Mechanical Control Cables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

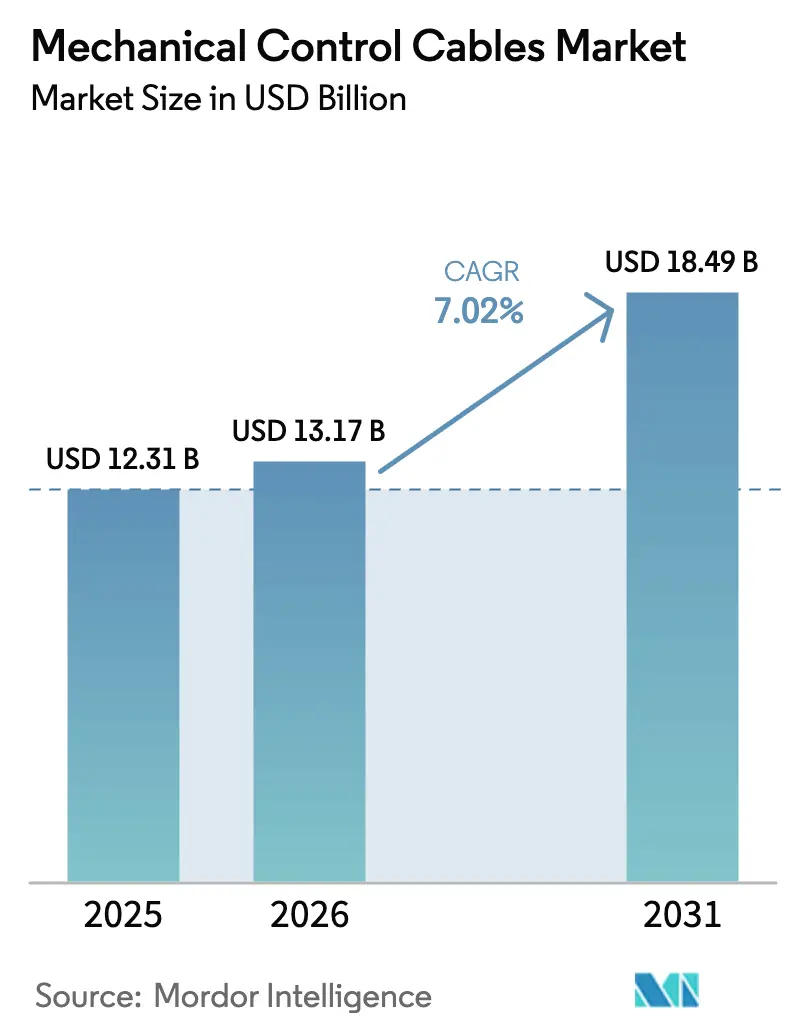

| Market Size (2026) | USD 13.17 Billion |

| Market Size (2031) | USD 18.49 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

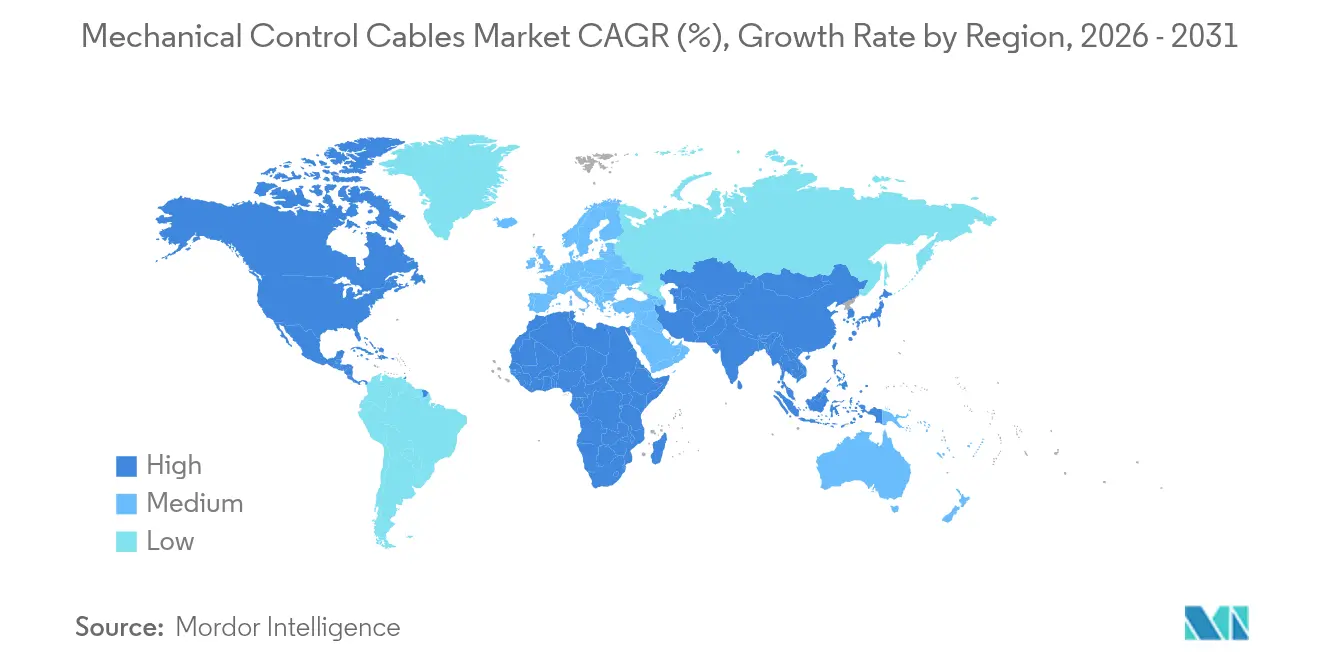

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

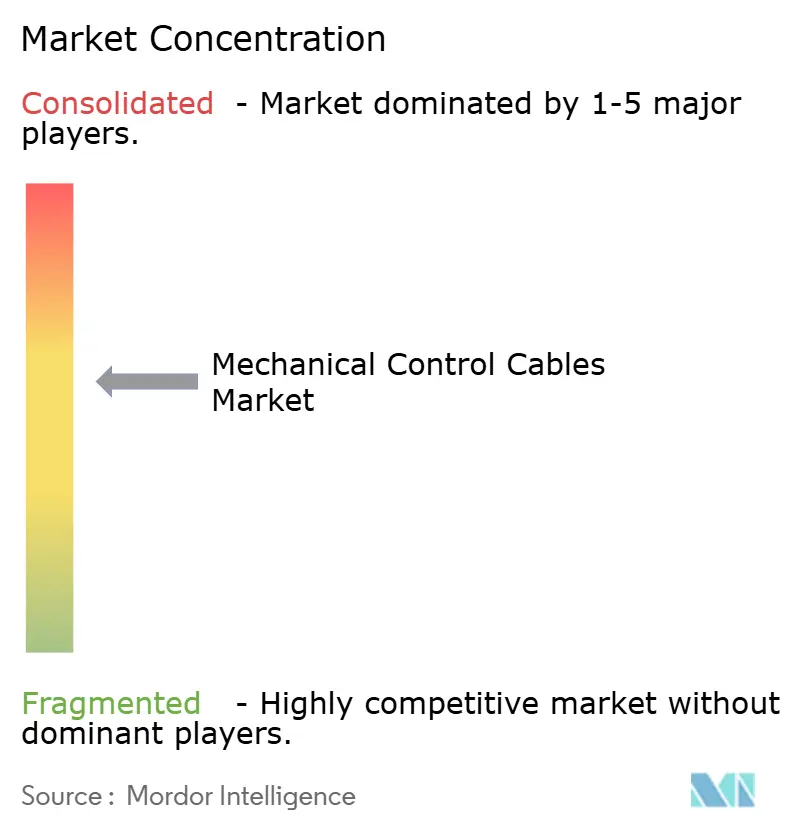

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mechanical Control Cables Market Analysis by Mordor Intelligence

Mechanical Control Cables Market size in 2026 is estimated at USD 13.17 billion, growing from 2025 value of USD 12.31 billion with 2031 projections showing USD 18.49 billion, growing at 7.02% CAGR over 2026-2031. Growth rests on the continuing preference for fail-safe mechanical linkages in sectors that cannot tolerate single-point electronic failure, such as advanced air mobility, medical robotics, and electrified off-highway machinery. Miniaturization in exoskeletons and precision robots, combined with electrification trends that still require mechanical redundancy, keeps product demand robust. Composite and hybrid materials register strong traction as aerospace and defense programs demand lighter yet stronger components.

Key Report Takeaways

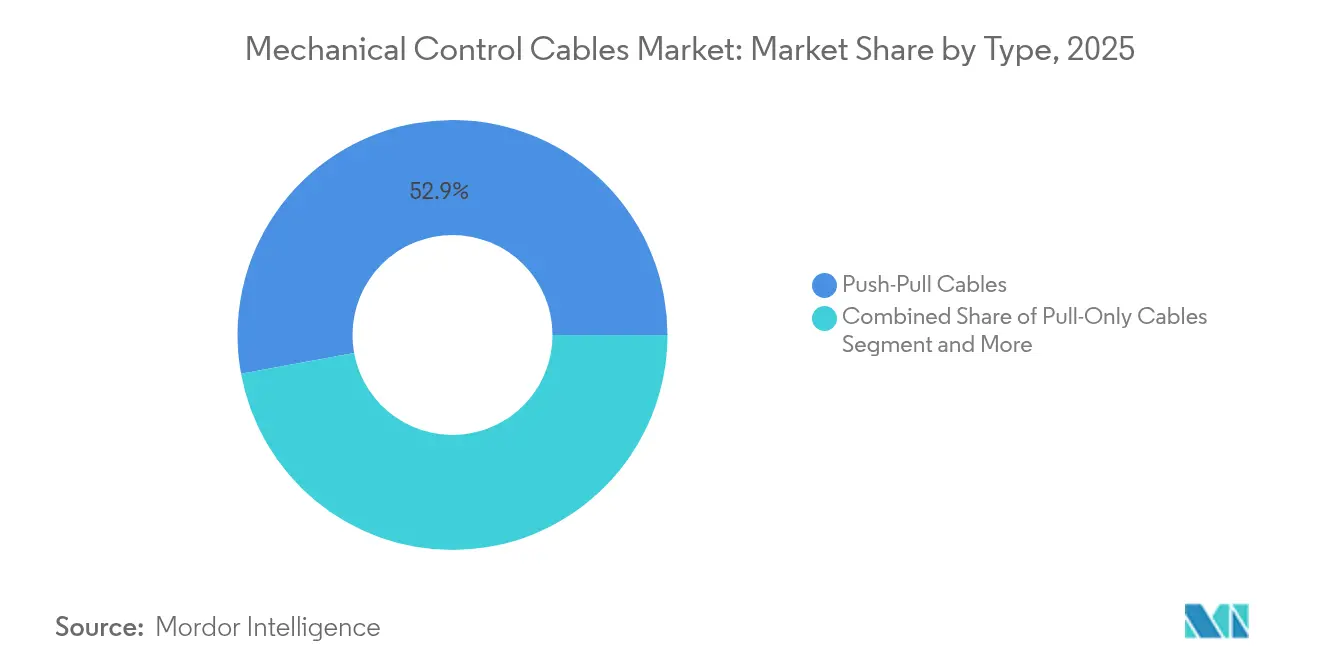

- By cable type, push-pull versions led with 52.89% revenue share in 2025; micro-diameter variants are expanding at a 7.43% CAGR through 2031.

- By end user, automotive held 40.74% of the mechanical control cables market share in 2025, whereas medical devices and exoskeletons are advancing at a 7.29% CAGR to 2031.

- By material, stainless-steel accounted for 46.55% of the mechanical control cables market size in 2025, while composite and hybrid alternatives are growing at a 7.55% CAGR to 2031.

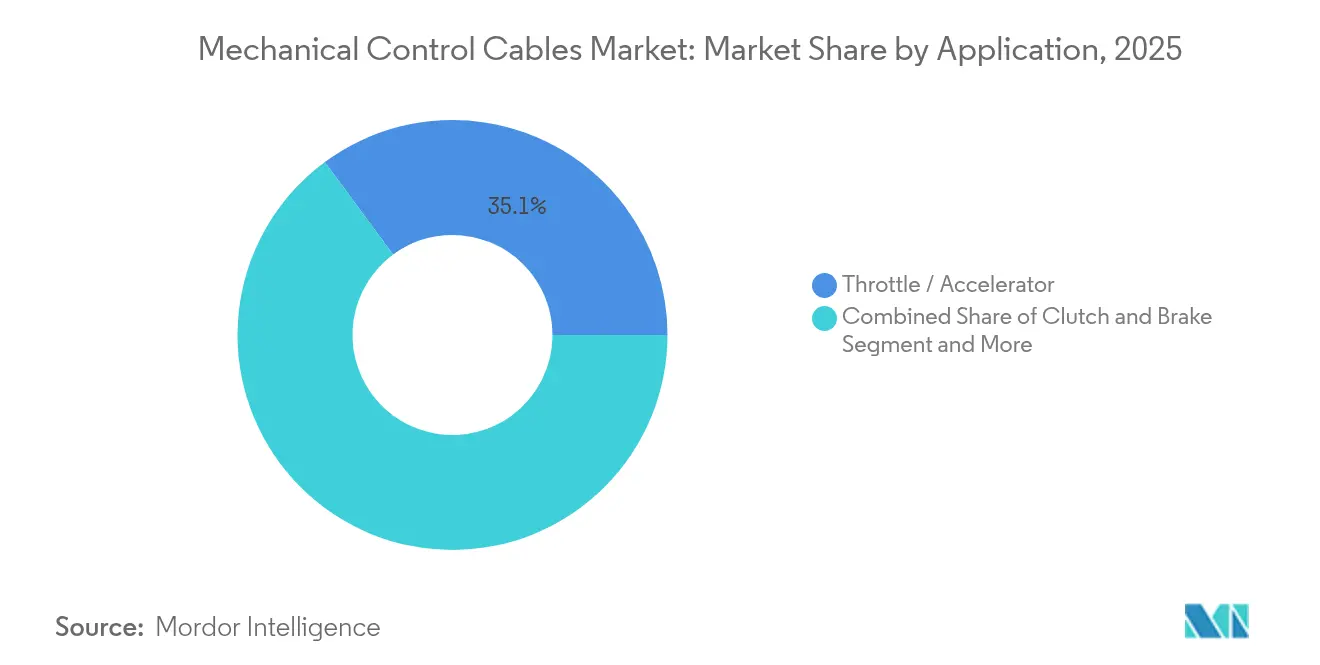

- By application, throttle and accelerator assemblies captured 35.12% of the overall market in 2025; remote valve and actuator control is projected to post an 8.12% CAGR between 2026 and 2031.

- By geography, Asia-Pacific contributed 37.21% of 2025 revenue; Africa is forecast to be the fastest-growing region at a 6.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mechanical Control Cables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand in automotive sector | +1.8% | Global, with APAC core concentration | Medium term (2-4 years) |

| Rising industrial automation | +1.5% | APAC core, spill-over to North America & EU | Long term (≥ 4 years) |

| Growth in commercial aerospace & defense | +1.2% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Electrification of off-highway machinery | +0.9% | Global, with early gains in North America, EU | Medium term (2-4 years) |

| Rapid adoption of eVTOL aircraft | +0.8% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Precision agriculture equipment retrofits | +0.6% | Global, with concentration in North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Automotive Demand for Hybrid Mechanical–Electronic Systems

Automotive OEMs continue to specify mechanical control cables for throttle, brake, and clutch functions where cost and reliability outweigh the benefits of full drive-by-wire controls. Electrified platforms amplify the need for mechanical redundancy that maintains vehicle operability during powertrain or software outages, keeping the mechanical control cables market firmly embedded in product development roadmaps. Push-pull cables remain the preferred format for this class of applications, especially in cost-sensitive segments across Asia-Pacific and Africa.

Industrial Automation and Material-Handling Expansion

Automated factories across China, India, and Southeast Asia invest in mixed architectures that pair high-precision servo drives with mechanical backups for critical positioning. Material-handling lines, packaging systems, and pharmaceutical clean-room equipment integrate micro-diameter cables to guarantee movement even when electronic controls are offline for maintenance. The mechanical control cables market benefits because such redundancy meets ISO 13849 safety levels without imposing disproportionate cost. Increasing labor costs in manufacturing hubs further encourage automation, yet operators still demand simple, maintainable fail-safe mechanisms that only mechanical links can deliver.

Higher Commercial Aerospace and Defense Outlays

Stringent certification rules in commercial aircraft mandate dual or triple redundant control paths. Mechanical cables therefore continue as an indispensable secondary system even on fly-by-wire platforms. In parallel, defense programs specify ruggedized stainless-steel or composite cores capable of withstanding electromagnetic pulses and battlefield vibration extremes. Composite carbon fiber reinforced polymer (CFRP) cables reduce mass while sustaining fatigue life, pushing the mechanical control cables market toward higher-margin aerospace grades. New eVTOL prototypes also integrate micro-gauge cables for back-up actuation to secure airworthiness approval.[1]European Union Aviation Safety Agency, “Special Condition: eVTOL SC-VTOL-01,” easa.europa.eu

Electrification of Off-Highway Machinery

Construction and agricultural equipment shift to electric and hybrid drivetrains to meet emission regulations, yet OEMs retain mechanical implements to guarantee immediate, forceful response under heavy loads. Three-point hitch systems and front-loader assemblies still rely on cables to initiate hydraulic valve movement. Precision farming technology, reliant on GNSS-guided implements, demands positional accuracy unimpeded by software lag, reinforcing the need for direct mechanical feedback loops. The practice safeguards uptime, which is critical during fixed planting and harvesting windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward drive-by-wire & electric actuation | -1.4% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Volatility in stainless-steel | -0.8% | Global, with manufacturing concentration in APAC | Short term (≤ 2 years) |

| Recyclability mandates limiting PTFE-lined housings | -0.5% | EU & North America, expanding globally | Long term (≥ 4 years) |

| Miniaturization limits in micro-robotics applications | -0.3% | Global, with R&D concentration in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to Drive-by-Wire and Electric Actuation

Premium passenger vehicles now specify electronic steering, braking, and throttle assemblies that remove most mechanical linkages, trimming demand in higher-margin markets. Regulatory incentives for advanced driver assistance and connectivity further entrench full electronic control. Where drive-by-wire becomes standard, cable content falls sharply, particularly in throttle assemblies that represented 35.47% of 2024 application revenue. Nevertheless, functional safety standards such as ISO 26262 continue to mandate some mechanical fail-safe capability, preventing complete elimination.

Stainless-Steel and Specialty Alloy Price Volatility

Nickel price swings influence stainless-steel rod costs, directly impacting 47.11% of 2024 cable material demand. Quarterly spikes disrupt contract pricing with automotive Tier-1 suppliers, compressing margins and delaying capacity additions. Asia-Pacific producers face additional foreign-exchange exposure when importing alloying elements, intensifying cost uncertainty. These dynamics encourage a gradual pivot toward composite substitutes, but the switch remains constrained by certification timelines in aerospace and medical applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Push-Pull Versatility Sustains Dominance

Push-pull designs accounted for 52.89% of 2025 revenue, reflecting unmatched versatility across throttle, clutch, and directional control. The mechanical control cables market size for push-pull products was USD 6.51 billion in 2025, with demand anchored in automotive throttle assemblies and industrial machinery that favors simple bidirectional motion. Pull-only variants serve marine shift control and aerospace trim applications where force transmission in a single direction suffices.

Micro-diameter products, while starting from a lower base, are projected to notch the fastest 7.43% CAGR because robotic surgical instruments and exoskeleton joints need cables under 2 mm diameter with consistent tensile strength. Precision-ground stainless-steel or Ni-Ti alloys wrapped in low-friction PTFE sleeves allow repeatable micro-motions in confined spaces without electronic drift or overheating. The trend underscores OEM preference for physical redundancy in surgical systems, sustaining growth even as electromechanical drives proliferate.

By End User: Automotive Still Leads but Healthcare Accelerates

Automotive retained 40.74% of 2025 revenue, yet growth moderates to a mid-single-digit pace as electronic architectures expand. In contrast, medical devices and exoskeletons exhibit a 7.29% CAGR and are set to capture an outsized share of the mechanical control cables market size by 2031. Rehabilitation robotics, powered orthoses, and minimally invasive surgery rigs rely on micro-cables that emulate tendon behavior.

Demand is further propelled by an aging population and extended post-operative care that drive uptake of assistive mobility systems. Aerospace and defense remain stable end-users given airworthiness rules, while industrial machinery continues to adopt hybrid control schemes that blend servo accuracy with mechanical post-fail positioning. The mechanical control cables industry therefore sees portfolio balancing, with suppliers broadening into medical and aerospace channels to offset softer automotive growth in highly digitized regions.

By Application: Throttle Control Faces Remote Actuator Upside

Throttle and accelerator assemblies contributed 35.12% of 2025 demand. Continuous engine downsizing and turbo integration, however, push OEMs toward electronic throttle control, pressuring future cable volumes. Remote valve and actuator control grows at an 8.12% CAGR as process industries and energy platforms require dependable back-up actuation capable of maintaining flow in blackout conditions.

Rising investments in LNG terminals, chemical processing, and offshore platforms place a premium on corrosion-resistant, low-maintenance solutions. Composite-sheathed stainless-steel cores extend service life in salt-spray environments, ensuring operational continuity when electronic supervisory controls are offline. The mechanical control cables market therefore shifts toward higher specialized content with stronger margins even as traditional throttle systems plateau.

By Material: Stainless-Steel Holds but Composites Surge

Stainless-steel continues to dominate because its corrosion resilience and fatigue life exceed cheaper carbon-steel options. Yet composites post 7.55% CAGR due to double-digit weight-saving targets in next-generation aircraft and high-cycle robotics. Carbon fiber reinforced polymer models supply equivalent tensile performance at roughly half the mass, which translates directly into fuel or payload advantages.

Hybrid formats, where a metallic core delivers conductivity and a composite overbraid supplies strength, are gaining certification in aerospace control surfaces and medical haptic devices. CNT-infused laminates display specific modulus values close to 256 GPa/(g cm–3), topping legacy carbon fiber panels and extending product life curves. Cost barriers remain, but with nickel and chromium volatility, composite price parity is closing, reshaping long-term material sourcing strategies within the mechanical control cables market.

Geography Analysis

Asia-Pacific generated 37.21% of 2025 revenue, powered by high-volume automotive output in China, Japan, and India. Regional industrialization, combined with a 9% CAGR projection for MedTech manufacturing through 2030, anchors sustained offtake. Government incentives for domestic electric vehicle supply chains further stimulate cable demand in battery pack actuators and thermal-management subsystems.

North America and Europe form mature yet lucrative markets because aerospace, defense, and precision agriculture activities mandate top-tier reliability. Composite and hybrid materials gain earlier acceptance here, enabling suppliers to command stronger margins despite volume plateaus. Regulatory safety frameworks also require mechanical back-ups, guaranteeing a baseline replacement cycle for critical applications.

Africa, though starting from a smaller base, logs the mechanical control cables market’s fastest regional expansion at 6.55% CAGR. Automotive assembly corridors in Morocco, South Africa, and Egypt take advantage of regional trade protocols, stimulating localized cable production and lowering import duties. Infrastructure projects in mining and power distribution necessitate ruggedized actuation solutions capable of functioning in dust-laden or high-humidity conditions where electronic sensors fail prematurely.

Competitive Landscape

The market shows moderate fragmentation. HI-LEX Corporation ships more than 30 million units yearly across global auto programs, benefiting from vertically integrated rod drawing and plastic extrusion lines.[2]HI-LEX Corporation, “Corporate Profile 2025,” hi-lex.co.jp Suprajit Engineering vaulted into the top tier by purchasing Germany-based Stahlschmidt Group and now supplies light-vehicle cables across 50 countries.[3]Suprajit Engineering, “Investor Presentation FY 2025,” suprajit.com

Strategic moves trend toward automated, traceable production cells that deliver Six Sigma level defect rates. DIN 72036, approved in June 2024, standardizes fully automated cable harness assembly, allowing first movers to guarantee tighter tolerances and faster model changeovers. Composite capability is emerging as a key differentiator; firms that master CFRP or CNT processes secure aerospace contracts with life-of-program value streams stretching 15 years or more.

Material cost volatility and PFAS compliance drive in-house polymer compounding and recycling initiatives. Suppliers located near stainless-steel mills in Japan or India hedge alloy exposure, while European players partner with chemical producers to formulate fluorine-free liners. Such vertical moves temper price shocks and satisfy forthcoming EU recyclability directives, positioning incumbents to defend share in a tightening regulatory climate.

Mechanical Control Cables Industry Leaders

Orscheln Products

Bergen Cable Technology

Grand Rapids Controls, LLC

Carl Stahl Sava Industries, Inc.

Cablecraft Motion Controls

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Leoni unveiled liquid-cooled high-voltage cable sets for automated trucks under the ATLAS-L4 project, cutting system mass and enabling faster charging.

- June 2024: Sumitomo Electric acquired a 51% stake in Südkabel for EUR 90 million (USD 97 million) to expand 525 kV HVDC capability supporting Germany’s net-zero grid build-out.

- June 2024: Sumitomo Electric Bordnetze SE broke ground on a highly automated wiring plant in Cuenca, Spain, to supply Volkswagen Group EV models beginning in 2025.

Global Mechanical Control Cables Market Report Scope

A mechanical control cable is a flexible assembly designed to transmit mechanical force or energy between componenets in machinery or vehicles. It typically comprises an inner cable, often made of steel, that moves within an outer protective sheath. This configuration allows for the precise transfer of push, pull or rotational forces over a distance, facilitating remote operation of mechanisms such as throttles, brakes, or gear shifts.

The study tracks the revenue generated from the sale of mechanical control cables by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The mechanical control cables market is segmented by type (push-pull cables, pull-only cables), end-user vertical (automotive, aerospace and defense, marine, industrial, agriculture, construction), and geography (north america, europe, asia-pacific, latin america, and middle east and africa). The market sizes and forecasts are provided in terms of value (usd) for all the above segments.

| Push-Pull Cables |

| Pull-Only Cables |

| Self-Locking / Positive-Lock Cables |

| Micro-Diameter Cables |

| Automotive |

| Aerospace & Defense |

| Marine |

| Industrial Machinery |

| Construction & Off-Highway Equipment |

| Agriculture Equipment |

| Medical Devices & Exoskeletons |

| Throttle / Accelerator |

| Clutch & Brake |

| Door / Latch / Seat Control |

| Remote Valve & Actuator Control |

| Carbon-Steel |

| Stainless-Steel |

| Nickel & Specialty Alloys |

| Composite / Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia & New Zealand | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Type | Push-Pull Cables | |

| Pull-Only Cables | ||

| Self-Locking / Positive-Lock Cables | ||

| Micro-Diameter Cables | ||

| By End-User | Automotive | |

| Aerospace & Defense | ||

| Marine | ||

| Industrial Machinery | ||

| Construction & Off-Highway Equipment | ||

| Agriculture Equipment | ||

| Medical Devices & Exoskeletons | ||

| By Application | Throttle / Accelerator | |

| Clutch & Brake | ||

| Door / Latch / Seat Control | ||

| Remote Valve & Actuator Control | ||

| By Material | Carbon-Steel | |

| Stainless-Steel | ||

| Nickel & Specialty Alloys | ||

| Composite / Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia & New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current mechanical control cables market size?

The market is valued at USD 13.17 billion in 2026 and is projected to grow to USD 18.49 billion by 2031.

Which region leads mechanical control cable demand?

Asia-Pacific leads with 37.21% revenue share due to its large automotive and industrial base.

Which cable type holds the highest market share?

Push-pull cables dominate with 52.89% of 2025 revenue due to versatility across throttle, clutch, and industrial controls.

What is the fastest-growing end-user segment?

Medical devices and exoskeletons are forecast at a 7.29% CAGR because miniaturized micro-cables enhance surgical and mobility equipment.

How are composite materials influencing the market?

Composite and hybrid constructions, especially CFRP cables, are expanding at a 7.55% CAGR as aerospace and robotics seek lighter, high-strength alternatives.

Why does electrification still need mechanical cables?

Even in electrified vehicles and off-highway machinery, mechanical cables provide critical fail-safe actuation when electronic systems lose power or face software faults.

Page last updated on: