Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

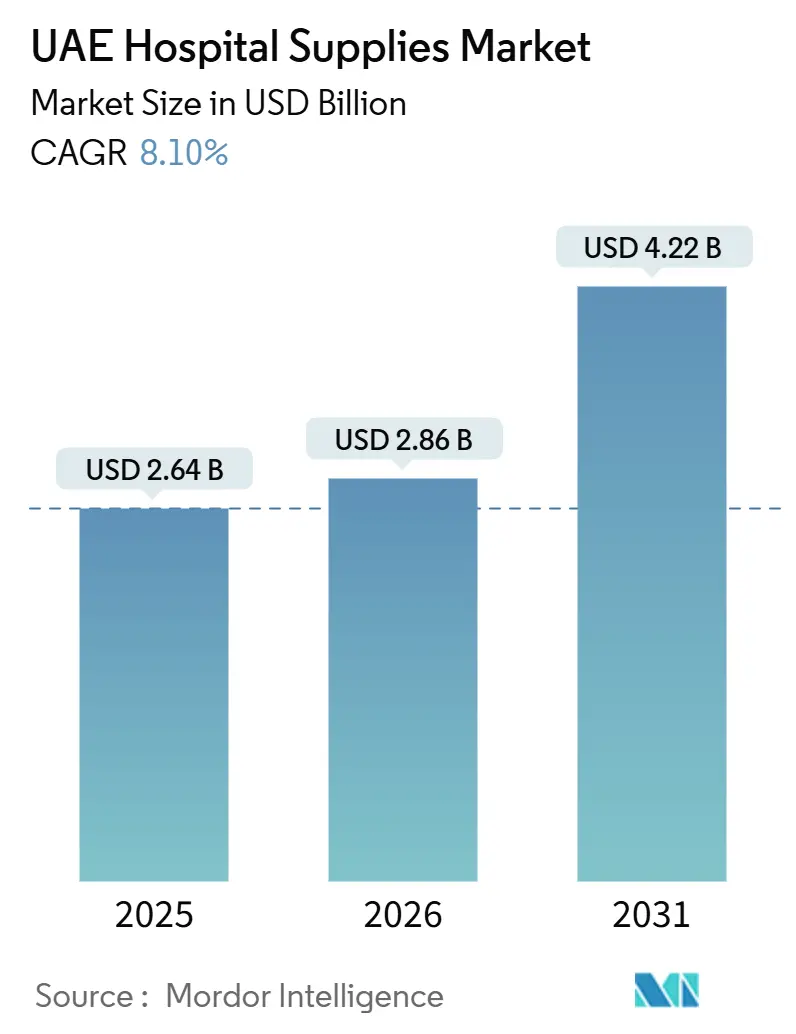

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.86 Billion |

| Market Size (2031) | USD 4.22 Billion |

| Growth Rate (2026 - 2031) | 8.10% CAGR |

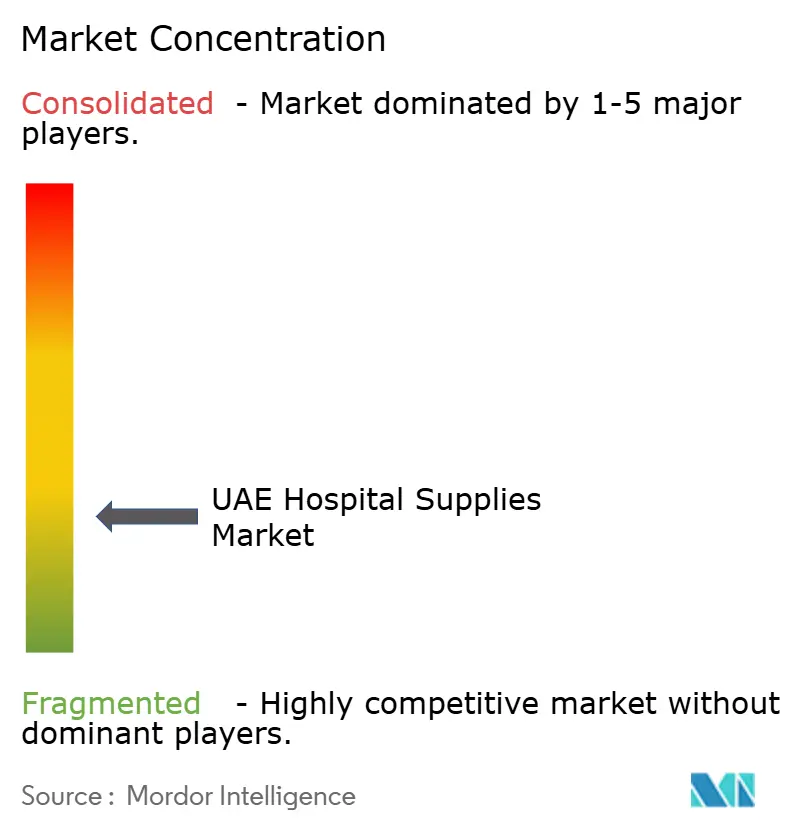

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Hospital Supplies Market Analysis by Mordor Intelligence

The UAE Hospital Supplies Market size is expected to increase from USD 2.64 billion in 2025 to USD 2.86 billion in 2026 and reach USD 4.22 billion by 2031, growing at a CAGR of 8.10% over 2026-2031.

In the UAE, sovereign capital spending, stricter infection-control regulations, and rapidly expanding digital procurement platforms are transforming how both public and private facilities procure items, ranging from single-use drapes to advanced robotic surgical consoles. A federal budget increase to AED 5.505 billion in 2025 has enabled Emirates Health Services to implement robotic pharmacies, reducing expired-stock write-offs by 18%. Despite growing demand for premium diagnostics, a centralized pricing-certificate process effectively controls cost growth. The UAE's hospital supplies market is witnessing steady growth, driven by mandatory infection-control audits, increasing medical tourism, and a shift towards home-healthcare programs.

Key Report Takeaways

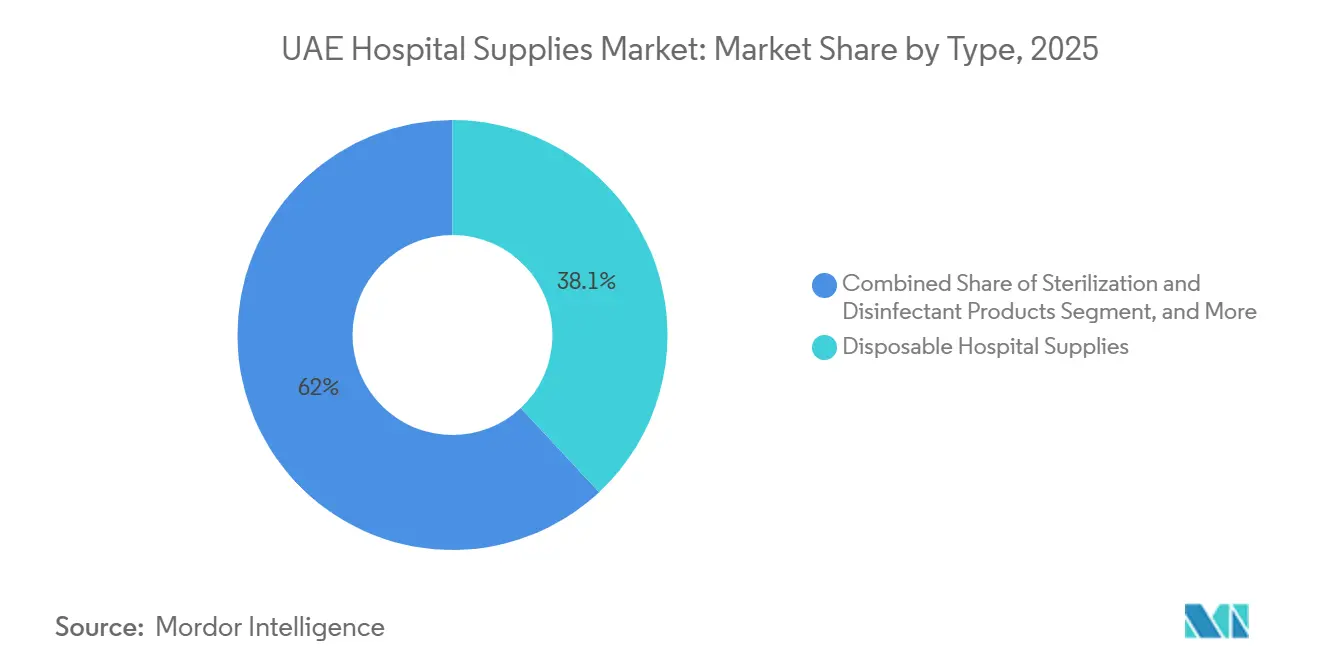

- By type, disposable hospital supplies led the UAE hospital supplies market with 38.05% market share in 2025, and sterilization & disinfectant products, the fastest-growing type category, are projected to expand at a 9.2% CAGR, outpacing all other product groups.

- By end user, hospitals & clinics accounted for 61.11% of the UAE hospital supplies market in 2025, while home healthcare providers are expected to grow at a 11.4% CAGR through 2031.

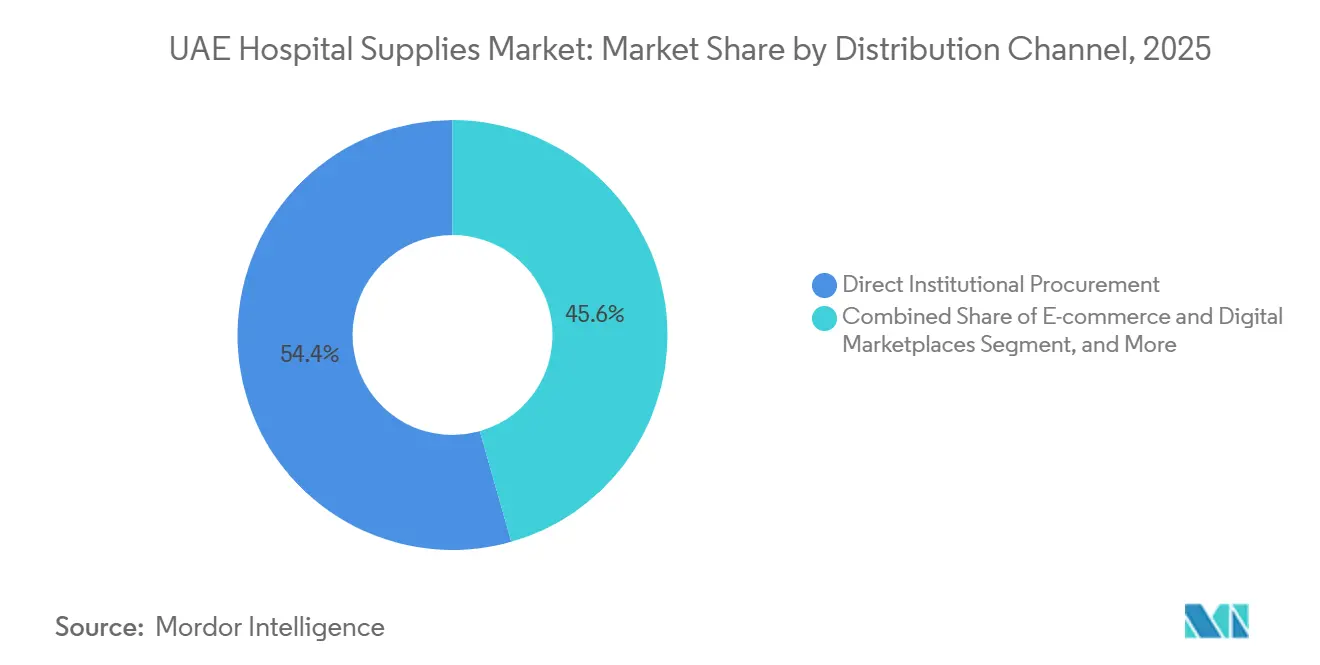

- By distribution channel, direct institutional procurement accounted for 54.4% of distribution volume in 2025; e-commerce and digital marketplaces are the fastest-growing channels, with a 12.2% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Hospital Supplies Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerating smart-hospital programs & AI-enabled procurement | +1.2% | Dubai, Abu Dhabi, Northern Emirates roll-out | Medium term (2–4 years) |

| Mandatory national infection-control standards escalation | +1.5% | All seven emirates | Short term (≤ 2 years) |

| Rapid bed-capacity expansion in Dubai & Abu Dhabi | +1.3% | Dubai, Abu Dhabi, spillover Sharjah & RAK | Medium term (2–4 years) |

| Surging medical-tourism driven premium device demand | +0.9% | Dubai & Abu Dhabi hubs | Long term (≥ 4 years) |

| Strategic stockpiling & local manufacturing incentives | +0.8% | Federal, free-zone clusters | Long term (≥ 4 years) |

| Shift to eco-friendly single-use consumables | +0.5% | Dubai & Abu Dhabi early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Smart-Hospital Programs & AI-Enabled Procurement

In 2024, the Dubai Health Authority partnered with Philips to integrate AI imaging analytics across 12 public hospitals.[1]Dubai Health Authority, “DHA-Philips AI Imaging MoU,” dha.gov.ae This initiative is expected to reduce repeat-scan consumable waste by 15%. In 2025, the Department of Health Abu Dhabi expanded its population-health intelligence initiative in collaboration with Microsoft, achieving a 22% reduction in pilot stockout incidents.[2]Department of Health Abu Dhabi, “Population Health Intelligence Framework,” doh.gov.ae Emirates Health Services introduced robotic pharmacies in five facilities, streamlining clinical staff workflows and minimizing inventory write-offs. Additionally, smart-facility pilots utilizing algorithm-guided dashboards are optimizing order redirection, reducing lead times for capital kits, and prioritizing suppliers with API-based catalogs. As these technologies gain wider adoption, the UAE hospital supplies market is benefiting from improved demand forecasting and reduced wastage.

Mandatory National Infection-Control Standards Escalation

In January 2025, Federal Decree-Law 38 of 2024 introduced stricter safety requirements for licensed hospitals, mandating the logging of sterilization cycles for reusable instruments.[3]Ministry of Health and Prevention, “Pricing Certificate Process,” mohap.gov.ae The Department of Health in Abu Dhabi is aligned with Joint Commission International standards, encouraging healthcare facilities to adopt antimicrobial-coated catheters. Suppliers offering traceable, single-use lines and closed-system transfer devices are gaining a competitive advantage. Additionally, the regulation has tightened ISO 13485 compliance for manufacturers, raising entry barriers and strengthening demand for audited consumables in the UAE hospital supplies market.

Rapid Bed-Capacity Expansion in Dubai & Abu Dhabi

Aster DM Healthcare is planning a 370-bed expansion, while Cleveland Clinic Abu Dhabi is set to open a 364-bed tower.[4]Pure Health. "Healthcare Services and Local Manufacturing Initiatives." Accessed February 2026. www.purehealth.ae These infrastructure developments are projected to increase first-year consumable spending by USD 12,000 to 15,000 per bed. The Department of Health Abu Dhabi has outlined plans to add 15,000 acute beds by 2030, with three tertiary projects currently under construction. Each new ward requires essential supplies such as sterile drapes, IV sets, and electrosurgical tools, driving baseline growth in the UAE hospital supplies market.

Surging Medical-Tourism Driven Premium Device Demand

Dubai attracted 674,000 medical tourists, generating USD 270 million in direct spending in 2023. These international patients, with their preference for premium implants and robotic surgeries, have prompted hospitals to stock da Vinci Xi disposables, priced at USD 2,000 to 3,500 per case. Mubadala Health, a sovereign investor, strengthened this trend through its 2024 oncology partnership with Mayo Clinic, increasing demand for single-use neurosurgery kits. The focus on higher-margin specialty supplies is protecting vendors from tender-price pressures while expanding the premium segment of the UAE hospital supplies market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price caps & tender-based procurement pressure | –0.7% | All emirates | Short term (≤ 2 years) |

| High import dependency amid logistics volatility | –0.6% | Dubai & Abu Dhabi port nodes | Medium term (2–4 years) |

| Emergence of hospital-at-home reducing inpatient volumes | –0.4% | Abu Dhabi & Dubai pilots | Medium term (2–4 years) |

| Skilled biomedical workforce shortages | –0.3% | Nationwide, acute in Northern Emirates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Caps & Tender-Based Procurement Pressure

Distributor margins for commodity catheters are capped at 8 to 12% as per MOHAP pricing regulations, putting pressure on profitability. The 2024 Unified Procurement Program by DoH Abu Dhabi eliminates volume rebates, reducing average discounts to 9%. Federal Law 11-2023 provides a 10% scoring advantage to UAE-based suppliers, creating challenges for multinational companies without local manufacturing facilities. Multi-year tenders that fix prices for five years restrict cost adjustments during fluctuations in resin or steel prices, limiting revenue growth in the UAE hospital supplies market.

Emergence of Hospital-at-Home Reducing Inpatient Volumes

In 2024, DoH Abu Dhabi authorized 14 home-health operators, resulting in a 1.8-day reduction in average inpatient stays. Hospitals adopting remote vitals kits, which replace single-use electrodes with reusable Bluetooth sensors, have experienced up to a 15% decline in central-supply volumes. Although the demand for home-use aids is growing rapidly, their overall market value remains lower than that of inpatient consumables, tempering overall growth in the UAE hospital supplies market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sterilization Demand Surges on Infection-Control Mandates

Between 2024 and 2031, the sterilization and disinfectant products market is projected to grow at an annual rate of 9.2%, making it the fastest-growing category. In 2025, audits introduced by the Dubai Health Authority will require logged cycles for reusable trays, driving increased adoption of hydrogen-peroxide vapor units and UVC robots. Disposable hospital supplies are expected to account for 38.05% of the market value in 2025, reflecting the preference of ambulatory centers for single-use kits to reduce turnover times. Physical-examination devices are evolving toward Bluetooth-enabled models that upload vital signs to EMRs. While these advancements align with smart-hospital objectives, they are anticipated to increase unit costs by 30%. Growth in operating-room equipment, which typically follows a ten-year replacement cycle, will depend on the development of new hospital wings in Dubai and Abu Dhabi. The UAE hospital supplies market for sterilization consumables is driven by increasing patient volumes, stricter cleaning regulations, and a focus on eco-friendly practices.

Key innovations include color-change biological indicators, enzymatic detergents, and RFID-tagged trays, which comply with MOHAP traceability requirements. Hospitals are also adopting continuous-flow washer-disinfectors that reduce water consumption, aligning with national sustainability objectives.

By End-User: Home-Healthcare Operators Erode Inpatient Dominance

In 2025, hospitals and clinics captured 61.11% of the demand, supported by growing licensed facilities and a growing focus on critical care. Large public buyers utilized three- to five-year tenders to stabilize volumes, accounting for 54.4% of the direct-procurement flows for 2025. Meanwhile, home-healthcare providers are anticipated to grow at a CAGR of 11.4%, driven by policies aimed at transitioning stable chronic-care cases from acute wards. Licensed providers under DoH Abu Dhabi deliver IV antibiotics, wound dressings, and remote-monitoring kits directly to patients' homes, fostering niche demand for portable oxygen, lift-assist chairs, and negative-pressure wound devices.

Ambulatory surgical centers in Dubai Healthcare City and Al Reem Island are increasingly favoring premium single-use arthroscopy and ophthalmic kits, which are not subject to the strictest price caps. Rehabilitation and long-term care centers are addressing the needs of the UAE's expanding 65-plus population, resulting in a doubling of suburban demand for pressure-injury dressings and mobility aids. Consequently, suppliers must manage two distinct purchasing approaches: bulk procurement for hospitals and just-in-time deliveries for decentralized care, each shaping specific segments of the UAE's hospital supplies market.

By Distribution Channel: Digital Marketplaces Capture Tail-Spend Growth

In 2025, direct institutional procurement accounted for 54.4% of the market volume, driven by unified tenders from Emirates Health Services and DoH Abu Dhabi. These tenders secured bulk rates and established 90-day terms. Third-party distributors, including Gulf Drug LLC and Al Mazroui Medical & Chemical Supplies, enhanced their offerings by incorporating consignment inventory and technician training, enabling them to achieve mark-ups of 8–12%. Digital marketplaces are experiencing significant growth, with a compound annual growth rate of 12.2%. Operating from a warehouse in Dubai Investment Park, these platforms stock 458 SKUs from 150 brands, provide next-day delivery, and integrate API feeds into hospital ERP systems. This integration enhances procurement teams' access to price transparency and real-time inventory management.

These marketplaces excel in addressing tail-spend items, urgent replenishments, and meeting the needs of home-health operators with limited bulk purchasing power. As smart-hospital dashboards automate stock reordering, sellers with API-enabled capabilities are well-positioned to capture additional market share. Traditional distributors are adapting by investing in e-portals and regional fulfillment centers to remain competitive. The UAE hospital supplies market increasingly prioritizes fast and data-driven services.

Geography Analysis

In 2025, Dubai and Abu Dhabi dominated the UAE's hospital supplies market, accounting for approximately 72% of the demand. The Dubai Health Authority reported a total of 19,102 licensed beds across the nation, with a significant concentration in Dubai's private medical hubs and the sovereign-backed networks of Abu Dhabi. Medical tourism is a key driver, with both emirates targeting one million health travelers by 2027. This increase in medical visitors is expected to boost demand for high-end products, such as robotic-surgery disposables and advanced imaging contrast agents. Abu Dhabi's roadmap plans to add 15,000 acute beds by 2030, requiring an investment of around USD 180 million in startup supplies, ensuring sustained demand for operating room and central-sterile line products.

Dubai's AI-driven procurement initiatives aim to reduce consumable waste, but the financial benefits are offset by the establishment of new ambulatory centers in Dubai Healthcare City, which favor single-use kits. Abu Dhabi's alliance with Mayo Clinic increases the complexity of medical cases, particularly driving demand for high-margin neuro and oncology products. Both Dubai and Abu Dhabi streamline procurement processes through integrated ERP systems, prioritizing suppliers with Electronic Data Interchange connections. This approach is shaping purchasing decisions across the broader UAE hospital supplies market.

Competitive Landscape

The UAE hospital supplies market demonstrates moderate fragmentation. Multinational OEMs such as Medtronic, GE Healthcare, Siemens Healthineers, Philips, and BD collaborate with distributors like Gulf Drug LLC, Al Mazroui Medical & Chemical Supplies, and Gulf Medical Co. to manage emirate-level registration and multi-year tenders. Sovereign investors leverage their scale advantage, with Mubadala Health’s 2024 partnership with Mayo Clinic utilizing financial strength to secure competitive pricing for proton-therapy consumables. At the same time, Pure Health is assessing joint ventures for local monitor assembly.

Market strategies are categorized into three key approaches. First, OEMs focus on securing direct contracts for capital equipment, often bundled with five-year service and training agreements, ensuring consistent demand for procedural consumables. Second, local distributors differentiate themselves by offering biomedical-engineer coverage and consignment stock, enabling them to sustain 8–12% margins on commodity goods. Third, digital platforms like Medikabazaar UAE target non-contract tail spend, using warehouse analytics to provide next-day delivery.

Growth opportunities exist in home-use mobility aids and portable monitors as the Department of Health Abu Dhabi expands its licensed hospital-at-home programs. Emerging disruptors are integrating API-driven catalog updates into hospital ERP systems, a feature that traditional distributors are rapidly adopting by digitizing order processes and incorporating real-time tracking. As buyers increasingly prioritize transparent pricing and sustainability credentials, competition within the UAE hospital supplies market continues to intensify.

UAE Hospital Supplies Industry Leaders

-

B. Braun SE

-

Baxter International Inc.

-

Boston Scientific Corporation

-

Medtronic plc

-

Johnson & Johnson Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Royal Philips unveiled AI-powered imaging and operational tools at World Health Expo Dubai, citing a 77% resident confidence rate in AI-enhanced care.

- February 2026: The Ministry of Health and Prevention introduced an ex-vivo organ-preservation device, extending viable transplant windows.

- December 2025: GE Healthcare and Dubai Health Authority broadened their 2024 AI-imaging partnership to six more hospitals, investing USD 18 million in cloud storage and cutting critical-finding turnaround by 28%.

- October 2025: Burjeel Holdings showcased new AI solutions at the Global Health Exhibition 2025, underscoring commitments to region-wide digital care pathways.

UAE Hospital Supplies Market Report Scope

As per the scope of the report, hospital supplies include every medical utility product that serves both patients and medical professionals within hospital infrastructure and enhances network and transportation between hospitals. The hospital supplies market is segmented by type, end-user, and distribution channel. By type, the market is segmented into physical examination devices, operating room equipment, mobility aids and transportation equipment, sterilization and disinfectant products, disposable hospital supplies, syringes and needles, and other types. By end-user, the market is segmented into hospitals & clinics, ambulatory surgical centers, home healthcare providers, and rehabilitation & long-term care centers. By distribution channel, the market is segmented into direct institutional procurement, third-party distributors, and e-commerce & digital marketplaces. The report offers market size and forecasts in value (USD) for the above segments.

By Type

| Physical Examination Devices |

| Operating Room Equipment |

| Mobility Aids & Transportation Equipment |

| Sterilization & Disinfectant Products |

| Disposable Hospital Supplies |

| Syringes & Needles |

| Other Types |

By End-User

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Home Healthcare Providers |

| Rehabilitation & Long-term Care Centers |

By Distribution Channel

| Direct Institutional Procurement |

| Third-party Distributors |

| E-commerce & Digital Marketplaces |

| By Type | Physical Examination Devices |

| Operating Room Equipment | |

| Mobility Aids & Transportation Equipment | |

| Sterilization & Disinfectant Products | |

| Disposable Hospital Supplies | |

| Syringes & Needles | |

| Other Types | |

| By End-User | Hospitals & Clinics |

| Ambulatory Surgical Centers | |

| Home Healthcare Providers | |

| Rehabilitation & Long-term Care Centers | |

| By Distribution Channel | Direct Institutional Procurement |

| Third-party Distributors | |

| E-commerce & Digital Marketplaces |

Key Questions Answered in the Report

What is the forecast size of the UAE hospital supplies market by 2031?

It is projected to reach USD 4.22 billion by 2031, growing at an 8.1% CAGR from 2026.

Which product category is growing the fastest?

Sterilization & disinfectant products, advancing at 9.2% CAGR on the back of tougher infection-control rules.

How big is the disposable segment inside the market?

Disposable hospital supplies held 38.05% share in 2025, the largest single category.

Why are digital marketplaces gaining share?

Platforms like Medikabazaar UAE provide API-fed catalogs, transparent pricing, and next-day delivery, growing at 12.2% CAGR.

Which emirates drive most demand?

Dubai and Abu Dhabi together account for about 72% of national hospital-supplies spending, fueled by dense bed capacity and medical-tourism inflows.

How do home-healthcare trends affect supplies demand?

Hospital-at-home programs trim inpatient consumable volumes by up to 15% in participating facilities but create new sales for portable monitoring and mobility aids.

Page last updated on: