Iraq Trailer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

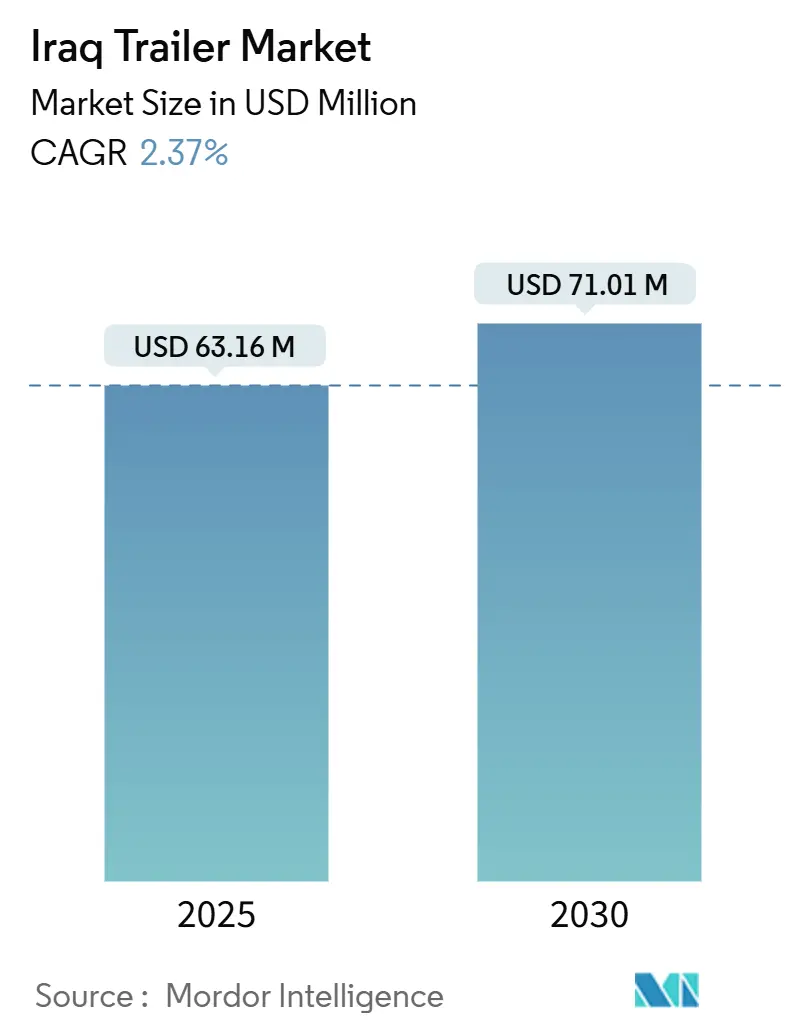

| Market Size (2025) | USD 63.16 Million |

| Market Size (2030) | USD 71.01 Million |

| Growth Rate (2025 - 2030) | 2.37% CAGR |

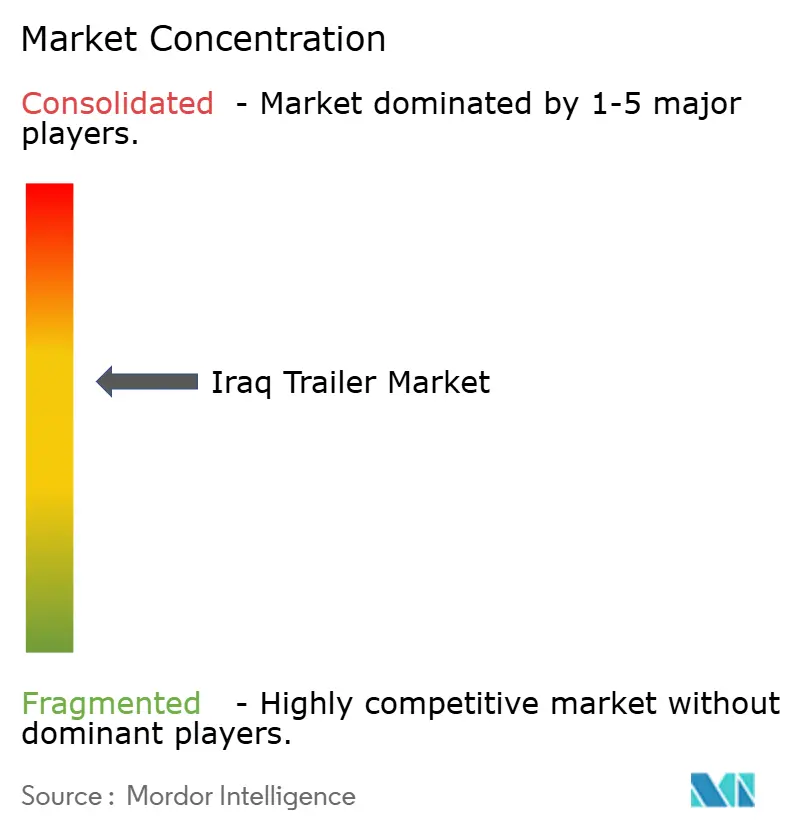

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Trailer Market Analysis by Mordor Intelligence

The Iraq Trailer Market size is estimated at USD 63.16 million in 2025, and is expected to reach USD 71.01 million by 2030, at a CAGR of 2.37% during the forecast period (2025-2030). This measured expansion is tied to reconstruction spending, the revival of oil and gas projects, and the government’s Development Road corridor that will connect Basra with Turkey and onward to Europe. Tipper units remain the workhorse as rebuilding activity demands high-volume aggregate haulage, while refrigerated units are gaining traction in response to rising cold-chain needs. Heavy-duty configurations exceeding 30 tons lead overall demand, underscoring the industrial weight of Iraq’s transport flows. Persistent security risks and currency volatility temper growth; however, the introduction of the TIR system in April 2025 is reducing cross-border transit times and costs, positioning the Iraq trailer market as a gateway between the Gulf, the Levant, and Europe.

Key Report Takeaways

- By trailer type, tipper trailers led the Iraqi trailer market with 34.15% of the market share in 2024, and refrigerated trailers are forecast to expand at a 2.39% CAGR through 2030.

- By end-use industry, construction accounted for a 36.63% share of the Iraq trailer market size in 2024, and food and grocery is projected to grow at a 2.48% CAGR between 2025 and 2030.

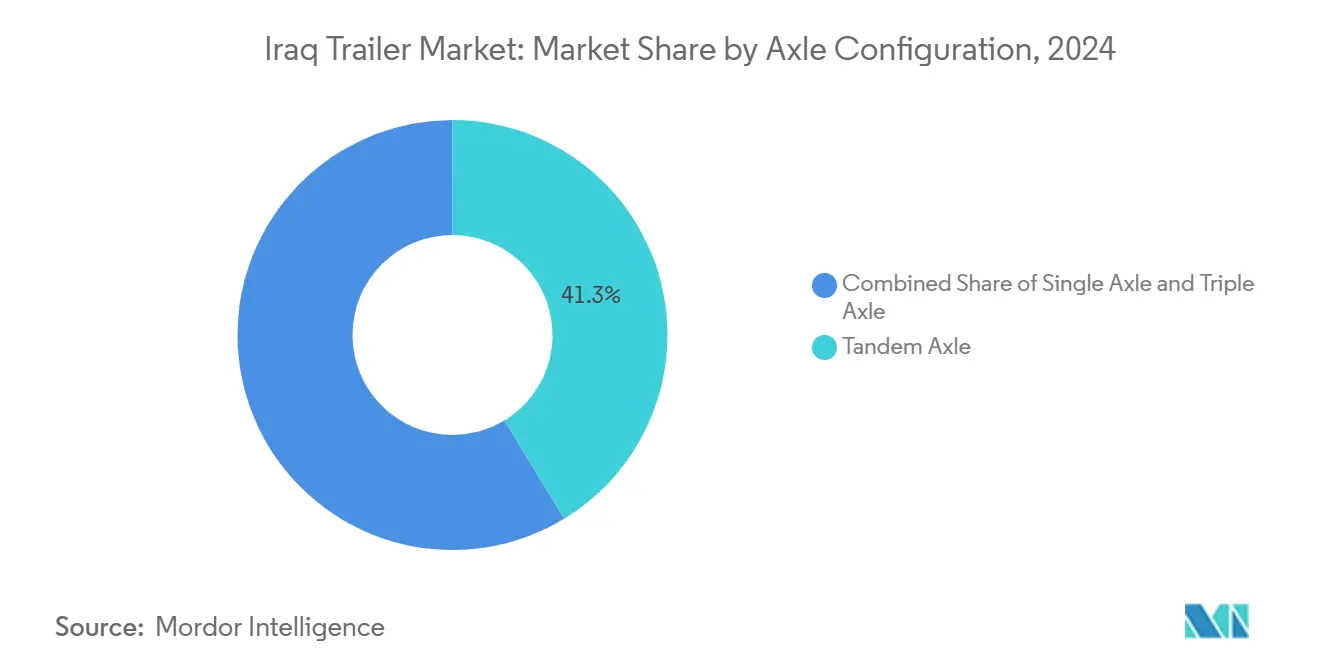

- By axle configuration, tandem axle units held a 41.27% share of the Iraqi trailer market size in 2024, and triple axle units are projected to post the fastest growth at a 2.43% CAGR to 2030.

- By load capacity, heavy-duty trailers above 30 tons represented 43.47% of the Iraqi trailer market share in 2024, and medium-duty trailers between 10 tons and 30 tons are set to rise at a 2.45% CAGR to 2030.

Iraq Trailer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-ISIS Reconstruction Boom | +0.8% | National, concentrated in Anbar, Ninewa, Salah al-Din | Medium term (2-4 years) |

| Expansion Of Basra Oil & Gas Projects | +0.6% | Southern Iraq, primarily Basra province | Long term (≥ 4 years) |

| Government-Funded Road-Infrastructure Upgrades | +0.5% | National, with focus on Development Road corridor | Long term (≥ 4 years) |

| Cross-Border Trade Growth | +0.4% | Northern and eastern border regions | Medium term (2-4 years) |

| Shift From Imported Used Trailers To Local Assembly | +0.3% | National | Short term (≤ 2 years) |

| Adoption Of Telematics-Enabled Trailers | +0.2% | National, with early adoption in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-ISIS Reconstruction Boom Fueling Construction Haulage Demand

Government-backed initiatives are driving the resurgence of Iraq's trailer market. The National Investment Commission has allocated a significant budget for various projects, with major investments in the Baghdad Metro and an expressway network spanning the liberated provinces. In 2024, numerous water and sewage projects commenced, creating a robust demand for high-capacity tipper and flatbed units to ensure consistent deliveries of aggregates and pipes. Contractors are increasingly favoring trailers adept at transporting bulk cement, steel, and precast structures over long distances, all while navigating bustling job sites. These ongoing public works not only keep older fleets in high demand but also ensure stable replacement cycles [1]“Iraq Investment Map 2024,” National Investment Commission, nic.gov.iq .

Expansion of Basra Oil & Gas Projects Driving Tanker Trailer Uptake

Basra's hydrocarbon boom is expanding the fleet of specialized tankers. A government-sanctioned pipeline, involving a substantial investment, is set to transport a significant volume of oil from Basra to Haditha, with operations expected to commence in the near future. At the same time, Geo-Jade's ambitious plan to significantly increase output at the Tuba field is ramping up the flow of drilling chemicals, fuel, and treated crude. Both ventures necessitate ADR-compliant stainless-steel tankers, adept at withstanding desert heat and making the long journey from fields to port depots. Furthermore, operators investing in GPS-equipped tankers are reaping the benefits of preferential contracts, a nod to the heightened security measures adopted by oil firms [2]“Basra-Haditha Crude Pipeline Approvals,” Ministry of Oil, oil.gov.iq .

Government-Funded Road-Infrastructure Upgrades

Highway upgrades are underway, with a significant portion of the planned network already resurfaced. Enhanced pavement tolerances now accommodate heavier axle loads, thereby expediting deliveries between key cities, including Basra, Baghdad, and Mosul. Additionally, a substantial rail rehabilitation project, financed by the World Bank, boosts the demand for flatbeds capable of transporting rails, ballast, and heavy machinery. These developments bolster the Development Road, a vital corridor stretching from Grand Faw Port to Turkey, which is expected to handle a considerable volume of containers annually in the near future.

Cross-Border Trade Growth With Turkey & Iran Increasing Flatbed Flows

In April 2025, Iraq joined the TIR regime, significantly reducing the door-to-door transit time on the Mersin-Umm Qasr route and substantially cutting logistics costs. Convoys at the Ibrahim Khalil and Fishkhabor crossings, which handle a high volume of daily truck traffic, are now predominantly using flatbed and skeletal chassis. Forwarders have noted an improvement in back-haul fill rates, with exporters in Erbil successfully sourcing return cargo from Turkish wholesalers. This consistent clearance has attracted EU haulers, who are now considering Basra port calls for Gulf traffic, further bolstering investments in multi-axle flatbeds [3]“Iraq Becomes 78th Country to Implement TIR,” International Road Transport Union, iru.org .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Security Risks | -0.6% | National, concentrated in disputed territories | Long term (≥ 4 years) |

| Dominance Of Informal Trucking | -0.5% | National, with higher concentration in rural areas | Long term (≥ 4 years) |

| Currency Volatility and LC Shortages | -0.4% | National | Medium term (2-4 years) |

| Lack Of ADR-Certified Service Stations | -0.3% | National, particularly rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Security Risks and Periodic Route Closures

Between early 2023 and early 2024, the European Union Agency for Asylum recorded a significant number of security incidents, with the majority involving explosions or remote violence. Northern regions, including Dohuk and Erbil, experience frequent drone strikes linked to clashes between Turkey and the PKK. This volatility has led insurers to either hike premiums or outright deny coverage. Additionally, landmines have contaminated a substantial portion of the country's territory, forcing haulers to take lengthy detours. These detours not only diminish fleet utilization but also inflate fuel expenses. As a result, haulers are compelled to factor in escorts and rerouting into their bids, which diminishes their price competitiveness.

Dominance of Informal Trucking Limiting Fleet Modernization

Thousands of small operators run single-truck businesses without formal registration, bypassing tax and safety checks. They operate older, imported trailers that often exceed axle limits and avoid using telematics that could expose route deviations. This ecosystem dilutes demand for new builds with advanced suspension, braking, and load-monitoring features. It also hampers authorities' efforts to enforce weight and emission standards, thereby delaying the transition to modern, more efficient fleets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Trailer Type: Tipper Dominance Drives Construction Recovery

Tipper units captured 34.15% of the Iraqi trailer market share in 2024, reflecting the round-the-clock movement of aggregates, rubble, and earth on reconstruction sites. Projects like the Baghdad Metro, which require significant excavation work, are driving the growth of Iraq's trailer market, particularly for tippers. Box or dry-van trailers occupy the second position, serving FMCG distribution to retailers in Baghdad, Basra, and Erbil. Tanker demand remains constant as the Basra-Haditha pipeline and Tuba field upgrade necessitate dedicated petroleum logistics. Refrigerated units, although with a small base, are projected to post the quickest 2.39% CAGR as supermarkets expand and vaccine imports remain high during post-pandemic rollouts. Flatbed volumes rise with container flows under the TIR program and oversized cargo for port-to-site moves. Domestic assemblers now quote 45-ton multi-purpose semi-trailers, signaling a shift from pure imports toward hybrid local builds.

Across 2025-2030, tipper dominance will moderate as flatbed and reefer fleets expand. Builders incorporate alloy steel and thermal insulation to withstand Iraq’s 50 °C summers, thereby extending trailer life and reducing operating costs. Parts interchangeability with Turkish makes support for uptime on long-haul desert routes. Price sensitivity remains high, but shippers are increasingly specifying ABS, load sensors, and GPS, which pushes upgrade cycles. OEMs offering in-country parts depots and training gain orders as contractors hedge against border delays.

By End-Use Industry: Construction Leads Infrastructure Renaissance

Construction accounted for 36.63% of Iraq's trailer market size in 2024, driven by megaprojects in housing, transport, and energy. Al-Rashid New City requires a significant number of bricks, necessitating a fleet of trailers, while the Grand Faw Port has an ongoing need for substantial supplies of concrete and steel. The public works pipeline offers multi-year visibility, enabling contractors to secure long-term leases and minimize capital expenditures. Food and grocery distribution is the fastest riser, with a 2.48% CAGR, driven by rising imports of chilled poultry, dairy, and fresh produce as incomes recover. Oil and gas remain a steady anchor, with procurement tied to field expansions and the construction of new pipelines. Logistics providers utilize the TIR regime to reposition empty chassis onto export routes, thereby increasing fleet utilization.

Industry diversification spreads risk for fleet owners. Construction-skewed fleets now add refrigerated and tanker units to tap new lanes. Government procurement also enforces ISO safety and environmental standards, raising the bar for compliance. Fleet owners with mixed-use capability and documented maintenance win broader contracts across water projects, refineries, and retail supply chains.

By Axle Configuration: Tandem Axle Versatility Meets Infrastructure Demands

Tandem axle designs accounted for 41.27% of the Iraqi trailer market size in 2024. These units satisfy axle load caps while offering maneuverability in urban sites. Operators value their lower tire wear and fuel consumption over triple axle alternatives. Single-axle units serve niche courier and small retail deliveries within Baghdad, where narrow streets and checkpoints restrict the use of larger rigs. Triple axle demand rises fastest at 2.43% CAGR as hauls lengthen on improved highways and customers seek higher payload per trip. The Development Road corridor will favor triple axle and multi-axle combinations once complete, encouraging fleets to invest ahead of traffic shifts.

Regulators enforce 25-ton limits on 3-axle semis and 34 tons on 4-axle semis, spurring interest in intelligent load monitoring. Weighbridge expansion at major crossings boosts compliance, and on-board weight sensors help avoid fines. Manufacturers offer air-suspension retrofits that reduce pavement damage and lower maintenance costs, a selling point as road concessions introduce axle taxes.

By Load Capacity: Heavy-Duty Dominance Reflects Industrial Requirements

Heavy-duty trailers weighing more than 30 tons secured 43.47% of the Iraqi trailer market share in 2024. Oil rigs, precast beams, and bulk aggregate runs keep these units busy, and domestic builder SCAI’s 45-ton lineup caters to the segment. Light-duty units, weighing under 10 tons, primarily focus on last-mile deliveries in city centers, often operated by small, family-owned firms. Medium-duty (10-30 tons) trailers show the fastest 2.45% CAGR through 2030, benefiting from trade lanes where road limits cap maximum payload. Upgraded pavements and modern bridges enable medium loads to travel at higher average speeds, reducing trip counts and fuel consumption.

Fleet planning now blends heavy-duty workhorses for megaprojects with medium units for regional distribution. Imported driveline components paired with local steelwork keep purchase prices competitive. Weight-enforcement upgrades at ports and border posts reinforce the medium-capacity sweet spot for owners who want to avoid excess-axle fines yet haul more than light units permit.

Geography Analysis

Southern Iraq is the most significant contributor to the Iraqi trailer market. Basra’s port throughput, the Grand Faw expansion, and petrochemical plants create continuous inbound steel, cement, and outbound liquid cargo. Stable security, compared to northern districts, supports capital spending on new fleets, although tribal disputes occasionally disrupt rural routes. Central Iraq, anchored by Baghdad, forms the administrative and commercial heart, channeling national reconstruction budgets and consumer imports. The Baghdad Metro and expressway networks feed steady trailer cycles, while moderate security risks keep insurance rates manageable.

Northern Iraq, covering the Kurdistan Region, is the fastest-growing sub-market. High truck counts at the Ibrahim Khalil gate, combined with the region’s role as a staging ground for Turkish exports, lift demand for container chassis and flatbeds. Nonetheless, drone strikes and military operations raise operating risks and delay deliveries. Harmonized customs procedures introduced in February 2024 trimmed clearance times, incentivizing larger fleets to station assets in Erbil. Fuel prices are marginally higher than in the south, but faster turnarounds offset cost gaps. Agricultural exports of pomegranates and grapes also add reefer demand during harvest peaks.

Western deserts remain thinly populated but are home to phosphate and cement plants. Poor road conditions and periodic security incidents deter widespread fleet investment, but niche operators with heavy-duty, low-bed trucks service moves involving mining equipment. Opportunities in Jordan's transit flow hinge on ongoing highway upgrades and are expected to grow once border terminals complete their planned expansion in 2026. Overall, geographic diversification helps carriers smooth revenue swings tied to project cycles and security flare-ups.

Competitive Landscape

The Iraqi trailer market is moderately fragmented—international brands like Kassbohrer, Schmitz Cargobull, and TIRSAN import SKD kits through Basra and Mersin. In contrast, Chinese firms are making their entry through Kurdistan. Domestic capacities are on the rise: the State Company for Automotive Industry is producing heavy-duty tippers and flatbeds, while Al-Walaa Trailers is fabricating tankers in Najaf. Market share is widely dispersed, with no single manufacturer holding a significant portion. Yet, global brands are securing government tenders through alliances with local dealers.

Technology adoption sets players apart. Kassbohrer’s telematics-ready suspensions and EBS are in demand by oil majors for their load tracking requirements. Schmitz Cargobull’s modular reefer bodies, boasting superior insulation, are essential for Iraq’s scorching summers. Local companies offer competitive advantages with shorter lead times, easier parts sourcing, and more favorable dinar pricing. As government bids increasingly emphasize domestic value addition, foreign OEMs are being nudged to localize operations, including licensing welding and painting.

Strategic maneuvers highlight the push for localization. In the near future, Scania, through SCAI, plans to initiate CKD truck and trailer assembly in Babylon province, aiming to deliver a significant volume of units to ministries over several years. CIMC Vehicles recently inked an MOU with Kurdish investors for a panel plant, set to produce box bodies and reefers within a few years. Opportunities abound in ADR-certified tanker builds and advanced cold-chain trailers. Companies that align with ISO 9001 and ISO 14001 standards are poised for an advantage, especially as state purchasers increasingly prioritize these certifications in their tenders.

Iraq Trailer Industry Leaders

GORICA Group

Kassbohrer

Schmitz Cargobull

CIMC Vehicles

Fruehauf SAS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The TIR (International Road Transport) system, a global standard for secure cross-border trade, went live in Iraq. This is a significant development for the trailer market as it is expected to reduce transport time by 80% and costs by 38% for international cargo, increasing the efficiency and demand for road transport using trailers across borders.

- October 2024: Global logistics giant Aramex unveiled a joint venture with Abu Dhabi's ZK Holding to enhance its services in Iraq. This partnership aims to bolster freight forwarding and contract logistics operations across over 15 Iraqi cities, which increases the demand for various types of trailers for efficient last-mile and general logistics.

Iraq Trailer Market Report Scope

The Iraqi trailers market encompasses the production, import, distribution, and use of diverse trailers in Iraq, catering to industries that transport goods, materials, and machinery. These trailers, ranging from flatbeds and lowbeds to tankers and refrigerated units, are tailored to meet the logistical demands of pivotal sectors, including construction, oil and gas, infrastructure, agriculture, and general trade.

The Iraqi trailers market is segmented based on type, axle, and application. By type, the market is segmented into flatbed trailers, dry van trailers, refrigerated trailers, tank trailers, lowboy trailers, and drop deck trailers. By application, the market is segmented into construction, agriculture, logistics and transportation, mining, recreation, and others (including chemical and hazardous material transport, petroleum and oil transport). By axle, the market is classified into single-axle trailers, tandem-axle trailers, and multi-axle trailers. For each segment, the market size is provided in terms of value (USD).

| Tipper |

| Flatbed |

| Box / Dry-Van |

| Refrigerated |

| Tanker |

| Logistics |

| Food & Grocery |

| Oil & Gas |

| Construction |

| Others |

| Single Axle |

| Tandem Axle |

| Triple Axle |

| Light-Duty (Less than 10 T) |

| Medium-Duty (10–30 T) |

| Heavy-Duty (More than 30 T) |

| By Trailer Type | Tipper |

| Flatbed | |

| Box / Dry-Van | |

| Refrigerated | |

| Tanker | |

| By End-Use Industry | Logistics |

| Food & Grocery | |

| Oil & Gas | |

| Construction | |

| Others | |

| By Axle Configuration | Single Axle |

| Tandem Axle | |

| Triple Axle | |

| By Load Capacity | Light-Duty (Less than 10 T) |

| Medium-Duty (10–30 T) | |

| Heavy-Duty (More than 30 T) |

Key Questions Answered in the Report

What is the current value of the Iraq trailer market?

The market reached USD 63.16 million in 2025 and is set to grow steadily toward USD 71.01 million by 2030.

Which trailer type holds the largest share?

Tipper trailers lead the Iraqi trailer market with a 34.15% share in 2024, driven by reconstruction activity.

Which segment is expanding the fastest?

Refrigerated trailers post the quickest 2.39% CAGR, thanks to growing demand for the cold chain in the food and pharmaceutical sectors.

How is cross-border trade influencing demand?

Iraq’s April 2025 TIR rollout slashed transit times and costs, boosting flatbed and container-chassis utilization on Turkey and Iran routes.

What challenges affect fleet modernization?

Security risks, currency volatility, and the prevalence of informal trucking constrain large-scale investments in advanced trailer technologies.

Page last updated on: