Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

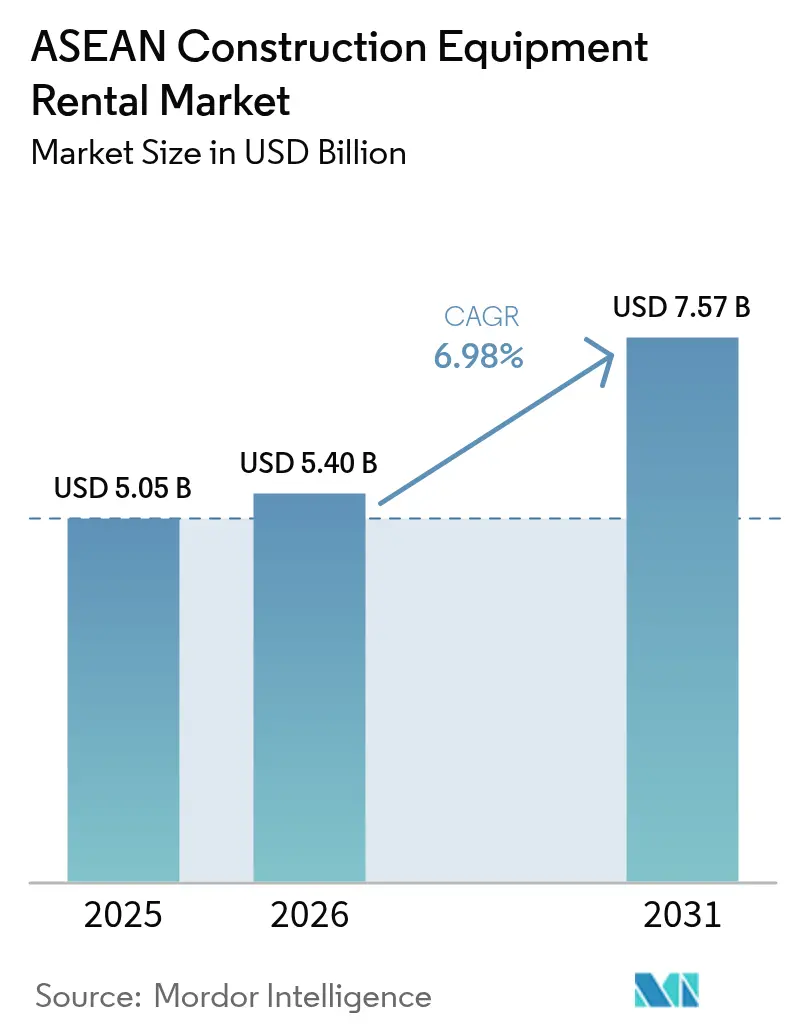

| Base Year Market Size (2025) | USD 5.05 Billion |

| Market Size (2026) | USD 5.4 Billion |

| Market Size (2031) | USD 7.57 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

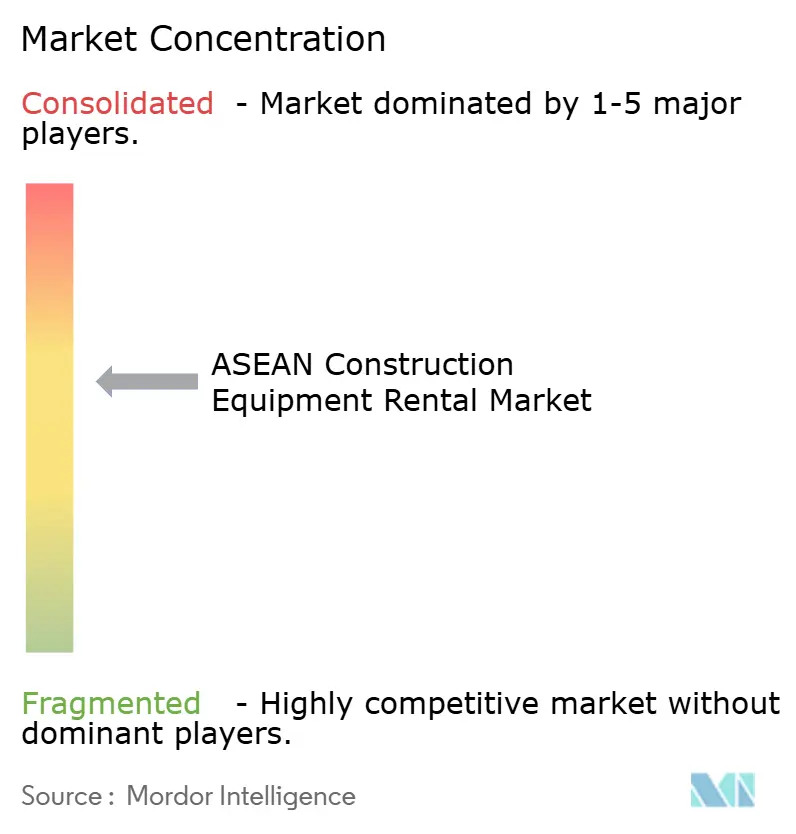

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Construction Equipment Rental Market Analysis by Mordor Intelligence

The ASEAN Construction Equipment Rental Market size was valued at USD 5.05 billion in 2025 and estimated to grow from USD 5.4 billion in 2026 to reach USD 7.57 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031). Robust infrastructure pipelines, surging FDI into manufacturing, and contractors’ preference for asset-light operating modes underpin the growth outlook even as tariff barriers and short project cycles introduce demand volatility. Indonesia’s National Strategic Projects and Vietnam’s rapid public-investment disbursement anchor equipment utilization, while Thailand’s capex program and Singapore’s early adoption of electric machinery broaden demand across equipment classes. Rental companies gain from telematics-enabled usage pricing, regional trade facilitation under the ASEAN Customs Transit System, and turnkey service contracts that bundle machines, operators, and maintenance. Competitive intensity remains moderate as Japanese incumbents expand regionally and local specialists leverage proximity advantages and digital fleet tools to protect share in the ASEAN construction equipment rental market.

Key Report Takeaways

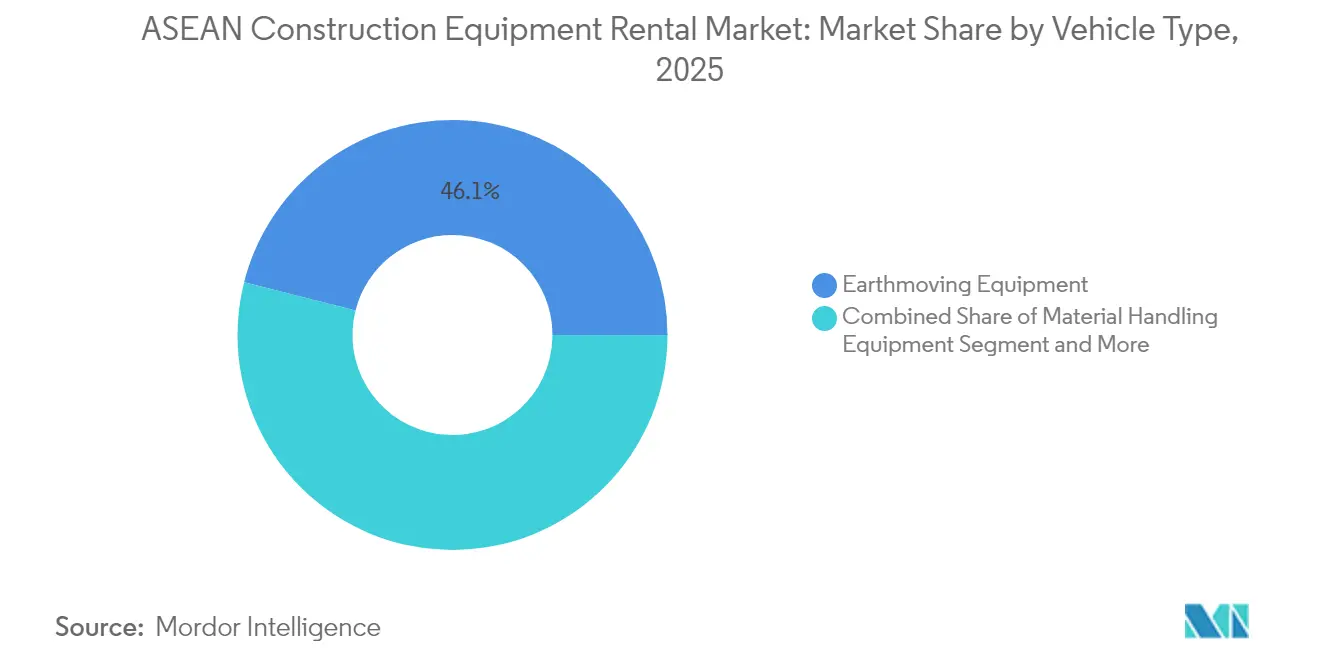

- By vehicle type, earthmoving equipment led the ASEAN construction equipment rental market in 2025, with a 46.05% revenue share; concrete and road construction machinery is projected to expand at a 7.09% CAGR through 2031.

- By propulsion, internal combustion drives retained a 72.40% share of the ASEAN construction equipment rental market in 2025, while electric drives are set to post the fastest growth at a 7.04% CAGR to 2031.

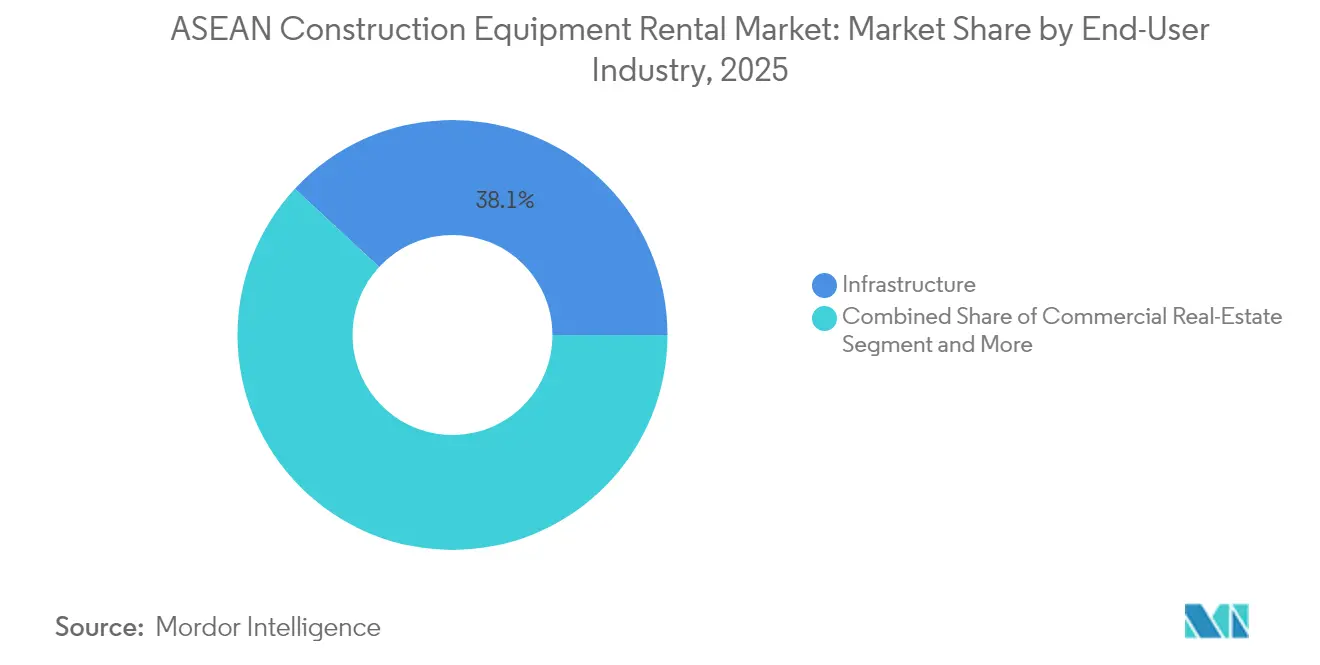

- By end-user industry, infrastructure commanded a 38.10% share of the ASEAN construction equipment rental market in 2025. In contrast, industrial and logistics applications are poised to rise at a 7.18% CAGR over the forecast period.

- By rental duration, short-term contracts under six months captured 62.60% of the ASEAN construction equipment rental market share in 2025; project-based turnkey agreements will record a 7.12% CAGR to 2031.

- By country, Indonesia held 27.35% of the ASEAN construction equipment rental market share in 2025, and Vietnam is expected to lead growth with a 7.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Construction Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Stimulus Programmes | +1.8% | Indonesia, Thailand, Vietnam core with spillover to Malaysia, Philippines | Medium term (2-4 years) |

| Expansion Of Industrial Parks | +1.5% | Vietnam, Indonesia, Thailand manufacturing corridors | Long term (≥ 4 years) |

| Growing Contractor Preference | +1.2% | Global ASEAN with strongest adoption in Singapore, Malaysia urban markets | Short term (≤ 2 years) |

| Digital Fleet-Management | +0.9% | Singapore, Malaysia, Thailand early adopters with regional expansion | Medium term (2-4 years) |

| Early-Stage Electrified Equipment Pilots | +0.7% | Singapore, Thailand urban construction zones with emission regulations | Medium term (2-4 years) |

| ESG-Linked Green-Financing Incentives | +0.6% | Singapore, Malaysia, Thailand with expanding green bond markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Stimulus Programs

Consistent public spending in the ASEAN construction equipment rental market fuels steady work backlogs in transport, energy, and urban projects. Indonesia's PSN has allocated a significant budget for key initiatives, focusing on roads, ports, and water projects that heavily rely on expansive earthmoving fleets. Vietnam's proactive approach is evident as it has already disbursed a substantial portion of its public-investment budget for the year, a move that bolsters longer rental contracts. Meanwhile, Thailand has earmarked considerable funds for transport links over the next few years, driving up the demand for concrete pavers and compaction equipment. The OECD projects that Indonesia will require a massive investment in climate-resilient infrastructure within the next decade. This forecast highlights the urgency and signals a growing need for specialty machinery, particularly in drainage and flood protection, within rental fleets. Adding to the momentum, the Asian Development Bank points to a significant infrastructure gap across Asia through the decade's end, suggesting a robust, multi-year demand for diversified rental portfolios [1]“Meeting Asia’s Infrastructure Needs,” Asian Development Bank, adb.org .

Expansion of Industrial Parks & Logistics Hubs

In recent times, Vietnam has attracted substantial foreign direct investment and initiated the development of a significant logistics space in Bac Ninh. As ASEAN plans to expand its industrial land over the next few years, this ensures a consistent demand for equipment like piling rigs, telehandlers, and temporary power units. Meanwhile, Malaysia and Indonesia are becoming hotspots for electronics assemblers aiming for diversified supply chains, leading to multistage buildouts reliant on adaptable rental agreements. The ASEAN construction equipment rental market is witnessing a surge in demand for precision lifting tools, clean-room compatible gear, and compact earthmovers, fueled by nearshoring and e-commerce-driven warehouse and factory constructions.

Growing Contractor Preference for OPEX over CAPEX

In the ASEAN construction equipment rental market, developers are gravitating towards rentals to sidestep depreciation risks, all while navigating uneven project pipelines and tighter working-capital targets. Contractors in Singapore are opting to rent high-reach demolition rigs and electric mixers, allowing them to leverage advanced technology without hefty investments. In Malaysia, the post-pandemic rebuilding efforts have spurred firms to bolster their order books, doing so with a keen focus on minimizing fixed assets. Astra International's finance division for heavy equipment reported significant growth, reflecting a growing preference for usage-based financing, a trend that's bolstering the rental market. Furthermore, telematics platforms are pioneering pay-per-use billing, effectively lowering the cost barriers for short-term equipment access.

Digital Fleet-Management & Telematics Integration

Connected equipment platforms improve uptime and price transparency, letting renters in the ASEAN construction equipment rental market align costs with actual machine hours. Trackunit IrisX gives owners live utilization dashboards and predictive maintenance alerts that cut downtime. Komatsu’s Smart Construction links machines and site data on multiple projects, enabling integrated rental-plus-site-management packages. AEMP APIs standardize data flow across mixed fleets, easing adoption. Usage-based contracts and remote immobilization reduce delinquency risk, encouraging rental firms to scale fleets with lower working-capital drag.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short Project Cycles Causing Utilization Volatility | -1.1% | Thailand, Philippines, Malaysia with seasonal construction patterns | Short term (≤ 2 years) |

| Persistently High Import Tariffs | -0.8% | Indonesia, Vietnam with cross-border equipment movement restrictions | Long term (≥ 4 years) |

| Fragmented Equipment-Maintenance Ecosystem | -0.5% | Regional ASEAN with strongest impact in Cambodia, Laos, Myanmar | Medium term (2-4 years) |

| Slow Homologation Of Battery-Electric Heavy Machines | -0.4% | ASEAN-wide regulatory harmonization challenges | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short Project Cycles Causing Utilization Volatility

In the ASEAN construction equipment rental market, construction timelines are compressed, and idle-time spikes emerge, eroding margins. This is due to a combination of stop-start approvals, seasonal monsoons, and financing delays. In Thailand, budget approvals frequently push into the latter part of fiscal quarters. This results in simultaneous mobilizations, putting a strain on rental supply. Recently, a major construction company reported significant profits but fell short of its revenue targets due to delayed project starts, underscoring the volatility's impact on equipment planning. To navigate these challenges, rental companies either maintain larger idle inventories or impose higher premiums during slack periods, ultimately inflating project costs.

Persistently High Import Tariffs on Used Machinery

Indonesia imposes a duty, while Vietnam enforces an age cap on used machinery. These measures hinder cross-border fleet balancing and inflate acquisition costs in the ASEAN construction equipment rental market. Smaller firms, dependent on budget-friendly second-hand equipment to expand their fleets, grapple with rising prices and a constrained selection. Despite the ASEAN Customs Transit System's promise of significant trade-cost savings, customs bonds and extensive paperwork introduce added costs and delays. This discourages temporary equipment transfers for major regional projects. Market fragmentation continues, awaiting a liberalization of tariff regimes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Earthmoving Dominance Amid Road Construction Acceleration

Due to Indonesia's land-development drives and Malaysia's industrial-park grading, earthmoving equipment captured 46.05% of the ASEAN construction equipment rental market in 2025. Concrete and road machinery should post a 7.09% CAGR through 2031 as Thailand’s capex push accelerates paving and surface works. Skid-steer and compact track loaders gain favor in Singapore’s cramped sites, while vibratory rollers stay essential for expressway sub-grades across Vietnam.

Electric and hybrid powertrains emerge in concrete mixers and small loaders, supported by Singapore’s job-site chargers and Thailand’s pilot battery-swap depots. Komatsu unit deliveries fell in 2024, yet parts revenue climbed, showing high fleet utilization that sustains aftermarket rentals. Precision lifting cranes support Vietnam’s multi-story logistics builds, and demand for specialty dredging excavators rises for Indonesia’s flood-control projects.

By Propulsion: Electric Drive Momentum Despite IC Engine Dominance

Internal combustion systems retained a 72.40% share of the ASEAN construction equipment rental market in 2025, as diesel power remains unrivaled for remote or heavy-duty. Electric units, however, are forecast to grow 7.04% CAGR through 2031, led by Singapore mandates for low-emission sites and Thai pilots of battery concrete trucks. Hybrid drives serve bridge applications where long runtimes are essential, yet fuel savings are prized.

Battery density improvements and clustered charging depots allow rental firms to rotate electric fleets efficiently. H&E Equipment Services reports one-third of its active rental units are electric, validating operating-cost savings. Diesel engines stay prevalent in Indonesian mining projects lacking grid power, while gasoline engines shrink to small tools as battery parity approaches.

By End-User Industry: Infrastructure Leadership with Industrial Logistics Surge

Due to government transport, energy, and resilience spending, infrastructure projects commanded 38.10% of the ASEAN construction equipment rental market in 2025. Industrial and logistics builds are set to outpace at 7.18% CAGR, fueled by nearshoring of electronics assembly and e-commerce warehousing in Vietnam and Malaysia.

Commercial real estate sees selective demand in mixed-use zones of Singapore, although higher borrowing costs temper speculative builds. Mining rentals rise cyclically with Indonesian nickel extraction, while renewable energy plants lift orders for precision lifts and access platforms. Telecommunications tower rollout and solar farms add niche demand for truck-mounted cranes across rural ASEAN.

By Rental Duration: Short-Term Prevalence with Turnkey Integration Growth

Short-term contracts under six months delivered 62.60% of the ASEAN construction equipment rental market in 2025 because contractors hedge against project delays. Turnkey packages combining machines, operators, and service are projected to rise at a 7.12% CAGR as builders outsource logistics complexity.

Long-term agreements secure rates on multi-year infrastructure corridors yet remain a smaller slice where financing remains milestone-based. Mobilization-heavy gear, such as tower cranes, often stays on site beyond twelve months, stabilizing utilization for specialized rental houses like PT Mulia Rentalindo Persada, with fleets exceeding exponentially.

Geography Analysis

In 2024, Indonesia commanded a significant share of the ASEAN construction equipment rental market, buoyed by PSN megaprojects, nickel processing initiatives, and well-established distributor networks. Meanwhile, Vietnam is set to experience the most rapid growth, fueled by a substantial influx of FDI, expansive industrial developments, and a push for new expressways. The expansive PSN pipeline encompasses toll roads, ports, and water projects, all with a pronounced demand for excavators, cranes, and pavers. United Tractors’ Komatsu network, alongside Astra International’s financial services, streamlines equipment accessibility. However, it's noteworthy that Komatsu's sales took a hit, dropping in the same year, attributed to project rescheduling. Furthermore, OECD studies highlight a looming investment need for resilience, hinting at burgeoning opportunities for dredging pumps and flood-barrier rigs.

Vietnam charts the most promising course. In 2024, a significant portion of public investment disbursements bolstered contractor backlogs. Concurrently, a substantial FDI influx is channeling into electronics and renewable energy plants. Illustrating this momentum, BW Industrial and ESR are developing hubs in Bac Ninh, emphasizing logistics that heavily rely on concrete pumps and telehandlers. The entry of Korea Rental Vina, establishing nodes in both Hanoi and Ho Chi Minh, signals robust international confidence in the market. However, FiinRatings has flagged potential concerns: residential market distress and looming bond maturities could dampen enthusiasm in non-industrial segments .

Thailand finds itself in a balanced position. With a capex plan targeting rail, road, and airport enhancements, there's a noticeable uptick in demand for compaction and paving equipment. Rent (Thailand) Co. boasts an impressive inventory, offering a wide range of items across numerous categories, with telematics technology enhancing billing accuracy. Singapore, despite its smaller size, is at the forefront of innovation: pioneering electric concrete mixers, site chargers, and enforcing stringent emissions standards that are setting benchmarks for the region. While Malaysia’s industrial parks are reaping benefits from nearshoring trends, the Philippines is grappling with challenges: delayed PPP financing is stunting its rental demand growth. Emerging markets like Cambodia, Laos, Myanmar, and Brunei, though currently modest players, stand poised to benefit as regional supply chains continue to broaden.

Competitive Landscape

Competition in the ASEAN construction equipment rental market is moderate. Japanese multinationals Kanamoto and Aktio extend footprints from Thailand into Malaysia, Indonesia, and Myanmar to capture cross-border collaborations. Aktio leverages a common telematics backbone to reposition idle machines across borders, cutting ownership costs [3]“Global Network Overview,” Aktio Corporation, aktio.co.jp .

Local champions retain edges in speed and customer intimacy. Sin Heng Heavy Machinery and Tat Hong Holdings provide 24-hour service fleets, which are crucial when weather disruptions mandate rapid dispatch. PT Mulia Rentalindo Persada’s 700-unit fleet reflects depth in Indonesian earthmoving, while Rent (Thailand) Co. features specialized access platforms for urban high-rise work.

OEMs deepen vertical integration. Komatsu’s August 2024 acquisition of UMW Komatsu Heavy Equipment gives it direct rental outlets across Malaysia, Singapore, Myanmar, and Brunei. Caterpillar dealers pilot subscription models that fold maintenance and telematics analytics into rental rates, challenging independents. Niche opportunities arise in battery-electric equipment, high-capacity crawler cranes for wind-turbine erection, and amphibious excavators for climate-resilience projects.

ASEAN Construction Equipment Rental Industry Leaders

Kanamoto Co. Ltd

Aktio Co. Ltd

Sin Heng Heavy Machinery Limited

Rent (Thailand) Co. Ltd

Shanghai Pangyuan Machinery Rental Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Komatsu completed the acquisition of UMW Komatsu Heavy Equipment covering Malaysia, Singapore, Myanmar, Brunei, and Papua New Guinea, integrating distribution and rental operations to strengthen service support.

- May 2024: BW Industrial Development and ESR Group commenced construction on two joint-venture logistics projects totaling 270,000 sqm in Bac Ninh, Vietnam, with completion expected in Q3 2025.

ASEAN Construction Equipment Rental Market Report Scope

Construction equipment refers to heavy-duty vehicles specially designed for executing construction tasks, most frequently involving earthwork operations.

The ASEAN construction equipment rental market is segmented by vehicle type (earth moving equipment, material handling), by propulsion type (ic engine, hybrid drive), and by geography (Indonesia, Thailand, Vietnam, Singapore, Malaysia, Philippines, and the Rest of the ASEAN).

The report offers market size and forecasts for the ASEAN Construction equipment rental in terms of value (USD Billion) for all the above segments.

By Vehicle Type

| Earthmoving Equipment | Excavators |

| Loaders | |

| Bulldozers | |

| Skid-steer & Compact Track Loaders | |

| Material Handling Equipment | Cranes (Crawler, Mobile, Tower) |

| Forklifts & Telehandlers | |

| Concrete & Road Construction Machinery | |

| Compaction Equipment |

By Propulsion

| IC Engine | Diesel |

| Gasoline | |

| Hybrid Drive | |

| Electric Drive |

By End-User Industry

| Infrastructure |

| Commercial Real-Estate |

| Industrial & Logistics |

| Mining & Quarrying |

| Oil & Gas |

| Other Specialised Sectors |

By Rental Duration

| Short-term |

| Long-term |

By Country

| Indonesia |

| Thailand |

| Vietnam |

| Singapore |

| Malaysia |

| Philippines |

| Cambodia |

| Laos |

| Myanmar |

| Brunei |

| By Vehicle Type | Earthmoving Equipment | Excavators |

| Loaders | ||

| Bulldozers | ||

| Skid-steer & Compact Track Loaders | ||

| Material Handling Equipment | Cranes (Crawler, Mobile, Tower) | |

| Forklifts & Telehandlers | ||

| Concrete & Road Construction Machinery | ||

| Compaction Equipment | ||

| By Propulsion | IC Engine | Diesel |

| Gasoline | ||

| Hybrid Drive | ||

| Electric Drive | ||

| By End-User Industry | Infrastructure | |

| Commercial Real-Estate | ||

| Industrial & Logistics | ||

| Mining & Quarrying | ||

| Oil & Gas | ||

| Other Specialised Sectors | ||

| By Rental Duration | Short-term | |

| Long-term | ||

| By Country | Indonesia | |

| Thailand | ||

| Vietnam | ||

| Singapore | ||

| Malaysia | ||

| Philippines | ||

| Cambodia | ||

| Laos | ||

| Myanmar | ||

| Brunei | ||

Key Questions Answered in the Report

What is the current value of the ASEAN construction equipment rental market?

The market stands at USD 5.4 billion in 2026.

How fast is demand for electric construction equipment rising?

Electric drive rentals are projected to grow at a 7.04% CAGR through 2031, outpacing diesel demand.

Which country offers the highest growth potential for rental providers?

Due to large FDI inflows and accelerated infrastructure spending, Vietnam is forecast to expand at a 7.16% CAGR.

Why are short-term rentals dominant in ASEAN?

Contractors favor flexibility amid seasonal weather risks and variable project approvals, leading to a 62.60% share for rentals shorter than six months.

How do telematics platforms benefit rental companies?

Connected systems improve utilization tracking, enable pay-per-use pricing, and lower maintenance downtime, boosting fleet profitability.

What restrains cross-border equipment movement in ASEAN?

Import tariffs and age limits on used machinery in Indonesia and Vietnam raise costs and complicate regional fleet optimization.

Page last updated on: