Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

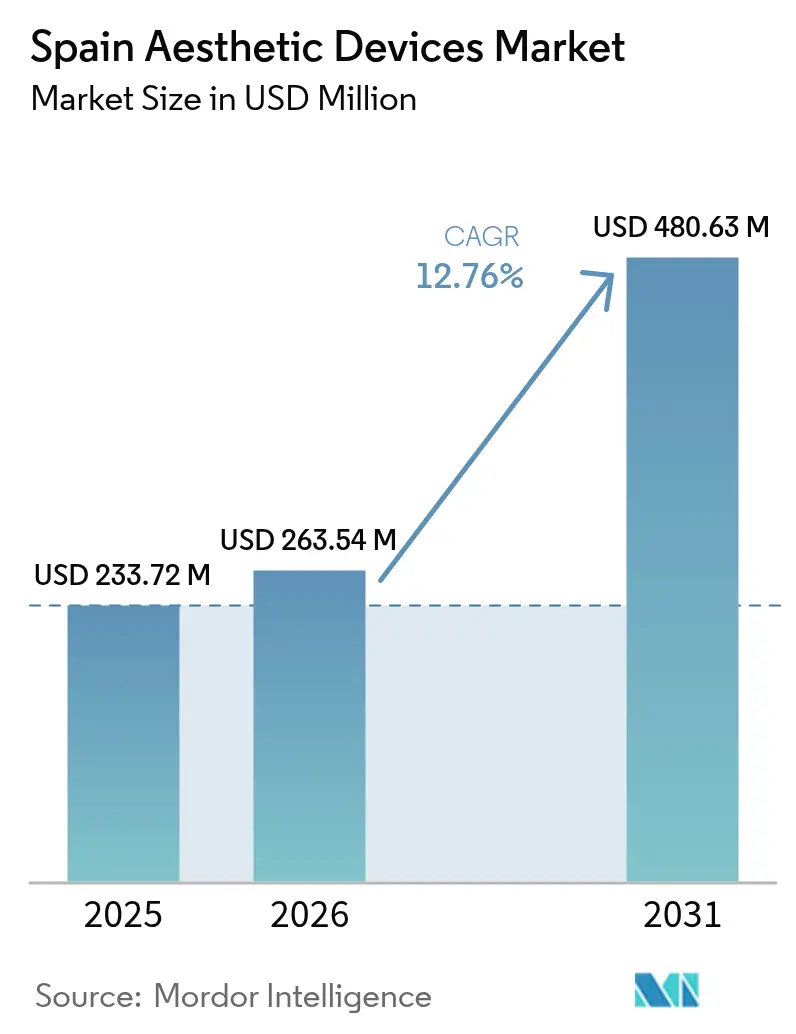

| Base Year Market Size (2025) | USD 233.72 Million |

| Market Size (2026) | USD 263.54 Million |

| Market Size (2031) | USD 480.63 Million |

| Growth Rate (2026 - 2031) | 12.76% CAGR |

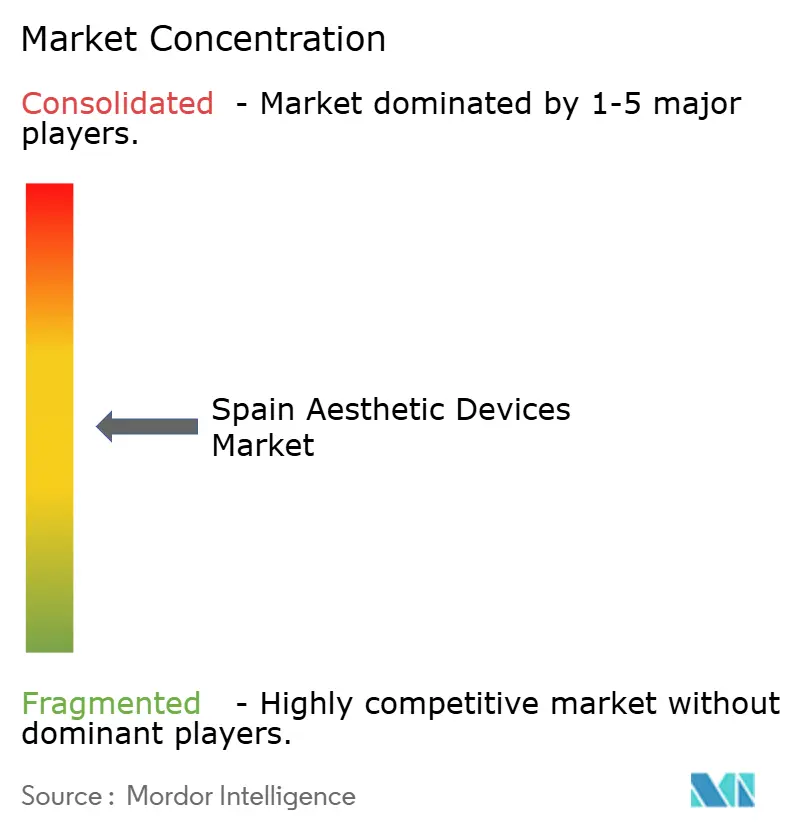

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Aesthetic Devices Market Analysis by Mordor Intelligence

The Spain Aesthetic Devices Market size was valued at USD 233.72 million in 2025 and estimated to grow from USD 263.54 million in 2026 to reach USD 480.63 million by 2031, at a CAGR of 12.76% during the forecast period (2026-2031).

Persistent demand for sophisticated, minimally invasive procedures anchors this trajectory, helped by 400,000 cosmetic interventions performed in the country every year. Recent regulatory tightening that limits invasive surgeries to board-certified plastic surgeons is concentrating procedure volumes in high-quality facilities, encouraging clinics to acquire compliant, premium equipment. Parallel advances in energy-based platforms, artificial intelligence–guided imaging, and home-use technologies are broadening the user base while improving treatment outcomes, reinforcing the long-term growth outlook for the Spain aesthetic devices market.

Key Report Takeaways

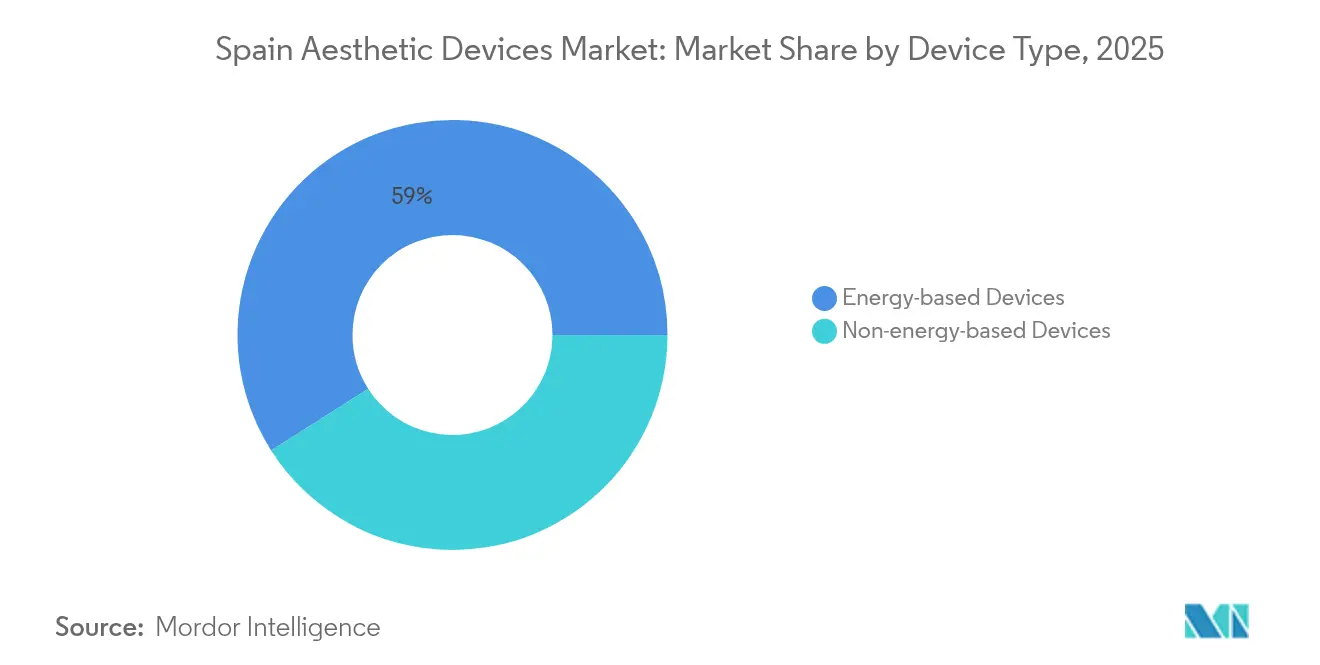

- By device type, energy-based platforms led with 59.02% of Spain aesthetic devices market share in 2025, and ultrasound-based systems are poised for the fastest expansion at a 15.62% CAGR through 2031.

- By application, skin resurfacing and tightening accounted for 32.55% of the Spain aesthetic devices market size in 2025, whereas body contouring and cellulite reduction is projected to grow quickest at a 14.28% CAGR to 2031.

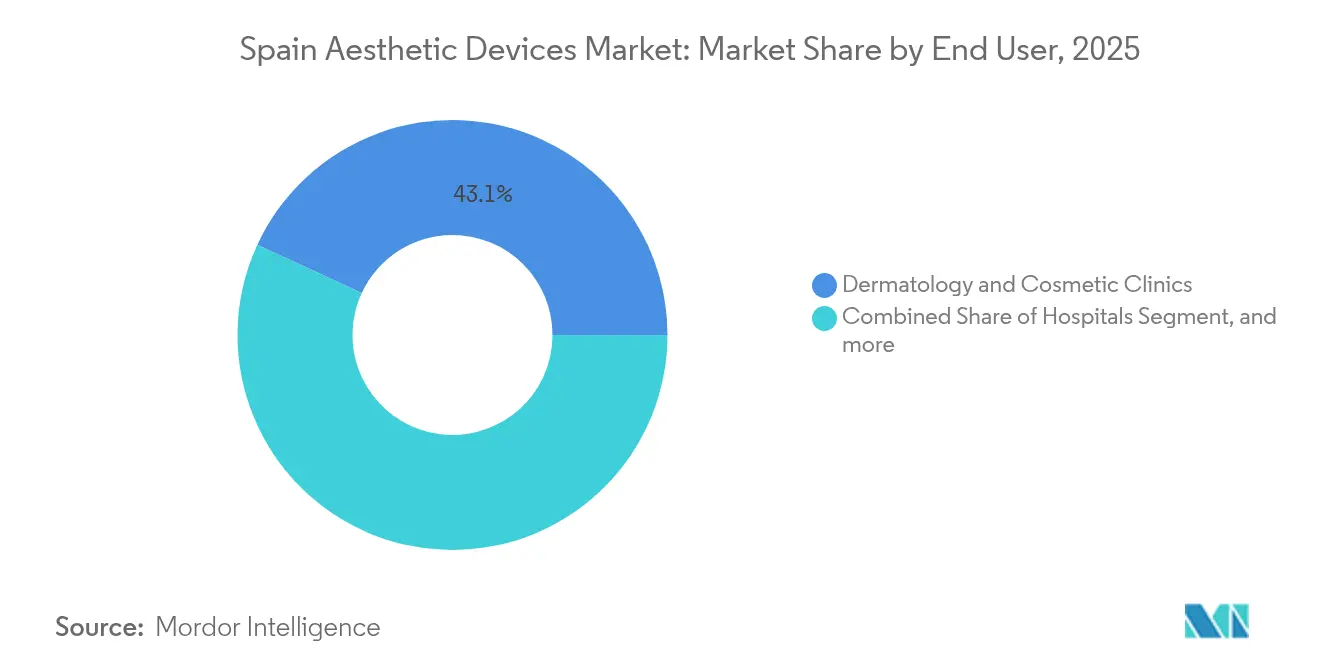

- By end user, dermatology and cosmetic clinics captured 43.10% revenue share of the Spain aesthetic devices market in 2025, while home-use settings are set to record the highest 13.22% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Aesthetic Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Youthful Appearance Demand | 3.2% | National, concentrated in Madrid, Barcelona, Valencia | Long term (≥ 4 years) |

| Rising Medical Tourism in Cosmetic Procedures | 2.8% | National, with coastal regions leading | Medium term (2-4 years) |

| Growing Popularity of Minimally-Invasive Treatments | 2.1% | National, urban centers primarily | Short term (≤ 2 years) |

| Technological Advancements in Aesthetic Devices | 1.7% | National, early adoption in major cities | Medium term (2-4 years) |

| Cultural Emphasis on Beauty & Wellness | 1.9% | National, stronger in metropolitan areas | Long term (≥ 4 years) |

| Expanding Private Aesthetic Clinics in Urban Centers | 1.3% | Urban centers, Madrid and Barcelona leading | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Youthful-Appearance Demand

Spain’s median age continues to inch upward, yet cosmetic consciousness is rising in parallel, pushing the 45-65 cohort toward non-surgical tightening and resurfacing options. Energy-based modalities that stimulate collagen, such as micro-focused ultrasound with visualization, fit this preference by delivering visible yet discreet results. Uptake is further reinforced by 3D skin-mapping systems that provide precise pre-treatment assessments, a feature embraced by quality-oriented consumers in Madrid and Barcelona.[1]Frontiers Editorial Team, “Three-Dimensional Imaging for Dermatologic Assessment,” frontiersin.org Hospitals and large clinic groups continue to market these procedures as preventive rather than corrective, lengthening patient lifecycles. As demographic momentum endures, so does the baseline demand floor for the Spain aesthetic devices market.

Rising Medical Tourism in Cosmetic Procedures

Spain’s accession to the EU cross-border healthcare directive through Real Decreto 81/2014 smooths reimbursement for intra-EU patients, making the country a logical destination for elective aesthetics.[2]Ministerio de Sanidad, “Real Decreto 81/2014 sobre Asistencia Sanitaria Transfronteriza,” sanidad.gob.es The September 2024 rule that confines cosmetic surgery to board-certified plastic surgeons has paradoxically improved the nation’s brand by signaling strict safety oversight. Clinics in Valencia and Málaga now bundle accommodation with HIFU-based body-contouring packages, leveraging coastal appeal to foreign visitors. High patient satisfaction ratings feed digital word-of-mouth, reinforcing a virtuous inflow cycle that elevates procedure volumes and equipment replacement needs across the Spain aesthetic devices market.

Growing Popularity of Minimally Invasive Treatments

Demand for reduced downtime is steering consumers toward injectables, fractional lasers, and temperature-controlled radiofrequency systems. The Spanish Agency for Medicines and Health Products classifies fillers under EU MDR 2017/745, boosting confidence in product safety. New ready-to-use liquid neuromodulator formulations such as Galderma’s Relfydess show perceptible effects one day after administration, resonating with time-pressed patients. Clinics are responding by training staff in combination protocols that merge energy-based skin-tightening with injectables, enhancing both ticket size and clinical outcomes.

Technological Advances in Aesthetic Devices

Artificial-intelligence algorithms embedded in the latest multi-modal systems tailor energy delivery to each patient’s skin impedance profile, elevating safety and efficacy.[3]MDPI Editors, “AI-Enhanced Personalized Aesthetic Protocols,” mdpi.com Innovators are commercializing 1726 nm lasers able to clear moderate acne across all phototypes while avoiding significant epidermal damage. Ultra-high-frequency ultrasound scanners are extending into diagnostic mapping, enabling real-time visualization of treatment impact. Regenerative aesthetics, including acoustic-wave therapies that activate endogenous stem cells, signal a future where biological stimulation complements mechanical correction. As clinics refresh equipment to stay competitive, technology diffusion sustains double-digit expansion in the Spain aesthetic devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Insurance Coverage for Cosmetic Procedures | -2.4% | National, affecting all regions equally | Long term (≥ 4 years) |

| Shortage of Certified Aesthetic Professionals in Rural Areas | -1.8% | Rural regions, northern and central Spain | Medium term (2-4 years) |

| Stringent EU Regulatory Oversight on Devices & Fillers | -1.2% | National, with stronger impact on smaller manufacturers | Short term (≤ 2 years) |

| Economic Sensitivity of Elective Procedures | -0.9% | National, with higher impact in lower-income regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Insurance Coverage for Cosmetic Procedures

Public insurance excludes elective aesthetics, obliging patients to self-fund expensive treatments. Average out-of-court settlements for cosmetic-related claims exceed EUR 33,000, illustrating the financial stakes involved. Because device amortization costs are rolled into procedure pricing, clinics must keep utilization high to remain profitable, raising affordability barriers for middle-income groups. The legal framework under Ley 29/2006 mandates rigorous proof of safety and efficacy, driving up manufacturer compliance costs that, again, echo down to consumers. Although consumer-grade light-therapy masks and handheld RF tools are proliferating, professional equipment remains inaccessible to many Spaniards outside major cities.

Shortage of Certified Aesthetic Professionals in Rural Areas

Concentration of plastic surgeons and dermatologists in Madrid, Barcelona, and coastal tourism belts leaves much of rural Spain underserved. The 2024 regulation that permits only board-certified specialists to perform invasive aesthetic surgery tightens supply still further. Smaller towns often lack the volumes needed to justify the capital expenditure on Class IIb or III devices, delaying technology penetration. The EU Medical Device Quality Management System requirement effective in 2024 adds training and documentation burdens, widening the urban-rural gap. Over time, tele-aesthetics consults and more automated equipment may mitigate access disparities, yet short-term growth outside metropolitan zones stays constrained.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Energy-Based Systems Sustain Dominance

Energy-based equipment accounted for 59.02% of Spain aesthetic devices market share in 2025 as lasers, radiofrequency, and ultrasound platforms proved versatile across multiple indications. Ultrasound-based systems are forecast to log a 15.62% CAGR through 2031, propelled by high-intensity focused ultrasound procedures that now extend to scalp rejuvenation protocols validated for androgenetic alopecia treatment.

Laser manufacturers are commercializing 1726 nm devices with real-time thermal imaging that achieve durable acne clearance without pigmentary complications. Temperature-controlled RF microneedling platforms record 86.7% patient satisfaction in clinical trials, keeping radiofrequency relevant even as lasers evolve. Non-energy alternatives such as fillers maintain share through improved rheology and tighter AEMPS oversight, while chemical peels enjoy a niche revival as cost-effective adjuncts. Microneedle rollers now fall under Class IIa rules, prompting clinics to adopt safer cartridge-based systems. Collectively, these trends ensure that the Spain aesthetic devices market continues to favor energy platforms while leaving space for targeted innovation in adjunct categories.

By Application: Body Contouring Accelerates

Skin resurfacing and tightening held 32.55% of Spain aesthetic devices market size in 2025 with micro-focused ultrasound systems that visualize collagen bands during treatment gaining traction. Body contouring and cellulite reduction, however, is the most dynamic niche, projected at a 14.28% CAGR, powered by cryolipolysis, multipolar RF, and AI-guided treatment mapping that reduces operator variability.

Laser hair removal remains resilient as diode heads achieve faster repetition rates, while tattoo-removal devices deploy dual-wavelength Q-switching to minimize ghosting. Acne and scar management benefit from 1726 nm laser breakthroughs that blend photothermal clearance with sebaceous-gland moderation. Emerging regenerative aesthetics, including platelet-rich plasma combined with low-energy acoustic waves, are blurring therapeutic lines and could spawn new application sub-segments by 2030. This broadening palette sustains multi-device procurement cycles, reinforcing revenue momentum in the Spain aesthetic devices market.

By End User: Home-Use Platforms Gain Ground

Dermatology and cosmetic clinics retained 43.10% revenue share of the Spain aesthetic devices market in 2025, still the primary channel for energy-intensive equipment. Hospitals are retreating from routine aesthetics to concentrate on reconstructive and high-complexity interventions, redirecting capital budgets toward robotics and hybrid operating rooms.

Home-use devices are the fastest-advancing outlet, set for a 13.22% CAGR through 2031 as miniaturization and automated safety cutoffs make consumer operation feasible. Skinvity’s revenue leap of 70% in 2024 to EUR 3 (USD 3.4) million illustrates domestic appetite for FDA-cleared light-therapy masks and RF pens. Peer-reviewed studies on home-phototherapy lamps for acne corroborate efficacy when protocols are followed, nurturing confidence in DIY regimens. Medical spas occupy a middle ground, marketing physician-overseen facial filler packages bundled with low-energy LED sessions to widen client funnels. As device ecosystems extend from clinics to living rooms, manufacturers that engineer modular product families stand to win share in the Spain aesthetic devices market.

Geography Analysis

Spain leverages its EU membership and robust hospitality infrastructure to attract patients from France, Italy, and the United Kingdom, amplifying procedure volumes in Barcelona, Madrid, and Valencia. Integration within Real Decreto 81/2014 removes administrative friction for visiting EU citizens, streamlining reimbursement and reinforcing Spain’s allure as a cosmetic hub. Coastal provinces combine leisure tourism with non-surgical body-contouring packages, while interior regions rely largely on domestic demand fueled by rising disposable incomes.

AEMPS enforces EU Medical Device Regulation 2017/745, mandating CE marking for fillers and implants, which consolidates the vendor base and channels purchases toward compliant distributors. The September 2024 statute confining invasive cosmetic surgery to plastic-surgery specialists further elevates procedural credibility, but also exacerbates specialist scarcity in Castilla-La Mancha and Extremadura. Tele-consultation portals now let urban surgeons pre-screen candidates from rural areas, yet physical treatment capacity remains uneven.

Spain’s contribution of EUR 10.4 (USD 12.0) billion to Europe’s EUR 96 (USD 111.0) billion cosmetics economy underscores national consumer zeal for beauty products, which extends naturally to device-based services. Venture funding gravitates to Barcelona’s health-tech cluster, supporting AI-driven skin-diagnostic startups that collaborate with local clinics on pilot deployments. Despite persisting regional disparities, the Spain aesthetic devices market benefits from coordinated national regulation, EU-level patient mobility, and a cultural affinity for personal appearance that spans age cohorts.

Competitive Landscape

The Spain aesthetic devices market exhibits moderate consolidation, with the top five suppliers owning significant market share of revenue in 2024. Cynosure’s January 2025 merger with Lutronic forged Cynosure Lutronic Inc., combining strong diode-laser intellectual property with broad distribution in 130 countries. This union pressures smaller laser manufacturers to differentiate through niche wavelengths or proprietary feedback algorithms.

Financial distress hit other incumbents: Cutera filed for Chapter 11 in March 2025 while arranging USD 65 million debtor-in-possession financing to stabilize operations. InMode’s reported 20% revenue slide in 2024 and Venus Concept’s 15% drop spurred cost-rationalization programs yet left R&D spend intact, evidencing belief in innovation-led turnaround strategies. Galderma contrasted by recording USD 1.13 billion in Q1 2025 sales, buoyed by 9.9% growth in injectable aesthetics, reinforcing the value of product-line breadth.

Emerging challengers include domestic firm Skinvity, which sells app-linked RF devices for home users and partners with dermatologists for post-treatment maintenance kits. Regenerative-medicine ventures also attract capital, exemplified by Merz Aesthetics’ investment in Acorn Biolabs to commercialize patient-specific stem-cell preservation services. Competitive success hinges on mastering EU MDR compliance, integrating AI for treatment personalization, and, increasingly, maintaining omni-channel portfolios that span clinical and at-home settings. Against this backdrop, continuous technology refresh cycles and customer-training support remain primary levers for sustaining advantage in the Spain aesthetic devices market.

Spain Aesthetic Devices Industry Leaders

Cutera Inc.

AbbVie (Allergan Aesthetics)

Bausch + Lomb (Solta Medical)

Hologic Inc. (Cynosure)

Lumenis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Cutera Inc. filed for Chapter 11 bankruptcy protection while continuing operations, implementing a restructuring plan to reduce debt by nearly USD 400 million and raise USD 65 million from existing lenders to strengthen its financial foundation and position for long-term success in the aesthetic and dermatology sectors.

- March 2025: AbbVie's Allergan Aesthetics showcased its commitment to innovation at AMWC 2025, introducing the AA Signature program focused on three key areas: Lift, Definition, and Skin Quality, while presenting eleven E-Poster presentations highlighting ongoing research and advancements in aesthetic medicine.

- January 2025: Cynosure completed its merger with Lutronic to form Cynosure Lutronic Inc., combining Cynosure's leadership in aesthetic energy devices with Lutronic's laser technology expertise to create a comprehensive portfolio serving over 130 countries globally.

Spain Aesthetic Devices Market Report Scope

As per the scope of the report, aesthetic devices refer to all medical devices that are used for various cosmetic procedures, which include plastic surgery, unwanted hair removal, excess fat removal, anti-aging, aesthetic implants, skin tightening, etc., that are used for beautification, correction, and improvement of the body. Aesthetic procedures include both surgical and non-surgical procedures. The Spain Aesthetic Devices Market is segmented by Device (Energy-based Aesthetic Devices and Non-energy-based Aesthetic Devices), Application (Skin Resurfacing and Tightening, Hair Removal, Tattoo Removal, Breast Augmentation, and Other Applications), and End-user (Hospitals, Clinics, and Home Settings). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

By Device Type

| Energy-based Devices | Laser-based |

| Light-based (IPL) | |

| Radio-frequency-based | |

| Ultrasound-based | |

| Cryolipolysis & Plasma-based | |

| Non-energy-based Devices | Botulinum Toxin |

| Dermal Fillers & Threads | |

| Chemical Peels | |

| Microdermabrasion | |

| Implants | |

| Mesotherapy & Others |

By Application

| Skin Resurfacing & Tightening |

| Body Contouring & Cellulite Reduction |

| Hair Removal |

| Tattoo & Pigmentation Removal |

| Breast Augmentation |

| Acne & Scar Treatment |

| Other Applications |

By End User

| Hospitals |

| Dermatology & Cosmetic Clinics |

| Medical Spas |

| Home-use Settings |

| By Device Type | Energy-based Devices | Laser-based |

| Light-based (IPL) | ||

| Radio-frequency-based | ||

| Ultrasound-based | ||

| Cryolipolysis & Plasma-based | ||

| Non-energy-based Devices | Botulinum Toxin | |

| Dermal Fillers & Threads | ||

| Chemical Peels | ||

| Microdermabrasion | ||

| Implants | ||

| Mesotherapy & Others | ||

| By Application | Skin Resurfacing & Tightening | |

| Body Contouring & Cellulite Reduction | ||

| Hair Removal | ||

| Tattoo & Pigmentation Removal | ||

| Breast Augmentation | ||

| Acne & Scar Treatment | ||

| Other Applications | ||

| By End User | Hospitals | |

| Dermatology & Cosmetic Clinics | ||

| Medical Spas | ||

| Home-use Settings | ||

Key Questions Answered in the Report

How fast is demand for at-home aesthetic devices growing in Spain?

Home-use platforms are forecast to expand at a 13.22% CAGR between 2026 and 2031, reflecting rapid consumer adoption and technology miniaturization.

Which technology will lead future growth?

Ultrasound-based systems are projected to post the strongest 15.62% CAGR through 2031, driven by expanded indications in skin tightening and body contouring.

What regulation most affects suppliers today?

EU Medical Device Regulation 2017/745, enforced locally by AEMPS, sets stringent CE-marking and quality-management requirements for all aesthetic devices marketed in Spain.

Why are energy-based devices so dominant?

They deliver versatile, clinically validated outcomes across multiple applications, securing 59.02% of 2025 revenue and attracting continuous R&D investment.

Is medical tourism still important post-regulation?

Yes; stricter standards enhanced Spain’s reputation, and cross-border directives keep the country attractive to EU patients seeking affordable, high-quality treatments.

Page last updated on: