Time-of-Flight (TOF) Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

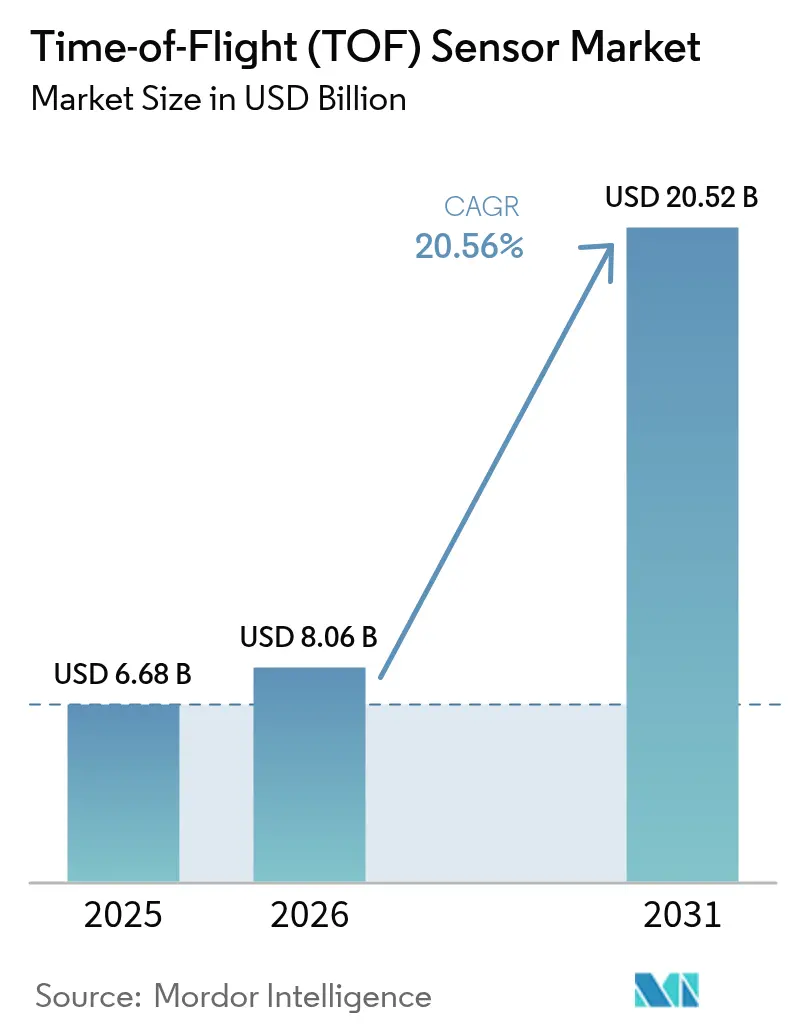

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 20.52 Billion |

| Growth Rate (2026 - 2031) | 20.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players_Sensor_Market_.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Time-of-Flight (TOF) Sensor Market Analysis by Mordor Intelligence

The global Time-of-Flight sensor market size was valued at USD 6.68 billion in 2025 and estimated to grow from USD 8.06 billion in 2026 to reach USD 20.52 billion by 2031, at a CAGR of 20.56% during the forecast period (2026-2031). Rising demand for high-accuracy depth perception in smartphones, driver-monitoring cameras mandated by EU General Safety Regulation 2026, and machine-vision upgrades in European and Japanese factories keep capital flowing into new production lines. Smartphone producers in China and South Korea are pivoting from indirect to direct Time-of-Flight architectures to power computational photography, while North American logistics operators adopt depth cameras to orchestrate robot fleets at scale. Investments in SPAD-based miniaturization, meta-optics, and low-power VCSEL emitters are shrinking module footprints, letting handset makers fit sub-6 mm camera islands without compromising range. Supply-chain concentration around VCSEL wafers in the Taiwan-US corridor and the need to mitigate multipath interference in outdoor LiDAR form the chief technical and commercial headwinds for the Time-of-Flight sensor market.

