Aircraft Arresting System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

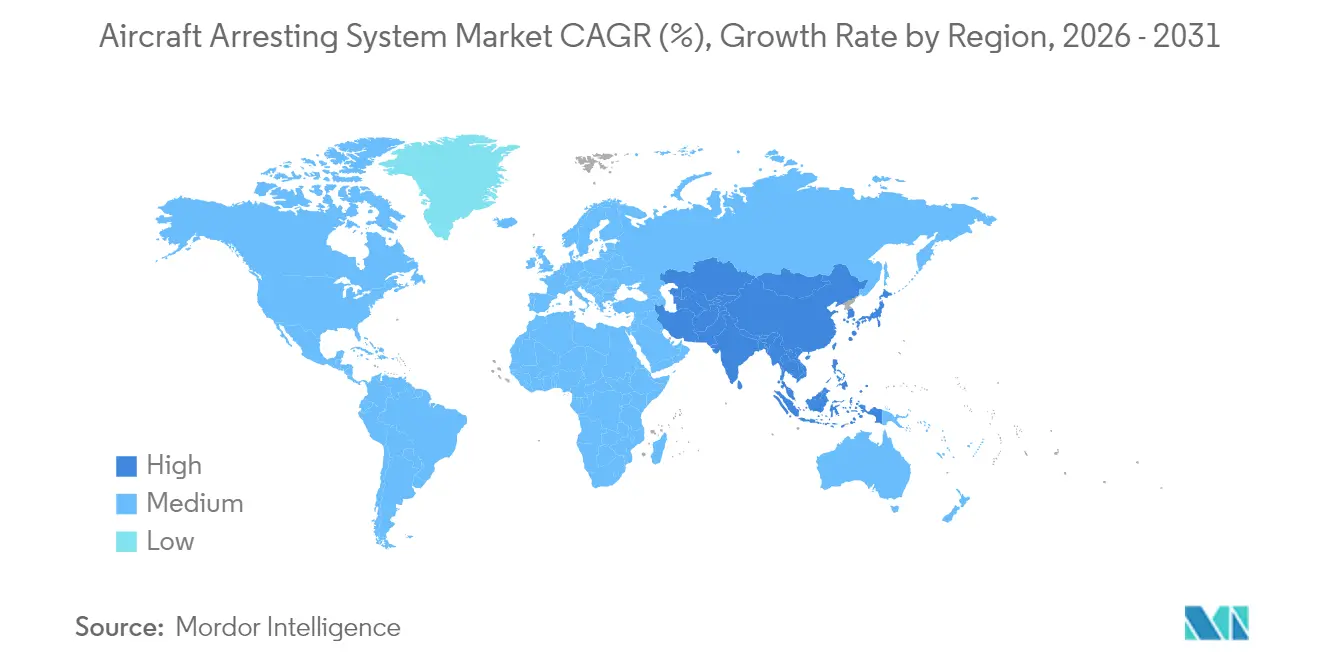

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Arresting System Market Analysis by Mordor Intelligence

The aircraft arresting system market size is expected to grow from USD 1.33 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 6.35% CAGR over 2026-2031. Demand is propelled by expanding fifth-generation fighter fleets, robust aircraft-carrier modernization, and converging global safety regulations that make over-run mitigation mandatory at many commercial airports. Technology is shifting from hydraulic arrestors to electromagnetic systems, as demonstrated by the US Navy’s Advanced Arresting Gear, which has logged more than 23,000 recoveries aboard CVN 78. Land-based platforms capture the largest revenue, yet sea-based applications show the fastest growth as Asia-Pacific navies field new carriers. Engineered Material Arresting Systems (EMAS) are accelerating in commercial aviation because the FAA mandates installations at airports that cannot build standard safety areas. Supply-chain constraints in specialty alloys and springs introduce near-term risk, but digital control units offering predictive maintenance offset part of this drag through life-cycle cost savings.

