Tyrosine Kinase Inhibitors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

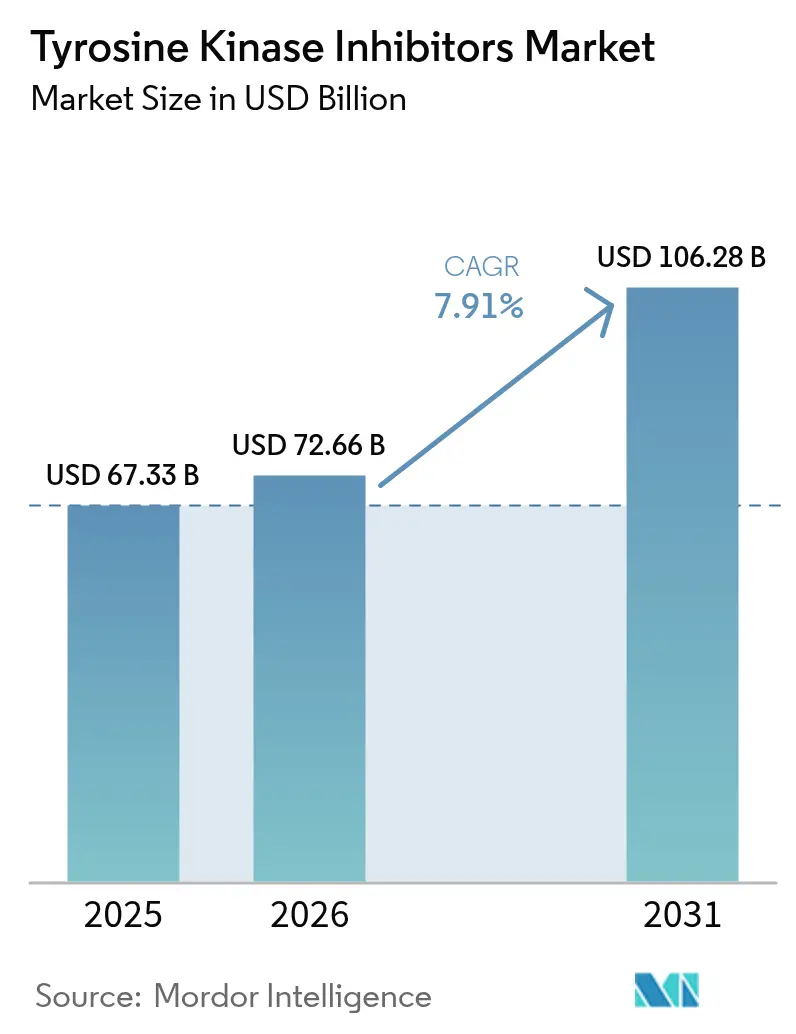

| Market Size (2026) | USD 72.66 Billion |

| Market Size (2031) | USD 106.28 Billion |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

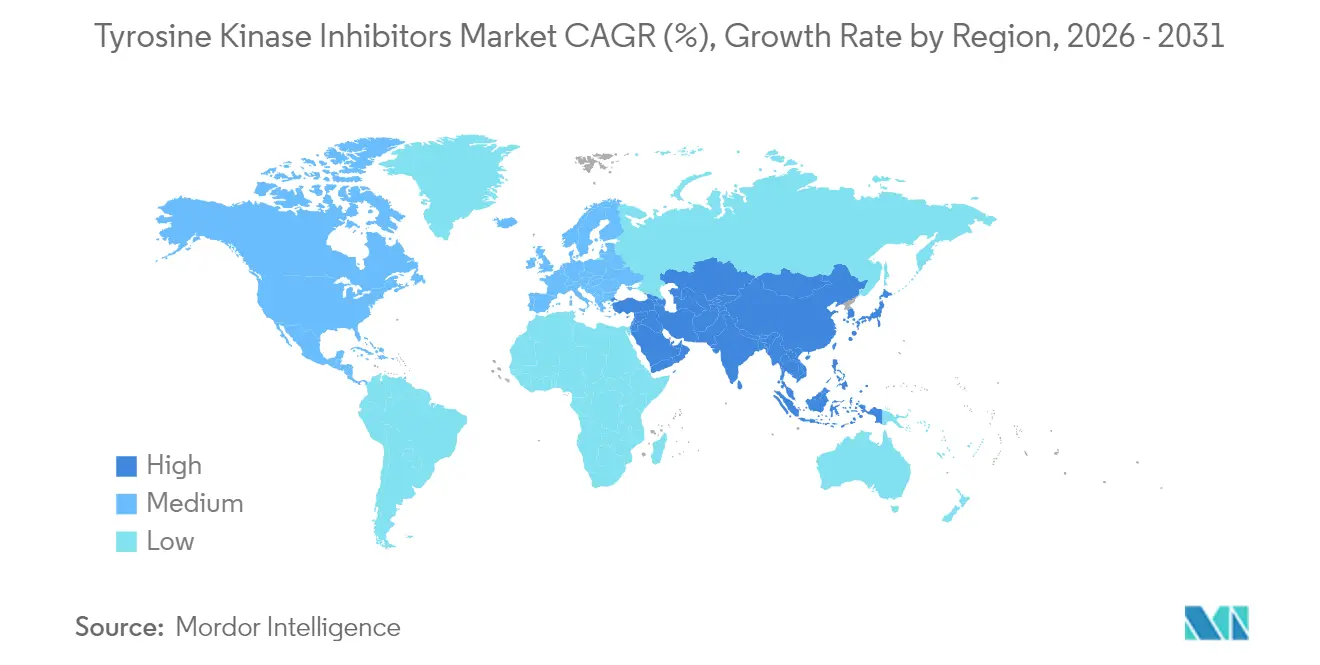

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tyrosine Kinase Inhibitors Market Analysis by Mordor Intelligence

The tyrosine kinase inhibitors market size is expected to grow from USD 67.33 billion in 2025 to USD 72.66 billion in 2026 and is forecast to reach USD 106.28 billion by 2031 at 7.91% CAGR over 2026-2031. This expansion is propelled by patent expirations that stimulate generic competition, artificial-intelligence platforms that shorten discovery cycles, and the clinical convenience of oral formulations that improve adherence. North America remains the revenue leader, yet Asia-Pacific records the fastest uptake thanks to regulatory harmonization, infrastructure upgrades, and a rapidly growing cancer burden. Target-specific drug design keeps EGFR inhibitors on top, while BTK inhibitors post the highest growth as developers move into solid tumors. Oral delivery dominates because it cuts infusion chair time and lowers overall treatment costs, and the onset of online pharmacies showcases digital health’s disruptive role. Meanwhile, resistance mutations and cardiovascular toxicities temper momentum, prompting investment in fourth-generation agents paired with companion diagnostics that guide precise patient selection.

Key Report Takeaways

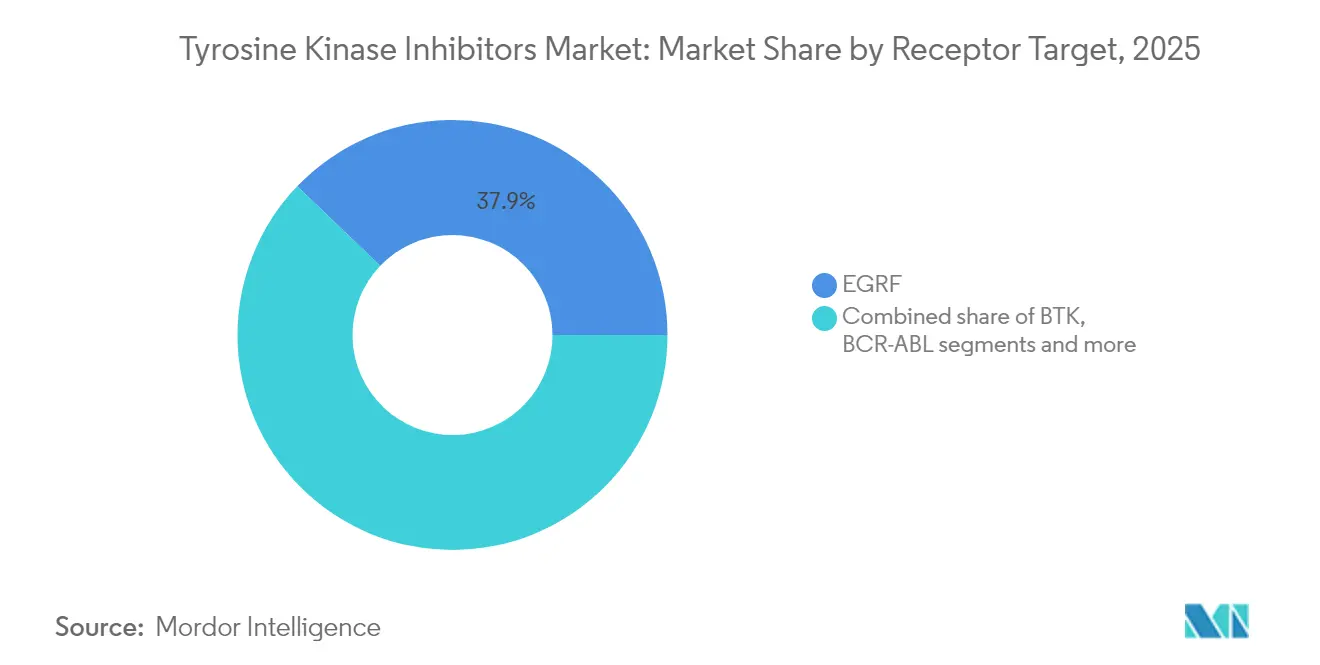

- By target receptor, EGFR inhibitors led with 37.85% of tyrosine kinase inhibitors market share in 2025; BTK inhibitors are projected to expand at an 8.78% CAGR through 2031.

- By application, non-small cell lung cancer accounted for 42.10% of the tyrosine kinase inhibitors market size in 2025, while hepatocellular carcinoma is advancing at a 9.01% CAGR to 2031.

- By generation, fourth-generation agents posted the fastest 2026-2031 CAGR at 11.03% as pipelines pivot to resistance-proof designs.

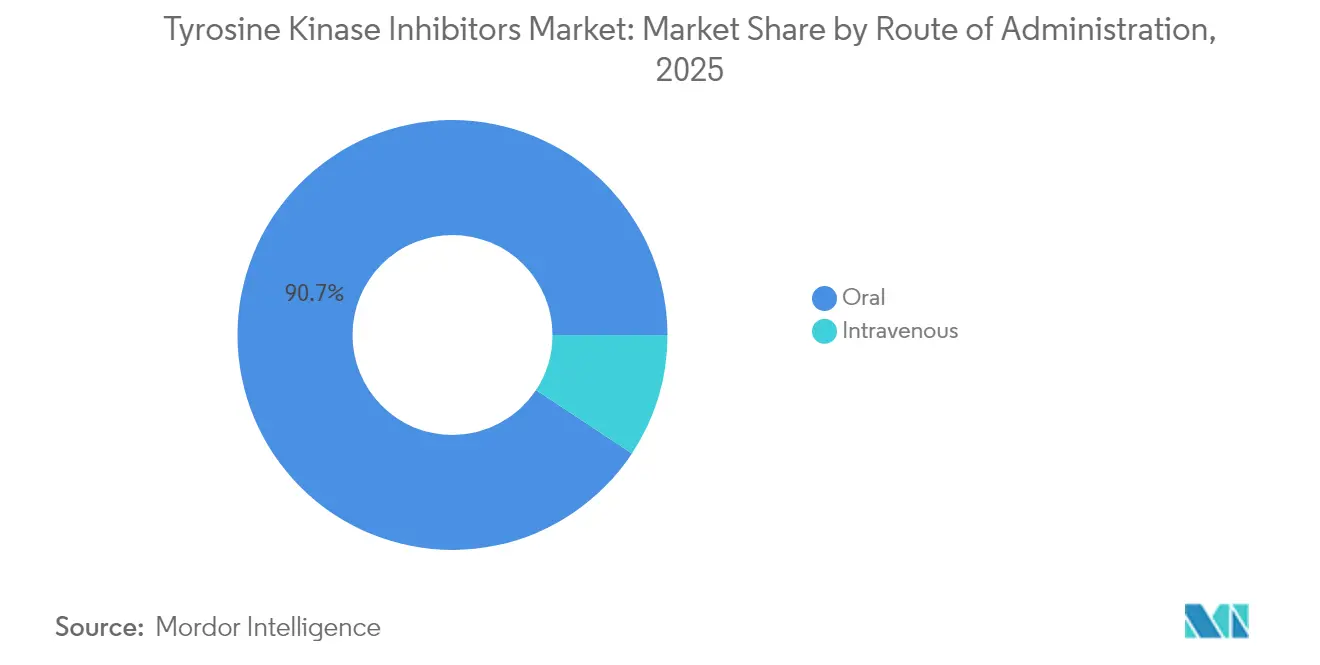

- By route of administration, oral formulations captured 90.72% revenue share in 2025 and are forecast to grow at 9.86% CAGR through 2031.

- By distribution channel, hospital pharmacies held 58.30% share in 2025, whereas online pharmacies are set to widen at 9.55% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tyrosine Kinase Inhibitors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of TKI-amenable cancers | +1.8% | Global, with highest impact in Asia-Pacific and North America | Long term (≥ 4 years) |

| Favourable reimbursement & guideline inclusion | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Patent cliffs enabling generic TKIs | +2.1% | Global, with accelerated impact in emerging markets | Short term (≤ 2 years) |

| Oral formulations boosting patient adherence | +0.9% | Global, particularly in outpatient care settings | Medium term (2-4 years) |

| AI-driven kinase modelling accelerating pipelines | +1.4% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of TKI-Amenable Cancers

Roughly 30% of solid tumors now reveal actionable kinase alterations through next-generation sequencing, widening the eligible patient pool for targeted therapy. Improved profiling uncovers rare drivers such as ROS1 fusions and MET exon 14 skipping, which Chinese regulators addressed by approving taletrectinib in June 2025. Aging populations and smoking prevalence push lung and liver cancer cases higher across Asia, while comprehensive genomic screening identifies candidates for existing regimens and spotlights novel targets.

Favorable Reimbursement & Guideline Inclusion

Value-based pricing frameworks in the United States, Europe, and Japan reward long-term health outcomes rather than unit sales, translating guideline upgrades directly into payer coverage. The 2024 NCCN update named several TKI combinations as preferred first-line therapies, triggering automatic formulary adoption by U.S. insurers. Japan now grants 5-10% price premiums for fast-tracked oncology drugs, incentivizing rapid market entry and offsetting development risk.

Patent Cliffs Enabling Generic TKIs

A wave of expirations through 2028 for first- and second-generation molecules opens the door for generics, historically cutting average selling prices by up to 80%. European guidelines already prioritize generic imatinib for chronic myeloid leukemia where clinical parity exists, expanding access in public systems . Regulatory simplification for complex small-molecule generics further accelerates approval timelines, especially in price-sensitive emerging markets.

Oral Formulations Boosting Patient Adherence

Real-world evidence shows oral TKIs reduce 30-day hospital admissions by 25% relative to infusion therapies, translating into lower episodic care costs[1]Source: Kite Pharma, “Real-World Data Supporting Yescarta in Outpatient Care,” kitepharma.com . Patients value convenience, absence of infusion reactions, and home dosing flexibility, driving 90% treatment persistence at 12 months in some studies. Fixed-dose and once-daily pills enhance adherence, and payers increasingly favor outpatient regimens that free infusion center capacity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy cost & value-based pricing pressure | -1.1% | Global, with highest impact in price-sensitive markets | Medium term (2-4 years) |

| Emergence of resistance mutations | -0.8% | Global, particularly affecting long-term treatment outcomes | Long term (≥ 4 years) |

| Cardiovascular toxicities prompting label warnings | -0.6% | Global, with enhanced regulatory scrutiny in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Value-Based Pricing Pressure

Payers now demand real-world cost-effectiveness beyond trial endpoints, placing risk on manufacturers to deliver outcome guarantees. Some European HTA bodies denied premium pricing for new agents lacking robust comparative evidence. Biosimilar entry adds downward pressure, possibly constraining R&D budgets for next-generation projects when return-on-investment thresholds tighten.

Emergence of Resistance Mutations

Most patients relapse within 12-18 months as tumors activate bypass pathways. Managing sequential treatments inflates total care costs and complicates dosing strategies. Providers need advanced diagnostics to guide switches, which can be scarce in resource-limited settings. Combination regimens curb resistance but raise toxicity and price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Target Receptor: Established EGFR Dominance Meets BTK Momentum

EGFR inhibitors contributed 37.85% of 2025 revenue due to their central role in biomarker-defined lung cancer. Recent conditional approval of Tagrisso for unresectable Stage III EGFR-mutated NSCLC further enlarged the eligible population. Meanwhile, BTK inhibitors registered an 8.78% CAGR as agents like pirtobrutinib moved into mantle cell lymphoma and exploratory solid-tumor studies. The tyrosine kinase inhibitors market size for BTK therapies is projected to add USD 3.82 billion by 2031. Competitive dynamics now pivot on tackling resistance; fourth-generation EGFR and non-covalent BTK scaffolds aim to sustain long-term control. Portfolio broadening also extends to VEGFR and ALK franchises, but their growth trails the BTK surge.

EGFR developers focus on combination regimens with immunotherapy, while BTK pipelines test tissue-agnostic designs compatible with FDA guidance released in 2025. Novel KAT6A and RET fusions illustrate discovery breadth, often seeded by AI screening. As companion diagnostics spread, target-specific uptake will mirror testing availability, reinforcing EGFR and BTK leadership yet allowing niche kinases to emerge.

By Application: NSCLC Leads; HCC Accelerates

Non-small cell lung cancer retained 42.10% revenue in 2025, supported by mature testing pathways and multiple approved regimens. Yet hepatocellular carcinoma displays the fastest 9.01% CAGR to 2031 as kinase-focused therapies outperform systemic standards, drawing developers to liver oncology. The tyrosine kinase inhibitors market share within HCC is expected to surpass 8% by 2031 as biomarkers expand eligibility. Breast and renal cancers continue stable demand through CDK4/6 and VEGF pathways, while basket trials test inhibitors across mutation-defined cohorts.

NSCLC strategy now segments patients by EGFR, ALK, ROS1, and MET alterations, enabling personalized first-line choices. HCC growth benefits from improved surveillance in hepatitis-driven geographies and better understanding of kinase biology. Basket designs may blur organ-based lines, letting rare tumors access targeted agents sooner.

By Generation: Fourth-Gen Wave Targets Resistance

Fourth-generation molecules record an 11.03% CAGR as their designs neutralize common escape mutations without heightening toxicity. Scemblix’s 2024 FDA nod in frontline CML demonstrated superior molecular response versus first-line standards. First-generation drugs persist via generics meeting cost-effectiveness goals, while second-generation agents face margin pressure. Third-generation options keep relevance in specific resistance niches but risk cannibalization by newer entrants.

Pharma learning curves show each generation fixing prior limits-greater selectivity, brain penetration, or allosteric binding. AI tools flatten discovery timelines, hinting at even quicker fifth-generation iterations that mix multi-target inhibition with favorable safety.

By Route of Administration: Oral Convenience Reigns

Oral products seized 90.72% of 2025 sales and are on track for 9.86% CAGR. Patients prefer home dosing, and payers value avoided infusion costs. The tyrosine kinase inhibitors market size attached to oral formats hit USD 61.09 billion in 2025 and should cross USD 95.62 billion by 2031. Intravenous agents linger for acute settings where rapid systemic exposure is critical, yet uptake wanes as oral bioavailability improves.

Developers pursue extended-release capsules and fixed-dose co-formulations to lift adherence. Vertex’s 2025 JOURNAVX launch reinforced premium pricing viability when differentiation is clear. Regulators now advise early oral feasibility work to de-risk programs.

By Distribution Channel: Hospital Control Meets Digital Surge

Hospital pharmacies delivered 58.30% of 2025 volume, justified by initiation protocols and adverse-event oversight. Online outlets expand fastest at 9.55% CAGR as oncology-focused platforms bundle delivery with adherence tools. Retail chains hold a bridging role, offering in-person counseling yet adding telepharmacy functions.

Hybrid models emerge where hospitals oversee first cycles, then transition stable patients to mail-order refills. Regulatory bodies craft e-pharmacy standards to safeguard potency and track pharmacovigilance, fostering trust in digital options.

Geography Analysis

North America held 37.90% of 2025 global revenue, reflecting advanced diagnostics, favorable coverage, and strong clinical-trial pipelines. The United States leads approvals, aided by accelerated review programs and large oncology budgets. Canada’s alignment with FDA decisions, seen in Tagrisso’s conditional 2025 nod, accelerates binational launches. Mexico gains through regional manufacturing and generic uptake, widening access to established regimens.

Asia-Pacific records a 10.74% CAGR, powered by China’s swift approvals under NMPA’s priority pathways and Japan’s price-premium policy for innovative medicines. India lifts volumes through government insurance expansion and domestic API capacity, while South Korea and Australia maintain high per-capita spending on precision oncology. Rising incomes and urbanization generate sustainable demand, and local companies increasingly co-develop agents for regional mutations.

Europe shows steady growth anchored in centralized EMA approvals yet tempered by country-level cost reviews. Germany and the United Kingdom swiftly integrate successful phase III data into reimbursement, whereas Spain and Italy apply stricter budget tests. Outcomes-based agreements spread, aligning insurer payments with real-world effectiveness. The continent also shapes global standards through scientific advice to foreign sponsors.

Competitive Landscape

The tyrosine kinase inhibitors market exhibits moderate concentration: the top five firms held about 60% of 2024 sales. AstraZeneca, Novartis, and Roche enjoy portfolio breadth, defensive patent estates, and manufacturing scale, but face erosion from generic entry and nimble biotech challengers. Strategic themes center on combination regimens that defer resistance, AI-enabled target discovery, and tissue-agnostic development to widen labels with smaller trials.

Mergers and licensing deals feature prominently. GSK’s USD 1.15 billion buyout of IDRx adds a gastrointestinal stromal tumor candidate, while Servier’s USD 780 million pact with Black Diamond secures rights to a RAS-focused agent. Big Pharma often trades upfront cash for diversified pipelines that hedge against individual asset risk. Biotechs leverage AI to shorten cycles, courting larger partners once proof-of-concept data emerges.

Real-world data and digital therapeutics now underpin competitive moats. Firms embed remote monitoring apps to collect adherence metrics that support value-based contracts. Companion diagnostics co-launched with drugs ensure rapid patient identification, boosting uptake and creating reimbursement rationale.

Tyrosine Kinase Inhibitors Industry Leaders

Boehringer Ingelheim International

F. Hoffmann-La Roche

AstraZeneca plc

Novartis AG

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Health Canada conditionally cleared Tagrisso for unresectable Stage III EGFR-mutated NSCLC.

- January 2025: Nuvation Bio gained Chinese approval for taletrectinib in ROS1-positive NSCLC, the first such TKI in Asia

Global Tyrosine Kinase Inhibitors Market Report Scope

As per the scope of the report, a tyrosine kinase inhibitor (TKI) is a pharmaceutical drug that inhibits tyrosine kinases. Tyrosine kinases are enzymes responsible for the activation of many proteins by signal transduction cascades. The Tyrosine Kinase Inhibitors Market is segmented by Type (BCR-ABL Tyrosine Kinase Inhibitor, Epidermal Growth Factor Receptor (EGFR) Tyrosine Kinase Inhibitors, Vascular Endothelial Growth Factor Receptor (VEGFR) Tyrosine Kinase Inhibitors, BRAF Kinase Inhibitors, ROS1 Inhibitors, and Other Types), Application (Chronic Myeloid Leukemia (CML), Lung Cancer, Breast Cancer, Renal Cell Cancer, and Other Applications), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| BCR-ABL |

| EGFR |

| VEGFR |

| ALK |

| BTK |

| Others |

| Chronic Myeloid Leukemia (CML) |

| Non-Small Cell Lung Cancer (NSCLC) |

| Breast Cancer |

| Renal Cell Carcinoma |

| Hepatocellular Carcinoma |

| Other Solid Tumors |

| First Generation |

| Second Generation |

| Third Generation |

| Fourth & Next-Gen |

| Oral |

| Intravenous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Target Receptor | BCR-ABL | |

| EGFR | ||

| VEGFR | ||

| ALK | ||

| BTK | ||

| Others | ||

| By Application / Indication | Chronic Myeloid Leukemia (CML) | |

| Non-Small Cell Lung Cancer (NSCLC) | ||

| Breast Cancer | ||

| Renal Cell Carcinoma | ||

| Hepatocellular Carcinoma | ||

| Other Solid Tumors | ||

| By Generation | First Generation | |

| Second Generation | ||

| Third Generation | ||

| Fourth & Next-Gen | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the tyrosine kinase inhibitors market in 2026?

The market is valued at USD 72.66 billion in 2026 and is forecast to reach USD 106.28 billion by 2031 at a 7.91% CAGR.

Which application segment is currently the largest user of TKIs?

Non-small cell lung cancer represents 42.10% of global 2025 revenue due to comprehensive biomarker testing and multiple approved first-line regimens.

Why are BTK inhibitors growing faster than other target classes?

BTK agents post an 8.78% CAGR because improved selectivity cuts off-target effects and developers are expanding into solid tumors beyond hematologic cancers.

What factor most limits long-term TKI efficacy?

The emergence of resistance mutations, often within 12-18 months of treatment start, undercuts durable responses and drives the need for next-generation agents.

Which region is expected to see the quickest uptake through 2031?

Asia-Pacific shows the fastest regional CAGR at 10.74%, aided by accelerated approvals in China and pricing incentives in Japan.

How is AI affecting TKI drug development timelines?

Machine-learning models predict binding and resistance patterns, shrinking lead-optimization cycles and supporting collaborations like the USD 500 million MenariniInsilico deal.

Page last updated on: