Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

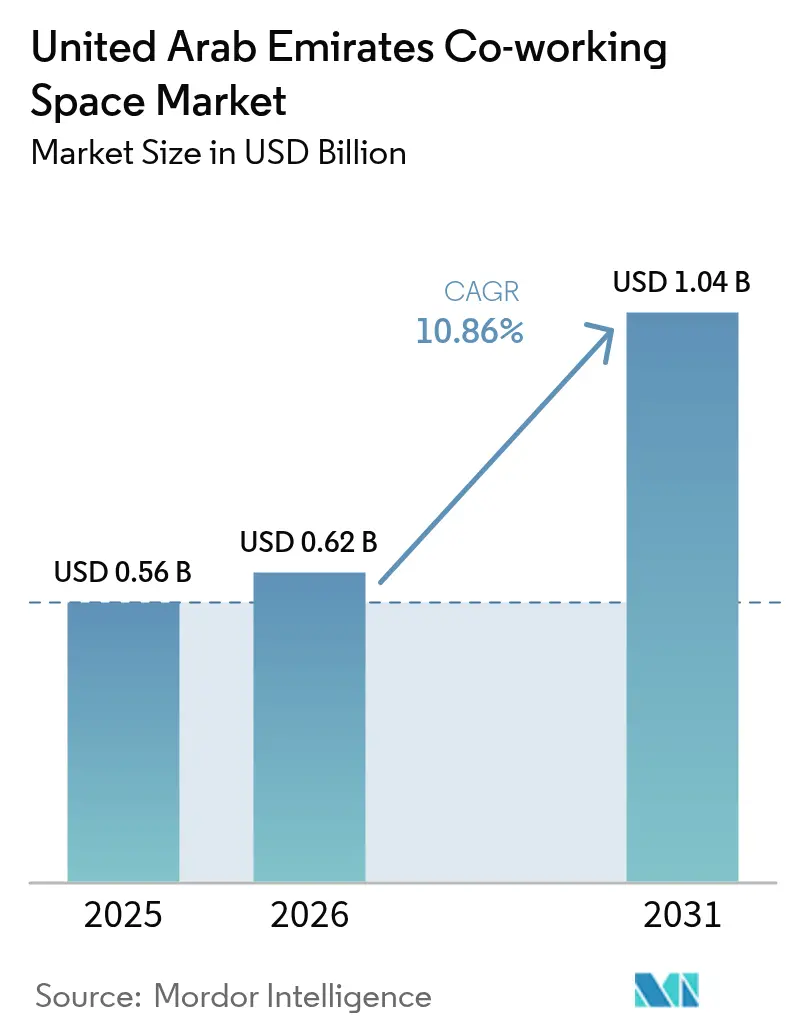

| Base Year Market Size (2025) | USD 0.56 Billion |

| Market Size (2026) | USD 0.62 Billion |

| Market Size (2031) | USD 1.04 Billion |

| Growth Rate (2026 - 2031) | 10.86% CAGR |

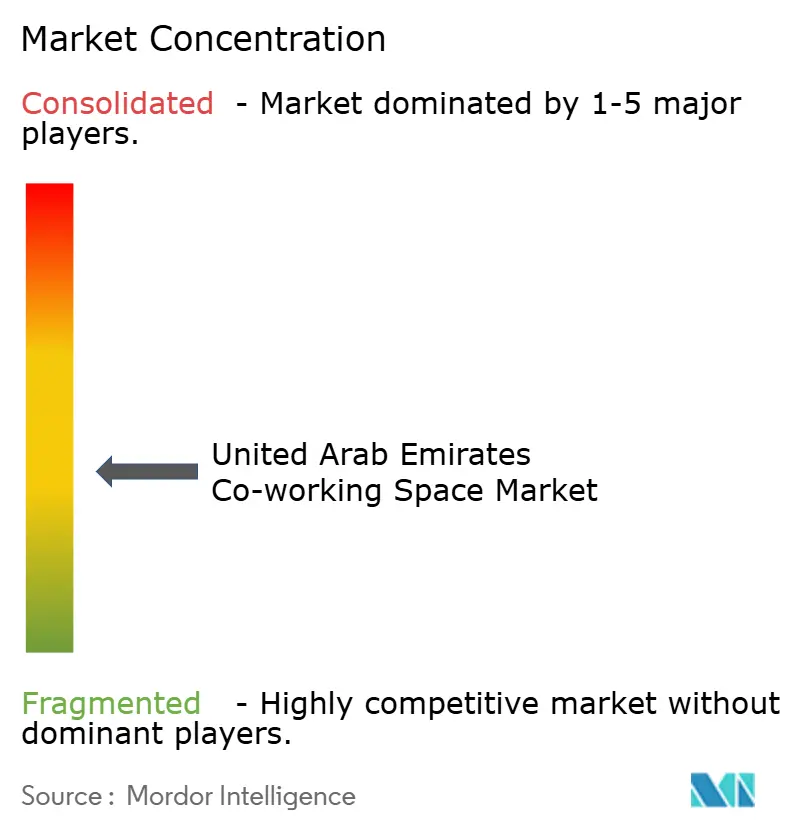

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Co-working Space Market Analysis by Mordor Intelligence

The UAE co-working office space market size was valued at USD 0.56 billion in 2025 and estimated to grow from USD 0.62 billion in 2026 to reach USD 1.04 billion by 2031, at a CAGR of 10.86% during the forecast period (2026-2031). This solid growth trajectory mirrors the nation’s economic diversification push, rising foreign direct investment, and a policy environment that views flexible workspaces as indispensable to entrepreneurial dynamism. Government programs such as Operation 300bn—aimed at lifting industrial GDP contribution to USD 81.6 billion—feed a stable pipeline of small and mid-sized enterprises that prefer flexible leases over conventional offices. International operators are reinforcing this momentum by entering asset-light partnerships with local landlords, while premium community-driven hubs cater to affluent digital nomads drawn by the Golden Visa program. Rents, although rising sharply (22% in Dubai; 11% in Abu Dhabi), have not yet stifled demand, but they are provoking a bifurcation between cost-conscious start-up spaces and enterprise-grade centers. The UAE co-working office space market, therefore, sits at the crossroads of rapid demand growth and evolving pricing dynamics, creating both opportunity and competitive intensity[1]Emirates News Agency, “UAE to Raise Industrial GDP Contribution to AED 300 Billion by 2031,” wam.ae.

Key Report Takeaways

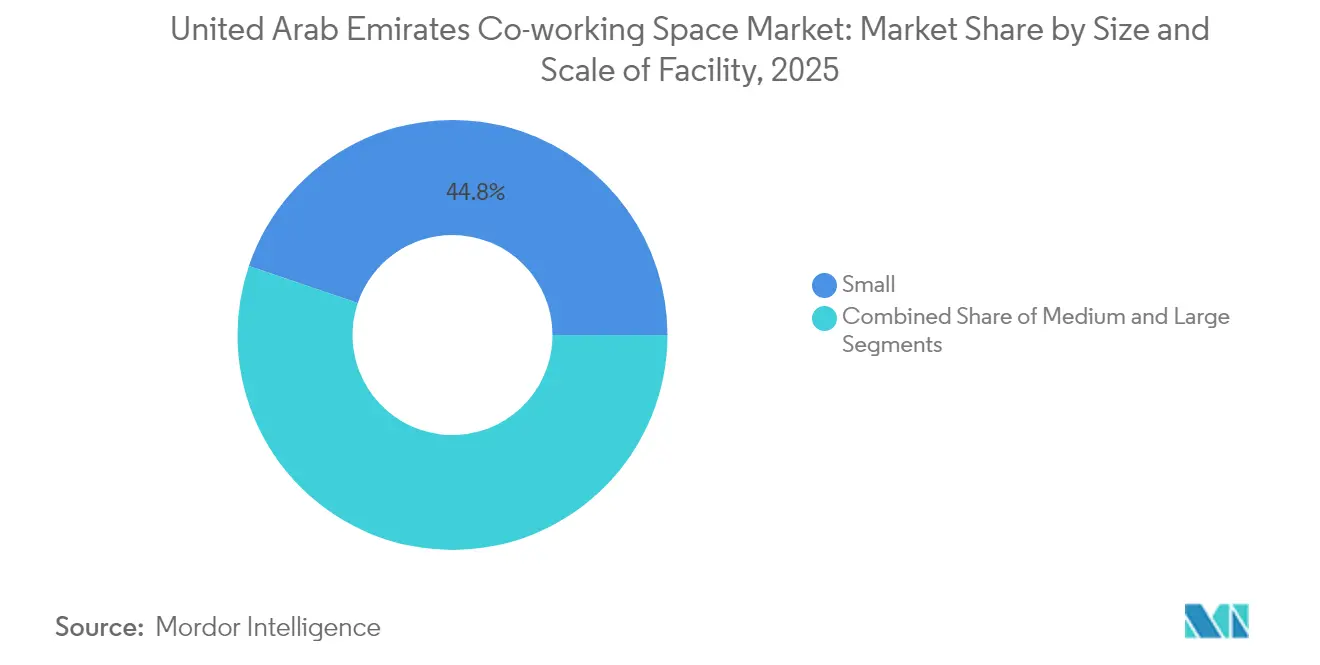

- By size of facility, small spaces captured 44.80% of the UAE co-working office space market share in 2025, while large facilities are projected to post an 11.70% CAGR through 2031.

- By sector, IT and ITES held 38.15% of the UAE co-working office space market size in 2025; BFSI is set to grow at a 11.92% CAGR to 2031.

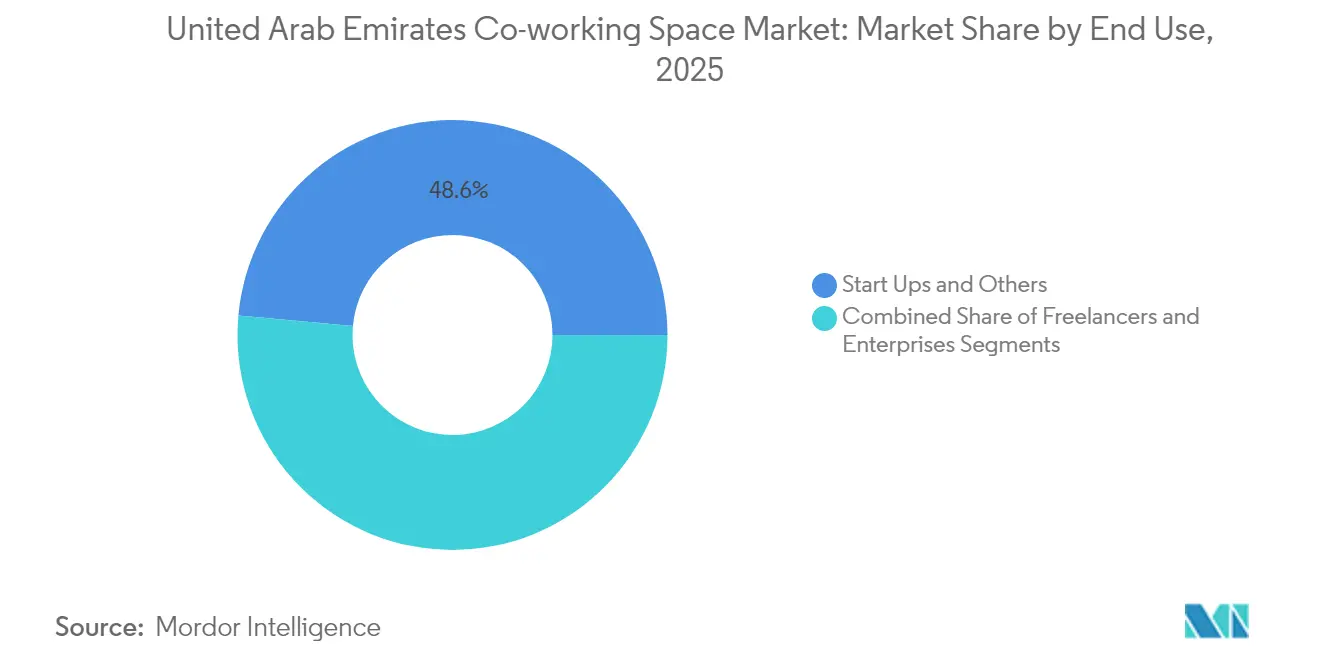

- By end use, start-ups commanded 48.55% share of the UAE co-working office space market in 2025, whereas enterprises represent the fastest-growing user group with a 12.06% CAGR.

- By city, Dubai led with a 68.65% slice of the UAE co-working office space market share in 2025; Abu Dhabi is advancing at a 12.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Co-working Space Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entrepreneurship & SME growth under diversification | +3.1% | National, concentrated in Dubai & Abu Dhabi | Long term (≥ 4 years) |

| Government-backed free zones & innovation districts | +2.8% | Dubai, Abu Dhabi, spillover to Sharjah | Medium term (2-4 years) |

| International operators’ rapid footprint expansion | +2.2% | Dubai & Abu Dhabi core markets | Short term (≤ 2 years) |

| Freelancer & start-up demand for serviced workspaces | +1.9% | National, Dubai leading adoption | Medium term (2-4 years) |

| Premium community-driven hubs for high-value users | +1.4% | Dubai & Abu Dhabi premium districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Diversification Accelerates Professional-Services Clustering

The UAE is witnessing a significant transformation as it diversifies its economy and reduces reliance on hydrocarbons. As the UAE's economy pivots away from hydrocarbons, knowledge services are taking the spotlight. With "Operation 300bn" aiming to empower 13,500 SMEs, there's a noticeable uptick in legal, accounting, and consulting activities, predominantly funneled into flexible office spaces. Highlighting the trend, the Ministry of Investment reported a significant USD 30.7 billion in FDI for 2023, emphasizing the need for robust local support teams. Notably, each new business registration often brings along two to three ancillary service providers, further driving up workspace demand. With ambitious targets set for the digital economy—aiming for 20% of the non-oil GDP by 2030—the demand for collaborative and tech-driven environments intensifies. This trend bodes well for the long-term growth of the UAE's co-working office space market.

Government-Backed Free Zones Drive Infrastructure-Led Growth

Government-backed free zones in the UAE are playing a pivotal role in driving infrastructure-led growth. Dubai Internet City and ADGM, two prominent free zones, have integrated co-working facilities into their blueprints, offering seamless solutions for businesses seeking both onshore and offshore operations. A recent resolution from the Dubai Executive Council, Resolution No. 11 of 2025, expands the potential clientele by allowing firms in free zones to obtain mainland licenses while still enjoying tax benefits. Additionally, ADGM's relocation to Al Reem Island comes with incentives, providing fee waivers to early adopters and thus reducing their workspace expenses. Such strategic policy adjustments not only attract companies prioritizing regulatory transparency and swift market entry but also set a precedent as other zones begin to adopt this blended approach. Consequently, the UAE's co-working office space market is witnessing a surge in demand, bolstered by these government-endorsed initiatives.

International Operators Leverage Capital-Light Expansion Models

Global brands are increasingly adopting innovative strategies to expand their presence in competitive markets. Global brands are expanding their footprint in Dubai, leveraging management contracts and franchising. This approach not only mitigates real-asset risks but also capitalizes on Dubai's impressive 92% office occupancy rate. In the first half of 2024, IWG inaugurated 306 new sites, generating a robust USD 2.1 billion in revenue. Meanwhile, local developer TECOM committed a substantial USD 462.4 million in 2024-2025, retrofitting properties to cater to the burgeoning demand for managed co-working spaces. With just 100,000 m² of new Grade-A office space set to debut in 2025—most of which is already pre-leased—these asset-light operators are wielding significant negotiating power. This advantage allows for swift deployments in areas with limited supply and provides a buffer against rising rental costs.

Premium Community-Driven Hubs Target High-Value Demographics

The co-working office space market in the UAE is witnessing a shift towards premium, community-driven hubs targeting high-value demographics. New lifestyle-centric hubs are emerging, catering to digital nomads and executives with Golden Visas. At TECOM’s D/Quarters, a private office goes for USD 1,224 monthly, inclusive of mentorship programs and sector-specific events. These hubs, often nestled in media and tech districts, seamlessly integrate leisure amenities with workspaces, promoting peer-to-peer learning. The National highlights Dubai and Abu Dhabi as prime spots for executive nomads, attracting a clientele that values experience over cost. This trend of premiumization is injecting higher margins into the UAE's co-working office market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium rental pricing limits early-stage start-ups | -1.8% | Dubai & Abu Dhabi prime districts | Short term (≤ 2 years) |

| Limited penetration in secondary emirates | -1.2% | Sharjah, Ajman, Ras Al Khaimah, Fujairah, UAQ | Long term (≥ 4 years) |

| Volatility tied to oil & global trade cycles | -0.9% | National; Dubai trade sector most exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Rental Inflation Creates Affordability Barriers

Rising rental costs in the UAE's office market are creating significant affordability challenges. Dubai's office rents surged by 22% year-on-year, while Abu Dhabi saw an 11% uptick. Co-working operators grapple with a tough choice: absorb rising costs or pass them onto tenants. While early-stage ventures enjoy a 0% corporate tax on earnings below AED 3 million, they find their budgets increasingly strained by workspace expenses. With supply shortages pushing occupancies to a projected 94% by the end of 2025, operators find it harder to negotiate favorable lease terms. As a result, a two-tier market is taking shape: premium centers attract established enterprises, while smaller start-ups are either downsizing or relocating to less central areas.

Geographic Concentration Limits Market Penetration

The geographic concentration of co-working spaces in the UAE poses challenges to market penetration. Dubai commands a dominant 69.3% share of the UAE's co-working office space market, with Abu Dhabi securing the majority of the remaining portion. While secondary emirates offer lower rents, their lack of robust business ecosystems and international connectivity has dampened operator interest. Compounding this challenge, visa regulations stipulate one visa per 9 m², creating hurdles in areas where economies of scale are limited. The heavy reliance on just two cities amplifies risk; any disruptions to Dubai's trade flows or shifts in Abu Dhabi's public-sector spending could send ripples throughout the national market. Although venturing into Sharjah or Ras Al Khaimah presents an opportunity for diversification, significant infrastructure gaps remain a deterrent for major players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Small Spaces Sustain Volume While Large Sites Accelerate Value Capture

Small co-working facilities held 44.80% of the UAE co-working office space market share in 2025, cementing their role as the entry point for budget-sensitive start-ups and freelancers. Their low build-out costs and neighborhood-level footprints allow rapid deployment, matching the quick-cycle nature of early-stage company formation. Visa quotas tied to office size also nudge micro firms toward compact suites. Medium-sized centers bridge simplicity and sophistication, often clustering around academic campuses and secondary commercial corridors.

Large facilities, although representing a smaller slice today, are registering the fastest 11.70% CAGR through 2031 because they satisfy the workspace, data-security, and branding needs of multinational clients. TECOM’s Innovation Hub Phase 3, adding 167,000 ft² of premium stock, illustrates how developers are designing contiguous floors that house co-working zones adjacent to anchor tenants. As enterprises embrace hybrid models, demand for flexible yet corporate-grade environments is swelling. This shift moves the UAE co-working office space market further up the value curve, enhancing average revenue per occupied desk.

By Sector: IT and ITES Remain the Cornerstone Amid BFSI Upsurge

The IT and ITES vertical accounted for 38.15% of the UAE co-working office space market size in 2025, reflecting the nation’s digital-economy roadmap and deep talent pool. Software developers, cloud-service integrators, and fintech start-ups favor plug-and-play offices that can scale headcount on short notice. These firms also appreciate the robust internet backbone and proximity to venture-capital networks concentrated in Dubai Internet City.

Banking, financial services, and insurance tenants are the fastest-growing cohort, clocking a 11.92% CAGR through 2031 as DIFC expands and ADGM’s regulatory sandbox welcomes Web3 ventures. Co-working providers now reserve entire floors for privacy-compliant meeting suites and secure data rooms to court these clients. Professional-services outfits—legal, HR, and accounting—round out demand as SME formation accelerates. Collectively, sector diversification shields the UAE co-working office space market from single-industry shocks.

By End Use: Start-Up Core Underpins Rapid Enterprise Uptake

Start-ups occupied 48.55% of the UAE co-working office space market share in 2025, undergirding the ecosystem with a constant churn of new ideas and teams. Government fee waivers, simplified licensing, and a USD 544 million Web3 fund have drawn founders who value flexibility over square footage. Many choose smaller desks at inception but graduate to private suites within the same facility, smoothing operator retention metrics.

Enterprises, however, are expanding fastest at 12.06% CAGR as multinational relocations follow the 0% corporate-tax incentive for qualifying free-zone businesses. Fortune 500 entrants often adopt co-working spaces as touchdown offices before committing to long leases, testing market fit and talent availability. Freelancers and digital nomads form a stable niche, buoyed by long-term visas that anchor them in the Emirates’ lifestyle hubs. The mix of users diversifies revenue streams and drives product innovation in the UAE co-working office space market.

Geography Analysis

In 2025, Dubai holds a significant 68.65% share of the UAE's co-working office space market, supported by strong air connectivity, a well-developed free-zone network, and robust business activity. Occupancy rates exceed 92%, while limited new supply sustains high prices, raising affordability concerns for new businesses. To address growing demand, particularly in the Downtown and Dubai Marina areas, landlords are increasingly forming asset-light partnerships with global operators.

Abu Dhabi is a strong competitor, with a projected 12.18% CAGR growth rate through 2031. The emirate's policies, including zero tax on qualifying income, a focus on the financial sector, and the Hub71+ initiative with a USD 544 million investment in digital assets, create a favorable environment for tenants in FinTech, Web3, and advanced manufacturing. Additionally, the mandatory relocation of firms to the ADGM’s Al Reem Island campus is driving both short-term and long-term demand for co-working spaces. This planned growth diversifies national exposure and provides scale advantages for operators managing spaces in both capitals.

Secondary emirates such as Sharjah and Ras Al Khaimah currently account for a smaller share but have growth potential as infrastructure improvements progress. Sharjah's lower rental costs and proximity to major academic institutions attract creative and research-focused startups. However, limited international flight connectivity and smaller client bases pose challenges to rapid expansion. Operators entering these markets will need to implement tailored community programs and collaborate with local municipal authorities to ensure sustainable occupancy, contributing to the broader development of the UAE's co-working office space market.

Competitive Landscape

Competition in the market is moderate but is gradually moving towards consolidation as international and domestic players refine their strategies. Global brands such as IWG, WeWork, and The Executive Centre are adopting managed partnerships to mitigate real-asset risks. IWG, for instance, added 306 sites in the first half of 2024 and reported a record revenue of USD 2.1 billion. Local players like TECOM’s D/Quarters and Astrolabs are leveraging their cultural understanding and specialized services—such as coding bootcamps and fintech accelerators—to build strong tenant communities.

Technology integration has become a key focus area. Operators are utilizing IoT sensors for space optimization, AI for predictive maintenance, and mobile applications to provide seamless access. These advancements align with the UAE’s goal of generating 20% of its non-oil GDP from the digital economy by 2030. Providers that deliver measurable productivity improvements for tenants are able to justify premium pricing, even as rents increase.

Niche differentiation is also accelerating. Lifestyle-focused hubs featuring wellness zones and networking lounges are appealing to high-net-worth digital nomads, while centers in secondary emirates emphasize affordability and relaxed regulatory frameworks. M&A activity is expected to increase as smaller independent operators either expand through franchising or are acquired by larger chains. At present, the UAE co-working office space market offers a wide variety of formats. However, as brand awareness and user expectations grow, the market is likely to experience medium-term consolidation, favoring operators with strong performance and comprehensive amenities[3]U.S. Department of Commerce, “UAE Digital Economy Strategy Overview,” trade.gov.

United Arab Emirates Co-working Space Industry Leaders

IWG (Regus, Spaces)

WeWork

The Executive Centre

Servcorp

Astrolabs

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: TECOM Group bought Office Park in Dubai Internet City for USD 195.8 million, adding 370,761 ft² of leasable space that is already 88% occupied and generates more than USD 16.3 million in annual rent.

- August 2024: The company announced a USD 544 million spending plan that covers new acquisitions and the USD 92.5 million Innovation Hub Phase 3 at Dubai Internet City, while two fully let buildings were secured for USD 114.2 million, expanding its portfolio by 501,000 ft².

- August 2024: TECOM also set aside an additional USD 462.4 million for projects aimed at widening its flexible-workspace footprint across the Emirates, signaling firm confidence in co-working demand.

- June 2024: Abu Dhabi Global Market launched Hub71+ Digital Assets, a regulated Web3 ecosystem backed by more than USD 2 billion that features dedicated co-working space for start-ups seeking global scale.

United Arab Emirates Co-working Space Market Report Scope

Co-working spaces refer to working arrangements in which people from different teams and companies come together to work in a single shared space. Co-working space is characterized by shared facilities, services, and tools. Sharing infrastructure in this way helps spread the cost of running an office across members. The UAE co-working space market size indicates the revenue generated by co-working space companies in the country.

The report covers a complete background analysis of the UAE co-working space market, which includes an assessment of the sector and contribution of the sector to the economy, market overview, market size estimation for key segments, key developments and emerging trends in the market segments, market dynamics, and key statistics.

The UAE co-working space market is segmented by type (new spaces, expansions, and chains), by application (information technology [IT and ITES], legal services, BFSI, consulting, and other services), end user (small to medium-sized enterprises [SMEs] and large-scale corporations), and geography (Abu Dhabi, Dubai, Sharjah, and Other Cities). The report offers the market size and forecasts in value (USD million) for all the above segments.

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By City

| Dubai |

| Abu Dhabi |

| Sharjah |

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, UAQ) |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By City | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, UAQ) |

Key Questions Answered in the Report

How large is the UAE co-working office space market today?

The market reached USD 0.62 billion in 2026 and is projected to hit USD 1.04 billion by 2031.

Which city hosts the majority of co-working demand?

Dubai held 68.65% of occupied co-working space in 2025, benefitting from dense free-zone clusters and high business-registration volumes.

What is driving enterprise adoption of flexible offices in the Emirates?

Multinationals value the 0% tax regime for qualifying free-zone income and use co-working hubs to test market potential before signing long leases.

Are rising rents likely to slow sector growth?

While premium rents climbed 22% in Dubai, demand remains resilient, prompting operators to explore secondary locations and asset-light models.

Which user segment is expanding the fastest?

Enterprises show the quickest trajectory, advancing at a 12.06% CAGR as large corporates integrate flexible space into hybrid work strategies.

How are international brands entering the UAE market?

Global operators favor management agreements and franchising, allowing rapid scale-up without heavy capital outlays in a tight real-estate market.

Page last updated on: