Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

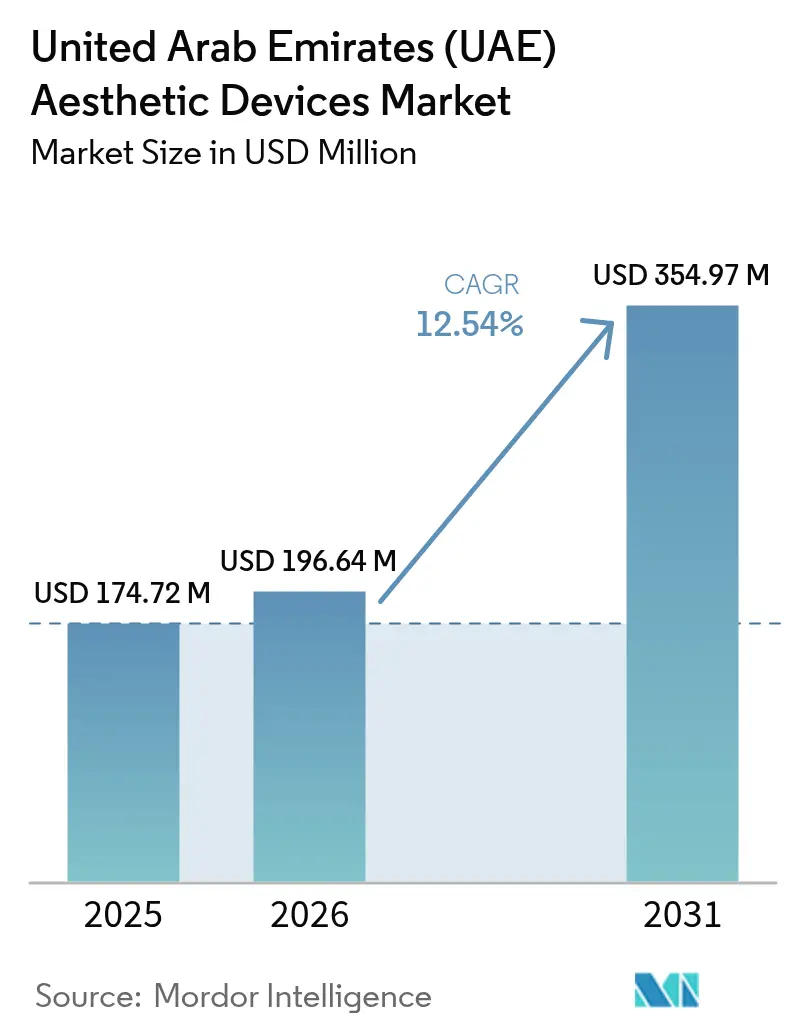

| Base Year Market Size (2025) | USD 174.72 Million |

| Market Size (2026) | USD 196.64 Million |

| Market Size (2031) | USD 354.97 Million |

| Growth Rate (2026 - 2031) | 12.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates (UAE) Aesthetic Devices Market Analysis by Mordor Intelligence

The United Arab Emirates Aesthetic Devices Market size is expected to grow from USD 174.72 million in 2025 to USD 196.64 million in 2026 and is forecast to reach USD 354.97 million by 2031 at 12.54% CAGR over 2026-2031.

This rapid expansion reflects the country’s emergence as the Middle East’s premier medical tourism center, where luxury hospitality and cutting-edge technology converge to attract both domestic and international patients. Growth is propelled by rising procedure volumes, favorable Golden Visa reforms, and high disposable incomes that encourage discretionary spending on cosmetic enhancements. A concurrent regulatory overhaul, led by the new Emirates Drug Establishment, streamlines device approvals, while device-leasing models lower upfront costs for clinics and accelerate technology adoption. Intensifying competition among global brands and local distributors further stimulates innovation, particularly in energy-based platforms that address demand for minimally invasive solutions.

Key Report Takeaways

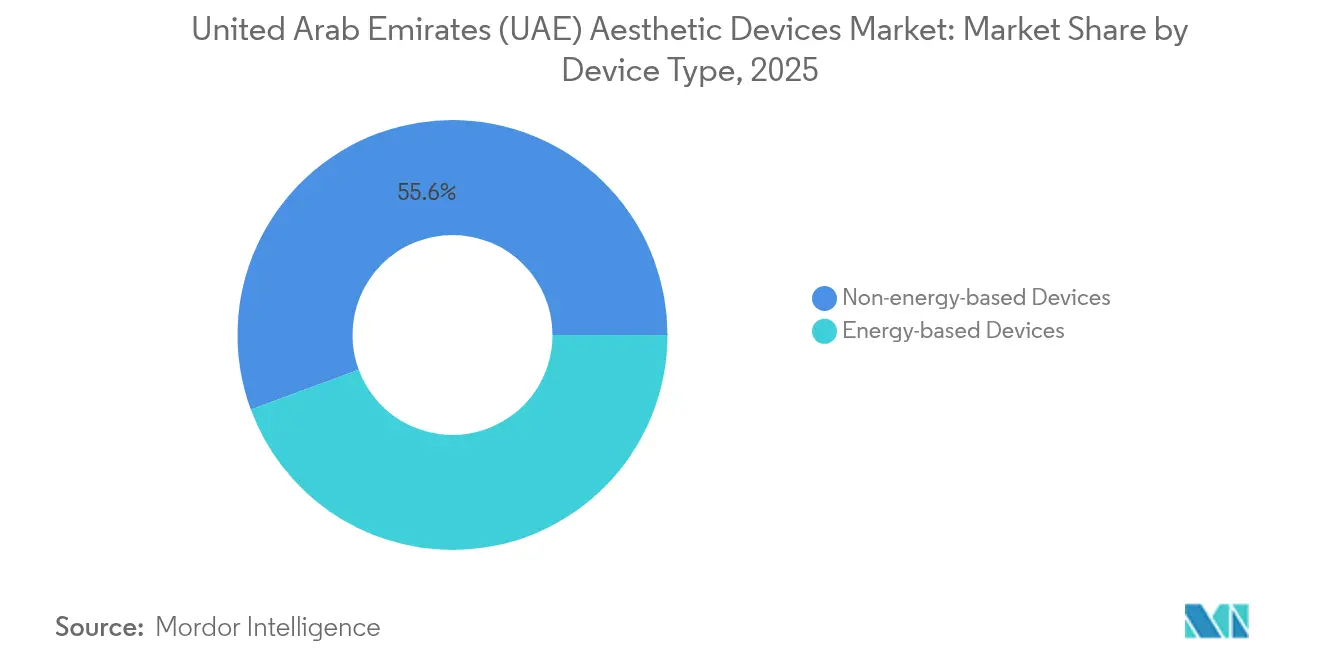

- By device type, non-energy-based systems held 55.63% of the UAE aesthetic devices market share in 2025. Radio-frequency platforms are projected to post the fastest 17.38% CAGR through 2031.

- By application, skin resurfacing and tightening accounted for a 32.58% revenue share in 2025. Body contouring and cellulite reduction are on track to expand at a 15.89% CAGR between 2026 and 2031.

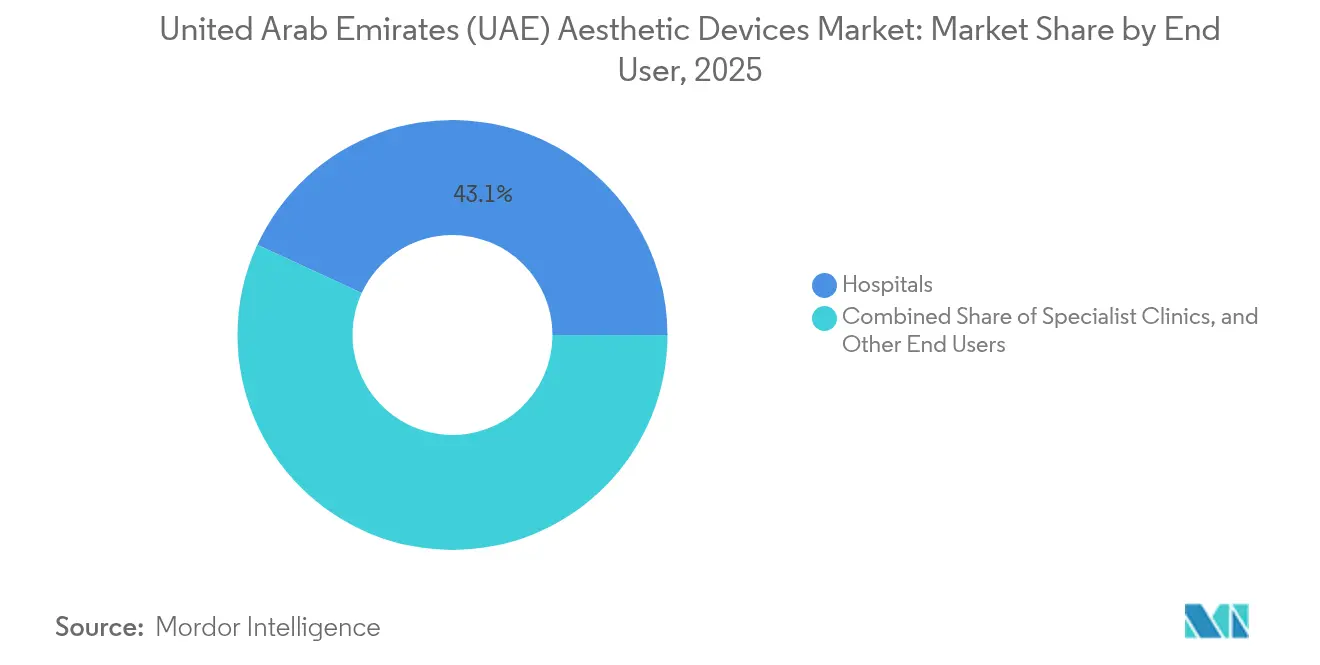

- By end user, hospitals retained a 43.11% share of the UAE aesthetic devices market size in 2025, while specialist and multi-specialty clinics are expected to record a 14.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates (UAE) Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming Inbound Medical Tourism | +3.2% | Dubai Healthcare City, Abu Dhabi medical zones | Long term (≥ 4 years) |

| Rising Volume of Cosmetic Procedures | +2.8% | UAE nationwide, concentrated in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Device-Leasing Models Lowering CAPEX for Clinics | +2.1% | UAE nationwide, particularly smaller clinics | Short term (≤ 2 years) |

| Rising Disposable Income of UAE Residents | +1.9% | UAE nationwide, higher impact in Northern Emirates | Medium term (2-4 years) |

| Golden Visa Reforms Boosting Wellness Stays | +1.5% | Dubai, Abu Dhabi premium healthcare districts | Long term (≥ 4 years) |

| AI-Driven Patient Acquisition & Tele-Consults | +1.1% | Dubai, Abu Dhabi tech-forward facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Inbound Medical Tourism

The country attracted 691,000 medical tourists in 2023, with a sizeable portion seeking aesthetic care.[1]Ministry of Economy UAE, “Golden Visa for Investors,” moec.gov.ae Dubai Healthcare City issues specialized medical visas that streamline cross-border patient access. A government commitment to spend AED 112.7 billion on healthcare infrastructure by 2027 enhances supply capacity. Premium facilities, such as American Hospital Dubai and Aesthetics by King’s, offer market-integrated hotel-clinic experiences, reinforcing the UAE as a luxury destination for aesthetic devices. International patients expect state-of-the-art equipment, prompting providers to invest heavily in new platforms that justify premium pricing. Continued medical-tourism inflows stabilize revenue streams and elevate equipment refresh cycles to maintain brand reputations.

Rising Volume of Cosmetic Procedures

Procedure counts in Dubai doubled between 2022 and 2024, as social media visibility, wellness culture, and expanding male participation increased overall demand. Male patients accounted for 47% of interventions in 2024, narrowing a historical gender gap and broadening the patient base. Expenditure on surgical and nonsurgical services reached AED 300 million, underpinned by one of the world’s highest plastic-surgeon densities per capita. Treatment mix shifts toward body-contouring options instead of facial surgeries, mirroring consumer priorities for rapid results with minimal downtime. Higher procedure throughput directly increases the utilization of injectables, lasers, and emerging radio-frequency devices, sustaining long-term procurement cycles for clinics that must refresh their technology to remain competitive.

Device-Leasing Models Lowering CAPEX for Clinics

Small and mid-sized clinics face cost barriers when purchasing capital-intensive laser or radio-frequency systems. Flexible leasing structures spread expenses over multiyear terms, allowing operators to diversify service menus without large upfront outlays. Vendors lock in predictable revenue streams, while clinics boost patient volumes by advertising access to cutting-edge technologies, reinforcing the overall ecosystem’s growth momentum.

Rising Disposable Income of UAE Residents

Economic diversification and Golden Visa initiatives attract high-net-worth individuals, expanding the domestic clientele for aesthetic services.[2]My 1Health, “Best Countries for Medical Tourism Partnerships in 2025,” my1health.com The aesthetic medicine segment is growing at a rate of 10% annually, as evidenced by Aster Hospitals’ reported uptick in skincare, dental aesthetics, and injectables. Residents value on-demand treatments that align with lifestyle aspirations of perpetual youth, fostering regular repeat visits for botulinum toxin or dermal filler top-ups. Clinics respond by purchasing premium devices that deliver faster results, fueling vendor pipelines and sparking competitive pricing among suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Insurance Reimbursement | -2.3% | UAE nationwide | Long term (≥ 4 years) |

| Social Stigma Among Conservative Sub-Populations | -1.8% | UAE nationwide, varying by emirate | Medium term (2-4 years) |

| Shortage of Board-Certified Aesthetic Physicians | -1.5% | UAE nationwide, acute in Northern Emirates | Short term (≤ 2 years) |

| Regulatory Approval Delays for Novel Devices | -0.9% | UAE federal level | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Insurance Reimbursement

Most aesthetic procedures remain elective and are excluded from health insurance plans, leading to out-of-pocket costs ranging from USD 5,000 to USD 50,000. Financing schemes help, but do not fully bridge affordability gaps for middle-income residents. Hospital procurement decisions often rely on insured volumes, so the absence of reimbursement shifts provider focus toward affluent clients and may restrict device rotation in public facilities.

Social Stigma Among Conservative Sub-Populations

While acceptance is rising, pockets of conservative sentiment still associate cosmetic enhancement with vanity, curbing demand in some communities.[3]Nick Webster, “Demand for Plastic Surgery Doubles in Dubai as Tech Dependence Takes Its Toll,” The National, thenationalnews.com Geographic disparities persist, with Dubai and Abu Dhabi showing the highest uptake compared with the Northern Emirates. Educational campaigns and influencer endorsements are gradually normalizing treatments as a form of preventive self-care. Clinics tailor their marketing to emphasize safety and wellness, rather than beauty alone, thereby mitigating cultural resistance over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Platforms Sustain Leadership Amid RF Upswing

The UAE aesthetic devices market size for non-energy systems held a 55.63% share in 2025, underscoring the popularity of injectables and micro-cannula delivery kits. The consistent appeal of botulinum toxin and dermal fillers keeps demand steady, thanks to their immediate visible outcomes and low downtime. Clinics bundle injectable sessions with adjunct treatments such as LED masks, creating cross-selling opportunities that strengthen supplier relationships.

Energy-based technologies collectively register faster growth, with radio-frequency equipment forecast to expand at a 17.38% CAGR through 2031. Consumers respond positively to the non-surgical skin-tightening and body-shaping effects. Vendors capitalize on this trend by integrating real-time temperature monitoring to enhance safety. Laser platforms maintain relevance for hair removal across mixed-phototype populations, while IPL devices gain adoption for pigment issues common in sun-exposed climates. Ultrasound-based lipolysis and cryolipolysis machines capture niche demand among patients unwilling to undergo invasive liposuction, and plasma-based devices find traction for eyelid rejuvenation. The Emirates Drug Establishment’s stringent but efficient certification process supports clinician confidence and promotes continued diversification within the UAE aesthetic devices market.

In the medium term, leasing programs enable smaller practices to experiment with multi-modal workstations that combine RF, ultrasound, and pulsed light. Suppliers differentiate by offering operator training and predictive maintenance, ensuring 24/7 uptime that aligns with consumer expectations for same-day appointments. As energy-based adoption expands, non-energy treatments will coexist rather than be displaced, creating complementary revenue streams for providers seeking to offer comprehensive aesthetic solutions.

By Application: Body Contouring Gains Momentum Beyond Facial Focus

Skin resurfacing and tightening accounted for 32.58% of revenues in 2025, reflecting the climatic need for photodamage repair and collagen stimulation. Fractional laser, RF microneedling, and plasma resurfacing deliver visible texture improvements, anchoring many clinic service menus. Demand remains high among residents seeking rejuvenation without extended social downtime, with packages often bundled into annual skincare memberships that secure recurring traffic.

Body contouring and cellulite reduction will outpace all other indications at a 15.89% CAGR. The rise of gym culture, exposure to global beauty standards, and social media visibility encourage consumers to pursue sculpted silhouettes. Non-invasive fat-reduction devices, such as cryolipolysis and high-intensity focused electromagnetic systems, appeal to time-pressed professionals. Providers invest in complementary shock-wave platforms that improve lymphatic drainage and amplify lipolysis results, boosting cumulative revenues.

Hair-removal services maintain their resilience because cultural norms favor smooth skin, and the country’s year-round warm climate makes beachwear a common choice. Laser and IPL technologies enjoy broad appeal across genders and phototypes, with diode and alexandrite systems frequently cited for high throughput. Tattoo and pigmentation-removal procedures are on the rise as body-art norms evolve; improved Q-switch laser speeds shorten treatment courses, increasing affordability. Acne and scar management benefits from advancements in blue-light therapy and RF microneedling, while demand for breast augmentation devices grows selectively among younger expatriates. Collectively, these applications cement the UAE aesthetic devices market as a destination for head-to-toe enhancement solutions.

By End User: Clinics Widen Lead with Agile Business Models

Hospitals held a 43.11% revenue share in 2025, supported by integrated surgical theaters, postoperative care units, and established regulatory oversight that ensures safety-focused patient care. Many houses have dedicated cosmetic wings offering both surgical and nonsurgical options, leveraging cross-specialty referrals from dermatology, bariatric surgery, and dentistry. These institutions typically negotiate volume-based purchase agreements that secure favorable pricing for consumables and high-end lasers.

Specialist and multi-specialty clinics, however, are set to record a 14.67% CAGR through 2031 as they benefit from boutique service environments, flexible operational hours, and marketing agility. New entrants position clinics inside premium malls and upscale neighborhoods, reducing patient travel time and integrating aesthetic treatments into routine lifestyle errands. Clinic operators adopt subscription plans and loyalty programs, fostering predictable cash flow that supports rapid device upgrades. Consolidation trends, such as Medcare’s 60% stake acquisition in Skin111 Clinics, illustrate how networks achieve economies of scale in procurement and branding.

Other providers include dermatology offices and wellness centers that combine functional medicine, weight-loss coaching, and aesthetic add-ons. These settings favor compact, multimodal devices that maximize floor-space efficiency. Vendor training programs ensure safe operation even for general practitioners expanding into aesthetics, further enlarging the UAE aesthetic devices market user base.

Geography Analysis

Dubai and Abu Dhabi account for more than two-thirds of spending within the UAE aesthetic devices market, thanks to their world-class airports, luxury hospitality, and concentrated wealth. Medical tourists arriving via Dubai International Airport often schedule treatments during extended leisure stays, enabling clinics to bundle procedure packages with hotel accommodations. Dubai Healthcare City’s specialized zoning facilitates one-stop licensing, attracting international brands that prefer turnkey setups. Regulatory clarity, combined with high digital-payment penetration, expedites patient onboarding and device monetization.

Abu Dhabi’s Department of Health operates a Technology Registry that evaluates the safety, efficacy, and cost-effectiveness of capital equipment before approval, providing providers with transparent criteria that encourage early adoption. The emirate’s focus on smart hospitals supports integration of AI-enabled robotics in hair transplantation and laser guidance systems. Government co-investment initiatives reduce financial risk for early pilots, thereby accelerating the diffusion of energy-based platforms across public-private partnerships.

The Northern Emirates, including Sharjah, Ras Al Khaimah, and Fujairah, currently have lower penetration but offer significant greenfield potential. Growing industrial clusters and rising middle-income segments create untapped demand for mid-priced treatments. Mobile aesthetic units and franchised clinic chains explore these areas, frequently adopting pay-per-use device models to test market response. Over time, infrastructure upgrades and physician recruitment incentives are expected to narrow regional disparities, expanding the overall UAE aesthetic devices market footprint.

Strategically, the country’s position between Europe, Asia, and Africa enables manufacturers to use the UAE as a re-export hub. Warehousing units in Jebel Ali Free Zone cut lead times for deliveries across the Gulf, East Africa, and South Asia. Partnerships such as Cynosure-Lutronic’s distribution deal with Amico Aesthetics illustrate how global brands leverage local expertise for rapid scale-up, reinforcing the nation’s role as an innovation gateway for aesthetic technology.

Competitive Landscape

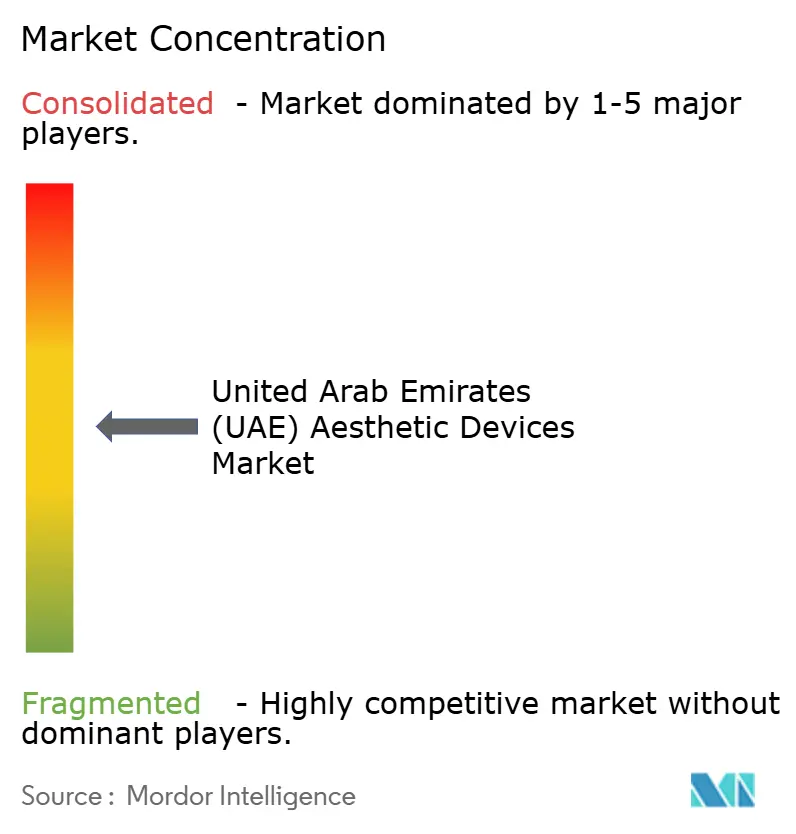

The UAE aesthetic devices market shows moderate concentration. AbbVie (Allergan Aesthetics) dominates injectables, while Candela, Cynosure, Lumenis, and InMode lead various energy-based categories. Strategic differentiation focuses on multi-modality workstations and consumable ecosystems that lock providers into proprietary supply chains. High margins entice new entrants, yet stringent Emirates Drug Establishment requirements act as quality filters.

Recent strategy pivots include Cynosure-Lutronic’s exclusive Middle East distribution agreement, which bundles clinical training, warranty, and integrated marketing to fast-track adoption. Candela invests in local demonstration labs to provide hands-on workshops for physicians, enhancing product stickiness. Meanwhile, Galderma and Merz Aesthetics bolster their injectable franchises with companion skincare lines, extending patient life-cycle value.

Device-leasing programs gain traction, particularly among start-ups in luxury retail zones. Venus Concept offers subscription-style agreements that bundle hardware, software updates, and marketing collateral into a monthly fee, minimizing capital outlay. AI integration is the next battleground: suppliers are racing to embed real-time analytics that adjust energy settings automatically based on patient phenotype, thereby improving outcomes and documentation for medico-legal compliance. Mergers, such as CosmeSurge’s continued clinic rollout under Aster DM Healthcare, point to synergistic models where corporate capital supports aggressive footprint expansion, ensuring sustained equipment procurement.

United Arab Emirates (UAE) Aesthetic Devices Industry Leaders

Bausch Health Companies Inc. (Solta Medical)

Abbvie Inc. (Allergan PLC)

Sisram Medical (Alma Lasers)

Cynosure Inc

Candela Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Heka Trading, a prominent company specializing in medical devices, integrated healthcare solutions, and skincare products, launched its Lumenis advanced machinery in the United Arab Emirates.

- April 2024: SciBase Holding AB, a developer of augmented intelligence solutions for skin disorders, entered a strategic partnership with Al Shirawi Healthcare Solutions, a prominent distributor of medical technologies in Dubai. This collaboration will enable the availability of Nevisense to patients across the United Arab Emirates.

United Arab Emirates (UAE) Aesthetic Devices Market Report Scope

As per the scope of the report, aesthetic devices refer to all medical devices that are used for various cosmetic procedures, which include plastic surgeries, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, and skin tightening. These devices are used for beautification, correction, and improvement of the body contour.

The United Arab Emirates aesthetics devices market is segmented by product type, application, and end user. By product type, the market is segmented into energy-based aesthetic devices and non-energy-based aesthetic devices. By application, the market is segmented into skin resurfacing and tightening, body contouring and cellulite reduction, hair removal, facial aesthetic procedures, breast augmentation, and other applications. By end user, the market is segmented into hospitals, clinics, and home settings. The report offers market sizes and forecasts in terms of value (USD) for the above segments.

By Device Type

| Energy-based Devices | Laser-based |

| Light-based (IPL) | |

| Radio-frequency-based | |

| Ultrasound-based | |

| Cryolipolysis & Plasma-based | |

| Non-energy-based Devices | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Chemical Peels | |

| Microdermabrasion | |

| Implants | |

| Mesotherapy & Others |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Tattoo & Pigmentation Removal |

| Breast Augmentation |

| Acne & Scar Treatment |

| Other Applications |

By End User

| Hospitals |

| Specialist & Multi-specialty Clinics |

| Other End Users |

| By Device Type | Energy-based Devices | Laser-based |

| Light-based (IPL) | ||

| Radio-frequency-based | ||

| Ultrasound-based | ||

| Cryolipolysis & Plasma-based | ||

| Non-energy-based Devices | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Chemical Peels | ||

| Microdermabrasion | ||

| Implants | ||

| Mesotherapy & Others | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Tattoo & Pigmentation Removal | ||

| Breast Augmentation | ||

| Acne & Scar Treatment | ||

| Other Applications | ||

| By End User | Hospitals | |

| Specialist & Multi-specialty Clinics | ||

| Other End Users | ||

Key Questions Answered in the Report

What is the current value of the UAE aesthetic devices market?

It is valued at USD 196.64 million in 2026 and projected to hit USD 354.97 million by 2031.

Which device category is growing the fastest?

Radio-frequency platforms are expected to lead with a 17.38% CAGR through 2031, driven by demand for non-invasive tightening and contouring.

Why is body contouring gaining traction in the UAE?

The rising fitness culture, social media influences, and preference for minimal downtime are driving consumers toward non-invasive fat-reduction solutions.

How do Golden Visa reforms affect demand?

Long-term residency increases the base of affluent consumers who view cosmetic treatments as recurring lifestyle investments, boosting procedure volumes.

What role do specialist clinics play in market growth?

Agile clinic networks offer personalized services and adopt devices quickly, enabling a 14.67% CAGR in their segment through 2031.

Page last updated on: