Thin Layer Deposition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

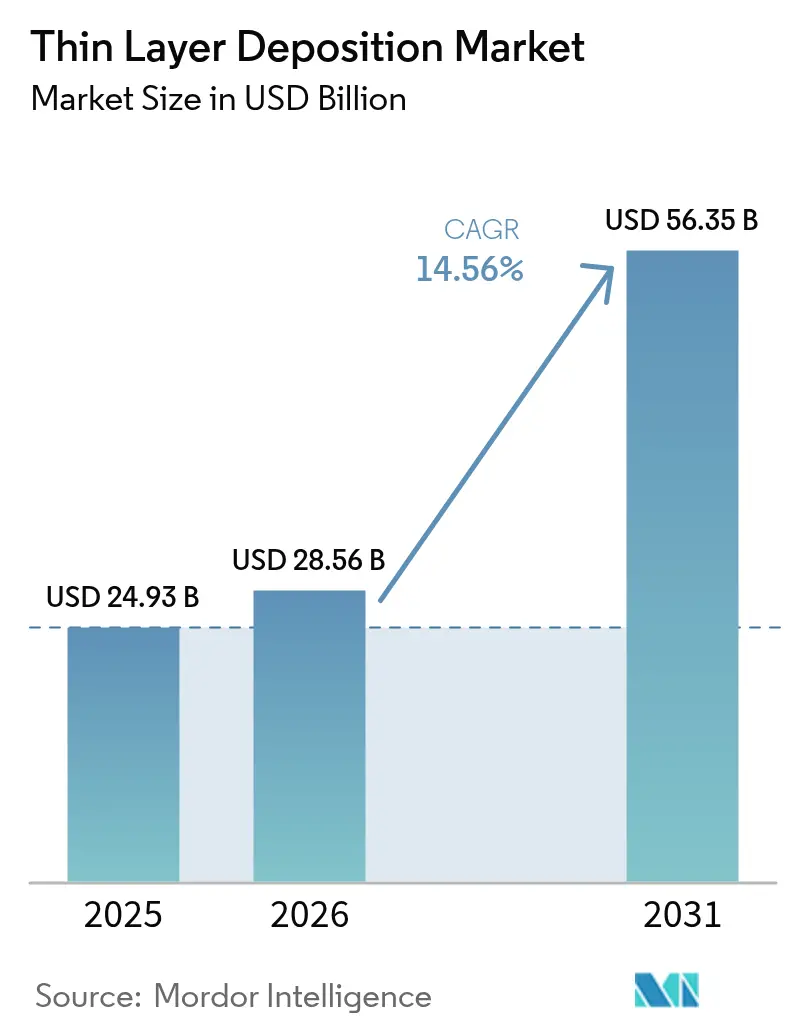

| Market Size (2026) | USD 28.56 Billion |

| Market Size (2031) | USD 56.35 Billion |

| Growth Rate (2026 - 2031) | 14.56% CAGR |

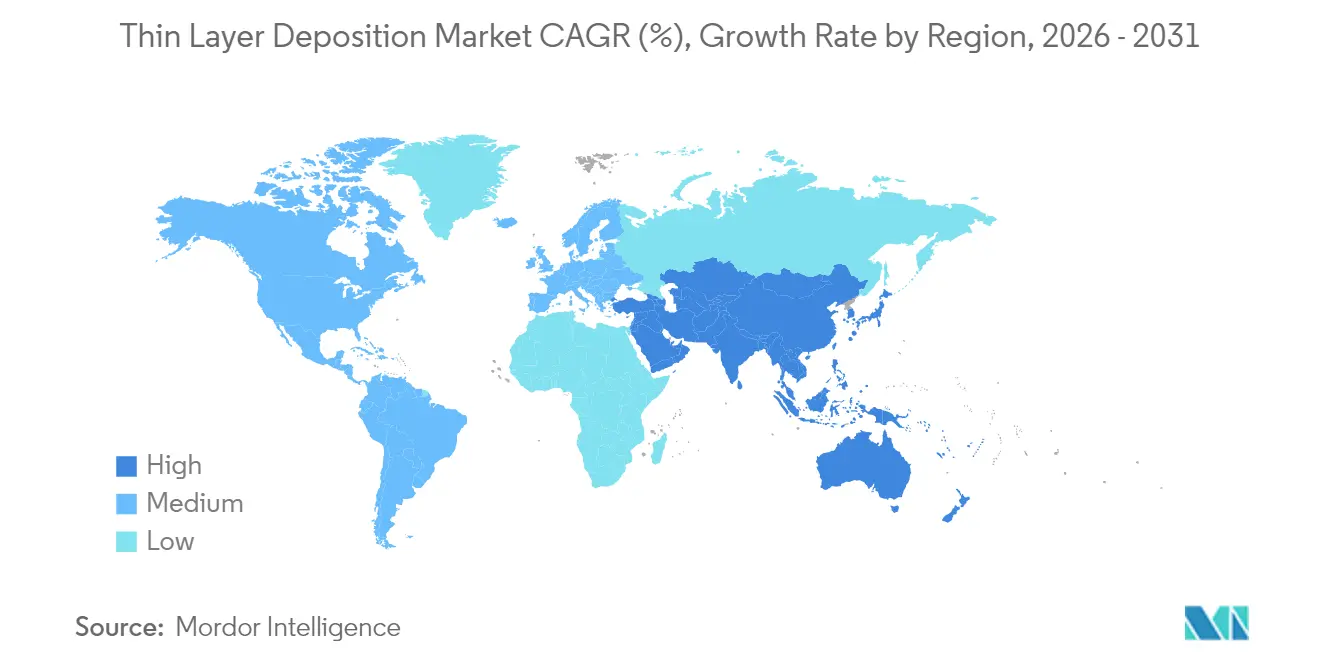

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thin Layer Deposition Market Analysis by Mordor Intelligence

The thin layer deposition market size was valued at USD 24.93 billion in 2025 and estimated to grow from USD 28.56 billion in 2026 to reach USD 56.35 billion by 2031, at a CAGR of 14.56% during the forecast period (2026-2031). Growth stems from structural shifts in semiconductor scaling, perovskite tandem photovoltaics, and medical-grade surface engineering. Foundries rely on atomic layer deposition for sub-5-nanometer gate stacks, while solar manufacturers adopt roll-to-roll physical vapor deposition to reduce the cost per watt. Government CHIPS-style incentives channel capital toward domestic equipment plants, and AI-driven predictive maintenance reduces tool downtime, thereby increasing overall equipment effectiveness. Material diversification into nitrides, carbides, and 2D compounds opens up incremental revenue streams for specialty chemical suppliers and toolmakers. At the same time, helium scarcity, Scope-3 carbon rules, and talent shortages temper the growth outlook, nudging suppliers to develop closed-loop gas recovery and low-power reactor designs.

Key Report Takeaways

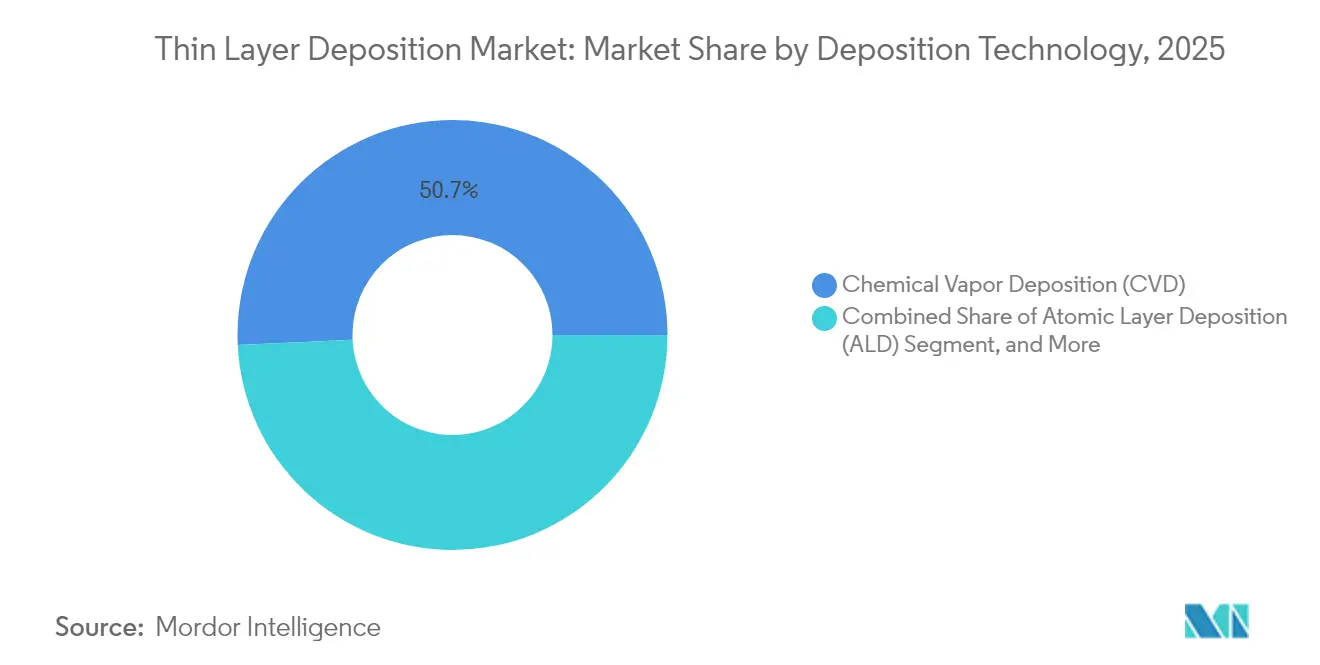

- By deposition technology, chemical vapor deposition accounted for 50.74% of the thin layer deposition market size in 2025, while atomic layer deposition is advancing at a 17.18% CAGR to 2031.

- By equipment type, batch systems accounted for 56.05% of the thin layer deposition market size in 2025, and roll-to-roll plus spatial systems are projected to expand at a 16.36% CAGR through 2031.

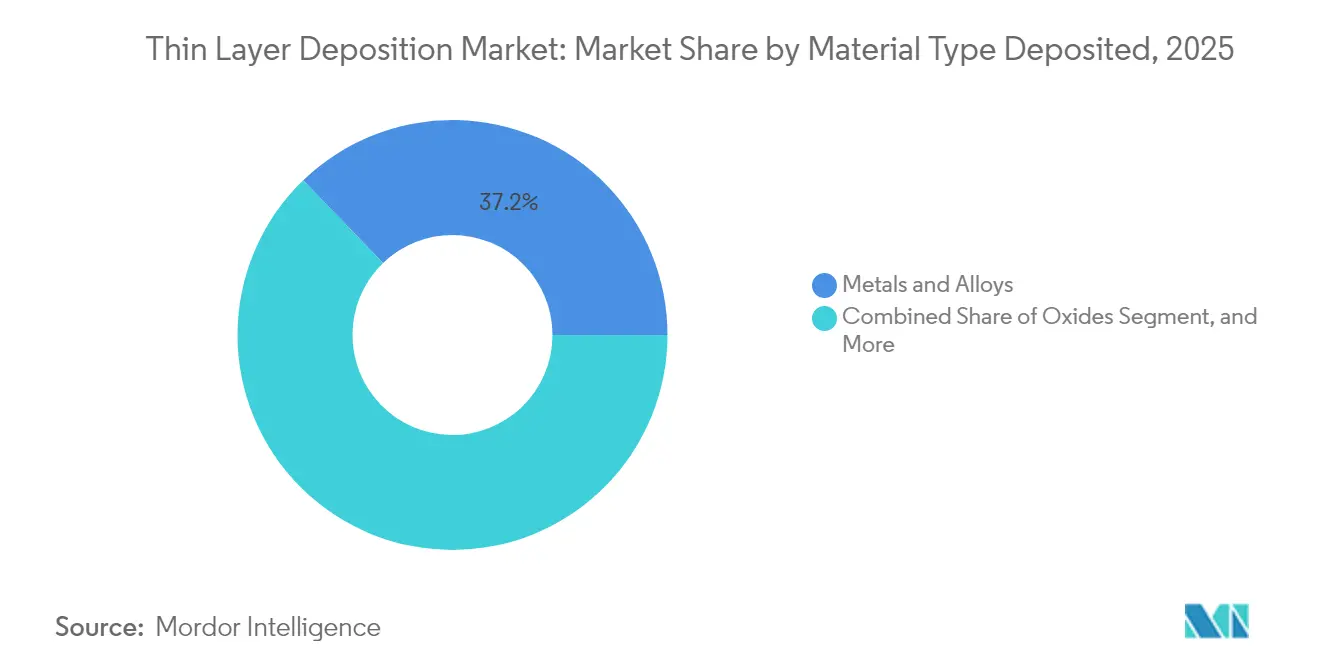

- By material type deposited, metals and alloys accounted for 37.22% of the thin layer deposition market size in 2025, and nitrides and carbides are projected to expand at a 17.01% CAGR through 2031.

- By end-use industry, semiconductors and micro-electronics captured 41.35% of the thin layer deposition market size in 2025, whereas photovoltaics and energy storage is forecast to post an 17.74% CAGR until 2031.

- By geography, the Asia Pacific commanded 44.78% of the thin layer deposition market size in 2025, and is poised to grow at a 16.92% CAGR over the next five years.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thin Layer Deposition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chiplet and 3D-IC architectures intensify the need for ultra-conformal interconnect films | +3.2% | Global with hubs in Taiwan, South Korea, United States | Medium term (2-4 years) |

| Rapid scale-up of perovskite tandem solar cell manufacturing | +2.8% | Asia Pacific core, spillover to Europe and Middle East | Medium term (2-4 years) |

| Spatial ALD and roll-to-roll PVD breakthroughs slashing cost per nanometer | +2.5% | Global, early adoption in China, Germany, United States | Short term (≤ 2 years) |

| Government CHIPS-like incentives boosting domestic deposition tool CAPEX | +2.1% | United States, European Union, India, Japan | Long term (≥ 4 years) |

| AI-powered predictive maintenance reducing deposition tool downtime | +1.6% | Global, led by advanced fabs in Taiwan, South Korea, United States | Short term (≤ 2 years) |

| Emergence of biodegradable implant coatings in med-tech | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chiplet And 3D-IC Architectures Intensify The Need For Ultra-Conformal Interconnect Films

Heterogeneous integration is changing interconnect design, demanding barrier and seed layers that cover high-aspect-ratio vias without voids. Taiwan Semiconductor Manufacturing Company’s CoWoS-S stacks logic with high-bandwidth memory using 20:1 aspect-ratio through-silicon vias that require titanium nitride deposited by atomic layer deposition for copper diffusion control. Intel’s 2024 Foveros Direct technology reduced bump pitch to 25 μm, forcing a shift to cobalt seed layers with 95% step coverage that chemical vapor deposition struggles to achieve. Samsung Foundry aims for 2 μm line-and-space redistribution by 2027, which will rely on plasma-enhanced atomic layer deposition of ruthenium liners. Tool vendors saw orders surge; Applied Materials reported 38% year-over-year growth in advanced-packaging deposition tools in fiscal 2024.[1]Applied Materials Inc., “Form 10-K FY 2024,” sec.gov Industry consortia are pushing new precursors, such as cyclopentadienyl-based ruthenium, to enable sub-300 °C processing compatible with organic interposers.

Rapid Scale-Up of Perovskite Tandem Solar Cell Manufacturing

Perovskite-silicon tandems surpassed the 33% efficiency mark in 2024, sparking a surge in the development of pilot lines. Oxford Photovoltaics commenced 200 MW production in Brandenburg, utilizing slot-die perovskite layers in combination with PECVD tin oxide electron transport films. Longi has partnered with Meyer Burger to integrate perovskites into TOPCon modules, aiming for 30% efficiency by 2026. The U.S. Department of Energy has granted USD 40 million to spatial atomic layer deposition projects, aiming for 10× throughput gains in passivation layers. Venture capital is flowing: Swift Solar raised USD 27 million to commercialize lightweight tandem panels that rely on roll-to-roll sputtered transparent conductors. The International Energy Agency forecasts 50 GW of tandem capacity by 2030, provided that deposition tools maintain uptime above 90% and material utilization exceeds 70%.

Spatial ALD And Roll-To-Roll PVD Breakthroughs Slashing Cost Per Nanometer

Spatial atomic layer deposition eliminates pump-down cycles by moving substrates through isolated precursor zones, achieving 300 mm wafer throughput of nearly 1,000 units per hour. Beneq’s 2024 demo hit 5 nm min⁻¹ Al₂O₃ on flexible polyimide with around 2% uniformity across 600 mm webs. Veeco’s Picosun roll-to-roll system coated lithium-ion separators at 10 m/min⁻, cutting the cost per square meter from USD 0.50 to USD 0.08. Applied Materials’ Olympia platform integrates spatial atomic layer deposition and physical vapor deposition within a single cluster, reducing cobalt liner and copper seed times by 40%. On the sputtering front, Von Ardenne logged 100 nm s⁻¹ ITO rates on 1.5 m glass, halving capex for display backplanes. NREL demonstrated that roll-to-roll CdTe modules could achieve 18% efficiency at sub-USD 0.20 W⁻¹ costs, reinforcing the thin film’s cost edge.

Government CHIPS-Like Incentives Boosting Domestic Deposition Tool CAPEX

The U.S. CHIPS and Science Act earmarked USD 39 billion in grants and USD 75 billion in loan guarantees, triggering a home-grown equipment supply push. Intel’s Arizona build secured USD 8.5 billion and includes 150 deposition tools slated for 18-Å nodes by 2026. Europe’s EUR 43 billion Chips Act funds fabs in Germany, where Infineon and TSMC Dresden expansions will install 200 reactors. India accounts for up to 50% of fab capex; Micron’s Gujarat assembly plant will utilize 80 PVD tools. Japan pledged JPY 2 trillion to Rapidus for 2nm logic, prompting tool orders to be directed to Tokyo Electron. China’s “Big Fund” phase III added USD 47.5 billion to localize CVD and ALD hardware at AMEC and NAURA.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Helium and high-purity precursor supply crunch inflates OPEX | -2.4% | Global, acute in United States, Europe, Japan | Short term (≤ 2 years) |

| Escalating Scope-3 carbon-reporting mandates penalize vacuum processes | -1.8% | North America and Europe | Medium term (2-4 years) |

| Skilled vacuum-process talent shortage lengthens fab ramps | -1.3% | United States, Germany, Japan, India | Long term (≥ 4 years) |

| Competition from additive manufacturing of functional layers | -0.7% | Niche uses in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Helium And High-Purity Precursor Supply Crunch Inflates OPEX

The U.S. Federal Helium Reserve depletion drove spot prices from USD 8 m⁻³ in 2023 to USD 16 m⁻³ by mid-2024.[2]U.S. Bureau of Land Management, “Federal Helium Reserve Status,” blm.gov A 300 mm fab consumes 15 million m³ annually, and Lam Research disclosed USD 12 million extra helium costs in fiscal 2024. Closed-loop recovery systems recapture 95% of process gas but cost USD 3 million per installation. High-k precursors face similar strain; hafnium tetrachloride capacity is restricted to three makers, stretching lead times from 8 to 20 weeks. China’s August 2024 export controls on zirconium compounds further tightened the supply, prompting fabs to enter into dual-source agreements that increase unit costs by 18%.

Escalating Scope-3 Carbon-Reporting Mandates Penalize Vacuum Processes

The U.S. SEC now mandates Scope-3 disclosure from fiscal 2026, and the EU’s CSRD already applies to firms with over 250 employees.[3]U.S. Securities and Exchange Commission, “Climate Disclosure Rules,” sec.gov An atomic layer deposition reactor draws 40-60 kW in deposition mode, making vacuum tools significant emitters. ASM International recorded 18 tCO₂e per Pulsar tool per year when powered by EU-average grids. Customers respond by situating fabs near renewable energy clusters and by adopting Applied Materials’ Centura variant, which reduces idle power by 30% through adaptive throttling. Carbon pricing above EUR 80 t⁻¹ in the EU adds further pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deposition Technology: Atomic Layer Deposition Gains As Logic Nodes Shrink

Chemical vapor deposition held a 50.74% market share in the thin layer deposition market in 2025, reflecting its versatility in depositing dielectrics, polysilicon, and tungsten at high rates. Atomic layer deposition is forecast to grow at a 17.18% CAGR, driven by the need for sub-3 nm transistor gates, which require angstrom-scale thickness control. The thin layer deposition market size allocated to ALD reached USD 9.2 billion in 2025 and is expected to double by 2031. Physical vapor deposition remains entrenched for aluminum interconnects at mature nodes; however, hybrid flows, such as Lam Research’s SABRE 3D, merge ionized PVD with ALD barriers to reduce interface resistance by 25%. The emerging molecular layer deposition of polymers broadens the functional options for flexible electronics, adding a nascent but fast-growing revenue stream.

Logic foundries moving to gate-all-around nanosheets employ up to 15 ALD steps, versus eight in the prior generation. Intel’s 18A node epitomizes this leap with hafnium oxide and titanium nitride stacks wrapped around channels with 5:1 aspect ratios. CVD maintains dominance in shallow trench isolation and inter-layer dielectric gap-fill because 100 nm min⁻¹ rates keep wafer costs down. As aspect ratios increase, suppliers are advancing high-density plasma CVD and high-reflow liners to delay switchover points. Selective deposition is an active frontier: Tokyo Electron’s Tactras Vigus tool combines ALE and ALD with in-situ metrology, achieving ±0.5 nm self-aligned contacts that could eliminate lithography steps in the next logic cycle.

By Equipment Type: Spatial Systems Disrupt Batch Dominance

Batch furnaces delivered 56.05% of 2025 revenue, prized for their low cost per wafer in commodity logic, solar, and optical coatings. However, roll-to-roll and spatial tools registered a 16.36% CAGR, reflecting a pivot toward flexible OLED displays, battery separators, and bifacial solar modules that need web-based continuous processing. Single-wafer clusters remain indispensable in advanced logic and 3D NAND, where vacuum-integrated chambers ensure particle control. The thin layer deposition market size for spatial ALD equipment was USD 2.8 billion in 2025 and is expected to reach USD 6 billion by 2031 as throughput concerns ease.

Beneq’s spatial ALD uptime moved past 85% in 2024, removing a historical barrier to mass adoption. Applied Materials’ Olympia integrates spatial ALD and PVD modules in a shared transfer system, achieving 1,200 wafers per hour for TOPCon passivation, a 15× productivity increase over batch reactors. Roll-to-roll magnetron sputtering at Von Ardenne coats indium zinc oxide on polyimide at a rate of 20 m min⁻¹, enabling foldable phones with a bend radius of 3 mm. Canon Anelva’s ENAS platform integrates machine learning into sputter power control, reducing thickness variation to around 1.5% on 300 mm wafers, thereby easing process windows for sub-10 nm copper interconnects.

By Material Type Deposited: Nitrides And Carbides Surge In Power Electronics

Metals and alloys accounted for 37.22% of the 2025 volume, led by copper, aluminum, and titanium. Nitrides and carbides posted a 17.01% CAGR owing to titanium nitride barriers, aluminum nitride heat spreaders, and silicon carbide interfaces. The thin layer deposition market size for nitrides alone exceeded USD 6 billion in 2025. Oxides remain indispensable for dielectrics and passivation, while 2D compounds, such as molybdenum disulfide and hexagonal boron nitride, gain early traction in neuromorphic and quantum devices.

Applied Materials’ Endura Volta deposited titanium nitride with 90% step coverage in 2:1 trenches, allowing TSMC’s 3 nm node to gain 15% speed over tantalum nitride baselines. Aluminum nitride’s 285 W m⁻¹ K⁻¹ thermal conductivity boosts GaN radio-frequency amplifiers, and Aixtron’s AIX G5 WW C reactor achieved ±3% film uniformity on 200 mm silicon carbide wafers. Research at Osaka University showed that nitric oxide-annealed oxides on silicon carbide trimmed interface traps are below 1×10¹¹ cm⁻² eV⁻¹, a critical metric for electric vehicle traction inverters.

By End-Use Industry: Photovoltaics Accelerate Past Semiconductor Growth

Semiconductors absorbed 41.35% of the 2025 spend but will grow at a slower rate than photovoltaics, which posts an 17.74% CAGR on the back of TOPCon and heterojunction architectures that require ALD aluminum oxide passivation. Photovoltaic demand pushed the thin layer deposition market size for solar applications to USD 5.7 billion in 2025. Medical devices, optics, and industrial tooling round out demand with specialty coatings that command higher margins per wafer equivalent.

Longi’s TOPCon modules achieved 25.5% efficiency using ALD rear passivation, increasing the energy yield per area by 1.5 percentage points. LG Energy Solution coats 1.2 m-wide polyethylene separators at a rate of 5 m/min⁻, covering 500 MWh of battery output annually. In med-tech, 200 nm hydroxyapatite layers extended the integrity of magnesium stents from 3 to 12 months, opening a new premium tool segment. OLED displays require ALD encapsulation, delivering water vapor transmission below 1 × 10⁻⁶ g m⁻² day⁻¹, as adopted by Samsung Display’s QD-OLED TVs.

Geography Analysis

The Asia Pacific region controlled 44.78% of 2025 revenue, driven by fabrication expansions at TSMC, Samsung, and multiple Chinese foundries. Capital spending in the region exceeded USD 36 billion, with TSMC alone accounting for a significant portion, 25% of which was earmarked for deposition equipment. China increased its equipment self-sufficiency to 28% in 2024, as AMEC tools were integrated into SMIC’s 14 nm lines. South Korean subsidies of KRW 20 trillion supported SK Hynix’s HBM ramps that ordered 120 ALD reactors. Japan’s Rapidus alliance purchased 30 tools for gate-to-gate R&D, leveraging expertise from IBM and IMEC.

North America is rebounding under the CHIPS Act. Intel and TSMC Phoenix will install more than 300 reactors by 2026, while Micron’s New York DRAM fab plans to use 80 ALD tools for capacitor dielectrics. Applied Materials broke ground on a USD 4 billion factory in Montana to serve this surge, adding 200,000 square feet of cleanrooms. Europe focuses on power and compound semiconductors; Infineon’s Dresden fab and TSMC European JV add 60 PVD and CVD tools for silicon carbide and copper interconnects. Middle East solar mega-projects, such as Saudi Arabia’s 20 GW tender, order large-area sputter lines from Von Ardenne and Singulus, thereby extending the regional share. South America and Africa remain nascent, but they benefit indirectly from commodity solar imports that rely on Asian manufacturing capacity. Regional research institutes explore roll-to-roll ALD for flexible sensors, building local know-how that could translate into modest equipment sales post-2030. Collectively, these emerging regions represent under 5% of current revenue, yet they provide a long tail of opportunity once cost curves fall.

Regulatory Landscape

Thin layer deposition tools operate in a tightening semiconductor trade and dual-use compliance environment, which affects ALD, PEALD, and selective-deposition capable systems used in advanced interconnect and TSV flows. In the United States, export controls administered by the U.S. Department of Commerce, Bureau of Industry and Security (BIS) cover certain ALD tool configurations (including area-selective deposition capabilities and tungsten interconnect applications at small feature sizes), increasing licensing and end-use screening requirements for tool shipments, upgrades, and spares.

In Europe, export compliance has also escalated after the European Commission updated the EU dual-use framework (Regulation (EU) 2021/821) to include categories covering ALD tools and related deposition systems (September 2025 update referenced in the evidence pack). Alongside controls, industrial policy continues to steer capital formation: the EU Chips Act (Regulation (EU) 2023/1781) remains a key named framework, and the European Commission proposal titled EU Chips Act 2.0 (COM/2026/504/FIN) reinforces resilience tools such as pilot lines and advanced engineering capacities, which in turn shapes where deposition capability and applications engineering get built and qualified.

Value Chain Analysis

The thin layer deposition value chain begins with ultra-high-purity inputs (process gases, targets, and specialty precursors such as high-k and nitride chemistries), followed by subsystems (vacuum pumps, RF and microwave power, valves, metrology sensors, gas delivery, and thermal management) that OEMs integrate into CVD, PVD, and ALD platforms. Applied Materials, Lam Research, Tokyo Electron, ASM International, Veeco, and a long tail of specialist suppliers (for spatial ALD, lab-to-pilot tools, and web coating) deliver equipment into foundries, memory manufacturers, advanced packaging lines, PV thin-film lines, and industrial coating users, with field service, spares, chamber refurbishment, and process recipes supporting a meaningful downstream revenue layer.

Recent supply-side signals point to broader deposition modalities and application pull. Applied Materials introduced new ALD and selective process modules in 2026 for high-aspect-ratio structures, while ACM Research shipped a first PECVD SiCN system for customer site validation (April 2026), showing deeper participation by additional OEMs in dielectric and liner films. On the demand side, silicon photonics and compound-semiconductor adjacencies also tighten the chain: Veeco disclosed over USD 250 million of orders for Ion Beam Deposition and MOCVD systems tied to indium phosphide laser demand (May 2026), linking optical interconnect roadmaps to deposition tool orders, qualification cycles, and sustained consumables and service pull.

Competitive Landscape

Market concentration is moderate, with the top five suppliers accounting for 65% of the 2024 revenue. Applied Materials, Lam Research, and Tokyo Electron dominate the single-wafer cluster market, while ASM International and Veeco focus on the ALD and MOCVD niches. Beneq, Picosun, and Kurt J. Lesker thrive in spatial ALD and R&D-scale systems. Competitive intensity rises as customers demand integrated deposition-etch-metrology platforms that shrink footprint and support real-time control. Lam Research’s Striker selective tungsten fill exemplifies horizontal expansion beyond etch.

Throughput, uniformity, and precursor efficiency remain the key differentiators. Applied Materials’ Olympia achieved 98% trimethylaluminum utilization, cutting TOPCon cost per wafer to USD 0.12. Lam Research’s AI suite reduced downtime to 3%, and Tokyo Electron filed 87 ALD patents in 2024, with a focus on selective area flows. Smaller rivals disrupt niches: CVD Equipment’s roll-to-roll graphene system won a European battery contract at 60% lower capex than batch solutions. Patent races spill into precursors, where ASM International secured rights to high-vapor-pressure plasma ALD chemistries, eliminating the need for heated lines.

Supply chain localization reshapes competition. AMEC received USD 180 million orders from SMIC for Prismo HiT3 etch-deposition clusters after U.S. export controls tightened. Beneq’s JV with Longi will build 100 spatial ALD tools annually in Xi’an, cutting lead times by 50%. Oerlikon Balzers has added ten Rapid Coating Units in Germany to address tool coatings, demonstrating that industrial PVD continues to grow under the umbrella of energy transition manufacturing.

Thin Layer Deposition Industry Leaders

Applied Materials Inc.

Lam Research Corporation

Tokyo Electron Limited

ASM International NV

Veeco Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace is forming around atomic layer processing flows that combine ALD with area-selective deposition and adjacent steps to accommodate increasingly complex 3D device geometries. Evidence from 2026 academic work indicates scalable, inhibitor-free area-selective ALD approaches, including nitride films demonstrating selectivity sustained beyond 200 ALD cycles and pattern scaling down to 20 nm line widths, which aligns with the market need for self-aligned features and reduced patterning overhead in advanced interconnect, gate-all-around, and vertical device concepts.

Memory vertical scaling and related high-aspect-ratio integration also create an opportunity cluster for toolmakers and materials suppliers, as deposition share of flash-line capex is discussed as higher in 3D eras than in 2D baselines and industry commentary flags rising deposition and etch intensity as 3D NAND targets extremely high layer counts. This supports demand for higher-throughput PEALD/ALD dielectrics and liners, improved conformality at extreme aspect ratios, and tighter process-window control through integrated metrology and advanced plasma delivery, while also opening space for precursor innovation that reduces cycle time and improves utilization in high-volume manufacturing environments.

Recent Industry Developments

- June 2026: Applied Materials launched the Centris Spectral SiN ALD system alongside the Producer Selectra Mo Etch capability for processing high-aspect-ratio 3D logic and memory structures. The releases highlight a shift toward plasma-enabled thin film control and selective integration steps as devices add vertical complexity and tighter electrical constraints.

- July 2025: ASM International acquired Forge Nano for USD 320 million to expand access to spatial ALD reactors used in battery-related thin film applications. The deal broadened ASM International's exposure beyond wafer-centric ALD into higher-throughput coating formats that map to energy storage manufacturing.

- March 2024: Lam Research introduced a Pulsus pulsed laser deposition (PLD) tool to deposit AlScN films used in RF filters and MEMS. The introduction strengthened Lam Research's position in specialty deposition for performance materials where film quality and composition control support end-device differentiation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the thin layer deposition market is defined as the revenue generated from processes and tools used to deposit thin films on substrates, to achieve functional surfaces or device layers. Coverage is mainly targeted to electronics, optics, energy, and industrial coatings.

Scope exclusions: we exclude downstream device assembly and packaging value. We also exclude non-deposition surface treatments where no deposited thin-film layer is formed.

Segmentation Overview

- By Deposition Technology

- Physical Vapor Deposition (PVD)

- Chemical Vapor Deposition (CVD)

- Atomic Layer Deposition (ALD)

- Hybrid / Emerging Techniques

- By Equipment Type

- Batch Systems

- Single-wafer Cluster Tools

- Roll-to-Roll / Spatial Systems

- In-line Production Lines

- By Material Type Deposited

- Metals and Alloys

- Oxides

- Nitrides and Carbides

- Compound / 2-D Materials

- By End-Use Industry

- Semiconductors and Micro-electronics

- Photovoltaics and Energy Storage

- Medical Devices and Healthcare

- Optics and Displays

- Tools and Industrial Components

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the technical boundary, build the demand map, and create a starting view on where thin films are being adopted fastest. We relied on public sources such as SEMI releases for semiconductor equipment signals, USGS mineral statistics for metals and specialty inputs, US International Trade Commission trade data for category-level import and export direction, and US Department of Energy and IEA publications for solar and energy-transition indicators. For process innovation signals, we reviewed USPTO patent publications.

In parallel, we reviewed company filings, investor presentations, annual reports, and product literature to understand tool types, typical applications, and pricing direction in broad bands (not invoice-level). Select paid subscriptions were used only for company financials and intelligence, patent coverage, and shipment-level import and export checks, so the model does not depend on any single narrative source. This source list is illustrative, and additional public documents and datasets were also referenced for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was done through expert interviews and structured surveys with equipment suppliers, materials and precursor ecosystem participants, fab and line-level engineering teams, and procurement or operations stakeholders across key end-use industries. For a global market, responses were balanced across APAC, EMEA, and the Americas, so the model reflects differences in semiconductor capacity cycles, display and optics build-outs, and renewable manufacturing activity.

Where desk research left gaps, we used field inputs to confirm adoption rates by process type, typical tool utilization patterns, and how pricing moves with node shifts and coating performance requirements.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 41% |

| Mid tier: 55% | Functional/Unit leaders: 31% | EMEA: 34% |

| Smaller Players: 16% | Managers: 56% | Americas: 25% |

Market-Sizing & Forecasting

The market was built using a top-down model that reconstructs demand from thin-film deposition intensity in core end markets, then converts that demand into revenue using fit-for-purpose price bands. In practice, we start from indicators such as semiconductor fabrication capacity additions and upgrade cycles, thin-film use in displays and optical coatings, photovoltaic manufacturing activity, and changes in the mix of deposition methods used for tighter feature control. After mapping the demand pool, we apply pricing and utilization assumptions to estimate the annual market value.

We then corroborated those totals with selective bottom-up approximations, including rolling up sampled tool and process revenues across a set of suppliers and using channel checks for typical average selling price ranges by tool class. Key inputs that repeatedly influenced the model included wafer-start and capacity expansion timing, deposition step counts for advanced nodes, precursor availability constraints for certain processes, tool uptime and utilization expectations, and the share shift between PVD, CVD, and ALD based on performance needs. For forecasting, scenario analysis was used with expert-led assumptions on capex cycles and thin-film intensity trends, then the results were cross-checked against recent demand signals before finalizing the trajectory.

Data Validation & Update Cycle

Validation was done through repeated variance checks across regions and end uses, then review of the biggest drivers that can swing results, including capex timing, utilization, and price bands. When a modeled output looked out of line with observed signals such as equipment order commentary, trade movement direction, or announced capacity expansions, we revisited the relevant assumptions and re-contacted the same expert set to confirm what changed.

Before sign-off, the model went through a multi-step internal review where the logic, units, and year-to-year movements were checked for consistency, and any anomalies were documented and resolved. Reports are refreshed annually, and interim updates are added when material events occur, such as sharp shifts in semiconductor equipment cycles or major policy-driven investment waves. Right before delivery, a final analyst pass is completed so clients receive the most current, internally consistent view.

Mordor Intelligence's Thin Layer Deposition Market Size Measured Against Other Published Estimates

Published thin layer deposition market numbers can look far apart even when they appear to cover the same topic, because the scope boundary is often drawn differently and the conversion from activity indicators into revenue is not handled the same way. Differences usually come from what is counted as deposition revenue, the year chosen for sizing, and how fast pricing is assumed to move when tool mixes change.

Semiconductor capacity expansion signals, end-market adoption checks in displays and photovoltaics, and cross-verification using trade-direction indicators are the evidence points that keep Mordor Intelligence's estimate tied to an identifiable demand pool rather than a broad materials narrative. In practice, the spread is usually driven by whether the estimate includes adjacent equipment categories, whether materials-only or equipment-only definitions are used, and whether long-horizon forecasts embed aggressive penetration assumptions without re-checking utilization and average selling price progression.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.93 B (2025) | |

| Global Research Publisher A | USD 10.99 B (2025) | Often presented as a narrower revenue pool that appears to lean toward equipment-only counting, with limited visibility on how deposition intensity and utilization are converted into revenue across semiconductors, displays, and energy-related uses. |

| Industry Analytics Firm B | USD 2.93 B (2025) | Typically reflects a tightly scoped subset of thin layer deposition, which can exclude several deposition tool classes and end-use demand pools, thereby producing a smaller total even when similar technologies are referenced. |

The table indicates that most of the gap comes from scope boundary choices and from how demand indicators are translated into annual revenue. By keeping inclusions explicit, using market signals that can be independently checked, and re-validating pricing and utilization assumptions with interviews, the final number stays traceable and repeatable for decision making.

Key Questions Answered in the Report

What is the expected value of the thin layer deposition market by 2031?

The market is projected to reach USD 56.35 billion by 2031, reflecting a 14.56% CAGR

Which deposition technology is growing the fastest?

Atomic layer deposition is advancing at a 17.18% CAGR due to its role in sub-3 nm transistor and capacitor fabrication

Why is Asia Pacific the largest region for thin layer deposition?

Concentrated investments by TSMC, Samsung, and Chinese foundries drive 44.78% regional share and a 16.92% growth rate.

How are CHIPS-style incentives affecting equipment demand?

Subsidies in the United States, EU, India, and Japan accelerate domestic tool purchases, adding hundreds of CVD and ALD reactors to new fabs.

What materials segment shows the highest growth?

Nitrides and carbides post a 17.01% CAGR, propelled by titanium nitride barriers and aluminum nitride heat spreaders for power electronics.

How are suppliers mitigating helium shortages?

Fabs install closed-loop helium recovery, while tool makers redesign reactors for lower flow rates, limiting operating expense spikes.

Page last updated on: