Thyristor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

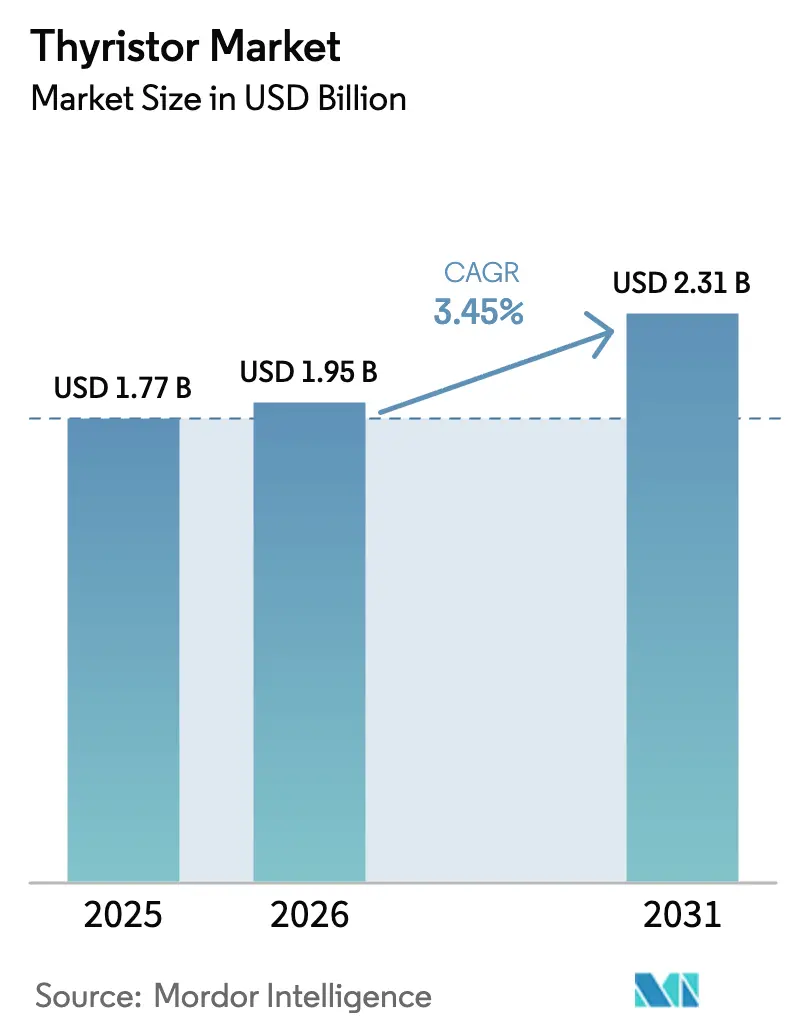

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thyristor Market Analysis by Mordor Intelligence

The Thyristor market size was valued at USD 1.77 billion in 2025 and is estimated to grow from USD 1.95 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 3.45% during the forecast period (2026-2031). Demand is steady because utilities still favor line-commutated valves for multi-gigawatt high-voltage direct current (HVDC) corridors, even as silicon-carbide metal-oxide-semiconductor field-effect transistors (SiC MOSFETs) win share in automotive and high-frequency industrial drives. Procurement cycles are shaped by large grid projects that lock in orders years ahead, while module integrators diversify toward intelligent power modules that embed gate drivers and sensors. Price competition is intensifying in low-and mid-power ratings as Chinese discrete suppliers offer stud and capsule devices at 20-30% lower average selling prices than European peers. At the same time, counterfeit risk and certification delays are raising the importance of traceability and vertically integrated manufacturing.

Key Report Takeaways

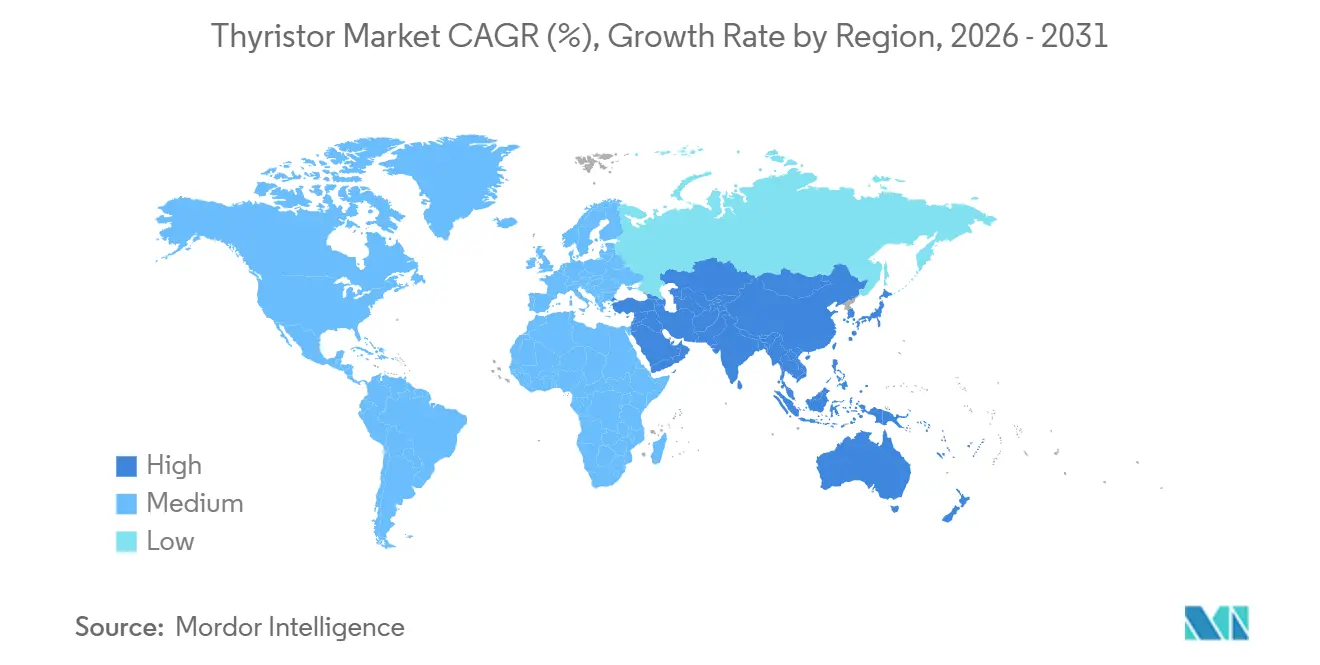

- By geography, Asia-Pacific captured 45.48% revenue in 2025, while the Middle East is expected to be the fastest-growing region at a 4.08% CAGR over 2026-2031.

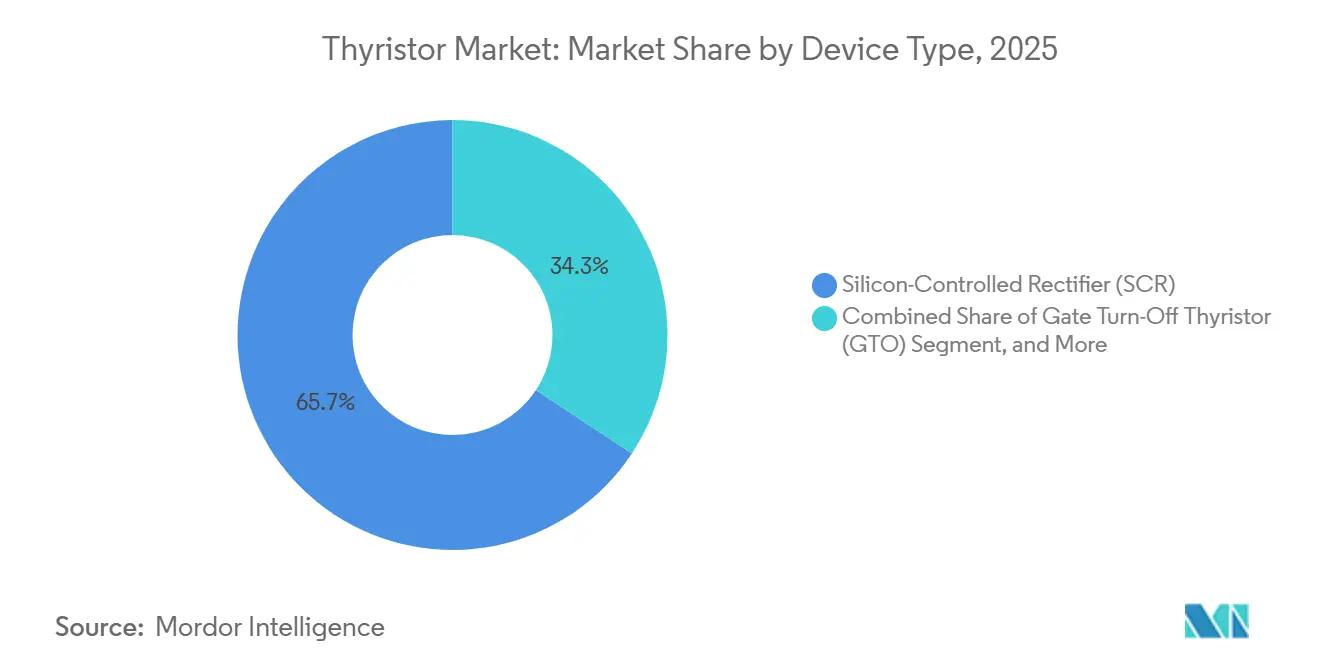

- By device type, silicon-controlled rectifiers led with 65.71% revenue share in 2025, while gate turn-off thyristors are projected to advance at a 3.82% CAGR through 2031.

- By power rating, systems below 500 MW held 45.83% of the Thyristor market share in 2025, whereas installations above 1,000 MW are forecast to grow at a 3.97% CAGR between 2026-2031.

- By mounting format, stud-type packages accounted for 40.27% of the Thyristor market size in 2025, and intelligent power modules are poised to expand at a 4.11% CAGR to 2031.

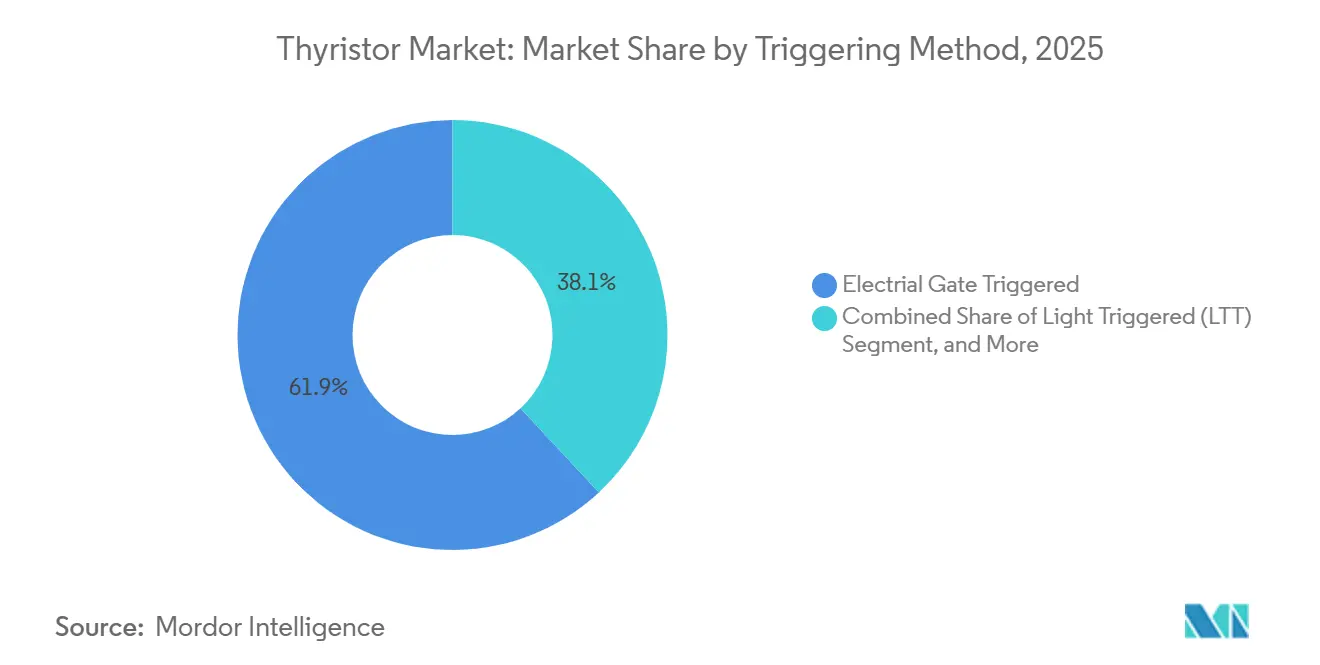

- By triggering method, electrical gate triggering retained 61.92% share in 2025, yet light-triggered devices are projected to rise at a 4.25% CAGR through 2031.

- By end-use industry, industrial drives and motor control dominated demand with 28.64% in 2025, but renewable power conversion applications are set to record the fastest 4.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thyristor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of HVDC links integrating offshore wind in Asia | +0.8% | Asia-Pacific core, spill-over to Middle East and Europe | Medium term (2-4 years) |

| Grid-code-mandated dynamic reactive-power compensation in EU utilities | +0.6% | Europe, adoption spreading to North America | Long term (≥ 4 years) |

| Modernization of aluminum-smelter rectifiers in Gulf Cooperation Council countries | +0.5% | Middle East, secondary demand in Asia-Pacific and Africa | Medium term (2-4 years) |

| Fast-charging infrastructure for two-wheeler EVs in China and India using SCR stacks | +0.4% | Asia-Pacific, primarily China and India | Short term (≤ 2 years) |

| Surge in solid-state circuit breakers for rail locomotives in India and Germany | +0.3% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Adoption of radiation-hard optically triggered thyristors in avionics | +0.2% | Global, concentration in aerospace hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of HVDC Links Integrating Offshore Wind in Asia

Mega-scale offshore wind corridors continue to anchor new ±800 kV lines across China, South Korea, and Australia, each requiring between 200-300 press-pack devices per gigawatt of capacity. China’s Hami-Chongqing and Ningxia-Hunan lines alone add 16 GW of converter capacity that specifies thyristor valves for line-commutated stages. Korea’s West Coast Energy Expressway, approved in 2024, locks in 1,600 high-power devices through 2028 [1]Korea Electric Power Corporation, “West Coast Energy Expressway HVDC Project Approval,” home.kepco.co.kr . Australia’s Marinus Link adopts a mixed valve approach that still reserves discrete high-voltage positions for thyristors [hitachienergy.com]. Project backlogs therefore extend into the early 2030s, sustaining the Thyristor market even as voltage-source converter (VSC) choices rise.

Grid-Code-Mandated Dynamic Reactive-Power Compensation in EU Utilities

Updated ENTSO-E guidance now obliges distribution operators to maintain power factor within ±0.95 during peak and off-peak windows.[2]ENTSO-E, “Guidance on Reactive Power Management at Transmission-Distribution Interface,” entsoe.eu Germany’s Federal Network Agency sets a January 2026 deadline for plants above 10 MW to install dynamic support, stimulating orders for thyristor-switched capacitor banks and static var compensators. Spain has already deployed 1,800 MVAr of static synchronous compensators equipped with 48-pulse valve assemblies. Italy awarded 900 MVAr of flexible alternating current transmission systems (FACTS) gear in 2024 to reduce renewable curtailment. Compliance windows to 2028 underpin a rolling retrofit wave that supports the Thyristor market across Europe and North America.

Modernization of Aluminum-Smelter Rectifiers in Gulf Cooperation Council Countries

Qatar, Oman, and Bahrain finalized multi-year upgrades that lower specific energy consumption by up to 1 kWh/kg aluminum. Bahrain’s 1,354 MW expansion integrated 2,000 V devices from Fuji Electric, absorbing roughly 800 high-current capsules . Saudi Arabia’s Ras Al-Khair green-field smelter specifies 400 kA stacks for 12-pulse rectifiers.[3]Terna, “FACTS Equipment Procurement for Grid Stabilization,” terna.it Each new potline needs 800-1,200 thyristors, and at least four projects are scheduled through 2028, keeping Gulf demand resilient despite commodity

Fast-Charging Infrastructure for Two-Wheeler EVs in China and India Using SCR Stacks

Electric two-wheelers topped 12.4 million sales in 2025 in China, with fast-charge models rising to 18% share. India standardized cost-efficient 48/60 V silicon-controlled rectifier chargers under IS 17017 Part 2. Operators in Bangalore and Delhi installed more than 4,500 SCR-stack chargers that tolerate grid voltage sags common in semi-urban feeders. Shenzhen suppliers shipped 280,000 assemblies to OEMs such as Yadea and Ola, illustrating how price sensitivity keeps silicon-controlled rectifiers competitive. Although efficiency trails active front-ends, the capital-expense advantage accelerates near-term roll-outs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SiC MOSFET cannibalization in EV inverters | -0.7% | Global, highest in automotive hubs | Short term (≤ 2 years) |

| Counterfeit SCR modules causing OEM recalls in Southeast Asia | -0.4% | Asia-Pacific, concentrated in Southeast Asia | Short term (≤ 2 years) |

| Volatile polysilicon pricing inflating discrete thyristor cost | -0.3% | Global semiconductor supply chains | Medium term (2-4 years) |

| Lengthy certification cycles for GTOs in United States utilities | -0.2% | North America utility sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SiC MOSFET Cannibalization in EV Inverters

Leading automakers have migrated to SiC devices that shrink inverter volume by nearly one-third and raise vehicle range by about 6%, displacing legacy thyristor-based auxiliaries in 400-V and 800-V systems. Mass-production scale has reduced the SiC premium to less than triple insulated-gate bipolar transistor (IGBT) pricing, encouraging mid-tier models to switch. Thyristor vendors lack comparable high-frequency switching capability, so content per vehicle fell below USD 6 in 2025 for many brands. Automotive revenue, formerly a growth pillar, is now retreating, limiting the Thyristor market’s upside in mobility segments.

Counterfeit SCR Modules Causing OEM Recalls in Southeast Asia

An October 2025 crackdown in Shenzhen found recycled die re-labeled as premium brands, with forward voltage drops 15-20% above data-sheet limits. Failures surfaced in uninterruptible power supplies across Vietnam and Thailand, prompting widespread recalls. Independent labs in Singapore traced reverse leakage currents well outside specification, confirming reliability threats [a-star.edu.sg]. Tier-one vendors now etch QR codes and embed blockchain tracking, adding up to USD 1 per device but shortening unauthorized distribution channels. Procurement managers increasingly specify “non-China origin” clauses, fragmenting the supply chain and lifting compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: SCR Dominance, GTO Momentum in Rail and HVDC

Silicon-controlled rectifiers secured 65.71% of demand in 2025, anchoring low-frequency phase-controlled rectifiers across electro-chemical processing, motor soft-starters, and automotive alternator regulators. These devices combine 6,000-8,000 V blocking strength with surge tolerance above 10× rated current, while selling for under USD 15 in volume, which keeps the Thyristor market pervasive in price-sensitive industrial niches. Gate turn-off thyristors are forecast to log a 3.82% CAGR to 2031 as modular multilevel converters and urban rail upgrades adopt their self-commutating capability for simplified protection. The segment’s growth is evident in China’s high-speed train fleet, where new converters withstand vibration and temperature swings yet still rely on GTOs for fault isolation. Triacs, reverse-conducting, and asymmetric variants each address smaller pockets such as residential dimming or chopper drives, but none rival the scale of core SCR demand.

Design-in decisions reflect a trade-off between switching speed and per-ampere economics. The Thyristor market size for SCRs in industrial service remains stable, whereas GTO penetration rises where power density and ride-through dictate faster turn-off. Bidirectional triac sales stay flat because smart-home hubs replace legacy dimmers with solid-state relays. Reverse-conducting types gain in traction choppers, collapsing diode and thyristor into one die to cut inductance, while asymmetric parts meet HVDC poles that rarely see reverse stress. Suppliers that span all five device families capture cross-sell benefits, contributing to moderate revenue concentration.

By Power Rating: Below 500 MW Dominates, >1 GW Segment Accelerates

Applications under 500 MW held 45.83% share in 2025, covering medium-voltage drives, regional static var compensators, and distribution-level converters. Standardized ratings streamline engineering, favorite for brownfield upgrades where footprint constraints override ultimate current density. Above 1,000 MW installations are forecast to grow at a 3.97% CAGR because multibillion-dollar HVDC corridors link offshore wind farms and cross-border grids. South Korea’s 8 GW West Coast backbone will use about 1,600 stacked levels of high-power devices, each level series-connecting multiple press packs [home.kepco.co.kr]. Mid-tier 500-1,000 MW projects such as Saudi Arabia’s 750 MW aluminum rectifier complex demonstrate balanced capital efficiency and manageable harmonics.

High-power orders favor capsule packages that tolerate 3-4 kW heat dissipation per device, necessitating direct liquid cooling. Certification under IEC 60747-9 can take 18 months, so incumbents with in-house test bays enjoy an access moat. Meanwhile, next-generation 8,500 V press-pack IGBT modules from Mitsubishi Electric offer smaller footprints, but their 40-50% cost premium limits adoption to space-constrained substations. The Thyristor market share in mega-watt segments therefore expands steadily as gigawatt-scale links multiply, even though wide-bandgap devices nibble at the mid-range.

By Mounting and Package: Modules Rising, Studs Still Vital**

Stud-type parts commanded 40.27% revenue in 2025 because retrofit motor drives and legacy plant tooling rely on bolt-down heatsinks. However, intelligent power modules are forecast to climb at a 4.11% CAGR through 2031 as rail and renewable inverters shift to plug-and-play designs that integrate gate drive, snubbers, and sensors. Mitsubishi Electric’s 3.3 kV full-SiC module illustrates this trend, trimming inverter volume by 30% while easing assembly. Capsule and disc formats remain indispensable in ultra-high-voltage converter halls, where each press-pack must handle 200-400 W losses and survive mechanical clamping forces exceeding 20 kN.

Labor economics push integrators to favor factory-tested modules that cut field wiring by 30-40% and reduce warranty claims tied to torque errors or interface degradation. Yet, repairability is lower—one failed chip forces replacement of the entire module, inflating lifecycle cost in applications with 25-30 year horizons. Surface-mount and clip-mount variants occupy low-power control boards, but their volume is small. The packaging mix therefore evolves toward intelligent modules without displacing studs entirely, preserving diversity within the Thyristor market.

By Triggering Method: Electrical Leads Today, Optic Links Tomorrow

Electrical gate triggering held 61.92% share in 2025 thanks to the low cost of transformer-isolated drivers, typically USD 2-5 per channel. Light-triggered architectures are projected to expand at a 4.25% CAGR through 2031 because fiber links withstand 100-200 kV common-mode voltage in ultra-high-voltage converter halls. They also meet electromagnetic interference limits of 200 V/m demanded in avionics, where radiation-hardened optically triggered devices avoid latch-up under 100 krad total dose. ABB’s HVDC Light stations in Australia and China now specify light-triggered capsules that eliminate copper gate leads, improving dv/dt immunity by nearly 2×.

Pulse-transformer triggering stays relevant in medium-voltage drives and FACTS where transient levels top out at 20 kV. Cost premiums restrict light-triggered devices to mission-critical or very-high-voltage duty, but patent filings for integrated photodiodes and on-chip gate drivers foreshadow broader uptake. Over the forecast window, a gradual migration toward optical isolation will raise the Thyristor market size for light-triggered parts without erasing entrenched electrical designs.

By End-Use Industry: Drives Lead, Renewables Grow Fastest

Industrial drives and motor control captured 28.64% revenue in 2025 and will continue to anchor shipment volumes because replacement cycles stretch 10-15 years. Soft-starters, variable-speed pumps, and electro-chemical rectifiers prize rugged SCR stacks over faster yet costlier SiC devices. Renewable power conversion is forecast to clock the highest 4.41% CAGR as static synchronous compensators (STATCOMs), HVDC terminals, and thyristor-switched capacitor banks stabilize grids with renewables above 30% penetration. Wind and solar farm owners value the sub-cycle response of thyristor valves that clamp voltage swings and manage harmonics.

HVDC and FACTS projects, while fewer in count, consume multi-kilosemiconductor volumes per site and thus underpin long-term demand. Transportation uses—rail traction choppers, marine propulsion, and solid-state breakers—are trending toward gate turn-off and reverse-conducting designs, sustaining mid-single-digit growth. Automotive penetration contracts because SiC MOSFET inverters displace auxiliary thyristors in 400-V to 1,200-V rails, although on-board chargers still employ SCRs in cost-optimized trims. Aerospace and defense, despite tiny unit volumes, generate premium margins for radiation-qualified optically triggered parts, helping suppliers offset price pressure in commodity tiers.

Geography Analysis

Asia-Pacific dominated the Thyristor market with 45.48% share in 2025, lifted by China’s addition of 12 GW HVDC capacity and India’s electrification of 6,400 route-kilometers of railway track. Japan is reinforcing inter-island links with modular multilevel converter hybrids that still need high-voltage gate turn-off stacks, and South Korea’s 8 GW backbone project sustains a multiyear order book. Australia’s Marinus Link introduces VSC technology, trimming devices per megawatt yet extending construction through the early 2030s. The region also houses the world’s largest discrete manufacturing clusters, with Chinese fabs shipping 420 million units in 2025 for drives, appliances, and traction.

The Middle East is projected to post the fastest 4.08% CAGR during 2026-2031 as Saudi Arabia’s NEOM mega-project orders rectifiers for 4 GW of electrolyzers, each gigawatt requiring 800-1,000 high-current capsules [neom.com]. Solar plants such as Sudair and Al Dhafra integrate thyristor-switched capacitor banks and static var compensators that together exceed 900 MVAr of reactive support. Aluminum smelter upgrades in Bahrain and Qatar consume thousands of high-current devices, and at least three Gulf potline projects are queued through 2028. Regional demand therefore ties closely to energy-diversification budgets linked to hydrocarbon revenue.

North America and Europe exhibit moderate expansion. Germany’s mandate for dynamic reactive support effective 2026 is triggering retrofits, and Spain’s 1,800 MVAr STATCOM rollout showcases immediate grid benefits. Certification cycles for gate turn-off stacks in U.S. utilities, however, may exceed 18 months, delaying revenue recognition. South America centers on Brazil’s 600 MVAr FACTS contracts that integrate Northeastern wind, while Africa’s pipeline is led by South Africa’s series capacitor corridor, yet fiscal constraints push commissioning beyond 2027. Collectively, the global footprint underscores how region-specific policies and project financing rates govern the Thyristor market trajectory.

Competitive Landscape

Revenue concentration is moderate: Infineon, Mitsubishi Electric, ABB, and STMicroelectronics account for roughly 55-60% of sales thanks to vertically integrated fabs, assembly, and applications engineering. Infineon’s EUR 5 billion (USD 5.65 billion) 300 mm SiC fab in Kulim began shipping wafers in 2026, lowering die cost by 30% relative to 150 mm processes and freeing capital to defend high-voltage insulated-gate bipolar and thyristor positions. Mitsubishi Electric’s full-SiC railway module provides a hedge against rapid wide-bandgap uptake while preserving GTO back-compatibility. ABB leverages its system-level expertise in HVDC Light to bundle thyristor valves and services, and STMicroelectronics is doubling SiC output at its Catania campus to bridge automotive and industrial needs.

Chinese challengers—Jiangsu JieJie Microelectronics, Dongguan Yangjie Electronic, and WeEn Semiconductors—target the <2 kV segment with capsule and stud parts priced up to 30% below European averages. Their voltage derating and shorter mean-time-between-failure metrics limit penetration in mission-critical grids but capture price-sensitive drives and appliance markets. Counterfeit exposure remains a reputational hazard; after the 2025 Shenzhen bust, major OEMs tightened approved-vendor lists and demanded blockchain traceability, a shift favoring vertically integrated makers

Innovation patterns show a bifurcation. Wide-bandgap SiC light-triggered thyristors and integrated gate-commutated variants appear in recent patent filings, but volume hinges on cost parity with electrical trigger stacks. Vendors are also exploring hybrid thyristor-IGBT assemblies for medium-voltage drives, yet no dominant topology has emerged. Capital intensity is high; each new high-power platform requires USD 500 million-plus investment in die, packaging, and test infrastructure, reinforcing barriers to late entrants and sustaining the existing moderate concentration.

Thyristor Industry Leaders

STMicroelectronics

Vishay Intertechnology

Infineon Technologies AG

ABB Ltd.

Mitsubishi Electric Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Infineon Technologies started volume production at its 300 mm SiC facility in Kulim, Malaysia, targeting automotive and industrial modules with a 30% lower die cost benchmark.

- January 2026: Saudi Arabia’s NEOM awarded thyristor-based rectifier contracts covering 4 GW of electrolyzer capacity, with commissioning slated for late 2026.

- December 2025: South Korea’s Ministry of Trade, Industry and Energy approved the 8 GW West Coast Energy Expressway HVDC line, securing valve orders through 2028.

- October 2025: Shenzhen authorities dismantled a counterfeit operation re-labeling SCRs, prompting industry-wide adoption of blockchain traceability.

Global Thyristor Market Report Scope

Thyristors are semiconductor devices with four layers of alternating P-type and N-type materials. It comes in three categories: anode (positive terminal), cathode (negative terminal), and gate (control terminal). A thyristor, a semiconductor device with four layers of alternating P- and N-type materials, acts exclusively as a bistable switch, conducting when the gate receives a current trigger and continuing to conduct until the voltage across the device is reversed biased or until the voltage is removed.

The Thyristor Market Report is Segmented by Device Type (Silicon-Controlled Rectifier, Gate Turn-Off Thyristor, Bidirectional Triac, Reverse Conducting Thyristor, Asymmetric Thyristor), Power Rating (Less than 500 MW, 500-1,000 MW, Above 1,000 MW), Mounting and Package (Stud-Type, Capsule/Disc, SMD and Clip-mount, Module), Triggering Method (Electrical Gate Triggered, Light Triggered, Pulse Transformer Triggered), End-use Industry (Industrial Drives and Motor Control, HVDC and FACTS, Renewable Power Conversion, Transportation, Automotive, Consumer Electronics and Appliances, Aerospace and Defense), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Silicon-Controlled Rectifier (SCR) |

| Gate Turn-Off Thyristor (GTO) |

| Bidirectional Triac |

| Reverse Conducting Thyristor |

| Asymmetric Thyristor (ASCR) |

| Less than 500 MW |

| 500 - 1 000 MW |

| Above 1 000 MW |

| Stud-Type |

| Capsule / Disc |

| SMD and Clip-mount |

| Module (Intelligent Power Module, Hybrid) |

| Electrical Gate Triggered |

| Light Triggered (LTT) |

| Pulse Transformer Triggered |

| Industrial Drives and Motor Control |

| HVDC and FACTS (SVC, STATCOM) |

| Renewable Power Conversion (Solar, Wind) |

| Transportation (Rail Traction, Marine) |

| Automotive (On-board Chargers, EV Powertrain) |

| Consumer Electronics and Appliances |

| Aerospace and Defense |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Device Type | Silicon-Controlled Rectifier (SCR) | |

| Gate Turn-Off Thyristor (GTO) | ||

| Bidirectional Triac | ||

| Reverse Conducting Thyristor | ||

| Asymmetric Thyristor (ASCR) | ||

| By Power Rating | Less than 500 MW | |

| 500 - 1 000 MW | ||

| Above 1 000 MW | ||

| By Mounting and Package | Stud-Type | |

| Capsule / Disc | ||

| SMD and Clip-mount | ||

| Module (Intelligent Power Module, Hybrid) | ||

| By Triggering Method | Electrical Gate Triggered | |

| Light Triggered (LTT) | ||

| Pulse Transformer Triggered | ||

| By End-use Industry | Industrial Drives and Motor Control | |

| HVDC and FACTS (SVC, STATCOM) | ||

| Renewable Power Conversion (Solar, Wind) | ||

| Transportation (Rail Traction, Marine) | ||

| Automotive (On-board Chargers, EV Powertrain) | ||

| Consumer Electronics and Appliances | ||

| Aerospace and Defense | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Thyristor market expected to become by 2031?

The Thyristor market size is projected to reach USD 2.31 billion by 2031, growing at a 3.45% CAGR from 2026.

Which device type leads current revenue?

Silicon-controlled rectifiers held 65.71% of 2025 revenue due to entrenched use in industrial motor control and phase-controlled rectification.

What is the fastest-growing regional opportunity?

The Middle East is forecast to log the highest 4.08% CAGR between 2026-2031, fueled by green hydrogen rectifiers and large-scale solar balance-of-plant investments.

How are counterfeit risks affecting procurement?

Post-2025 recalls in Southeast Asia triggered mandatory blockchain traceability and QR-code marking, lengthening lead times but improving supply integrity.

Why are light-triggered thyristors gaining interest?

Fiber-optic isolation tolerates 100-kV common-mode voltages and high electromagnetic fields, making light-triggered devices attractive for HVDC valves and avionics.

Will SiC devices completely replace thyristors?

SiC MOSFETs dominate high-frequency automotive inverters, yet thyristors remain favored for ≥3.3 kV applications where cost per ampere and surge tolerance matter most.

Page last updated on: