True Wireless Stereo (TWS) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

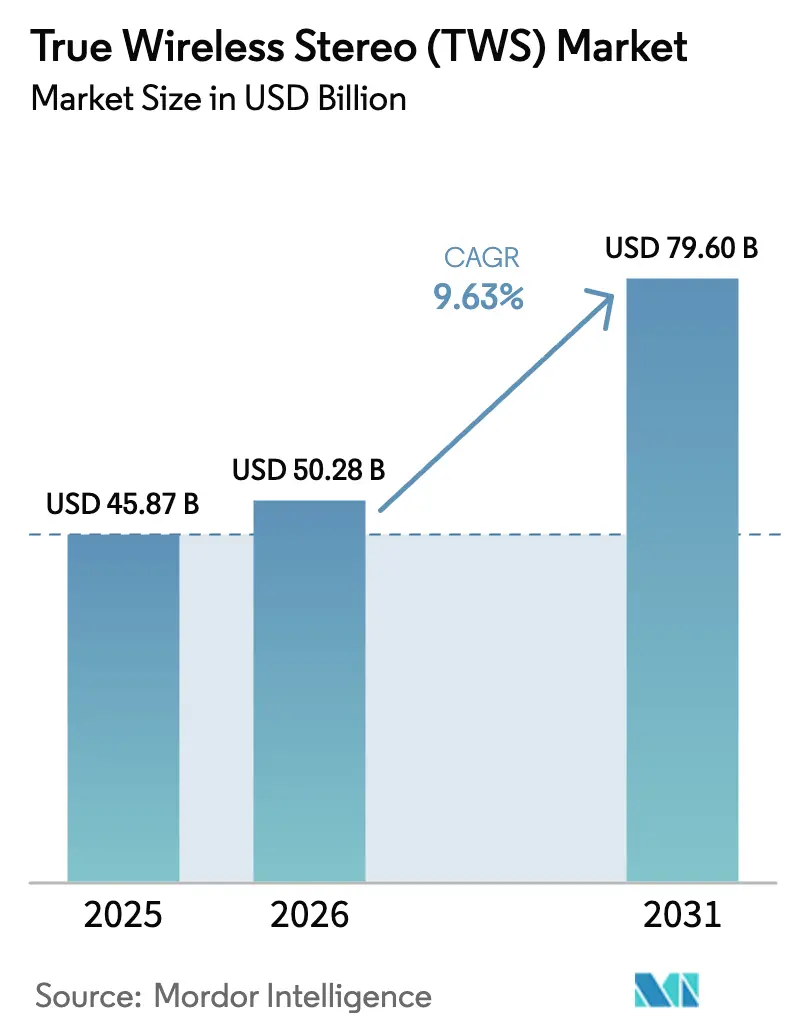

| Market Size (2026) | USD 50.28 Billion |

| Market Size (2031) | USD 79.6 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

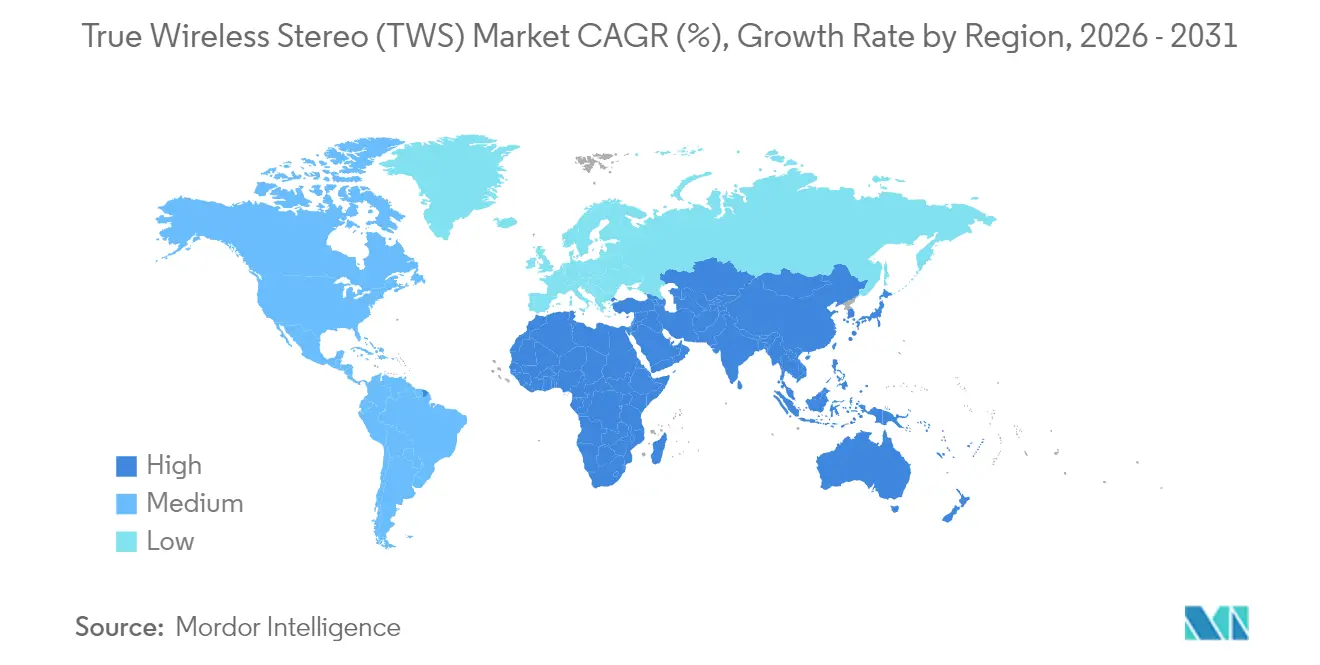

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

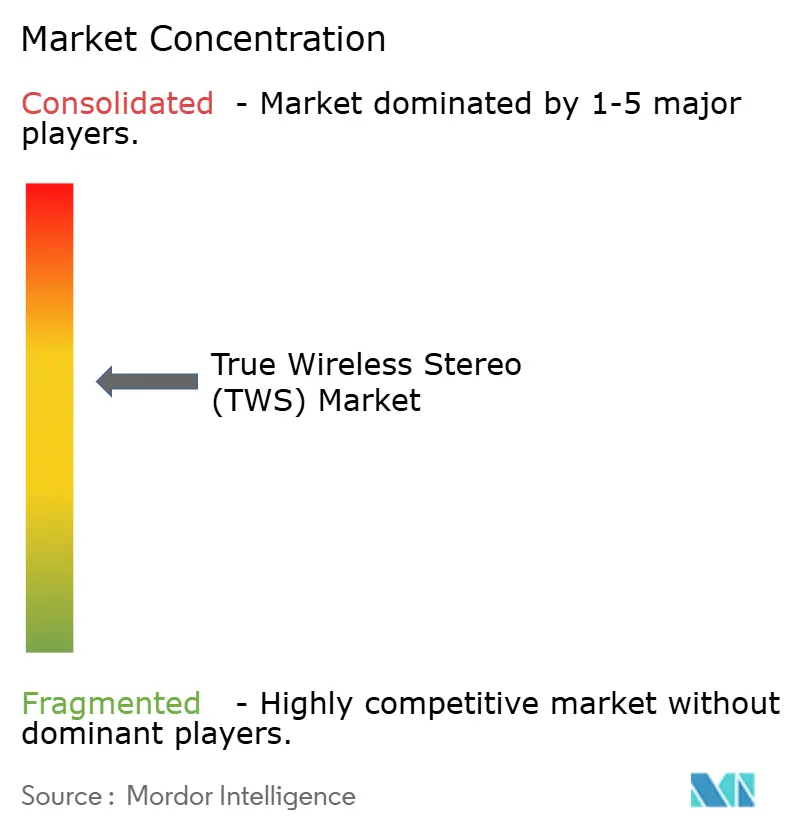

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

True Wireless Stereo (TWS) Market Analysis by Mordor Intelligence

True wireless stereo market size in 2026 is estimated at USD 50.28 billion, growing from 2025 value of USD 45.87 billion with 2031 projections showing USD 79.6 billion, growing at 9.63% CAGR over 2026-2031. Growth stems from technology convergence, broader price-tier coverage, and a shift toward experience-centric differentiation. Momentum is visible in unit volumes: shipments of 78 million pairs in Q1 2025 reflected 18% year-on-year expansion, confirming renewed demand for seamless, cable-free audio. Health-tracking biosensors, spatial audio, and Bluetooth LE Audio adoption are transforming earbuds from single-purpose accessories into multi-functional wearables. Competitive pressure is rising as Chinese brands scale internationally while premium incumbents add wellness and AI features to defend their share. Regionally, the Asia Pacific true wireless stereo market benefits from unmatched manufacturing depth, whereas the Middle East and Africa offer the fastest growth runway as smartphone penetration accelerates.

Key Report Takeaways

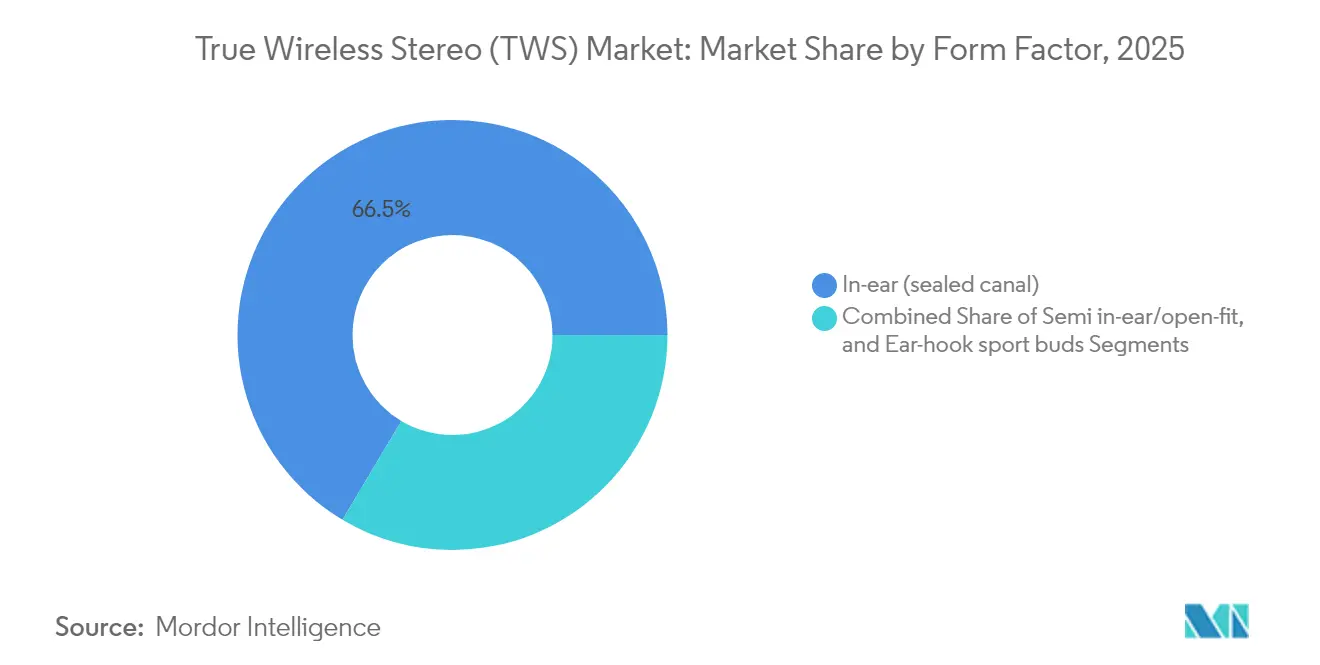

- By form factor, in-ear (sealed canal) designs led with 66.45% of the true wireless stereo market share in 2025; ear-hook sport buds are expected to expand at a 10.62% CAGR through 2031.

- By technology feature set, active noise-cancellation accounted for 54.85% of the true wireless stereo market size in 2025, while health-tracking biosensors are projected to grow at an 11.12% CAGR.

- By application, music and entertainment captured 42.75% revenue share in 2025; gaming and e-sports should post a 12.55% CAGR to 2031.

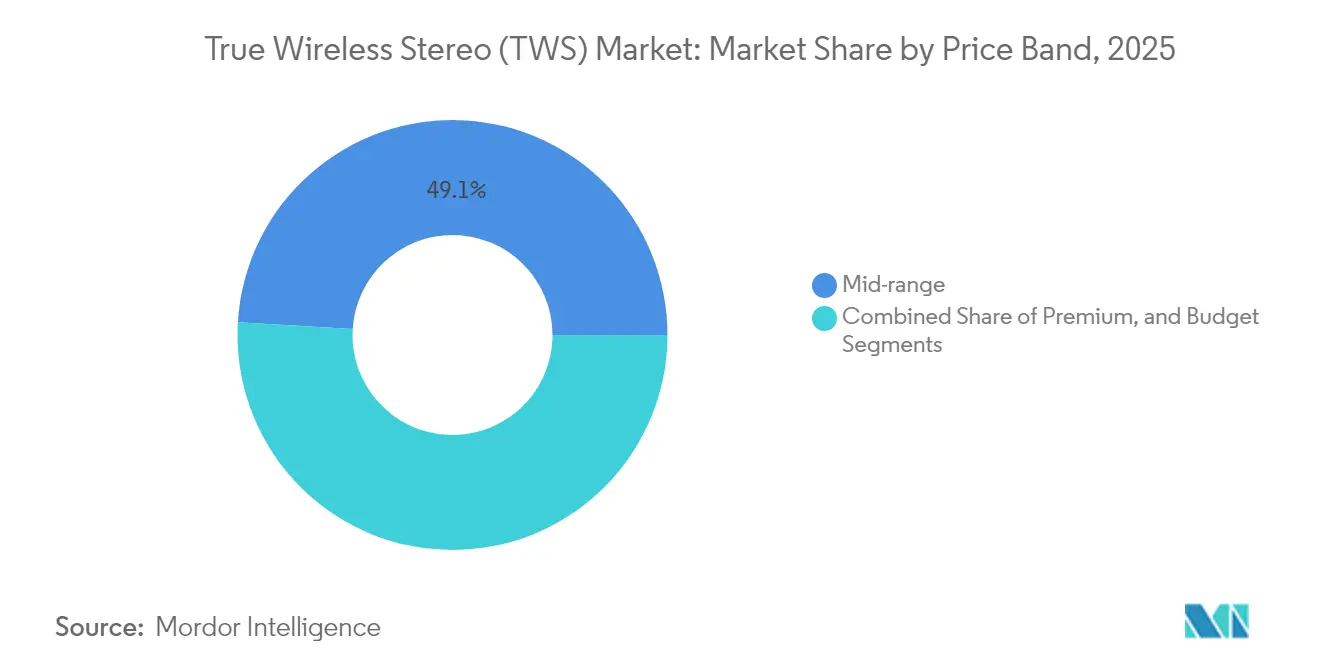

- By price band, the USD 75–150 mid-range commanded 49.05% of the true wireless stereo market size in 2025, whereas the premium tier above USD 150 is set to rise at 10.74% CAGR.

- By distribution channel, online marketplaces held 50.95% share in 2025; direct-to-consumer platforms are forecast to advance at a 12.21% CAGR.

- By geography, Asia Pacific dominated with 30.70% market share in 2025; Middle East and Africa is anticipated to register an 11.03% CAGR through 2031.

- Apple, Xiaomi and Samsung collectively represented 34.5% of global shipments in 2025, underlining a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global True Wireless Stereo (TWS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for wireless convenience | +3.40% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Phasing-out of 3.5 mm audio jacks in smartphones | +2.40% | Global, with higher adoption in premium smartphone markets | Medium term (2-4 years) |

| Rapid adoption of Bluetooth LE Audio and LC3 codec | +2.00% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expanding affordability via low-cost Asian ODMs | +1.50% | Asia Pacific, Latin America, Middle East and Africa | Short term (≤ 2 years) |

| Emergence of spatial-audio ecosystems driving upgrades | +1.00% | North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Integration of biosensors enabling wellness use-cases | +1.50% | Global, with higher adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Wireless Convenience

Cable-free listening quickly moved from novelty to baseline expectation, driving repeat upgrades across demographics. Shipment growth of 18% in Q1 2025 highlighted renewed appetite for hassle-free, multi-device audio. Design strategies now emphasize all-day comfort, single-tap switching, and sweat protection that suit workouts, commuting, and remote meetings alike. Brands strengthen lifestyle positioning by offering fashion-forward colors and compact charging cases that extend playback well past an eight-hour workday. Ecosystem integration further locks in loyalty as users appreciate seamless pairing with laptops, tablets, and watches.

Phasing-Out of 3.5 mm Audio Jacks in Smartphones

Removal of analog ports has structurally tilted demand toward the true wireless stereo market. Premium handset makers triggered the trend; mass-market vendors soon followed once economies of scale lowered BOM costs for entry-level earbuds. Consumers increasingly regard wireless audio as the default, not a premium alternative, which expands the total addressable base and supports higher accessory attach rates per smartphone sold. Device OEMs benefit from thinner chassis and larger batteries after eliminating the jack, reinforcing the mutually beneficial cycle between phones and earbuds.

Rapid Adoption of Bluetooth LE Audio and LC3 Codec

Bluetooth LE Audio introduces lower power transmission, multi-stream support and improved latency. The LC3 codec pairs high fidelity with reduced bit-rate overhead, enhancing battery runtime without sacrificing sound quality. Semiconductor suppliers have responded with integrated SoCs that support 48 kHz, 16-bit streams at sub-200 kbps while extending case-plus-earbud endurance beyond 35 hours. These advances open new use cases such as lossless Wi-Fi hand-over, adaptive spatial audio and real-time translation, helping premium models justify higher ASPs.

Expanding Affordability via Low-Cost Asian ODMs

Original design manufacturers in China, Vietnam and India produce reference designs that bundle ANC, wireless charging and companion apps at sub-USD 40 wholesale. Their speed compresses feature trickle-down cycles to roughly 12 months, bringing advanced tech to mid-range buyers far sooner than before. Budget-friendly releases stimulate first-time adoption in cost-sensitive markets, feeding volume growth that stabilizes component demand for the entire supply chain. Established brands counter with affordable sub-lines or strategic collaborations that retain brand cachet while matching entry-level price brackets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited battery life and thermal management challenges | -1.00% | Global, with higher impact in regions with extreme climates | Medium term (2-4 years) |

| Semiconductor supply-chain price volatility | -0.80% | Global, with higher impact on budget and mid-range segments | Short term (≤ 2 years) |

| Stricter global e-waste and recycling compliance costs | -0.70% | Europe, North America, developed APAC markets | Long term (≥ 4 years) |

| User health concerns from prolonged in-ear usage | -0.50% | Global, with higher impact in health-conscious markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Battery Life and Thermal Management Challenges

Miniaturized housings restrict battery capacity to 20–50 mAh per bud, creating tight energy budgets for ANC, high-resolution codecs and biosensing. Elevated ambience temperatures amplify thermal strain, forcing power throttling that can degrade audio experience. Component suppliers have developed buck-boost PMICs with efficiency above 85% and charging topologies that cut heat rise by 70%, yet sustained high-bit-rate playback beyond eight hours remains difficult. These physical constraints will temper proliferation until solid-state batteries or ultra-low-leakage semiconductors mature.

Semiconductor Supply-Chain Price Volatility

Audio SoC demand competes with smartphone, IoT, and automotive requirements, causing allocation bottlenecks and periodic price spikes. Smaller brands have limited leverage and often resort to design mid-cycle changes when preferred chips become unavailable. Integrated power-management ICs that consolidate charging, discharging, and protection functions lower part counts, and partly shield BOM exposure, but true strategic resilience requires multi-source qualification and deeper supplier partnerships. Volatility, therefore, introduces forecasting uncertainty and working capital strain, especially in the budget tier.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Sport Designs Driving Outdoor Adoption

In-ear models held 66.45% true wireless stereo market share in 2025 thanks to compact cases and effective passive isolation. Ear-hook sport buds, although niche, are forecast to post a 10.62% CAGR because gymgoers value secure fit and sweat resistance. The semi-open-fit category gained momentum as workers sought all-day comfort and situational awareness during remote meetings. Semi-designs now integrate 14 mm-plus dynamic drivers and adaptive ANC that balance ambiance with clarity. Fashion-oriented open-ear wearables extend battery life past 30 hours through larger surface batteries housed in hoop-like structures, broadening appeal to style-conscious users. Hardware diversity demonstrates manufacturers’ intent to serve discrete lifestyles rather than chase a one-size-fits-all shell.

Product engineers are refining nozzle angles, interchangeable tips, and pressure-relief vents to combat ear fatigue, while medical-grade silicones improve hygiene for prolonged wear. Sport models increasingly leverage ear-hook bio-monitors that capture heart-rate variability with greater accuracy than wrist devices, merging wellness with outdoor audio. Open-fit lines target professional creators who prefer minimal occlusion when editing video. These differentiated designs widen the true wireless stereo market’s user base and support parallel device ownership within households.

By Technology Feature Set: Biosensors Redefining Value Proposition

Active noise-cancellation dominated 54.85% of the 2025 true wireless stereo market size, yet biosensor-equipped models are projected to expand at 11.12% CAGR through 2031. Combining photoplethysmography, skin temperature, and EEG sensors within earbuds permits continuous health data capture close to the carotid artery, improving signal fidelity versus wristbands. Voice-based algorithms further detect respiratory irregularities, enabling early intervention services. Spatial audio capabilities serve entertainment and professional mixing, while low-latency gaming modes ensure synchronization under 50 ms. Manufacturers position multi-function bundles as personal wellness hubs rather than audio peripherals, thereby elevating perceived value and supporting ASP uplift.

Technology roadmaps illustrate integration momentum: premium SoCs now encode concurrent ANC, head-tracking, and sensor fusion pipelines under 6 mA average current. Mid-range chipsets add transparency modes plus adaptive EQ derived from otoacoustic feedback. Budget tiers still rely on electronic noise cancellation only, yet ODM reference boards forecast biosensor inclusion within two generations. This convergence nurtures ecosystem lock-in as mobile apps collate fitness, hearing and travel metrics into unified dashboards.

By Application: Gaming Ecosystem Drives Feature Innovation

Music and entertainment led usage with 42.75% share in 2025, but gaming and e-sports should outpace at a 12.55% CAGR. Competitive players demand precise spatial cues for footsteps and projectiles, prompting brands to develop custom drivers and 5 GHz Wi-Fi relays that cut latency to single-digit milliseconds. Sports and fitness usage aligns with ear-hook and open-fit expansion, emphasizing drop-proof housings and IP68 ratings. Workplace collaboration is a structurally growing niche as hybrid work normalizes; enterprise-oriented earbuds embed multi-device pairing, beam-forming mics and certified security protocols.

Hearing enhancement and ambient amplification sit at the intersection of consumer and medical segments. Firmware that meets basic regulatory thresholds can act as an over-the-counter hearing aid, unlocking older demographics. Content providers collaborate with audio brands to optimize codecs for podcasts and audiobooks, fostering differentiated subscriptions. Application-specific releases diversify revenue streams and mitigate seasonal demand swings.

By Price Band: Premium Features Trickle Down

Mid-range models priced USD 75-150 captured 49.05% of the 2025 true wireless stereo market size, reflecting optimal balance between specification depth and affordability. Premium devices above USD 150 are forecast to advance 10.74% CAGR as consumers reward lossless streaming, spatial audio and biosensing. Developers justify price premiums by bundling personalized sound calibration and on-device AI that automatically adapts EQ to content genre. Budget units below USD 75 remain vital for volume growth in emerging economies; ODM platforms now integrate Bluetooth 5.4 and basic ANC at this level.

Feature cascades are accelerating: firmware promoting dual-device connectivity appeared in flagship models in 2023 and migrated to mid-range by 2025. Wireless charging and high-density GaN cases debut in top tiers before diffusing downward. Premiumization elevates brand differentiation yet raises expectations for after-sales service, battery replacement and sustainable packaging. Consequently, revenue diversification includes subscription-based spatial-audio libraries and health analytics that prolong customer lifetime value beyond hardware margins.

By Distribution Channel: Direct-to-Consumer Reshapes Retail Strategy

Online marketplaces supplied 50.95% of 2025 shipments thanks to breadth, promotions and review ecosystems. Direct-to-consumer storefronts, growing at 12.21% CAGR, empower brands with granular customer data, controlled merchandising and higher gross margins. Embedded financing, loyalty points and bundle offers improve conversion for premium SKUs. Brick-and-mortar electronics stores still matter for experiential demos, crucial for seal-quality validation and fit testing. Telecom carrier outlets bundle earbuds with handset upgrades, locking users into contract cycles and ensuring frequent refresh.

Omnichannel orchestration is emerging: customers research online, audition offline and finalize purchases via brand app to secure warranty extensions. Warehousing investments near urban centers shorten delivery times for D2C fulfilment, while pop-up kiosks in high-footfall malls showcase limited-edition colors. These tactics synchronize inventory, pricing and promotion across lines, curbing arbitrage and gray-market leakage. Retail evolution thus supports sustainable growth for the true wireless stereo market through richer customer engagement.

Geography Analysis

Asia Pacific retained a 30.70% share of the 2025 true wireless stereo market, aided by vertically integrated supply chains and rising discretionary income. China combined vast domestic demand with agile ODM clusters that slashed lead times for feature updates. India recorded 4% shipment growth in Q1 2025 as consumers upgraded beyond entry-level units, and government production-linked incentives encouraged local assembly that trims import duties and retail prices. Southeast Asian economies such as Indonesia and Vietnam witnessed double-digit unit expansion as e-commerce platforms improved rural reach.

North America and Europe formed a mature, high-value corridor where average selling prices exceed USD 120. Consumers favored models that integrate seamlessly with smartphones, tablets and smartwatches, supporting Apple’s leadership through cohesive ecosystem services. Environmental regulations in the European Union pushed manufacturers to adopt modular designs and recycled plastics, creating a second-hand refurbishment channel. Spatial audio adoption has been strongest in these markets, influencing global content mastering standards.

Middle East and Africa, though currently smaller in absolute terms, should advance at 11.03% CAGR to 2031. Smartphone ownership growth, improved 4G/5G coverage and rising middle-class income underpin demand. Price sensitivity encourages competition among mid-range brands offering durable cases and extended battery life suitable for intermittent power supply. Cross-border e-commerce eases access to global releases, while regional lifestyle trends such as outdoor desert sports propel ear-hook sales. Governments investing in digital economy initiatives further stimulate adoption, indicating sizeable headroom for the true wireless stereo market.

Competitive Landscape

The market exhibits moderate concentration with ecosystem-centric giants at the top and a long tail of challenger brands. Apple held 23% global unit share in Q1 2025, leveraging proprietary H-class chips and a services bundle that includes spatial audio libraries. Xiaomi’s 11.5% share reflected aggressive international rollout and rapid cadence of feature-rich sub-USD 100 models. Samsung defended presence via Galaxy ecosystem unification but ceded rank to Xiaomi due to slower refreshes. Regional challenger Boult posted 46% year-on-year shipment growth in India by tailoring spec-to-price balance for online flash sales.

Strategic collaborations enhance credibility: Noise partnered with Bose for tuning algorithms aimed at premium seekers, while QCY adopted MEMS micro-speakers to cut weight and improve transient response. Semiconductor innovation is a key battleground; Thinkplus Semiconductor shipped 700 million audio SoCs with integrated power-management, granting OEMs single-vendor procurement and simplified PCB layouts. Supply chain control over battery, driver and codec IP yields cost advantages and faster launches, helping entrants narrow the performance gap with incumbents.

White-space opportunities include hearing enhancement, professional-grade conference earbuds and wellness-centric biosensor models targeting insurers and healthcare providers. Companies such as Analog Devices and IDUN Technologies are piloting EEG-enabled earbuds for cognitive monitoring, indicating potential convergence with medical-device segments. Meanwhile, solid-state tweeter breakthroughs from xMEMS Labs may reduce bill-of-materials by 25% for premium drivers, intensifying acoustic differentiation. Competitive heat is thus spreading across hardware, software and service layers, ensuring dynamic evolution of the true wireless stereo market through the decade.

True Wireless Stereo (TWS) Industry Leaders

Apple Inc

Sony Corporation

Bose Corporation

Sennheiser Electronic SE & Co. KG

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Xiaomi launched Buds Pro 5 Wi-Fi, the first earbuds to stream 24-bit Hi-Res Audio over Wi-Fi using Qualcomm’s S7 Pro chip.

- May 2025: Boult recorded 46% year-on-year shipment growth in Q1 2025, reinforcing momentum among regional challengers.

- March 2025: QCY partnered with USound to introduce MEMS-driver earbuds scheduled for release later in 2025.

- March 2025: xMEMS Labs unveiled the Lassen solid-state tweeter, targeting mass production by September 2025 with 25% integration cost savings.

Global True Wireless Stereo (TWS) Market Report Scope

The true wireless stereo (TWS) market comprises wireless earbuds that deliver stereo sound without any cables connecting the earpieces or to the audio source. Driven by Bluetooth technology, TWS devices offer portability, convenience, and advanced features like active noise cancellation, touch controls, and voice assistants.

The study tracks the revenue generated from the sale of true wireless stereo (TWS) products by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The true wireless stereo (TWS) market is segmented by product type (in-ear, over-ear, and neckband), by technology (active noise cancellation (ANC), and non-anc), by application (music and entertainment, sports and fitness, gaming, and professional/workplace), by brand positioning (high end/prestige brands, value brands and niche brands) and by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| In-ear (sealed canal) |

| Semi in-ear/open-fit |

| Ear-hook sport buds |

| Active Noise Cancellation (ANC) |

| Non-ANC/ENC |

| Spatial-audio enabled |

| Health-tracking biosensors |

| Low-latency gaming mode |

| Music and Entertainment |

| Sports and Fitness |

| Gaming and e-sports |

| Professional/Workplace collaboration |

| Hearing assistance/ambient sound amplification |

| Premium ( Above USD150) |

| Mid-range ( USD75-USD150) |

| Budget (Less than USD75) |

| Online direct-to-consumer (brand.com) |

| Online marketplaces |

| Offline consumer-electronics stores |

| Telecom-carrier retail |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Form Factor | In-ear (sealed canal) | ||

| Semi in-ear/open-fit | |||

| Ear-hook sport buds | |||

| By Technology Feature Set | Active Noise Cancellation (ANC) | ||

| Non-ANC/ENC | |||

| Spatial-audio enabled | |||

| Health-tracking biosensors | |||

| Low-latency gaming mode | |||

| By Application | Music and Entertainment | ||

| Sports and Fitness | |||

| Gaming and e-sports | |||

| Professional/Workplace collaboration | |||

| Hearing assistance/ambient sound amplification | |||

| By Price Band | Premium ( Above USD150) | ||

| Mid-range ( USD75-USD150) | |||

| Budget (Less than USD75) | |||

| By Distribution Channel | Online direct-to-consumer (brand.com) | ||

| Online marketplaces | |||

| Offline consumer-electronics stores | |||

| Telecom-carrier retail | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Indonesia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the true wireless stereo market?

The true wireless stereo market size in 2026 is USD 50.28 billion and is projected to reach USD 79.6 billion by 2031.

Which form factor is growing the fastest?

Ear-hook sport buds are forecast to expand at a 10.62% CAGR between 2026 and 2031 as fitness and outdoor activities drive demand for secure, sweat-resistant designs.

How quickly are health-tracking biosensor earbuds expected to grow?

Earbuds with integrated biosensors should register an 11.12% CAGR through 2031, the highest among all feature categories.

Which region holds the largest share of the true wireless stereo market?

Asia Pacific accounted for 30.70% of global revenue in 2025, supported by deep manufacturing ecosystems and rising consumer spending.

Why are direct-to-consumer sales channels important for TWS brands?

D2C platforms are projected to grow at 12.21% CAGR because they offer higher margins, direct customer data and richer brand storytelling compared with third-party marketplaces.

What is the main technological hurdle limiting further feature expansion in earbuds?

Battery capacity and thermal management remain primary constraints; compact 20–50 mAh cells must power energy-intensive ANC, spatial audio and sensor suites without exceeding safe temperature thresholds.

Page last updated on: