Traffic Signal Controller Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 11.54 Billion |

| Growth Rate (2026 - 2031) | 12.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Traffic Signal Controller Market Analysis by Mordor Intelligence

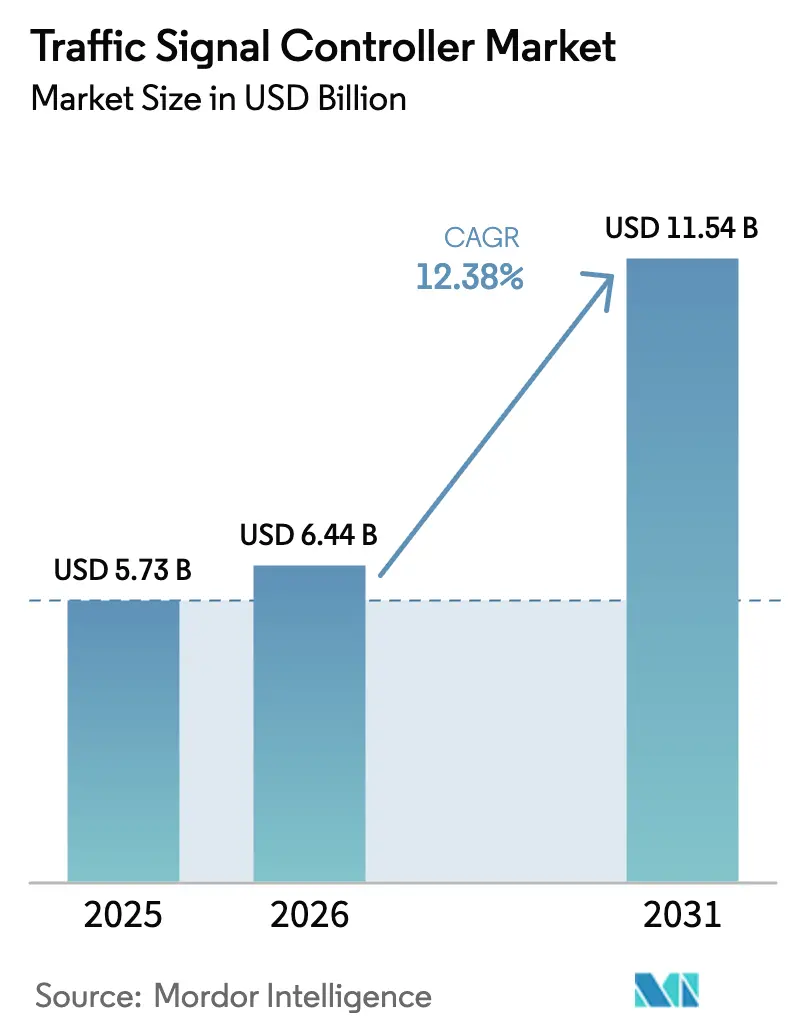

The Traffic Signal Controller Market size was valued at USD 5.73 billion in 2025 and estimated to grow from USD 6.44 billion in 2026 to reach USD 11.54 billion by 2031, at a CAGR of 12.38% during the forecast period (2026-2031). Rising urban populations, national commitments to smart-city spending, and the shift toward artificial-intelligence optimisation have moved traffic management from periodic signal timing updates to predictive control systems that adjust in real time. Federal support in the United States through the SMART Grants Program, together with Asian mega-city infrastructure programs, has created a continuous funding pipeline for new deployments.

Key Report Takeaways

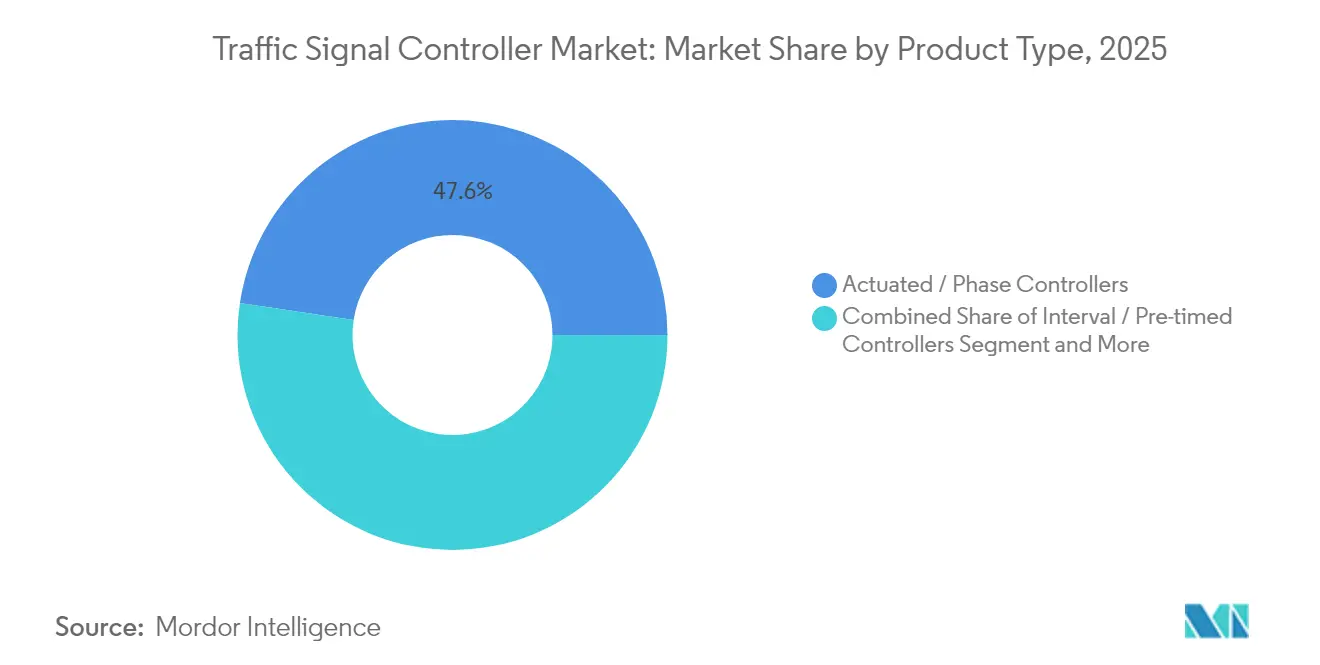

- By product type, actuated/phase controllers held 47.62% of the traffic signal controller market share in 2025, while adaptive/intelligent controllers are projected to grow at a 12.22% CAGR through 2031

- By technology, fully-actuated systems commanded 38.92% of the traffic signal controller market's market share in 2025, while AI-powered adaptive systems are advancing at 12.87% CAGR through 2031.

- By installation environment, urban intersections accounted for 57.64% of the traffic signal controller market share in 2025 and highway and expressway deployments are expanding at 11.12% CAGR to 2031.

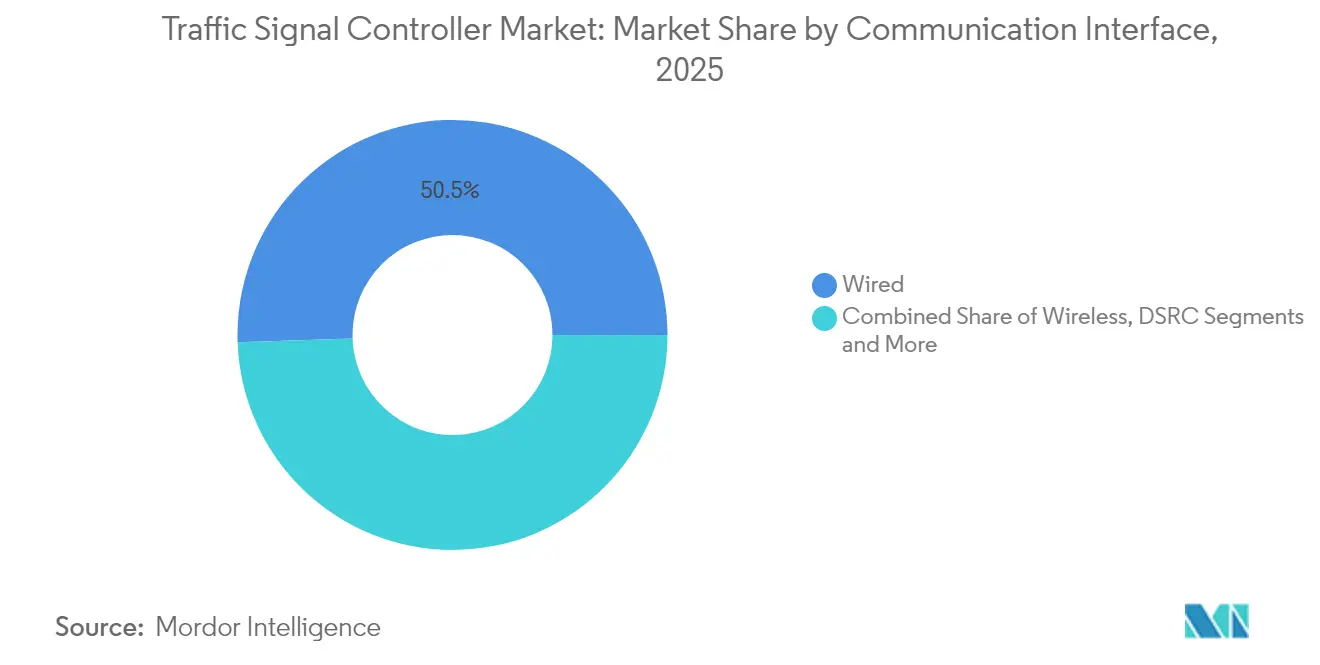

- By communication interface, wired retained 50.54% of the traffic signal controller market's market share in 2025; Cellular-V2X interfaces are growing at 12.41% CAGR through 2031.

- By end user, municipal and city traffic agencies led with 64.05% of the traffic signal controller market's revenue share in 2025; smart-city integrators are projected to expand at a 12.79% CAGR through 2031.

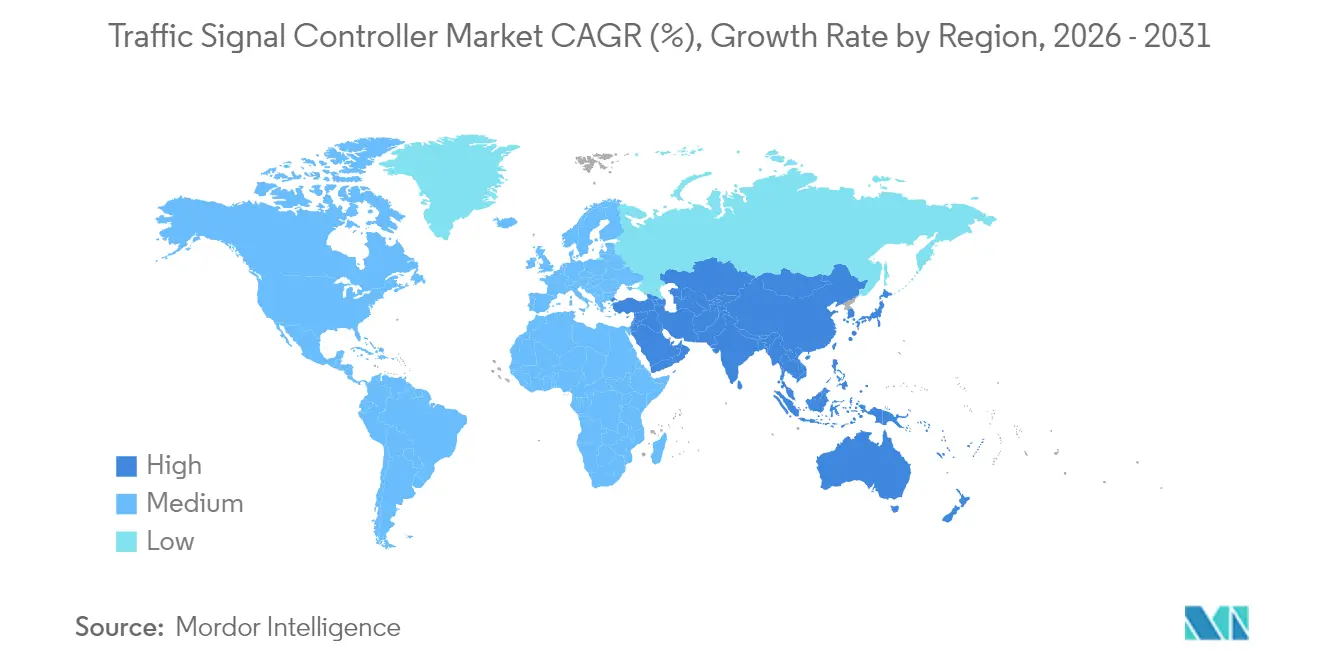

- By geography, North America held 36.95% share of the traffic signal controller market's market share in 2025 while Asia-Pacific is set to grow at 12.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Traffic Signal Controller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban Congestion and Smart-City Traffic Growth | +2.8% | Global, concentrated in Asia-Pacific megacities | Medium term (2-4 years) |

| Government Funding | +2.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| AI-Enabled Adaptive Traffic-Signal | +1.9% | Global, led by developed markets | Medium term (2-4 years) |

| IoT / V2X Integration | +1.6% | North America and Europe early adoption, Asia-Pacific scale | Long term (≥ 4 years) |

| Edge-Compute Decentralised Controllers | +1.4% | Global, technology-forward cities | Medium term (2-4 years) |

| Emission-Reduction Mandates | +1.2% | Europe and North America regulatory pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urban Congestion and Smart-City Traffic Growth

Traffic delays already cost Asian megacities 2-4% of GDP in lost productivity, prompting city governments to prioritise signal modernisation within broader mobility masterplans. The Asian Development Bank estimates USD 43 trillion will be spent on transport infrastructure in Asia Pacific by 2035, with 63% directed to road assets that require advanced signal control for throughput gains[1]“Meeting Asia’s Infrastructure Needs,” Asian Development Bank, adb.org . Medellín’s adaptive corridor upgrade reduced average journey times 25% and cut traffic accidents 15%, offering proof that signal retrofits deliver immediate social returns. Such performance records are convincing municipal treasurers to reallocate funds from periodic retiming exercises to capital programmes that install AI-ready controllers. The resulting demand surge ensures the traffic signal controller market remains a core component of every metropolitan digital-infrastructure roadmap.

Government Funding for Smart Transportation Infrastructure

Public financing models have evolved from mileage-based refurbishment to innovation grants that underwrite sophisticated traffic signal solutions. The United States Department of Transportation awarded USD 54 million in SMART grants across 34 projects in 2024, with eight awards earmarked for intelligent signal pilots[2]“SMART Grants Program Awards 2024,” United States Department of Transportation, transportation.gov . Europe mirrors this pattern: the United Kingdom set aside GBP 0.999 million in 2024 for adaptive pedestrian-priority trials. Dedicated programmes de-risk procurement for local agencies by absorbing upfront technology costs, and they promise recurring funds tied to performance milestones. Consequently, manufacturers experience predictable order pipelines, while integrators form consortia to satisfy increasingly complex grant-compliance specifications.

AI-Enabled Adaptive Traffic-Signal Deployment

Artificial intelligence has moved from small-scale pilots toward portfolio-wide roll-outs. Parallel research into Large Language Model agents, such as the LLMLight framework, shows these controllers better handle a typical congestion than earlier reinforcement-learning engines. The cumulative evidence positions AI adaptation not as experimental technology but as baseline functionality for the next procurement cycle, accelerating the traffic signal controller market transition toward predictive optimisation.

IoT / V2X Integration for Real-Time Optimisation

Vehicle-to-Everything standards are reshaping controller architectures. The United States Department of Transportation funded USD 60 million in 2024 for Arizona, Texas and Utah to embed V2X emergency pre-emption and transit signal priority into corridor projects. Peer-review studies confirm roughly 15% faster travel times and 8% lower fuel burn when V2X-enabled signals coordinate with connected vehicles. Cellular-V2X outperforms DSRC on coverage and mobility, while 5G slicing offers deterministic latency for safety-critical phases. As fleets and infrastructure connect over the 5.9 GHz ITS band, controllers become nodes in a cloud-edge network that optimises mobility across an entire region rather than a single junction, cementing V2X as a core determinant of traffic signal controller market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Advanced Traffic-Engineering Talent | -2.3% | Global, acute in Asia-Pacific and developing markets | Long term (≥ 4 years) |

| Legacy-System Interoperability Hurdles | -2.3% | Global, concentrated in mature markets with aging infrastructure | Medium term (2-4 years) |

| High Installation and Lifecycle Costs | -1.8% | Global, acute in developing markets | Short term (≤ 2 years) |

| Cyber-Security and Data-Privacy Risks | -1.2% | Global, regulatory focus in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Installation and Lifecycle Costs

Deploying adaptive controllers often requires investment far beyond cabinet replacement. Intersection surveys, fibre backhaul, detection cameras, and staff retraining can raise per-site costs from USD 10,000 to USD 120,000, depending on scope. The National Traffic Signal Report Card places ongoing US operating expenditure at USD 1.23 billion annually, which strains small municipalities with limited tax bases. Hampton Roads’ migration study showed that aligning disparate legacy cabinets onto a common platform necessitated multijurisdictional coordination, delaying procurement cycles. Developing regions face steeper challenges: currency volatility and import duties inflate hardware prices, while shortages of certified technicians extend deployment timelines. Without concessional financing or grant support, cost barriers can defer projects and temper traffic signal controller market expansion.

Cyber-Security and Data-Privacy Risks

As controllers connect to cloud management layers, their attack surfaces grow. Federal Highway Administration research identified some vulnerable traffic sensors worldwide capable of being hijacked to create stop-go waves and emergency routing chaos. Proof-of-concept hacks show that altering a few phase parameters can congest an entire network within minutes. Consequently, the ATC Cybersecurity Project is drafting hardened firmware and authentication guidelines that raise baseline capital costs. European General Data Protection Regulation rules add further complexity by classifying vehicle probe data as personal information. Agencies, therefore, demand NIST-aligned encryption, two-factor authentication, and remote kill-switch capabilities in new tenders. Vendors unable to demonstrate robust cyber controls risk exclusion from high-value procurement processes, constraining their traffic signal controller market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Actuated Systems Lead Despite Adaptive Growth

Actuated/phase-based controllers held 47.62% of the traffic signal controller market in 2025, supported by decades-long reliability and a large installed base favoring incremental upgrades. Their relatively modest price points and compatibility with inductive loop detectors align with municipality budgets pursuing gradual modernisation. In contrast, adaptive/intelligent models are forecast to record 12.22% CAGR through 2031 as city agencies prioritise dynamic optimisation that lowers delays without widening roads. Technological advancements now overlay cloud analytics onto traditional actuated hardware, extending service life while adding AI functions. Emerging controllers embed GPU modules to execute reinforcement-learning algorithms, enabling the transition from reactive phase selection to predictive split optimisation.

By Technology: AI-Powered Systems Transform Traditional Approaches

Fully actuated technology captured a 38.92% share of the traffic signal controller market in 2025, reflecting its role as the default standard for intersections equipped with vehicle detection. Pre-timed cycles continue in secondary streets, where flow remains predictable. Semi-actuated solutions handle peak-period variability for suburban arterials. AI-powered adaptive controllers, however, deliver the best growth outlook at 12.87% CAGR thanks to measurable outcomes. Taipei’s night-time optimisation yielded 35% shorter waits and TWD 1.83 million annual benefits per intersection. Edge compute allows latency-sensitive decisions to be made locally, while cloud dashboards offer macro-level coordination. These architectures enable agencies to pivot from reactive to self-learning operations, solidifying AI as the technological fulcrum of the traffic signal controller market development.

By Installation Environment: Urban Dominance Faces Highway Challenge

Urban intersections accounted for 57.64% of the traffic signal controller market share in 2025, reflecting the sheer density of signalised junctions in metropolitan cores. Multimodal pressures—buses, cyclists, and pedestrians—drive demand for advanced phasing logic, transit priority, and pedestrian scramble capabilities. Highway and expressway corridors, though traditionally governed by ramp meters rather than full controllers, are forecast to register 11.12% CAGR as agencies adopt coordinated signal systems along suburban arterials feeding regional freeways. The USD 60 million V2X corridor grants awarded in 2024 illustrate this shift, funding Arizona and Texas projects that synchronise interchange ramps with mainline flow for smoother throughput. As inter-urban travel rebounds, coordinated highway solutions ensure that the traffic signal controller market growth expands beyond inner-city boundaries to wide-area networks.

By Communication Interface: Wired Systems Yield to Cellular Innovation

Wired will still constitute 50.54% of controller communication links in 2025 because of its proven uptime and bandwidth advantages. Serial connections linger in legacy networks where capital for fibre upgrades remains scarce. The momentum, however, swings toward Cellular-V2X, forecast to post a 12.41% CAGR to 2031. Direct vehicle-infrastructure messaging eliminates the need for roadside units, reducing deployment costs and enabling speed harmonisation. Independent studies show potential 15% delay savings and 8% fuel reductions when phase selection incorporates probe vehicle data. Wi-Fi and mesh solutions serve campus and event applications requiring rapid setup. Over time, dual-mode radios capable of Ethernet backhaul plus 5G sidelink are expected to dominate new orders, ensuring the traffic signal controller market evolves in tandem with connected vehicle penetration.

By End User: Municipal Agencies Face Smart-City Integrator Competition

Municipal traffic departments commanded 64.05% of 2025 revenues as they own most signalised intersections worldwide. Their procurement often follows five-year replacement cycles, tightly coupled to capital budgets. Smart-city integrators, however, are the fastest-expanding customer group at 12.79% CAGR, benefitting from design-build-operate contracts that bundle connectivity, SCADA, and urban analytics layers with signal control. The SMART grants scheme channels funds to integrators able to deliver multi-domain projects, including environmental sensors and curb-side management, alongside traditional signal hardware. Highway agencies adopt corridor solutions to meet freight-mobility targets, while private industrial parks specify bespoke control to manage shift-change peaks. This diversification redistributes bargaining power toward service-oriented firms that orchestrate complex ecosystems, reshaping value pools within the traffic signal controller industry.

Geography Analysis

North America led with 36.95% of the traffic signal controller market revenue in 2025, supported by predictable federal programmes such as the USD 54 million SMART grants allocated to intelligent signal projects. Mature asset-management frameworks allow rapid disbursement, and the Biden-Harris Administration’s infrastructure law secures multiyear funding. Canadian provinces complement federal actions through regional smart-corridor schemes synchronizing cross-border freight flows. The result is continuous upgrade activity, with agencies migrating from legacy NEMA cabinets to ATC cyber-secure platforms.

Asia-Pacific is the fastest-growing region at 12.92% CAGR to 2031. The Asian Development Bank’s projection of USD 43 trillion in transport investments, of which 63% targets road networks, underscores the scale of opportunity. China’s national smart-city programme funds AI controllers across tier-two urban clusters, while India’s Smart Cities Mission accelerates tenders for adaptive signals that cut congestion without land acquisition. Japan, Singapore, and South Korea exploit domestic semiconductor capacity to pilot V2X-ready systems ahead of commercial vehicle rollouts. Collectively, these initiatives enlarge the traffic signal controller market faster than in any other geography.

Europe maintains a steady trajectory driven by climate legislation that prioritises traffic optimisation as a carbon-reduction lever. Cities deploying low-emission zones turn to adaptive phasing to prevent rerouted flows from creating new hotspots. The July 2024 acquisition of Ireland’s Elmore Group by SWARCO bolsters regional consolidation, offering agencies pan-European service coverage. The United Kingdom deploys dynamic traffic management funded by GBP 0.999 million national grants, and Nordic countries digitise arterial networks to support connected-autonomous tests. Cyber-security regulations such as NIS-2 raise procurement hurdles but also favour vendors with proven security credentials, sustaining premium pricing within the traffic signal controller market.

Competitive Landscape

The traffic signal controller market displays moderate concentration dominated by Siemens Mobility, Yunex Traffic and SWARCO, each leveraging acquisition strategies to extend geographic reach and product breadth. Yunex, now under Atlantia, deploys the Stratos UTMC suite that Lancashire installed in December 2024 to manage citywide congestion, demonstrating the firm’s ability to integrate software with roadside hardware.

SWARCO follows an expansion pathway centred on regional bolt-ons; the July 2024 purchase of Ireland’s Elmore Group augmented its European intelligent transportation portfolio and added service capacity in Western Europe. Earlier acquisitions of McCain and Dynniq strengthened SWARCO’s foothold in North America and Benelux, evidencing a deliberate strategy to secure local maintenance bases that agencies value for uptime guarantees. Competitors such as Econolite and Trafficware focus on NEMA cabinets for the United States but increasingly partner with AI analytics start-ups to remain relevant as software differentiates bids.

Technology competition now tilts toward edge AI, V2X readiness and cyber hardening rather than metal enclosures. Vendors incorporate Trusted Platform Modules and zero-trust architectures to satisfy FHWA’s ATC Cybersecurity Project guidelines. Strategic alliances with cellular operators underpin 5G-V2X pilots, while open-API controllers invite third-party algorithm developers, creating an ecosystem play. White-space opportunities persist in emerging markets where infrastructure commitments outstrip current supplier capacity, allowing medium-sized regional firms to secure early mover status. Overall, differentiation hinges on software agility and security assurance, themes that will continue to shape future traffic signal controller market share.

Traffic Signal Controller Industry Leaders

Siemens Mobility

Econolite

SWARCO

Q-Free ASA

Sumitomo Electric Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Yunex Traffic deployed its Stratos UTMC system in Lancashire, enhancing urban traffic management through network-wide adaptive control.

- December 2024: The United States Department of Transportation announced USD 130 million in SMART Grants funding for 23 states, with smart traffic signal technologies receiving a dedicated allocation.

- October 2024: The Biden-Harris Administration awarded over USD 96 million in advanced technology grants for projects including Florida’s adaptive signal upgrades and Texas’ V2X corridor deployment.

Global Traffic Signal Controller Market Report Scope

A traffic signal controller refers to an automated system that regulates the sequence and timing of traffic lights by monitoring the demand of automobiles and pedestrians. These controllers use sensors and timers to determine when to change the traffic light, allowing for smooth movement of vehicles through the intersections and helping to reduce traffic congestion, improve safety, and increase the overall efficiency of the transportation network.

The market is segmented into product type and geography. By product type, the market is segmented into interval controllers, phase controllers, and adaptive controllers. By geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World.

For each segment, the market sizing and forecast have been done based on value (USD).

| Interval / Pre-timed Controllers |

| Actuated / Phase Controllers |

| Adaptive / Intelligent Controllers |

| Centralised Cloud Controllers |

| Solar-powered Controllers |

| Pre-timed Fixed-Cycle |

| Semi-actuated |

| Fully-actuated |

| AI-powered Adaptive |

| Edge-compute Enabled |

| Urban Intersections |

| Highways & Expressways |

| Pedestrian Crosswalks & School Zones |

| Parking Facilities & Campuses |

| Public-transport Priority Corridors |

| Wired (Ethernet / Serial) |

| Wireless (Wi-Fi / Cellular) |

| DSRC |

| Cellular-V2X |

| Municipal & City Traffic Agencies |

| Highway & Transport Departments |

| Smart-city Integrators & EPCs |

| Private Industrial Parks & Campuses |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Interval / Pre-timed Controllers | |

| Actuated / Phase Controllers | ||

| Adaptive / Intelligent Controllers | ||

| Centralised Cloud Controllers | ||

| Solar-powered Controllers | ||

| By Technology | Pre-timed Fixed-Cycle | |

| Semi-actuated | ||

| Fully-actuated | ||

| AI-powered Adaptive | ||

| Edge-compute Enabled | ||

| By Installation Environment | Urban Intersections | |

| Highways & Expressways | ||

| Pedestrian Crosswalks & School Zones | ||

| Parking Facilities & Campuses | ||

| Public-transport Priority Corridors | ||

| By Communication Interface | Wired (Ethernet / Serial) | |

| Wireless (Wi-Fi / Cellular) | ||

| DSRC | ||

| Cellular-V2X | ||

| By End User | Municipal & City Traffic Agencies | |

| Highway & Transport Departments | ||

| Smart-city Integrators & EPCs | ||

| Private Industrial Parks & Campuses | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the traffic signal controller market and how fast is it growing?

The market is valued at USD 6.44 billion in 2026 and is forecast to reach USD 11.54 billion by 2031, registering a 12.38% CAGR.

Which end-user segment holds the largest share?

Municipal and city traffic agencies account for 64.05% of 2025 revenue, reflecting their ownership of most signalised intersections.

Which technology segment is expanding the quickest?

AI-powered adaptive controllers are the fastest-growing technology, advancing at a 12.87% CAGR through 2031.

Which region offers the highest growth potential?

Asia-Pacific is projected to grow at 12.92% CAGR, supported by USD 43 trillion in planned transport infrastructure spending through 2035.

What are the main drivers propelling market demand?

Urban congestion, government funding programmes such as the U.S. SMART Grants, and the shift toward AI-enabled, V2X-ready systems are the primary growth catalysts.

How significant are cyber-security risks in new deployments?

Some of the vulnerable traffic sensors have been identified worldwide, prompting agencies to mandate hardened firmware and zero-trust architectures in procurement specifications.

Page last updated on: