Low Speed Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

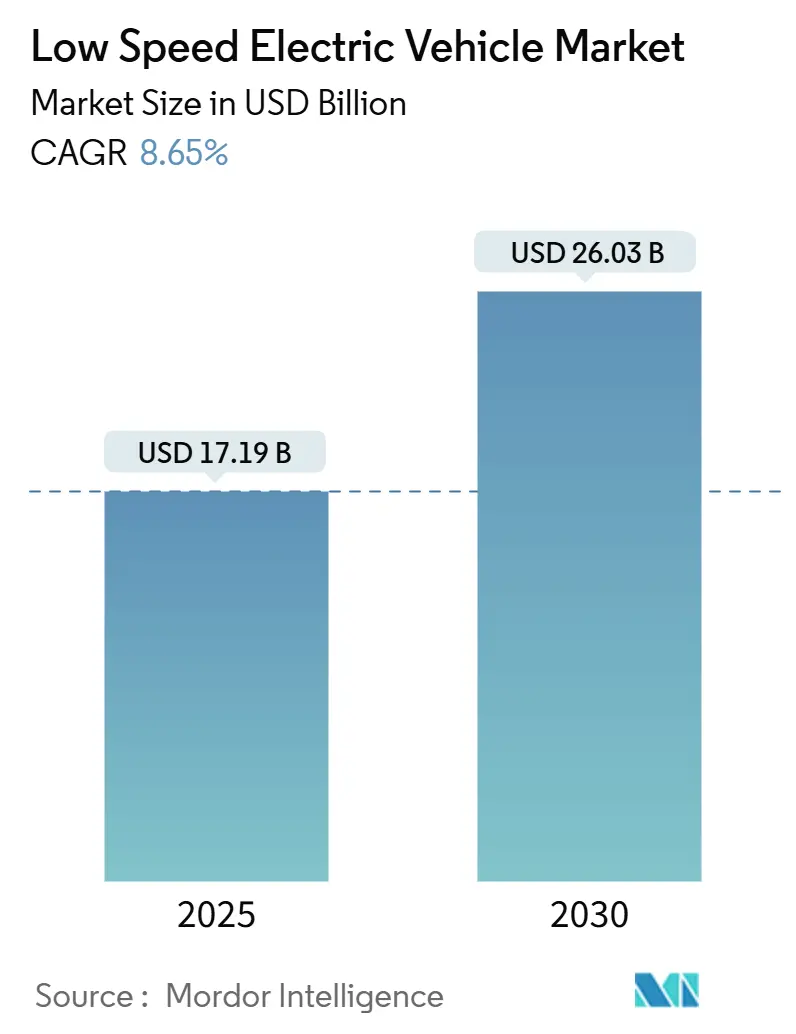

| Market Size (2025) | USD 17.19 Billion |

| Market Size (2030) | USD 26.03 Billion |

| Growth Rate (2025 - 2030) | 8.65% CAGR |

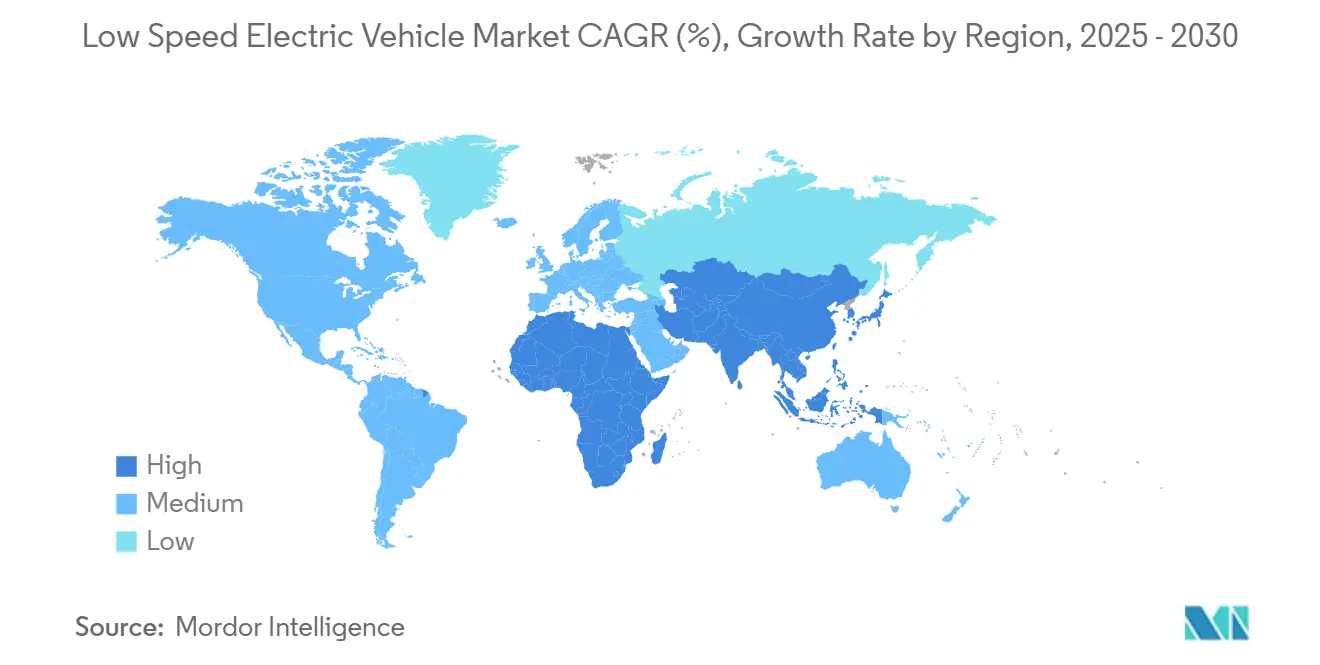

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

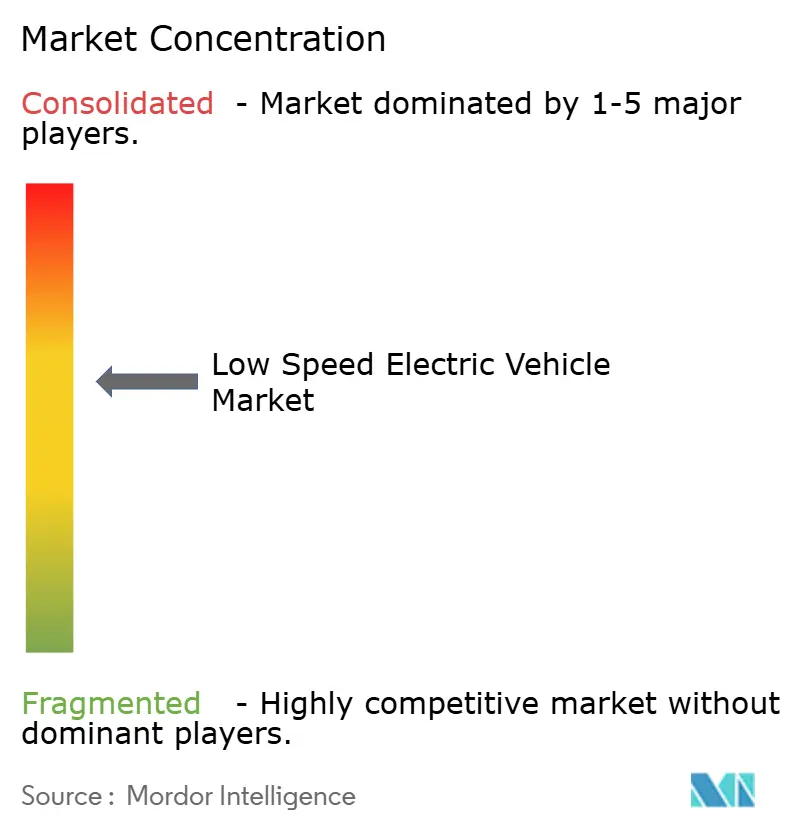

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Speed Electric Vehicle Market Analysis by Mordor Intelligence

The low-speed electric vehicle market size is estimated at USD 17.19 billion in 2025, and is expected to reach USD 26.03 billion by 2030, at a CAGR of 8.65% during the forecast period (2025-2030). Spiralling urban populations, congestion pricing, and increasingly stringent exhaust-emissions rules are nudging commuters toward compact battery-powered formats that operate below 50 km/hr. Falling lithium-ion pack prices, factory-gate tax incentives in emerging Asia, and the visible success of delivery fleets using electric two- and three-wheelers reinforce demand. Established motorcycle brands retool production lines while Chinese specialists flood world markets with aggressively priced models, accelerating technology diffusion. Battery-swapping corridors in India and parts of the Middle East and Africa, now underpin business case certainty for operators prioritizing uptime over home charging.

Key Report Takeaways

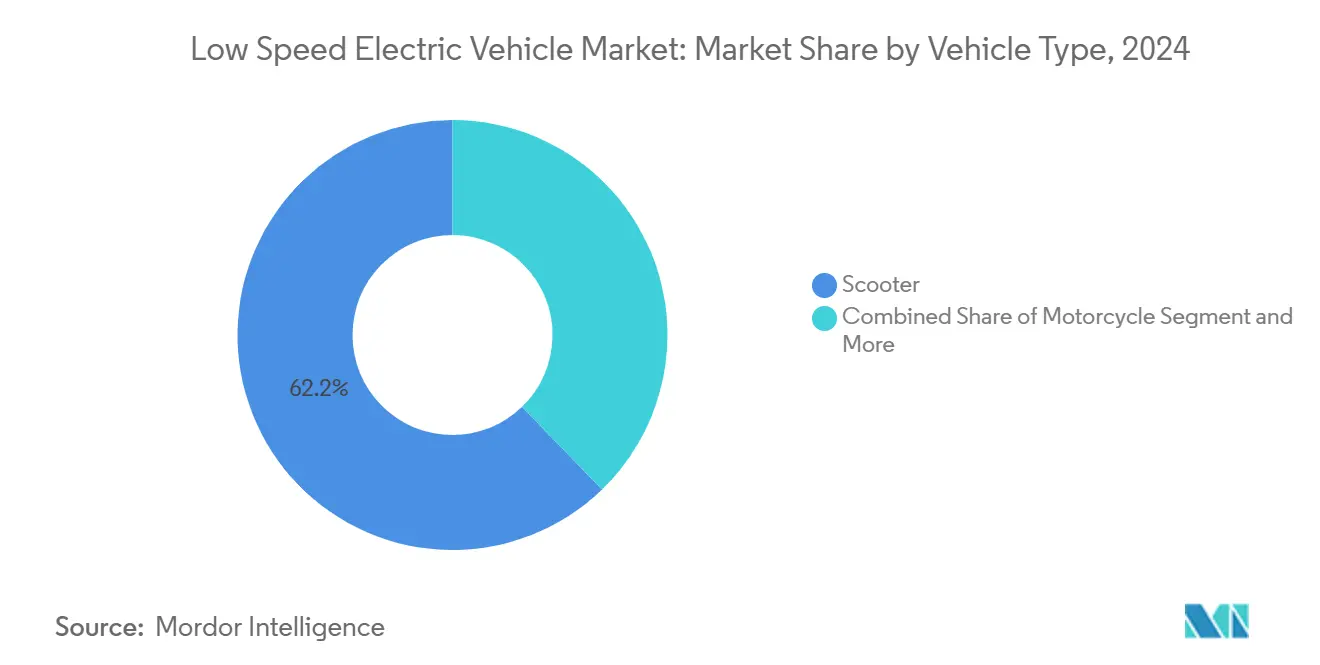

- By vehicle type, Scooters led the low-speed electric vehicle market with a 62.24% revenue share in 2024; three-wheelers are projected to expand at an 11.34% CAGR through 2030.

- By battery chemistry, lithium-ion batteries captured a 71.74% share of the low-speed electric vehicle market in 2024, whereas solid-state variants are forecast to grow at a 14.26% CAGR.

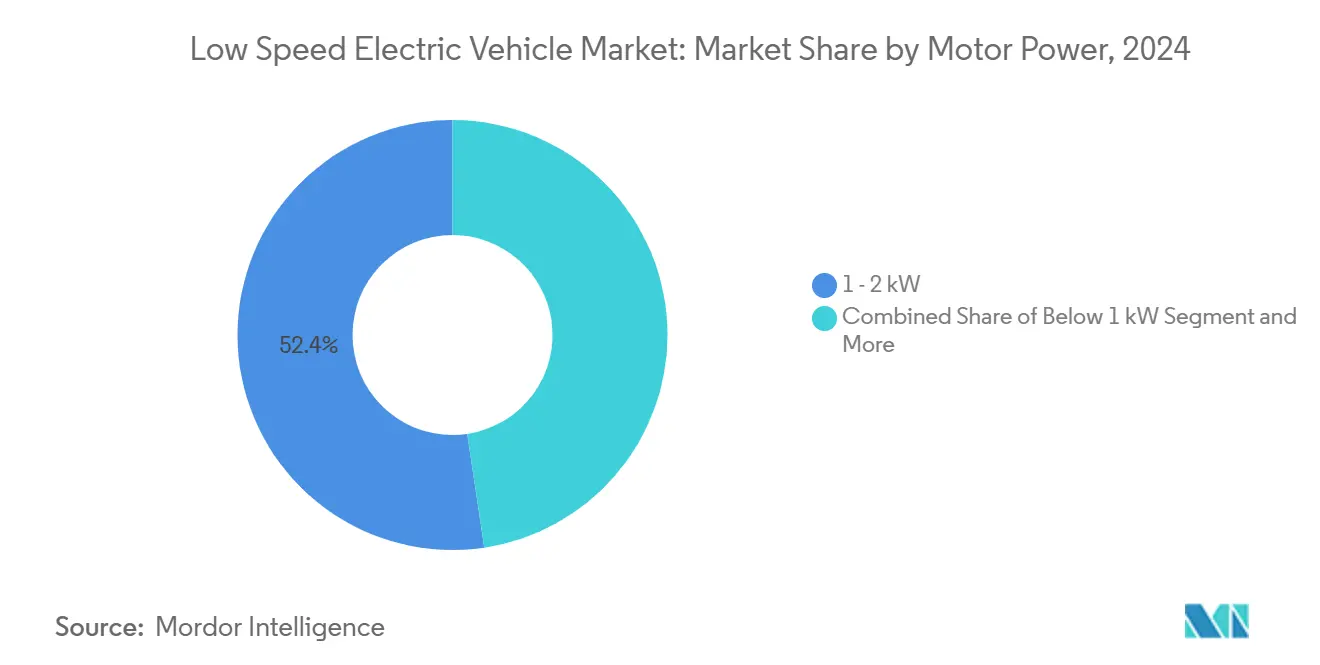

- By motor power, 1-2 kW systems held 52.36% of the low-speed electric vehicle market share in 2024; motors above 3 kW will advance at 12.28% CAGR to 2030.

- By distribution channel, offline dealerships retained a 58.28% share of the low-speed electric vehicle market in 2024. Still, fleet and subscription operators are set to rise at an 11.78% CAGR, signaling a structural pivot toward mobility-as-a-service.

- Geographically, Asia-Pacific dominated the low-speed electric vehicle market, with a 76.57% share in 2024; the Africa is the fastest-growing region, with a 14.28% CAGR to 2030.

Global Low Speed Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization and traffic congestion | +2.8% | Global; strongest in Asia-Pacific and Middle East and Africa | Long term (≥ 4 years) |

| Falling lithium-ion battery costs | +2.1% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Government incentives for ≤ 50 km/hr e-2ws | +1.9% | India, China, Southeast Asia, South America | Short term (≤ 2 years) |

| E-commerce and delivery-fleet electrification | +1.6% | Urban centres worldwide | Medium term (2-4 years) |

| Battery-swapping rollout in emerging markets | +1.3% | India, Southeast Asia, select African economies | Long term (≥ 4 years) |

| Subscription-based micro-mobility adoption | +1.1% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Lithium-Ion Battery Costs

Average pack prices dropped 15-25% in 2024, as gigafactories unlocked scale economies and cathode chemistries shifted toward lower-nickel blends[1]“Battery Cost Dynamics After Budget 2025-26,”, Down To Earth, downtoearth.org.in. India’s 2025-26 budget waived customs duties on critical minerals, slicing off mid-range scooter sticker prices. Similar fiscal tweaks in Kenya and Vietnam trim import-related freight costs. As parity with lead-acid batteries is achieved, manufacturers can preserve margins while cutting retail prices, sustaining the low-speed electric vehicle market’s double-digit growth trajectory. Local cell production plants under construction in Indonesia and Tamil Nadu will buffer currency swings and improve supply resilience.

Government Incentives for Less Than 50 km/hr E-2Ws

Targeted subsidy frameworks create regulatory moats where low-speed electric vehicles compete on features rather than against petrol rivals. India’s PM E-DRIVE earmarks USD 1.3 billion in purchase grants and battery R&D through March 2026[2]“PM E-DRIVE Scheme 2025,”, Government of India, pib.gov.in. China’s forthcoming mid-2026 safety code exempts sub-50 km/hr models from costly fire-suppression hardware mandated for high-power machines. Thailand’s EV 3.5 programme fast-tracks investment licences for light commercial three-wheelers, linking tax holidays to local-value thresholds. These country-specific levers jointly widen the total addressable pool for the low-speed electric vehicle market.

E-Commerce and Delivery-Fleet Electrification

Courier companies grind through daily stop-and-go cycles that heighten operating expenditures for petrol bikes. Regional super-apps partner with battery-as-a-service start-ups, installing kiosk networks that complete swaps in under a minute, enabling three-shift utilisation. Growing expectations for same-day delivery oblige fleet managers to maximise uptime, steering them toward modular powertrains and cloud diagnostics. Their high-visibility road presence normalises electric formats for individual riders, creating an adoption flywheel for the low-speed electric vehicle market.

Battery-Swapping Rollout in Emerging Markets

Hard-wiring charging docks is capital-intensive in dense neighbourhoods where real-estate premiums are steep. Compact swap stations can tuck into convenience-store forecourts, extending practical range without grid upgrades. Africa’s pan-regional energy utilities pilot pay-as-you-go battery lockers that leverage mobile-money platforms. Standardisation pacts among Japanese OEMs now filter into Southeast Asia, cutting inventory costs for ride-sharing operators. Over the long run, interoperability could unlock cross-brand rural charging corridors, enlarging the low-speed electric vehicle market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety and regulatory fragmentation | -1.7% | Europe, North America | Long term (≥ 4 years) |

| Competition from e-bikes and kick-scooters | -1.2% | Urban markets in developed economies | Medium term (2-4 years) |

| Chinese price wars and margin pressure | -0.9% | Global spillovers from Chinese overcapacity | Short term (≤ 2 years) |

| Lead-acid dependence and environmental push-back | -0.8% | Asia-Pacific, Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety and Regulatory Fragmentation

A patchwork of local standards forces manufacturers to redesign each market's lighting, brake, and telemetry systems. Europe’s EN 17128 tries to harmonise personal light EV norms, yet individual capitals impose bespoke helmet or speed caps. The US Consumer Product Safety Commission limits federal oversight to 20 mph e-bikes, leaving electric scooters to state legislatures, some of which mandate vehicle registration while others classify them as toys. Compliance engineering drains resources that could be channelled into R&D, ultimately slowing global roll-outs for the low-speed electric vehicle market.

Competition From E-Bikes and Kick-Scooters

Dockless share fleets have achieved near-corner ubiquity in Paris, Madrid, and several US college towns. For inner-city errands under 5 km, lightweight e-bikes can outmanoeuvre bulkier scooters whilst skirting parking fees. Riders who rent on demand may postpone outright purchases, clipping addressable volumes for the low-speed electric vehicle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Three-Wheelers Surge

The Low-Speed Electric vehicle Market segment with scooters controls 62.24% of revenue, owing to deep model catalogues and competitive consumer financing. Three-wheelers, however, are on course for an 11.34% CAGR as courier and grocery chains standardise on enclosed cargo trikes for last-mile drops. India’s e-rickshaw registrations topped 57% of total three-wheeler sales in 2024, a milestone attributed to high petrol prices and city-centre access perks. Market observers expect OEM partnerships with fleet financiers to accelerate deployments, especially once residual-value benchmarks mature.

Scooter OEMs are enhancing smartphone integration, regenerative braking, and cloud-linked theft tracking to preserve segment leadership. Meanwhile, motorcycles aim at aspirational urban youth, but their growth curve flattens as cities cap roadway speeds, reducing the advantage of higher-power formats. Highlight commercial electrification keeps three-wheelers in the investor spotlight, reinforcing their strategic weight within the low-speed electric vehicle market.

By Battery Type: Solid-State Advancements

Lithium-ion packs represented 71.74% revenue in the 2024 Low-Speed Electric Vehicle Market, fuelled by falling per-kWh prices and mature recycling streams. Still, solid-state prototypes promise energy densities up to three times higher, and Toyota vows a 750-mile range demonstrator by 2027. The low-speed electric vehicle market share for solid-state units could approach 10% by the late decade as pilot projects prove cycle life beyond 1,000 charges. Lead-acid batteries linger only in ultra-price-sensitive rural fleets, but environmental levies and scrap-handling fees erode their economic case.

Manufacturers prioritising in-house battery development are better positioned to capture integration synergies in BMS software, thermal management, and cell-to-chassis architectures. Supply chains will face realignment when solid-state enters mass production, as conventional liquid-electrolyte cathode suppliers diversify into sulphide powders and ceramic separators. The low-speed electric vehicle industry thus stands on the cusp of a chemistry transition that could lift range anxiety restrictions and open peri-urban commuting segments.

By Motor Power: Premiumisation Underway

By motor power, 1–2 kW systems held 52.36% of the low-speed electric vehicle market share in 2024, ideal for city-speed acceleration and acceptable hill-climb performance. Yet riders engaged in commercial hauling or longer suburban journeys gravitate toward motors above 3 kW, a slice projected to grow at 12.28% CAGR. Early adopters report smoother throttle response and superior payload stability, aligning with courier key performance indicators.

Ola Electric’s forthcoming heavy rare-earth-free motors target an efficiency uplift, cutting cell requirement per vehicle and easing raw-material risk. Experimenting with fractional slot concentrated windings has trimmed torque ripple, delivering car-like ride comfort. These incremental hardware gains dovetail with intelligent controllers that modulate output based on GPS-inferred gradients, matching energy demand to topography.

By Distribution Channel: Mobility-as-a-Service Expansion

Offline dealerships retained a 58.28% share of the low-speed electric vehicle market in 2024, buoyed by legacy showroom footprints and spare-parts availability. Nevertheless, fleet and subscription operators are forecast to grow at an 11.78% CAGR as big-box retailers outsource same-day logistics to specialised e-mobility vendors. OEM-direct e-commerce storefronts further chip away at traditional retail by bundling financing approval, insurance, and doorstep delivery in a single digital journey.

Buyers spend fewer hours on dealer lots when purchasing EVs than petrol cars, reinforcing the appetite for click-to-buy journeys. Regulatory reforms in South Korea and Germany now permit manufacturers to act as authorised sellers, hastening the shift toward agency models. The transition could unlock higher margin mixes for dealerships that pivot to service-only hubs-software upgrades, diagnostics, and battery reconditioning.

Geography Analysis

Asia-Pacific accounted for 76.57% of 2024 revenue, underscored by China’s scale economies and India’s accelerating two-wheeler conversion push. Although price wars led by BYD’s 34% list-price cuts have compressed gross margins across tier-2 brands. In India, fiscal year 2025 saw 1.14 million electric two-wheeler registrations, with incumbent motorcycle brands recapturing share from early-stage start-ups through after-sales network strength[3]“India EV Sales FY 2025,”, Autocar Professional, autocarpro.in. Southeast Asian governments compete for assembly investments, and Vietnam’s Bac Giang plant by Yadea will add 2 million yearly units when fully ramped.

Africa’s low-speed electric vehicle market is set to post a 14.28% CAGR, rising from a modest base but benefiting from smartphone-centric ride-hail economies. Kenya’s boda-boda operators who switch to electric motorcycles report daily income lifts as fuel outlays plunge. Ghana and Morocco are drafting battery-recycling codes that lure foreign downstream players, while Rwanda’s pay-per-swap billing platforms integrate with national ID databases to mitigate credit risk. With over a dozen African states introducing EV import-duty holidays by 2025, deployment bottlenecks are shifting from policy to grid capacity and training of service technicians.

North America and Europe represent commanding premium ASPs, underpinning a sizeable profit pool. The European Commission values shared micromobility-powered heavily by low-speed electric scooters-at more than EUR 100 billion by 2030, yet tight safety certification cycles can delay product refreshes. In the United States, state-level caps on max-allowable e-scooter speed vary from 25 km/hr in California to 32 km/hr in Utah, demanding adaptive firmware from OEMs. These regions will continue to shape safety benchmarks and software-defined features that cascade into global designs, indirectly raising the technology bar for the low-speed electric vehicle market

Competitive Landscape

The market is moderately fragmented, leaving room for challenger brands from China, India, and Vietnam to scale quickly. Legacy two-wheeler majors-TVS, Bajaj, and Hero MotoCorp-benefit from nationwide parts depots, trained mechanics, and finance arms, insulating them against early-life reliability scares that have dogged certain start-ups. Ola Electric’s share plunged from 49.2% in May 2024 to near-20% a year later as customer forums flagged quality lapses and service backlog issues.

Chinese manufacturers ship low-speed units. Domestic oversupply pressures have therefore triggered export offensives into Latin America, Eastern Europe, and Africa. Aggressive FOB pricing, often 20–30% below local incumbents, forces rivals to refine propositions around after-sales support, warranty longevity, and connected-vehicle apps. Meanwhile, Japanese consortia of Honda, Yamaha, and Suzuki are co-developing swappable batteries to fight range anxiety and preserve brand interchangeability.

Winning strategies increasingly centre on vertical integration-owning cells, motors, and firmware stacks-to secure margin headroom and data monetisation options. Several OEMs have rolled out over-the-air updates that unlock a subscription fee for performance boosts or new ride modes. Start-ups with cloud telematics platforms offer fleet managers dashboards of state-of-charge, route-level energy burn, and predictive maintenance alerts. These services, once ancillary, are rapidly becoming table stakes in the low-speed electric vehicle market.

Low Speed Electric Vehicle Industry Leaders

Yadea Group Holdings Ltd.

Niu Technologies

Jiangsu Xinri E-Vehicle (Sunra)

Hero Electric Vehicles Pvt. Ltd.

AIMA Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Yamaha Motor acquired Brose’s bicycle drive-unit business, establishing Yamaha Motor eBike Systems in Europe to accelerate electric drive-train rollout.

- January 2025: Hyundai and TVS unveiled a joint electric three-wheeler concept at Bharat Mobility Global Expo, signalling big-brand confidence in commercial light EV demand.

- August 2024: Honda and Yamaha signed an OEM supply agreement under which Honda provides EM1 e: and BENLY e: I models to broaden Yamaha’s Japanese portfolio of Class-1 electrics.

Global Low Speed Electric Vehicle Market Report Scope

| Scooter |

| Motorcycle |

| Three-Wheeler |

| Lead-acid |

| Lithium-ion |

| Other |

| Below 1 kW |

| 1 - 2 kW |

| 2 - 3 kW |

| Above 3 kW |

| Offline |

| OEM-Direct / Online |

| Fleet and Subscription |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Scooter | |

| Motorcycle | ||

| Three-Wheeler | ||

| By Battery Type | Lead-acid | |

| Lithium-ion | ||

| Other | ||

| By Motor Power | Below 1 kW | |

| 1 - 2 kW | ||

| 2 - 3 kW | ||

| Above 3 kW | ||

| By Distribution Channel | Offline | |

| OEM-Direct / Online | ||

| Fleet and Subscription | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the low-speed electric vehicle market?

The low-speed electric vehicle market size is estimated at USD 17.19 billion in 2025, and is expected to reach USD 26.03 billion by 2030, at a CAGR of 8.65% during 2025-2030 period.

Which region dominates low-speed electric vehicle sales?

Asia-Pacific held 76.57% of global revenue in 2024, Due to China’s production scale and India’s subsidy-driven demand surge.

Why are fleet operators embracing low-speed electric vehicles?

Courier and food-delivery fleets report up to 80% lower running costs versus petrol bikes, making electric models financially attractive despite higher upfront prices.

What are the main challenges facing the market?

Fragmented safety regulations across countries, margin pressure from Chinese price competition, and environmental concerns about lead-acid disposal are the primary headwinds slowing growth.

Are subscription models likely to displace traditional ownership?

Yes. Flat-fee subscriptions that bundle battery access, maintenance, and insurance are expanding at 11.78% CAGR, indicating growing consumer preference for use-over-ownership.

Page last updated on: