Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

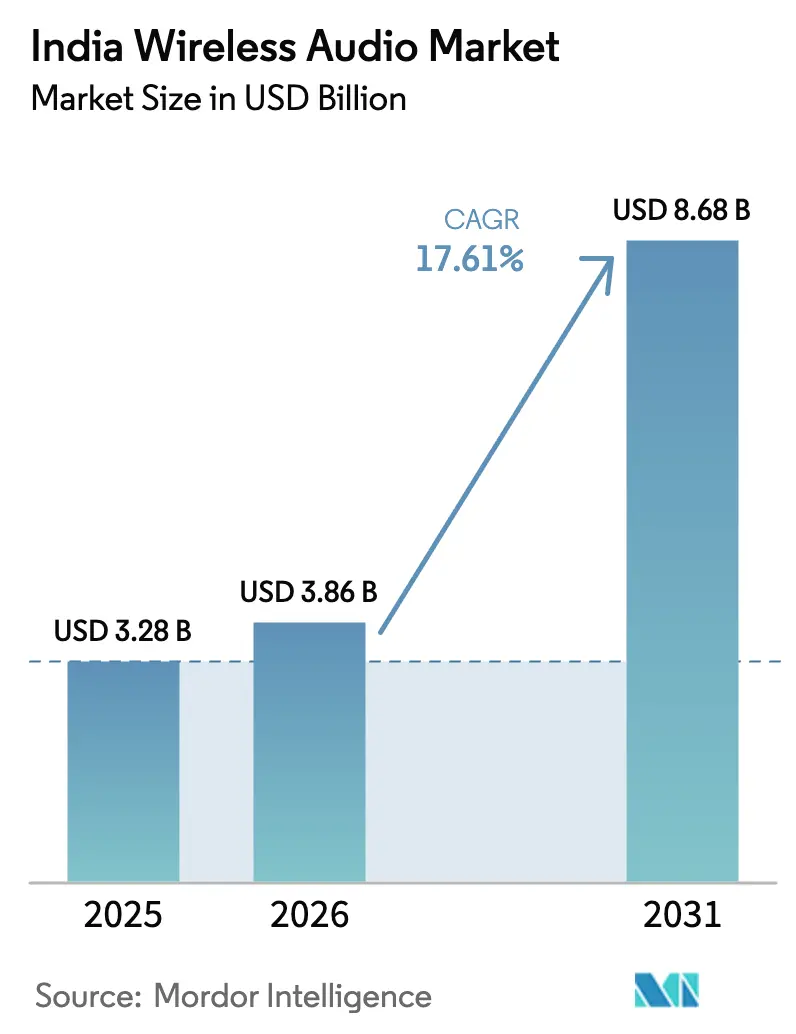

| Base Year Market Size (2025) | USD 3.28 Billion |

| Market Size (2026) | USD 3.86 Billion |

| Market Size (2031) | USD 8.68 Billion |

| Growth Rate (2026 - 2031) | 17.61% CAGR |

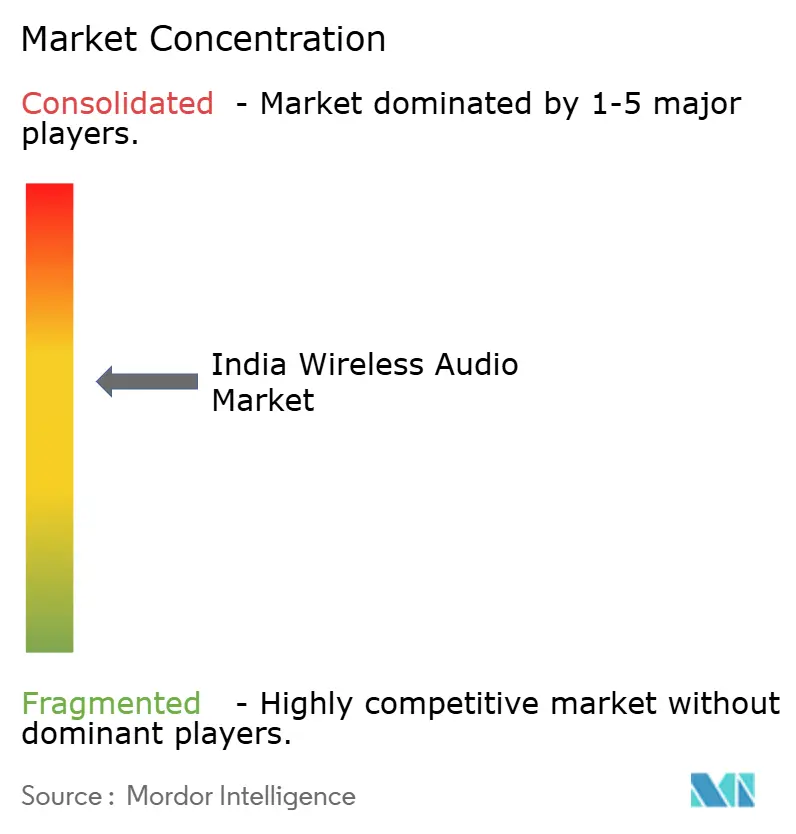

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wireless Audio Market Analysis by Mordor Intelligence

India wireless audio market size in 2026 is estimated at USD 3.86 billion, growing from 2025 value of USD 3.28 billion with 2031 projections showing USD 8.68 billion, growing at 17.61% CAGR over 2026-2031. Rapid smartphone proliferation, affordable 5G rollouts, and local manufacturing incentives collectively push the India wireless audio market toward mass-market penetration. Active noise cancellation and spatial audio, once premium features, now appear in sub-INR 2,000 devices, while domestic firms achieve 85% local value addition, reducing landed costs and bolstering supply resilience. Online channels account for 74% of 2024 revenues, driven by quick-commerce logistics that deliver same-day fulfillment in major metros. Tier-2 and tier-3 cities emerge as new demand centers as vernacular audio content increases daily listening hours and encourages entry-level upgrades. Competitive intensity intensifies as chipset shortages restrict LC3 and LE-Audio deployments, creating execution risk for brands reliant on next-generation differentiators.

Key Report Takeaways

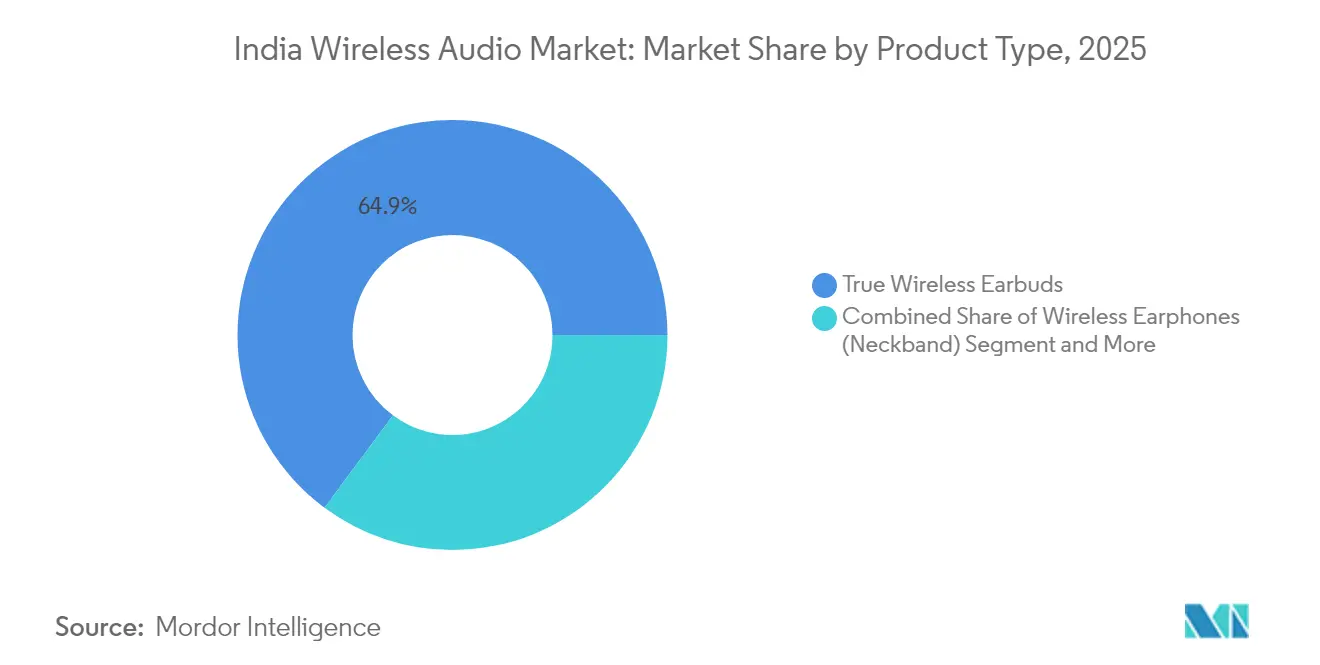

- By product type, true wireless earbuds captured 64.85% of India wireless audio market share in 2025, while the segment is projected to post a 19.05% CAGR through 2031.

- By distribution channel, online sales held 73.60% of the India wireless audio market size in 2025; offline retail is forecast to record the highest CAGR at 18.95% to 2031.

- By price band, the entry segment below INR 1,500 commanded 51.60% of the India wireless audio market size in 2025, whereas the same segment is poised to expand at an 18.55% CAGR through 2031.

- By end-user, consumer applications accounted for 88.20% of India wireless audio market share in 2025, while sports and fitness is advancing at an 17.85% CAGR during 2026-2031.

- boAt, Noise, and Boult collectively controlled 42.6% of 2024 shipments, with boAt alone holding 32.9% share and maintaining the category leadership needed to influence design standards.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Wireless Audio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone penetration and 5G affordability | +4.0% | National, with early gains in metro cities and tier-1 urban centers | Medium term (2-4 years) |

| Expansion of e-commerce and quick-commerce logistics | +3.6% | National, strongest in North India and West India corridors | Short term (≤ 2 years) |

| Domestic brands' aggressive TWS pricing | +2.9% | National, with spillover effects to South Asia markets | Short term (≤ 2 years) |

| Production-Linked Incentive (PLI) scheme boosting local hearables manufacturing | +2.5% | Manufacturing hubs in Tamil Nadu, Karnataka, Telangana, Maharashtra | Long term (≥ 4 years) |

| Rise of vernacular audio OTT and podcast platforms | +2.2% | Regional focus on Hindi belt, South India vernacular markets | Medium term (2-4 years) |

| Audio-quality differentiation (Dolby Atmos, spatial audio) in mid-range smartphones | +2.0% | Urban markets and tech-savvy consumer segments nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Smartphone Penetration and 5G Affordability Drive Mass Adoption

India’s 750 million smartphone users convert the India wireless audio market into an indispensable peripheral landscape rather than a luxury accessory segment. Telecom operators prioritize tier-2 rollouts, Jaipur, Lucknow, and Chandigarh saw pilot 5G networks during 2024, narrowing the urban-rural divide and enabling lossless streaming that validates wireless upgrades. Policy frameworks under the National Digital Communications Policy further reduce coverage gaps, thereby reinforcing user expectations for seamless audio connectivity. As battery efficiency improves, entry-level devices achieve day-long playback, meeting the functional must-have criteria of first-time buyers. The resulting multiplier effect elevates device replacement cycles, pulling forward demand and supporting the 17.9% CAGR for the India wireless audio market.

E-commerce Expansion Reshapes Distribution Economics

Online dominance at 74% illuminates deep structural shifts in buyer behavior within the India wireless audio market. Flipkart and Amazon integrate same-day and next-day delivery promises across 20 top cities, stripping physical retailers of immediacy advantages. Domestic labels leverage direct-to-consumer models to harvest feedback, iterate designs quarterly, and push firmware updates that unlock new codec support, reinforcing brand stickiness. Quick-commerce players tap under-two-hour delivery windows for impulse buys tied to music launches or sporting events. The economics favor large-scale sellers able to absorb logistics fees while preserving razor-thin margins characteristic of the entry price band. This environment forces international brands to recalibrate retail mark-ups or risk share erosion to agile local competitors.

Domestic Brands Leverage Aggressive Pricing Strategies

boAt surpassed the 50 million “Made in India” milestone in August 2024, proving that value engineering and backward integration can meet global reliability benchmarks without premium price tags.[1]Source: Electronics For You, “Apple To Start AirPods Production In India Soon For US, Europe Exports,” electronicsforyou.biz Devices under INR 1,500 now feature Bluetooth 5.3 and hybrid ANC, compressing the feature hierarchy and accelerating commoditization. Price competition aligns with local consumer expectations shaped by low-cost data plans, but it compresses gross margins, compelling manufacturers to seek component localization beyond enclosures into micro-electromechanical systems (MEMS) microphones and power-management ICs. Continuous bill-of-materials optimization allows domestic players to defend share against premium-oriented multinationals despite marketing budget disparities.

PLI Scheme Catalyzes Manufacturing Ecosystem Development

The Production Linked Incentive framework reimburses up to 6% of incremental sales value for qualifying hearables, coaxing global suppliers into joint ventures with Indian EMS partners. Foxconn’s Telangana AirPods plant and Optiemus Infracom’s realme Buds line illustrate how foreign IP converges with domestic labor cost advantages. Cluster formation in Sriperumbudur and Hosur gathers PCB fabricators, injection-molders, and acoustic testing labs within 50 kilometers, reducing transit lead times and enabling just-in-sequence assembly. Long term gains include workforce upskilling in acoustic tuning and RF validation, supplying future generations of the India wireless audio market while increasing export competitiveness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hearing-health concerns from prolonged usage | -2.0% | National, with regulatory focus from central health authorities | Medium term (2-4 years) |

| High price-sensitivity and grey-import competition | -1.7% | Border regions and major metropolitan areas with parallel import channels | Short term (≤ 2 years) |

| Chipset shortages delaying LC3 / LE-Audio roll-out | -1.4% | Global supply chain impact with manufacturing concentration effects | Short term (≤ 2 years) |

| Stricter e-waste and battery-disposal compliance costs | -1.2% | National, with state-level implementation variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Create Regulatory Compliance Challenges

The Directorate General of Health Services’ February 2025 advisory recommending sub-50 dB listening for under two hours daily elevates safety features to compliance checkpoints certification (IS 616:2017) now scrutinizes output pressure, forcing firmware-level volume-cap enforcement that increases validation costs. Tamil Nadu’s state-level alert on rising youth hearing loss signals potential patchwork regulations, compelling nationwide brands to pre-emptively standardize to the strictest rule set to avoid recall risks. As educational campaigns gain traction, some consumers may reduce daily listening hours, softening replacement demand and shaving 2.1 percentage points from the forecast CAGR of the India wireless audio market.

Price Sensitivity Limits Premium Segment Growth

Grey imports of AirPods and Sony WF-1000XM5 through parallel channels keep price floors low, compelling authorized resellers to subsidize or bundle offers to preserve footfall. Despite rising disposable incomes, cost-conscious buyers still favor sub-INR 1,500 devices for everyday use, relegating premium models to gifting or niche use cases. Multinationals design India-specific trims that remove wireless charging and multi-point pairing to reach INR 6,999 price tags, but brand dilution risk persists. Consequently, premium adoption curves lag GDP per-capita growth, creating a structural headwind against upscale migration in the India wireless audio market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TWS Leadership Accelerates Innovation Cycles

True wireless earbuds dominated with 64.85% share of the India wireless audio market size in 2025 and are forecast to post a 19.05% CAGR through 2031. Their untethered form factor aligns with Gen Z lifestyle expectations of seamless portability and on-the-go content capture. Neckband earphones held 22.35% share, appealing to cost-sensitive users who value battery longevity and physical security. Over-ear and on-ear headphones serve specialized segments such as gaming and studio mixing, retaining the balance of share under niche demand profiles.

Battery density, hybrid ANC, and low-latency gaming modes head the innovation roadmap as brands squeeze premium features into entry tiers to protect share. Local EMS partners introduce semi-automated SMT lines for compact driver assemblies that lower defect rates, supporting higher volume throughput. Meanwhile, multinational flagships position spatial audio as an aspirational upgrade path, hoping to extract value from audiophile niches. Regulatory testing under IS 616:2017 now spans all form factors, promoting a baseline quality that narrows perceived gaps between domestic and imported offerings, thus fuelling substitution within the India wireless audio market.

By Distribution Channel: Digital Commerce Transforms Market Access

Online storefronts contributed 73.60% to India wireless audio market size in 2025 and are projected to grow at 18.70% CAGR until 2031. Flash sales during festival seasons spike unit volumes, and embedded video reviews accelerate conversion by substituting in-store demos. Offline retail retained 26.40% share, particularly in tier-3 towns where experiential touch-and-feel remains critical before purchase.

Cash-on-delivery, EMIs, and no-cost returns lower adoption hurdles and build trust among first-time buyers. Same-day logistics extend beyond metros into 120 tier-2 locations, shrinking the historical delivery gap. In response, national retail chains launch store-within-store brand pods, providing live ANC comparisons to preserve relevance. Hybrid strategies emerge; brands push inventory via e-commerce while using pop-up kiosks at transit hubs for discovery. This omnichannel matrix strengthens reach and stabilizes unit flow across festival and wedding cycles, insulating revenue seasonality in the India wireless audio market.

By Price Band: Entry Segment Expansion Drives Market Democratization

Devices priced below INR 1,500 accounted for 51.60% of India wireless audio market share in 2025 and will advance at an 18.55% CAGR to 2031. Sub-USD 20 bill-of-materials targets shape design blueprints, mandating single-microphone ANC and generic plastic casings. Mid-range models between INR 1,500 and INR 4,999 captured 33.30% share, supported by urban aspirers seeking longer battery life and IP54 ratings for commute resilience. Premium units above INR 5,000 held 15.10% share, suiting brand enthusiasts and semi-professional creators.

Import duties of 20% incentivize local PCB population and final assembly, cushioning exchange-rate volatility. As die-shrink roadmaps lower SoC costs, premium features cascade downward, compressing perceived value gaps. Brands differentiate tiers through bundled subscriptions to vernacular podcasts or limited-edition colorways tied to cricket leagues. This price-band laddering sustains upgrade pathways while preserving segmentation clarity in the India wireless audio market.

By End-User: Consumer Applications Dominate with Fitness Emerging

Consumer uses drove 88.20% of shipments in 2025, reaffirming entertainment’s primacy in the India wireless audio industry. However, sports and fitness devices are slated for an 17.85% CAGR, propelled by sensor-integrated designs that measure heart rate and VO₂ max during workouts. Enterprise and professional segments comprised 7.00% share, driven by remote work call quality demands and audio-for-video production.

Wearable convergence accelerates; neckbands with in-line thermistors feed health-app dashboards, while TWS form factors integrate bone-conduction microphones for outdoor runs. Corporate procurement guidelines emphasize ENC for open-plan offices, nudging vendors to develop beam-forming solutions. As Gen Z’s device usage niches diversify into gaming and vlogging, micro-segmented SKUs emerge, enriching catalog depth and stretching lifecycle management capabilities across the India wireless audio market.

Competitive Landscape

The competitive environment features a blend of agile domestic manufacturers and premium international incumbents. boAt leads with 32.9% share, leveraging social-media micro-influencer campaigns and rapid SKU refreshes every six months. Noise follows at 9.7%, recently partnering with Bose to debut Master Buds and lift brand equity in the INR 5,000-plus tier. Boult, Truke, and Wings Lifestyle compete in the value segment, capturing students and first-time job-seekers.

International players maintain technology leadership but face pricing headwinds. Apple’s AirPods assembly in Telangana signifies a strategic shift to hedge geopolitical supply risk while chasing potential duty rebates. Samsung invests in codec co-development with local SoC partners to deliver spatial audio without inflating BOM. Sony banks on brand loyalty for audiophile and streamer sub-segments, bundling creation-suite software trials with its flagship over-ear models.

Strategic collaborations intensify. ODMs like Optiemus Infracom align with realme to roll out five million AIoT units annually, pooling capex and smoothing component procurement cycles. Component firms that supply micro-speakers and MEMS mics expand local assembly, reducing lead times and curbing currency exposure. As LC3 rollouts stall, software stack optimization becomes a battleground; brands push OTA updates that unlock multi-device pairing, enhancing perceived longevity and cutting churn within the India wireless audio market.

India Wireless Audio Industry Leaders

Imagine Marketing Ltd (boAt)

Samsung Electronics Co Ltd (Samsung, AKG, Infinity, JBL)

Apple Inc.

Sony Group Corporation

Bose Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Apple began AirPods production at Foxconn’s Telangana facility, committing USD 400 million to create an export-oriented hub.

- October 2024: Apple mapped dual-site AirPods assembly in Pune and Hyderabad, aiming for multibillion-dollar export volumes.

- September 2024: Nothing, OnePlus, and Apple refreshed line-ups across INR 2,299 to INR 17,999, signaling continued pace of feature infusion.

- August 2024: boAt crossed its 50 million locally produced cumulative device milestone, underscoring scale benefits of indigenous capacity.

India Wireless Audio Market Report Scope

A wireless audio system provides connection, flexibility, expandability, and convenience. These wireless audio devices transmit audio from audio-enabled gadgets to wireless output systems using a variety of wireless technologies, including Bluetooth, Wi-Fi, infrared, radio frequency, SKAA, and AirPlay.

The Indian wireless audio market provides an in-depth analysis of the market by tracking demand, technological trends, and recent developments in the market. The study segments the market based on product type (wireless earphones, wireless headphones, truly wireless earbuds, wireless soundbars, wireless speakers) and distribution channel (online and offline). The study also provides a detailed analysis of COVID-19's impact on the Indian wireless audio market. The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Product Type

| True Wireless Earbuds |

| Wireless Earphones (Neckband) |

| Wireless Headphones (Over / On-ear) |

By Distribution Channel

| Online |

| Offline |

By Price Band

| Entry (less than INR 1,500) |

| Mid-range (INR 1,500 - 4,999) |

| Premium (above INR 5,000) |

By End-User

| Consumer |

| Enterprise / Professional |

| Sports and Fitness |

| By Product Type | True Wireless Earbuds |

| Wireless Earphones (Neckband) | |

| Wireless Headphones (Over / On-ear) | |

| By Distribution Channel | Online |

| Offline | |

| By Price Band | Entry (less than INR 1,500) |

| Mid-range (INR 1,500 - 4,999) | |

| Premium (above INR 5,000) | |

| By End-User | Consumer |

| Enterprise / Professional | |

| Sports and Fitness |

Key Questions Answered in the Report

What is the current value of the India wireless audio market?

The market stands at USD 3.86 billion in 2026 and is projected to reach USD 8.68 billion by 2031.

Which product type leads unit sales?

True wireless earbuds lead with 64.85% share of 2025 revenues and are forecast to grow at a 19.05% CAGR.

How important is online retail to industry revenues?

Online channels accounted for 73.60% of 2025 sales, supported by quick-commerce logistics and festival flash events.

What role does the PLI scheme play?

Production incentives reimburse up to 6% of incremental sales, attracting investments such as Foxconn’s Telangana AirPods plant.

Page last updated on: