Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Thick Film Resistor Market is Segmented by Resistor Type (Standard Thick Film Chip Resistors, and More), Package / Mounting Type (Surface-Mount Chip (0201–2512), and More), End-User Industry (Automotive, Industrial Automation and Control, and More), Vehicle Type (Internal Combustion Engine Vehicles, Hybrid Electric Vehicles, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

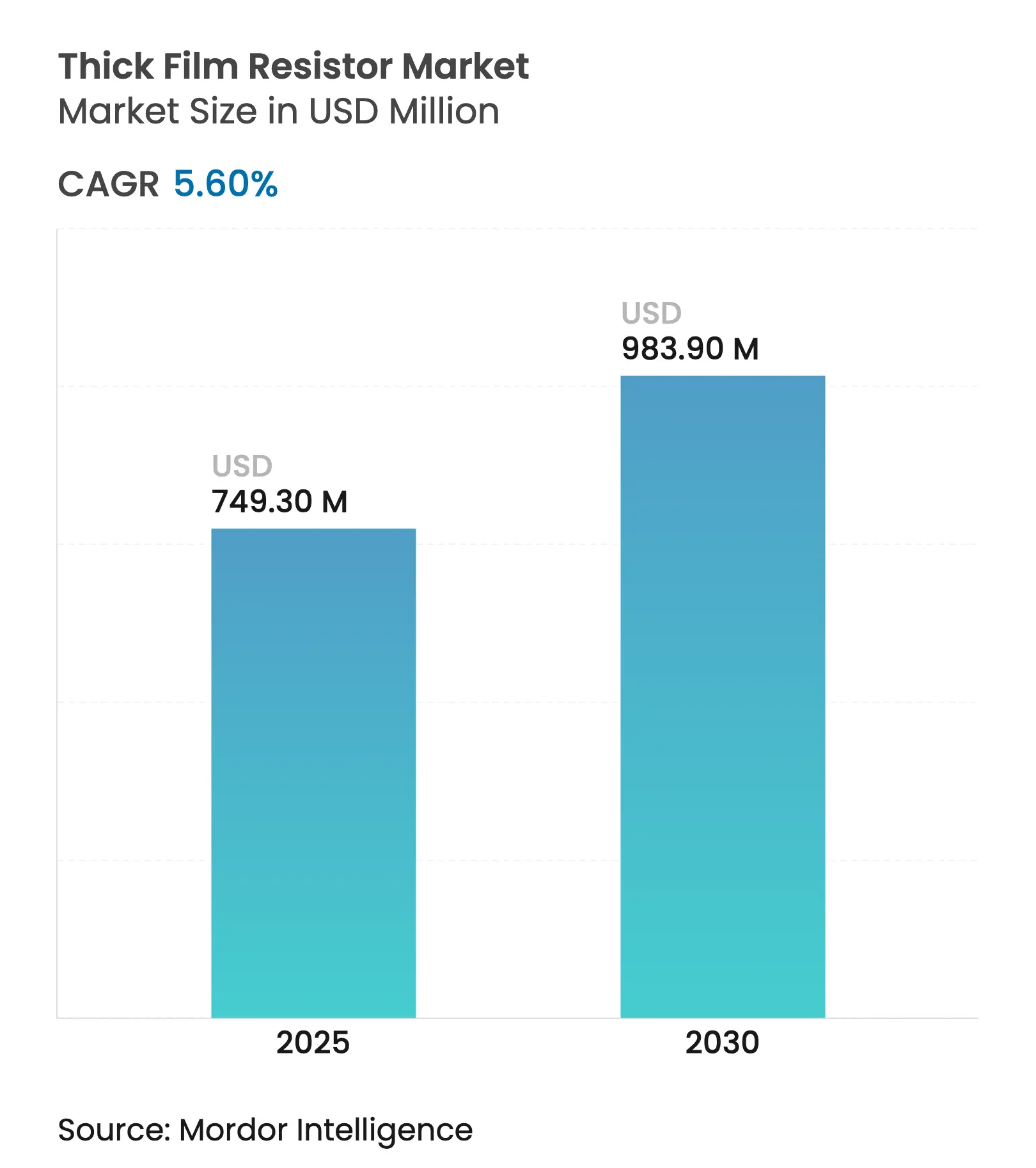

| Market Size (2025) | USD 749.30 Million |

| Market Size (2030) | USD 983.90 Million |

| Growth Rate (2025 - 2030) | 5.60 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The thick film resistor market size was valued at USD 749.3 million in 2025 and is forecast to reach USD 983.9 million in 2030, reflecting a steady 5.6% CAGR during the period. Growth stemmed from accelerating electrification across vehicles and industrial power electronics, coupled with the electronics sector’s relentless push toward miniaturization. Automakers raised procurement volumes for high-voltage resistors that protect 800 V powertrains, while 5G infrastructure upgrades elevated demand for ultra-compact chips able to manage millimetre-wave signals. Material scarcity reshaped competitive strategies as volatile ruthenium prices forced suppliers to redesign pastes and secure alternate sources. Producers that mastered low-lead or bismuth-based formulations captured early orders from customers facing tighter environmental rules in Europe and North America. Asia-Pacific held a self-reinforcing advantage through its integrated supply chain, yet localization incentives under the US CHIPS Act and the European Chips Act encouraged new capacity closer to end users, setting the stage for a more regionally balanced thick film resistor market.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging Adoption of High-Voltage Thick Film Resistors in

Electric Powertrains Across Asia-Pacific

Surging Adoption of High-Voltage Thick Film Resistors in

Electric Powertrains Across Asia-Pacific

| +1.8% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.8%

|

Geographic Relevance

:

Asia-Pacific, Europe, North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Demand for Miniaturized Passive Components in 5G RF

Modules Driving Chip Form-Factor Migration

Demand for Miniaturized Passive Components in 5G RF

Modules Driving Chip Form-Factor Migration

| +1.2% | Global, with a concentration in Asia-Pacific | Short term (≤ 2 years) | |||

Rapid Expansion of Vehicle ADAS and Power Electronics

Requiring High-Temperature-Stable Resistors

Rapid Expansion of Vehicle ADAS and Power Electronics

Requiring High-Temperature-Stable Resistors

| +0.9% | Global, led by Europe and North America | Medium term (2-4 years) | |||

Growth of Smart Grid and Renewable Inverters Elevating

Need for High-Power Thick Film Shunts

Growth of Smart Grid and Renewable Inverters Elevating

Need for High-Power Thick Film Shunts

| +0.7% | North America, Europe, China | Long term (≥ 4 years) | |||

Supply-Chain Localization Incentives in US and EU Boosting

On-shore Thick Film Production Lines

Supply-Chain Localization Incentives in US and EU Boosting

On-shore Thick Film Production Lines

| +0.5% | North America, Europe | Medium term (2-4 years) | |||

Reliability Requirements in Medical Electronics: Favouring

Thick Film over Thin Film Alternatives

Reliability Requirements in Medical Electronics: Favouring

Thick Film over Thin Film Alternatives

| +0.4% | Global, with emphasis on North America and Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Adoption of High-Voltage Thick Film Resistors in Electric Powertrains Across Asia-Pacific

Electric vehicle platforms shifted from 400 V to 800 V architectures, which heightened demand for chips rated up to 3kV. Stackpole’s RVCA series illustrated this requirement by offering 100 V to 3,000 V ratings for pre-charge and inverter circuits. Designers prioritized pulse endurance and thermal stability, so suppliers that optimized paste chemistry for low drift captured design wins in traction inverters and on-board chargers. High-voltage capability, therefore, became a strategic differentiator, adding 1.8% to the projected CAGR of the thick film resistor market.

Demand for Miniaturized Passive Components in 5G RF Modules Driving Chip Form-Factor Migration

The first wave of 5G base stations required ultra-compact resistors to reduce parasitic at mm-wave frequencies. Yageo’s RC0075, just 0.3 mm × 0.15 mm, cut footprint by 44% versus the 01005 size and highlighted how process precision increased entry barriers.[1]Yageo Corporation, “Yageo Has Developed the Smallest Chip Resistor in the World – RC0075,” RFGlobalnet, rfglobalnet.com Rapid adoption across Asia-Pacific handset and infrastructure plants drove short-term demand spikes, lifting overall CAGR by 1.2%. Suppliers invested in advanced laser trimming and vision-guided placement to support these sizes while sustaining yield.

Rapid Expansion of Vehicle ADAS and Power Electronics Requiring High-Temperature-Stable Resistors

Advanced driver assistance features placed electronics near hot zones inside engine bays. Panasonic’s ERJ-PM8 series met AEC-Q200 and anti-sulphuration standards, offering stable resistance at 155 °C. These specifications increased unit value and steered buyers toward premium thick film products, lifting CAGR by 0.9%. Automakers widened qualification lists for anti-sulphuration options, tightening the link between material science investment and share gains.

Growth of Smart Grid and Renewable Inverters Elevating Need for High-Power Thick Film Shunts

Utility-scale solar farms installed higher-power inverters that required precise current shunts. ROHM’s wide-terminal thick film series delivers up to 4 W in compact footprints, aligning with inverter makers’ space limits. The long-term nature of grid buildouts added a 0.7% uplift to the thick film resistor market CAGR and encouraged joint development programs between power equipment OEMs and resistor specialists.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Price Volatility of Ruthenium and Palladium Thick-Film

Pastes Increasing BOM Costs

Price Volatility of Ruthenium and Palladium Thick-Film

Pastes Increasing BOM Costs

| -0.8% | Global, with the highest impact in Asia-Pacific | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.8%

|

Geographic Relevance

:

Global, with the highest impact in Asia-Pacific

|

Impact Timeline

:

Short term (≤ 2 years)

|

Competitive Substitution by Thin-Film and Metal-Foil

Resistors in Ultra-Precision Circuits

Competitive Substitution by Thin-Film and Metal-Foil

Resistors in Ultra-Precision Circuits

| -0.6% | Global, with emphasis on North America and Europe | Medium term (2-4 years) | |||

Environmental Regulations on Lead-Bearing Glass Frits

Raising Compliance Spend

Environmental Regulations on Lead-Bearing Glass Frits

Raising Compliance Spend

| -0.5% | Europe, North America, with gradual expansion globally | Medium term (2-4 years) | |||

Capacity Bottlenecks in Alumina Substrates Limiting

Surge-Demand Fulfilment

Capacity Bottlenecks in Alumina Substrates Limiting

Surge-Demand Fulfilment

| -0.4% | Asia-Pacific, with impact spreading globally | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Price Volatility of Ruthenium and Palladium Thick-Film Pastes Increasing BOM Costs

Ruthenium prices spiked in early 2025, raising paste costs and squeezing margins for commodity chip resistors. TTI’s raw material index reported sustained volatility across precious metals, leaving suppliers to hedge procurement or redesign formulations. Smaller manufacturers struggled to secure long-term contracts, leading to sporadic shortages that reduced shipment volumes by the equivalent of 0.8% CAGR.

Competitive Substitution by Thin-Film and Metal-Foil Resistors in Ultra-Precision Circuits

Instrumentation OEMs shifted high-precision boards toward metal-foil devices that offered temperature coefficients down to ±50 ppm/°C, half that of thick film parts. Viking Tech’s MF series exemplified this performance leap. Although thick film resistors kept a cost advantage, erosion in premium niches removed 0.6% from forecast CAGR, prompting suppliers to accelerate hybrid thick-film processes to reclaim share.

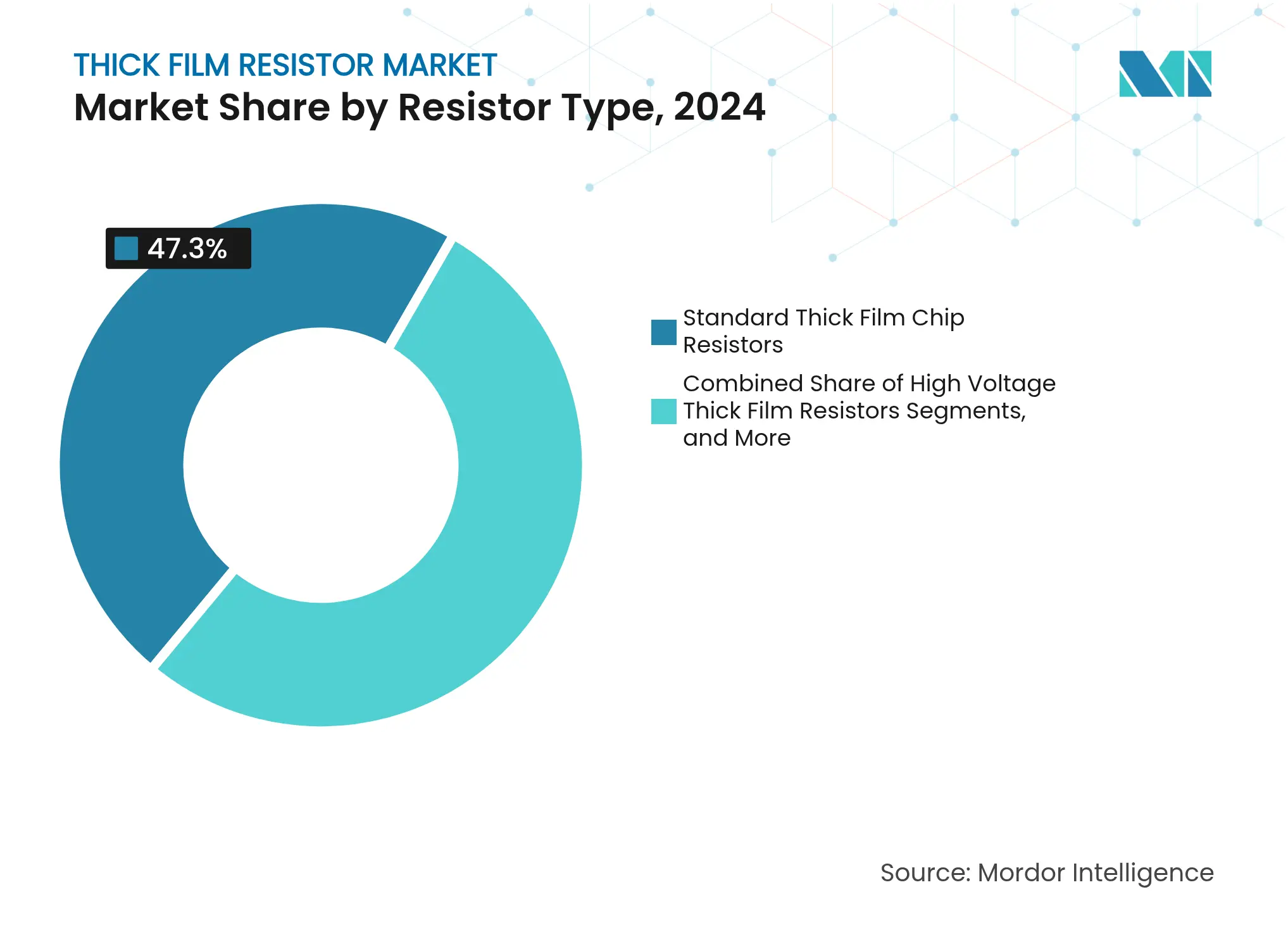

By Resistor Type: High-Voltage Variants Redefining Performance Boundaries

The standard chip category held 47.3% of the thick film resistor market share in 2024, underpinning widespread consumer and industrial electronics applications. High-voltage models, however, expanded at an 8.4% CAGR and were instrumental in lifting the thick film resistor market size for powertrain electronics during the forecast. Suppliers integrated arc-suppression design tweaks and refined paste grain structures to ensure stability above 1 kV.

Precision thick film resistors gained momentum where tighter tolerances offset earlier process limitations, while surge-resistant variants protected power stages in industrial drives. Continuous investment in anti-sulphuration chemistry preserved resistance stability under corrosive exhaust conditions. The innovation pipeline demonstrated that thick film technology still delivered competitive cost-performance ratios against foil or thin-film alternatives, sustaining demand across mainstream designs.

By Package/Mounting Type: Miniaturization Driving Manufacturing Innovation

Surface-mount chips represented 82.6% of sales in 2024, evidencing entrenched automation across EMS production lines.[2]Panasonic, “Industry Smallest 01005 Anti-Sulfurated Thick Film Chip Resistors,” doeeet.com Their ubiquity lifted the thick film resistor market size for handheld devices, with 01005 and 0075 footprints supporting smartwatch and earbud boards.

Array and network packages recorded the top 8.7% CAGR because they consolidated multiple resistors into one substrate, trimming pick-and-place counts for 5G radios. Through-hole parts preserved relevance in high-pulse defense power supplies. Custom substrates such as thick film on steel improved power density and thermal cycling for aerospace uses. These packaging advances kept thick film resistors aligned with next-generation assembly standards.

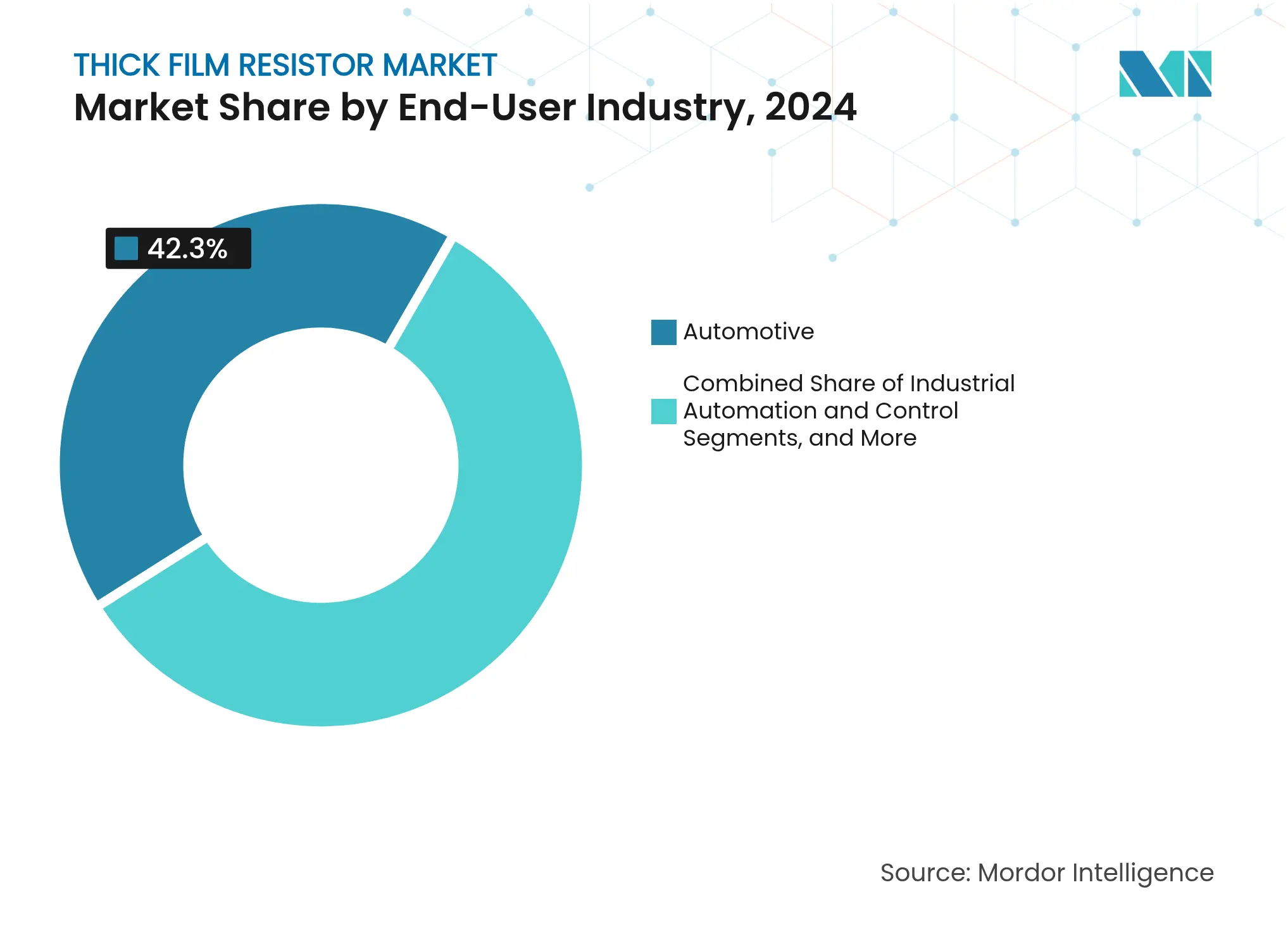

By End-User Industry: Automotive Electrification Reshaping Demand Patterns

Automotive electronics absorbed 42.3% of shipments in 2024, reflecting the surge in control modules and battery-management boards per vehicle. This dominance supported a stable revenue base within the thick film resistor market, while growing adoption of high-voltage safety resistors increased unit value.

Telecommunications and networking applications grew at 9.1% CAGR thanks to the 5G rollout, which required low-noise, high-frequency chips inside remote radio heads. Industrial automation expanded alongside smart-factory retrofits, and renewable power systems created a niche for high-power shunts. Medical device makers favoured thick film parts for defibrillators and diagnostic gear where reliability drove stringent qualification.

By Vehicle Type: Battery Electric Vehicles, Accelerating Component Evolution

Internal-combustion models still consumed 61.4% of automotive-grade resistor volumes in 2024, but battery electric vehicles lifted the thick film resistor market size for high-voltage applications through a 17.9% CAGR outlook. EV traction inverters demanded low-inductance current sense chips to manage rapid switching.

Hybrid electric vehicles created mixed-voltage design complexities, blending 48V boost circuits with conventional 12V loads. Suppliers developed multi-layer isolation techniques to satisfy these diverse requirements. Ongoing model launches ensured sustained growth through the decade.

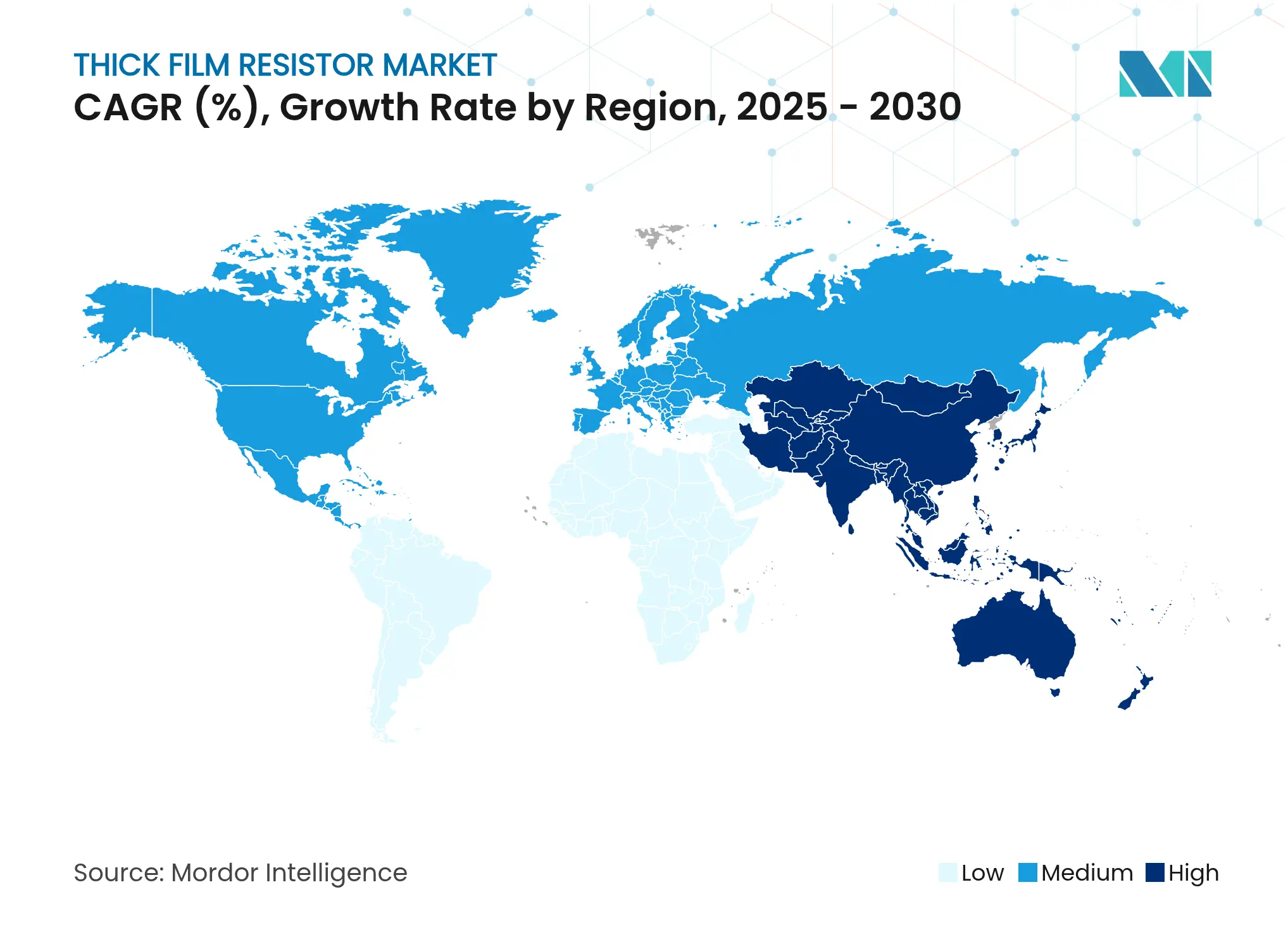

Asia-Pacific controlled 48.3% of revenue in 2024 and expanded at 8.3% CAGR, reflecting concentrated EMS capacity in China, Japan, and Taiwan, along with explosive EV production in China.[3]Dennis M. Zogbi, “Passive Electronic Components: Global Market Update – April 2025,” TTIEurope, ttieurope.com Governments promoted local supply networks for passive components, which encouraged the co-location of resistor paste and substrate plants, further reinforcing regional dominance.

North America gained momentum once the US CHIPS Act stimulated domestic fabs for both active and passive parts. Automakers built battery plants across the Midwest, which drew resistor suppliers closer to final assembly lines. Medical device manufacturers in Minnesota and California sourced high-reliability chips from new regional lines to reduce lead times. Europe followed a similar path under the European Chips Act, with Germany and France funding thick film pilot lines linked to automotive Tier-1s and renewable inverter makers.

South America, the Middle East and Africa together formed an emerging demand cluster. Brazilian electronics assemblers increased orders as local automotive output recovered, while Saudi smart-city projects specified sulphur-resistant chips for harsh outdoor nodes. South African telecom operators upgraded 4G towers to 5G, fuelling resistor imports. Although these areas held modest shares, rising infrastructure budgets signalled multi-year growth potential beyond 2026.

Market Concentration

The five largest suppliers—Yageo, Vishay, Panasonic, KOA, and ROHM—captured more than 50% of global revenue, indicating moderate concentration in the thick film resistor market. Scale advantages in powder metallurgy and screen-printing automation let these firms defend margins on commodity 0603 chips, yet differentiation shifted toward specialty pastes and substrates. Several mid-tier companies focused on high-voltage or anti-sulphuration niches to avoid direct price wars with mass producers.

Product roadmaps showed a bifurcation. Volume leaders pursued cost leadership through larger wafer-level pad printing and backend robotics, whereas niche players invested in bismuth-glass formulations and thick film on steel substrates to address aerospace or medical requirements with higher ASPs. Material innovation emerged as the primary lever to escape commoditization.

Strategic moves in 2024 and 2025 reinforced this pattern. Vishay previewed 3 kV chips at APEC 2025 for EV charging modules. KOA broadened its high-precision RS73 line to win automotive body-control placements. Yageo expanded 5G chip resistor capacity to support telecom OEMs. TT Electronics commercialized thick film on steel resistors that delivered superior thermal cycling for surgical equipment, strengthening its medical foothold.[4]James Spencer, “Thick Film on Steel Resistor Technology,” ttelectronics.com

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the thick film resistor market as the annual sales value of discrete resistors whose metal-oxide paste is screen-printed and fired onto a ceramic substrate to a thickness of roughly 10-100 µm. The scope covers chip, shunt, high-voltage, power, and precision parts sold in surface-mount, array, or through-hole formats to automotive, industrial, consumer, telecom, energy, aerospace, and medical sectors.

Scope Exclusions: Integrated thin-film networks, potentiometers, and custom thick-film hybrids are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Interviews with procurement engineers, OEM component buyers, paste suppliers, and distributors across Asia-Pacific, North America, and Europe helped refine yield, ASP, and penetration assumptions.

Desk Research

Mordor analysts build the baseline from customs codes, UN Comtrade, Eurostat, and electronics trade groups, matched with shipment data from WSTS and IMTMA. Public 10-Ks, investor decks, patents, and tier-one media clarify design wins, pricing, and material cost swings. We enrich the desk pool with D&B Hoovers financial splits, Dow Jones Factiva news counts, and Questel patent momentum on ruthenium inks and AEC-Q200 chips. The sources listed are illustrative; many others supported data collection and sanity checks.

Market-Sizing & Forecasting

A top-down build starts with global chip-resistor output volumes, which are then multiplied by region-specific thick-film shares and blended ASPs. Supplier roll-ups and channel checks give a bottom-up cross-check. Key drivers include ECU count per vehicle, 5G macro-cell rollout, ruthenium prices, SMT line utilization, and EV production; these feed a multivariate regression overlaid with ARIMA tracking to extend forecasts. According to Mordor Intelligence, the model currently anchors the market value, providing the reference for all downstream analysis.

Data Validation & Update Cycle

Outputs face variance screens against independent shipment audits and metal price indices before peer review. We refresh each model yearly, issuing mid-cycle updates when raw-material shocks or regulation materially shift demand.

Why Mordor's Thick Film Resistor Baseline Earns Trust

Benchmark comparison

Published market values often diverge because firms choose different component baskets, price ladders, base years, and refresh speeds.

Divergence here stems chiefly from whether shunt parts are included, the use of list rather than blended prices, and slower update schedules that miss recent 5G and EV pull-through.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 749.3 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 533.9 million (2024) | Global Consultancy A | excludes power and precision variants, relies on 2023 price deck | ||

USD 745.0 million (2024) | Industry Insights B | uses uniform ASP across regions, limited primary validation | ||

USD 615.0 million (2025) | Regional Consultancy C | groups thick-film with shunt totals, older production baselines |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.