Key Report Takeaways

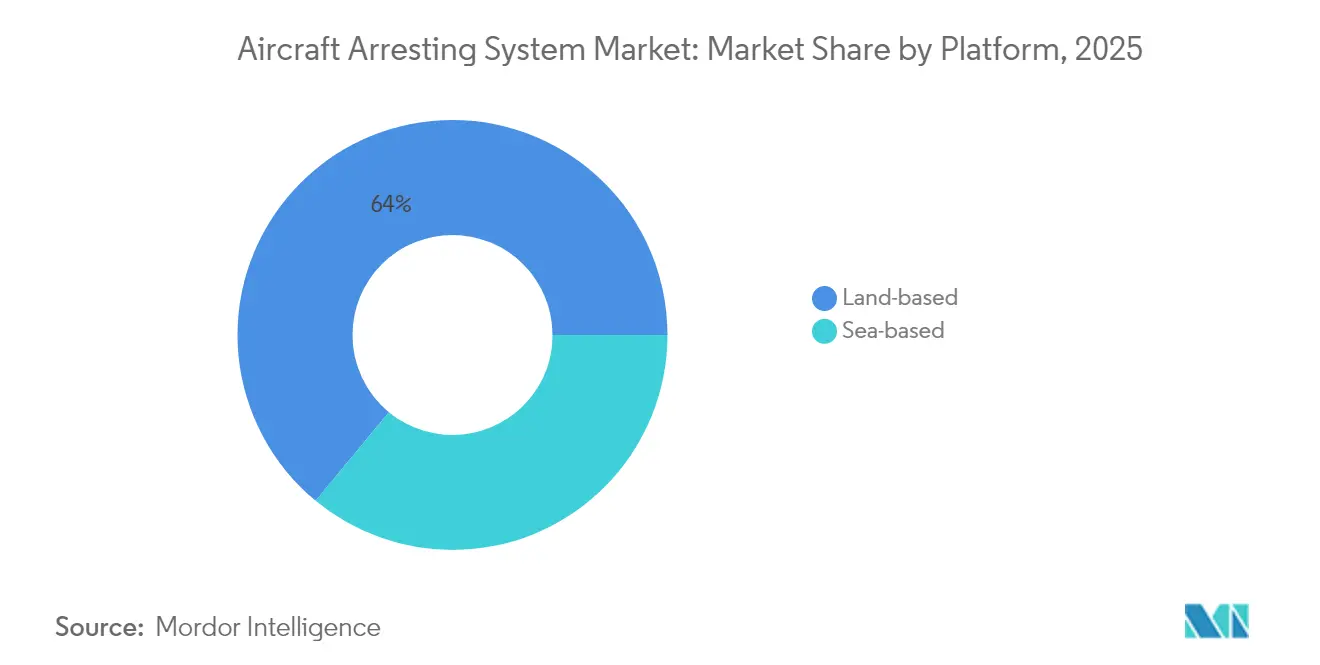

- By platform, land-based installations held 64.02% of the aircraft arresting system market share in 2025, while sea-based systems are forecast to expand at an 8.12% CAGR through 2031.

- By technology type, cable and reel systems led with a 36.72% revenue share in 2025; EMAS is projected to rise at a 8.86% CAGR.

- By end user, military airbases accounted for 42.10% of the aircraft arresting system market size in 2025, whereas aircraft carriers represent the fastest-growing segment at an 8.43% CAGR.

- By component, energy absorbers captured a 36.95% share of the aircraft arresting system market size in 2025; control and monitoring units are advancing at a 7.58% CAGR.

- By fit, new installations represented 55.94% of total revenue in 2025, but retrofit activities are forecast to grow at a 6.87% CAGR.

- By geography, North America commanded 40.02% of 2025 revenue while Asia-Pacific is on track for an 7.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aircraft Arresting System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of fifth-generation combat aircraft fleets | +1.2% | North America and Asia-Pacific | Medium term (2-4 years) |

| Growth in short-runway and expeditionary airfield operations | +0.9% | Asia-Pacific and Middle East | Short term (≤2 years) |

| Global safety-regulation convergence toward runway-end over-run protection | +0.8% | North America and EU, expanding to Asia-Pacific | Long term (≥4 years) |

| Technological shift from hydraulic to electromagnetic and rotary-friction systems | +1.1% | Global, led by naval programs in North America and Asia-Pacific | Medium term (2-4 years) |

| Insurance and liability pressures driving civil-airport retrofits | +0.7% | Developed markets worldwide | Long term (≥4 years) |

| Increase in worldwide aircraft-carrier and LHD/LHA deployments | +0.6% | Asia-Pacific with spill-over to Middle East and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Fifth-Generation Combat Aircraft Fleets

F-35 variants place unprecedented loads on arresting hooks, prompting rapid material upgrades and hook-point redesigns to meet 15-engagement life requirements. Carrier-borne F-35C testing revealed early wear that forced replacement after single-digit cycles, driving innovation in high-strength alloys. Elevated approach weights, 18,000 lbs with full payload, require larger energy-absorber capacity, fueling procurement of electromagnetic systems able to modulate deceleration precisely. Marine Corps trials with M-31 gear at Twentynine Palms proved the aircraft’s flexibility for Expeditionary Advanced Base Operations. The US FY 2025 aviation budget of USD 61.2 billion underwrites aircraft and corresponding arresting upgrades.

Growth in Short-Runway and Expeditionary Airfield Operations

Distributed-operations doctrine pushes arresting systems into austere zones. The Air Force’s Mobile Aircraft Arresting System (MAAS) can be installed on gravel or asphalt in two hours by six airmen. Exercises such as Operation BEEFY validated the MAAS deployment for F-16s under challenging weather. Expeditionary interest extends to adapting Electromagnetic Aircraft Launch System (EMALS) for shore bases, offering catapult-like flexibility without full-length runways. These deployments enlarge the aircraft arresting system market as nations harden dispersed operating bases.

Global Safety-Regulation Convergence toward Runway-End Over-Run Protection

Canada’s 2022 rules mandate 150m Runway End Safety Areas at busy airports, allowing EMAS where terrain limits expansion.[1]Government of Canada, “Regulations Amending the Canadian Aviation Regulations,” gazette.gc.ca ICAO’s Global Runway Safety Action Plan aligns developing and advanced states on excursion mitigation through engineered materials. The FAA has begun canvassing the industry for next-generation EMAS as early units near the end of their design life, a signal of continuing demand. Such harmonization facilitates cross-border certification and economies of scale, expanding the aircraft arresting system market.

Technological Shift from Hydraulic to Electromagnetic and Rotary-Friction Systems

General Atomics’ EMALS and Advanced Arresting Gear (AAG) surpassed 8,000 cycles during post-delivery trials and withstood shock testing, proving combat reliability.[2]General Atomics Electromagnetic Systems, “EMALS and AAG Successful Performance,” ga.com Electromagnetic arrestors reduce parts count and maintenance hours, while offering real-time force modulation that lowers airframe stress. Research into eddy-current braking pairs electromagnetic torque with conventional hydraulic absorption for finer control, indicating a hybrid future. International cooperation, such as the US-India working group on carrier technology, broadens export horizons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | |

|---|---|---|---|

| High up-front capital expenditure and lengthy certification cycles | -1.4% | Global, with pronounced effect in emerging markets | Medium term (2-4 years) |

| Supply-chain dependence on specialty alloys and high-cycle springs | -0.8% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤2 years) |

| Competing investment priorities: autobrake and runway-surface enhancements | -0.7% | North America and EU, expanding to commercial airports globally | Long term (≥ 4 years) |

| Limited standardization across aircraft types | -0.5% | Global, with particular challenges in multi-platform military operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Capital Expenditure and Lengthy Certification Cycles

Full EMAS installation can exceed USD 10 million per runway end, forcing smaller airports to rely on FAA grants that cover up to 95%, yet remain competitive to secure. Defense programs face similar burdens; AAG unit costs breached procurement thresholds after design changes, underscoring certification complexity in new technology. Proprietary systems limit vendor competition, elevating acquisition and lifecycle costs, which restrains broader adoption in the aircraft arresting system industry.

Supply-Chain Dependence on Specialty Alloys and High-Cycle Springs

Arresting gear relies on high-strength wire ropes and titanium springs, with limited suppliers. Obsolescence tracking under the Defense Logistics Agency’s DMSMS program flags critical shortages that can idle systems. Cold-dwell fatigue in titanium threatens component life, spurring stricter inspection intervals that elevate maintenance costs. Disruptions ripple through production schedules, delaying deliveries and increasing the risk profile for expansion projects in the aircraft arresting system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Sea-Based Systems Drive Innovation

Sea-based platforms are forecast to grow at an 8.12% CAGR, closing the gap with dominant land installations with a 64.02% aircraft arresting system market share in 2025. Fleet expansion in Asia-Pacific—including China’s Fujian and South Korea’s CVX—requires electromagnetic arrestors to handle heavier jets and future unmanned systems. US–French collaboration on next-generation carriers signals similar technology migration to Europe.

Land systems remain essential for dispersed operations. MAAS enables two-hour deployment on roads and packed earth, supporting fighter detachments without traditional infrastructure. Commercial airports adopt EMAS, where terrain blocks runway extensions, with more than 500 installations recorded by 2024. Both trends sustain a diversified aircraft arresting system market.

By Technology Type: Engineered Material Arresting System (EMAS) Disrupts Traditional Dominance

Engineered Material Arresting System (EMAS) revenue grows at a 8.86% CAGR, eroding the 36.72% share held by Cable and Reel designs. FAA studies on next-generation materials anticipate end-of-life replacement waves, opening space for lighter, recyclable blocks that maintain crush characteristics. Finite-element tests of pervious concrete confirm its capacity to decelerate aircraft rapidly while simplifying drainage, demonstrating future low-carbon options.

Cable and Reel remains entrenched in legacy bases because of hook compatibility and lower purchase cost. Rotary-friction units offer middle-ground solutions for regional airports needing reliable performance without electromagnetic complexity. Electromagnetic designs secure flag-carrier interest due to higher sortie rates and simplified maintenance cycles, positioning them as the premium tier in the aircraft arresting system market.

By End User: Aircraft Carriers Accelerate Growth

Aircraft carriers are projected to climb at an 8.43% CAGR, sustained by Indo-Pacific naval build-ups. South Korea’s 45,000-ton CVX intends to field F-35Bs with potential STOBAR upgrades that demand advanced arresting technology. US–India dialogue on electromagnetic recovery broadens the export pool US Navy.

Military airbases, holding 42.10% of 2025 revenue, invest in mobile gear that supports agile combat employment. Commercial airports respond to excursion liability, with EMAS credited for 18 successful saves protecting 419 occupants, Federal Aviation Administration. Converging military and civil standards streamline certification and bolster the aircraft arresting system market size.

By Component: Control Systems Lead Innovation

Control and monitoring units expand at a 7.58% CAGR as operators shift to predictive maintenance platforms with embedded sensors. Sustainable energy-recovery research illustrates the potential to harvest landing energy into grid power, covering aircraft from A319 to A380. Energy absorbers remain foundational, representing 36.95% of 2025 revenue, yet must evolve to manage heavier fifth-generation fighters.

Hook and cable durability drives R&D into advanced wire alloys; military carriers are adopting compact swaging machines for at-sea cable repairs that once required shore facilities. Improved foundations and anchoring systems accelerate MAAS deployment, underscoring infrastructure’s strategic weight in the aircraft arresting system market.

By Fit: Retrofit Applications Gain Momentum

Retrofits grow at a 6.87% CAGR as aging systems struggle with heavier aircraft and tightened regulations. Belgium’s upgrade of rotary-friction absorbers through Curtiss-Wright illustrates European demand for modernization without full replacement. FAA funding prioritizes safety at existing runways, keeping retrofit budgets buoyant.

New builds still dominate, accounting for 55.94% of 2025 revenue. Asia-Pacific greenfield bases specify electromagnetic technology from inception, bypassing legacy hybrids. Rapid-setback guidance published in 2025 trims MAAS setup to two hours, aligning with expeditionary doctrine and supporting fresh procurements.

Geography Analysis

North America retains a 40.02% share of the aircraft arresting system market, anchored by the US Navy’s AAG program and an FAA mandate that has delivered more than 500 EMAS runway ends. Canada’s 150 m safety-area rule further expands civil demand, especially at land-locked airports, while Curtiss-Wright's collaboration on helicopter handling builds specialized niches. The FAA’s USD 4.0 billion airport-grant line item for 2026 sustains capital flows into safety infrastructure.

Asia-Pacific is the fastest-expanding region, with an 7.94% CAGR, propelled by China’s multi-carrier fleet and India’s collaboration on next-generation electromagnetic recovery. South Korea’s CVX program underscores the region's appetite for advanced solutions. ICAO’s Asia-Pacific Aerodrome Design Task Force has codified runway-end safety, ensuring steady civil aviation demand.

Europe maintains incremental growth driven by NATO standardization. French and Belgian upgrades reinforce a shared supplier base, easing logistics for deployed operations, Air Force Technology. Emerging markets in Africa embrace ICAO guidance; Sierra Leone’s safety plan specifies arresting systems where terrain prevents wider safety areas. The Middle East leverages US and European foreign military sales channels for carrier and land-based gear, diversifying the global aircraft arresting system market.

Regulatory Landscape

Aircraft arresting systems operate under a split civil-military compliance environment that affects specifications, certification evidence, and approved supplier lists. In the United States, civil airport installations follow FAA Advisory Circular AC 150/5220-9B for aircraft arresting systems, while military programs use design and performance criteria such as MIL-STD-3035 and maintenance and certification guidance in US Air Force manuals (for example, AFMAN 32-1040). For multinational operators and deployed operations, NATO STANAG 3697 standardizes procedures and terminology for airfield aircraft arresting systems, supporting interoperability across member nations.

Procurement and sustainment also adopt defense quality controls for safety-critical hardware, including controlled technical data packages, source approvals, and configuration management for items with critical safety implications. These requirements raise barriers for new entrants and concentrate demand among vendors that can demonstrate compliance across FAA, DoD, and NATO frameworks while maintaining audit-ready maintenance and inspection records over long service lives.

Value Chain Analysis

The value chain begins with specialty inputs and engineered subassemblies, including high-strength wire ropes and webbing, energy absorbers (rotary-friction or hydraulic), foundations and anchoring hardware, and, increasingly, digital control and monitoring units. Arresting system OEMs and prime suppliers (such as Curtiss-Wright/ESCO, General Atomics for carrier electromagnetic programs, and ATECH) integrate these systems and deliver them through defense procurement channels and airport capital programs. For naval applications, the chain also includes shipyard integration and fleet sustainment, where OEM engineering support, diagnostics, and spares provisioning become central to lifecycle cost and readiness.

Aftermarket services represent a substantial share of delivered value, since arresting gear requires periodic inspections, component refurbishment, and configuration-controlled replacements, particularly for high-cycle parts and other safety items. Contracting patterns often favor vendors with proprietary designs and specialized tooling, which can lead to sole-source or limited-competition awards for certain assemblies and upgrades. Supply risk is concentrated among limited producers of specialty alloys, springs, and certified rope or webbing products, while digital health monitoring and predictive maintenance capabilities are increasingly bundled to reduce downtime and support long-term service agreements.

Competitive Landscape

Market concentration is moderate. General Atomics dominates naval electromagnetic systems, winning a USD 1.19 billion contract for EMALS and AAG on USS Doris Miller. Curtiss-Wright maintains strong positions in rotary-friction installations and mobile systems, recently securing Belgian and French upgrades.

Runway Safe is the only FAA-approved EMAS supplier in the civil segment, giving it a quasi-monopoly in US commercial projects. The firm invests in alternative foams to extend product life, although upcoming FAA inquiries into new materials may attract challengers. Patent data show rising filings on crash-barrier concepts for unmanned aircraft, an indicator that new entrants see openings in the aircraft arresting system industry.

Strategically, suppliers bundle digital monitoring with hardware to cement long-term service contracts. General Atomics and Hanwha’s 2025 collaboration on Gray Eagle STOL unmanned aircraft reveals an ecosystem view that pairs platform design with tailored arresting solutions. Such vertical integration could shift competitive balance as the aircraft arresting system market evolves toward data-driven performance guarantees.

Aircraft Arresting System Industry Leaders

General Atomics

Safran SA

Sojitz Aerospace Corporation

MacTaggart, Scott and Company Limited

QinetiQ Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Civil runway-end overrun protection is an actionable whitespace where airports face physical limits on standard safety areas and therefore turn to engineered arresting solutions under established FAA guidance. A replacement and refresh cycle is also emerging as earlier-generation EMAS installations approach design-life limits, and the FAA has signaled interest in next-generation EMAS materials and concepts. This is creating room for product redesign (for example, improved durability, drainage, and recyclability) and differentiation beyond first-generation blocks.

On the defense side, modernization programs and distributed-operations doctrine are expanding demand for mobile and expeditionary recovery capability, alongside upgrades that align with heavier fifth-generation aircraft landing loads. The US Marine Corps 2026 Aviation Plan outlines modernization of Aircraft Arresting Gear (AGS) with 25 systems and defined IOC and FOC targets, reinforcing a multi-year pipeline for hardware, site preparation, training, and sustainment. For sea-based growth, Ford-class carrier sustainment requirements around EMALS and Advanced Arresting Gear (AAG) point to a high-value support niche, where specialized diagnostics, spares, and depot-level services can be contracted via multi-year vehicles and basic ordering agreements.

Recent Industry Developments

- June 2026: The US Naval Air Systems Command (NAVAIR) issued a sources sought notice for a five-year Basic Ordering Agreement to support Electromagnetic Aircraft Launch System (EMALS) and Advanced Arresting Gear (AAG) on Ford-class carriers. The action formalized a long-duration sustainment pathway for electromagnetic launch and recovery hardware, expanding demand for diagnostics, spares, and specialized engineering support tied to carrier sortie generation.

- April 2025: Curtiss-Wright reported Royal Australian Air Force testing of ESCO Mobile Aircraft Arresting Systems (MAAS) at RAAF Base Amberley, including 12 Rotor BAK-12 energy absorbers. The validation work strengthens the export and allied-operability case for mobile arresting capability and adds reference performance data for rapid runway recovery and dispersed operations.

- September 2024: Curtiss-Wright secured a USD 26 million multi-year Belgian Air Force contract to modernize aircraft arresting systems at Florennes, Kleine-Brogel, and Beauvechain airbases. The program aligns arresting infrastructure with Belgiums F-35 transition and reinforces the role of turnkey modernization, spares, and sustainment services as a recurring revenue stream in European retrofit cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the annual revenue generated from equipment and related installation used to safely stop or slow an aircraft during an aborted takeoff, emergency landing, or routine recovery (mainly on carriers), across civilian and defense airfields.

Scope exclusions: We exclude simple ground handling items such as wheel chocks, basic ropes, and non-specialized runway blocks that are not engineered arresting solutions.

Segmentation Overview

- By Platform

- Sea-based

- Land-based

- By Technology Type

- Cable and Reel

- Net Barrier

- Engineered Material Arresting System (EMAS)

- Rotary-Friction/Hydraulic

- Electromagnetic/Magnetic

- By End User

- Military Airbase

- Commercial Airport

- Aircraft Carrier

- By Component

- Energy Absorber

- Hook and Cable

- Support Structure and Foundations

- Control and Monitoring Unit

- By Fit

- New Installation

- Retrofit

- By Geography

- North America

- United States

- Canada

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set clear boundaries for what gets counted as an aircraft arresting system sale versus nearby runway safety spending, and it also helped frame where demand is coming from. We reviewed public defense budget documents and readiness plans to understand likely spending cycles for carrier decks and military airfields.

For market inputs, we leaned on non-paywalled sources such as FAA airport and runway safety publications, ICAO aerodrome operations guidance, US DoD budget justification books, NATO and national defense procurement notices, and technical papers in aerospace engineering journals. We also used customs and trade statistics where relevant, plus company annual reports, investor presentations, and reputable aviation press to confirm product coverage and delivery patterns, which are then cross-checked with selective company financials and intelligence and an import-export shipment-level database when it supports validation. The sources listed here are illustrative, and many other public references were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought and installed, and how spending splits between new builds, upgrades, and sustainment for arresting gear and EMAS-style solutions. We spoke with a mix of airfield operations stakeholders, program and procurement contacts, and technical experts involved in runway and carrier deck safety, with coverage across major demand regions so assumptions could be adjusted to local procurement patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 19% | APAC: 38% |

| Mid tier: 42% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 19% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

The core sizing starts from a top-down build that reconstructs demand using defense and civil aviation spending signals, planned runway and carrier maintenance cycles, and expected installation counts, which are then translated into value using typical system-level pricing. To keep the totals practical, we corroborate them with selective bottom-up checks such as sampled program awards, shipment visibility where available, and volume-by-ASP sanity checks for common configurations.

Key inputs that shaped the model included runway safety upgrade frequency, carrier deck arresting-gear overhaul cycles, airbase modernization intensity, the mix of fixed versus portable systems, and typical contract packaging (equipment only versus equipment plus installation and testing). Because procurement can be lumpy, scenario analysis was used around large defense awards and multi-year airport programs, and then the forecast path was aligned with expert feedback on lead times, qualification requirements, and funding timing. Where bottom-up visibility was incomplete, gaps were handled through proxy installation rates and conservative price bands that were later re-tested during validation calls.

Data Validation & Update Cycle

Outputs were checked against independent signals such as disclosed contract awards, publicly announced runway projects, and changes in defense readiness plans, and then exceptions were reviewed before sign-off. When large variances appeared by region or year, assumptions were revisited and, where needed, follow-up conversations were triggered to confirm whether timing, scope, or pricing was being misread.

The report is refreshed annually, and interim updates are made when material events occur, such as a major procurement program launch or a shift in airbase investment priorities. Before delivery, a final analyst pass is completed so clients receive the latest updated view based on newly available public information and the most recent validation feedback.

Mordor Intelligence's Aircraft Arresting System Market Estimate Compared With Other Published Estimates

Published numbers for this market can vary even when they look close, mainly because firms do not always count the same equipment, services, or timing of contract recognition. Differences also come from how each study handles defense versus civil demand, and whether one-time carrier programs are smoothed or left as spikes.

The benchmark table shows a spread that is mostly explained by what gets counted as system value and how the yearly spend is timed, and in Mordor Intelligence's model the totals reflect installed arresting solutions at runways and flight decks, including major components and installation elements, while excluding simple ground handling items such as wheel chocks and basic ropes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.33 B (2025) | |

| Global Research Publisher A | USD 1.53 B (2025) | This estimate appears to include a wider basket of runway safety and recovery spending, and it also uses a higher assumed revenue capture for portable and auxiliary equipment within airbase programs. |

| Industry Research House B | USD 1.40 B (2024) | This figure seems closer to a single-year program-timing view, where large naval and airbase awards are captured as reported in the year, rather than being normalized across delivery and installation timelines. |

Overall, the gap is not driven by one single input, but by scope boundaries and the way lumpy defense procurement is converted into annualized market value. By tying the model to observable installation cycles, award signals, and realistic price bands, the final number stays traceable to clear steps that can be repeated and re-checked.

Key Questions Answered in the Report

What is the current size of the aircraft arresting system market?

The market is valued at USD 1.41 billion in 2026 and is forecasted to reach USD 1.92 billion by 2031, witnessing a 6.35% CAGR.

Which platform segment is expanding the fastest?

Sea-based systems aboard aircraft carriers are projected to grow at an 8.12% CAGR to 2031 due to extensive carrier modernization in Asia-Pacific.

Why are Engineered Material Arresting Systems (EMAS) gaining traction?

EMAS growth at a 8.86% CAGR is driven by FAA and ICAO mandates that require runway-end over-run protection where standard safety areas cannot be built.

How do fifth-generation fighters influence arresting gear design?

F-35 variants impose higher landing loads and electromagnetic compatibility needs, accelerating R&D in durable hooks and energy absorbers.

What limits broader adoption of advanced arresting systems?

High capital cost and lengthy certification cycles, especially for electromagnetic systems, remain primary barriers, particularly in emerging markets.

Which region is expected to see the fastest demand growth?

Asia-Pacific leads with an 7.94% CAGR through 2031 as China, India, and South Korea invest in new carriers and supportive shore infrastructure.

Page last updated on: