Tungsten Carbide Powder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.06 Billion |

| Market Size (2031) | USD 21.74 Billion |

| Growth Rate (2026 - 2031) | 4.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

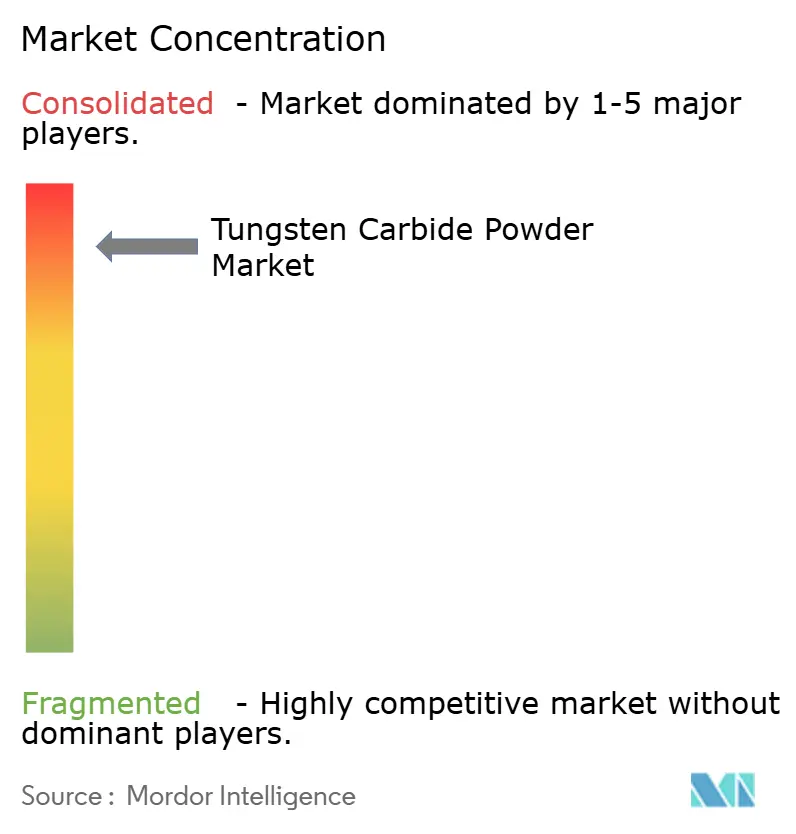

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tungsten Carbide Powder Market Analysis by Mordor Intelligence

The tungsten carbide powder market size was valued at USD 16.25 billion in 2025 and estimated to grow from USD 17.06 billion in 2026 to reach USD 21.74 billion by 2031, at a CAGR of 4.98% during the forecast period (2026-2031). Sustained capital spending on precision machining, mining equipment, and advanced medical instruments keeps demand resilient even as raw-material prices fluctuate. Growing electrification of transport, expanding renewable-energy installations, and widening adoption of additive manufacturing continue to pull the tungsten carbide powder market into new, higher-value applications. Governments in the United States, Canada, and Australia are underwriting critical-mineral projects, which stabilize long-term supply expectations and support capacity ramp-ups by established powder producers. At the same time, Chinese export controls and six-year-high ammonium paratungstate prices heighten procurement risk, prompting end users to diversify suppliers and favor recycled material streams.

Key Report Takeaways

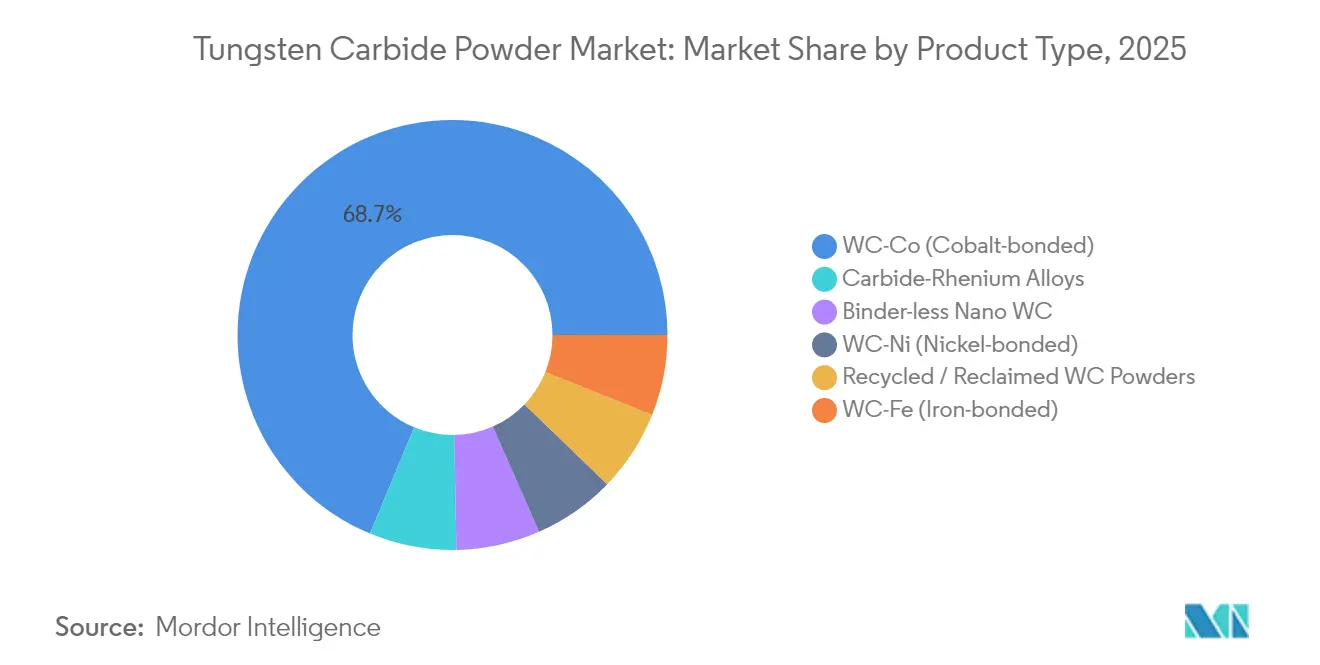

- By product grade, WC-Co (Cobalt Bonded) maintained 68.74% share of the tungsten carbide powder market in 2025; carbide-rhenium alloys register the highest projected CAGR at 6.08% to 2031.

- By application, machining tools held 35.74% of the tungsten carbide powder market share in 2025; other applications, led by additive manufacturing and thermal-spray coatings, are forecast to expand at a 5.92% CAGR through 2031.

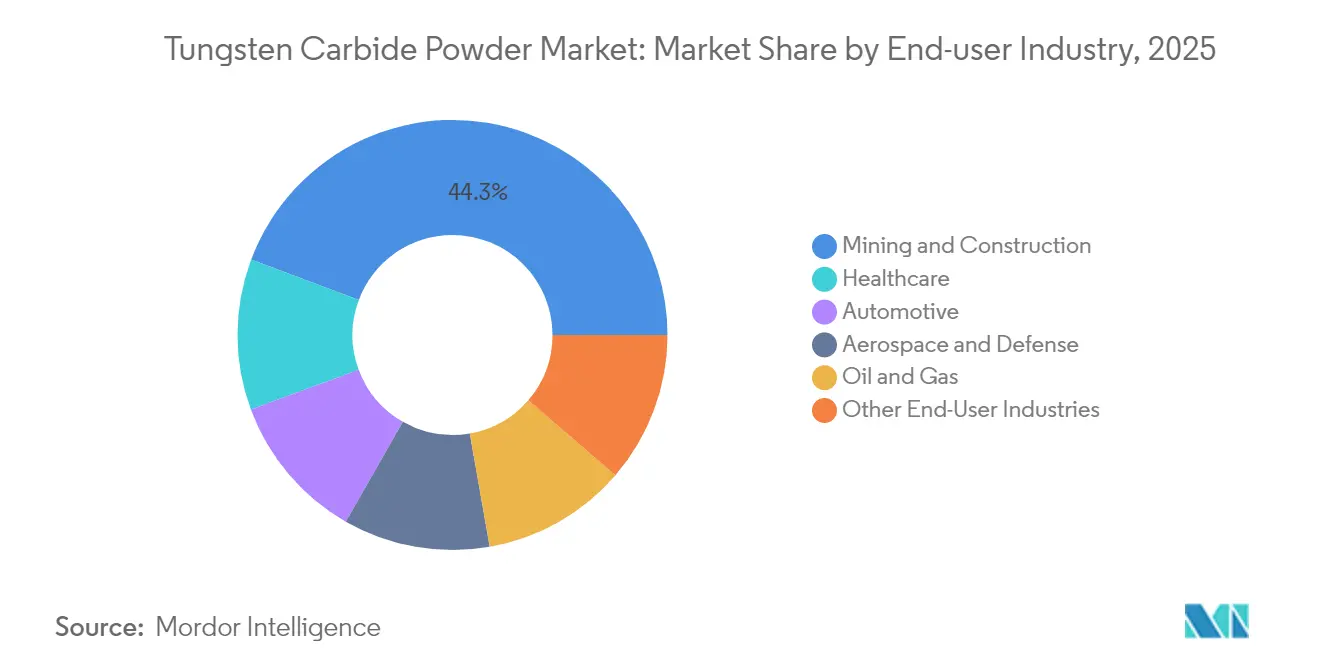

- By end-user industry, mining and construction commanded 44.29% of the tungsten carbide powder market size in 2025, while healthcare records the fastest growth path at 6.10% CAGR to 2031.

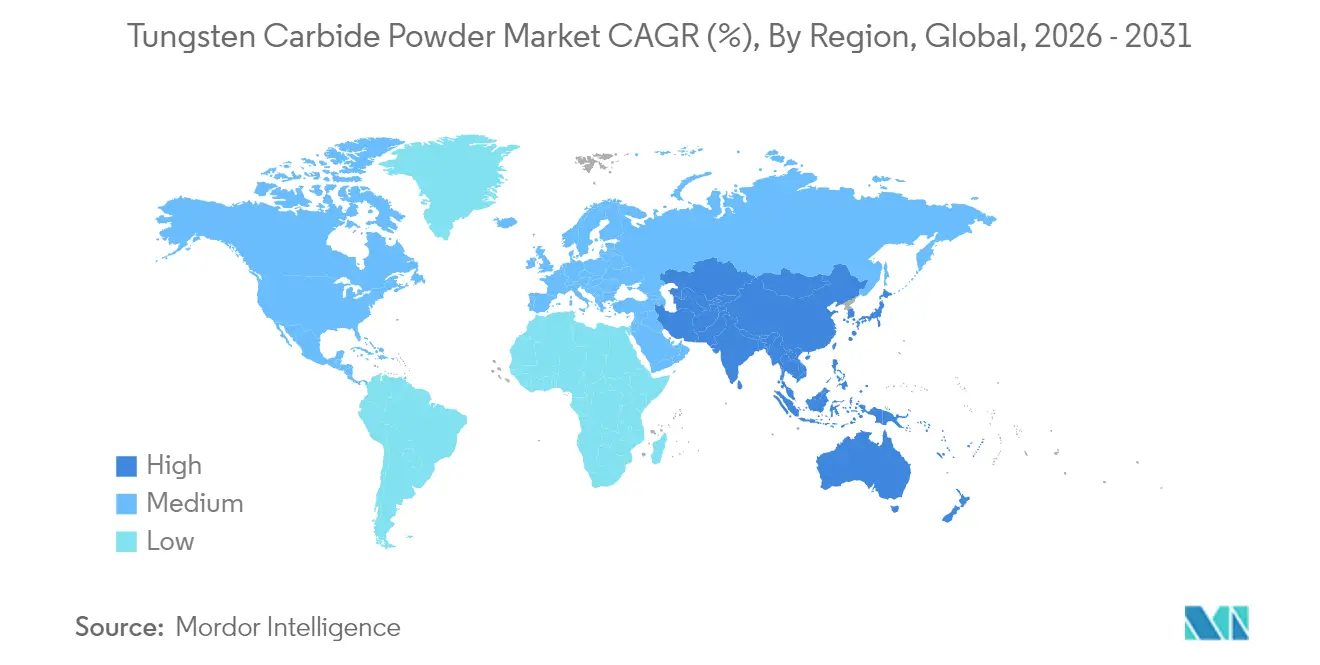

- By geography, Asia-Pacific accounted for 53.82% of 2025 revenue and is poised to lead expansion with a 6.36% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tungsten Carbide Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for precision cutting and machining tools | 1.5% | Global, with a concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid expansion of EV and renewable energy component machining | 0.8% | North America, Europe, China | Short term (≤ 2 years) |

| Shift toward wear-resistant powders in oil-sand and fracking equipment | 0.7% | North America, Middle East | Long term (≥ 4 years) |

| Integration of tungsten carbide powders in high-speed additive manufacturing | 0.6% | Global, early adoption in developed markets | Medium term (2-4 years) |

| Government-funded critical minerals and defense stockpiling programs | 0.4% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Precision Cutting and Machining Tools

Manufacturers facing ever-tighter tolerances rely on tungsten carbide inserts to preserve edge integrity during high-speed operations. Longer tool life limits unplanned stoppages and supports continuous, lights-out production. In CNC environments connected through Industry 4.0 networks, consistent insert performance is essential for predictive-maintenance algorithms that trigger tool changes only when statistically justified. Recent TiC surface-engineering techniques have raised Vickers hardness from 1,317 HV30 to 1,496 HV30, extending wear intervals in mass-production lines. Demand clustering in Asia-Pacific and the United States anchors short-term volume growth for the tungsten carbide powder market.

Rapid Expansion of EV and Renewable Energy Component Machining

Battery housings, e-motor shafts, and power-electronic enclosures require micro-tolerance machining that favors cemented-carbide tooling. Wind-turbine gearboxes and solar-tracker drive units add a steady stream of hardened-steel components that conventional HSS tools cannot machine economically. Oak Ridge National Laboratory recently printed crack-free tungsten structures with an electron-beam process, signaling a pathway to fusion-reactor and extreme-environment parts that will use high-purity powder feedstock[1]Oak Ridge National Laboratory, “Electron-beam additive manufacturing of tungsten,” ornl.gov. Localized EV supply chains in North America and Europe translate that technical success into regional pull for the tungsten carbide powder market.

Shift Toward Wear-Resistant Powders in Oil-Sand and Fracking Equipment

Horizontal wells and oil-sand slurry pipelines impose abrasive loads that can triple maintenance outlays when inferior materials fail. Tungsten carbide-coated drill sleeves extend mean-time-between-failure and compress cost-per-hole metrics over the full well life. Linde Advanced Material Technologies cites strong thermal conductivity and chemical inertness as dual advantages that preserve integrity in high-temperature down-hole zones. Despite crude-price volatility, the resulting Opex reductions keep the tungsten carbide powder market firmly positioned within upstream-service CAPEX plans.

Government-Funded Critical Minerals and Defense Stockpiling Programs

The United States Government Accountability Office estimates USD 18.5 billion is needed to close defense-critical-mineral shortfalls, with tungsten topping the list[2]United States Government Accountability Office, “Defense critical mineral shortfalls,” gao.gov. The REEShore Act bans Chinese tungsten in military programs from 2026, prompting accelerated funding for North American projects and strategic stockpiles. Joint US-Canadian backing of the Mactung development underpins a hemispheric supply corridor for the tungsten carbide powder market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in tungsten ore (APT) prices due to supply concentration | -0.9% | Global, particularly affecting Western markets | Short term (≤ 2 years) |

| High manufacturing and processing costs | -0.6% | Global, with higher impact in cost-sensitive markets | Medium term (2-4 years) |

| Capital-intensive powder metallurgy equipment for nano-grades | -0.4% | Developed markets with advanced manufacturing | Long term (≥ 4 years) |

| Competitive threat from advanced ceramics and cermets in wear parts | -0.3% | Global, concentrated in high-performance applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Tungsten Ore (APT) Prices Due to Supply Concentration

Western buyers scramble for long-term contracts, yet alternative mines need multi-year development cycles, limiting near-term relief. Price swings complicate project budgeting for aerospace and defense primes that rely on indexed contracts, creating a drag on the tungsten carbide powder market.

High Manufacturing and Processing Cost

Powder-production furnaces run at 2,700 °C and require refractory linings, high-vacuum systems, and skilled operators. Each energy-intensive batch inflates the per-kilogram cost relative to tool-steel competitors. Precision grades destined for surgical or turbine components demand x-ray diffraction and scanning-electron-microscopy certification, adding further overhead. Sumitomo Electric’s closed-loop recycling cuts virgin-feed consumption but needs extra clean-room powder sorting lines, which raise fixed costs in the near term. These economics factors temper the tungsten carbide powder market growth rate, especially in price-sensitive geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Grade: Cobalt-Bonded Leadership Faces Advanced-Alloy Competition

WC-Co grades anchored 68.74% of 2025 shipments owing to mature supply chains, broad-spectrum toughness, and an installed base of sintering furnaces optimized for cobalt binders. Even so, binder safety and cobalt price volatility spur the development of nickel-, iron-, and hybrid-binder systems. Carbide-rhenium alloys exhibit a compelling 6.08% CAGR curve as aerospace burners and hypersonic-vehicle parts demand elevated hot-hardness thresholds. Binder-less nano-WC powders push hardness beyond 2,200 HV30 and satisfy micro-tool manufacturers chasing sub-50 µm tip diameters.

By Application: Machining Tools Drive Precision Manufacturing

Machining tools generated the largest slice of the 2025 revenue pool with a 35.74% share of the tungsten carbide powder market. The segment benefits from the continuous growth of CNC machining centers and automated production cells, which depend on predictable insert wear patterns to uphold statistical-process-control targets. Rising investment in electric-vehicle driveline parts and miniaturized medical implants bolsters volume flow, while thermal-spray coatings and additive components registered the quickest 5.92% CAGR, reflecting the design freedom enabled by complex geometries. Ammunition applications maintain a niche yet stable demand for high-density projectiles where kinetic-energy transfer is essential.

By End-User Industry: Mining Dominance Meets Healthcare Innovation

Mining and construction consumed 44.29% of global shipments in 2025, reflecting the relentless abrasion and impact loads in rock-removal, crushing, and earth-moving machinery. Capital projects in copper, lithium, and critical-mineral deposits keep mining outfits replenishing drill bits and wear plates even as metal prices gyrate. Healthcare, by contrast, clocks the fastest 6.10% CAGR through 2031 on the back of single-use surgical blades, fine dentistry burs, and exploratory work on tungsten-based implants with superior biocompatibility. Automotive machining transitions from internal-combustion engines to electric-motor components, preserving stable insert demand while raising specifications for surface finish and edge quality.

Geography Analysis

Asia-Pacific held 53.82% of global revenue in 2025 and continues to outpace the field with a 6.36% CAGR through 2031. China’s mine head grades decline, yet process-efficiency gains and state incentives prolong its leadership position, even as export restrictions reshape the destination mix of downstream powders.

North America benefits from strategic-mineral legislation and defense sourcing rules that rank tungsten alongside rare earths and niobium. The USD 15.8 million US Department of Defense grant to Fireweed Metals accelerates feasibility studies at Mactung and locks in offtake expectations for domestic powder compaction lines.

Europe, though volume-constrained, preserves a technology-rich customer base in automotive, medical, and precision engineering. The tungsten carbide powder market in Europe remains sensitive to energy-cost spikes, yet the bloc’s net-zero mandates enhance the appeal of long-life carbide tooling that reduces resource intensity over multiple product cycles.

Competitive Landscape

Global supply is consolidated among vertically integrated groups that own raw-material mines, powder-production kilns, and insert-manufacturing lines. Chemical vapor deposition coatings, laser-printed gradient structures, and other process innovations create entry barriers rooted in intellectual property. Sandvik’s 2023 acquisition of Buffalo Tungsten enhances raw-material security for its North American insert factories, lowering logistical risk and shortening customer lead times.

Tungsten Carbide Powder Industry Leaders

Global Tungsten & Powders

CERATIZIT S.A.

Umicore

Kennametal

Hyperion Materials & Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Wall Colmonoy unveiled WallCarb HVOF tungsten carbide powders engineered to deposit dense coatings with high wear and corrosion resistance.

- December 2023: Sandvik AB completed the acquisition of Buffalo Tungsten Inc., expanding its tungsten metal and tungsten carbide powder footprint in North America.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the tungsten carbide powder market as all grades of sinter-ready WC feedstock, whether virgin, recycled, nano, or binder-enriched, sold in bulk or packaged form for use in cemented carbides, wear parts, thermal-spray, and additive-manufacturing blends. According to Mordor Intelligence, the addressable pool is restricted to powder revenues and excludes downstream fabricated inserts, hard-metal compacts, or finished tooling assemblies.

Scope exclusion: revenues linked to fused tungsten carbides, cast carbides, and tungsten-heavy alloys are outside this assessment.

Segmentation Overview

- By Product Grade

- WC-Co (Cobalt-bonded)

- WC-Ni (Nickel-bonded)

- WC-Fe (Iron-bonded)

- Carbide-Rhenium Alloys

- Binder-less Nano WC

- Recycled / Reclaimed WC Powders

- By Application

- Machining Tools

- Ammunition

- Wear and Die Parts

- Mining and Drilling Tools

- Other Applications (Additive Manufacturing, Thermal Spray Coatings, etc.)

- By End-User Industry

- Automotive

- Aerospace and Defense

- Mining and Construction

- Oil and Gas

- Healthcare

- Other End-User Industries (Electronics and Semiconductors,Industrial Manufacturing, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct ongoing interviews with powder producers, carbide tool makers, trading intermediaries, and regional distributors across Asia-Pacific, North America, and Europe. Dialogues probe contract volumes, binder mix shifts, average selling prices (ASP), and inventory turns, allowing us to validate secondary clues and close information gaps.

Desk Research

We begin with public datasets issued by authorities such as the US Geological Survey, UN Comtrade, and the International Tungsten Industry Association, which illuminate ore production, APT exports, and powder trade flows. Industry statistics from bodies like the European Powder Metallurgy Association, machine-tool output indices from Gardner Business Intelligence, and automotive build data from OICA help our team benchmark end-use health. Company 10-Ks, investor decks, and patent filings enrich trend discovery, while D&B Hoovers and Dow Jones Factiva provide structured financials for leading powder suppliers.

This list is illustrative, not exhaustive, and many other open sources were mined for corroboration.

Market-Sizing & Forecasting

A top-down construct starts with regional tungsten ore output and APT conversion yields, then applies penetration-rate assumptions to derive powder demand pools before selective bottom-up roll-ups of supplier shipments and sampled ASP × tonnage checks fine-tune totals. Key variables feeding the model include benchmark APT pricing, global machine-tool production, active rotary-rig counts, passenger-vehicle builds, and additive-manufacturing powder sales. Multivariate regression links these drivers to historical powder revenues, while scenario-tested CAGR paths (base, upside, downside) inform forecasts to 2030.

Data Validation & Update Cycle

Outputs undergo variance screening versus independent trade statistics; anomalies trigger re-checks with primary respondents. Senior analysts review every workbook prior to sign-off. We refresh each model annually and issue interim updates when ore disruptions, price spikes, or major capacity additions arise.

Why Mordor's Tungsten Carbide Powder Baseline Commands Reliability

Published estimates diverge because firms choose different powder grades, pricing resets, and refresh cadences.

Below we benchmark 2025 values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.25 B (2025) | Mordor Intelligence | - |

| USD 17.84 B (2024) | Global Consultancy A | Uses blended powder and sintered parts revenue; forecast rolled forward without 2025 ore-price correction |

| USD 16.90 B (2024) | Industry Association B | Relies on member survey averages; excludes nano-grade and reclaimed powders |

The comparison shows that when scope creep or outdated price decks slip in, values drift. By anchoring volumes to verified ore flows, tightening grade definitions, and running yearly refreshes, Mordor delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the tungsten carbide powder market?

The tungsten carbide powder market is valued at USD 17.06 billion in 2026 and is on course to reach USD 21.74 billion by 2031.

Which application segment leads the tungsten carbide powder market?

Machining tools lead, accounting for 35.74% of 2025 revenue, driven by precision requirements in automated manufacturing.

Why is Asia-Pacific the largest regional market?

Asia-Pacific hosts the majority of global tungsten mining and houses expansive automotive, electronics, and construction supply chains, resulting in 53.82% market share in 2025.

How are governments influencing tungsten supply security?

Legislations such as the US REEShore Act and defense stockpiling programs fund new mines and restrict reliance on Chinese tungsten, fostering diversified supply networks.

Which product grade is growing fastest?

Carbide-rhenium alloys show the highest projected CAGR at 6.08% through 2031 as aerospace and energy sectors seek higher temperature capability.

Page last updated on: