Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Tunable Diode Laser Analyzer Market Report is Segmented by Device Type (Portable, and Fixed), Measurement Methodology (In-Situ, and Extractive), Analyzer Type (Oxygen, Ammonia, Cox, Cxhx, Moisture, and More), End-User Industry (Oil and Gas, Power and Utilities, Metals and Mining, Chemicals and Petrochemicals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

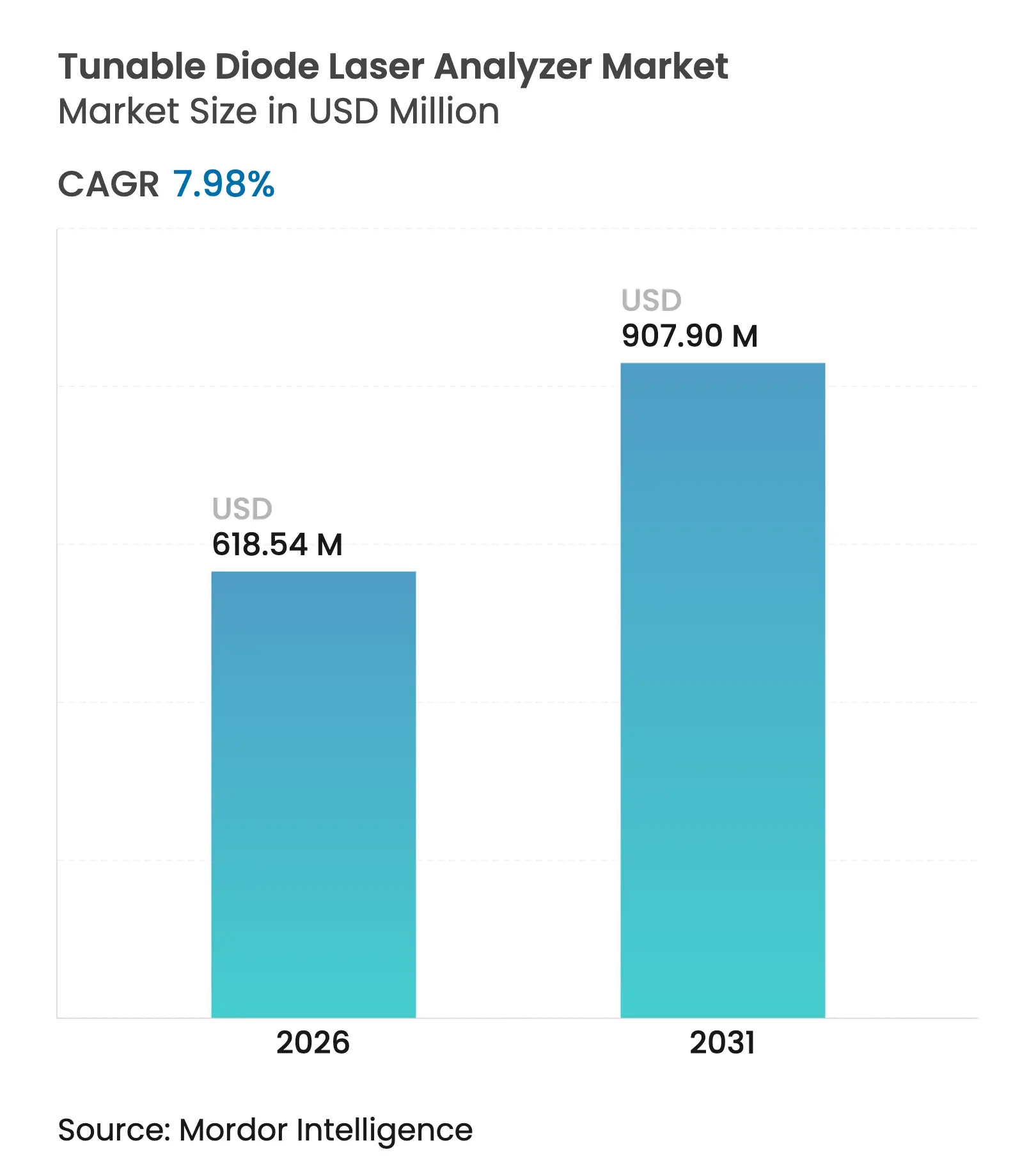

| Market Size (2026) | USD 618.54 Million |

| Market Size (2031) | USD 907.9 Million |

| Growth Rate (2026 - 2031) | 7.98 % CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The tunable diode laser analyzer market size was valued at USD 572.82 million in 2025 and estimated to grow from USD 618.54 million in 2026 to reach USD 907.9 million by 2031, at a CAGR of 7.98% during the forecast period (2026-2031). Demand is concentrated in heavy industries that face round-the-clock compliance checks, and suppliers that tie analyzers into wider digital control systems capture a price premium. Regulatory revisions in the European Union and real-time monitoring mandates across Asia explain much of the near-term uptake, while hydrogen blending in turbines and refinery decarbonization anchor longer-term growth. Technology risk from quantum-cascade solutions is real, yet ongoing cost reductions in TDLA optics and the arrival of dual-laser platforms help preserve competitiveness. Partnerships that fuse gas analysis, edge analytics, and predictive maintenance-such as the SICK-Endress+Hauser joint venture-serve as a template for how vendors will scale global reach without carrying full R&D costs.[1]Endress+Hauser, “Strategic Partnership Launched,” us.endress.com

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (-) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stricter decarbonization mandates in Asia-Pacific refineries driving continuous gas monitoring Stricter decarbonization mandates in Asia-Pacific refineries driving continuous gas monitoring | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) | (-) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:Asia-Pacific core, spill-over to MEA | Impact Timeline:Medium term (2-4 years) |

EU Industrial Emissions Directive revisions for real-time SOx/NOx tracking in smelters EU Industrial Emissions Directive revisions for real-time SOx/NOx tracking in smelters | +1.0% | Europe, extending to aligned jurisdictions | Short term (≤ 2 years) | |||

Hydrogen-ready gas turbine build-out increasing demand for moisture/oxygen TDLAs Hydrogen-ready gas turbine build-out increasing demand for moisture/oxygen TDLAs | +0.8% | Global, concentrated in North America & EU | Long term (≥ 4 years) | |||

Digitalization of GCC petrochemical complexes integrating TDLA-enabled predictive maintenance Digitalization of GCC petrochemical complexes integrating TDLA-enabled predictive maintenance | +0.6% | Middle East, expanding to emerging markets | Medium term (2-4 years) | |||

Sour-gas mega projects in Canada requiring H₂S-grade TDLAs Sour-gas mega projects in Canada requiring H₂S-grade TDLAs | +0.6% | North America, applicable to global sour gas fields | Medium term (2-4 years) | |||

China’s ultra-low-emission coal plant retrofits adopting in-flue NH₃ and O₂ TDLAs China’s ultra-low-emission coal plant retrofits adopting in-flue NH₃ and O₂ TDLAs | +0.5% | China, potential adoption in India & Southeast Asia | Short ter | |||

| Source: Mordor Intelligence | ||||||

Stricter Decarbonization Mandates in Asia-Pacific Refineries Driving Continuous Gas Monitoring

Asia-Pacific refineries are fitting continuous monitoring to track volatile organic compounds and greenhouse gases in real time, satisfying mandates that tighten annually.[2]BloombergNEF, “Asia Pacific’s Energy Transition Outlook,” assets.bbhub.io Storage tanks release 88.2% of typical refinery VOCs, so operators rely on in-situ TDLAs to pick up parts-per-trillion leaks rapidly. Australia’s 2025 fuel-quality revision forces refiners to lower aromatics and sulfur, raising the need for sub-second analytical feedback.[3]Department of Climate Change, Energy, the Environment and Water, “Regulating Australian Fuel Quality,” dcceew.gov.au Real-time gas composition feeds straight into advanced process-control loops that trim energy use and curb flare events. By merging analyzer data with cloud-based analytics, refiners unlock predictive maintenance routines that defer shutdowns while staying within emissions caps.

EU Industrial Emissions Directive Revisions for Real-Time SOx/NOx Tracking in Smelters

The 2022 amendment to the Industrial Emissions Directive adds stringent SO₂ and NOx thresholds that apply to 50,000 large EU installations, forcing capital budgets toward continuous analyzers.[4]International Energy Agency, “Directive 2010/75/EU on Industrial Emissions,” iea.org Smelters now transmit live stack readings to regulators, and TDLAs meet the directive’s low-drift accuracy targets in particulate-laden flues. Industrial air-pollution costs fell because plants that upgraded to optical monitors acted fast on excursions, saving EUR billions in externalities.[5]European Environment Agency, “Industrial Air Pollution Costs Update,” eea.europa.eu Vendors gain by offering analyzers with built-in cybersecurity and remote calibration, which dovetail with the directive’s digital-reporting clauses. Multinational metals firms replicate EU setups in Latin America and Southeast Asia, exporting demand beyond Europe.

Hydrogen-Ready Gas Turbine Build-Out Increasing Demand for Moisture/Oxygen TDLAs

Announced hydrogen projects could yield 49 million t per year by 2030, and utilities retrofit turbines to burn blends that lift thermal efficiency yet risk NOx spikes. Moisture and O₂ readings inside fuel lines guide control systems that balance flame temperature and emissions within milliseconds. Academic trials show efficiency rising from 39.4% to 40.2% when switching from methane to 30% hydrogen mixes, provided moisture stays inside a tight band. TDLAs excel here because they tolerate high-pressure lines without sample conditioning. With blades sensitive to water vapor corrosion, accurate moisture feedback prolongs component life and underpins turbine OEM warranties.

Digitalization of GCC Petrochemical Complexes Integrating TDLA-Enabled Predictive Maintenance

GCC producers implement AI maintenance platforms that ingest TDLA outputs to model wear patterns across pumps, crackers, and reformers. At one Saudi natural-gas-liquid plant, AI-driven schedules cut maintenance spend by 80% versus time-based routines. Analyzer data joins vibration and acoustic feeds inside digital twins, letting engineers forecast failure modes weeks ahead. As the region chases Vision 2030 diversification goals, digital plants become showcase assets that export know-how to Southeast Asian joint ventures. Vendors supplying rugged analyzers with OPC-UA connectivity gain preferred-supplier status on megaprojects financed by state oil companies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

OECD coal-plant CAPEX freeze limiting replacement units OECD coal-plant CAPEX freeze limiting replacement units | –0.6% | OECD countries, primarily North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:–0.6% | Geographic Relevance:OECD countries, primarily North America & Europe | Impact Timeline:Long term (≥ 4 years) |

High-particulate kiln exhaust performance drift delaying Indian cement uptake High-particulate kiln exhaust performance drift delaying Indian cement uptake | –0.5% | India, applicable to other emerging cement markets | Medium term (2-4 years) | |||

Substitution threat from multi-gas QCL spectrometers in EU chemicals Substitution threat from multi-gas QCL spectrometers in EU chemicals | –0.4% | Europe, potential expansion to North America | Medium term (2-4 years) | |||

IECEx-2024 hazardous-area re-certification delays IECEx-2024 hazardous-area re-certification delays | –0.2% | Global, affecting hazardous location deployments | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

OECD Coal-Plant CAPEX Freeze Limiting Replacement Units

Investors in North America and Europe postpone large retrofits amid policy debates on coal exit dates, so utilities maintain aging monitors rather than buy new TDLA stacks. A cautious spend climate caps short-term shipment volumes to legacy plants, even though existing stacks still need certification. Vendors respond with service contracts and modular optics that slot into older housings, keeping installed-base revenue flowing. Longer term, skills accrued in coal retrofits transfer to biomass and waste-to-energy projects where optical analyzers remain mandatory, cushioning the restraint’s impact on overall growth.

High-Particulate Kiln Exhaust Performance Drift Delaying Indian Cement Uptake

Cement kilns expose optics to dust loads that attenuate laser beams, forcing frequent lens cleaning that drives life-cycle cost up. Indian producers trial enhanced beam-folding designs and purge-gas shields, yet routine drift still erodes data confidence. Local certification lags compound the hurdle because plants need on-site labs to recalibrate optics. Suppliers now bundle auto-zero algorithms and sapphire-window assemblies to hold alignment longer in 1,600 °C gases. Once reliability proves out, the segment could swing from resistance to accelerated catch-up spending.

By Device Type: Fixed Systems Drive Continuous Monitoring

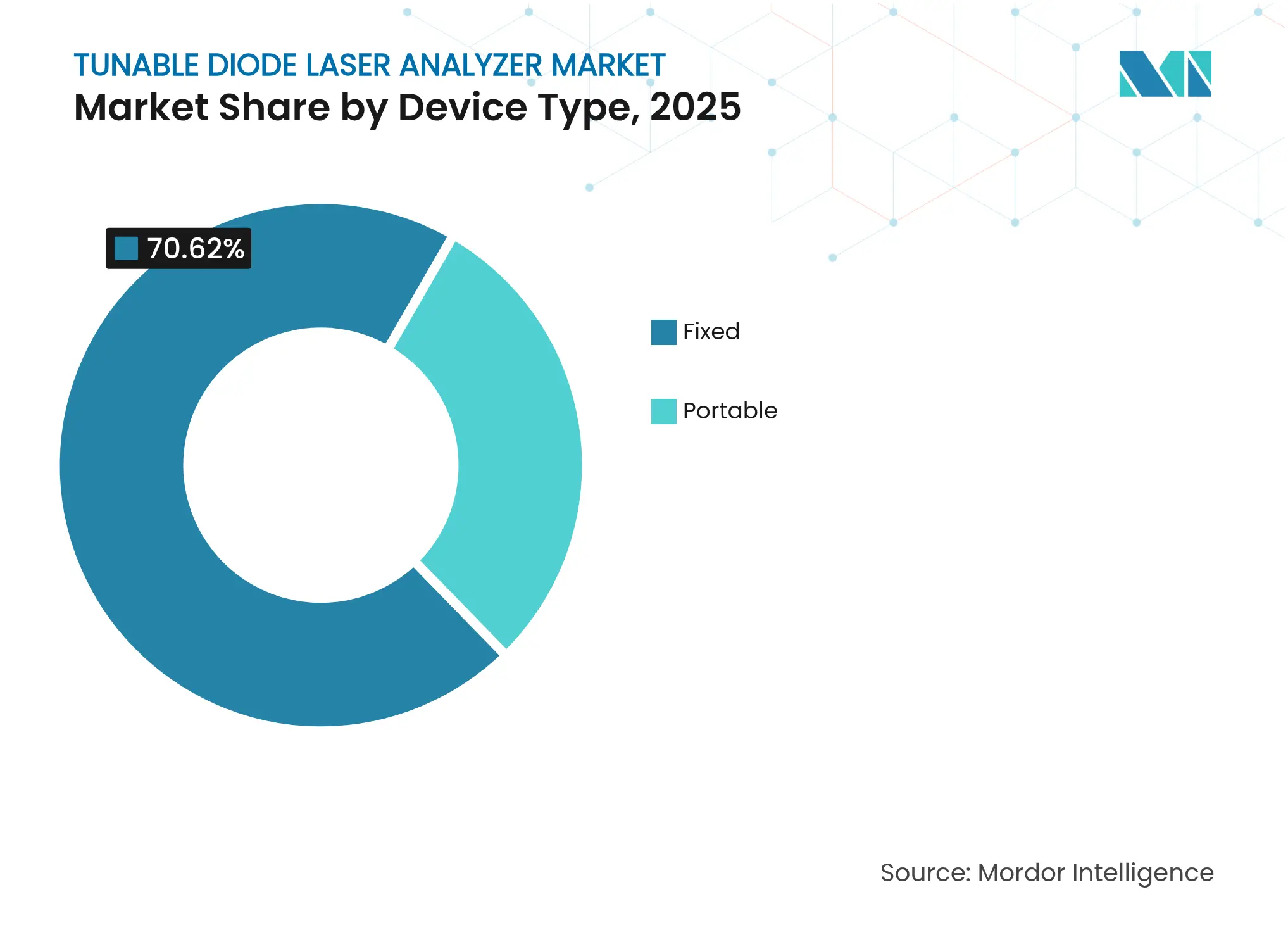

Fixed systems accounted for 70.62% revenue in 2025, reflecting their deep entrenchment in compliance workstreams where uninterrupted data logging is mandatory. Most power stations embed several fixed heads per stack, pairing analyzers with distributed control systems that auto-adjust dampers and burners. The tunable diode laser analyzer market size attributable to fixed platforms reached USD 404.57 million and is set to rise in line with stricter stack limits. Portable designs, while smaller in revenue, logged a lively 9.32% CAGR as safety teams adopt walk-around detectors to chase fugitive leaks on offshore decks and chemical tank farms. Lightweight frames, battery packs with eight-hour endurance, and Bluetooth data offload improve productivity for service crews that once relied on heavier sampling carts.

Field maintainers praise portable units for cutting incident response time because crews can confirm source gas within minutes and validate repairs before departing a site. Growth is further unlocked by rental companies that assemble regional fleets, giving smaller operators access without upfront capital. Fixed systems nevertheless retain the largest installed base because they interface seamlessly with plant historians that feed environmental dashboards, automated regulator filings, and insurance audits. Vendors bolster fixed offerings through dual-laser modules that cover wider gas ranges in a single stub, minimizing wall penetrations and purge requirements. Across both formats, wireless gateways and edge firmware upgrades keep instruments current without halting processes, a critical benefit when plants run near 95% utilization.

Note: Segment shares of all individual segments available upon report purchase

By Measurement Methodology: In-Situ Maintains Process Advantages

In-situ designs held 63.95% share because they read gas concentrations directly in hot, pressurized ducts, eliminating transport lag and condensate errors. Operators value sub-second feedback that captures load swings in boilers or reformers. The tunable diode laser analyzer market size for in-situ installations generated USD 366.3 million in 2025 and should expand steadily as emerging economies bypass extractive cabinets altogether. Extractive approaches, growing at 7.94% CAGR, stay relevant where sample conditioning boosts repeatability, such as chlorine plants or multipoint refineries wanting centralized analytics. Miniaturized chillers and low-dead-volume filters now make extractive skids smaller, letting them fit on crowded offshore topsides.

Process engineers weigh methodology trade-offs on a case-by-case basis, balancing fast response against maintenance exposure. In-situ probes cope better with dust and acid gases when fitted with air-knife purges, yet optical windows still require periodic cleaning. Extractive shelters simplify calibration because all instruments cluster in one safe enclosure, easing technician access during monsoon seasons or Arctic winters. Both camps adopt common digital backbones, with Modbus TCP and OPC-UA riding secure VLANs to plant servers. Cyber-hardened gateway modules encrypt firmware updates, preserving data integrity across lifecycles that stretch 12-15 years.

By Analyzer Type: Oxygen Leads While Ammonia Accelerates

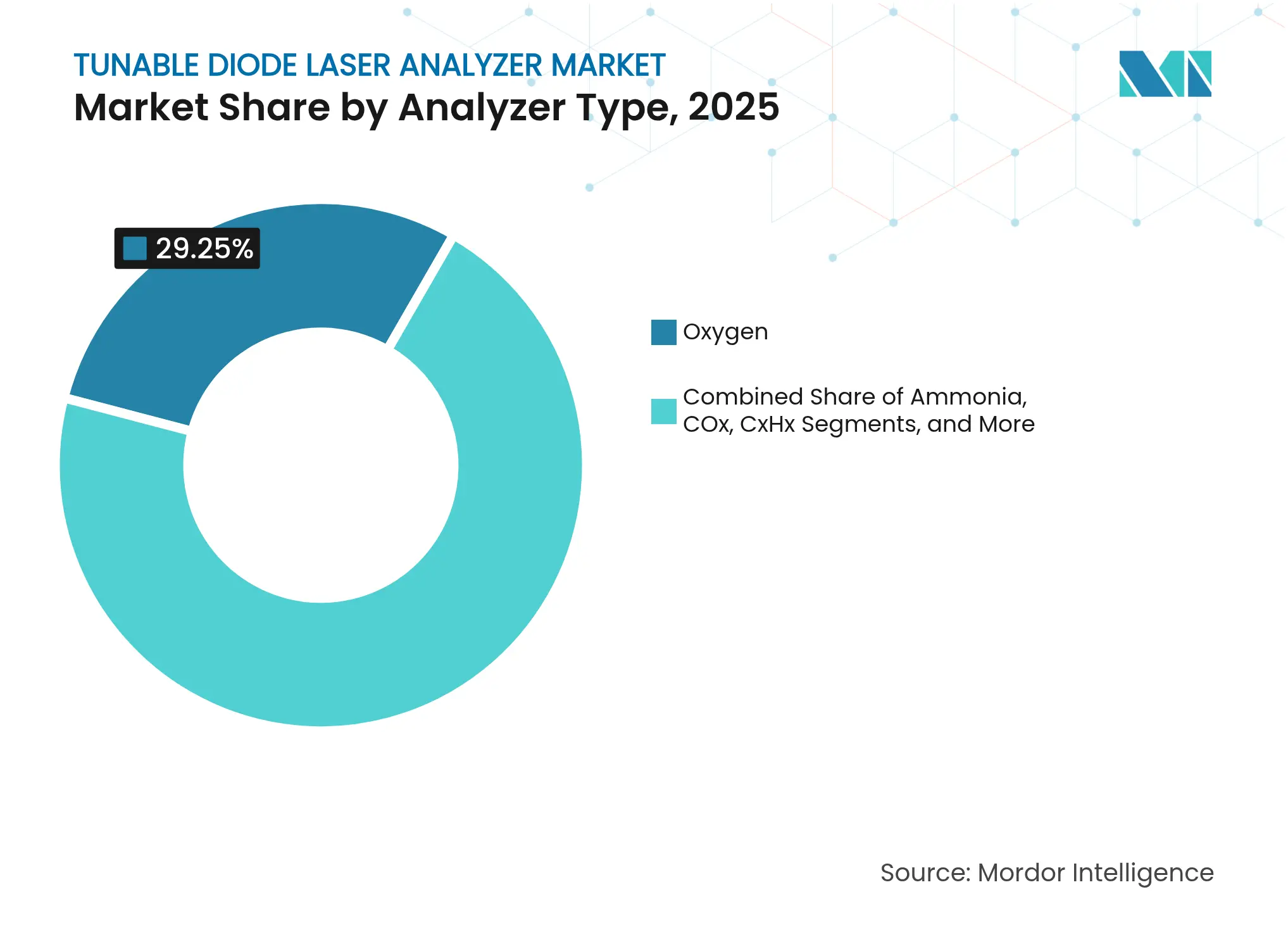

Oxygen analyzers captured 29.25% revenue owing to their foundational role in combustion control across steam boilers, gas turbines, and glass furnaces. Plants trim air-fuel ratios to within 0.5% excess oxygen, saving fuel while slashing CO output, so real-time O₂ feedback is indispensable. Ammonia units, advancing at 9.05% CAGR, receive a lift from selective catalytic reduction projects that need continuous NH₃ slip monitoring to confirm urea dosing efficiency. Segment demand also sprouts from fertiliser complexes and blue-ammonia export hubs that track product purity from synthesis loop to storage.

COx analyzers occupy a mature niche in carbon-management programs that link stack CO₂ trends with carbon-credit dashboards. Moisture models enjoy new interest in hydrogen pipelines where parts-per-million water can embrittle steels. HF and HCl variants find use in waste-to-energy plants and battery-material recyclers that handle halogen-rich feedstock. Hydrocarbon analyzers help petrochemicals detect flare imbalances and diagnose catalytic-cracker yields. Multi-gas modules bundle two or more species in a single housing, yielding capex savings of up to 25% relative to single-gas fleets and reinforcing the total value proposition.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Oil and Gas Dominates, Healthcare Surges

Oil and gas remained the top customer, holding 34.40% revenue in 2025 on the back of refinery expansions, LNG surge lines, and high-pressure pipeline safety mandates. Offshore platforms justify multiple tunable diode laser analyzer market size deployments because any H₂S excursion endangers crew and equipment. Downstream complexes integrate analyzer outputs into advanced-process-control loops that squeeze an extra 0.5% distillate yield, delivering rapid payback. Healthcare and pharmaceuticals, although smaller, record the fastest 9.72% CAGR, driven by vaccine fill-finish lines and novel diagnostic devices that need parts-per-trillion gas purity.

Utilities deploy TDLAs to regulate O₂, CO, and NH₃ in flue gases, ensuring boilers meet 15 mg/Nm³ NOx limits while extracting incremental megawatts. Metals and mining operators monitor off-gases in smelters and sinter plants to comply with sulfur caps. Chemical producers wield analyzers to guard polymer reactors against oxygen ingress that ruins batch integrity. Pulp and paper mills employ in-situ lasers for lime-kiln optimization, shaving fuel and minimizing opacity complaints in nearby communities. Newer verticals include semiconductor fabs that track moisture in ultra-high-purity nitrogen networks and food processors that validate modified-atmosphere packaging lines.

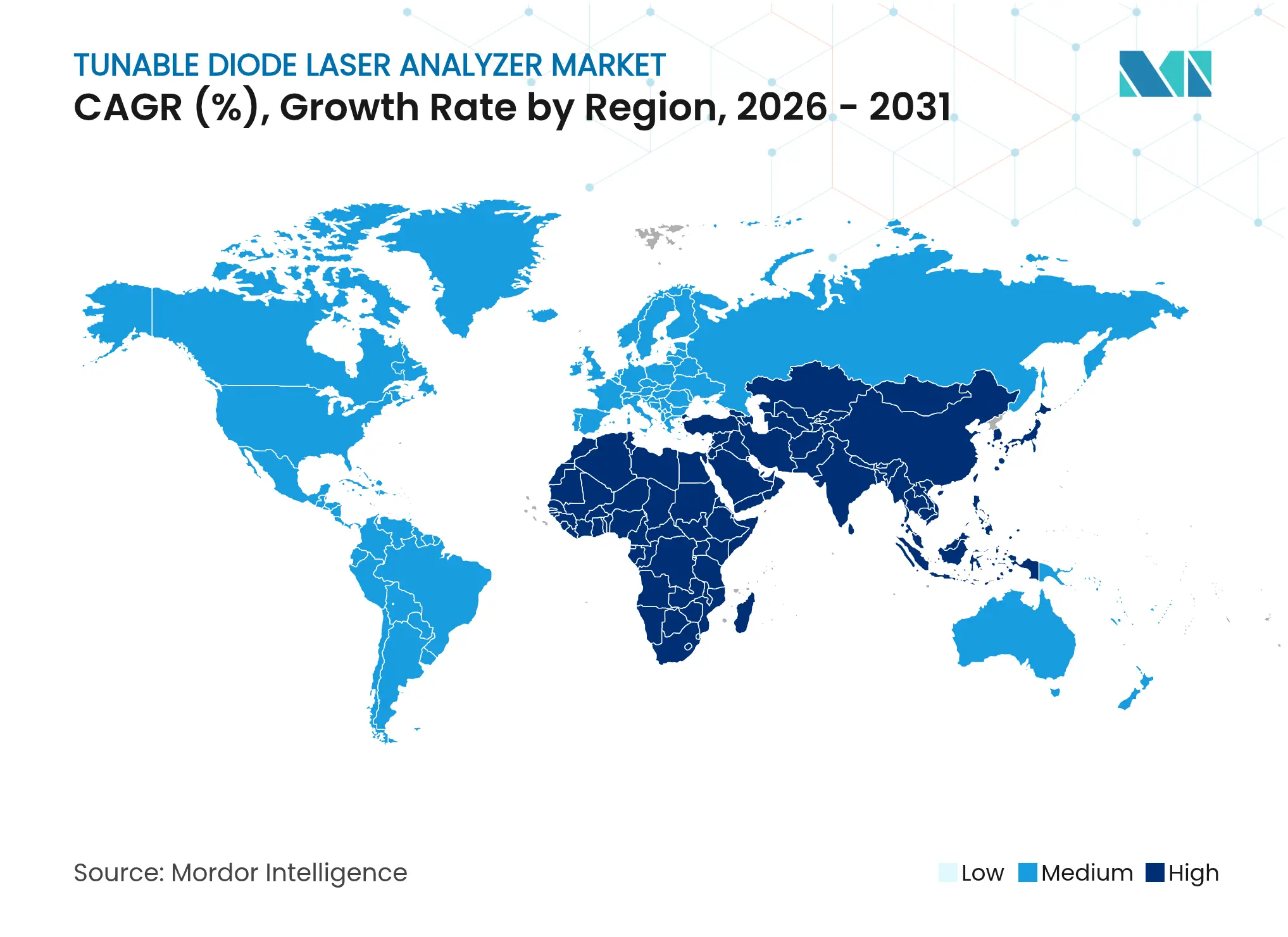

Asia-Pacific delivered 39.10% of global 2025 revenue, powered by aggressive industrial expansion, reinforced environmental oversight, and massive infrastructure investment cycles. China’s ultra-low-emission retrofit program pulls in hundreds of in-flue NH₃ and O₂ lasers annually, while India’s steel mills and cement kilns prepare for tighter particulate and NOx rules. Japan supplements the regional base with hydrogen pilot networks that require moisture and trace-oxygen instruments. Southeast Asia enforces sulfur caps on marine bunkers, extending demand from land-based stacks to ship-borne scrubber outlets.

North America commands a stable installed base anchored in EPA Clean Air Act directives that stipulate continuous emission monitoring for boilers above 25 MW. Canadian sour-gas projects fund specialty H₂S analyzers rated to -40 °C ambient and 1,000 psi line pressure. Mexico’s industrial corridors, aided by near-shoring trends, add incremental momentum as foreign investors insist on environmental controls mirroring US standards.

Europe upholds sophisticated compliance regimes under the Industrial Emissions Directive, yet coal-capex austerity tempers new unit sales in traditional power. Nevertheless, chemical parks retrofit multi-wavelength optics to outmaneuver QCL competition by combining TDLA speed with broader spectral coverage. The Middle East and Africa post the highest 8.12% CAGR, reflecting giga-scale refinery and petrochemical ventures that integrate predictive maintenance from day one. South America shows steady growth as Brazil tightens state environmental codes and ethanol plants demand moisture control. Across these regions, distributors that preload firmware in local languages and offer rapid field service achieve faster penetration.

Market Concentration

he tunable diode laser analyzer market remains moderately fragmented, yet consolidation is accelerating as incumbents strive for full-line portfolios and geographic depth. SICK’s divestment of its process-analysis division to Endress+Hauser in July 2025 transferred 800 staff and a rich patent bank, forming a dedicated gas-analysis joint venture that wields combined sales channels on every continent. ABB strengthened its environmental suite by adding FTIR modules that complement TDLA speed with broader compound coverage, giving clients one-stop procurement for complex permits. Honeywell, for its part, packaged analyzers with methane-management software certified for offshore hazardous zones, carving a niche in upstream sustainability reporting.

Technology race dynamics center on long-wavelength quantum-cascade lasers that promise multi-gas detection in a single beam, though Fraunhofer’s June 2025 cost-cut breakthrough narrows price gaps and raises competitive pressure. TDLA leaders retaliate by shrinking optical benches, boosting diode lifetime to 10 years, and layering AI calibration routines that halve zero-drift. Start-ups exploit low-cost gallium-antimonide diodes, bundling cloud dashboards targeted at small utilities lacking deep IT staff.

Partnerships extend beyond hardware; Yokogawa and Microsoft co-develop digital twins that model gas-plant emissions in real time, embedding TDLA datapoints to forecast compliance risk. Service revenue rises as vendors guarantee analyzer uptime, with premium plans featuring 24/7 remote diagnostics and auto-replenished consumables. The competitive script also includes geographic alliances-Latin American distributors gain exclusivity by stocking spares locally, cutting downtime for miners in the Andes. Intellectual-property barriers stay high because diode fabrication know-how and proprietary modulation algorithms remain costly to replicate, preserving incumbents’ pricing power.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Tunable diode laser analyzers (TDL analyzers) are gas analyzers designed to measure the concentration of specific species within a gas mixture using laser absorption spectrometry. A laser beam in a TDL analyzer is adjusted to detect a specific gas type as it moves through the gas and reaches a detector. When this gas is present in the gas stream, it absorbs light and lowers the signal intensity. A photodiode in the TDL analyzer then analyzes the light gathered by the detector to accurately measure the gas concentration.

The tunable diode laser analyzer market is segmented by device type (portable and fixed), measurement type (in situ and extractive), analyzer type (ammonia analyzer, oxygen analyzer, CXHX analyzers, COX analyzers, moisture analyzers, HX analyzers, and other analyzers), end-user industry (oil and gas, power and utilities, metal and mining, healthcare, paper and pulp, chemical and petrochemicals, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the market size and forecasts for all the above segments in value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.