Key Report Takeaways

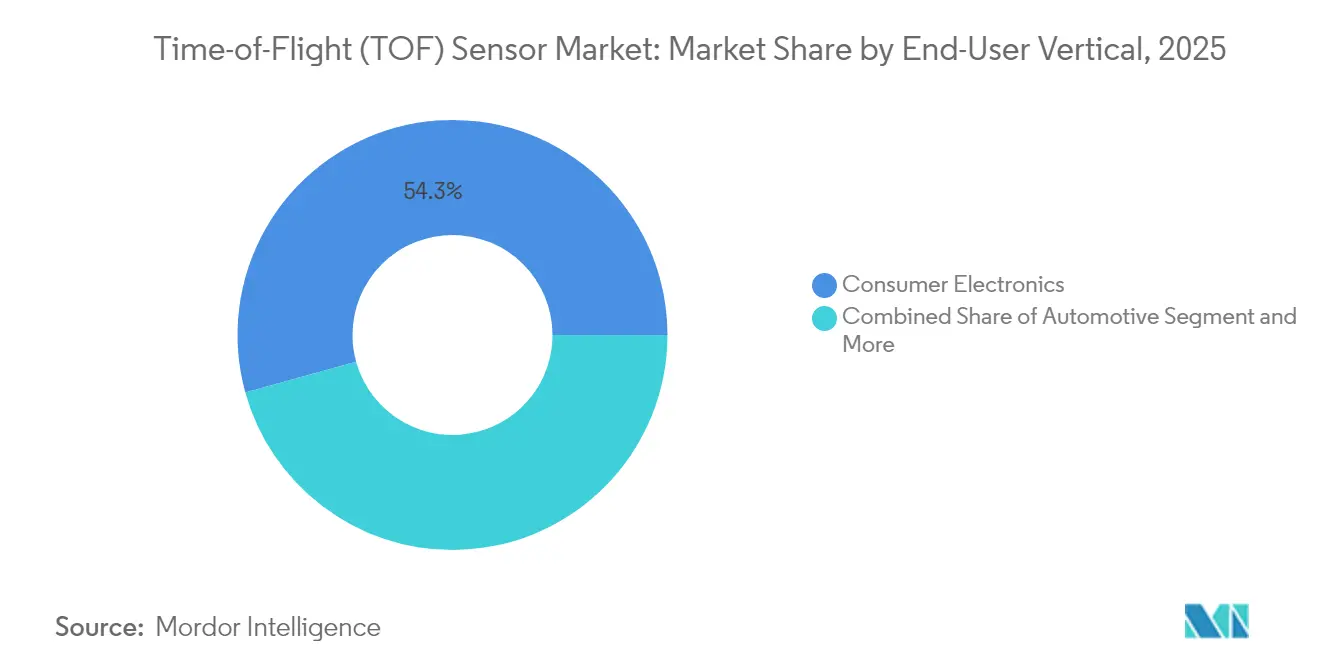

- By end-user, consumer electronics led with 54.30% revenue share in 2025; automotive is advancing at a 24.4% CAGR through 2031.

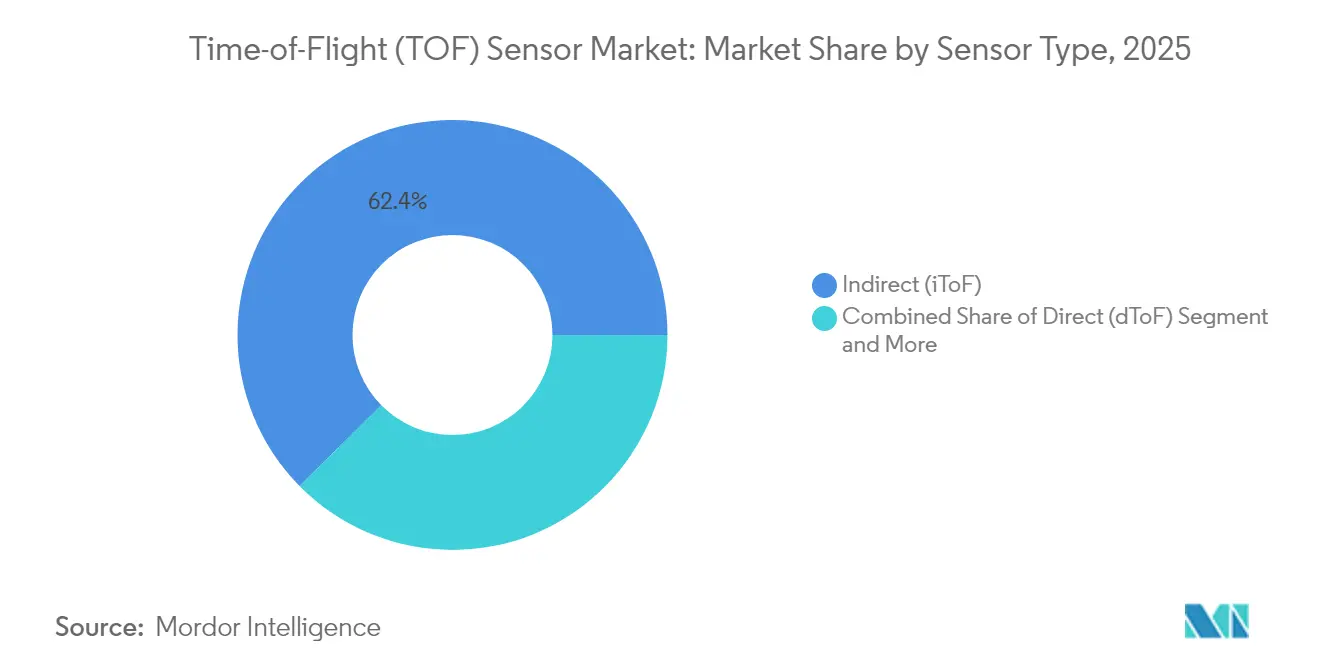

- By sensor type, indirect ToF captured 62.40% of the Time-of-Flight sensor market share in 2025, while direct ToF is projected to climb at a 22.6% CAGR to 2031.

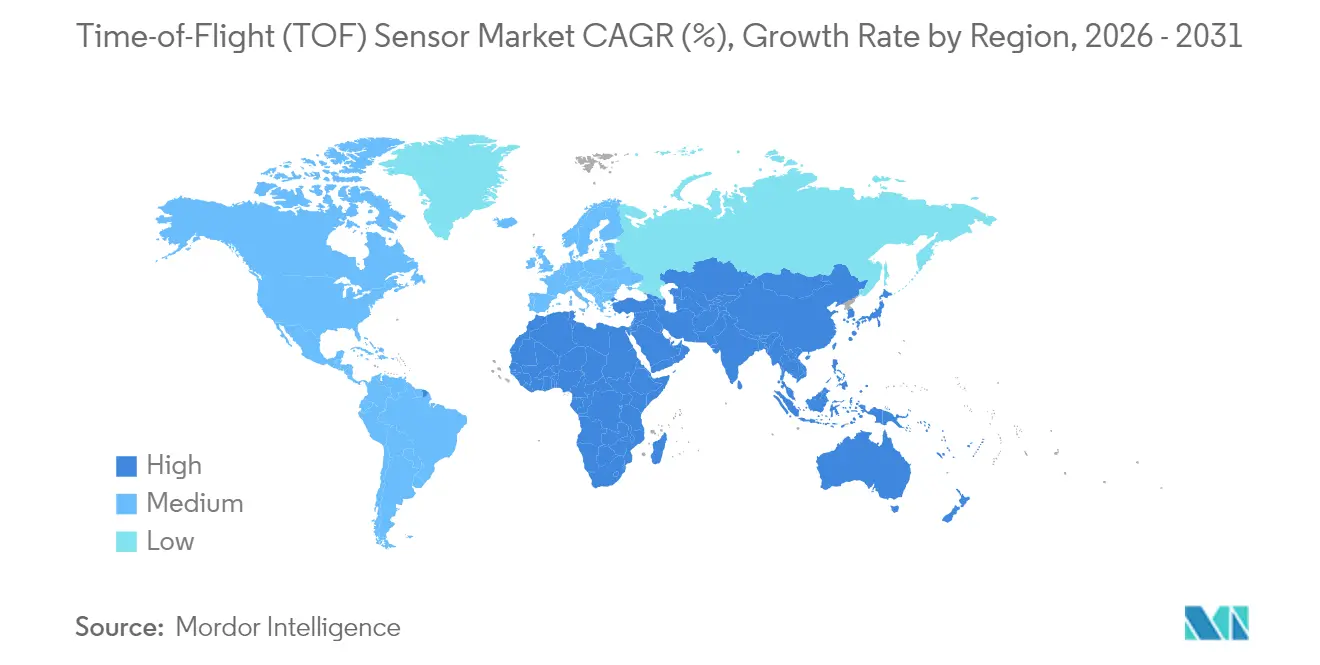

- By region, Asia-Pacific held 51.60% of the Time-of-Flight sensor market in 2025; the Middle East is set to expand at a 25.9% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Time-of-Flight (TOF) Sensor Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Adoption of Machine Vision Systems Across Manufacturing Hubs in Europe and Japan | +3.2% | Europe and Japan, spill-over to APAC | Medium term (2-4 years) |

| Rising Demand for Smartphones Integrating dToF 3-D Cameras in China and South Korea | +4.1% | China and South Korea, global smartphone market | Short term (≤ 2 years) |

| Integration of dToF LiDAR for Level-3+ ADAS Roll-outs in EU and U.S. | +3.8% | EU & U.S., expanding to global automotive | Medium term (2-4 years) |

| Miniaturization of SPAD-Based ToF Modules Enabling Sub-6 mm Camera Islands | +2.9% | Global, led by premium smartphone segment | Short term (≤ 2 years) |

| Warehouse Automation Push Elevating iToF Depth Cameras in North-American Logistics | +2.7% | North America, expanding to global logistics | Medium term (2-4 years) |

| Government-Mandated Driver-Monitoring Systems under EU GSR-2026 | +3.5% | EU, influencing global automotive standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of machine-vision systems in Europe and Japan

Industrial clusters in Germany, Italy, and Japan are equipping robots with Time-of-Flight imagers to improve bin-picking and random-order depalletizing. Nikon’s robot-vision package, shipping since late 2024, streams 250 fps depth frames, cutting cycle time for automotive stamping lines.[1]Nikon Corporation, “Nikon Releases Industrial Robot Vision System,” nikon.com Japanese integrators now couple these sensors with private 5 G to stop machines instantly when intrusion is detected, an approach validated by Tokyo Boeki and Net One Systems in 2025. As labor shortages worsen and EU factories upgrade to Industry 4.0 standards, the Time-of-Flight sensor market expects steady purchase orders for mid-range iToF arrays.

Rising demand for dToF 3-D smartphone cameras in China and South Korea

Samsung’s Galaxy S24 Ultra debuted a refined dToF module that improves bokeh accuracy and AR anchoring, reinforcing the shift from structured-light to direct ToF in flagships. Chinese OEMs mirror this move to differentiate imaging, and analysts see smartphone 3-D camera revenues climbing to USD 44.01 billion by 2030.[2]Electro Optics, “ST Releases First 3D Sensor with Meta-Optics,” electrooptics.com Because handset refresh cycles are short, every design win lifts annual unit volumes, magnifying the contribution of mobile shipments to the Time-of-Flight sensor market.

dToF LiDAR integration for Level-3+ ADAS roll-outs in EU and US

Sony’s IMX479 stacked SPAD depth sensor meets automotive AEC-Q100 reliability while detecting obstacles 300 m ahead at 20 fps.[3]Sony Semiconductor Solutions Group, “Sony Semiconductor Solutions to Release Stacked SPAD Depth Sensor for Automotive LiDAR Applications,” sony-semicon.com EU Regulation 2019/2144 locks in demand, as new passenger cars must fit advanced emergency braking and driver-monitoring packages from 2026. Automakers now combine dToF LiDAR, radar, and vision processors to authorize hands-free highway pilots, expanding revenue opportunities for the Time-of-Flight sensor market across tier-1 suppliers.

Miniaturization of SPAD-based modules enabling sub-6 mm camera islands

Sony’s 2025 LiDAR sensor shrinks footprint and power draw, while STMicroelectronics’ planar meta-optics replace multi-element lenses, halving z-height in VR headsets. ams-osram’s 1 mm² NanEyeC proves the optics-sensor package can vanish behind smartwatch glass. These breakthroughs let phone vendors squeeze three or four depth modules into increasingly thin devices, broadening consumer awareness and recurring revenue for the Time-of-Flight sensor industry.

Restraints Impact Analysis of Time-of-Flight (TOF) Sensor Market*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Multipath Interference and Ambient-Light Noise at >30 m Range | -2.8% | Global, particularly outdoor applications | Short term (≤ 2 years) |

| Volatile VCSEL Supply Concentration in Taiwan–U.S. Corridor | -2.1% | Global, concentrated supply chain risk | Medium term (2-4 years) |

| Strict EU GDPR Rules on In-Store People-Counting Cameras | -1.3% | EU, influencing global privacy standards | Long term (≥ 4 years) |

| Price Erosion from Competing Structured-Light Depth Solutions in Entry Smartphones | -1.9% | Global smartphone market, entry-level segment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multipath Interference and Ambient-Light Noise at Greater than30 m Range

Laboratory trials at MIT show that photons bouncing off multiple surfaces distort raw phase data, misplacing objects in depth maps. Microsoft’s SPUMIC algorithm corrects this in software, yet its compute footprint discourages budget deployments. Sensor vendors respond with larger pixels and global-shutter arrays, but performance still drops outdoors at noon, restraining some smart-city and long-haul industrial use cases inside the Time-of-Flight sensor market.

Volatile VCSEL supply concentration in the Taiwan-US corridor

Most high-power 940 nm emitters ship from a handful of fabs. When a major handset brand canceled a 2024 VCSEL order, one supplier’s UK plant headed for divestiture, spurring OEMs to dual-source or design fallback structured-light modules. onsemi’s Hyperlux roadmap eases reliance by integrating higher-efficiency pixels that demand fewer laser watts for identical range. Until diode capacity spreads across more regions, procurement teams will factor contingency premiums into Time-of-Flight sensor market contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Time-of-Flight (TOF) Sensor Market Segment Analysis

By Sensor Type:

Direct ToF accelerates despite iToF dominanceIndirect ToF technology accounted for 62.40% of the Time-of-Flight sensor market in 2025, reflecting its cost advantage and maturity in smartphones, webcams, and pick-and-place robots. Direct ToF units, though pricier, are surging at a 22.6% CAGR because range-gated SPAD arrays guarantee centimeter-grade accuracy beyond 200 m. The Time-of-Flight sensor market size for direct ToF modules is projected to swell rapidly as automakers fixate on LiDAR-centric ADAS stacks. Tier-1 suppliers value the latency-free depth output that dToF delivers, enabling redundancy with radar tracks during sensor-fusion. Indirect ToF chipsets continue to gain new features—global-shutter, HDR, and embedded DSP—positioning them as the default for AR handsets and factory cobots.

Advanced foundry nodes now pack on-chip histogramming that reduces external DRAM needs, cutting bill-of-materials in half for VR controllers. The Time-of-Flight sensor market benefits when handset OEMs can reuse a single iToF die across front-facing portrait cameras and rear-facing autofocus assist. Automobile LiDAR, however, mandates avalanche diodes, galvanically isolated from logic, which keeps the direct ToF bill higher through 2031. Both architectures coexist, filling discrete performance slots and stabilizing revenue diversity within the Time-of-Flight sensor market.

By Application:

3-D imaging leads while LiDAR surgesSmartphone portraiture and AR mapping drove 48.10% of 2025 demand, cementing 3-D imaging as the largest revenue bucket. The Time-of-Flight sensor market size for LiDAR is climbing at a 23.1% CAGR because Level-3 ADAS roll-outs require multiple roof-line lasers per vehicle. Machine-vision retrofits in electronics assembly lines adopt iToF cameras to identify solder misalignment at real-time takt speed, and e-commerce distribution centers fit depth arrays on aisle-roaming robots for dynamic obstacle avoidance.

Robotics and drones, while smaller today, represent high-growth greenfields: oxygen-starved mines use dToF scanners to map voids, and crop-spraying UAVs leverage low-weight ToF altimeters to maintain canopy distance. Gesture-recognition in smart TVs, gaming consoles, and XR headsets shifts toward multizone iToF, avoiding the privacy pitfalls of RGB capture. In-cabin driver monitoring—mandated in Europe from 2026—advances ultrawide near-infrared ToF optics that track gaze and microsleep behavior without emitting visible light, broadening safety-related revenues for the Time-of-Flight sensor market.

By End-User Vertical:

Consumer electronics leads, automotive acceleratesHandsets, tablets, and wearable cameras consumed 54.30% of shipments in 2025. Smartphone OEMs keep layering depth-enabled AR filters, 3-D scanning, and under-display authentication, anchoring predictable demand. The automotive sector rises at a 24.4% CAGR because regulators now treat driver-monitoring lenses as core safety components. The Time-of-Flight sensor market size for automotive interiors is set to more than quadruple as Euro NCAP rewards gaze tracking and child-presence detection.

Industrial automation adds steady baseline volume: surface-mount lines use ToF to validate component pick depth in milliseconds, and cobots rely on 360° depth domes to navigate coworker zones safely. Healthcare providers pilot contactless vitals monitoring for neonatal wards, logging respiration from subtle chest displacement. Logistics operators, empowered by Amazon’s 5,000-unit Colorado fleet, buy ceiling-mounted iToF depth pods to orchestrate tote routing. Privacy-focused smart buildings complement this uptake, installing anonymous ToF people-counting nodes that comply with GDPR while hitting 99.8% accuracy. Together, these niches diversify revenue and cushion cyclicality across the broader Time-of-Flight sensor market.

By Resolution:

QVGA dominance challenged by VGA growthQVGA-and-below arrays held 40.30% share in 2025 because proximity-sensing, autofocus, and collision-avoidance tasks rarely need more than 320×240 pixels. Yet automotive and warehouse robots are switching to VGA (640×480) as neural-network classifiers profit from denser point clouds. The Time-of-Flight sensor market share for VGA units is expected to jump alongside ADAS take-rates. Melexis’s MLX75027 demonstrates 120 fps VGA capture with ASIL-B fail-safes, persuading tier-1 suppliers to standardize on the higher resolution.

HD-class ToF sensors sit at the premium end, reserved for surgical navigation and film-production rigs that demand millimeter precision. Although their ASP remains triple that of QVGA, volume manufacturing at 90 nm nodes is trimming cost curves. As meta-optics mature, pixel pitch can shrink without losing quantum efficiency, positioning HD to encroach on VGA price bands by the decade’s close, further expanding the addressable Time-of-Flight sensor market.

Geography Analysis

APAC Time-of-Flight (TOF) Sensor Market

Asia-Pacific remains the epicenter of the Time-of-Flight sensor market, supplying and consuming over half of global output. China’s smartphone assembly clusters in Guangdong absorb millions of iToF dies each quarter, while Jiangsu-based back-end houses attach meta-optics lenses at scale. Japanese fabs refine SPAD wafers for high-margin automotive contracts, leveraging domestic robotics ecosystems to pilot new process nodes. South Korea’s vertically integrated conglomerates anchor both emitter and image-sensor production, providing internal demand and export revenue that stabilizes fab utilization. The Time-of-Flight sensor market size in this region grows in lockstep with handset ASP gains and regional EV roll-outs that specify multi-beam LiDAR.

North America Time-of-Flight (TOF) Sensor Market

North America drives technological specification. Silicon Valley lidar start-ups push range and eye-safety envelopes, and Seattle-area e-commerce warehouses prove out high-density robot-to-robot coordination. Federal highway regulators studying hands-free pilot deployments indirectly promote adoption of redundant cabin cameras, enlarging local demand for the Time-of-Flight sensor market. Canada’s agritech scene pilots drone-based biomass estimation using NIR ToF altimeters, marking niche rural growth.

Europe Time-of-Flight (TOF) Sensor Market

Europe blends regulatory pull and industrial automation. The EU General Safety Regulation 2026 mandates advanced driver-monitoring, guaranteeing baseline shipments. German Tier-1s, Italian packaging-line specialists, and Nordic robotics makers integrate iToF in quality-driven workflows. Tax incentives for energy-efficient factory retrofits help finance sensor refresh cycles. Although economic headwinds temper consumer electronics demand, industrial capital expenditure stabilizes the regional Time-of-Flight sensor market.

Competitive Landscape

Top Companies in Time-of-Flight (TOF) Sensor Market

The Time-of-Flight sensor market tilts toward moderate concentration, with the top five suppliers—Sony, STMicroelectronics, onsemi, Infineon, and ams-osram—controlling just above two-thirds of revenue. Sony’s proprietary SPAD stacks and backlog of automotive design wins grant economies of scale. STMicroelectronics focuses on meta-optics and multizone ranging, frequently bundling its VL53 family with companion 32-bit MCUs to lock customers into its ecosystem. onsemi differentiates via global-shutter pixels that read both ambient-light and depth in a single exposure, appealing to industrial-automation OEMs.

Infineon and pmd’s co-developed 5 µm pixel REAL3 imagers ship in lidar cleaning robots and under-display face-ID modules, highlighting a system-integrator partnership model. ams-osram, leveraging EEL and VCSEL emitter portfolios, pursues package co-design that reduces driver size and thermal load. Component shortages in 2024-2025 pushed each vendor to pursue dual foundry sourcing or in-house epi-growth to hedge geopolitical risk. Emerging challengers concentrate on niche breakthroughs—event-driven histograms to cut in-sensor power, or hybrid CMOS-SPAD pixels to extend HDR—that could upset incumbent share if mass-production hurdles fall.

Time-of-Flight (TOF) Sensor Industry Leaders

Texas Instruments Incorporated

STMicroelectronics NV

Infineon Technologies AG

Panasonic Corporation

Sony Corporation

- *Disclaimer: Major Players sorted in no particular order

Time-of-Flight (TOF) Sensor Market Companies Covered in this Report

- Sony Corporation (Sony Semiconductor Solutions)

- STMicroelectronics N.V.

- Infineon Technologies AG

- Texas Instruments Incorporated

- onsemi (ON Semiconductor Corp.)

- Panasonic Holdings Corp.

- Sharp Corp.

- Keyence Corp.

- Teledyne Technologies Inc.

- Omron Corp.

- ams-OSRAM AG

- Melexis N.V.

- PMD Technologies AG

- Analog Devices Inc.

- Cognex Corp.

- LMI Technologies Inc.

- Samsung Electronics Co. Ltd.

- LG Innotek Co. Ltd.

- Hamamatsu Photonics K.K.

- Renesas Electronics Corp.

- Himax Technologies Inc.

- Tower Semiconductor Ltd.

Recent Industry Developments in Time-of-Flight (TOF) Sensor Market

- May 2025: Amazon introduced Vulcan, a warehouse robot with tactile sensing that now handles 75% of SKUs up to 8 lb and will roll out to more sites by 2026.

- April 2025: Sony unveiled the world’s smallest LiDAR depth sensor designed for robotics and AR glasses.

- March 2025: onsemi launched the Hyperlux ID family, the first real-time iToF sensor measuring up to 30 m for industrial automation.

Global Time-of-Flight (TOF) Sensor Market Report Scope

The time-of-flight principle (ToF) is a method for measuring the distance between a sensor and an object based on the time difference between the emission of a signal and its return to the sensor after being reflected by an object. ToF sensors use a tiny laser to fire out infrared light, which bounces off any object and returns to the sensor. The sensor can measure the distance between an object and itself by measuring the time difference between the emission of light and its return to the sensor after being reflected by an object.

The Time-of-flight (TOF) sensor market is segmented by type (RF-modulated light sources with phase detectors, range-gated imagers, and direct Time-of-Flight imagers), by application (augmented reality & virtual reality, LiDAR, machine vision, 3D imaging & scanning, and robotics & drones), by end-user vertical (consumer electronics, automotive, entertainment & gaming, industrial, healthcare, and other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Segmentation Overview

| Indirect (iToF / RF-Modulated) |

| Direct (dToF) |

| Range-Gated Imagers |

| Illumination (VCSEL/LED) |

| Sensor/Receiver Array |

| Depth Processor |

| QVGA and Below |

| VGA |

| HD and Above |

| Short |

| Medium |

| Long |

| Augmented and Virtual Reality |

| LiDAR |

| Machine Vision |

| 3-D Imaging and Scanning (incl. Smartphone Cameras) |

| Robotics and Drones |

| Gesture Recognition and Biometrics |

| In-Cabin Driver-Monitoring Systems |

| Security and Surveillance |

| Consumer Electronics |

| Automotive |

| Entertainment and Gaming |

| Industrial and Manufacturing |

| Healthcare and Medical Imaging |

| Logistics and Warehouse Automation |

| Security and Smart Buildings |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa | |

| Oceania | Australia |

| New Zealand |

| By Sensor Type | Indirect (iToF / RF-Modulated) | |

| Direct (dToF) | ||

| Range-Gated Imagers | ||

| By Component | Illumination (VCSEL/LED) | |

| Sensor/Receiver Array | ||

| Depth Processor | ||

| By Resolution | QVGA and Below | |

| VGA | ||

| HD and Above | ||

| By Range | Short | |

| Medium | ||

| Long | ||

| By Application | Augmented and Virtual Reality | |

| LiDAR | ||

| Machine Vision | ||

| 3-D Imaging and Scanning (incl. Smartphone Cameras) | ||

| Robotics and Drones | ||

| Gesture Recognition and Biometrics | ||

| In-Cabin Driver-Monitoring Systems | ||

| Security and Surveillance | ||

| By End-User Vertical | Consumer Electronics | |

| Automotive | ||

| Entertainment and Gaming | ||

| Industrial and Manufacturing | ||

| Healthcare and Medical Imaging | ||

| Logistics and Warehouse Automation | ||

| Security and Smart Buildings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Oceania | Australia | |

| New Zealand | ||

Key Questions Answered in the Report

What is the current value of the Time-of-Flight sensor market?

The market is valued at USD 8.06 billion in 2026 and is forecast to grow to USD 20.52 billion by 2031.

Which end-user vertical holds the largest share?

Consumer electronics accounted for 54.30% of revenue in 2025, mainly from smartphones and tablets.

Why are direct ToF sensors gaining momentum?

Automotive LiDAR and long-range industrial tasks need centimeter-level accuracy beyond 200 m, a performance space where direct ToF outperforms indirect variants.

Why are direct ToF sensors gaining momentum?

Automotive LiDAR and long-range industrial tasks need centimeter-level accuracy beyond 200 m, a performance space where direct ToF outperforms indirect variants.

Which region is the fastest growing?

The Middle East is projected to expand at a 25.9% CAGR during 2026-2031 due to smart-city and logistics investments.

How are privacy rules influencing adoption?

EU GDPR pushes retailers to adopt depth-only people-counting cameras that deliver 99.8% accuracy while ensuring 100% anonymity.

What technical challenge most limits long-range ToF?

Multipath interference and strong sunlight introduce phase errors beyond 30 m, prompting sensor makers to develop larger pixels, HDR readouts, and AI-based correction algorithms.

Page last updated on: