Europe Construction Machinery Rental Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

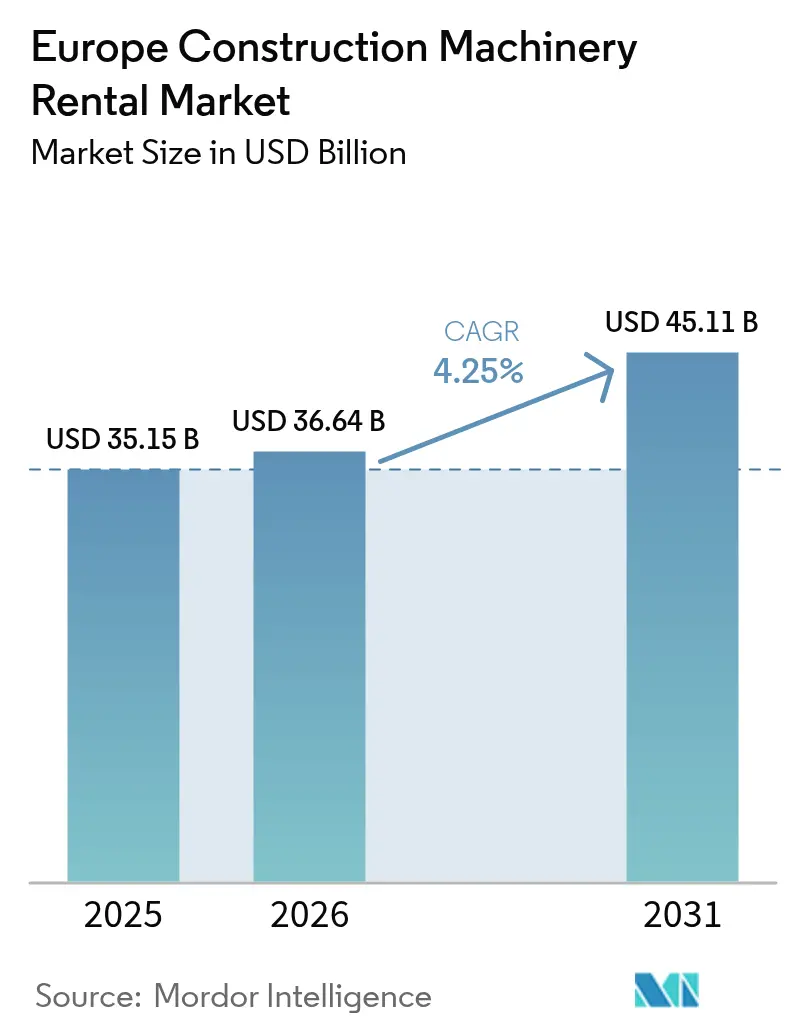

| Base Year Market Size (2025) | USD 35.15 Billion |

| Market Size (2026) | USD 36.64 Billion |

| Market Size (2031) | USD 45.11 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

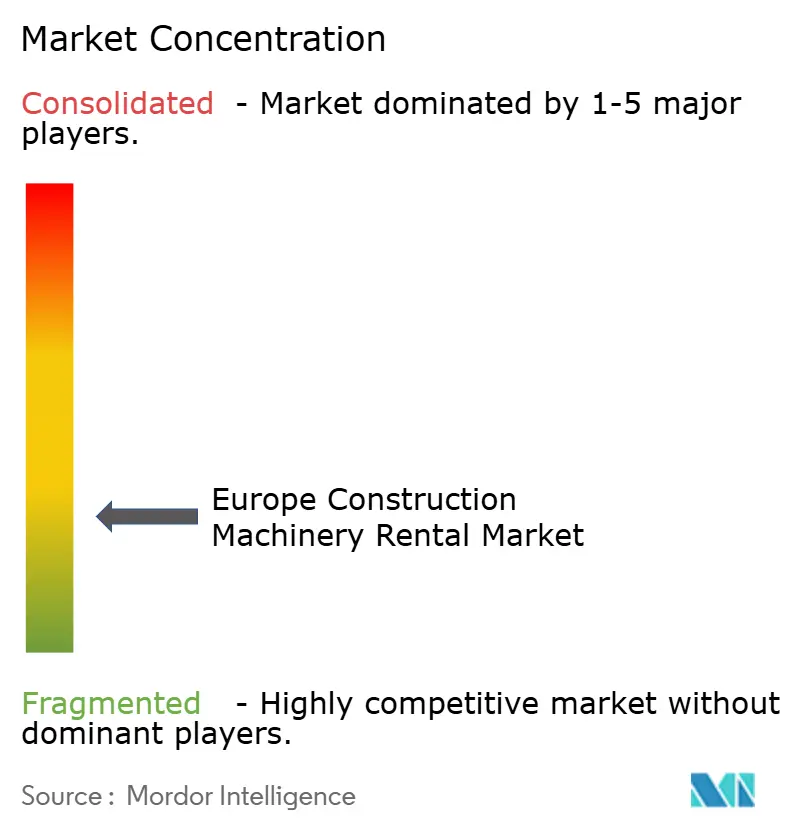

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Construction Machinery Rental Market Analysis by Mordor Intelligence

The European construction machinery rental market size is expected to grow from USD 35.15 billion in 2025 to USD 36.64 billion in 2026 and is forecast to reach USD 45.11 billion by 2031 at 4.25% CAGR over 2026-2031. This steady climb reflects resilient demand for rented machinery, expanding equipment-as-a-service agreements, and emission-driven fleet renewal across the region. The European construction equipment rental market benefits from EU-backed infrastructure stimulus, rapid electrification mandates, and ESG-linked lending that lowers capital costs for sustainable fleets. Operators prioritize telematics-enabled utilization gains, while governments reinforce demand with green transport corridors and digital connectivity projects. Competitive intensity is growing as OEMs form direct rental units, traditional rental giants accelerate pan-European acquisitions, and digital marketplaces shrink search and transaction costs for contractors.

Key Report Takeaways

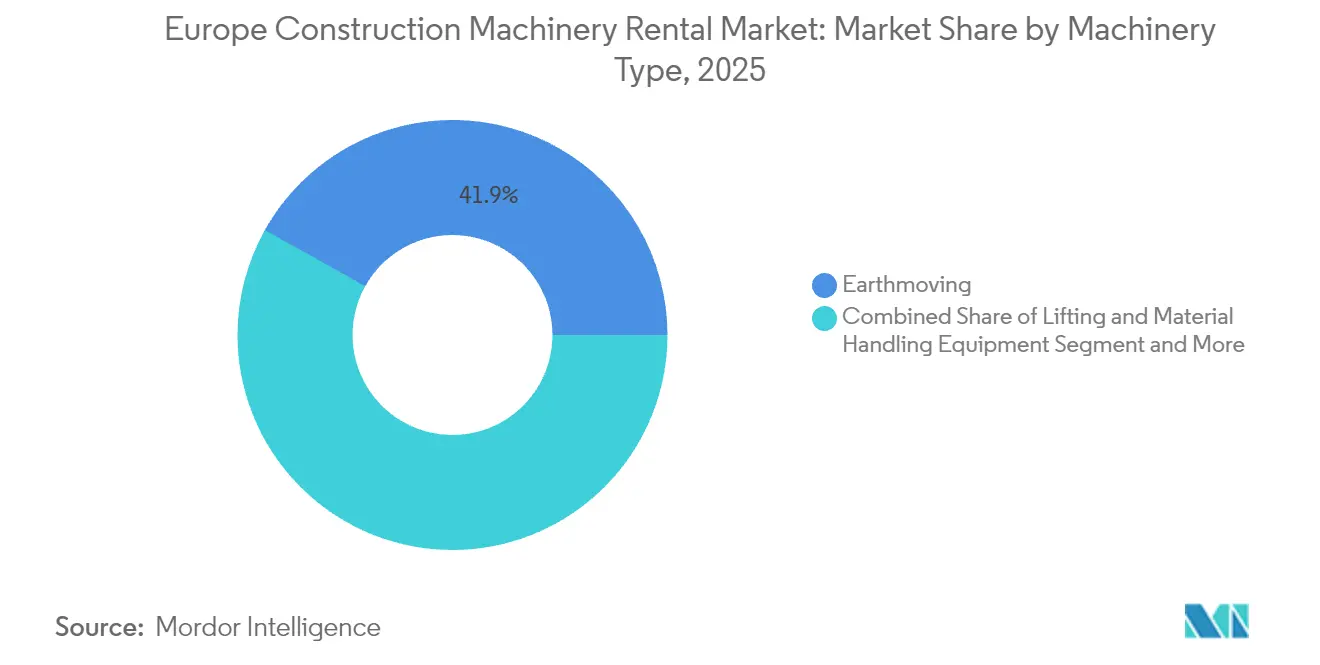

- By machinery type, earthmoving equipment led with 41.88% of the European construction equipment rental market share in 2025; it is projected to advance at a 4.55% CAGR to 2031.

- By drive type, hydraulic systems held 77.95% of the European construction equipment rental market in 2025, while fully electric alternatives are expanding at a 11.85% CAGR through 2031.

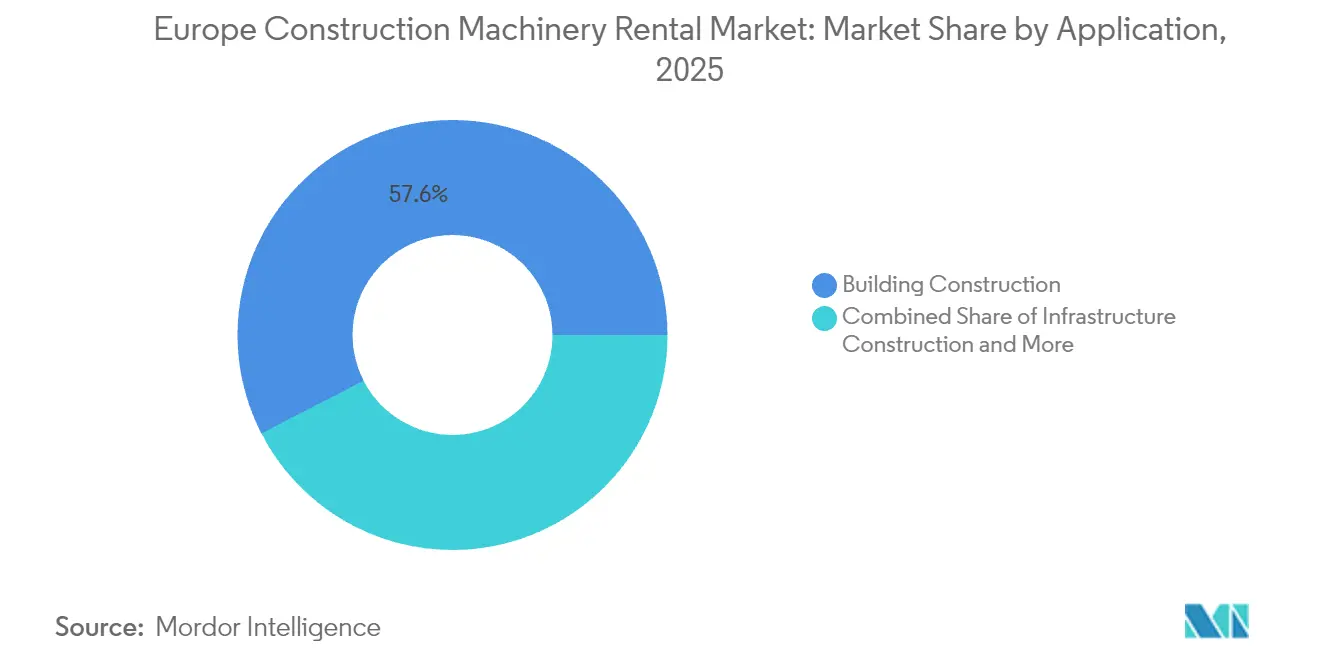

- By application, building construction commanded a 57.56% share of the European construction equipment rental market size in 2025 and is progressing at a 4.62% CAGR through 2031.

- By payload capacity, medium-duty machines captured a 47.35% share of the European construction equipment rental market in 2025; light-duty units recorded the fastest 5.08% CAGR between 2026 and 2031.

- By geography, Germany dominated with 24.52% European construction equipment rental market share in 2025, while Spain posted the highest 5.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Construction Machinery Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EU Infrastructure Stimulus | +1.2% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Accelerated Fleet Electrification Mandates | +0.8% | EU-wide with Nordic early adoption | Long term (≥ 4 years) |

| Shift Toward Equipment-as-a-Service Models | +0.7% | Concentrated in mature markets | Short term (≤ 2 years) |

| ESG-Linked Financing Lowering CAPEX | +0.6% | Western Europe expanding east | Medium term (2-4 years) |

| EU Taxonomy Focus on Embodied-Carbon Reports | +0.4% | EU-wide with UK and Switzerland spillover | Long term (≥ 4 years) |

| On-Site Modular Power Units | +0.3% | Northern and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EU Infrastructure Stimulus (Post-2025)

The European Investment Bank has earmarked EUR 1.1 trillion for climate-aligned infrastructure through 2030, triggering a sustained uptick in rentals of excavators, pavers, and tower cranes as projects break ground across transport and digital corridors [1]“EIB Group Climate Bank Roadmap 2021-2025,”, European Investment Bank, eib.org. Germany is making a bold push to modernize its infrastructure and digital capabilities. A substantial investment commitment has been set aside to upgrade transport networks and accelerate digital transformation over the coming years, creating demand for specialized earthmoving fleets. Unlike past cycles, current allocations stress renewable energy and fiber rollout, forcing rental companies to secure niche machinery such as cable plows and wind-turbine erection cranes. Supply tightness amplifies utilization rates and elevates short-term pricing. Stimulus-driven linkages also ripple into private housing and commercial builds around upgraded transit hubs.

Accelerated Fleet Electrification Mandates

The European Commission’s Fit for 55 package requires a 55% emissions cut by 2030, pressuring rental firms to pivot from diesel to battery and hydrogen powertrains [2]“Green Loans Gain Traction in Europe’s Equipment Sector,”, Financial Times Staff, ft.com. JCB’s hydrogen engine program, now trialed in 11 countries, exemplifies OEM response. Early adopters in Sweden and Norway leverage subsidies to recoup higher purchase prices and pass premium rates to contractors looking to enter zero-emission zones. The mandate stimulates parallel investment in charging depots, technician retraining, and digital monitoring systems, raising capital intensity yet lowering lifecycle costs.

ESG-Linked Financing Lowering CAPEX

Banks have begun rewarding rental companies that disclose carbon metrics and electrification roadmaps with 25–50 basis-point interest discounts, cutting fleet acquisition costs. Loxam Group integrated sustainability KPIs into a multi-currency revolving credit that spans 1,091 branches, freeing capital for bulk electric mini-excavator orders. Preferential rates widen the cost gap between large, data-rich players and smaller rivals, inadvertently accelerating consolidation as well-funded buyers scoop up legacy fleets ripe for electrification.

EU Taxonomy Focus on Embodied-Carbon Reporting

Beginning in 2024, large builders must disclose Scope 3 emissions from rented equipment under the Corporate Sustainability Reporting Directive. Demand therefore concentrates on fleets with proven carbon accounting systems, pushing rental firms to tag each unit with cradle-to-grave CO₂ metrics. Providers lacking digital traceability risk exclusion from tender lists, especially on publicly funded projects anchored to strict green criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operator Talent Shortage | -1.1% | Western Europe most acute | Medium term (2-4 years) |

| Disharmony in NRMM Stage V Adoption | -0.9% | EU-wide with uneven enforcement | Short term (≤ 2 years) |

| Secondary Diesel Asset Glut | -0.6% | Western Europe spreading east | Long term (≥ 4 years) |

| High Telemetry Retrofit Cost | -0.4% | Mature rental markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Disharmony in NRMM Stage V Adoption

Non-Road Mobile Machinery Stage V rules entered force in 2019 yet penalty rigor differs by member state, compelling rental fleets to juggle dual compliance standards. Companies operating across borders incur surging logistics and refitting costs to ensure each unit meets the strictest locale.

Secondary Market Glut from Diesel Obsolescence

Rapid policy shifts and urban low-emission zones slash residual values on diesel excavators, loaders, and generators, forcing accelerated write-downs for rental companies holding legacy fleets. Firms relocate units to looser regulatory regions or accept discounted export sales that erode balance-sheet strength.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Earthmoving Dominance Drives Electrification

Earthmoving equipment accounted for 41.88% of the European construction equipment rental market share in 2025, and this category is forecast to grow at a 4.55% CAGR through 2031. Excavators, particularly crawler variants, dominate heavy civil works while wheeled models support urban mobility. Skid-steer loaders gain traction in refurbishment projects that demand compact maneuverability. Motor graders and dozers sustain demand from Eastern Europe’s expanding highway corridors. The European construction equipment rental market size within earthmoving is also a focal point for electrification pilots such as Hitachi’s 1.7-ton battery excavator slated for 2027 rollout.

The segment’s electrification cadence accelerates as contractors seek to meet city-center emission caps without compromising performance. OEMs experiment with swappable battery packs to mitigate charging downtime, and rental houses deploy mobile chargers to keep utilization high. Tier-one rental firms bundle earthmoving packages with on-site power units to capture higher value from integrated offerings.

By Drive Type: Electric Disruption Accelerates Despite Hydraulic Dominance

Hydraulic systems retained 77.95% share of the European construction equipment rental market size in 2025 because of their proven reliability and wide service network. Yet purely electric drives are posting a 11.85% CAGR, aided by Nordic subsidies and expanding urban low-emission zones. Diesel-electric hybrids offer a transitional path, providing fuel savings without range anxiety on remote sites.

The European construction equipment rental market registers divergent adoption curves by equipment class. Compact excavators and scissor lifts shift first as battery energy density now supports full-shift operation. Heavier equipment awaits next-generation solid-state batteries or hydrogen fuel cells, where JCB’s ongoing trials signal longer-term promise. Rental firms hedge by procuring modular fleets that can swap between diesel and electric drivelines.

By Application: Building Construction Sustains Growth Momentum

Building construction absorbed 57.56% of market demand in 2025, expanding at a 4.62% CAGR as Europe tackles housing deficits and commercial space reconfiguration. Residential projects benefit from government loan guarantees and streamlined permitting for affordable units. Commercial builders upgrade facilities with flexible layouts and smart-building features, driving scissor lift and telehandler demand. Industrial expansions linked to near-shoring of electronics and pharmaceuticals maintain steady equipment utilization.

Infrastructure is the second-largest application, propelled by EU transport corridors, grid upgrades, and broadband rollout. Renewable energy construction commands high-margin rentals for specialized cranes and drilling rigs. Mining and quarrying remain small but stable, while disaster recovery rentals spike seasonally amid severe floods and wildfires.

By Payload Capacity: Light-Duty Growth Reflects Urban Constraints

Medium-duty units held a 47.35% share in 2025, balancing versatility and transport cost efficiency. Light-duty machines, however, clock the fastest 5.08% CAGR as dense cities impose weight and noise limits that favor compact loaders, mini-excavators, and battery scissor lifts. Contractors appreciate simplified licensing and lower operator skill thresholds. Heavy-duty rentals persist for mega-projects but face scheduling volatility tied to permit lead times.

Light-duty growth also aligns with refurbishment and retrofit programs under the EU Green Deal, emphasizing energy-efficient building upgrades requiring compact indoor equipment. Major rental firms respond with urban-tailored fleets and last-mile logistics hubs that shorten delivery windows.

Geography Analysis

Germany led the European construction equipment rental market with 24.52% share in 2025, driven by a sophisticated industrial base and a EUR 269.6 billion infrastructure commitment to 2027 that sustains earthmoving and road-building rentals. Strict diesel bans in major cities also prompt early adoption of electric mini-excavators, helping rental firms secure premium rates. Spain exhibits the fastest 5.05% CAGR, buoyed by tourism infrastructure upgrades and renewable energy parks supported by EU cohesion funds. Spanish rental providers leverage flexible credit schemes to modernize fleets rapidly.

France and Italy maintain significant volumes through rail modernization and seismic retrofit programs. The United Kingdom, while outside the EU, influences fleet flows as companies redeploy equipment across the Channel during seasonal lulls. Nordic nations like Sweden set benchmarks for zero-emission equipment uptake and digital job-site connectivity. Poland and the Czech Republic present expansion corridors for pan-European rental chains, capitalizing on EU-funded highway and energy projects. Eastern borders confront geopolitical uncertainty, yet domestic construction continues to underpin localized rental demand. Pan-regional providers balance fleets across these markets to offset seasonality: transferring heaters and generators south for winter builds, then rotating aerial platforms north for summer refurbishments. Regulatory heterogeneity necessitates dynamic asset allocation to avoid idle non-compliant units.

Competitive Landscape

Top Companies in Europe Construction Machinery Rental Market

The European construction equipment rental market remains fragmented yet shows accelerating consolidation. Loxam Group, posting EUR 2.6 billion in 2024 revenue across 1,091 branches[3]“2025 Universal Registration Document,”, Loxam Group, loxam.com, revamped its revolving credit to include sustainability KPIs that lower funding costs for electric fleet expansion. Sunbelt Rentals, part of Ashtead Group, continues acquisitive growth to build a trans-continental platform capable of pooling large-scale procurement and telematics data. Meanwhile, OEMs such as Volvo CE pilot direct rental offers, potentially sidelining intermediaries on premium technology units.

Digital differentiation intensifies as firms roll out customer portals offering real-time equipment location, CO₂ dashboards, and automated off-hire workflows. Predictive maintenance algorithms cut downtime and reinforce service contracts, fostering stickier client relationships. Autonomous equipment prototypes, like John Deere’s retrofittable articulated dump truck showcased at CES 2025, foreshadow a future where rental firms negotiate software licenses alongside hardware leases. Competitive advantage increasingly hinges on data analytics, financing agility, and regional compliance expertise rather than sheer fleet size alone.

Europe Construction Machinery Rental Industry Leaders

LOXAM SAS

Kiloutou Group

Ashtead Group (Sunbelt Rentals)

Boels Rental

Caterpillar Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Robert Baran Crane Group Petrolift will expand its crane fleet with 21 new Grove all-terrain cranes to meet the increasing demand for diverse lifting support. The expansion aims to enhance the company's operational capabilities and service offerings across various industrial sectors. This strategic fleet enhancement will enable the company to handle more complex lifting projects and accommodate the growing requirements of its client base.

- March 2024: Boels Rental announces its planned acquisition of Riwal, a company specializing in Aerial Work Platforms (AWP). The acquisition completion depends on fulfilling customary conditions, including approvals from competition authorities. This acquisition supports Boels Rental's growth strategy to strengthen its European market position, expand its geographical presence, and increase its AWP fleet.

Europe Construction Machinery Rental Market Report Scope

Construction machinery rental services allow users to utilize the machinery for a short or long period in exchange for paying a higher daily cost or monthly cost. It is an agreement between the user and the machinery rental company.

The European construction machinery rental market is segmented by machinery type (cranes, telescopic handlers, excavators, loaders, motor graders, road construction equipment, and other machinery types), drive type (hydraulic and hybrid), application (building construction, road construction, and other applications), and geography (Germany, United Kingdom, France, Spain, Italy, and Rest of Europe). The report offers market size and forecasts in value (USD) for all the above segments.

| Earthmoving Machinery | Excavators | Crawler |

| Wheeled | ||

| Loaders | Skid-Steer | |

| Wheel | ||

| Backhoe | ||

| Motor Graders | ||

| Dozers | ||

| Lifting and Material-Handling | Cranes | Mobile Cranes |

| Tower Cranes | ||

| Telescopic Handlers | ||

| Aerial Work Platforms | ||

| Road Construction Equipment | Pavers | |

| Road Rollers | ||

| Asphalt Mixers | ||

| Other Machinery Types | ||

| Hydraulic |

| Diesel-Electric Hybrid |

| Fully Electric |

| Hydrogen Fuel Cell |

| Building Construction | Residential |

| Commercial | |

| Industrial | |

| Infrastructure Construction | Road and Highway |

| Rail | |

| Airport | |

| Energy Infrastructure | |

| Mining and Quarrying | |

| Disaster and Emergency Relief | |

| Other Applications |

| Light-Duty (Below 3 tons) |

| Medium-Duty (3-10 tons) |

| Heavy-Duty (10-30 tons) |

| Super Heavy-Duty (Above 30 tons) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Russia |

| Rest of Europe |

| By Machinery Type | Earthmoving Machinery | Excavators | Crawler |

| Wheeled | |||

| Loaders | Skid-Steer | ||

| Wheel | |||

| Backhoe | |||

| Motor Graders | |||

| Dozers | |||

| Lifting and Material-Handling | Cranes | Mobile Cranes | |

| Tower Cranes | |||

| Telescopic Handlers | |||

| Aerial Work Platforms | |||

| Road Construction Equipment | Pavers | ||

| Road Rollers | |||

| Asphalt Mixers | |||

| Other Machinery Types | |||

| By Drive Type | Hydraulic | ||

| Diesel-Electric Hybrid | |||

| Fully Electric | |||

| Hydrogen Fuel Cell | |||

| By Application | Building Construction | Residential | |

| Commercial | |||

| Industrial | |||

| Infrastructure Construction | Road and Highway | ||

| Rail | |||

| Airport | |||

| Energy Infrastructure | |||

| Mining and Quarrying | |||

| Disaster and Emergency Relief | |||

| Other Applications | |||

| By Payload Capacity | Light-Duty (Below 3 tons) | ||

| Medium-Duty (3-10 tons) | |||

| Heavy-Duty (10-30 tons) | |||

| Super Heavy-Duty (Above 30 tons) | |||

| By Country | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Sweden | |||

| Poland | |||

| Russia | |||

| Rest of Europe | |||

Key Questions Answered in the Report

What is the current value of the European construction equipment rental market?

The market is valued at USD 36.64 billion in 2026 and is projected to reach USD 45.11 billion by 2031.

How fast is demand for electric construction equipment growing in Europe?

Fully electric drives in the European construction equipment rental market are expanding at a 11.85% CAGR through 2031, outpacing all other drive types.

Which country leads European equipment rentals by revenue?

Germany accounted for 24.52% of European construction equipment rental market share in 2025, the largest national slice.

Which machinery segment commands the biggest rental share?

Earthmoving machinery held 41.88% of 2025 rental revenue and is forecast to remain dominant through 2031.

Why are rental firms adopting equipment-as-a-service models?

Labor shortages, demand for uptime guarantees, and digital monitoring needs encourage bundled offerings that combine machines, certified operators, and maintenance into one contract.

Page last updated on: