Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

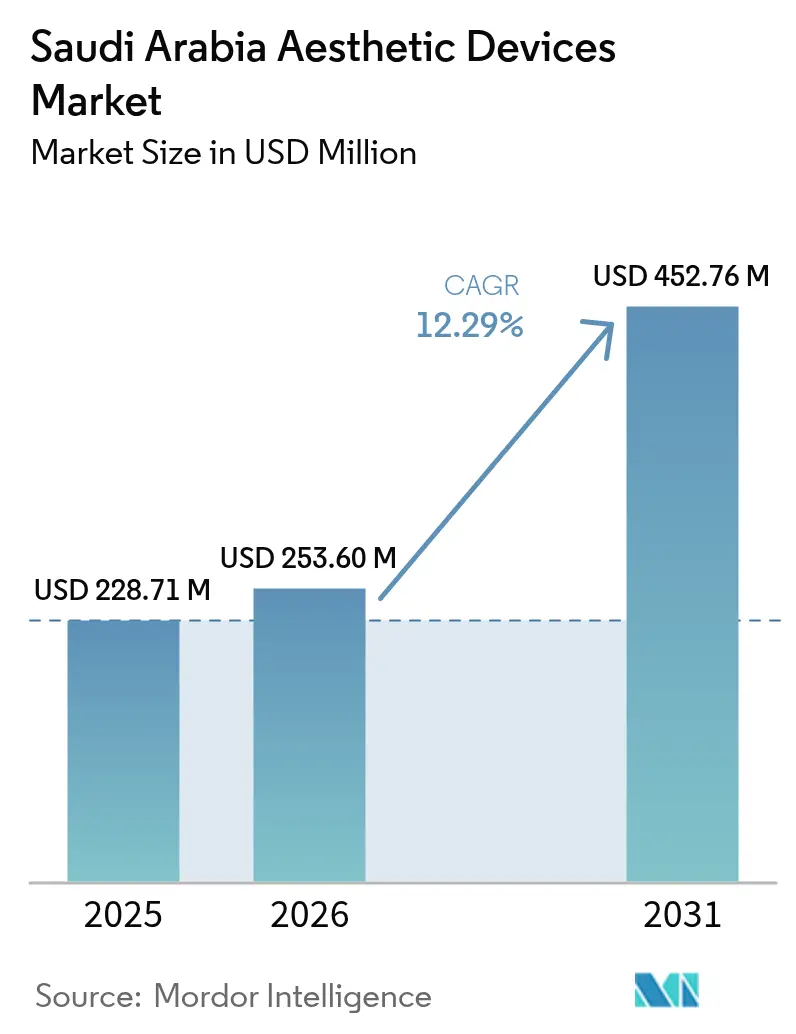

| Base Year Market Size (2025) | USD 228.71 Million |

| Market Size (2026) | USD 253.60 Million |

| Market Size (2031) | USD 452.76 Million |

| Growth Rate (2026 - 2031) | 12.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Aesthetic Devices Market Analysis by Mordor Intelligence

The Saudi Arabia Aesthetic Devices Market size is projected to be USD 228.71 million in 2025, USD 253.60 million in 2026, and reach USD 452.76 million by 2031, growing at a CAGR of 12.29% from 2026 to 2031.

Robust capital inflows triggered by Vision 2030’s healthcare-privatization mandate, a 79% social-media penetration rate that amplifies beauty trends, and streamlined Saudi Food and Drug Authority (SFDA) approvals for Class IIb devices combine to accelerate equipment purchases by licensed clinics.[1]Saudi Vision 2030, “Healthcare Transformation Program,” vision2030.gov.sa Riyadh and Jeddah anchor a medical-tourism program that targets 1 million inbound patients annually, positioning the Saudi Arabia aesthetic devices market as a regional hub for energy-based laser resurfacing and body-contouring procedures. Device distributors benefit from the Ministry of Finance’s SAR 260 billion (USD 69.3 billion) healthcare allocation for 2025-2026, which raises the private-sector share of service delivery from 25% to 35% and funds digital platforms that widen patient catchment areas.[2]Ministry of Finance, “Saudi Arabia Budget 2025-2026: Healthcare Allocation,” mof.gov.sa The market also gains momentum from Gen-Z demand for minimally invasive treatments that require low downtime and from the growing availability of halal-certified dermal fillers that satisfy religious preferences.

Key Report Takeaways

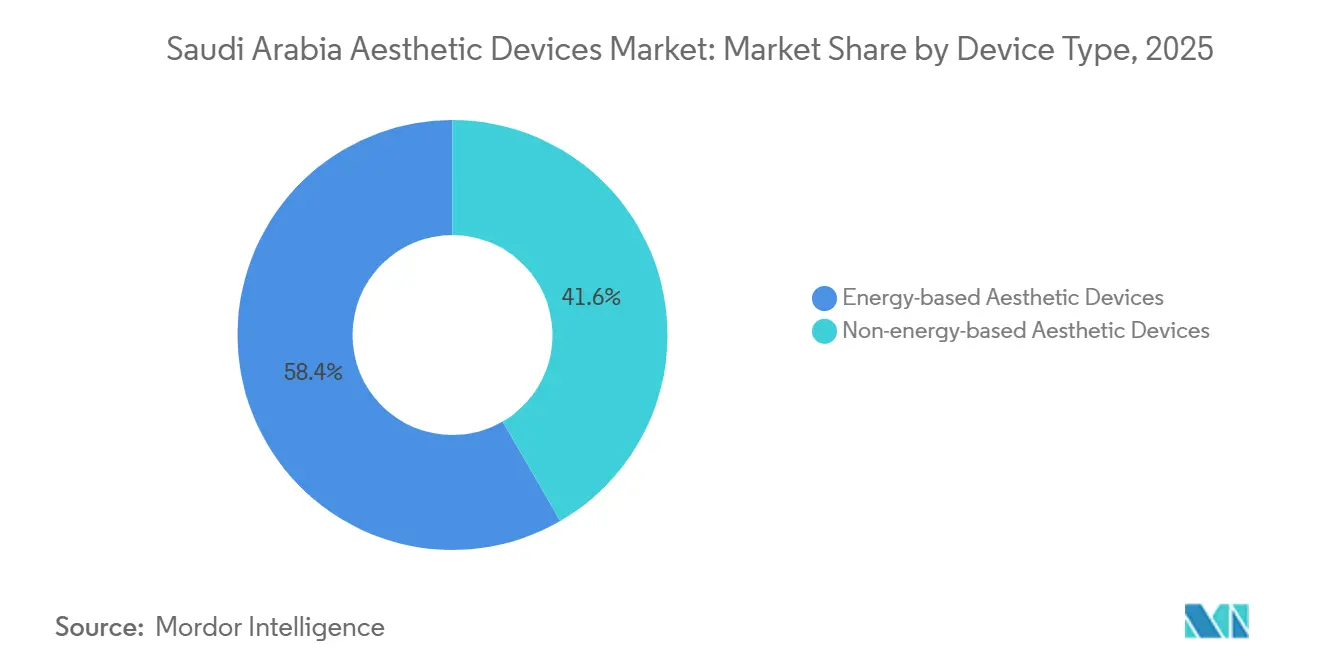

- Energy-based aesthetic devices led with 58.36% of the Saudi Arabia aesthetic devices market share in 2025. Non-energy platforms are projected to expand at 15.83% CAGR between 2026-2031, the fastest growth among device types.

- Hair removal captured 39.34% revenue in 2025, while body-contouring and cellulite reduction are forecast to rise at 15.78% CAGR through 2031.

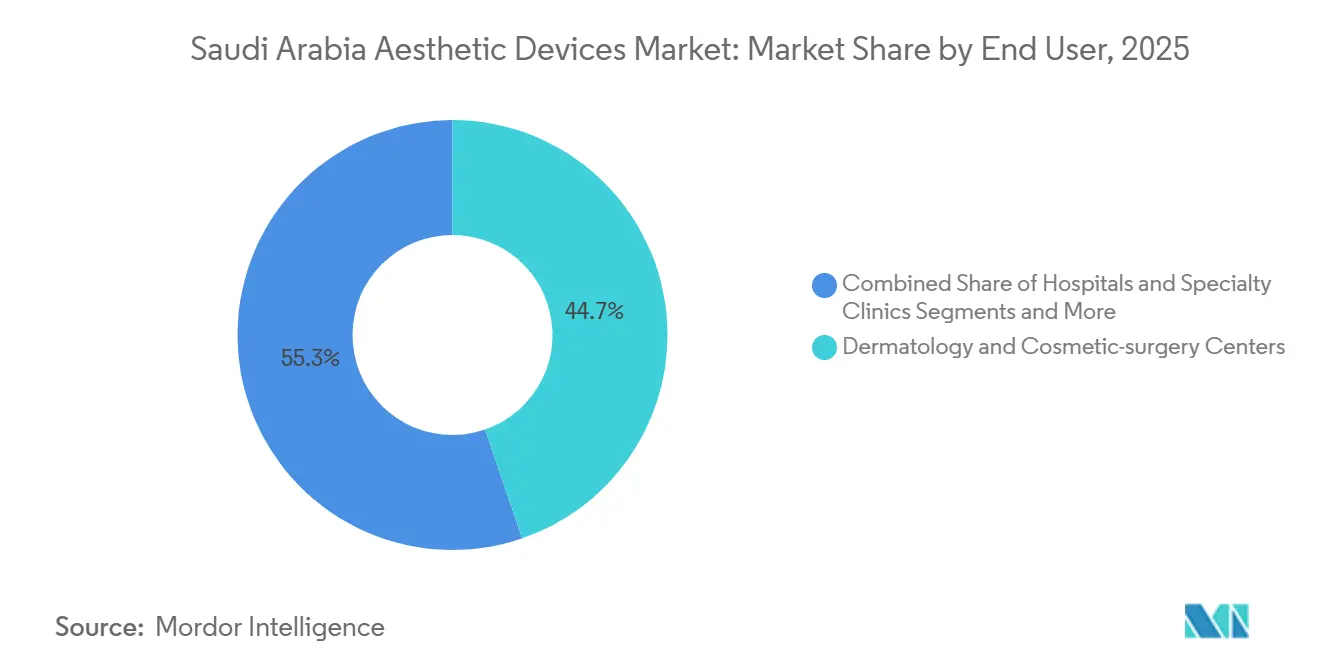

- Dermatology and cosmetic-surgery centers held 44.74% share of the Saudi Arabia aesthetic devices market size in 2025; home-use settings are advancing at 14.36% CAGR to 2031.

- Female patients accounted for 86.25% of 2025 procedures, yet male treatments are slated to climb at 14.69% CAGR.

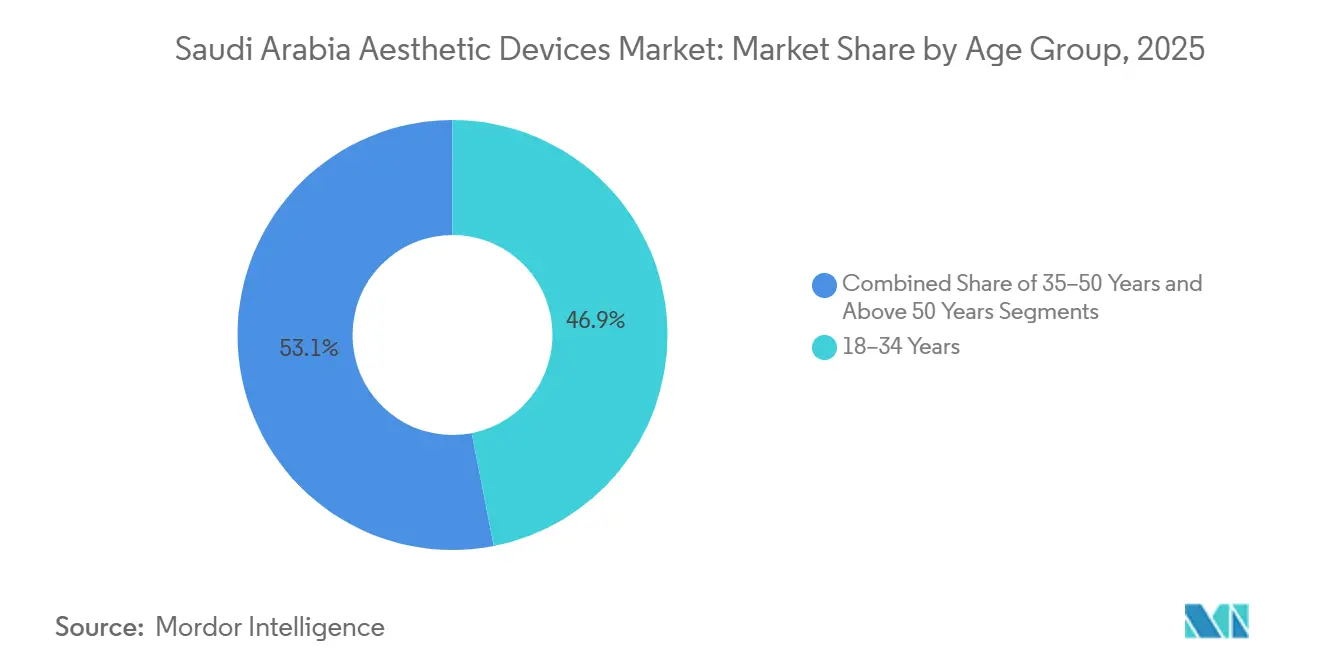

- The 18-34 cohort represented 46.92% of 2025 demand, whereas the 35-50 segment is moving at 14.83% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Medical Tourism in Riyadh & Jeddah | +2.8% | National, concentrated in Riyadh, Jeddah, Eastern Province | Medium term (2-4 years) |

| Government Support Via Vision 2030 Private-Healthcare Investments | +3.1% | National, early gains in Riyadh, Jeddah, Dammam | Long term (≥ 4 years) |

| Rising Adoption of Minimally Invasive Energy-Based Devices Among Gen-Z | +2.4% | National, urban centers leading | Short term (≤ 2 years) |

| Social-Media Influence Accelerating Demand for Body-Contouring | +1.9% | National, strongest in metros | Short term (≤ 2 years) |

| Expansion of Licensed Aesthetic Clinics Beyond Tier-1 Cities | +1.2% | National, tier-2 cities | Medium term (2-4 years) |

| Islamic-Law-Compliant Dermal Fillers Gaining Availability | +0.9% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Medical Tourism in Riyadh & Jeddah

Vision 2030 targets 1 million international health visitors annually by 2030, with laser resurfacing, body-sculpting, and injectables positioned as core offerings. Riyadh and Jeddah host new medical cities plus fast-track visa desks that shorten entry to fewer than 48 hours for Gulf Cooperation Council nationals. SFDA approvals for picosecond lasers and high-intensity focused ultrasound (HIFU) platforms rise as clinics differentiate through cutting-edge technology. The market incentive is reinforced by a March 2024 Riyadh study revealing that 94.1% of body-contouring patients self-funded treatment, confirming strong willingness to pay despite insurance exclusions.[3]Yazeed Alharbi et al., “Patient Satisfaction and Outcomes of Non-Invasive Facial Aesthetic Procedures in Saudi Arabia,” Cureus, cureus.com Device makers therefore queue new launches to secure early-mover share inside the Saudi Arabia aesthetic devices market.

Government Support Via Vision 2030 Private-Healthcare Investments

The National Transformation Program lifts the private share of healthcare capacity to 35% by 2030, channeling capital to dermatology chains and ambulatory surgery centers that specialize in elective aesthetics. Public Investment Fund stakes in clinic networks lower borrowing costs, while a 12-month SFDA review cycle for Class IIb devices accelerates revenue realization for foreign manufacturers. Digital-health spending funds teleconsultation portals, electronic records, and remote follow-up, enabling clinics to tap patients in tier-2 cities without brick-and-mortar branches. In turn, suppliers with in-country service hubs and ISO 13485 certification capture preferred-vendor status among expanding operators.

Rising Adoption of Minimally Invasive Energy-Based Devices Among Gen-Z

Saudi Arabia’s median age of 31.8 years provides a demographic surge for quick-recovery procedures. A February 2024 survey of 1,171 patients recorded 73.5% satisfaction after non-invasive facial treatments, validating fractional lasers, IPL hair removal, and cryolipolysis for younger consumers. Instagram-driven demand favors devices that deliver same-day results and photogenic outcomes, prompting manufacturers to design portable, clinic-friendly platforms. Lower upfront capital versus operating-room-grade lasers spurs entrepreneurial dermatologists to open boutique facilities, swelling the installed base of energy-based systems inside the Saudi Arabia aesthetic devices market.

Social-Media Influence Accelerating Demand for Body-Contouring

Instagram and TikTok reach 79% of Saudi internet users, with before-and-after content normalizing cryolipolysis, radiofrequency, and magnetic-field body-sculpting. The Kingdom’s 35.5% adult obesity prevalence widens the candidate pool for fat-reduction and skin-tightening sessions. Clinics leverage influencer partnerships to broadcast results, generating a referral flywheel that boosts utilization rates of high-margin body-contouring platforms. Vendors supplying devices with visible, camera-friendly outcomes enjoy faster payback periods and stronger retention contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural Conservatism Limiting Male Procedures | -1.4% | National, stronger outside metros | Long term (≥ 4 years) |

| Price Sensitivity Due to Lack of Insurance Coverage | -2.1% | National, mid-income segments | Medium term (2-4 years) |

| Fragmented Regulatory Approval Delays Device Launches | -0.8% | National | Short term (≤ 2 years) |

| Shortage of Board-Certified Female Surgeons Outside Metros | -1.1% | National, tier-2/3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity Due to Lack of Insurance Coverage

Saudi health plans exclude elective aesthetics, compelling 94.1% of patients to self-fund body-contouring sessions that can exceed SAR 5,000 (USD 1,333) per cycle. High-income households absorb costs, yet 60% of families earn below the SAR 20,000 (USD 5,333) threshold, capping mass-market uptake. Installment schemes via fintech firms add 15-20% annual interest, deterring repeat treatments such as laser hair removal where cumulative expense reaches SAR 10,000 (USD 2,667). Premium devices therefore face longer ROI horizons within the Saudi Arabia aesthetic devices market.

Shortage of Board-Certified Female Surgeons Outside Metros

Only 18% of board-certified dermatologists and plastic surgeons were women in 2024, with five-to-one concentration ratios favoring Riyadh. Cultural norms that prefer same-gender care limit clinic schedules, especially for intimate treatments such as Brazilian laser hair removal. While telemedicine eases consultation bottlenecks, hands-on procedures demand local presence. Labor premiums of 20-30% for female clinicians inflate operating costs and slow expansion into tier-2 cities, tempering growth for the Saudi Arabia aesthetic devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Non-Energy Platforms Gain Share

Energy-based systems held 58.36% of the Saudi Arabia aesthetic devices market share in 2025, led by diode lasers for hair removal and fractional CO₂ for skin resurfacing. Market growth is now tilting toward non-energy platforms, which are projected to advance at 15.83% CAGR through 2031. Botulinum-toxin injectors and dermal-filler delivery pens ride on recurring consumable demand that locks in predictable revenue streams for clinics. Microdermabrasion devices lure cost-sensitive Gen-Z users with SAR 500-800 (USD 133-213) tickets, stimulating footfall and cross-selling opportunities.

Radiofrequency handpieces continue to erode ablative lasers by offering minimal downtime, a benefit aligned with the lifestyles of Saudi professionals. Ultrasound-based HIFU devices move from niche to mainstream as collagen-remodeling evidence grows, adding fresh orders to the Saudi Arabia aesthetic devices market. Regulatory compliance favors multinationals able to clear ISO 13485 audits swiftly, putting pressure on smaller entrants still navigating SFDA dossiers. Meanwhile, implants stay subdued because surgical risks and sociocultural reservations counterbalance aesthetic benefits.

By Application: Body-Contouring Surges Post-Bariatric

Hair removal dominated revenue with 39.34% in 2025 thanks to established acceptance among women and a budding male customer base. The Saudi Arabia aesthetic devices market size for body-contouring is forecast to climb at a dramatic 65.78% CAGR, capitalizing on a 35.5% national obesity rate and rising bariatric-surgery volumes. Cryolipolysis, RF lipolysis, and HIFU platforms deliver 20-30% fat reduction per course, generating photo-friendly outcomes that thrive on social-media virality.

Facial and neck aesthetics remain sizable, driven by Botox, fillers, and thread lifts, though penetration is plateauing in tier-1 cities. Skin-rejuvenation and resurfacing gain steam as sun-damage awareness rises, supporting sales of fractional lasers and RF microneedling units. Tattoo-removal and vascular-lesion treatments remain niche yet command premium fees because few competitors maintain the requisite Q-switch or pulsed-dye lasers.

By End-User: Home-Use Devices Gain Momentum

Dermatology and cosmetic-surgery centers captured the largest slice at 44.74% in 2025. However, the home-use channel is projected to log a 14.36% CAGR as millennials snap up IPL hair-removal handsets and LED masks through e-commerce. Influencer-led tutorials demystify usage, pushing brands such as Philips Lumea and NuFace deeper into households.

Hospitals continue to handle complex surgeries—implants, deep resurfacing—and thus maintain stable revenue albeit slower growth. Medical spas, positioned between physician clinics and DIY, feel competitive heat from both ends and are up-skilling into higher-energy procedures to defend margins. Vendors that supply consumable cartridges for home-use gadgets add annuity revenue that cushions cyclical swings in capital-equipment orders across the Saudi Arabia aesthetic devices market.

By Gender: Male Segment Accelerates

Women generated 86.25% of procedure volume in 2025, yet male treatments are set to rise at 14.69% CAGR thanks to shifting grooming norms in Riyadh, Jeddah, and Dammam. Beard-line laser shaping, back-hair removal, and jawline filler sculpting headline male demand.

Cultural conservatism still suppresses uptake in rural zones, and a paucity of male dermatologists limits capacity during peak hours. Clinics address privacy concerns by offering men-only appointment blocks and anonymized billing. Female volume growth moderates as urban penetration climbs, but tier-2 diffusion keeps the base expanding for the Saudi Arabia aesthetic devices market.

By Age Group: Mid-Age Cohort Expands

The 18-34 bracket held 46.92% share in 2025 on the back of preventive Botox and acne-scar laser sessions. The 35-50 cohort is forecast to move at 14.83% CAGR, the fastest of any age segment, propelled by sun-induced pigmentation and wrinkle correction needs. Rising female workforce participation feeds discretionary spending in this group, nudging demand for collagen-stimulating HIFU and RF microneedling treatments.

The above-50 segment stays modest because marketers rarely target older consumers, and cultural expectations equate aging gracefully with minimal intervention. Still, dermal-filler brands are exploring softer marketing that frames treatments as “wellness” instead of vanity, hinting at future upside for the Saudi Arabia aesthetic devices market.

Geography Analysis

Riyadh, Jeddah, and the Eastern Province collectively generated an estimated 75% of 2025 procedures, underpinned by 40% of the Kingdom’s board-certified aesthetic specialists and higher household incomes exceeding SAR 20,000 (USD 5,333). Government-backed medical cities and expedited GCC visas funnel foreign patients seeking laser resurfacing and body sculpting into these hubs. Multinationals prioritize on-site training centers in the capital to cement their grip on the Saudi Arabia aesthetic devices market.

Tier-2 cities such as Taif, Abha, and Buraidah are registering 16-18% CAGR as highway upgrades cut travel times and populations demand local services. Licensed clinic density still trails tier-1 benchmarks—one aesthetic center per 150,000 residents—creating ample headroom. Device sellers package versatile IPL-RF platforms that suit the varied case mix in smaller cities, while service depots in Dammam and Jeddah guarantee under-24-hour maintenance.

Rural areas remain thinly penetrated; patients often travel to the nearest metro for major treatments. Teleconsultation mitigates early-stage patient screening but cannot replace in-clinic energy procedures because SFDA forbids remote operation of high-power devices. Home-use tools priced at SAR 800-3,000 (USD 213-800) partially fill the gap, marking a secondary revenue path for manufacturers in the Saudi Arabia aesthetic devices market.

Competitive Landscape

Multinational suppliers including AbbVie’s Allergan Aesthetics, Galderma, Merz Pharma, Candela Medical, Cynosure, and Lumenis, leveraging ISO 13485 manufacturing and established SFDA dossiers to speed launches. Regional distributors control 40%, capitalizing on hospital relationships and flexible financing for clinics. Technology differentiation centers on hybrid energy stacks (RF + ultrasound, picosecond laser + micro-coring) that shrink session counts, a key selling point in time-pressed urban markets.

Patent filings in 2024-2025 soared for AI-guided treatment parameters that standardize outcomes, lowering operator dependence amid a shortage of specialist physicians. Halal-certified fillers from Galderma and Merz unlock conservative segments and provide a moat versus un-certified rivals. Pricing pressure surfaces as clinic numbers swell—2,377 primary healthcare centers bear aesthetic licenses—forcing equipment vendors to bundle training, consumables, and service into subscription-style contracts that cement share inside the Saudi Arabia aesthetic devices market.

Telemedicine start-ups offer video consultations and postoperative monitoring, yet regulatory bars on remote toxin or filler prescribing curb disruption. Home-use device brands such as Philips, NuFace, and Foreo nibble at entry-level treatments but also cross-promote professional upgrades, yielding coopetition rather than direct cannibalization.

Saudi Arabia Aesthetic Devices Industry Leaders

Lumenis Inc.

Candela Medical

AbbVie Inc (Allergan Aesthetics)

Galderma S.A.

Alma Lasers (Sisram Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Wontech obtained SFDA clearance for its V-Laser platform, widening the laser-vascular device portfolio in the Kingdom.

- June 2025: Daewoong Pharmaceutical launched the high-purity botulinum toxin Nabota in Qatar, Saudi Arabia, and the UAE, cementing its Gulf footprint.

- March 2025: Cytrellis Biosystems received SFDA approval to commercialize its ellacor® Micro-Coring device, introducing a non-thermal skin-tightening alternative.

Saudi Arabia Aesthetic Devices Market Report Scope

As per the scope of the report, Aesthetic devices are tools used for non-surgical or minimally invasive cosmetic procedures to improve appearance through technologies like lasers, radiofrequency, ultrasound, and light.

The Saudi Arabia Aesthetic Devices Market Report is segmented by Device Type, Application, End User, Gender, and Age Group. By Device Type, the market is segmented into Energy-based and Non-energy devices. By Application, the market is segmented into Facial & Neck, Body-contouring, Hair Removal, Skin Rejuvenation, and Others. By End User, the market is segmented into Hospitals, Dermatology Centers, Medical Spas, and Home-use settings. By Gender, the market is segmented into Female and Male. By Age Group, the market is segmented into 18–34, 35–50, and Above 50. Market Forecasts are Provided in Terms of Value (USD).

By Device Type

| Energy-based Aesthetic Devices | Laser-based Devices |

| Radiofrequency-based Devices | |

| Ultrasound-based Devices | |

| Other Energy-based Devices | |

| Non-energy Aesthetic Devices | Botulinum-toxin & Dermal-filler Delivery Devices |

| Micro-dermabrasion Devices | |

| Implants | |

| Others |

By Application

| Facial & Neck Aesthetics |

| Body-contouring & Cellulite Reduction |

| Hair Removal |

| Skin Rejuvenation & Resurfacing |

| Others |

By End-user

| Hospitals & Specialty Clinics |

| Dermatology & Cosmetic-surgery Centers |

| Medical Spas & Beauty Centers |

| Home-use Settings |

By Gender

| Female |

| Male |

By Age Group

| 18–34 Years |

| 35–50 Years |

| Above 50 Years |

| By Device Type | Energy-based Aesthetic Devices | Laser-based Devices |

| Radiofrequency-based Devices | ||

| Ultrasound-based Devices | ||

| Other Energy-based Devices | ||

| Non-energy Aesthetic Devices | Botulinum-toxin & Dermal-filler Delivery Devices | |

| Micro-dermabrasion Devices | ||

| Implants | ||

| Others | ||

| By Application | Facial & Neck Aesthetics | |

| Body-contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Skin Rejuvenation & Resurfacing | ||

| Others | ||

| By End-user | Hospitals & Specialty Clinics | |

| Dermatology & Cosmetic-surgery Centers | ||

| Medical Spas & Beauty Centers | ||

| Home-use Settings | ||

| By Gender | Female | |

| Male | ||

| By Age Group | 18–34 Years | |

| 35–50 Years | ||

| Above 50 Years | ||

Key Questions Answered in the Report

How fast is the Saudi Arabia aesthetic devices market expected to grow through 2031?

It is projected to climb from USD 268.55 million in 2026 to USD 452.76 million by 2031, registering a 12.29% CAGR.

Which device category will add the most incremental revenue?

Non-energy platforms such as botulinum-toxin injectors and dermal-filler pens are forecast to post the fastest 15.83% CAGR, adding the largest incremental revenue.

What is driving demand for body-contouring equipment?

A 35.5% adult obesity rate, strong social-media influence, and high self-payment rates are propelling body-contouring applications at 65.78% CAGR.

How significant is home-use equipment in Saudi sales?

Home-use devices remain smaller than physician channels but are expanding at 14.36% CAGR, aided by e-commerce and influencer tutorials.

Why do halal-certified fillers matter for suppliers?

SFDA halal guidelines unlock conservative markets such as Mecca and Medina, widening the customer base for certified dermal fillers and associated delivery devices.

What limits adoption among male patients?

Cultural conservatism and a shortage of male aesthetic specialists, especially outside metros, restrain growth even as urban acceptance improves.

Page last updated on: