asset settlement.

UAE Fintech Market Report Scope

Fintech is used to describe any business that provides financial services or apps heavily reliant on technology. FinTech makes financial transactions easier and more affordable for consumers or businesses.

The UAE fintech market is segmented by service proposition (money transfer and payments, savings and investments, digital lending and lending marketplaces, and online insurance & insurance marketplaces). The report offers market size and forecasts for the UAE fintech market in value (USD billion) for all the above segments.

By Service Proposition

| Digital Payments |

| Digital Lending and Financing |

| Digital Investments |

| Insurtech |

| Neobanking |

By End-User

| Retail |

| Businesses |

By User Interface

| Mobile Applications |

| Web / Browser |

| POS / IoT Devices |

By Emirate

| Dubai |

| Abu Dhabi |

| Rest of UAE |

| By Service Proposition | Digital Payments |

| Digital Lending and Financing | |

| Digital Investments | |

| Insurtech | |

| Neobanking | |

| By End-User | Retail |

| Businesses | |

| By User Interface | Mobile Applications |

| Web / Browser | |

| POS / IoT Devices | |

| By Emirate | Dubai |

| Abu Dhabi | |

| Rest of UAE |

Key Questions Answered in the Report

How large is the UAE fintech market in 2026?

The UAE fintech market size is USD 52.07 billion in 2026, on track to hit USD 90.06 billion by 2031.

What is the growth rate of digital payments within UAE fintech?

Digital payments account for 56.88% of market share and continue to grow alongside a national push toward 90% cashless transactions by 2026.

Which emirate leads in fintech activity?

Dubai leads with 59.68% market share, leveraging DIFC infrastructure and VARA crypto regulations.

Why are businesses adopting fintech solutions rapidly?

SMEs seek cost-efficient cross-border payments and embedded finance, driving a 12.85% CAGR for the business segment through 2031.

What role will the Digital Dirham play?

The Digital Dirham will provide instant programmable settlements, lowering remittance costs and integrating with existing mobile wallets across the federation

Page last updated on: