Laser Diode Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

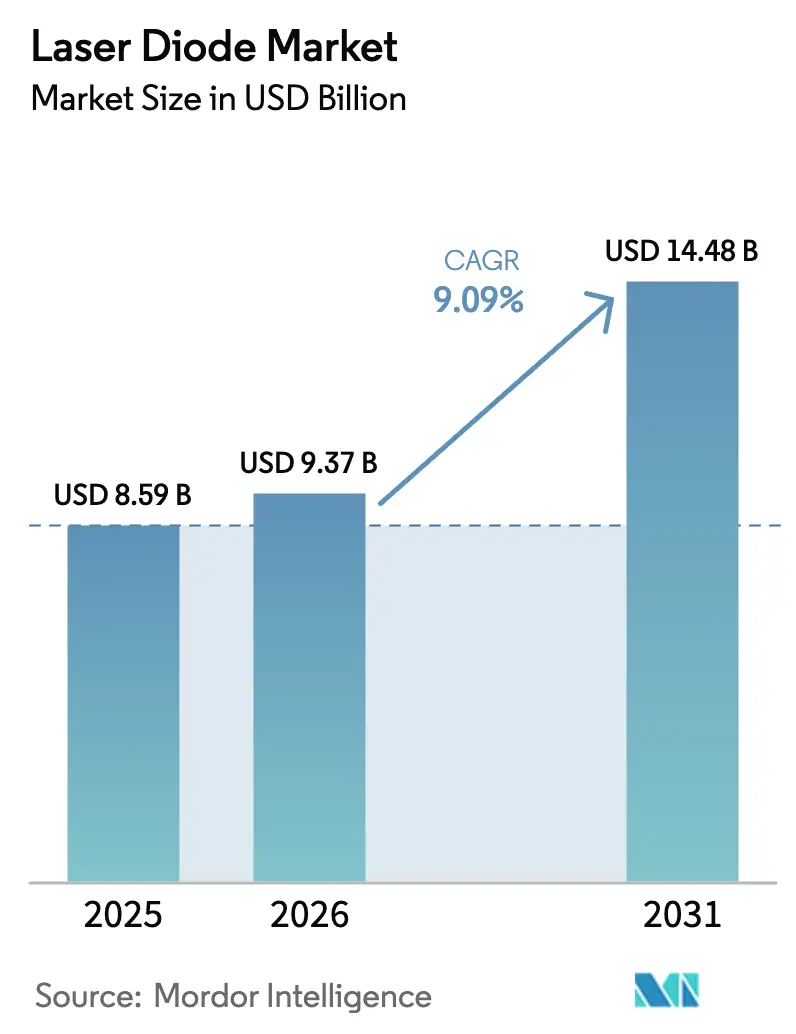

| Market Size (2026) | USD 9.37 Billion |

| Market Size (2031) | USD 14.48 Billion |

| Growth Rate (2026 - 2031) | 9.09% CAGR |

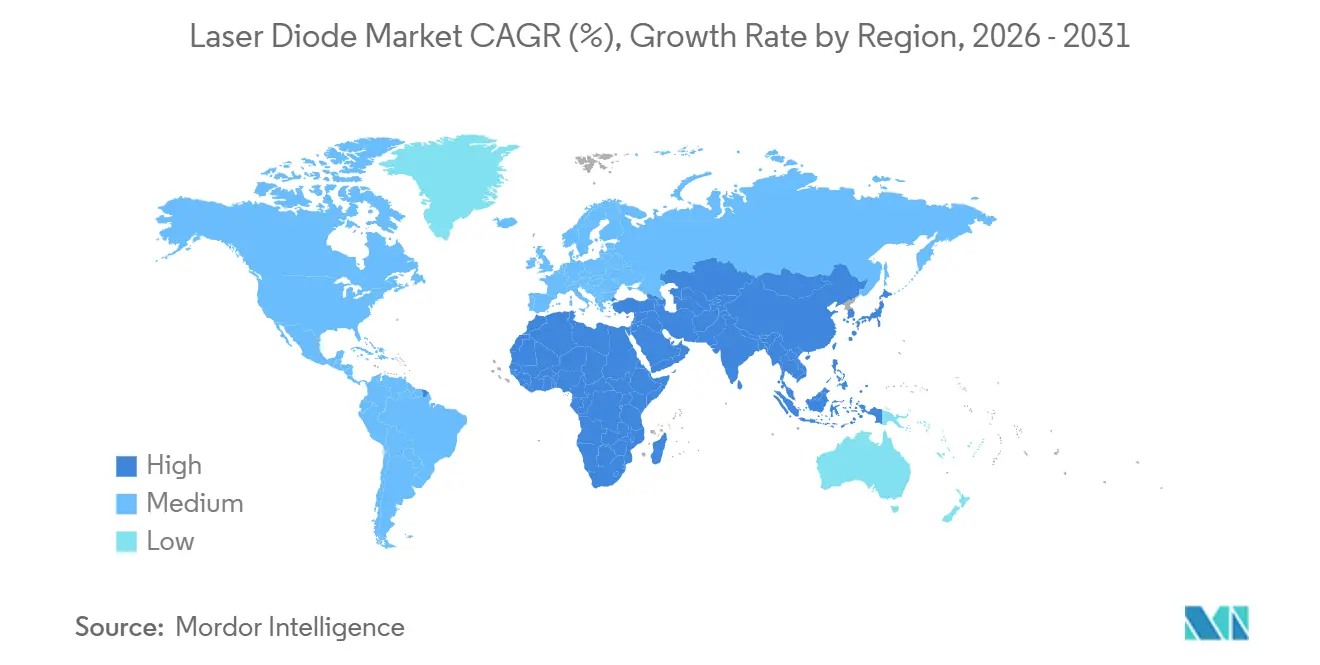

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laser Diode Market Analysis by Mordor Intelligence

The Laser Diode Market size is projected to be USD 8.59 billion in 2025, USD 9.37 billion in 2026, and reach USD 14.48 billion by 2031, growing at a CAGR of 9.09% from 2026 to 2031. Growing demand for 800-gigabit and 1.6-terabit optical links in hyperscale data centers, the integration of solid-state LiDAR in production vehicles, and defense funding for diode-pumped directed-energy weapons are reshaping competitive priorities within the laser diode market. Edge-emitting designs remain vital for long-haul fiber deployments, yet vertical-cavity surface-emitting lasers (VCSELs) are taking share in 3D sensing and short-reach parallel optics, while high-power stacks are powering additive-manufacturing lines that now build titanium parts at triple the 2023 throughput. Asia-Pacific leads installed capacity thanks to vertically integrated fabs in Japan and large-scale subsidies in China, whereas North American suppliers are expanding domestic epitaxy to comply with local-content mandates and to buffer gallium-indium price swings. Together, these shifts are expected to keep the laser diode market on a steady high-single-digit growth path despite thermal-management bottlenecks above 20 watts continuous output.

Key Report Takeaways

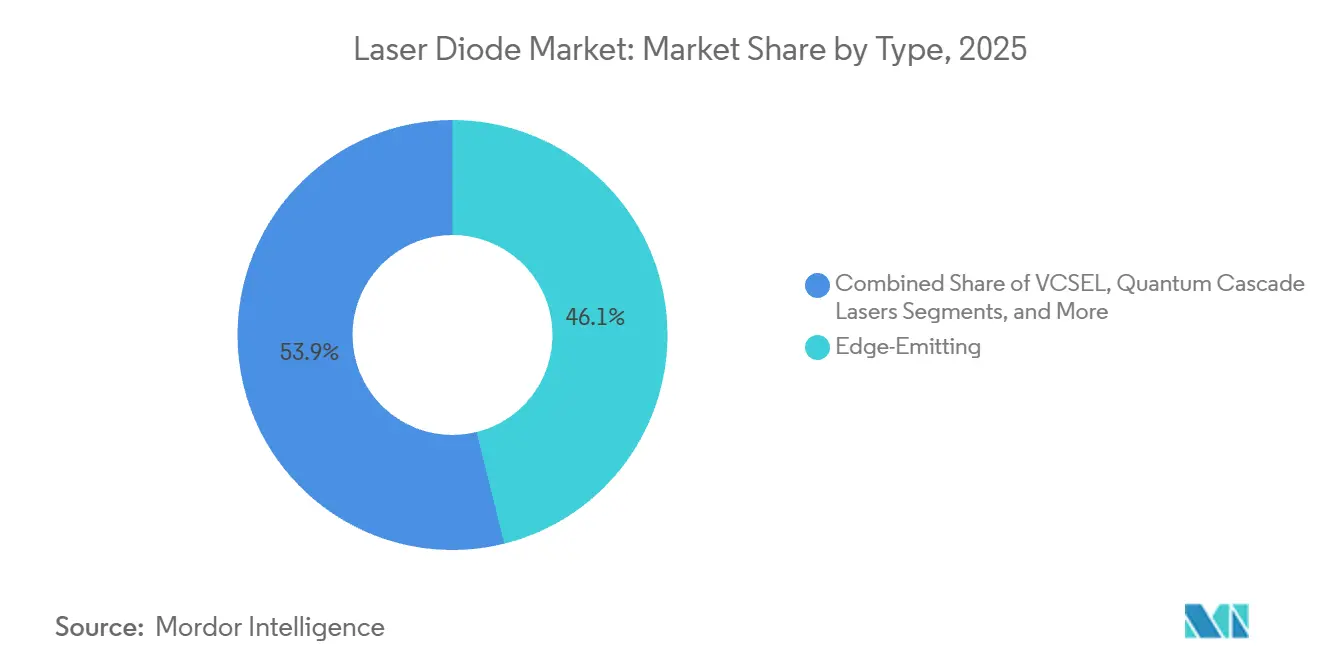

- By type, edge-emitting devices commanded 46.13% of laser diode market share in 2025, while VCSELs are forecast to expand at a 10.98% CAGR through 2031.

- By wavelength, infrared sources held 49.21% revenue share in 2025, whereas blue emitters are projected to grow at 11.82% to 2031.

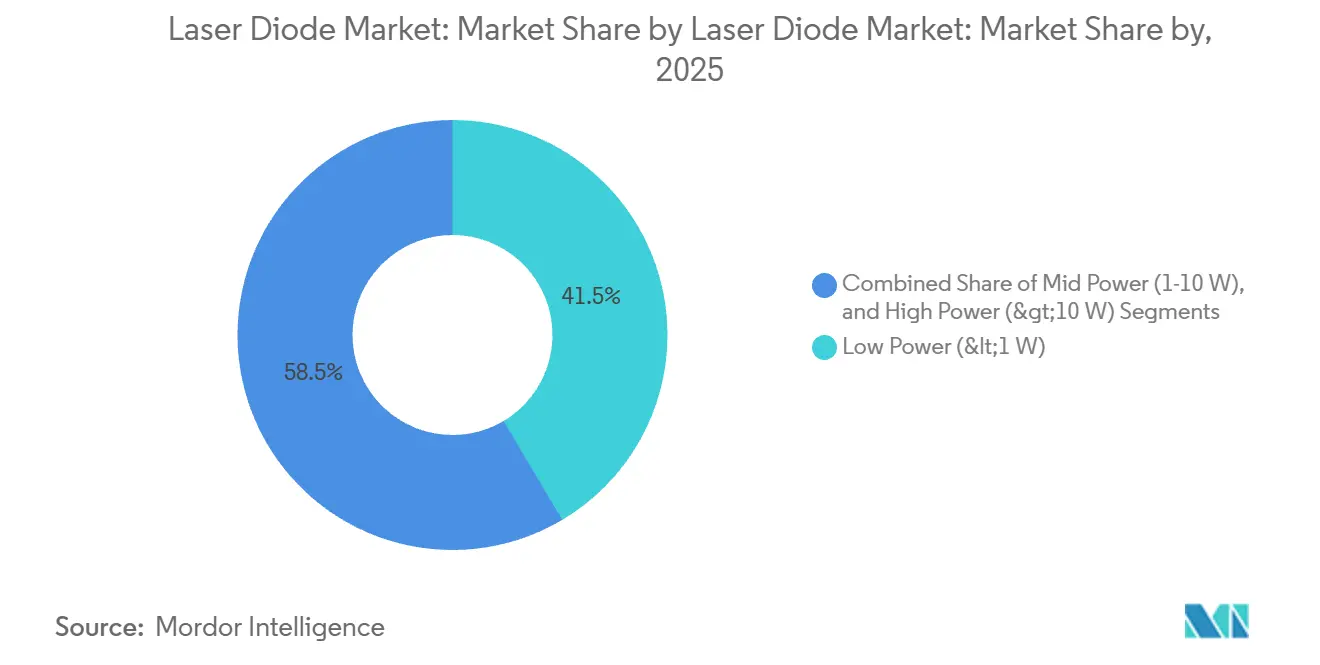

- By output power, low-power diodes below 1 watt led unit shipments with 41.47% in 2025, yet modules above 10 watts are poised for a 12.69% CAGR.

- By operating mode, continuous-wave operation accounted for 63.71% of shipments in 2025, while pulsed lasers are set to advance at 11.32% through 2031.

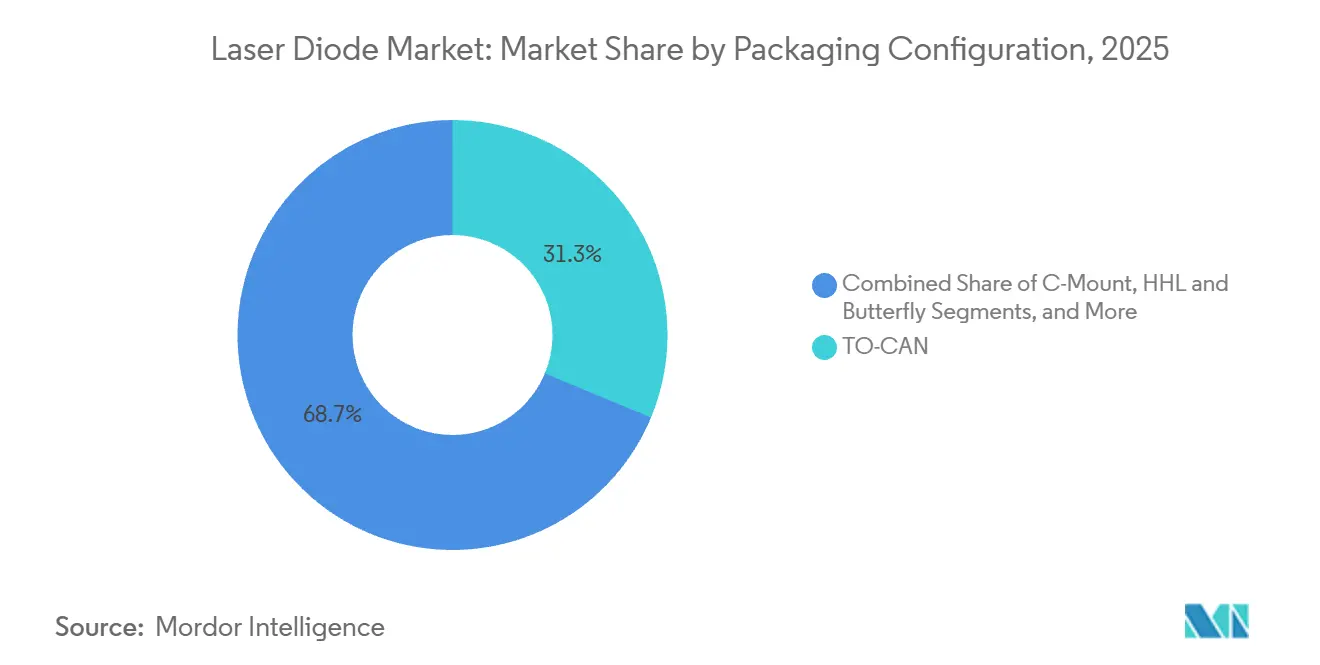

- By packaging, TO-CAN retained 31.27% share in 2025, and integrated modules are expected to grow at 10.23% over the outlook.

- By end-user, telecommunications and datacom held 39.18% revenue share in 2025, whereas automotive applications are projected to expand at 13.12% CAGR.

- By geography, Asia-Pacific captured 53.61% of 2025 revenue, and the Middle East is forecast to grow at 12.46% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laser Diode Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 3D sensing and Face-ID in smartphones propelling VCSEL demand | +1.8% | Global, with APAC core manufacturing and North America design leadership | Medium term (2-4 years) |

| Rapid deployment of FTTH networks leveraging 1550 nm DFB lasers | +1.5% | APAC core, spill-over to Middle East and South America | Short term (≤ 2 years) |

| Automotive LiDAR programs adopting 905 nm pulsed lasers | +2.1% | Europe and North America regulatory push, APAC production scale | Long term (≥ 4 years) |

| Rising use of high-power diode lasers in metal additive manufacturing | +1.3% | North America and Europe industrial hubs, emerging APAC adoption | Medium term (2-4 years) |

| Defense funding surge for directed-energy weapons utilizing diode-pumped modules | +1.2% | North America and Europe defense budgets, Middle East procurement | Long term (≥ 4 years) |

| Miniaturization of medical aesthetic devices integrating blue-green GaN lasers | +0.9% | Global, with early adoption in North America and Europe clinical markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 3D Sensing and Face-ID in Smartphones Propelling VCSEL Demand

Global smartphone makers shipped roughly 1.2 billion handsets with embedded VCSEL arrays in 2025, enabling secure facial authentication and depth-enhanced imaging. Apple drove the pace by expanding TrueDepth adoption, prompting Lumentum to boost its Thailand die-sorting capacity by 30% to meet iPhone 17 orders. Android OEMs followed suit, with Samsung and Xiaomi selecting ams OSRAM 940-nanometer arrays that maintain false-reject rates below 0.5% in bright sunlight.[1]ams OSRAM, “VCSEL Technology,” AMS-OSRAM.COM VCSELs cut assembly cost because they withstand reflow humidity, eliminating hermetic sealing that edge-emitters require. Compliance with IEC 60825-1 Class 1 limits has led suppliers to finetune beam divergence and duty cycles, keeping peak exposure within 0.39 milliwatts at the cornea, thereby sustaining momentum in the laser diode market.

Rapid Deployment of FTTH Networks Leveraging 1550 nm DFB Lasers

Worldwide FTTH lines exceeded 680 million in 2025, with China contributing 58% of net additions under provincial gigabit mandates. Distributed-feedback lasers at 1550 nanometers minimize chromatic dispersion, enabling 40 kilometer passive optical links that support 1:128 split ratios. MACOM released a 25-gigabit indium-phosphide DFB with integrated electro-absorption modulator in 2025, shrinking module footprint by 40% and lowering power budgets in dense access nodes. Turkey’s national fiber plan deployed 4.2 million new homes that same year using Sumitomo Electric lasers, further broadening the addressable laser diode market. OpenLight’s 1.6-terabit DR8 transceiver, demoed in September 2025, validates that these same 1550 nanometer lanes will move inside AI clusters by 2027.

Automotive LiDAR Programs Adopting 905 nm Pulsed Lasers

Automotive LiDAR shipments in 2025 centered on 905 nanometer emitters because silicon APDs deliver higher quantum efficiency than 1550 nanometer InGaAs detectors, saving about 35% on device cost. Coherent delivered 400-watt VCSEL arrays that enable flash LiDAR architectures with no moving parts, achieving 200 meter pedestrian detection and meeting Euro NCAP 2026 emergency-braking criteria. Lumentum’s 300-watt arrays in 5-nanosecond pulses meet similar ranges with adaptive beam shaping to satisfy IEC Class 1 eye safety. Excelitas launched a 12-cubic-centimeter module integrating driver and thermal sensor, allowing side-mirror placement for blind-spot monitoring, illustrating how module integration boosts unit economics within the laser diode market. Regulatory convergence in Europe and China around Level 3 autonomy by 2028 underpins a strong long-term growth runway.

Rising Use of High-Power Diode Lasers in Metal Additive Manufacturing

Metal additive-manufacturing system shipments rose 22% in 2025 as aerospace and medical implant makers embraced laser powder-bed fusion. TRUMPF’s TruDiode stacks provide up to 6 kilowatts, letting EOS push build rates to 110 cubic centimeters per hour, cutting titanium part cost by 25% relative to 2023 baselines. IPG Photonics recorded USD 89 million in Q3-2024 diode revenue tied to pump sources for fiber lasers employed in battery-pack welding. Coherent improved wall-plug efficiency to 65%, saving USD 0.08 per kilowatt-hour in continuous 24-hour production runs. Thermal spikes above 20 watts are now mitigated with diamond heat spreaders that drop junction temperature by 18 degrees Celsius, extending diode life to 25,000 hours and reinforcing high-power credibility in the laser diode market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal management challenges limiting continuous-wave scaling above 20 W | -0.8% | Global, with acute impact in high-power industrial and defense applications | Short term (≤ 2 years) |

| Supply-chain dependency on gallium and indium causing price volatility | -1.1% | Global, with supply concentration in China and refining bottlenecks | Medium term (2-4 years) |

| Safety regulations on eye exposure restricting consumer-grade power in Europe | -0.6% | Europe primary, with spill-over to markets adopting IEC standards | Long term (≥ 4 years) |

| Yield variability in GaN-on-silicon wafer fabrication raising costs for Blu-ray lasers | -0.7% | Global, with manufacturing concentrated in Japan and Taiwan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal Management Challenges Limiting Continuous-Wave Scaling Above 20 W

Junction temperatures climb above 85 degrees Celsius when continuous output exceeds 20 watts, cutting carrier-recombination efficiency by 12% per 10-degree rise and shortening lifetime. Microchannel coolers add USD 45 per module and consume 15 watts for pumping, eroding the efficiency edge over lamp-pumped solid-state lasers. Synthetic diamond plates offer five-fold higher thermal conductivity, tested by nLIGHT in 100-watt fiber-coupled modules that achieved an 18 degree reduction in junction temperature but at USD 12 per square centimeter premium. IEEE researchers in 2025 proposed gallium-indium phase-change inserts that absorb transient heat during pulsed duty but remain incompatible with telecom hermeticity standards.[2]IEEE Photonics Journal, “Thermal Management in High-Power Laser Diodes,” IEEE.ORG Until packaging costs fall, this restraint will moderate the top-end of the laser diode market power roadmap.

Supply-Chain Dependency on Gallium and Indium Causing Price Volatility

Chinese export controls announced in 2023 sent gallium spot prices to USD 400 per kilogram in 2024, a 180% spike over 2022 averages, before easing to USD 320 by late-2025 as Japanese and South Korean recyclers scaled secondary output. Indium hovered between USD 300 and USD 350 per kilogram amid primary supply of only 950 tons worldwide, 58% sourced from China. Nichia trimmed active-region thickness in its 450 nanometer blue lasers by 20% in 2025, cutting indium per wafer without losing quantum efficiency. Sumitomo Electric’s gallium-recovery program reclaimed 72% of metal from retired telecom modules, satisfying 8% of internal demand by mid-2025. Nevertheless, price volatility increases working capital and margin pressures across the laser diode market until geographic diversification of refining gains momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: VCSEL Momentum Reshapes Emitter Economics

Edge-emitting devices led the laser diode market with 46.13% share in 2025, owing to unmatched single-mode coupling efficiency for long-haul links. VCSEL arrays are forecast to grow at 10.98% through 2031, driven by wafer-level testing speeds that reach 12,000 dice per hour, far surpassing cleaved-facet edge emitters. Quantum-cascade lasers remain niche in mid-infrared sensing, while Fabry-Perot diodes serve cost-sensitive short-reach networks.

Production economics favor VCSELs in consumer electronics where board space is at a premium and hermetic sealing can be skipped, cutting assembly steps by 25%. Edge emitters will stay dominant in dense wavelength-division multiplexing, yet a gradual mix shift toward VCSELs keeps competitive focus on high-throughput wafer fabrication. This dynamic underscores how emitter innovation is central to sustaining long-run expansion of the laser diode market.

By Wavelength: Blue Diodes Advance on GaN Cost Declines

Infrared sources between 700 and 1600 nanometers generated 49.21% of 2025 revenue, underlining their role in telecom, industrial sensing, and fiber-laser pumping. Blue diodes at 400 to 500 nanometers are projected to expand at 11.82% CAGR as laser-phosphor projectors deliver 4,000 lumens from 3-watt chips, replacing mercury lamps in displays and automotive head-up systems.

Nichia’s 450 nanometer devices achieved 42% wall-plug efficiency, enabling a 5,000-lumen portable projector that weighs just 1.8 kilograms. Red and green bands grow modestly, while ultraviolet yields lag due to GaN-on-silicon defect densities. Collectively these trends diversify revenue streams, supporting stable long-term prospects for the laser diode market.

By Output Power: High-Power Modules Gain Industrial Traction

Low-power devices below 1 watt represented 41.47% of 2025 unit shipments, serving peripheral and consumer applications. High-power modules above 10 watts are expected to post a 12.69% CAGR, propelled by welding, cutting, and additive-manufacturing lines that now rely on kilowatt-class stacks.

TRUMPF’s 6 kilowatt TruDiode units deliver 68% wall-plug efficiency, lowering energy cost by USD 0.11 per kilowatt-hour versus legacy CO₂ lasers. IPG and Coherent added fiber-coupled outputs that slice 12 millimeter stainless steel at 2 meters per minute. This shift toward higher power broadens addressable segments and enlarges the laser diode market size in industrial verticals.

By Operating Mode: Pulsed Adoption Accelerates in LiDAR and LIBS

Continuous-wave operation held 63.71% share in 2025 as datacom and medical segments favor steady output. Pulsed lasers are forecast to climb 11.32% on the back of LiDAR and laser-induced breakdown spectroscopy that demand nanosecond timing accuracy.

Lumentum’s 300-watt 5-nanosecond arrays enable 200-meter pedestrian detection, while TRUMPF’s TruMark series etches titanium implants at 400 characters per second. Rising mining adoption of LIBS sensors for ore-grade analysis further expands pulsed revenue, reinforcing diversified growth in the laser diode market.

By Packaging Configuration: Integrated Modules Displace Discrete Cans

TO-CAN designs retained 31.27% market share in 2025 thanks to telecom-grade hermeticity and proven field life. Integrated modules are projected to grow at 10.23% as customers seek turnkey housings that bundle drivers, thermistors, and fiber pigtails.

Excelitas’ 12-cubic-centimeter LiDAR package cuts assembly steps from 14 to 3 and trims USD 18 per unit, demonstrating why automakers value integration. C-mount and HHL formats maintain relevance in high-power and DWDM niches, yet the trajectory favors module density, boosting overall competitiveness in the laser diode market.

By End-User Application: Automotive Emerges as Fastest-Growing Vertical

Telecommunications and datacom accounted for 39.18% of 2025 revenue, anchored by 400-gigabit and 800-gigabit transceiver demand. Automotive applications are forecast to expand at 13.12% CAGR as Level 3 autonomy rules in Europe and China mandate solid-state LiDAR in new vehicles by 2028.

Industrial processing absorbed 24% of high-power shipments for welding and cutting, while healthcare posted steady growth with blue-green diodes in dermatology. Defense contracts for fiber-pumped directed-energy systems add high-value volume, further diversifying downstream pull in the laser diode market.

Geography Analysis

Asia-Pacific generated 53.61% of global revenue in 2025, backed by Japan’s integrated supply chains and China’s USD 47 billion semiconductor stimulus that lifted compound-semiconductor wafer output by 34% from 2023.[3]China State Council, “Semiconductor Plan,” GOV.CN South Korea consumed 92 million diodes for smartphones and 5G backhaul, illustrating the region’s balanced mix of consumer and infrastructure demand.

North America contributed roughly 22% of sales, leveraging defense appropriations and hyperscaler procurement. Lumentum expanded California cleanrooms in August 2025 to meet CHIPS Act domestic-content thresholds. Europe held an 18% share, with German automakers integrating LiDAR in 1.8 million cars and the UK National Health Service rolling out laser-based diagnostics in 420 hospitals.

The Middle East, projected at a 12.46% CAGR, is wiring Saudi Vision 2030’s fiber backbone and UAE hyperscale clusters that will drive 15 exabytes per month of cross-border traffic by 2029. South America and Africa remain emerging, yet Brazil’s national broadband plan and Kenya’s fiber backhaul projects underscore incremental opportunities for suppliers attuned to local standards. Together, these patterns reinforce a geographically diversified laser diode market.

Regulatory Landscape

Laser diode shipments into consumer, industrial, and medical end uses continue to be shaped by safety and conformity regimes that increasingly reference IEC methods. In the United States, FDA radiation safety requirements under 21 CFR 1040.10 and 1040.11 govern laser products, and FDA Laser Notice No. 56 provides a pathway for conformance using IEC 60825-1 and IEC 60601-2-22 provisions in lieu of specific US performance standard clauses. For medical lasers, FDA-recognized consensus standards are also shifting, with declarations of conformity to IEC 60601-2-22 Edition 3.1 no longer accepted after July 4, 2027, requiring suppliers and OEMs to refresh test plans and documentation cycles.

For Europe, medical laser equipment aligns with the EU Medical Device Regulation (MDR) 2017/745 and related harmonized standards updates, including the 2026 amendment SIST EN IEC 60601-2-22:2020/A11:2026 that supports essential safety requirements. On the trade and security side, export-control tightening has added an additional compliance layer for high-power laser-related items: on June 26, 2026, the US Bureau of Industry and Security issued an interim final rule placing certain laser optical control modules (10 kW or above with dynamic beam-shaping capability) under additional export licensing requirements for specified destinations. This can affect qualification, configurability, and order acceptance for parts used in high-power processing systems that utilize diode-based sources and pump modules.

Value Chain Analysis

The laser diode value chain starts with constrained raw materials (notably gallium and indium) and compound-semiconductor substrates (GaAs and InP), then moves through epitaxial wafer growth (MOCVD/MBE), wafer fabrication, facet processing and coating, die singulation, and packaging into TO-CAN, butterfly, C-mount, and integrated modules. Packaging, burn-in, and reliability qualification are key value-add steps for telecom/datacom, automotive LiDAR, and medical applications, where customer certification cycles commonly run 12 to 24 months. This extends switching costs and tends to favor incumbent supplier positions.

Bottlenecks remain visible in indium phosphide substrate availability and in scaling qualified capacity for AI-driven optical interconnects and co-packaged optics, which pushes players toward vertical integration and regional capacity adds. In 2025, Lumentum announced a major expansion of its San Jose, California semiconductor facility to support ultra-high-power indium phosphide lasers. Separately, imec demonstrated monolithic fabrication of GaAs-based nano-ridge laser diodes on 300 mm silicon wafers in its CMOS pilot line, highlighting an alternate scaling route through silicon-compatible manufacturing. On the visible emitter and industrial side, ams OSRAM launched a higher-efficiency blue laser diode in 2025, and Nuvoton Technology Corporation Japan started mass production of a 420 nm indigo semiconductor laser in 2025, reflecting continued investment across epitaxy, device design, and manufacturing to diversify supply beyond traditional infrared telecom parts.

Competitive Landscape

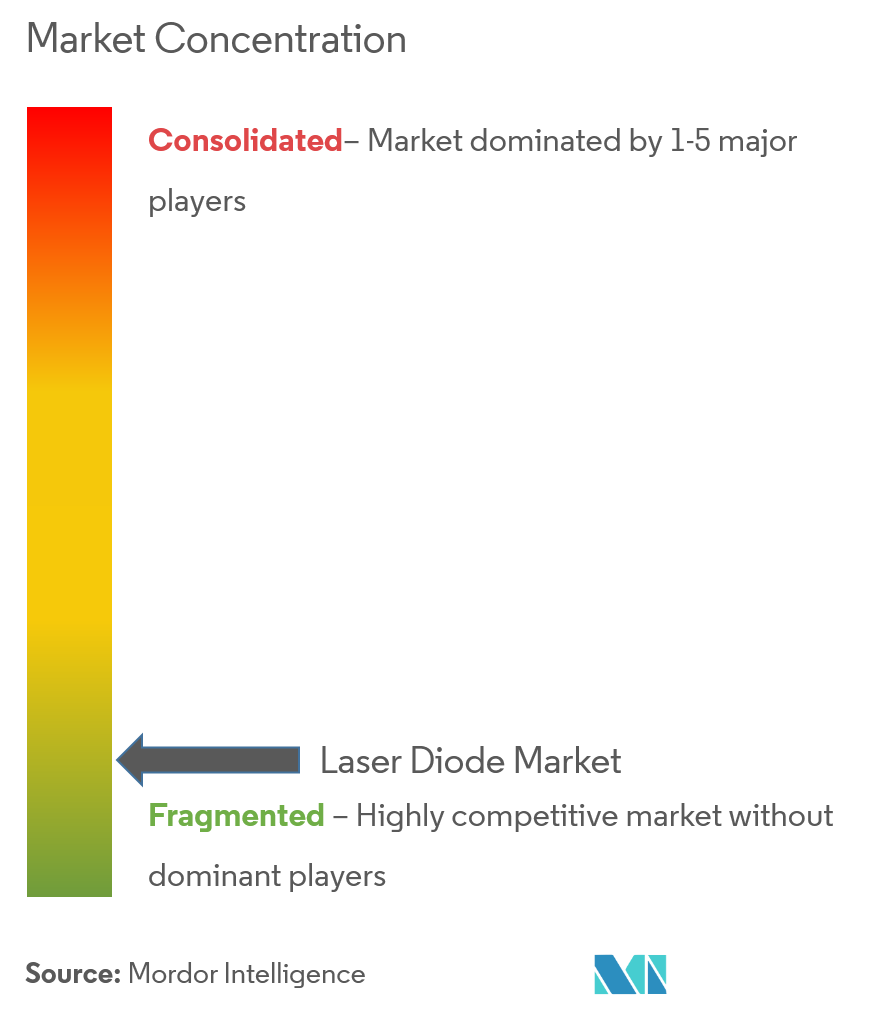

The top five suppliers, Coherent, Lumentum, TRUMPF, ams OSRAM, and IPG Photonics, held about 38% of 2025 revenue, indicating moderate fragmentation. Vertical integration dominates strategy as companies secure epitaxy to mitigate gallium-indium volatility, exemplified by nLIGHT’s USD 22 million reactor expansion in Washington State that cut wafer lead times to nine weeks.

Patent activity in microchannel cooling and beam combination widened differentiation. Coherent filed 14 US patents in 2024-2025 covering cooler designs that reduce junction temperature by 18 degrees Celsius, enabling continuous-wave outputs above 50 watts without external chillers.

Specialists exploit white-space niches: Thorlabs shipped 1,200 mid-infrared quantum-cascade modules for methane leak detection, while Excelitas leveraged module integration to shave five months from automotive customer time-to-market. ISO beam-quality and IEC safety certifications act as soft barriers, as testing adds nine to 12 months and USD 45,000 per product line. These dynamics keep competitive entry viable yet challenging, preserving healthy innovation cycles in the laser diode market.

Laser Diode Industry Leaders

Coherent Corp.

Lumentum Holdings Inc.

Nichia Corporation

TRUMPF SE + Co KG

OSRAM Opto Semiconductors GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Datacom and telecom upgrades continue to create an opportunity space for edge emitters, DFB/EML devices, and VCSEL-based short-reach optics as hyperscale operators target higher lane rates and tighter power budgets. A clear signal came from Lumentum at OFC 2026, where it demonstrated 400 Gbps-per-lane electro-absorption modulated laser (EML) technology, reinforcing demand for higher-speed indium phosphide-based sources feeding 800G and 1.6T class optical links already highlighted in the report scope. This increases the value of suppliers that can provide hermetic packaging, co-packaged optics-compatible footprints, and stable high-volume qualification alongside domestic manufacturing investments designed to meet local-content expectations.

Outside telecom, integration and compliance readiness open whitespace for module suppliers in automotive LiDAR and medical systems that must meet IEC 60825-1 Class 1 constraints and medical laser safety norms, while also reducing OEM assembly steps. The regulatory and standards ecosystem supports differentiation through measurement and qualification consistency, including IEC 60747-5-4:2022 (and its amendment) for semiconductor laser terminology, ratings, and measurement methods, alongside IEEE Photonics Society standards activity and industry standardization forums such as IPEC. On the technology side, substrate and epitaxy innovation remains a lever for cost and yield, illustrated by Sony Semiconductor Solutions Corporation filing a US patent in January 2026 related to an InxGa1-xAs substrate with low carrier concentration aimed at improving light emission efficiency, which aligns with ongoing efforts to improve performance in the material systems used across infrared laser diode classes.

Recent Industry Developments

- March 2026: Lumentum announced plans for a 240,000-square-foot manufacturing facility in Greensboro, North Carolina, to produce indium phosphide-based optical devices for AI data centers. The announcement supports domestic capacity and supply assurance for high-volume transceiver components as hyperscalers expand 800G and 1.6T deployments. It also complements broader efforts to localize compound-semiconductor manufacturing in response to procurement and compliance requirements.

- March 2026: Coherent announced a major upgrade to its pump-laser portfolio aimed at scaling deployment in data-center interconnects. The update signals a shift toward higher-volume manufacturing and broader market reach.

- June 2025: Excelitas introduced a compact 905 nm LiDAR laser module integrating the driver and thermal management within a 12 cubic-centimeter housing. The design reduces integration steps for automotive and industrial sensing OEMs while addressing packaging and thermal constraints. Integrated modules like this support faster customer qualification cycles and strengthen supplier positioning in LiDAR programs moving toward higher levels of integration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the laser diode market is the global revenue from newly manufactured semiconductor junction laser diodes sold as die, packaged chips, or compact sub-modules, covering UV to near-infrared wavelengths, and sold into electronics, industrial, and other end uses.

Scope exclusions: We exclude gas, solid-state, fiber, and organic lasers, and we also exclude refurbished or salvaged laser diodes.

Segmentation Overview

- By Type

- Edge-Emitting Laser Diodes

- VCSEL

- Quantum Cascade Lasers

- DFB and DBR

- Fabry-Perot Laser Diodes

- By Wavelength

- Infrared (700-1600 nm)

- Red (630-700 nm)

- Blue (400-500 nm)

- Green (500-570 nm)

- Ultraviolet (Less than 400 nm)

- By Output Power

- Low Power (Less than 1 W)

- Mid Power (1-10 W)

- High Power (More than 10 W)

- By Operating Mode

- Continuous-Wave (CW)

- Pulsed

- By Packaging Configuration

- TO-CAN

- C-Mount

- HHL and Butterfly

- Module/Sub-System

- By End-User Application

- Telecommunications and Datacom

- Industrial Processing and Manufacturing

- Healthcare and Medical

- Automotive

- Consumer Electronics and Display

- Defense and Security

- Research and Academia

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping how laser diodes move from wafer-level production through packaging and then into end equipment, so the market boundary stays consistent. We reference public sources such as national trade statistics portals, customs import and export datasets, World Bank and IMF macro indicators, and standards and safety references from bodies such as IEC and ISO, since these help anchor activity levels and pricing context.

On the demand side, we use technical papers and peer-reviewed journals to understand shifts like VCSEL adoption in sensing, higher power density for industrial uses, and wavelength choices for communications. Company filings, investor presentations, and credible press are also reviewed to identify capacity expansion, mix changes, and regional exposure. A paid subscription for company financials and a patent database are used selectively to cross-check innovation cadence and portfolio focus. The desk source list is not exhaustive, and many other public references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions that usually shift the total the most, including average selling price progression, mix across diode types, and where packaged devices get counted versus sub-modules. We spoke with a balanced set of stakeholders across manufacturing, packaging, distribution, and procurement roles, and we ensured coverage reflected major producing and consuming regions, so the final totals were not driven by a single geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 22% | APAC: 44% |

| Mid tier: 47% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 22% | Managers: 40% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing starts with a top-down approach where production and trade signals are reconstructed into an addressable revenue pool for newly manufactured laser diodes, and then filtered by the scope rules on what is in and out. We then corroborate the totals using selective bottom-up approximations, such as sampling typical diode pricing by power class and wavelength, and matching it with estimated unit demand tied to major use cases.

Inputs that are tracked in the model include diode shipment momentum into optical communications and data centers, adoption of VCSEL-based sensing in consumer and industrial devices, the mix shift between edge-emitting lasers and VCSEL designs, packaging intensity (die versus packaged chip versus sub-module), and regional capacity additions in epitaxy and packaging. Where bottom-up checks have gaps, missing parts are bridged using conservative ranges from interviews, and then normalized so totals remain consistent with the top-down demand pool.

For forecasting, scenario analysis is used so the forward view can reflect different outcomes for electronics cycles, data center buildouts, and automotive sensing uptake, followed by an annual smoothing step to avoid unrealistic jumps in price or volume. Assumptions on mix, pricing, and adoption are reviewed with primary inputs so the forecast remains explainable and traceable to a small set of drivers.

Data Validation & Update Cycle

Validation is done by triangulating the sized totals against independent signals, such as directionally matching the implied unit demand with end-market shipment trends and checking whether implied pricing stays within realistic bands shared by respondents. Outliers are flagged, and the model is re-run after reviewing whether the issue comes from currency timing, a mix assumption, or an overstatement tied to a single end use.

Before sign-off, the work goes through multi-step analyst reviews, and follow-up outreach is triggered when a key assumption moves outside the interview-backed range. Reports are refreshed annually, and interim updates are made when material events occur, such as capacity announcements, major demand shocks, or meaningful pricing resets. Right before delivery, a fresh pass is completed so the numbers reflect the latest available information.

Mordor Intelligence's Laser Diode Market Estimate Compared With Other Published Estimates

Published market sizes for laser diodes can look far apart even when they are describing a similar space, because the boundaries and counting rules are not always the same. Differences usually come from what gets included as a laser diode product, how packaged devices versus sub-modules are treated, and whether the sizing is anchored to observable demand signals or mainly to long-range growth expectations.

By tracking packaging form factors and price-per-unit ranges, and then applying consistent inclusion rules, Mordor Intelligence keeps the 2025 market value focused on newly manufactured semiconductor junction laser diodes, instead of blending in adjacent laser types or refurbished supply. Gaps also show up when a study uses a more aggressive adoption curve for sensing or data center optics, uses different currency conversion timing, or does not refresh the key assumptions after major capacity and pricing changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.58 B (2025) | |

| Global Consultancy A | USD 11.88 B (2025) | This estimate likely uses a broader product boundary that can pull in adjacent semiconductor laser categories or more of the module value, which increases the counted revenue beyond diode-only sales. |

| Industry Publisher B | USD 14.10 B (2025) | The gap can be explained by higher assumed ASP levels and faster adoption in large end uses, plus a wider interpretation of what is counted as a laser diode offering across packaged solutions. |

The spread in the table is mainly explained by scope and counting choices, followed by how pricing and adoption are projected for core applications. Our approach stays repeatable because the sizing is tied back to clear product inclusions, realistic price bands, and demand indicators that can be checked and updated as the market moves.

Key Questions Answered in the Report

What is the projected size of the global laser diode landscape by 2031?

It is forecast to reach USD 14.48 billion by 2031, rising from USD 9.37 billion in 2026 at a 9.09% CAGR.

Which geographic region currently leads revenue in laser diodes?

Asia-Pacific generated 53.61% of worldwide revenue in 2025, helped by Japan’s integrated fabs and China’s USD 47 billion subsidy program.

Why are VCSELs gaining traction over traditional edge-emitting designs?

VCSEL arrays support wafer-level testing, lower assembly cost, and meet 3D sensing needs, underpinning a 10.98% CAGR forecast through 2031.

How fast is automotive LiDAR demand for laser diodes expected to grow?

Consumption tied to solid-state LiDAR is projected to expand at a 13.12% CAGR as Level 3 autonomy regulations phase in by 2028.

What raw-material risks do laser diode manufacturers face?

Gallium and indium prices remain volatile due to concentrated supply in China, increasing input-cost uncertainty despite recycling gains.

Which packaging format is becoming more popular with laser diode buyers?

Integrated module packages that embed drivers and cooling are set to grow at 10.23%, gradually taking share from discrete TO-CAN housings.

Page last updated on: