Bluetooth Speaker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.93 Billion |

| Market Size (2031) | USD 53.79 Billion |

| Growth Rate (2026 - 2031) | 19.65% CAGR |

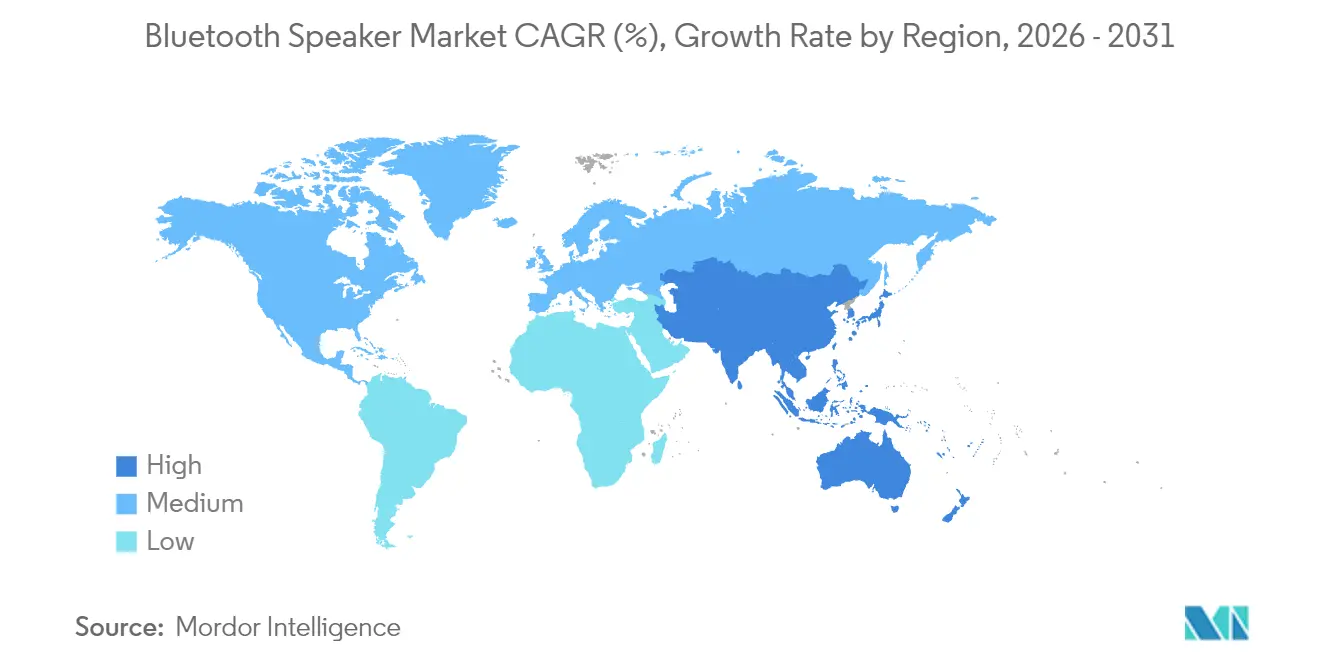

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

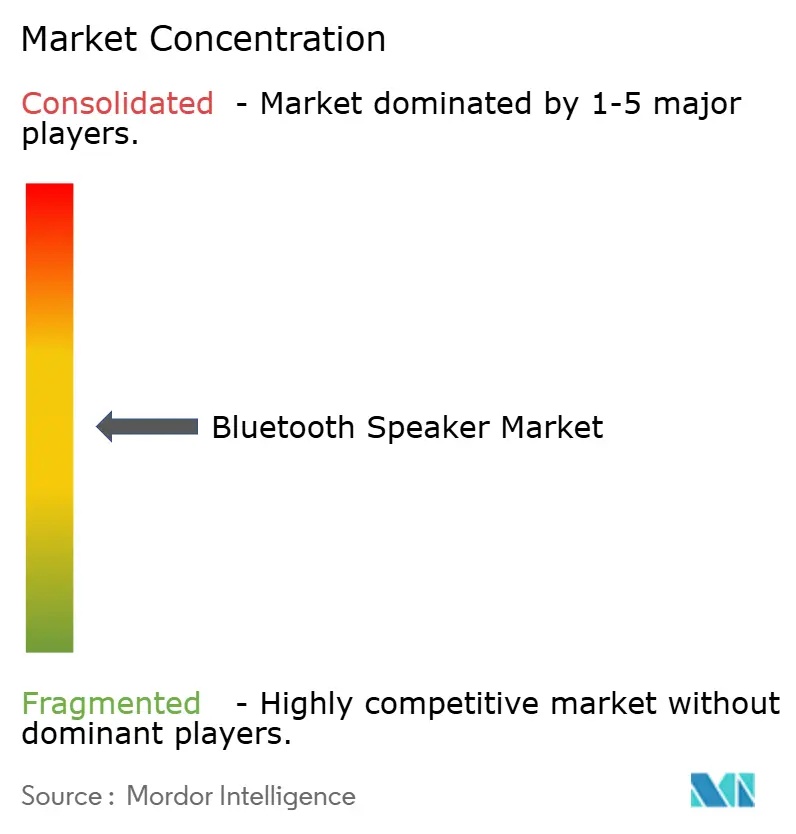

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bluetooth Speaker Market Analysis by Mordor Intelligence

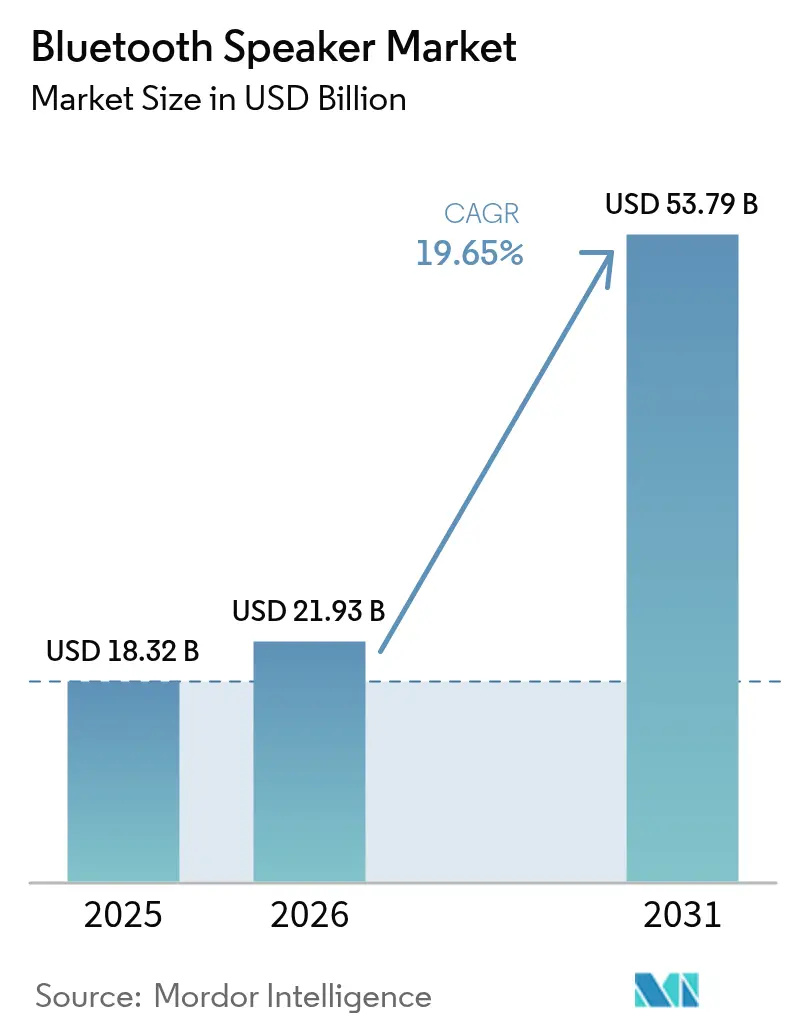

The Bluetooth Speaker Market size was valued at USD 18.32 billion in 2025 and estimated to grow from USD 21.93 billion in 2026 to reach USD 53.79 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031).

Robust demand stems from smart-home adoption, mass music-streaming uptake, battery cost declines, and the commercialization of Bluetooth LE Audio, each widening the addressable user base while shortening replacement cycles. Asia-Pacific leads current unit volumes thanks to competitive manufacturing clusters and a rapidly expanding middle class, while North America and Europe deliver premium average selling prices (ASPs) on the back of early smart-home penetration. Voice-assistant–enabled models are the fastest-growing category, yet Bluetooth-only speakers still represent the largest sub-segment because they deliver a simple, low-latency experience that does not rely on Wi-Fi. Competitive dynamics are shifting toward consolidation as established brands purchase luxury audio houses to secure patented technologies and brand cachet, thereby raising entry barriers for commodity players.

Key Report Takeaways

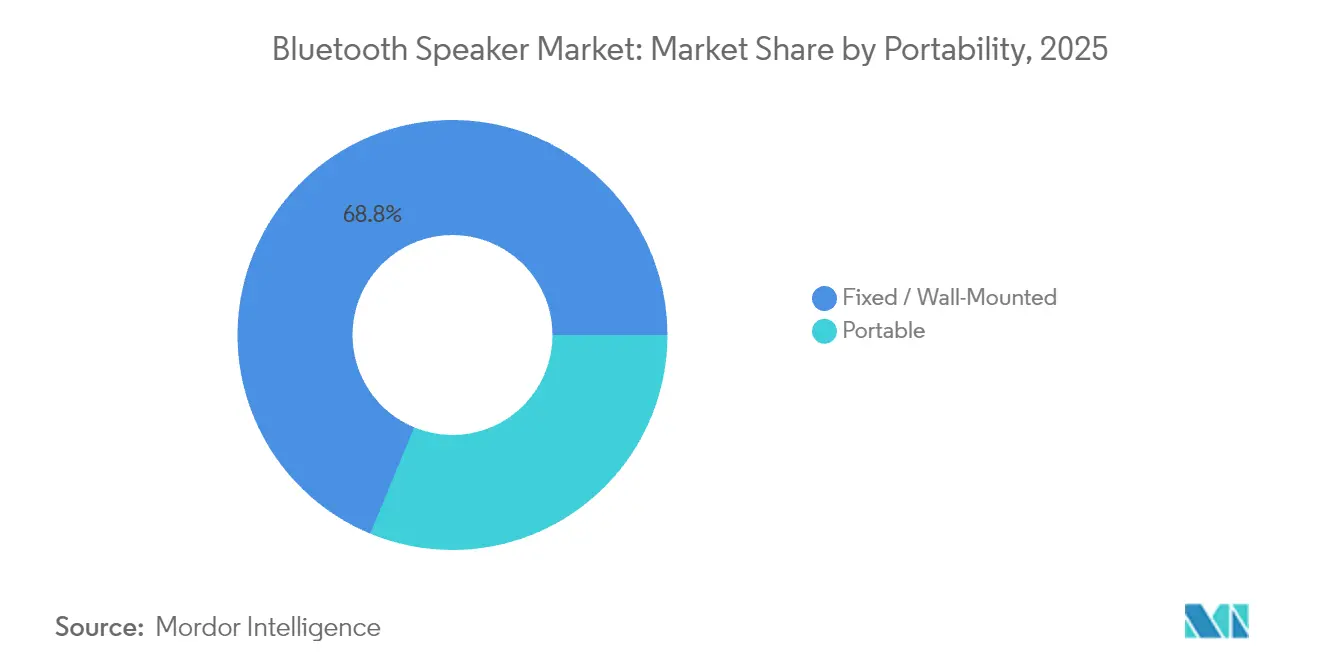

- By portability, fixed and wall-mounted units captured 68.75% of the Bluetooth speaker market share in 2025; portable speakers are advancing at a 21.95% CAGR through 2031.

- By application, residential solutions accounted for 60.55% of the market size in 2025 and are expanding at a 21.85% CAGR to 2031.

- By connectivity technology, Bluetooth-only designs held 57.10% share of the Bluetooth speaker market in 2025, while smart speakers with voice assistants posted the fastest 21.35% CAGR through 2031.

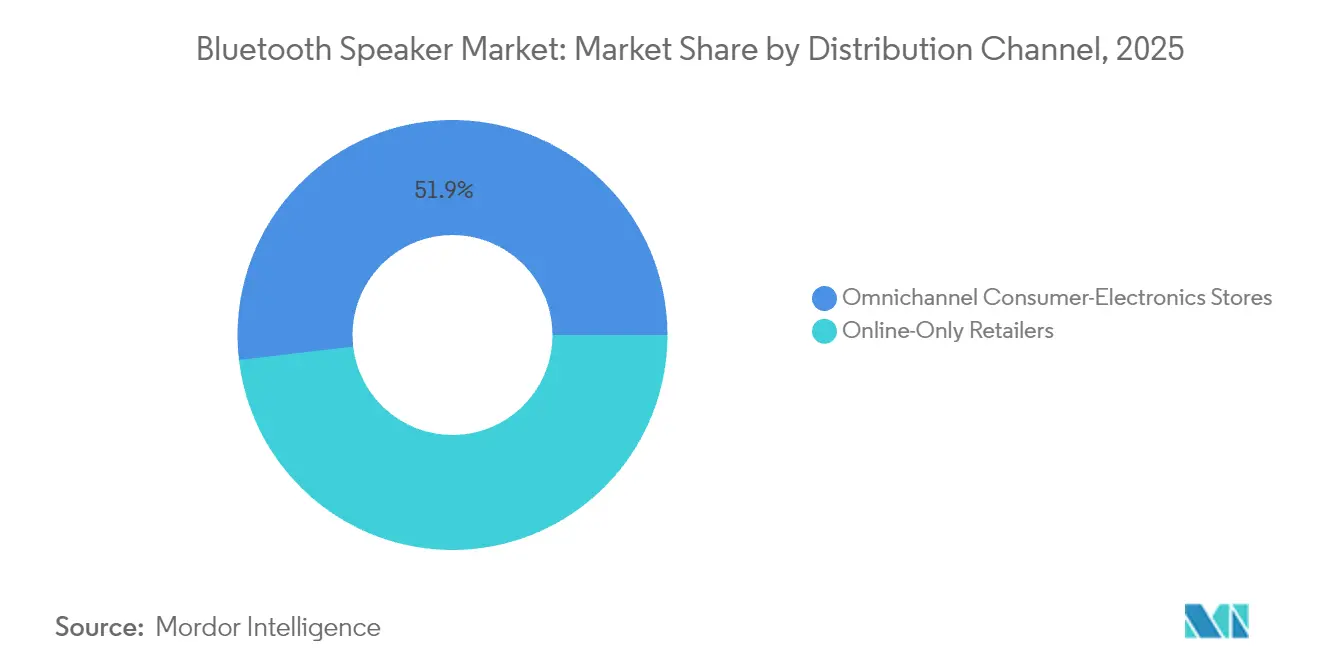

- By distribution channel, omnichannel consumer-electronics stores led with 51.85% revenue share in 2025; online-only retailers are growing at a 21.55% CAGR to the end of the decade.

- By price range, the USD 50-199 mid-range bracket commanded 44.55% share of the Bluetooth speaker market size in 2025, whereas economy models under USD 50 record the highest 21.25% CAGR.

- By geography, Asia-Pacific held 31.45% of market share in 2025 and is projected to post a 21.15% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bluetooth Speaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of smart-home ecosystems | +3.0% | North America, Europe, East Asia | Medium term (2-4 years) |

| Expansion of music-streaming subscriptions | +2.4% | Global, notably APAC and North America | Short term (≤ 2 years) |

| Falling ASPs of lithium-ion batteries | +1.6% | Global manufacturing hubs | Long term (≥ 4 years) |

| Outdoor recreation and van-life boom | +2.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Bluetooth LE Audio and Auracast roll-out | +2.8% | Developed markets worldwide | Medium term (2-4 years) |

| Growing demand for immersive classroom audio | +1.8% | Global, strongest in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Smart-Home Ecosystems

Seamless interoperability delivered by the Matter standard elevates Bluetooth speakers from stand-alone entertainment devices to multifunction smart-home hubs. Amazon’s 2025 Echo Show range illustrates the shift by embedding Fire TV services, auto-framing video communications, and full Matter, Zigbee, and Thread support in a single unit. Inter-brand compatibility lowers switching costs and drives premium replacement demand as households unify lighting, HVAC, and security control via voice-enabled speakers. Chinese ODM platforms such as LegatoXP shorten product development cycles, letting second-tier brands enter the smart-home space with smaller engineering budgets. Collectively, these forces accelerate household penetration, intensify brand competition, and enlarge the total volume opportunity for the Bluetooth speaker market.

Expansion of Music-Streaming Subscriptions

Music-streaming services surpassed 750 million paid subscribers in 2024, boosting demand for hardware capable of high-resolution and spatial-audio playback. As codecs such as LC3, LDAC, and aptX Lossless mature, users recognize audible quality deltas between legacy devices and next-generation speakers, prompting replacement purchases. Subscription platforms also encourage multi-device plans that natively support group listening, thereby favoring multi-room speakers over single-speaker setups. Streaming’s recurring revenue model fosters promotional bundling, where discounted speakers act as customer-acquisition vehicles, further stimulating hardware volumes throughout the forecast window.

Bluetooth LE Audio and Auracast Roll-out

Auracast broadcast audio transforms point-to-point Bluetooth into a one-to-many architecture, permitting a single smartphone, TV, or kiosk to serve multiple speakers or earbuds simultaneously[1]Jason Marcel, “Auracast Broadcast Audio Will Deliver Life-Changing Audio Experiences,” Bluetooth SIG, bluetooth.com. Samsung has shipped Auracast-ready Galaxy S24 handsets and Neo QLED televisions, while JBL, Marshall, and Sennheiser have pushed over-the-air updates to compatible speakers. Mass adoption reduces latency, boosts battery life, and unlocks public-venue use cases such as silent concerts, airport broadcasts, and assistive listening, all expanding the addressable market. Vendors that certify early gain first-mover reputational advantages and greater pricing power, elevating the overall Bluetooth speaker market growth trajectory.

Outdoor Recreation and Van-Life Boom

Post-pandemic lifestyle shifts toward camping, overlanding, and remote work accelerate demand for IP67-rated, shock-resistant speakers that deliver 20-plus hours of battery life. The global mobile-living economy exceeded SEK 200 billion in 2024 as consumers invested in high-durability accessories to accompany recreational vehicles[2]Dometic Group, “Annual and Sustainability Report 2023,” dometic.com . Brands capitalize by releasing rugged lines such as JBL PartyBox or Marshall Willen II, both commanding premium ASPs that cushion margin compression elsewhere. Social-media communities amplify experiential marketing, converting lifestyle imagery into purchase intent more effectively than traditional feature-centric advertising. As van-life culture spreads to Europe and Australia, demand for durable Bluetooth speakers enjoys a sustained multi-year lift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rampant counterfeiting and piracy | -1.2% | Emerging markets worldwide | Short term (≤ 2 years) |

| Margin erosion from price wars | -0.8% | Global, high in budget tier | Medium term (2-4 years) |

| Safety recalls tied to battery fires | -0.6% | North America and EU | Short term (≤ 2 years) |

| Stricter EU EMI limits for >30 W models | -0.4% | European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rampant Counterfeiting and Piracy

Unauthorized factories replicate popular designs, flooding e-commerce channels with low-quality imitations that undercut legitimate brands on price and erode consumer trust[3]Sabine Carrell, “Counterfeiting in the Electronics Industry: A Threat to Innovation and Safety,” Scribos, scribos.com. Counterfeits often omit essential safety circuits, raising the risk of battery fires and accelerating brand-protection expenditures for authentication technologies, blockchain labeling, and legal enforcement. While premium players deploy security holograms and supply-chain tracing, smaller vendors lack capital for large-scale monitoring, exposing them to revenue leaks and reputational damage.

Safety Recalls Tied to Battery Fires

High-energy-density lithium-ion cells can enter thermal runaway if poorly engineered, prompting proposed U.S. legislation that empowers regulators to mandate nationwide recalls for non-compliant products. Manufacturers now face extra certification steps—UL 2272, IEC 62133, and UN 38.3—that lengthen design cycles and raise compliance costs. Media coverage of isolated incidents undermines consumer confidence, particularly within the economy segment, where suppliers sometimes cut corners on cell quality. Heightened oversight benefits established brands with robust quality-assurance frameworks but could depress short-term unit sales until new standards stabilize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Fixed Installations Anchor Household Spend

Fixed and wall-mounted units accounted for 68.75% of the Bluetooth speaker market share in 2025, illustrating consumers' preference for power-fed systems that integrate seamlessly with televisions and multi-room platforms. This segment's steady revenue base gives manufacturers predictable upgrade cycles tied to smart-home renovation projects. Portable speakers, however, post a 21.95% CAGR, gaining from urban outdoor activities and remote-work mobility.

Fixed solutions emphasize audio fidelity, bass response, and voice-assistant control, traits that favor higher ASPs and bundling with streaming services. Portable designs optimize for rugged builds, lighter weight, and prolonged battery life, attracting first-time buyers in emerging markets. The two sub-segments, therefore, expand in parallel rather than cannibalize, yielding a diversified revenue structure for the overall Bluetooth speaker market.

By Application: Residential Spaces Dominate Growth

Residential settings delivered 60.55% of the Bluetooth speaker market size in 2025 and also hold the fastest 21.85% CAGR, underscoring the permanence of home-centric entertainment habits formed during pandemic lockdowns. Continuous smart-home upgrades keep the replacement cycle under four years, far shorter than the historical averages for legacy hi-fi components.

Commercial demand, restaurants, hotels, and small offices, remains important for premium installed systems but faces elongated procurement processes and tighter capital budgets. As voice assistants mature, residential speakers increasingly serve as hubs for lighting and HVAC control, blending functional utility with leisure use and cementing their primacy in long-term demand projections for the Bluetooth speaker market.

By Connectivity Technology: Simplicity vs. Intelligence

Bluetooth-only models retained 57.10% market share in 2025, offering dependable pairing without network complexity, especially in regions with limited broadband penetration. These units are favored for travel and budget use cases. Smart speakers possessing voice assistants, however, outpace all categories at a 21.35% CAGR as AI services propel command-and-control adoption for smart appliances.

Premium multi-room systems that layer Bluetooth, Wi-Fi, and proprietary mesh radios bridge both worlds by enabling lossless streaming indoors and basic Bluetooth when on the go. Auracast's introduction will further blur category lines, reinforcing the Bluetooth speaker market's transition from single-purpose gadgets to converged communication nodes.

By Distribution Channel: Showroom Experience vs. Digital Convenience

Omnichannel consumer-electronics retailers held 51.85% share of 2025 revenues, capitalizing on the human desire to audition sound quality before committing sizable discretionary spend. In-store demos, same-day pickup, and bundled warranties remain decisive factors for mid-range and premium tiers. Online-only retailers, escalating at 21.55% CAGR, capture price-sensitive and repeat buyers comfortable with brand reputations.

Brick-and-click models evolve as chains embed virtual try-before-you-buy tools and extend return windows, effectively hybridizing tactile assurance with digital convenience. This convergence mitigates channel conflict and sustains broad accessibility, supporting continued unit growth for the Bluetooth speaker market.

By Price Range: Mid-Range Sweet Spot Persists

Units priced between USD 50 and USD 199 delivered 44.55% of category revenue in 2025, balancing feature richness-IP67 sealing, extended playback, voice-assistant compatibility-and affordability. Lower component costs and vertical integration allow these SKUs to adopt codecs and battery chemistries previously restricted to premium lines.

Economy SKUs (< USD 50) record the fastest 21.25% CAGR as component commoditization lowers bill-of-materials outlays, unlocking first-time purchases in price-sensitive geographies. Conversely, luxury models (> USD 200) cater to audiophiles demanding wood cabinetry, high-excursion drivers, and manual EQ tuning. Such stratification broadens consumer reach without undermining margins, sustaining the Bluetooth speaker market's elastic pricing ladder.

Geography Analysis

Asia-Pacific commanded 31.45% of the Bluetooth speaker market share in 2025, generating a 21.15% CAGR to 2031 on the back of manufacturing scale, youth-oriented consumption, and rapid smartphone proliferation. Chinese OEMs leverage proximity to printed-circuit and battery supply chains to compress lead times and capitalize on domestic demand, which is forecast to surpass CNY 5.8 trillion for professional AV equipment by 2030. Government incentives for IoT ecosystems further accelerate the adoption of smart speakers, solidifying regional leadership in both volume and innovation.

North America trails in unit volumes yet achieves the highest ASPs. Early smart-home adoption and consumer willingness to pay for voice-assistant integration keep the region's gross margins above global averages. Outdoor recreation trends-from national park camping to city rooftop gatherings- stimulate demand for ruggedized models with multi-device pairing. Brand loyalty is strong, allowing category leaders such as Sonos to maintain premium shelf space even amid price-based competition.

Europe posts steady mid-teen growth, backed by stringent quality and cybersecurity standards that favor established brands. The updated Radio Equipment Directive effective August 2024 mandates secure boot and network safeguards, effectively filtering out low-end imports lacking compliance budgets. Consumers reward compliance with premium pricing, prompting local and international manufacturers to certify early and use CE markings as marketing differentiators, sustaining a value-heavy contribution to global Bluetooth speaker market revenues.

Competitive Landscape

Market fragmentation remains moderate, with the top five brands controlling roughly 42% of global revenues. Consolidation is accelerating as titans absorb niche luxury houses for intellectual property and brand prestige. Samsung’s Harman paid USD 350 million for Masimo’s Sound United portfolio, Bowers & Wilkins, Denon, and Marantz, gaining entry into audiophile circles while reinforcing its technology stack for smartphones and TVs.

Bose responded by acquiring McIntosh Group, adding heritage brands McIntosh Labs and Sonus Faber in a bid to penetrate the USD 2.8 billion high-end loudspeaker segment. These moves compress the supplier base, giving buyers fewer but more vertically integrated partners capable of end-to-end ecosystems, from automotive head units to living-room home theaters, thus raising switching costs for consumers.

Technological differentiation concentrates on proprietary DSP algorithms, beam-forming microphones, and machine-learning–based room calibration. Sonos alone holds over 4,300 active patents, using litigation to defend its platform. Meanwhile, newcomers pivot toward rugged outdoor niches, classroom reinforcement systems, and assistive-listening devices, segments inadequately served by mainstream portfolios. As Auracast reaches mass deployment, expect open-standard interoperability to erode some walled-garden advantages, intensifying innovation races in AI acoustics and materials science within the Bluetooth speaker market.

Bluetooth Speaker Industry Leaders

-

Sony Corporation

-

Koninklijke Philips NV

-

Samsung Electronics Co. Ltd. (Harman International Industries)

-

Bose Corporation

-

Beat Electonics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Amazon unveiled Echo Show 21 and an upgraded Echo Show 15, integrating Fire TV, deeper bass drivers, and multi-standard smart-home radios.

- January 2025: Samsung subsidiary Harman closed its USD 350 million purchase of Masimo’s Sound United audio division, adding Bowers & Wilkins, Denon, Marantz, and Polk Audio.

- January 2025: JBL introduced the PartyBox 520, Encore 2, and Encore Essential 2 with LE Audio support and AI Sound Boost, priced between USD 299 and USD 799.

- January 2025: Marshall Group sold a majority stake to HongShan Capital for EUR 1.1 billion while launching new amplifier and pedal lines.

Global Bluetooth Speaker Market Report Scope

Bluetooth technology is the global wireless standard for exchanging data over short distances and enabling the Internet of Things (IoT). The technology makes use of short-wavelength UHF radio waves in the ISM band from 2.4 to 2.485 GHz from both fixed and mobile devices and building personal area networks (PANs). A Bluetooth speaker is a sound device that needs no wires to connect.

The Bluetooth Speaker market is segmented by type (portable and fixed), application (residential and commercial), and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Portable |

| Fixed / Wall-Mounted |

| Residential |

| Commercial |

| Bluetooth-only |

| Bluetooth + Wi-Fi (Multi-room) |

| Smart Speakers w/ Voice Assistant |

| Online-Only Retailers |

| Omnichannel Consumer-Electronics Stores |

| Economy (Less than USD 50) |

| Mid-range (USD 50-199) |

| Premium (More than USD 200) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Portability | Portable | |

| Fixed / Wall-Mounted | ||

| By Application | Residential | |

| Commercial | ||

| By Connectivity Technology | Bluetooth-only | |

| Bluetooth + Wi-Fi (Multi-room) | ||

| Smart Speakers w/ Voice Assistant | ||

| By Distribution Channel | Online-Only Retailers | |

| Omnichannel Consumer-Electronics Stores | ||

| By Price Range | Economy (Less than USD 50) | |

| Mid-range (USD 50-199) | ||

| Premium (More than USD 200) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How big is the Bluetooth speaker market in 2026?

The Bluetooth speaker market size is valued at USD 21.93 billion in 2026.

What is the projected growth rate for Bluetooth speakers through 2031?

The market is forecast to expand at a 19.65% CAGR, reaching USD 53.79 billion by 2031.

Which region leads global demand for Bluetooth speakers?

Asia-Pacific holds 31.45% market share and posts the fastest 21.15% CAGR.

Which connectivity option is growing the fastest?

Smart speakers with integrated voice assistants exhibit a 21.35% CAGR through 2031.

What drives consumer upgrades from legacy speakers?

Key drivers include smart-home ecosystem integration, Auracast broadcast audio, and higher-resolution music streaming.

Why are battery safety standards critical for manufacturers?

Stricter legislation empowers regulators to recall non-compliant devices, making robust cell testing essential to avoid costly recalls.

Page last updated on: