Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

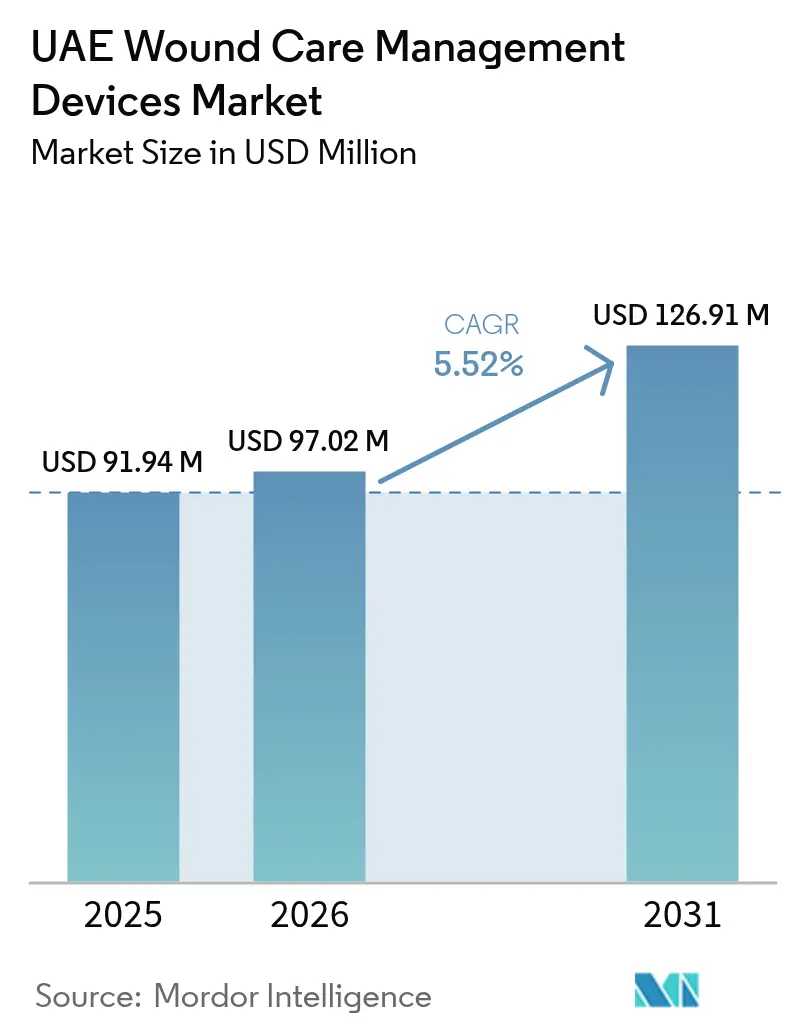

| Base Year Market Size (2025) | USD 91.94 Million |

| Market Size (2026) | USD 97.02 Million |

| Market Size (2031) | USD 126.91 Million |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Wound Care Management Devices Market Analysis by Mordor Intelligence

The UAE wound care management devices market size is expected to grow from USD 91.94 million in 2025 to USD 97.02 million in 2026 and is forecast to reach USD 126.91 million by 2031 at 5.52% CAGR over 2026-2031. Demand growth mirrors the country’s dual role as a regional healthcare hub and a destination for medical tourists seeking sophisticated wound management. Uptake of advanced dressings, neuromuscular electro-stimulation devices, and 4D-bioprinted grafts is accelerating as hospitals compete on clinical outcomes and speed of healing. Rising surgical volumes, a high diabetes prevalence, and new home-care quality mandates add further momentum, while extreme heat logistics and reimbursement gaps temper the pace of adoption. Market competition remains fragmented, with multinationals, regional specialists, and technology start-ups pursuing hospital contracts, home-care partnerships, and product localization initiatives.

Key Report Takeaways

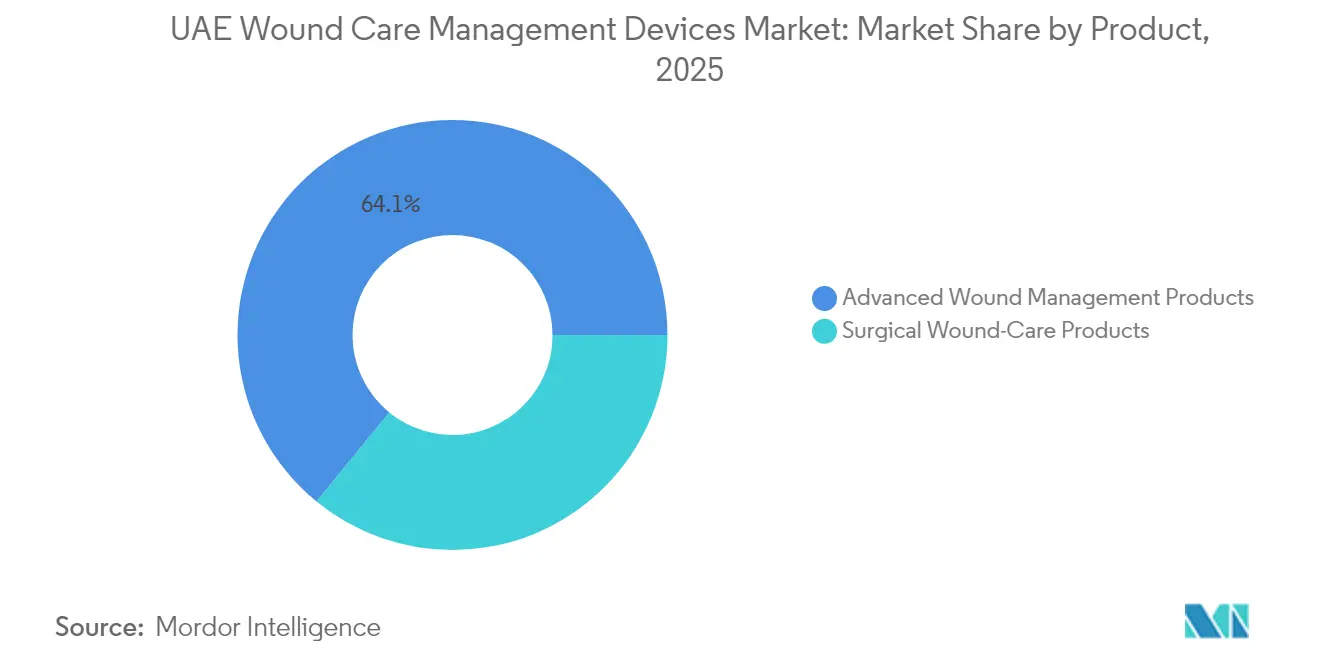

- By product category, Advanced Wound Management Products led with 64.10% revenue share in 2025; Surgical Wound-Care Products are projected to expand at a 6.28% CAGR through 2031.

- By wound type, Chronic Wounds accounted for 60.85% of the UAE wound care management devices market share in 2025, whereas Acute Wounds are advancing at a 6.63% CAGR to 2031.

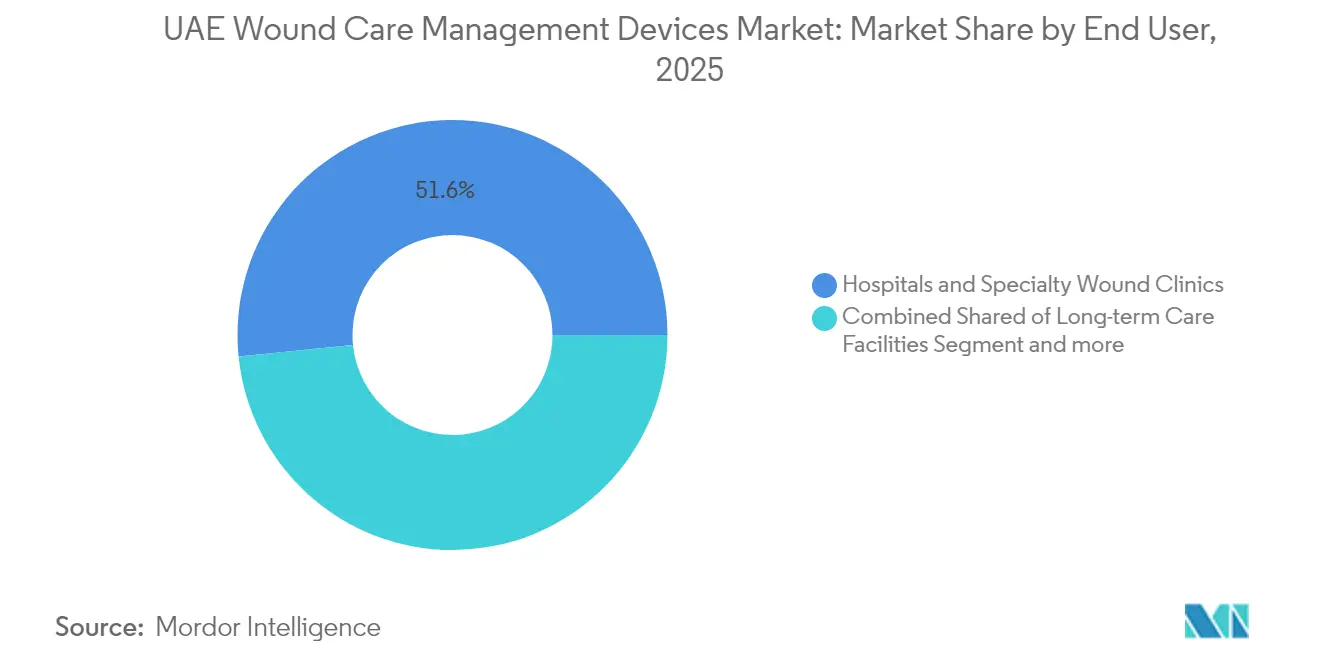

- By end-user setting, Hospitals & Specialty Wound Clinics held 51.60% of the UAE wound care management devices market size in 2025, but Home-Healthcare Settings are growing fastest at a 6.72% CAGR.

- By mode of purchase, Institutional Procurement captured 65.80% of demand in 2025, yet the Retail/OTC Channel is rising at a 6.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic wounds (diabetic foot ulcers, pressure ulcers) | +1.8% | National, concentrated in Dubai and Abu Dhabi | Long term (≥ 4 years) |

| Growth in surgical & trauma procedures | +1.2% | National, with Dubai and Abu Dhabi leading | Medium term (2-4 years) |

| Rapid increase in UAE's ageing/expatriate population & healthcare spend | +1.0% | National, with spillover to Northern Emirates | Long term (≥ 4 years) |

| Federal investments under Dubai Health Strategy | +0.8% | Dubai-centric, with regional expansion | Medium term (2-4 years) |

| DHA-mandated wound-healing Key Performance Indicators for hospitals | +0.5% | Dubai-specific, potential national adoption | Short term (≤ 2 years) |

| Accelerating medical-tourism inflow for advanced wound care | +0.4% | Dubai and Abu Dhabi focused | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds Drives Market Expansion

High diabetes prevalence underpins a steady rise in diabetic foot ulcers, while plantar-pressure studies recording 911 kPa peak forces link gait mechanics to ulcer risk. Multidrug-resistant organisms complicate care, with methicillin-resistant Staphylococcus aureus rates reaching 25–35% across GCC hospitals. In response, the Ministry of Health and Prevention introduced 4D bioprinting to create patient-specific grafts for diabetic wounds, reinforcing the UAE wound care management devices market’s technology leadership. Nursing staff—63,366 professionals across 19,102 beds—now follow enhanced pressure-injury protocols that improve outcomes in acute and home settings. Collectively, these factors lift demand for advanced dressings, antimicrobial gels, and remote-monitoring solutions.

Growth in Surgical & Trauma Procedures Spurs Product Uptake

A national network of hospitals delivers rising volumes of orthopedic, cardiovascular, and bariatric surgeries that require specialized closure materials and infection prevention systems. Dubai’s emergency department KPI framework mandates time-bound wound management [1]Dubai Health Authority, “Guidelines for Reporting Emergency Unit Services KPIs,” dha.gov.ae, steering hospitals toward faster-acting tissue adhesives and negative-pressure wound therapy devices. Medical tourists add further volume, as facilities such as American Hospital Dubai promote complex surgical packages across 30 overseas offices. Surgical growth, therefore, catalyzes the uptake of antimicrobial sutures, collagen dressings, and post-operative compression systems.

Ageing Expatriate Demographics Elevate Long-Term Care Needs

An older expatriate workforce raises the prevalence of venous leg ulcers and pressure injuries, driving demand beyond tertiary hospitals into long-term and community settings. Abu Dhabi’s JAWDA quality program now requires quarterly reporting of pressure-injury incidence in home-care services, positioning data-enabled dressings, and tele-wound platforms as essential for compliance. This demographic shift sustains a structural need for preventative foam dressings, silicone heel protectors, and nurse training programs nationwide.

Federal Investments Under Dubai Health Strategy Accelerate Technology Adoption

Targeted capital projects add 5,770 licensed facilities, including 5,021 private clinics, creating scale for wound-care procurement. The Dubai Health Authority’s outpatient standards mandate infection-control audits and evidence-based wound protocols, prompting health systems to upgrade to moisture-balancing dressings and digital documentation tools. Procurement cycles favor suppliers able to bundle training, data dashboards, and local warehousing, accelerating market penetration of integrated wound-care kits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced consumables & devices | -0.9% | National, stronger in Northern Emirates | Medium term (2-4 years) |

| Limited reimbursement for outpatient modalities | -0.7% | Nationwide, insurer-dependent | Long term (≥ 4 years) |

| Extreme-heat logistics risk to biologic dressings | -0.4% | Nationwide, peak summer | Short term (≤ 2 years) |

| Shortage of certified wound-care nurses | -0.3% | Northern Emirates focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Barriers Limit Advanced Technology Adoption

Premium hydrofiber dressings, negative-pressure pumps, and hyperbaric chambers raise procurement budgets at smaller clinics, especially in the Northern Emirates with tighter funding envelopes. Storage and cold-chain requirements inflate operating costs during 45 °C summer peaks, prompting selective roll-outs and reliance on bulk tenders in Dubai and Abu Dhabi. Providers, therefore, weigh clinical gains against pay-out ratios when adopting next-generation modalities such as growth-factor gels and bioengineered skin substitutes.

Reimbursement Limitations Restrict Outpatient Care Access

Insurance adjudication rules often bundle wound cleansing with evaluation fees, constraining standalone billing for advanced modalities. Home-care nurses must document stringent criteria before payers authorize negative-pressure therapy, delaying initiation and shifting costs to patients [2]Daman, “Wound Care Management – Adjudication Guideline,” damanhealth.ae. As a result, uptake of portable pumps, smart dressings, and single-use NPWT units remains concentrated in premium plans and self-funded expatriate segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Technologies Drive Premium Segment Growth

Advanced Wound Management Products accounted for 64.10% of the UAE wound care management devices market in 2025, reflecting strong demand for alginate, hydrocolloid, and antimicrobial foam dressings used in chronic and post-surgical settings. Deployment of 4D-bioprinted grafts for diabetic foot ulcers underscores hospitals’ preference for regenerative therapies that shorten healing cycles. Surgical Wound-Care Products, though smaller, are set to advance at a 6.28% CAGR as laparoscopic and orthopedic volumes climb, driving sales of absorbable sutures, tissue sealants, and hemostatic patches.

Local manufacturing moves—such as Ayu Life Sciences’ AED 33 million factory in Jebel Ali—promise import substitution, potentially stabilizing prices and insulating hospitals from supply-chain shocks. The UAE wound care management devices industry continues to prize products that integrate moisture control, antimicrobial action, and data capture for KPI reporting.

By Wound Type: Chronic Care Dominance Meets Acute Growth Acceleration

Chronic wounds represented 60.85% of the UAE wound care management devices market share in 2025, driven by diabetic foot ulcers, venous leg ulcers, and pressure injuries common among older expatriates. Hospitals invest in collagen matrices, silver alginates, and compression systems that address biofilm challenges and venous insufficiency.

Acute wounds are projected to expand faster, at a 6.63% CAGR, supported by rising surgical throughput and trauma services that require rapid-closure adhesives and advanced hemostats. As the UAE wound care management devices market size for acute wound supplies grows, vendors highlight ease-of-use kits suited to emergency settings where DHA KPIs specify strict door-to-closure timelines. The UAE wound care management devices industry, therefore, balances chronic protocols with trauma-ready products across its multi-tier health system.

By End-User: Home Healthcare Transformation Challenges Hospital Dominance

Hospitals and specialty clinics held 51.60% of 2025 revenues, benefiting from multidisciplinary teams and reimbursement pathways tailored to inpatient care. They remain the primary customers for negative-pressure consoles, hyperbaric suites, and biosynthetic grafts.

Home-Healthcare Settings, however, will post a 6.72% CAGR as tele-consults, portable NPWT pumps, and adhesive-free dressings such as HidraWear gain traction. The UAE wound care management devices market size for home-based services is widening as JAWDA metrics tie insurer payments to pressure-injury avoidance and rehospitalization rates . Investor interest centers on digital platforms that connect nurses, physicians, and pharmacists in real time, positioning the UAE wound care management devices industry for hybrid care pathways.

By Mode of Purchase: Retail Growth Challenges Institutional Procurement

Institutional procurement commanded 65.80% of purchases in 2025, reflecting centralized tenders by Dubai Health Authority, SEHA and private chains. Bulk orders lock in supply for foam dressings, antimicrobial gels and closure devices across inpatient wards and OR suites.

The retail/OTC channel is forecast to grow at 6.19% CAGR as pharmacies broaden inventories of silicone gel sheets, hydrocolloid patches and wound moisturizers for post-discharge regimens. Consumer education campaigns, coupled with pharmacist training, expand access while easing pressure on outpatient clinics. Nevertheless, insurer copays for OTC items remain limited, capping volume until reimbursement frameworks evolve.

Geography Analysis

Dubai and Abu Dhabi form the commercial heart of the UAE wound care management devices market, housing flagship facilities such as Rashid Hospital and Cleveland Clinic Abu Dhabi that attract regional and international patients. Both emirates leverage medical-tourism branding, with Dubai Healthcare City and American Hospital’s overseas offices funneling complex wound cases into local centers. Investment in data-linked wound programs aligns with DHA outpatient standards and emergency KPIs, ensuring consistent adoption of integrated dressings, digital photography, and outcome dashboards.

Abu Dhabi complements this by enforcing JAWDA quality benchmarks across its public and private sectors, compelling providers to log pressure-injury rates and healing times. These mandates require electronic health record integration and analytics-ready dressings that upload exudate trends for clinician review. As a result, software-enabled wound platforms gain a foothold alongside traditional consumables.

The Northern Emirates—Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain—present lower facility density and workforce challenges. Scholarship graduates often relocate south, leaving shortages of certified wound nurses that restrict advanced-therapy adoption. Nonetheless, Ministry of Health and Prevention initiatives such as portable 4D-bioprint labs aim to extend cutting-edge care nationwide, signalling longer-term convergence in service levels.

Competitive Landscape

The UAE wound care management devices market is moderately fragmented. Global leaders like Mölnlycke, ConvaTec and Smith+Nephew supply broad portfolios of dressings, NPWT and biosurgeries used in institutional tenders. They compete with technology innovators such as Sky Medical Technology, whose geko neuromuscular-stimulation device has been adopted by Genesis Healthcare, Dubai London Hospital and Mediclinic Parkview Hospital, accelerating post-operative microcirculation.

Local manufacturing is emerging as a differentiator. Ayu Life Sciences’ forthcoming Jebel Ali facility will produce Velgraft and Velvert artificial skin lines, potentially reducing import reliance and customs lead times. Distribution alliances also shape competition; Hidramed Solutions granted Razan Medical a three-year exclusive for its adhesive-free dressings, broadening access across pharmacy and home-care channels.

Digital health capabilities offer additional competitive levers. Vendors integrating wound-image AI, exudate sensors and auto-generated KPI reports align closely with DHA and DoH compliance needs. As home-care volumes mount, suppliers that bundle tele-nursing platforms with consumables are poised to gain share, particularly in insurer-backed chronic-care programs.

UAE Wound Care Management Devices Industry Leaders

Smith & Nephew Plc

Medtronic Plc

Coloplast A/S

ConvaTec Group plc

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Ayu Life Sciences committed AED 33 million (USD 8.99 million) to a Jebel Ali Free Zone plant for Velgraft, Velvert and VelNez artificial-skin products, targeting late-2025 launch with GCC distribution capabilities

- January 2025: Dubai Health Authority enforced outpatient facility standards that elevate wound-care protocols, infection control and documentation across emirate-wide clinics.

- September 2024: OXYBARICA declared Middle East entry plans for hyperbaric oxygen therapy systems, prioritizing diabetic ulcer and radiation injury centers in Dubai and Abu Dhabi

- September 2024: Hidramed Solutions signed a three-year distribution agreement with Razan Medical for adhesive-free HidraWear dressings following UAE regulatory approval.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the UAE wound care management devices market as the sale of equipment and consumable devices designed to cleanse, close, or actively heal acute or chronic wounds. This includes advanced dressings (film, foam, alginate, hydrogel, hydrocolloid, collagen and silver-based), negative-pressure wound therapy systems, oxygen and hyperbaric devices, electrical stimulation units, pressure-relief devices, and surgical closure tools such as sutures, staples, tissue adhesives, and sealants.

Scope exclusion: Traditional cotton gauze, generic antiseptics, and any pharmaceuticals solely used for infection control are outside the modeled revenue pool.

Segmentation Overview

- By Product

- Advanced Wound Management Products

- Advanced Wound Dressings

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Other Advanced Dressings

- Wound Therapy Devices

- Pressure-relief Devices

- Negative Pressure Wound Therapy (NPWT) Systems

- Oxygen & Hyperbaric Oxygen Equipment

- Electrical Stimulation Devices

- Other Therapy Devices

- Advanced Wound Dressings

- Surgical Wound-Care Products

- Sutures & Staples

- Tissue Adhesives / Sealants / Glues

- Advanced Wound Management Products

- By Wound Type

- Chronic Wounds

- Diabetic Foot Ulcers

- Venous Leg Ulcers

- Pressure Ulcers

- Acute Wounds

- Surgical / Traumatic Wounds

- Burns

- Chronic Wounds

- By End-User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

- By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Interviews with wound-care nurses, biomedical engineers, procurement officers, and regional distributors across Dubai, Abu Dhabi, and Sharjah allowed us to verify utilization rates, average selling prices, and typical replacement cycles. Follow-up surveys with home-health providers highlighted rising demand for portable NPWT systems among diabetic patients. These insights filled data gaps and aligned model assumptions with real-world practice.

Desk Research

We built the foundation with authoritative data from sources such as the UAE Ministry of Health & Prevention, Dubai Health Authority inpatient statistics, the International Diabetes Federation, UN Comtrade shipment codes 3005 and 9018, peer-reviewed articles on diabetic foot prevalence in the Gulf, and trade-association newsletters from the European Wound Management Association. Company filings, investor decks, and selected paid databases, including D&B Hoovers for hospital procurement spend and Dow Jones Factiva for tender notices, helped size supplier footprints.

Regulatory updates from the Emirates Health Services portal and patent trends pulled through Questel gave context on device innovation flows. This list is illustrative; many other public and proprietary references were reviewed to cross-check figures and clarify gray areas.

Market-Sizing & Forecasting

A top-down reconstruction from hospital procedure volumes, diabetic prevalence, and import-export tallies is corroborated with selective bottom-up checks such as sampled ASP times unit shipments and channel stock audits. Key variables include: (1) diabetes incidence per 1,000 adults, (2) lower-limb amputation surgery counts, (3) licensed hospital bed growth, (4) median wound-closure device ASP shifts, and (5) NPWT penetration in chronic ulcer care. Multivariate regression, validated through expert consensus, projects these drivers to 2030; any supply disruptions are modeled through scenario analysis. Gaps in bottom-up estimates are adjusted by aligning distribution mark-ups with tender price logs.

Data Validation & Update Cycle

Mordor analysts run variance checks against import invoices and insurance reimbursement dashboards before sign-off. Reports refresh every twelve months, with interim adjustments triggered by currency swings above 8 percent or material regulatory changes; a final analyst review ensures clients receive the latest calibrated view.

Why Mordor's UAE Wound Care Management Baseline Commands Reliability

Published market values often diverge.

Differences in scope, device mix, and refresh cadence mean numbers will rarely match line-for-line.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 91.94 M (2025) | Mordor Intelligence | - |

| USD 151.8 M (2024) | Global Consultancy A | Includes traditional gauze and wound wash, uses GCC-level shipment allocation ratios |

| USD 147.7 M (2024) | Industry Journal B | Adds OTC creams, assumes flat device ASPs and five-year-old diabetes data |

The comparison shows that when scope is tightly focused on regulated devices and variables are refreshed annually, Mordor's baseline yields a narrower yet more decision-ready figure that executives can trace back to transparent drivers and reproducible steps.

Key Questions Answered in the Report

What is the current value of the UAE wound care market?

The market stands at USD 97.02 million in 2026 and is projected to grow to USD 126.91 million by 2031.

Which product segment leads the UAE wound care market?

Advanced Wound Management Products hold the largest share at 64.10% and dominate procurement in hospitals and specialty clinics.

Why are home-healthcare services growing rapidly in UAE wound care?

Home-care growth stems from patient convenience, quality mandates such as Abu Dhabi’s JAWDA indicators, and portable technologies that enable complex wound management outside hospitals.

What factors restrain wider adoption of advanced wound technologies?

High device costs, limited outpatient reimbursement, extreme-heat logistics and a shortage of certified wound nurses in smaller emirates are key barriers.

How does medical tourism influence demand?

Medical tourists seeking complex surgeries in Dubai and Abu Dhabi amplify demand for premium dressings, NPWT systems and regenerative therapies that speed recovery and minimize scarring.

Which emirates generate most UAE wound care revenue?

Dubai and Abu Dhabi lead, backed by advanced infrastructure, regulatory KPIs and targeted federal investment that drive consistent adoption of cutting-edge wound solutions.

Page last updated on: