Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 175.50 Billion |

| Market Size (2026) | USD 177.83 Billion |

| Market Size (2031) | USD 189.99 Billion |

| Growth Rate (2026 - 2031) | 1.33% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Poultry Market Analysis by Mordor Intelligence

The Asia-Pacific poultry market size is expected to grow from USD 175.50 billion in 2025 to USD 177.83 billion in 2026 and is forecast to reach USD 189.99 billion by 2031 at 1.33% CAGR over 2026-2031. While the overall growth appears slow, there's significant variation across sub-regions. Producers adept at managing feed-cost fluctuations and transitioning to value-added offerings, such as processed, frozen, and antibiotic-free products, are outpacing their commodity-focused counterparts. Chicken remains the dominant choice for consumers, but duck is gaining traction, driven by surging demand for Chinese waterfowl and a growing preference for premium formats in urban retail. The landscape is evolving, with quick-service restaurants (QSRs) expanding, incomes rising, and e-commerce innovations in grocery reshaping the distribution landscape. However, challenges persist, as recurring avian influenza outbreaks and fluctuating grain prices test the resilience of the supply chain. In 2023, Vietnam's Ministry of Industry and Trade highlighted the country's robust food service sector, boasting over 540,000 businesses. As the market evolves, competitive strategies are increasingly centered on automation, traceability, and meeting the demands of QSRs and retailers for standardized cuts and timely cold-chain deliveries.

Key Report Takeaways

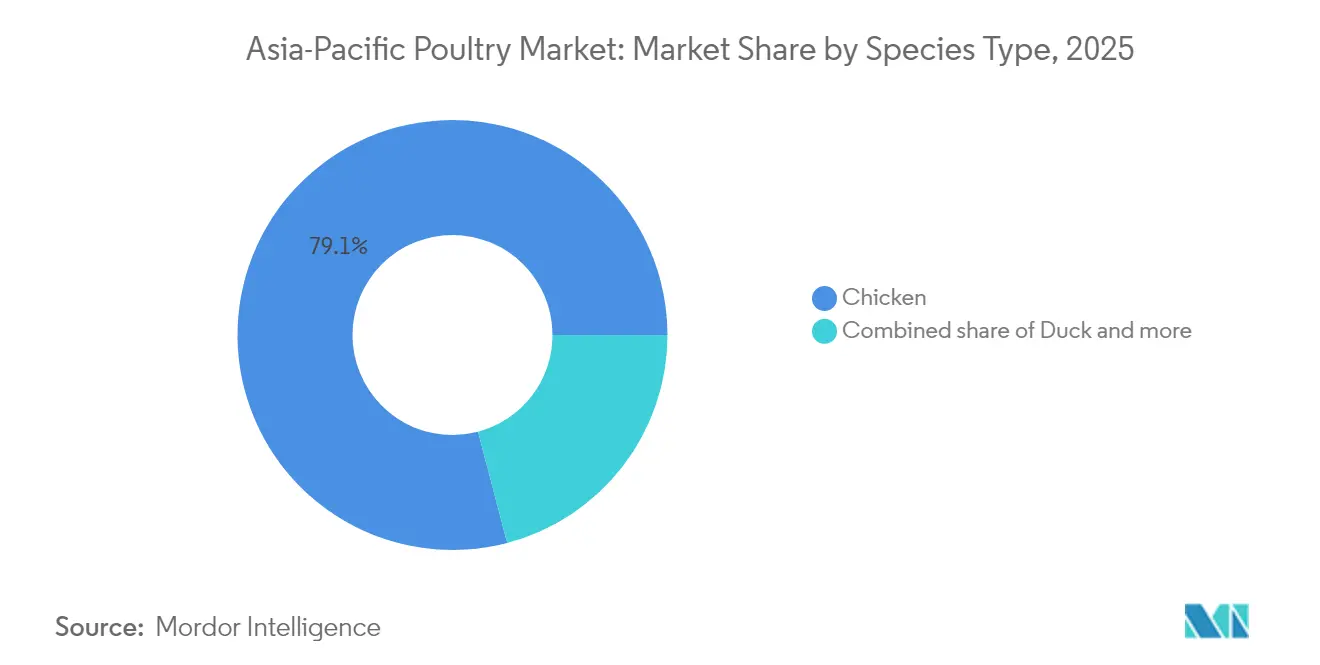

- By Species Type, chicken commanded 79.10% of the Asia-Pacific poultry market share in 2025, whereas duck is growing at a 3.15% CAGR through 2031.

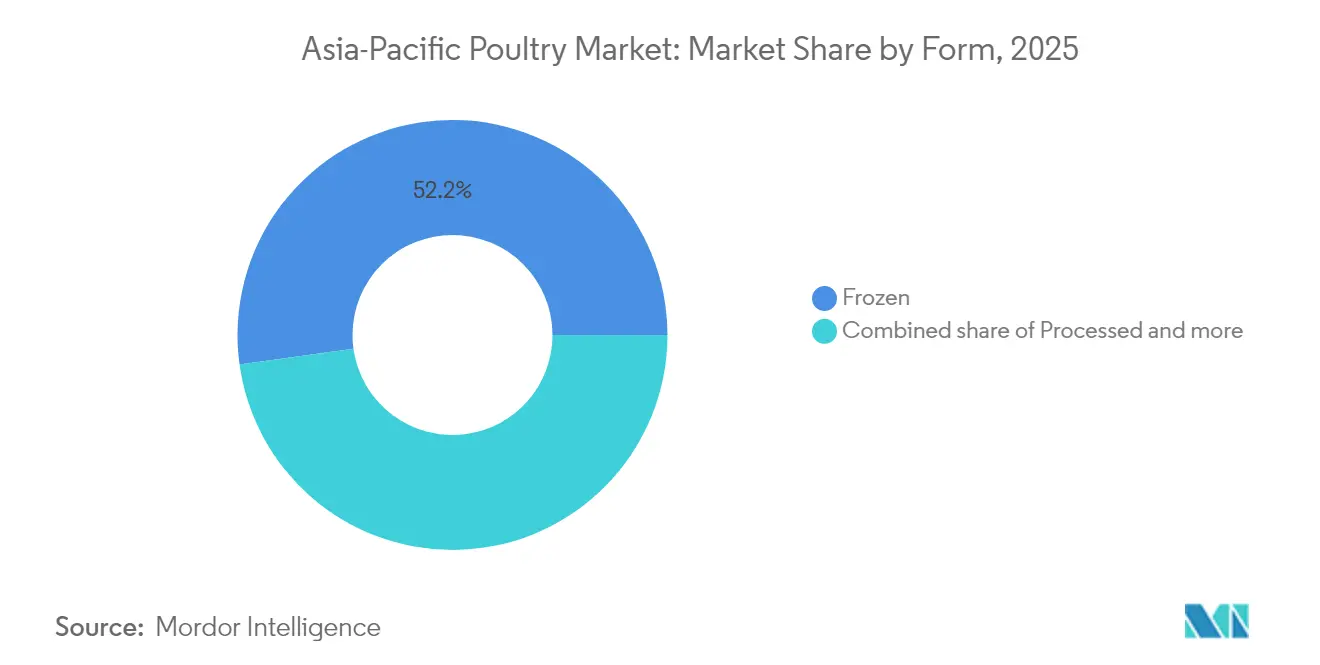

- By Form, processed poultry is advancing at a 2.12% CAGR, but frozen formats still held 52.20% share of the Asia-Pacific poultry market size in 2025.

- Foodservice captured 47.60% of 2025 revenues; however, retail, spurred by e-commerce, posts a 3.89% CAGR to 2031.

- By Geography, China retained a 33.10% value share in 2025, while India is the fastest-growing geography at 2.44% annually.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Poultry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization-driven demand for convenient animal protein | +0.35% | China, India, Indonesia, Vietnam, with spillover to tier-2 cities across ASEAN | Medium term (2-4 years) |

| Expansion of QSR chains in tier-2 and tier-3 Asian cities | +0.28% | India, China, Vietnam, Philippines, with early gains in secondary urban clusters | Short term (≤ 2 years) |

| Rising disposable incomes are lifting per-capita egg consumption | +0.22% | India, Vietnam, Indonesia, Bangladesh, with rural-to-urban migration amplifying demand | Long term (≥ 4 years) |

| Adoption of antibiotic-free and traceable poultry for export compliance | +0.18% | Thailand, Vietnam, and Australia, with regulatory influence from the EU and Japan, import standards | Medium term (2-4 years) |

| Government incentives for protein self-sufficiency amid feed volatility | +0.15% | India, Malaysia, and South Korea, with national food-security mandates driving capacity additions | Long term (≥ 4 years) |

| E-commerce grocery growth is improving cold-chain penetration | +0.12% | Singapore, urban China, India metro regions, with last-mile logistics enabling fresh/chilled delivery | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid urbanization-driven demand for convenient animal protein

As Asia-Pacific's urban population grows faster than infrastructure can keep up, there's a rising demand for quick-preparation and shelf-stable protein sources. According to the OECD-FAO Agricultural Outlook, by 2034, poultry is set to make up 45% of global meat protein consumption, a rise from current figures[1]Source: OECD-FAO, “Agricultural Outlook 2024-2033,” oecd.org. This change is largely driven by urban households favoring convenience and affordability over traditional wet-market purchases. In China, this trend is especially evident, with white broilers now constituting over 60% of the country's broiler population, thanks to their efficient feed conversion and compatibility with mechanized processing. Meanwhile, in India, processing capacity is on track to hit 267,800 birds per hour by mid-2026, marking a robust 15.75% annual growth since 2018. This surge is fueled by integrators pouring investments into automated evisceration and chilling lines, all to cater to the urban appetite. Yet, in Vietnam and Indonesia, the enduring presence of live-bird markets hampers the adoption of cold-chain logistics, curtailing the market potential for pre-packaged poultry. Urbanization is also ushering in a wave of premiumization. Consumers in tier-1 cities are now willing to shell out 20-30% more for poultry that's antibiotic-free or carries organic certifications. Processors are keenly tapping into this trend, using it as a strategy to counterbalance shrinking margins in commodity segments.

Expansion of QSR chains in tier-2 and tier-3 Asian cities

Quick-service restaurant (QSR) operators are increasingly targeting secondary cities, drawn by lower real estate costs and reduced competition, after saturating tier-1 metros. Yum China, for instance, has set its sights on operating 20,000 stores by 2026, with a notable focus on tier-3 cities. Here, KFC and Pizza Hut frequently stand out as the inaugural Western-style dining choices. This ambitious expansion not only underscores the growing appetite for Western dining but also drives a heightened demand for specific chicken cuts, like breast fillets, wings, and tenders, that align with franchise standards on size and fat content. Similarly, Jollibee's ventures into Vietnam and China underscore the importance of vertically integrated supply chains, ensuring consistent quality. This approach inherently benefits larger integrators, sidelining fragmented local suppliers. The QSR sector is also championing the use of frozen poultry, a necessity for franchisees aiming to reduce spoilage, especially in regions with sporadic cold-chain facilities. In 2024, South Korea's Ministry of Agriculture, Food and Rural Affairs highlighted a surge in domestic chicken consumption per capita, a trend bolstered by the dominance of fried-chicken chains in the late-night dining arena[2]Source: Korea Ministry of Agriculture, “Livestock Statistics 2024,” mafra.go.kr. Yet, the growth trajectory of QSRs isn't without its challenges. Economic downturns pose a threat, particularly in tier-2 cities where heightened price sensitivity might push consumers back to traditional wet markets during financially uncertain times.

Rising disposable incomes lifting per-capita egg consumption

In South and Southeast Asia, rising incomes are driving a heightened demand for animal protein, with egg consumption leading the way into broader poultry adoption. In 2024-25, India produced 149.11 billion eggs, marking a 4.44% increase from the previous year. Andhra Pradesh, Tamil Nadu, and Telangana together contributed nearly 47% to this national output, as reported by the Government of India. This uptick in production is bolstered by government initiatives, which not only subsidize expansions in layer farms but also offer technical support to enhance biosecurity. The Asian Development Bank highlights a noteworthy trend: per-capita protein consumption in Vietnam and Indonesia is nearing that of Thailand and Malaysia. This convergence hints at a sustained growth trajectory, especially as rural households gradually shift from plant-based diets. Eggs enjoy a unique advantage; they are culturally accepted across various religious and ethnic groups, unlike beef or pork. This broad acceptance positions eggs as a politically neutral choice for nutrition programs. Yet, challenges loom. Price fluctuations, primarily influenced by feed costs, threaten to undermine affordability, especially in Bangladesh and Pakistan, where imports of maize and soybean meal are predominant. As we look ahead to 2030, the balance between rising incomes and feed price dynamics will be crucial in determining the sustainability of this growth trend.

Adoption of antibiotic-free and traceable poultry for export compliance

Producers in Thailand, Vietnam, and Australia, focusing on exports, are shifting towards antibiotic-free systems. This move aligns with tightening import standards from the European Union and Japan, which are clamping down on residues from key antimicrobials. Forecasts from the USDA Foreign Agricultural Service indicate a 2.6% uptick in Thailand's chicken production by 2025, spurred by export demand. This growth comes even as domestic consumption remains tepid, hampered by a scarcity of day-old chicks. In response to the European Union's prohibition on routine antibiotic use, Thai producers are pivoting to alternatives like probiotics and organic acids. While these shifts elevate production costs by 8-12%, they also pave the way for premium pricing in export markets. Echoing this trend, Australia's poultry industry has adopted comprehensive traceability systems, tracking every batch from hatchery to retail. This move caters to Japanese importers' rising demand, emphasizing food safety. Yet, a financial chasm exists: smaller producers in Indonesia and the Philippines can't afford these systems. This disparity has led to a divided market: export-ready facilities operate at near-full capacity, while those catering domestically grapple with oversupply. Compliance standards like ISO 22000 and GLOBALG.A.P. are emerging as essential gateways for premium market segments, further consolidating power among vertically integrated players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring avian-influenza outbreaks causing culling shocks | -0.42% | Vietnam, Australia, Japan, South Korea, with sporadic outbreaks in China and Indonesia | Short term (≤ 2 years) |

| Volatile feed raw-material prices linked to global grain markets | -0.38% | Global, with an acute impact in import-dependent markets like Malaysia, the Philippines, and Bangladesh | Medium term (2-4 years) |

| Fragmented cold-chain logistics in lower-income ASEAN markets | -0.22% | Indonesia, Philippines, Vietnam, and Myanmar, with infrastructure gaps in rural and peri-urban zones | Long term (≥ 4 years) |

| Competition from plant-based protein start-ups targeting flexitarians | -0.15% | Singapore, urban China, India metro regions, with niche adoption in Japan and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recurring avian-influenza outbreaks causing culling shocks

In June 2024, Australia reported an H7N3 outbreak, leading to the culling of over 1 million birds. Meanwhile, in May 2024, Vietnam dealt with H5N1 cases. Japan, in late 2024, detected multiple instances of H5N1, resulting in localized movement restrictions that delayed shipments to processors and retailers. South Korea's stringent culling protocols, which require the destruction of all birds within a 3-kilometer radius of confirmed cases, create supply shocks. These shocks ripple through integrated supply chains, compelling processors to source from distant regions at higher transport costs. While the World Health Organization, Food and Agriculture Organization, and World Organisation for Animal Health run joint surveillance programs, early-warning systems falter in lower-income markets due to underfunded veterinary infrastructure. The economic repercussions are significant: export bans from importing countries can linger for months post-outbreak containment, leaving producers with surplus inventory. In China and Vietnam, vaccination strategies are on the rise. However, concerns over vaccine efficacy and potential trade repercussions hinder broader adoption in export-centric markets such as Thailand and Australia.

Volatile feed raw-material prices linked to global grain markets

Poultry production costs are heavily influenced by corn and soybean meal, which together account for 60-70% of these expenses. This reliance makes poultry integrators vulnerable to price fluctuations, often driven by weather events, geopolitical tensions, and biofuel mandates. Throughout 2024, the World Bank's commodity price index for grains remained elevated, a trend attributed to ongoing supply constraints from the Black Sea region and adverse weather conditions in South America[3]Source: World Bank, “Commodity Prices Data 2024,” worldbank.org. Similarly, the FAO Food Price Index stayed above pre-2022 levels, putting pressure on producers' margins, especially those unable to swiftly transfer costs to consumers. Markets like Malaysia and the Philippines, which rely on imports, grapple with heightened currency risks. Depreciation against the US dollar further inflates feed costs. In 2024, India's poultry integrators enjoyed a boon from domestic maize surpluses, leading to reduced feed prices. However, this benefit is precarious, hinging on monsoon variability and shifts in export policies. While some integrators are exploring alternative feed ingredients like insect meal and algae, challenges such as regulatory approvals and scalability loom large. Moreover, the absence of futures markets for poultry products in many Asian nations hampers producers' ability to hedge against margin risks, leaving them vulnerable to simultaneous surges in input costs and drops in output prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species Type: Duck Outpaces Chicken in Growth Velocity

In 2025, chicken secured a commanding 79.10% share of the species-type market, solidifying its status as Asia-Pacific's preferred poultry choice, thanks to its affordability, religious neutrality, and culinary versatility. Meanwhile, duck is making waves, growing at an annual rate of 3.15% through 2031, the fastest among its peers. This surge is largely attributed to China's stronghold on waterfowl production and the escalating appetite for Peking duck in urban locales, as highlighted by the USDA Foreign Agricultural Service. Dominating the scene, China produces over 70% of the world's duck, boasting integrated supply chains that cover breeding, feed milling, and processing. This comprehensive approach gives China a cost advantage that outpaces smaller producers in Vietnam and Thailand. In China, duck meat enjoys a premium status, gracing the menus of upscale restaurants and specialty retailers. Here, it's not just a dish but a symbol of festive celebrations and traditional culinary art, a cultural nuance that shields it from direct price wars with chicken. Vietnam's duck farming is on the rise, buoyed by government initiatives offering subsidized feed and technical training to small farmers. Yet, it's not without hiccups; production faced a setback in May 2024 due to avian influenza outbreaks, as reported by the World Organization for Animal Health.

Turkey and other poultry types occupy a niche segment, sharing the remaining market space. Turkey finds its primary audience among expatriates and Western-style eateries in Singapore, Hong Kong, and Australia. Yet, it struggles to resonate culturally in most Asian markets. Its longer growth cycle and less efficient feed conversion further diminish its competitiveness against chicken. Still, there's a silver lining: Japan and South Korea present niche markets, with health-conscious diners exploring leaner proteins. Australia, too, carves out a space, with local turkey farms catering to holiday festivities. However, challenges loom. The scarcity of turkey breeding stock and a dearth of processing know-how stifle broader market growth. As it stands, chicken and duck are poised to maintain their dominance in the species landscape through 2031.

By Form: Processed Poultry Gains as Convenience Trumps Price

In 2025, frozen poultry captured 52.20% of the market share, thanks to its bulk purchasing appeal, extended shelf life, and seamless integration with cold-chain infrastructure. Meanwhile, processed poultry is on a growth trajectory, expanding at an annual rate of 2.12% through 2031. This surge, the fastest among all forms, is fueled by urbanization and the rise of dual-income households, leading to a heightened demand for ready-to-eat and ready-to-cook products that streamline meal preparation. By mid-2026, India's processing capacity is set to soar to 267,800 birds per hour. This leap is driven by integrators pouring investments into automated marination, breading, and packaging lines, churning out value-added products like chicken nuggets, sausages, and kebabs. These offerings boast gross margins 15-20 percentage points above commodity cuts, enticing producers to pivot towards processed formats, even with the associated capital demands.

Fresh and chilled poultry enjoys a loyal following in markets where consumers prioritize freshness and embrace daily shopping. This behavior is especially prevalent in Southeast Asia's wet markets. Yet, the fresh segment grapples with challenges: food-safety apprehensions and the hassle of frequent shopping trips. These issues tilt the scales in favor of pre-packaged alternatives. Canned poultry, while carving out a niche for emergency rations and in remote areas lacking cold-chain access, is unlikely to capture a significant market share, given the prevailing consumer preference for fresher options. The processed poultry trend dovetails with the expansion of quick-service restaurants. Franchisees seek standardized products that align with their specifications on size, breading thickness, and fat content. Such consistency is a hallmark of large processors, making them indispensable in this evolving landscape.

By Distribution Channel: Retail Surges on E-Commerce Tailwinds

In 2025, foodservice commanded a 47.60% share of the distribution channel, underscoring the stronghold of quick-service restaurants, hotels, and institutional catering in urban areas where dining out is commonplace. Retail channels, however, are on an upward trajectory, expanding at an annual rate of 3.89% through 2031. This growth, the fastest among distribution types, is largely fueled by e-commerce grocery platforms adept at cold-chain logistics and boasting 30-minute delivery windows. In 2024, Singapore's Deliveroo and Sheng Siong rolled out a 30-minute grocery delivery service, with fresh foods making up about 50% of online orders. This model is now gaining traction in urban centers of China and India. Supermarkets and hypermarkets, having invested in omnichannel capabilities, are reaping the rewards of this shift. They offer consumers the flexibility to order online for home delivery or in-store pickup, a convenience that traditional wet markets and convenience stores struggle to provide.

Meanwhile, online retailers are gaining ground by introducing subscription models, ensuring regular deliveries of frozen chicken and eggs. This strategy not only simplifies repeat purchases but also fosters customer loyalty. While specialty stores and butcheries still attract consumers seeking personalized service and premium cuts, their market share is dwindling. Younger shoppers increasingly favor convenience over traditional relationship-based shopping. The foodservice channel's tempered growth can be attributed to saturation in tier-1 cities and economic challenges curbing discretionary dining expenses. Yet, quick-service restaurants are making inroads in tier-2 and tier-3 cities, where their presence is still limited. Looking ahead, retail channels that harness data analytics for inventory optimization and spoilage reduction are poised for success, a feat that remains elusive for traditional foodservice operators.

Geography Analysis

In 2025, China held 33.10% of the regional market, driven by vertically integrated production and strong domestic consumption. In 2023, China consumed over 11.86 billion broilers, equating to 18.876 million tonnes of chicken meat (USDA GAIN Report). White broilers, now over 60% of the population, improved feed-conversion ratios but reduced flavor differentiation, creating opportunities for heritage-breed producers in premium markets. Fujian Sunner, China's third-largest broiler producer, reported a net income drop to CNY 102 million (USD 14 million) in H1 2024 from CNY 426 million (USD 59 million) in H1 2023, due to oversupply and high feed costs. While the government’s protein self-sufficiency mandate drives capacity growth, demand is slowing as urban per-capita consumption nears saturation. Limited export opportunities, due to trade restrictions and competition from Brazil and the U.S., are pushing integrators toward domestic value-added segments like processed poultry and duck products.

India is the fastest-growing market, expanding at 2.44% annually through 2031, supported by rising incomes, government incentives, and cultural acceptance of poultry. Egg production reached 149.11 billion units in 2024-25, up 4.44% year-on-year, with Andhra Pradesh, Tamil Nadu, and Telangana contributing nearly 47% of output (Government of India). Poultry accounts for 49% of India’s meat consumption, expected to grow with rising incomes and better cold-chain infrastructure. However, fragmented production and poor biosecurity practices increase disease risks, while unorganized players limit the branded market. Capital subsidies under the Andhra Pradesh Food Processing Policy are driving consolidation, benefiting major integrators like Suguna Foods and Venky's.

Japan, Australia, Thailand, Vietnam, Indonesia, South Korea, Malaysia, and Singapore account for the remaining market share, each with unique dynamics. Japan’s H5N1 outbreaks in late 2024 delayed shipments and raised prices (Japan Ministry of Agriculture). Australia’s H7N3 outbreak in June 2024 led to the culling of over 1 million birds and export bans (World Organisation for Animal Health). Thailand’s chicken production is forecast to grow 2.6% in 2025, driven by export demand despite limited day-old chick supplies (USDA Foreign Agricultural Service). Vietnam’s duck farming, supported by government programs, faced disruptions from H5N1 outbreaks in May 2024. Indonesia’s processed chicken exports are rising, with Japan as the largest importer. Malaysia’s National Agrofood Policy 2.0 targets 60% poultry self-sufficiency by 2030 with feed mill subsidies (Malaysian Ministry of Agriculture). Singapore’s Deliveroo and Sheng Siong partnership for 30-minute grocery delivery highlights its e-commerce leadership, a model larger markets are adopting.

Competitive Landscape

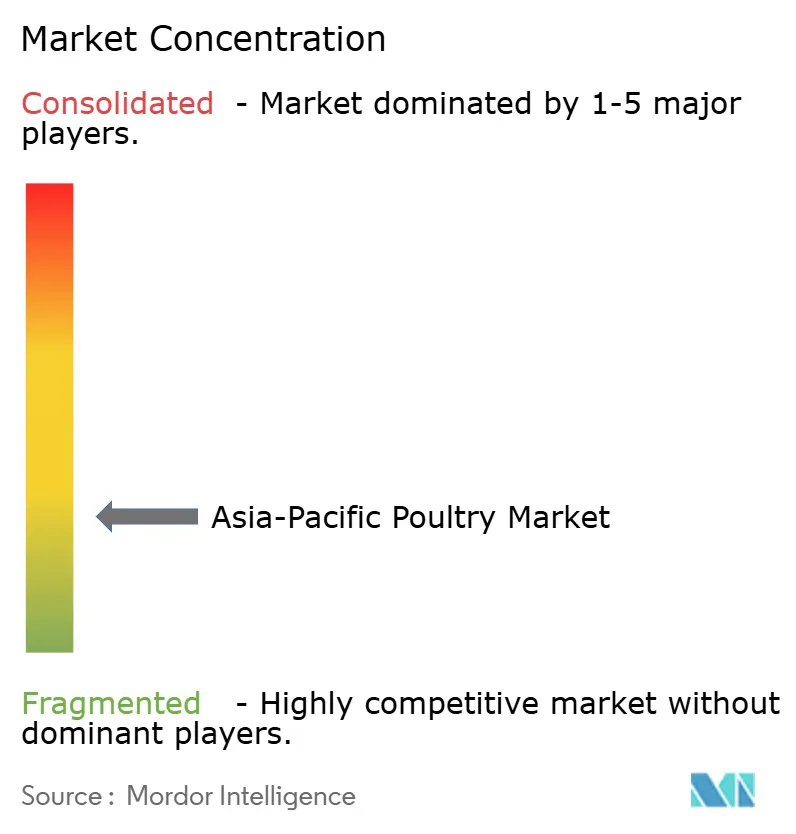

The Asia-Pacific poultry market is moderately fragmented, with a multitude of small-scale integrators coexisting with industry titans like Charoen Pokphand Foods, Wen's Foodstuff Group, and Suguna Foods. Market concentration varies: China and Thailand enjoy higher consolidation due to economies of scale in feed milling and processing, while India and Indonesia see dominance from unorganized players in rural and peri-urban supply chains. As integrators pour investments into automation, traceability systems, and antibiotic-free production, competitive intensity rises. This shift aims to capture premium segments and adhere to export compliance. In India, Meyn and Marel dominate the processing-equipment installation base, holding 45.9% and 19.6% respectively, underscoring the capital intensity that challenges smaller processors. Opportunities abound in processed poultry and duck farming, where demand outstrips supply, and in e-commerce channels necessitating cold-chain capabilities, a hurdle for traditional wet-market operators.

Plant-based protein disruptors like Green Monday and Growthwell are making inroads, appealing to flexitarian consumers in Singapore and Hong Kong. Yet, their growth is tempered by price premiums and taste preferences. Technology adoption is on the rise, with integrators leveraging AI-driven demand forecasting to fine-tune inventory and minimize spoilage. KPMG's 2024 survey highlights this capability as vital for omnichannel retailers catering to 45% of Asia-Pacific consumers who favor blended shopping experiences. Strategic maneuvers include expanding into tier-2 and tier-3 cities, forging partnerships with quick-service restaurant chains, and acquiring smaller processors to streamline fragmented supply chains.

However, not all players are thriving. Commodity broiler producers in China face significant challenges, with Fujian Sunner's net income plummeting 76% in H1 2024 due to oversupply and margin compression. The competitive landscape is poised for further bifurcation: large integrators are set to dominate premium and export segments, while smaller players vie for price competition in domestic commodity markets.

Asia-Pacific Poultry Industry Leaders

Charoen Pokphand Foods PCL

Wen’s Foodstuff Group Co. Ltd.

Suguna Foods Pvt. Ltd.

NH Foods Ltd.

Baiada Poultry Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Charoen Pokphand Foods PCL announced a USD 150 million investment to expand its integrated poultry operations in Vietnam, including the construction of a new feed mill with 500,000 tonnes annual capacity and a processing plant capable of handling 120,000 birds per day. The expansion aims to capture growing domestic demand and strengthen the company's position in export markets, particularly Japan and South Korea, where antibiotic-free certification is increasingly required.

- September 2024: Ingham's Group Ltd completed the acquisition of a regional poultry processor in New South Wales, Australia, for USD 85 million, adding 50,000 birds per day of processing capacity and expanding its footprint in the foodservice channel. The acquisition includes cold-storage facilities and distribution networks that will enable Ingham's to serve quick-service restaurant chains more efficiently.

- August 2024: Suguna Foods Pvt. Ltd. inaugurated a state-of-the-art processing facility in Telangana, India, with an investment of USD 40 million and capacity to process 100,000 birds per day. The plant incorporates automated evisceration and chilling systems from Meyn, positioning Suguna to capture growing demand for value-added products such as marinated chicken and ready-to-cook items in urban retail channels.

Asia-Pacific Poultry Market Report Scope

Poultry is domesticated avian species raised for eggs, meat, and feathers. Poultry covers a wide range of birds, from indigenous and commercial breeds of chickens. The Asia-Pacific poultry market is segmented by product type into table eggs and chicken meat. Chicken meat is further sub-segmented into fresh/chilled, frozen/canned, and processed. By distribution channel, the market is segmented into on-trade and off-trade. Off-trade is further segmented into supermarkets & hypermarkets, slaughterhouses, convenience stores, online retail, and others. By country, the market is studied for China, India, Japan, Australia, and the rest of the Asia Pacific region. The market sizing has been done in value terms in USD for all the abovementioned segments.

Species Type

| Chicken |

| Duck |

| Turkey |

| Other Poultry |

Form

| Canned |

| Fresh/Chilled |

| Frozen |

| Processed |

By Distribution Channel

| Foodservice | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Specialty Stores/Butcheries | |

| Online Retailers | |

| Other Distribution Channels |

Geography

| China |

| India |

| Japan |

| Australia |

| Thailand |

| Vietnam |

| Indonesia |

| South Korea |

| Malaysia |

| Singapore |

| Rest of Asia-Pacific |

| Species Type | Chicken | |

| Duck | ||

| Turkey | ||

| Other Poultry | ||

| Form | Canned | |

| Fresh/Chilled | ||

| Frozen | ||

| Processed | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores/Butcheries | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

Which species shows the fastest growth across Asia-Pacific?

Duck leads with a projected 3.15% CAGR through 2031 due to rising Chinese and Vietnamese demand.

Why is processed poultry gaining traction?

Urban households value convenience, and QSRs require standardized cuts, driving a 2.12% CAGR in processed formats.

What factors most threaten supply stability?

Recurring avian-influenza outbreaks and volatile feed-grain prices remain the two largest operational risks.

Which country offers the highest growth opportunity?

India is expanding at a 2.44% CAGR, supported by government processing incentives and increasing protein intake.

How are companies responding to export market requirements?

Leading integrators invest in antibiotic-free production and full traceability to meet EU and Japanese import standards.

Page last updated on: