Refrigerated Trailer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

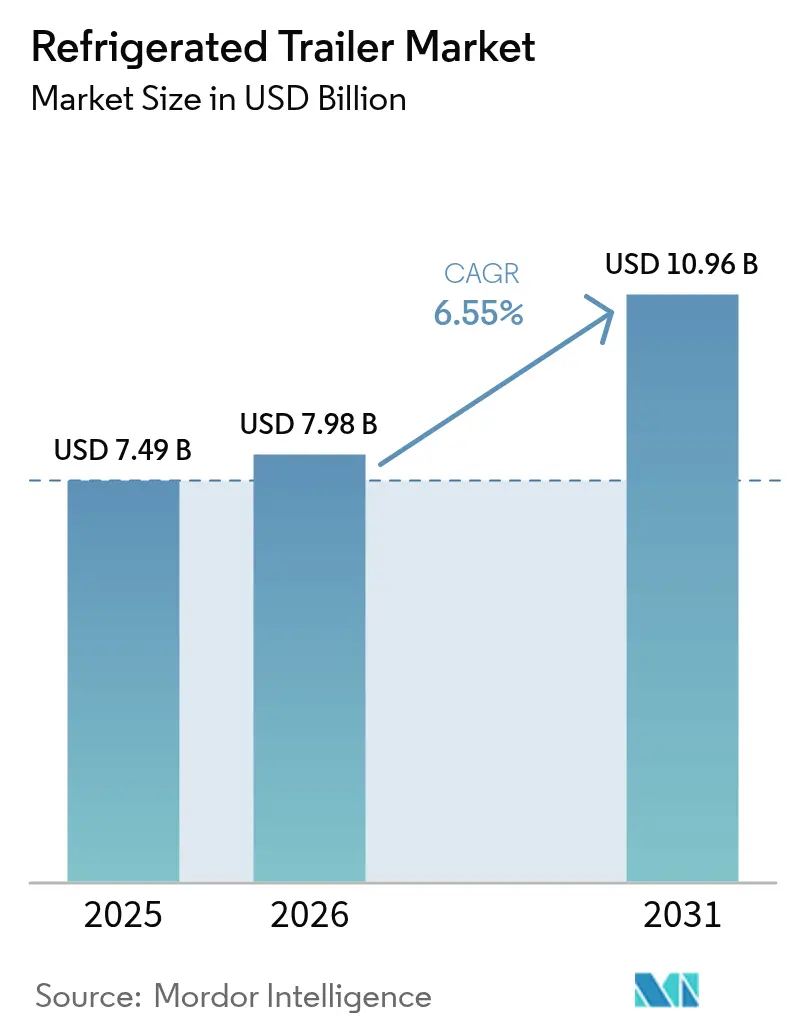

| Market Size (2026) | USD 7.98 Billion |

| Market Size (2031) | USD 10.96 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Refrigerated Trailer Market Analysis by Mordor Intelligence

The refrigerated trailer market size was valued at USD 7.49 billion in 2025 and estimated to grow from USD 7.98 billion in 2026 to reach USD 10.96 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031). E-commerce grocery fulfillment, rigorous food-safety mandates, and shifting toward electric refrigeration platforms fuel growth. The refrigerated trailer market continues to benefit from indispensable infrastructure needs that span pharmaceuticals, fresh produce, and animal protein distribution, shielding demand during macro-economic slowdowns. Competitive strategies now revolve around telematics integration, subscription-based asset services, and low-GWP refrigerants that meet tightening environmental rules. Simultaneously, large fleet operators accelerate equipment replacement cycles to comply with California Air Resources Board (CARB) and European F-Gas regulations. At the same time, emerging economies scale cold-chain capacity to serve urbanizing populations.

Key Report Takeaways

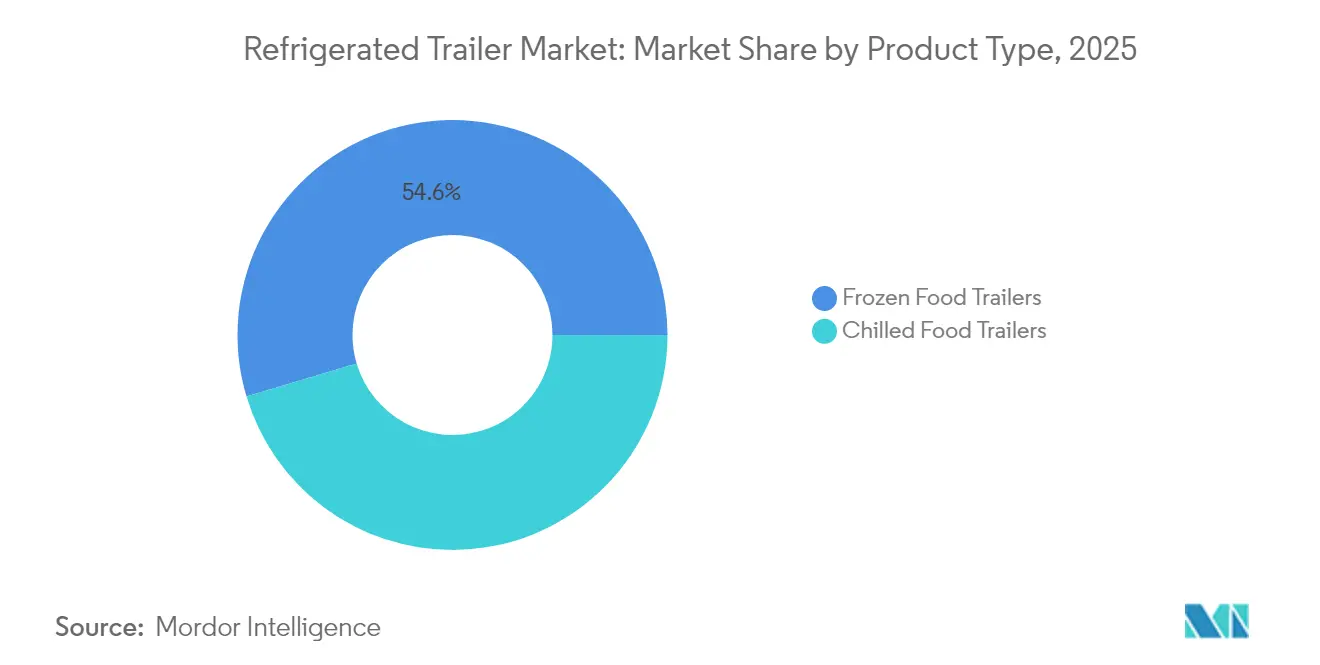

- By product type, frozen food trailers captured 54.62% of the refrigerated trailer market share in 2025; chilled food trailers are projected to expand at an 8.33% CAGR to 2031.

- By trailer length, units above 49 feet held 52.05% of the refrigerated trailer market share in 2025, while trailers up to 28 feet recorded the fastest 8.05% CAGR through 2031.

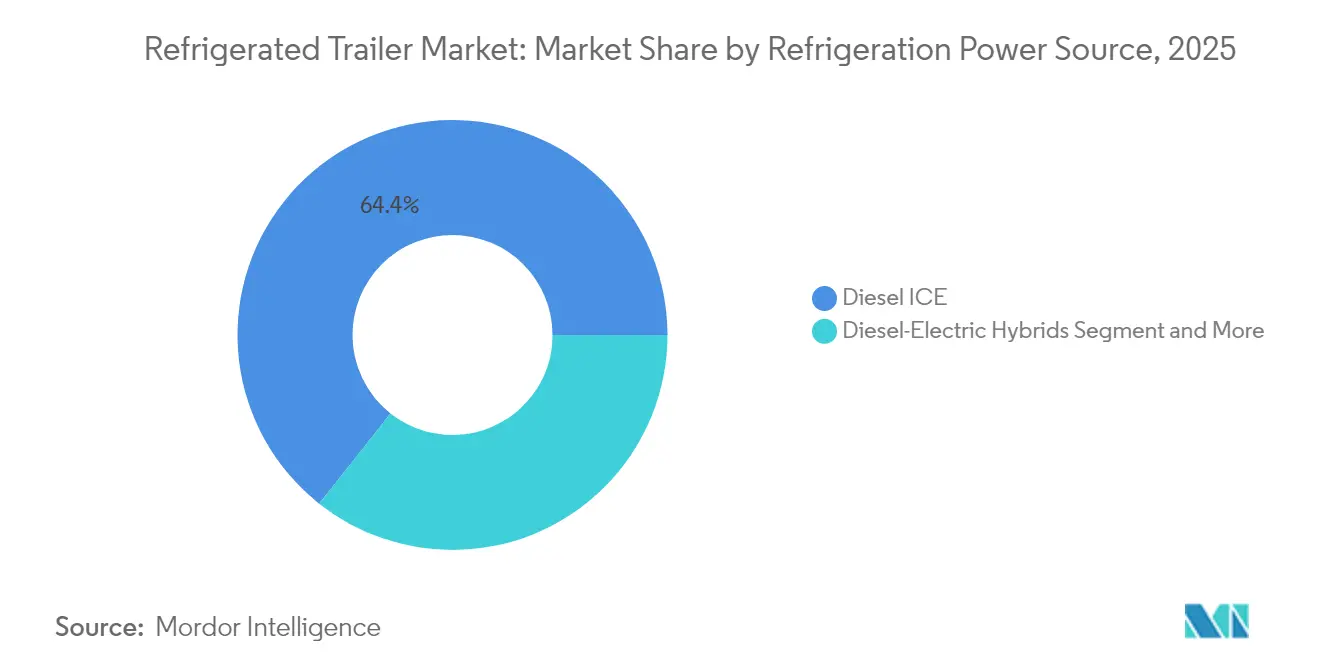

- By power source, diesel ICE platforms accounted for 64.35% of the refrigerated trailer market size in 2025; full-electric systems are forecast to grow at an 11.22% CAGR between 2026 and 2031.

- By end user, meat and seafood led with 38.86% of the refrigerated trailer market share in 2025; pharmaceuticals and life sciences represent the fastest-growing application at a 7.05% CAGR.

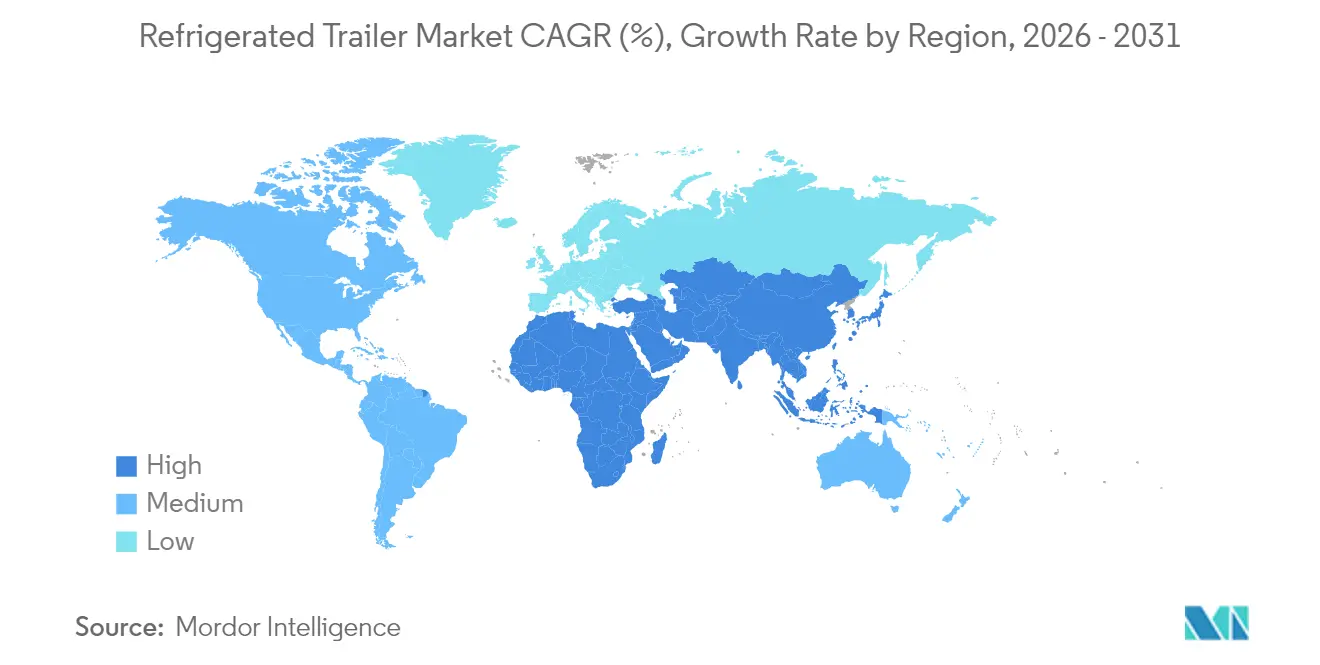

- By geography, North America commanded 39.15% of the refrigerated trailer market share in 2025, whereas Asia-Pacific is set to climb at a 8.92% CAGR through the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Refrigerated Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For E-Commerce-Led Last-Mile Cold-Chain Delivery | +1.8% | Global; focus on North America and Europe | Medium term (2-4 years) |

| Shift To Hybrid/Electric Refrigeration Units Over Diesel | +1.5% | North America and core; Asia-Pacific follow-on | Long term (≥ 4 years) |

| Tighter Food Safety Rules Requiring Temperature Tracking and Traceability | +1.2% | North America and Europe; spreading to Asia-Pacific | Long term (≥ 4 years) |

| Accelerated Cold-Chain Expansion in Asia-Pacific and Africa | +1.1% | Asia-Pacific core; MEA and South America spill-over | Medium term (2-4 years) |

| Fleet Analytics Driving Predictive Maintenance and Uptime | +0.8% | Global; early adoption in North America and Europe | Short term (≤ 2 years) |

| ESG Pressures Speeding Up Fleet Modernization | +0.5% | Global; concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for E-Commerce-Driven Last-Mile Cold-Chain Deliveries

Online grocery services reshape delivery frequency and trailer design, prompting fleets to deploy shorter, agile units that navigate dense urban corridors with multi-temperature zones. Performance Food Group deployed more than 30 battery-electric refrigerated trailers in California to support zero-emission fulfillment centers, underscoring the commercial viability of electric systems [1]“Electrifying the Cold Chain,”, Performance Food Group, pfgc.com. The versatility of up-to-28-foot units underpins their growth, while precise telematics such as Thermo King’s TracKing platform maintain cargo integrity within ±0.9 °F during stop-and-go routes[2]“TracKing Smart Trailer Brochure,”, Thermo King, thermoking.com. Fleets investing in electric trailers also capitalize on municipal noise-reduction rules and overnight delivery windows unattainable for diesel units. As cities roll out congestion pricing and zero-emission zones, operators see electric refrigerated trailers as a hedge against future access restrictions. Therefore, the convergence of e-commerce growth and sustainability policies cements compact, battery-powered equipment as an essential node in next-generation cold chains.

Stricter Food-Safety Regulations Mandating Temperature Logging and Traceability

Implementing FSMA 204 in the United States forces shippers to document end-to-end temperature histories for high-risk foods. Non-compliance can trigger recalls and civil penalties that outweigh incremental equipment costs, driving adoption of telematics-enabled trailers capable of automatic data uploads. Great Dane now fits FleetPulse telematics as standard on new refrigerated models, offering real-time alerts that simplify audit readiness [3]“FleetPulse Becomes Standard on Great Dane Trailers,”, Transport Topics, transporttopics.com. Regulation (EC) 852/2004 in the EU underpins similar traceability requirements, encouraging fleets to retrofit legacy trailers with Bluetooth probes and cloud dashboards. The regulatory push benefits suppliers that bundle hardware, software, and compliance reporting into subscription packages. Over the long term, temperature-logging mandates will likely harmonize globally, creating a rising baseline specification for every refrigerated trailer market participant.

Shift Toward Diesel-Free Hybrid and Fully Electric Transport Refrigeration Units

California's new regulations are hastening the move away from diesel-powered transport refrigeration units (TRUs), pushing fleets to adopt zero-emission alternatives. Hybrid solutions, exemplified by Carrier's advanced units using renewable fuels, are effectively reducing emissions during this transition. While fully electric TRUs boast lower maintenance requirements, they face challenges due to their reliance on charging infrastructure. Innovations like solar-powered reefers, which utilize rooftop and regenerative energy, are not only broadening operational ranges but also slashing fuel costs. With California's standards setting a precedent nationally, the once-dominant diesel is slowly making room for scalable electric platforms.

Fleet Data Analytics Enabling Predictive Maintenance and Uptime Gains

Artificial intelligence is revolutionizing refrigerated trailer operations. AI can now foresee component failures by merging real-time sensor data with historical maintenance records. This forward-thinking strategy minimizes emergency repairs, safeguarding temperature-sensitive cargo. Machine-learning models enhance inventory accuracy and mitigate spoilage risks in cold storage facilities. Fleet operators leverage telemetry to monitor tire pressure, averting breakdowns that could disrupt refrigeration cycles. Predictive maintenance streamlines technician scheduling, ensures parts availability, boosts trailer uptime, and manages warranty costs. With telematics becoming increasingly affordable, even mid-sized fleets are embracing analytics platforms, positioning data-driven operations as a pivotal competitive advantage in the refrigerated transport.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Premium of Electric / Hybrid TRUs Vs. Diesel | –1.2% | Global; sharpest in emerging markets | Medium term (2-4 years) |

| Limited Charging and Shore-Power Infrastructure Along Long-Haul Corridors | –0.8% | North America and Europe; global expansion | Long term (≥ 4 years) |

| Chronic Driver Shortage Constraining Refrigerated Capacity | –0.6% | North America and Europe; nascent in Asia-Pacific | Short term (≤ 2 years) |

| Volatile HFC Phase-Down Legislation Creating Technology Uncertainty | –0.4% | Global; region-specific rules | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Premium of Electric / Hybrid TRUs Versus Diesel

Battery-electric TRUs can cost two to three times more than diesel units, stretching payback horizons beyond five years for fleets lacking subsidy access. Smaller carriers reliant on commercial loans face higher interest rates, making cash-flow alignment difficult. Wabash National counters the hurdle via Trailers-as-a-Service subscriptions that bundle hardware, maintenance, and telematics into monthly payments, shifting capex to opex [4]“Trailers-as-a-Service Fact Sheet,”, Wabash National Corporation, wabashnational.com. Training technicians to safely maintain high-voltage systems adds indirect costs, while regional electricity prices influence the total cost of ownership. Until battery prices fall or incentives broaden, diesel will persist where fuel taxation and emission penalties remain modest.

Limited Charging and Shore-Power Infrastructure Along Long-Haul Corridors

Nationwide charging networks designed for tractors seldom account for trailer refrigeration loads, forcing fleets to plan detours or idle diesel backups. Performance Food Group installed 15 freeway-adjacent Boost Chargers to mitigate range anxiety for its California fleet. Even brief charging delays risk temperature drift for perishable loads, nudging operators toward hybrid configurations that can switch to diesel mid-route. Distribution centers with shore-power pedestals can slash idling, yet retrofits require electrical upgrades that tenants may resist funding. Broad utility collaboration is needed to align infrastructure timelines with zero-emission fleet mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Dominance Meets Chilled Growth

Frozen trailers controlled 54.62% of the refrigerated trailer market size in 2025 thanks to meat, seafood, and ready-meal logistics that demand sub-zero integrity. Operators justify higher insulation and dual-compressor systems because cargo values routinely exceed USD 100,000 per load. Conversely, chilled trailers are forecast to post an 8.33% CAGR through 2031 as online grocery and pharmaceutical biologics require 36 °F to 46 °F stability, prompting fleets to invest in multi-zone liners and rapid-cool evaporators.

Technological convergence blurs boundaries: Great Dane’s Everest platform allows operators to toggle between frozen and chilled modes via variable-speed compressors and movable bulkheads. CARB’s low-GWP mandates favor refrigerants effective across a broad temperature envelope, nudging OEMs to design flexible systems. As fresh-produce lead times tighten, carriers increasingly seek trailers that pivot between strawberries today and ice cream tomorrow without risking thermal leakage

By Trailer Length: Long-Haul Leadership Versus Urban Agility

Trailers exceeding 49 feet held 52.05% of 2025 revenue, reflecting economies of scale on interstate lanes where dock doors and cross-docks standardize around 53-foot assets. The segment’s endurance owes much to predictable cube utilization and reduced trips per ton-mile. Meanwhile, trailers up to 28 feet log the fastest 8.05% CAGR as city logistics mount congestion rules that penalize oversized rigs.

Municipal delivery windows prefer vehicles capable of tight-radius turns and curbside docking; smaller refrigerated bodies therefore capture e-grocery and meal-kit traffic in Chicago, Paris, and Singapore. Hybrid fleets mix 48-foot linehaul units feeding urban depots served by 28-foot satellites, echoing hub-and-spoke air-cargo logic. OEMs answer with modular refrigeration packages adaptable across chassis lengths, allowing fleet managers to consolidate parts inventories.

By Refrigeration Power Source: Diesel Incumbency Faces Electric Disruption

Diesel ICE solutions represented 64.35% of 2025 shipments, underpinned by mature fueling infrastructure and technician familiarity. Operating cost predictability and rapid refueling keep diesel appealing on 2,500-mile cross-country legs. Yet full-electric systems are projected to grow 11.22% annually as CARB and EU emission ceilings tighten. Incentives like California’s HVIP shave upfront costs, while battery density has climbed above 260 Wh/kg, enabling 12-hour cold-soak endurance.

Hybrid and cryogenic variants serve bridge markets; for example, liquid-nitrogen systems cut noise for overnight urban deliveries but face refilling-station scarcity. Thermo King’s Advancer electrifies the compressor but retains a Tier 4 generator, offering carriers a compliance hedge until charging networks mature. As lithium prices normalize and renewable share rises in grid mixes, total-life emissions recalculations favor electric TRUs.

By End User: Protein Dominance Meets Pharma Growth

Meat and seafood accounted for 38.86% of 2025 revenue, riding global protein demand and stringent pathogen-control norms that necessitate −4 °F setpoints. Consolidation among processors yields high-volume contracts that underpin fleet asset utilization. Pharmaceuticals and life sciences, projected at a 7.05% CAGR, galvanize demand for ±2 °F precision plus 24/7 telematics with audit trails, creating pricing latitude for premium features.

Dairy and fresh produce maintain mid-single-digit growth underpinned by health-conscious diets, while bakery and confectionery require seasonal surge capacity for holiday shipping. FDA GDP guidelines push pharma shippers to specify redundant power modules and door-opening analytics. These features trickle down to food segments over time, lifting the refrigerated trailer market’s overall technology baseline.

Geography Analysis

North America leads the refrigerated trailer market with a 39.15% revenue share in 2025, anchored by robust interstate highways, warehouse automation, and FSMA rules that obligate digital temperature logs. Core demand averages 44,000 units per year, with 2025 orders rebounding after a brief 2024 dip caused by chassis delays. Fleets adopt subscription models and electric TRUs to satisfy retailer ESG scorecards, while telematics penetration surpasses 70%, enabling predictive maintenance and route optimization.

Asia-Pacific records the fastest regional growth at a 8.92% CAGR, propelled by investments such as JBS’s USD 100 million Vietnamese meat hub and rapid urbanization that elevates per-capita cold-chain spending. Local assembly lines reduce import duties, making compliant trailers more affordable for regional fleets. Government subsidies in China and India for agricultural cold storage indirectly stimulate trailer demand, and ride-hailing platforms experiment with shared-capacity cold vans, signaling potential modal convergence.

Europe maintains steady expansion as the revised F-Gas Regulation spurs replacement of high-GWP R404A systems with natural refrigerants like CO₂ and propane, especially in Germany, France, and the Nordics. Total cost-of-ownership calculations favor fully electric trailers on dense distribution routes with ample shore power. Emerging markets in Latin America and Africa follow with infrastructure projects funded by development banks, though currency volatility tempers fleet investment pacing.

Mordor Intelligence provides coverage of the refrigerated trailer market across other key regional markets. Detailed country-level analysis extends to Indonesia, Saudi Arabia, and Malaysia incorporating local coverage and market participation, as required.

Competitive Landscape

Established OEMs such as Wabash National, Great Dane, and Utility command brand recognition and deep dealer footprints. However, the market remains moderately fragmented. Strategic differentiation centers on telematics, with Great Dane bundling FleetPulse sensors that deliver real-time tire, brake, and temperature data. Wabash National extends the value proposition through Trailers-as-a-Service, converting capital expense into a managed subscription that includes preventative maintenance.

Electrification intensifies rivalry as diversified industrials like Carrier and Trane Technologies cross-pollinate HVAC R&D into transport applications. Partnerships between trailer builders and e-power specialists multiply; TIP Group’s three-party alliance with SolarEdge and Mitsubishi Heavy Industries pioneers solar-assisted battery charging, signaling vertical integration opportunities. Midsize challengers carve cryogenic or hydrogen fuel-cell refrigeration niches, whereas Asian entrants leverage cost advantages to gain share in price-sensitive markets.

Service ecosystems grow in importance: OEMs expand parts depots and mobile repair coverage to guarantee uptime, while predictive analytics platforms monetize data through performance-based contracts. Regulatory compliance capability becomes a moat; manufacturers are able to certify equipment across CARB, EPA, and EU F-Gas standards and lock in multi-region fleet deals. Intellectual-property development skews toward battery management, thermal insulation composites, and low-GWP refrigerant circuits, reinforcing the knowledge barrier for new entrants.

Refrigerated Trailer Industry Leaders

Wabash National Corporation

Great Dane LLC.

Utility Trailer Manufacturing Company

Schmitz Cargobull AG

Fahrzeugwerk Bernard Krone GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Thermo King, renowned for its sustainable transport temperature control solutions and a key brand under global climate innovator Trane Technologies, has unveiled its latest telematics offering: the TracKing® Smart Trailer. This platform promises enhanced visibility into trailer health and cargo operations. Building on the foundation of the existing TracKing® Pro telematics, the new platform equips fleet operators with a comprehensive toolset to oversee trailers, cargo, and reefers.

- October 2024: AAA Trailers has unveiled a new lineup of refrigerated trailers tailored for operators throughout Australia. Equipped with advanced cooling technology from Thermo King and boasting road train ratings, these trailers are engineered to endure Australia's challenging conditions, all while integrating sustainable features for future savings.

Global Refrigerated Trailer Market Report Scope

Refrigerated trailers, also known as reefers, are specialized transport vehicles equipped with refrigeration systems to maintain specific temperature conditions for the transportation of perishable goods such as food and pharmaceuticals.

The refrigerated trailer market report covers all new technology trends and developments. The market is segmented based on product type (frozen food and chilled food), end user (dairy products, fruits and vegetables, meat and seafood, and other end users), and geography (North America, Europe, Asia-Pacific, and the Rest of the World). The report offers market size and forecasts in terms of value (USD) for all the mentioned segments.

| Frozen Food Trailers |

| Chilled Food Trailers |

| Up to 28 ft (Pup and City) |

| 29 - 49 ft (Standard) |

| Above 49 ft (Long-haul / 53 ft) |

| Diesel ICE Units |

| Diesel-Electric Hybrids |

| Full-Electric / Battery-Powered Units |

| Cryogenic and Alt-Fuel Units |

| Dairy Products |

| Fruits and Vegetables |

| Meat and Seafood |

| Pharmaceuticals and Life Sciences |

| Bakery and Confectionery |

| Other End Users |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type (Temperature Class) | Frozen Food Trailers | |

| Chilled Food Trailers | ||

| By Trailer Length / Capacity | Up to 28 ft (Pup and City) | |

| 29 - 49 ft (Standard) | ||

| Above 49 ft (Long-haul / 53 ft) | ||

| By Refrigeration Power Source | Diesel ICE Units | |

| Diesel-Electric Hybrids | ||

| Full-Electric / Battery-Powered Units | ||

| Cryogenic and Alt-Fuel Units | ||

| By End User | Dairy Products | |

| Fruits and Vegetables | ||

| Meat and Seafood | ||

| Pharmaceuticals and Life Sciences | ||

| Bakery and Confectionery | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the refrigerated trailer market in 2026?

The refrigerated trailer market size reached USD 7.98 billion in 2026, supported by e-commerce grocery expansion and stricter food-safety rules.

What is the projected growth rate for refrigerated trailers?

Global demand is anticipated to rise at a 6.55% CAGR, taking revenue to USD 10.96 billion by 2031.

Which product segment leads current sales?

Frozen food trailers accounted for 54.62% of 2025 sales due to the dominance of meat and seafood logistics.

How are regulations influencing trailer technology?

CARB’s zero-emission TRU requirements and the EU F-Gas phase-down are accelerating the shift to electric refrigeration and low-GWP refrigerants.

What financing models help fleets afford electric trailers?

Subscription models such as Wabash National’s Trailers-as-a-Service convert upfront capex into monthly opex, easing the adoption of higher-cost electric units.

Page last updated on: