Doxorubicin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

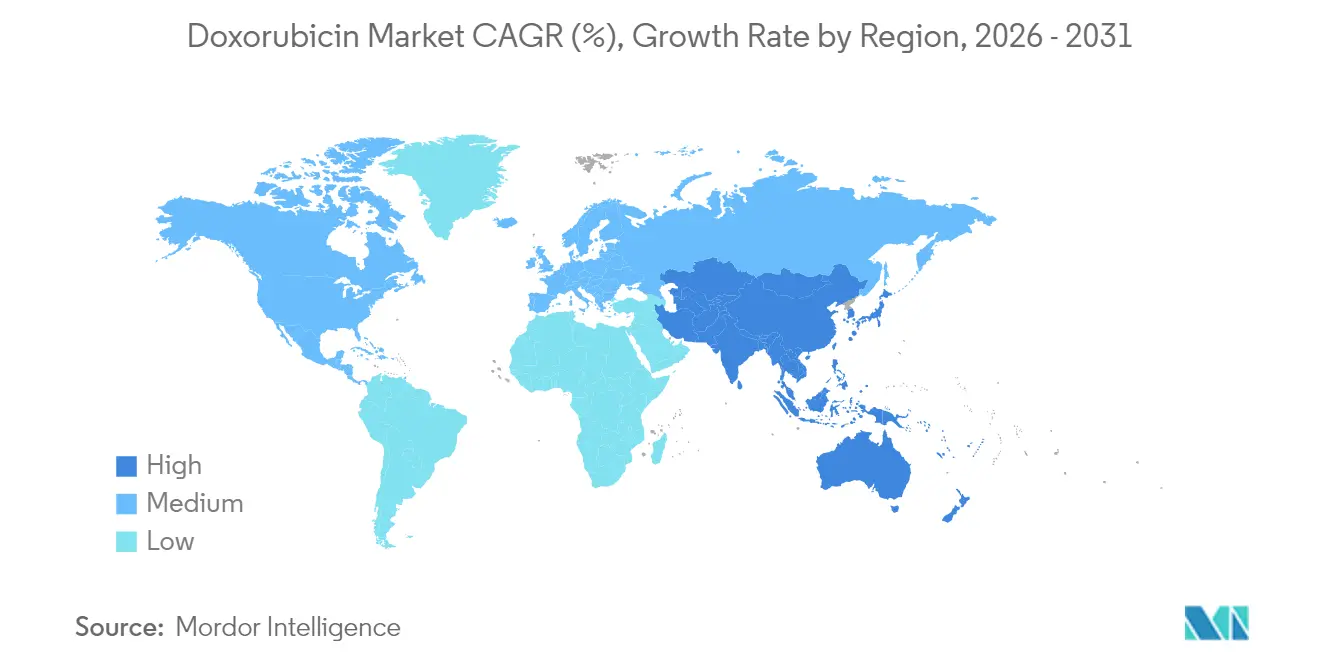

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

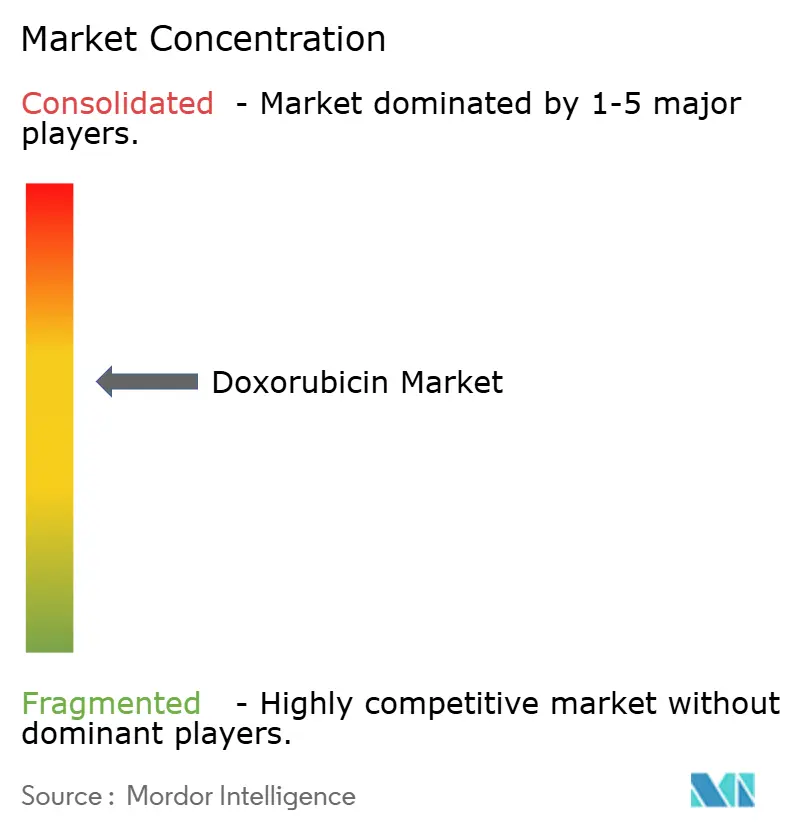

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Doxorubicin Market Analysis by Mordor Intelligence

Doxorubicin market size in 2026 is estimated at USD 1.3 billion, growing from 2025 value of USD 1.22 billion with 2031 projections showing USD 1.77 billion, growing at 6.42% CAGR over 2026-2031. Robust clinical evidence keeps the agent at the center of many oncology protocols, and continuous advances in liposomal delivery expand its therapeutic window. Sustained cancer prevalence, wider generic availability, and targeted formulation innovations are reinforcing demand even as high-cost biologics compete for market share. At the same time, cardiotoxicity concerns, stricter hazardous-drug handling rules, and workflow shifts toward specialty pharmacy models temper longer-term uptake.

Key Report Takeaways

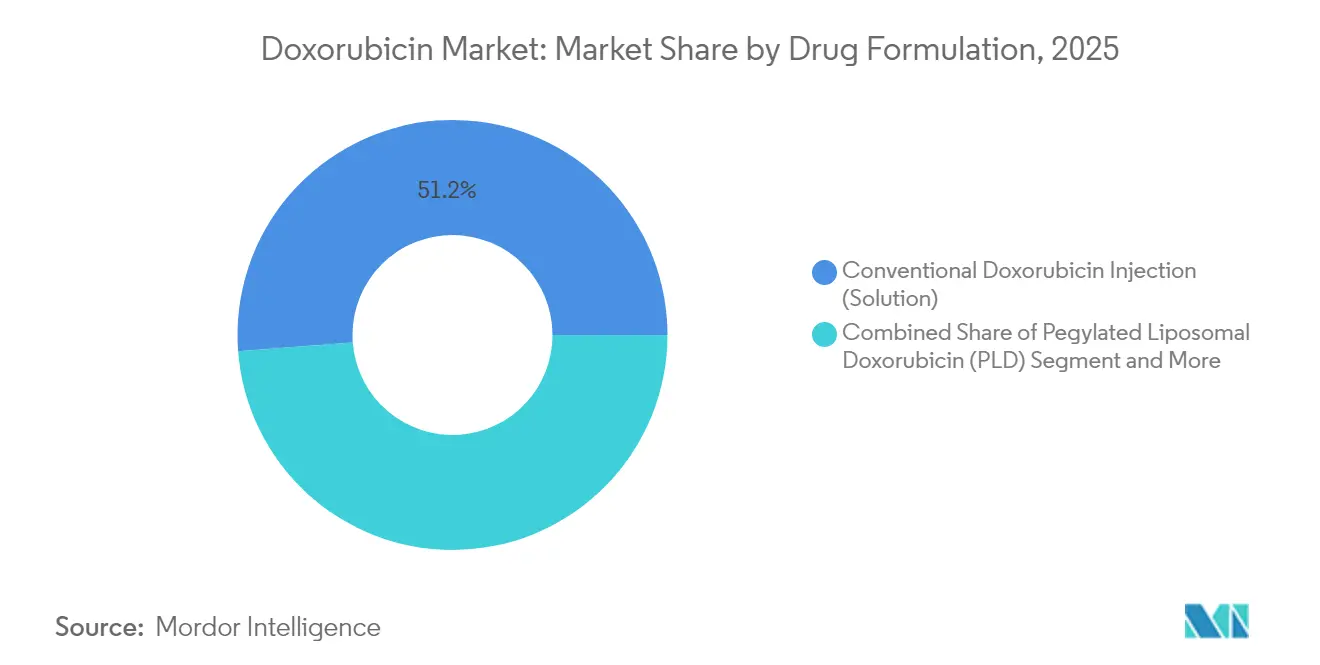

- By drug formulation, conventional doxorubicin injection led with 51.20% of the doxorubicin market share in 2025, while pegylated liposomal doxorubicin is set to grow at a 7.34% CAGR to 2031.

- By application, breast cancer accounted for 21.60% of the doxorubicin market size in 2025; ovarian cancer is advancing at an 7.88% CAGR through 2031.

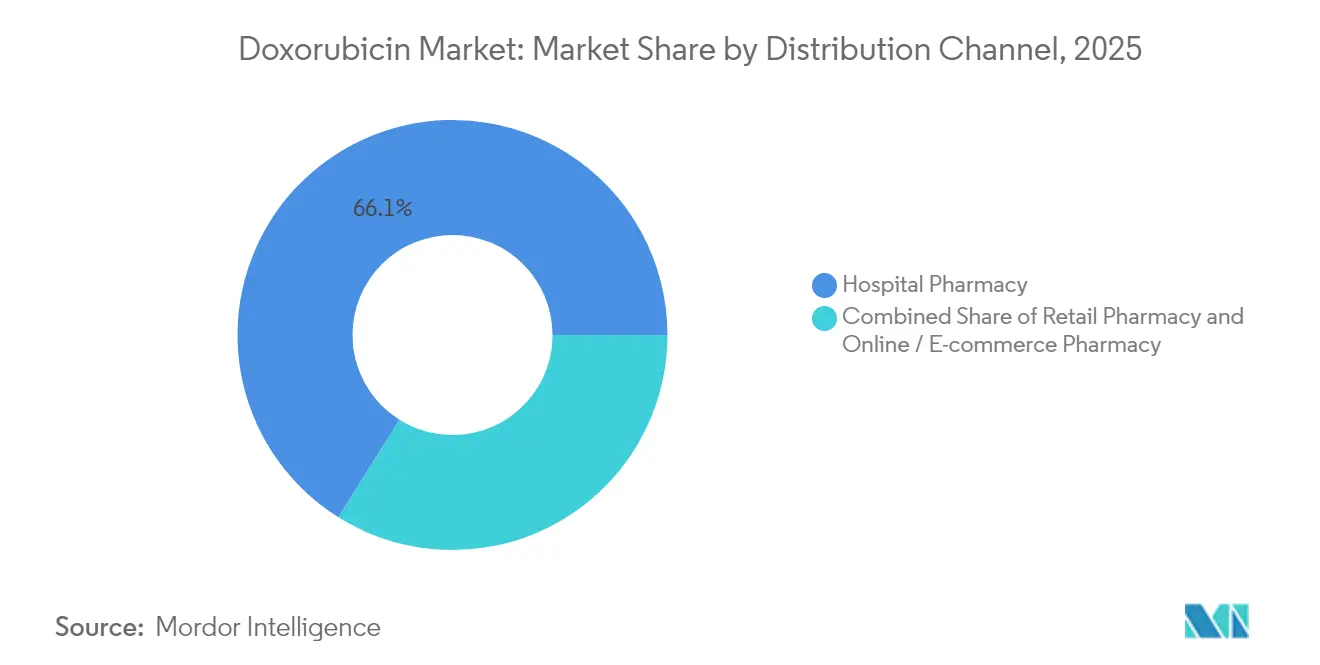

- By distribution channel, hospital pharmacies held 66.10% revenue share in 2025, whereas online/e-commerce pharmacies are growing at a 8.72% CAGR to 2031.

- By geography, North America captured 47.55% of the doxorubicin market size in 2025, and Asia-Pacific is the fastest-expanding region with an 8.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Doxorubicin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global cancer burden | +2.1% | Global, higher in Asia-Pacific | Long term (≥ 4 years) |

| Affordable generic & liposomal options | +1.8% | Emerging markets | Short term (≤ 2 years) |

| Progress in liposomal & nanocarrier delivery | +1.5% | North America & Europe, rising in APAC | Medium term (2-4 years) |

| Government-led oncology expansion programs | +1.2% | APAC, MEA, South America | Medium term (2-4 years) |

| Wider use in hematologic combination regimens | +0.9% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Cancer Burden Elevating Chemotherapy Volumes

Rising worldwide cancer incidence is driving persistent use of broad-spectrum cytotoxics such as doxorubicin. Even as precision biologics proliferate, clinicians continue to rely on anthracycline-taxane combinations for breast tumors with high recurrence scores, showing superior survival versus taxane monotherapy in recent Phase 3 data presented at the San Antonio Breast Cancer Symposium. Versatility across solid and hematologic indications expands procedure volumes, reinforcing the doxorubicin market despite premium biologic entrants.

Growing Availability of Affordable Generic & Liposomal Doxorubicin

Intensifying generic competition is widening patient access and pressuring prices. New entrants such as Lupin introduced doxorubicin hydrochloride liposome injection in the United States in August 2024, enlarging the liposomal category and catalyzing broader adoption in budget-constrained health systems[1]Lupin, “Lupin Launches Doxorubicin Hydrochloride Liposome Injection in the United States,” lupin.com. This influx of lower-priced alternatives supports treatment equity in Asia-Pacific and Latin America, further stimulating doxorubicin market growth.

Technological Progress in Liposomal & Nanocarrier Delivery

Pegylated liposomal doxorubicin formulations such as Doxil/Caelyx mirror the efficacy of conventional drug while markedly reducing cardiotoxicity, enabling higher cumulative dosing for frailer cohorts. Research into pH-responsive nanoparticles and thermosensitive liposomes promises tumor-triggered release, sharpening therapeutic precision. These advances expand prescriber confidence and heighten competitive differentiation, accelerating the doxorubicin market trajectory.

Government-Led Cancer Care Expansion Programs in Emerging Markets

Emerging economies are prioritizing oncology capacity. Infrastructure build-outs and insurance expansion across India, China, the Gulf states, and parts of Africa are raising chemotherapy utilization. China alone accounted for 60% of new global ADC trials in 2023, reflecting robust policy support for cancer innovation. These initiatives create fertile ground for the doxorubicin market, particularly for companies offering differentiated liposomal formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cumulative cardiotoxicity risk | −1.4% | Global | Long term (≥ 4 years) |

| Shift toward targeted therapies & IO agents | −1.7% | North America & Europe | Medium term (2-4 years) |

| Stringent hazardous-drug handling standards | −0.8% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cumulative Cardiotoxicity Risk Necessitating Strict Dose Caps & Monitoring

Anthracycline-induced cardiomyopathy limits lifetime exposure, with cumulative dose caps of 450-550 mg/m² enshrined in guidelines. Although dexrazoxane offers partial protection, no other FDA-approved cardioprotective agent exists, forcing prescribers to juggle efficacy and long-term cardiac safety. This restraint slows repeat-cycle utilization within the doxorubicin market, spurring innovation in safer delivery platforms.

Shift Toward Targeted Therapies and Immuno-Oncologics Displacing Anthracyclines

High-efficacy ADCs such as trastuzumab deruxtecan have outperformed conventional chemotherapy in HER2-positive breast cancer, edging anthracyclines toward earlier-line use in wealthy markets. Budget impact modeling still favors doxorubicin in many public systems, yet the strategic migration of payers to precision regimens moderates the growth curve for the doxorubicin market over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Formulation: Liposomal Innovations Redefining Treatment Paradigms

Conventional injection maintained a 51.20% revenue contribution to the doxorubicin market in 2025, anchored in decades of clinical familiarity and competitive generic pricing. Pegylated liposomal doxorubicin, while only a fraction of earlier volume, is expanding at a 7.34% CAGR and is pivotal to enlarging the doxorubicin market size owing to reduced cardiac toxicity and prolonged circulation time. Regulatory approvals for advanced carriers such as Myocet and Celdoxome in Europe underscore a growing consensus that lipid-based vectors can safely extend cumulative dose ceilings. Research on pH-triggered nanocarriers and thermosensitive liposomes reveals promising preclinical data, suggesting that co-development of device-based hyperthermia triggers could structurally differentiate future entrants and compound competitive intensity in this formulation segment.

Continued supply stability of lyophilized powder formulations protects treatment access in regions lacking sophisticated cold chains, particularly parts of Africa and rural South America. Volume demand here, though modest, provides durable revenue streams for manufacturers with cost-focused portfolios inside the broader doxorubicin market.

By Application: Precision Targeting Expands Therapeutic Utility

Breast cancer anchored 21.60% of total 2025 revenue, reflecting entrenched guidelines that pair anthracyclines with taxanes for high-risk profiles. Survival benefits confirmed at the San Antonio Breast Cancer Symposium reinforce frontline positioning and bolster segment adoption. By contrast, ovarian cancer is the fastest-moving application, charting an 7.88% CAGR through 2031 on the back of pegylated liposomal doxorubicin gains in platinum-resistant settings. Significant investigator interest in trabectedin-doxorubicin combinations for leiomyosarcoma, which improved median survival to 33 months in a 2024 French trial, further illustrates disease-specific growth pockets.

Meanwhile, the lymphoma subsegment is broadening under pola-R-CHP and similar regimens. Inclusion in first-line protocols increases infusion cycles per patient, thereby lifting doxorubicin market share within hematologic care pathways. Multiple myeloma, Kaposi sarcoma, bladder cancer, and gastric cancer together form a long-tail revenue pool that remains responsive to guideline shifts and local epidemiology.

By Distribution Channel: Hospital Dominance Challenged by E-pharmacy Growth

Hospital pharmacies controlled 66.10% of global volume in 2025 due to requirements for sterile compounding and on-site infusion. Nonetheless, tightening margins and insurer push-through of white-bagging mandates are migrating certain outpatient volumes toward specialty channels. E-pharmacies, growing at 8.72% CAGR, benefit from remote oncology programs and improved last-mile logistics that now support time-sensitive cold-chain delivery. Retail pharmacies continue to hold relevance in community oncology networks across North America and parts of Europe, although their share of the doxorubicin market is gradually eroding as vertical integration among wholesalers consolidates supply under large distributor-owned specialty entities.

Geography Analysis

North America remained the anchor geography with 47.55% of global revenue in 2025. Inpatient reimbursement structures, broad insurance coverage, and early adoption of cardioprotective delivery systems safeguard volume. Value-based contracts tying payments to progression-free survival may modify pricing headroom, yet the switch to liposomal variants is likely to sustain stable dollar growth for the regional doxorubicin market.

Asia-Pacific is set to be the principal acceleration engine, advancing at 8.05% CAGR to 2031. Rising diagnostic penetration, burgeoning private insurance pools in China and India, and government incentives for local manufacturing underpin robust demand. Sun Pharmaceutical Industries’ oncology build-out via acquisitions such as the USD 355 million Checkpoint Therapeutics deal shows local players’ intent to climb the innovation ladder. Indigenous production, combined with regulatory fast-tracking, is expected to shrink time-to-market for new formulations and entrench regional suppliers inside the doxorubicin market.

Europe benefits from a sophisticated reimbursement apparatus but faces budget constraints that favor generics. EMA approvals for multiple liposomal options diversify clinician choice yet subject pricing to national tender pressures. South America holds latent potential, particularly Brazil, where oncology hospital expansion and biosimilar uptake broaden patient throughput. Improvement in domestic fill-finish capabilities could lower import dependencies and stimulate localized segments of the doxorubicin market.

Regulatory Landscape

Regulation for doxorubicin continues to be shaped by generic ANDA approvals in the United States, lifecycle oversight of liposomal products, and increased attention to supply-chain resilience. FDA approvals for additional suppliers, such as Qilu Pharmaceutical Hainan (ANDA 219881, February 2026) for doxorubicin hydrochloride and Alembic (ANDA 219199, June 2025) for liposomal doxorubicin, expand the set of regulated sources serving hospital oncology compounding and infusion settings.

In Europe, the EMA maintains product-specific assessment and post-authorization documentation for pegylated liposomal doxorubicin options (for example, Zolsketil EPAR updates), while marketing authorization continuity can be affected by administrative provisions such as the EU sunset clause, highlighted by the September 2025 lapse of Baxter Holding B.V.'s Celdoxome pegylated liposomal authorization. In the United States, Presidential Proclamation 11020 (April 2026) introduced Section 232 tariffs on imports of patented pharmaceuticals, while excluding generics and biosimilars at the time, reinforcing a near-term trade-policy distinction between patented oncology products and widely used generic cytotoxics such as doxorubicin.

Competitive Landscape

The doxorubicin market is moderately concentrated. Janssen’s Doxil provides brand recognition, but patent expiries and region-specific licensing deals have ushered in a cadre of comparably bioequivalent competitors. Lupin’s 2024 liposomal launch highlights intensifying rivalry in the premium carrier niche. Baxter International’s five injectable launches in December 2024 illustrate a flurry of pipeline activity aimed at hospital formularies. Generic heavyweights such as Teva, Hikma, and Accord are consolidating economies of scale in conventional injection lines, leveraging widespread distribution networks to defend volume shares.

White-space opportunity lies in cardioprotective co-therapies. Current reliance on dexrazoxane leaves an unmet need that biotech start-ups are actively pursuing. Similarly, companies experimenting with thermo-sensitive carriers that pair with focused ultrasound devices could redefine future differentiation strategies within the doxorubicin market.

Doxorubicin Industry Leaders

Pfizer Inc.

Sun Pharmaceutical Industries Ltd

Johnson & Johnson (Janssen)

Baxter International Inc.

Teva Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Manufacturing innovation and supply reliability are emerging as key whitespace areas alongside formulation differentiation. In March 2026, University of Turku researchers reported a biosynthetic manufacturing advance in Nature Communications that increased doxorubicin yield by 180% through P450-redox partner optimization and use of the DnrV molecular sponge protein, with a related commercialization path visible via Meta-Cells Oy (formed in 2025). These developments support opportunities for new production platforms that reduce dependence on complex semi-synthetic steps and could broaden access where cost and quality variability constrain chemotherapy delivery.

Operational quality and packaging integrity also remain a practical lever for market participants, especially in liposomal presentations. Sun Pharmaceutical Industries initiated a voluntary nationwide US recall in May 2026 for a batch of doxorubicin hydrochloride liposome injection due to glass particles, underscoring the opportunity for investment in sterile fill-finish controls, container-closure improvements, and supplier qualification programs that reduce particulate-related disruptions. On the demand side, ongoing Phase 3 activity in established regimens (for example, NCT02488967 evaluating doxorubicin with cyclophosphamide in Stage IIIA breast cancer, with a listed completion target in 2026) keeps doxorubicin embedded in protocol-driven care, while encouraging manufacturers to prioritize continuity of supply, ready-to-use presentations, and differentiated liposomal alternatives for higher-risk patients.

Recent Industry Developments

- May 2026: Sun Pharmaceutical Industries initiated a voluntary nationwide US recall for one batch of doxorubicin hydrochloride liposome injection (50 mg/25 mL) after glass particles were detected. The action highlights how particulate control and container-closure performance can rapidly affect availability for liposomal oncology injectables and increases scrutiny on sterile manufacturing and packaging controls across suppliers.

- March 2026: University of Turku researchers published a biosynthetic production approach for doxorubicin reporting a 180% yield increase through redox partner optimization and the DnrV molecular sponge protein. The work supports alternative, scalable manufacturing routes that target long-standing bottlenecks in producing complex cytotoxic agents at consistent quality.

- August 2024: Lupin launched doxorubicin hydrochloride liposome injection in the United States. The entry expanded the competitive set in liposomal doxorubicin and added another option for hospital and oncology networks seeking alternatives to incumbent pegylated or conventional formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of doxorubicin medicines used in human cancer treatment across major countries, covering conventional and liposomal forms sold through the main distribution settings.

Scope exclusions: We exclude other anthracycline agents (such as epirubicin, daunorubicin, and idarubicin) and we do not count combination therapy value unless the revenue is directly tied to doxorubicin.

Segmentation Overview

- By Drug Formulation

- Conventional Doxorubicin Injection (Solution)

- Lyophilized Powder for Reconstitution

- Pegylated Liposomal Doxorubicin (PLD)

- Non-Pegylated Liposomal Doxorubicin

- By Application (Cancer Type)

- Breast Cancer

- Ovarian Cancer

- Leukemia

- Lymphoma

- Bladder Cancer

- Kaposi Sarcoma

- Multiple Myeloma

- Gastric Cancer

- By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online / E-commerce Pharmacy

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a clean disease and treatment context, and then connecting it to the doxorubicin supply chain. We use public health statistics and treatment guidance to understand where doxorubicin is used most often and how use shifts by region and over time.

Key inputs were pulled from sources such as the World Health Organization cancer and medicine references, the US FDA label and safety communications, the National Cancer Institute guidance pages, the European Medicines Agency public assessment information, and peer reviewed oncology and pharmacy journals that discuss anthracycline use and dosing practice. We also reviewed annual reports, investor presentations, and product announcements to understand volume direction, launch timing, and pricing movement, and we complemented this with paid subscriptions for company financials and intelligence plus patent databases for formulation activity. These examples are not exhaustive, and we also checked many other public sources to collect, cross verify, and clarify data points.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions and to fill gaps that are hard to see in public data, especially around tender behavior, hospital procurement cycles, and the extent of generic price erosion. We spoke with a mix of manufacturers, distributors, oncology pharmacists, and hospital buyers across APAC, EMEA, and the Americas so regional reimbursement and availability effects could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 43% |

| Mid tier: 52% | Functional/Unit leaders: 27% | EMEA: 35% |

| Smaller Players: 16% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is anchored on a top-down demand pool build that ties cancer incidence and treated patient volumes to where doxorubicin is clinically used, and then converts that demand into value using dosing norms and observed pricing bands. Once country totals are formed, they are rolled up to regions and then to the global number.

To keep the model realistic, we used a short list of practical inputs, such as cancer incidence trends in key indications where doxorubicin is common, typical cycles and mg per cycle patterns from clinical practice references, adoption mix between conventional and liposomal presentations, generic entry timing and expected price erosion, and the split of use across hospital and other dispensing settings. Where any variable was weak at country level, the gap was handled using regional proxy ratios that were validated with interviews before being applied.

Forecasts are built using scenario analysis, because pricing pressure, supply tightness, and substitution to adjacent regimens can move in different directions by year. The forward view is then cross checked with selective bottom-up approximations, such as sampled price times estimated packs or vials consumed for a few representative countries, and adjusted when the two views diverge beyond a reasonable range.

Data Validation & Update Cycle

Validation is done through multiple checks, so one number is not taken at face value. Outputs are compared against independent signals, such as oncology treatment volumes, reported shortages or restocking patterns, and known shifts between conventional and liposomal usage, which helps catch outliers early.

When a variance appears, assumptions are revisited and, if needed, we re-contact a small set of interviewees to confirm whether the change is real or a data artifact. Each report goes through stepwise analyst review before sign off, and the full dataset is refreshed annually with interim updates when material events occur. Right before delivery, a final pass is completed so clients receive an updated view aligned to the latest public releases.

Mordor Intelligence's Doxorubicin Market Estimate Compared With Other Published Estimates

Published market sizes for doxorubicin do not always match, even when the year looks the same, because the underlying counting rules can differ. The biggest drivers are what gets included as doxorubicin revenue, what price level is used, and how quickly assumptions are refreshed when shortages or price cuts show up.

Other estimates may fold in adjacent anthracyclines, add services bundled with the product value, or apply a broader oncology spend ratio without checking dose level demand signals. Currency timing also matters, and aggressive versus conservative assumptions on generic price erosion can move the total noticeably in a market where tendering is common.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.22 B (2025) | |

| Industry Publisher A | USD 1.42 B (2025) | Uses manufacturer level values that can include related services sold alongside the drug, and the scope description lists branded names and broader creator revenue, which can lift the total beyond product only doxorubicin value. |

| Global Publisher B | USD 1.10 B (2025) | Uses a longer horizon and often applies more conservative near term penetration and price assumptions, which can understate markets where liposomal mix and access improvements raise value faster in the early years. |

Other anthracycline analogs are not counted here, and that exclusion sits outside Mordor Intelligence's scope for this report, which helps explain why some published totals look higher when they group similar cytotoxic drugs together. With clear inclusion rules, practical demand inputs, and cross checks against interview feedback, the final number stays traceable and repeatable year to year.

Key Questions Answered in the Report

What is the current size of the doxorubicin market?

The doxorubicin market stands at USD 1.3 billion in 2026 and is forecast to reach USD 1.77 billion by 2031, growing at a 6.42% CAGR.

Which drug formulation is growing fastest?

Pegylated liposomal doxorubicin is the fastest-expanding formulation, projected to rise at a 7.34% CAGR through 2031 thanks to lower cardiotoxicity and enhanced tumor targeting.

Why is Asia-Pacific the fastest-growing region?

Expanding cancer care infrastructure, rising diagnosis rates, and wider generic availability propel an 8.05% CAGR for the region’s doxorubicin market.

How does cardiotoxicity affect doxorubicin use?

Lifetime doses are capped at 450-550 mg/m² due to cumulative heart damage risk, requiring cardiac monitoring and encouraging adoption of safer liposomal carriers and cardioprotective adjuncts.

What competitive pressures face the doxorubicin market?

Targeted biologics and ADCs increasingly capture share in developed markets, while stringent hazardous-drug handling rules add supply-chain costs. Nonetheless, generic competition and liposomal innovation keep doxorubicin relevant across many protocols.

Which distribution channel is growing fastest for doxorubicin?

Online and e-pharmacy channels are expanding at a 8.72% CAGR, supported by remote oncology programs and improved cold-chain logistics that enable home-based care.

Page last updated on: